1. Introduction

The development of mobile devices and e-commerce has driven the growth of the mobile payment market worldwide. It was predicted that the transaction value in the mobile payment segments will reach US

$4769 billion in 2020, with a compound annual growth rate (CAGR) of 12% between 2020 and 2023 [

1]. In response to the emergence of online shopping, which relies on mobile payment services, more firms are entering the mobile payment-related market. The critical role of mobile payment can be witnessed under these growing developments.

In recent years, the Taiwanese government has actively popularized the adoption of mobile payments. To optimize environmental fundamentals, several measures were implemented [

2]. For instance, a financial regulatory sandbox law that allows more leeway for field-testing financial services was enacted in 2017 [

3]. While the user penetration rate of mobile payment services rose from 39.7% in 2016 to 62.2% in 2019, there is still considerable room for growth compared to the existing huge credit card market. Like in other parts of the world, the largest group of potential adopters of this new payment option is the young generation, who are more comfortable with different online payment alternatives [

4], which thereby constitutes one crucial segment of the market for business to prosper [

5]. Nonetheless, what the pros or cons are of mobile payment from the viewpoint of the young generation in Taiwan is still an unanswered question. The major focus of the present study, therefore, is to gain insights into factors affecting the young generation’s behavioral intention and the actual usage behavior of mobile payment. Past studies on the drivers/barriers of the young generation’s mobile payment usage have been inconclusive. Taking the young generations in Taiwan as an example, this study provides a significant complement to the delineation of the young generation’s intention and use of mobile payment. With a projected CAGR of nearly 23.70%, the Asia-Pacific mobile payment market is predicted to be the fastest-growing segment in the world mobile payment market during 2018–2026 [

6]. A better understanding of the driving/deterring factors of the young generation’s mobile payment adoption can help the service practitioners and researchers in designing promotion strategies to make the new payment mode broadly acceptable to the largest group of potential adopters. Therefore, the findings in this research can render important implications for the development of cost-effective market communication strategies in the Asia-Pacific mobile payment market.

