A Literature Review of Taxes in Cross-Border Supply Chain Modeling: Themes, Tax Types and New Trade-Offs

Abstract

:1. Introduction

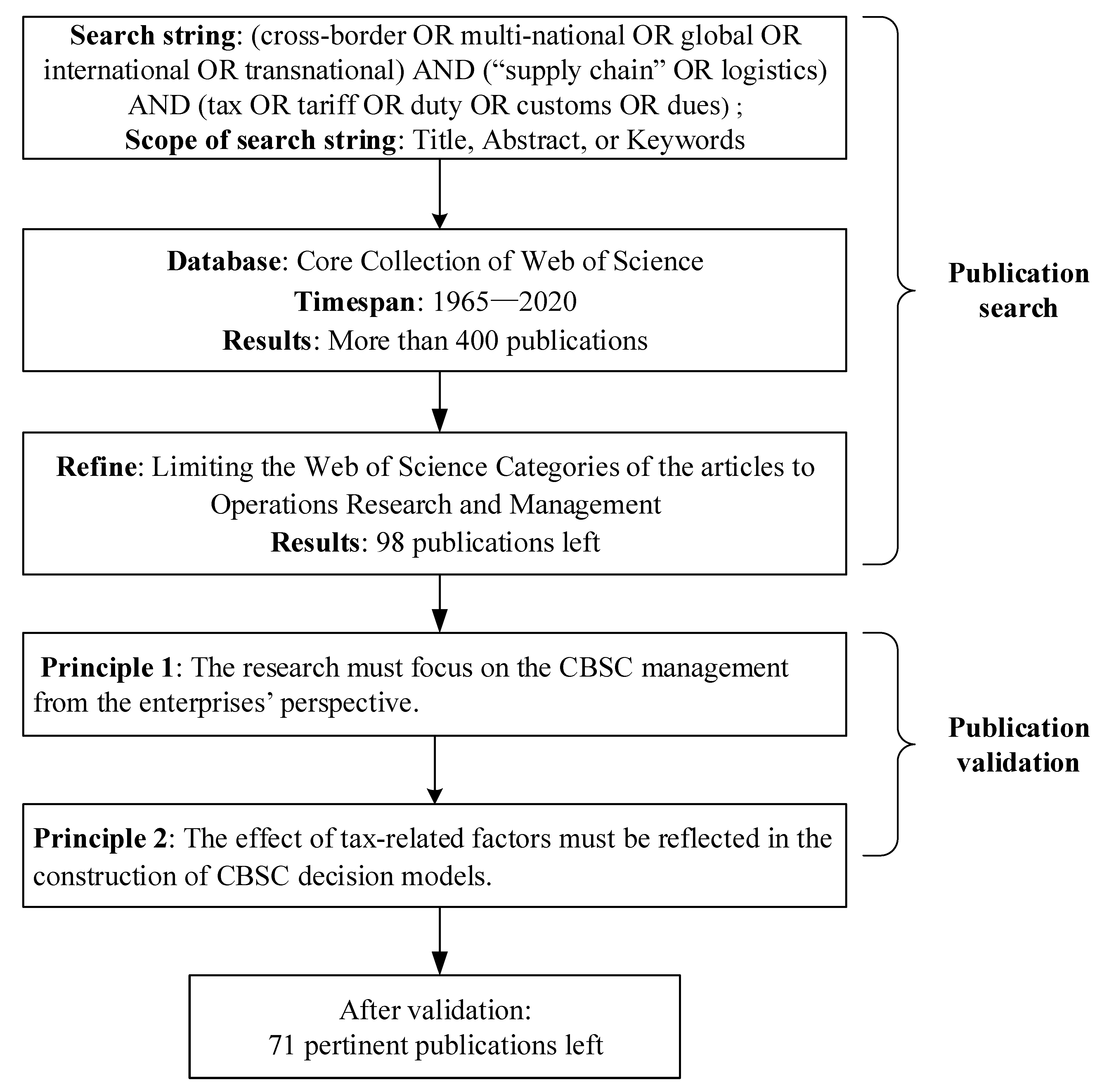

2. Methodology

2.1. Data Collection and Validation

- The publication must focus on CBSC management from the enterprises’ perspective. This excludes articles with a political or economic focus.

- The effect of tax-related factors must be one of the major considerations in the construction of CBSC decision models.

2.2. Coding Process

2.3. Validation of Coding Process

3. Descriptive and Content Analysis of Taxes in CBSC Modeling