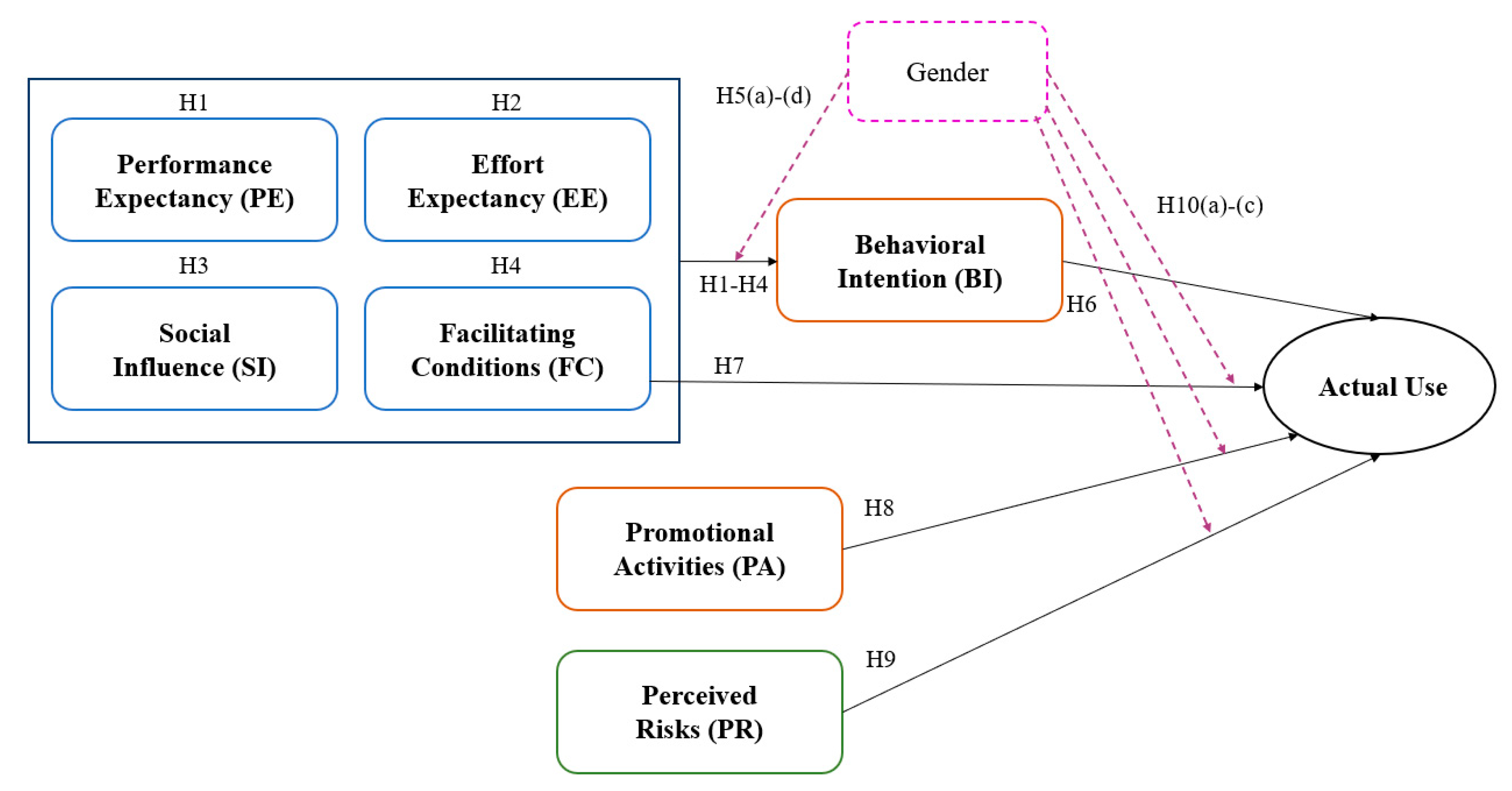

The behavioral model this study is based on is an extension of the unified theory of acceptance and use of technology (UTAUT). The extended UTAUT includes perceived risks and promotional activities as additional determinants of the actual usage of mobile payment. The young generation differs from other generations in terms of “systematic differences in values, preferences and behavior that are stable over time” [

7], p. 245. However, limited attention has been devoted to the understanding of the young generation’s risk preferences. In order to advance the body of knowledge on this subject, this study extends the UTAUT model to include perceived risks in the delineation of the young generation’s behavior. Perceived risk is one important dimension in shaping the behavioral intention and usage of mobile payment [

8,

9,

10]. Similar to the focus on consumers’ risk perception, one line of previous studies is to stress psychological concerns including trust [

11,

12,

13], distrust [

14], perceived security risk [

15], and perceived financial, privacy, and performance risks [

16] in modeling consumers’ intention to use online services. It is found that trust of the mobile service provider and mobile technology [

11] and the mobile payment vendor [

12] are key factors influencing intention to use mobile payment. A similar conclusion applies to the consumer’s online repurchase behavior [

13]. In light of the important role of both trust and distrust in influencing the decision to adopt IT-enabled exchange mode, some authors [

14] investigated the effects of trust and distrust through the use of “functional neuroimaging (fMRI) tools to complement psychometric measures of trust and distrust” [

14]. Neuroscience has also been applied to investigate the consumer’s neural response to risky and secure e-payments [

15] and how consumers process online risks [

16]. The authors [

15] found that consumers’ choice of payment systems is determined by the consumer’s neural response.

Financial incentives in different forms, monetary and/or nonmonetary rewards, have been found to be effective in attracting and attaining customers in the process of product or service promotion [

17,

18]. There were only a handful of studies providing empirical evidence to support the effect, especially that of monetary rewards offered by mobile pay companies, on the usage of this new payment alternative. In a very recent research addressing the pull, push, and mooring factors of mobile payment users’ switching behavior, it was found that monetary rewards provided by mobile payment applications pull the users to switch [

19]. Targeted on young US adults, some authors [

20] found cashback and discount to impact positively the intention to adopt near field communication (NFC) mobile payment. In addition to monetary rewards, this study considers two other forms of nonmonetary rewards offered by the mobile payment companies, including bonus points and gifts with targeted amounts of purchase. By emphasizing the influence of promotion strategies on the young generation’s mobile payment adoption, the present study makes a significant complement to the literature devoted to the modeling of technology acceptance behavior.

Additionally, this study adds to the literature on mobile payment by assessing the gender moderating effects among the young generation. When it comes to behavioral analysis of information communication technology (ICTs) adoption, it is important to recognize variations in terms of drivers/barriers between different demographic groups, namely, female vs. male [

21], and young vs. old [

22]. Gender as a moderator has been examined in the context of adopting mobile internet [

23], mobile payments [

24,

25,

26], mobile banking [

27,

28], and mobile apps [

29], etc. Although the effects of some UTAUT constructs on the adoption behavior were shown to be moderated by gender [

23,

24,

25,

30,

31], the gender moderation effect was not observed in some cases, for example, [

26,

28,

29]. One possible explanation for the diverse results may be due to not taking into account the possible interplay of the two demographic characteristics—gender and age. By focusing our attention on the young generation, this study provides a more concrete examination of the role of gender in moderating the relationships between determinants and adoption behavior.

The remainder of this paper proceeds as follows.

Section 2 presents the description of the UTAUT model extended to include the constructs of promotional activities and perceived risks and the research hypothesis built on the theoretical foundation.

Section 3 introduces the survey data and the empirical framework. Following

Section 3 is a discussion of the path analysis and the drivers/barriers of mobile payment use. The final section summarizes the major findings and limitations.

5. Discussion

One of the major purposes of this study is to examine the structural relationships between the UTAUT constructs and the young generation’s behavioral intention to use mobile payment. There are a couple of characteristics that distinguish the young generations, generations Y and Z, from the older generations before them. One of the unique characteristics of the young generation is tech-savvy since they grew up with new technologies and rely heavily on the Internet for their daily lives and work [

60]. Considering the unique characteristics of the young generations, this study focuses on examining: (1) if all the four UTAUT constructs—performance expectancy, effort expectancy, social influence, and facilitating conditions—are key determinants of the young generation’s intention to use mobile payment; and (2) if not, which of the four constructs shape the young generation’s intention to use mobile payment. The empirical investigations conducted in the present study, therefore, reinforce the applicability of the UTAUT model in predicting the young generation’s intention to use mobile payment.

Among the four UTAUT constructs (

Table 5), only the social influence construct has a significantly positive effect on Taiwanese young generation’s behavioral intentions to adopt mobile payment (β = 0.107,

p < 0.10). The result supports the hypothesized effect of social influence on the young generation’s behavioral intention, as stated in H3. This result is in line with previous findings of the positive influence of parental role model [

35] and family/peer influence [

5,

36,

38] on the young generation’s purchasing or usage of mobile technology. It was indicated that in countries where information systems have been well developed, generation Y are “followers of social norms, especially those in their circles of peers” [

5], p. 738. This also accords with the observation that generations Y and Z, which our sample is formed of, have a high level of social influence in trying the new technology services such as the tablet [

22] and use of financial services [

38]. The managerial implication of this finding reinforces the need to take into account the effect of social influence in designing promotion programs motivating the young generation’s adoption of mobile payment.

The moderating roles of gender on the behavioral intention to adopt mobile payment as reported in the lower part of

Table 5 indicate a stronger social influence impact on men’s intention to use the mobile payment services, which corroborates the finding in the context of applying mobile SNS [

34]. Besides, we observe a positive impact of effort expectancy among men, which is in line with [

25,

26,

29,

42]. However, no particular path was found to significantly affect female consumers. Although the UTAUT construct diversely affected men and women, gender was not found to moderate the UTAUT constructs significantly since none of the differences in the absolute value is different from zero. These results are in agreement with findings that gender does not moderate the young generation’s behavioral intention [

26,

29]. In the UTAUT literature of mobile payment, the moderator effect of gender in the structural relationships has been inconclusive [

26]. Understanding if gender moderates the structural relationship between UTAUT constructs and the young generation’s intention to use mobile payment in Taiwan can provide important managerial insights into the marketing strategies of the mobile-pay firms.

Celebrity endorsement has been studied within the context of social influence in affecting consumers’ purchase intention [

37,

39,

40,

41]. For instance, some authors [

40,

41] demonstrated that female customers are more attracted to celebrity endorsement of products. Under the consideration that celebrity endorsement may be some important factor for the young generation, we separate celebrity endorsement from other social influence factors to examine its path relationship with social influence. The path coefficients of celebrity endorsement, peers/families and image are 0.287 (

p < 0.01), 0.593 (

p < 0.01), and 0.323 (

p < 0.01), indicating their significantly positive effect on the social influence construct. Contrary to the finding that celebrity endorsement does not directly affect consumer’s intention to purchase online [

61], the results in this study suggest that product endorsement from celebrities has a significantly positive effect on young consumers’ intention to adopt mobile payment services. One of the marketing strategies in Taiwan’s mobile payment market is the product endorsement from young celebrities. The findings in this study confirm that celebrity endorsement is an effective way to increase potential users’ intention to use mobile payment.

In order to gain a better understanding of the young generation’s actual usage behavior, we calculate the average marginal effects of each of the determining factors in the probit model. The marginal effects (

Table 7) measure the influence of each of the determinants on the probability of actual usage holding all other predictors at the sample average.

The marginal effect estimate of behavioral intention indicates stronger behavioral intention results in an approximately 12% increase in the young generation’s actual usage of mobile payment. Among all the determinants of actual usage, the marginal effect of behavioral intention is found to be the most sizable. One of the main themes of the UTAUT is the strong structural relationship between behavioral intention and actual behavior. The findings in this study provide evidence to the validity of the extended UTAUT model in explaining generation Y’s and generation Z’s mobile payment usage.

The marginal effect estimate of facilitating conditions depicting the impact of infrastructure support exhibits a positive influence on the young generation’s mobile pay usage. The effect, however, is not significant. In comparison, the positive influence of financial incentives offered by the mobile payment companies, which include cash back rewards, bonus points and gifts with targeted amounts of purchase, is about the same size as the facilitating conditions but statistically significant. This result has important implications for increasing the adoption rate of mobile payment since the young generation is the largest group of potential users of this new payment mode. The bonus/rewards offered by credit card companies were found to induce the shift to its use [

62]. Some authors found a similar positive effect of cash back and discounts on Alipay users of various ages [

19] and for the US young adult’s NFC mobile payment adoption [

20]. It is worth noting that while the study of the impact of financial incentives on NFC mobile payment adoption [

20] was the first attempt with a focus on the young generation, this study is in turn one of the handful studies providing empirical evidence to delineate generation Y and Z’s adoption of mobile payment. The findings in this study provide solid evidence to support the view that the reward of cash/bonus may be one of the cost-efficient strategies to promote the use of mobile payment among young adults, which, thus, highlight the effect of financial incentives in the growing Asia-Pacific market.

According to the results in

Table 7, the two constructs capturing financial/privacy risks and psychological/social risks are found to significantly dampen the young generation’s probability of mobile payment adoption. The result, therefore, suggests the risk-averse preferences of Taiwan’s young generation. Some authors [

8] pointed out that despite the vast interests in examining the negative influence of perceived risk on the prevalence of mobile payment, there were limited attentions on the sources of risks perceived by the consumers. There are four sources of perceived risks considered in the present study: financial, privacy, psychological, and social risks. The estimates of marginal effect indicate a stronger effect of the first two facets on the probability of mobile payment use. According to the “Mobile Payment Consumer Survey and Analysis” by the Institute of Industrial Information (MIC) of the Council of Information Technology in 2017, the top two factors affecting Taiwanese mobile payment use are security concern (83.3%) and discount offered by the mobile payment firms (49.5%). The findings of a stronger effect of financial/privacy risk in this study concur with the dominant importance of perceived risks revealed by the nationally representative survey. Accordingly, the result further highlights the need for a more secure mobile payment network and policy in targeting the potential users of mobile payment in the future.

Celebrity endorsement is found to contribute positively to the young generation’s actual usage of mobile payment. Nonetheless, the effect is not statistically significant. Some authors [

63] concluded that the effect of celebrity endorsement depends largely on the nature of the product. Some previous studies of Indian teenagers [

63] concluded that in the case of products or services that require high involvement, celebrity endorsement may not create favorable results [

63]. The result in this study concurs with that conclusion.

The gender moderating effect is estimated by including the interaction terms as the independent variables in the probit model. Models 2–6 in

Table 6 and

Table 7 list the coefficient and marginal effect estimates from the probit model considering the moderation effect of gender. None of the interaction terms are statistically significant in

Table 6 and

Table 7, indicating that there does not exist a significant difference between the relationships proposed for different gender groups. The result of insignificant gender moderation effect may be due to the fact that there is a very mild difference in the mobile payment usage by gender exists in Taiwan. In a survey of internet usage in Taiwan, 24.6% of males and 25.5% of females reported the use of mobile payment [

64]. There is a broad agreement that gender is one dimension explaining the differences in the acceptance or adoption of internet-related products or services based on TAM (technology acceptance model) or UTAUT. The finding of insignificant gender moderation effect does not concur with the moderating role of gender featured in previous studies of mobile payments [

24,

25]. However, our finding is consistent with some previous studies of gender differences in computer and/or internet usage in Taiwan. It was found in previous research that an increase in age contributes significantly to the gender differences in the ICTs, which in turn suggests a much smaller gender gap among the young generations [

65].

In comparison, the mean scores of perceived risks (

Table 8) reveal that among the four risk facets, the young generation is more concerned with financial/privacy risks. A further comparison of the driving and deterring factors of generation Y’s and generation Z’s mobile payment use yield some interesting results. According to the group statistics of perceived risks by the two young generations (

Table 8), the statistics indicate that on average, generation Z’s concern of overall risk is stronger than that of generation Y. Moreover, it is interesting to find the presence of significant mean differences in psychological and social risks between generations Y and Z. On average, generation Z is found to be characterized with higher degree of anxiety, insecurity, and possible rejection associated with the usage of mobile payment.

6. Conclusions

The aim of the present research is to examine the factors affecting young generations’ behavioral intention and observed the adoption of mobile payment services in Taiwan. Furthermore, whether gender moderates the relationships between different constructs and behavioral intention or actual usage is tested through both path analysis and econometric modeling. Based on 295 samples aged from 16 to 38 collected from an online questionnaire, results from the structural equation analysis under the UTAUT framework reveal that social influence has a significantly positive effect on the young generation’s behavioral intention to adopt mobile payment. This result is consistent with previous findings [

21,

35,

42]. The empirical result also suggests that the influence of peers, celebrities, and role models uniquely contributes to the prevalence of mobile payment usage among the young generation. It is also found that the stronger the behavioral intention, the more likely young generations will adopt the services. One of the main themes of the UTAUT is the strong structural relationship between behavioral intention and actual behavior. The findings in this study provide evidence to the validity of the extended UTAUT model in explaining generation Y’s and generation Z’s mobile payment usage. Past studies on the drivers/barriers of mobile payment usage have been inconclusive. The findings in this study confirm that the reward of cash/bonus may be one of the efficient strategies to promote the use of mobile payment among young adults in Taiwan. The empirical evidence in this study provides a significant complement to the delineation of the effect of financial incentives on the actual use of mobile payment since there exist cultural differences between the young generations in the Western and Eastern societies.

The risk-averse preferences of Taiwan’s young generation are revealed in this study since different types of perceived risks significantly lowers the young generation’s probability to adopt mobile payment. The result highlights that a more secure mobile payment network and policy should be implemented. Finally, gender is found to neither moderate behavioral intention nor the actual usage. This finding, although being contrary to some previous studies, which are not focused on the young generation, reflects that there exists a relatively small gender gap in adopting ICTs as well as mobile payment services among the young generations in Taiwan. This study has advanced our understanding of the uniqueness of young consumers’ behavior in adopting new technological products such as mobile payment services. It is worth to mention that in the study of the usage of mobile banking in Singapore [

27], the insignificant moderation effect of risk on mobile banking adoption was attributed to the view of equal relevance of risk held by the two gender groups. Therefore, users’ perception of risk is one important aspect that needs to be addressed in order to deepen the adoption of mobile payment in the future.

The scope of this study is limited in terms of data representativeness. Specifically, as the survey was conducted online, the respondents are more concentrated in the student population. In addition, family background plays a major role in affecting students’ habits and tendency to use mobile payment since many of them rely on families’ monetary support. Therefore, the respondents’ household income is suggested to be taken into consideration. A promising avenue for further research is to explore how the drivers/barriers vary with respect to different subpopulations. The comparison of the moderation role of gender among different age cohorts also deserves further examination. It was indicated that the effect of celebrity endorsement can be addressed from various angles such as gender/personality congruity among users and endorsers [

66], celebrity persuasion, and brand-to-celebrity [

67]. In this study, the gender of the endorsers, the public image, and the personality of the endorsers were not taken into consideration. Since the endorsement of celebrity is found to be a crucial element of social influence in the present study, further research providing a more comprehensive delineation of the effect of celebrity endorsement may advance the understanding of the targeted potential consumers. Finally, the application of neuroscience to investigate the consumer’s neural response to risks has gained attention recently [

15,

16]. This line of research highlights the need for further research into the effects of psychological concerns, risks, and trust/distrust in explaining the behavioral intention and usage of mobile payment.

{kind=link}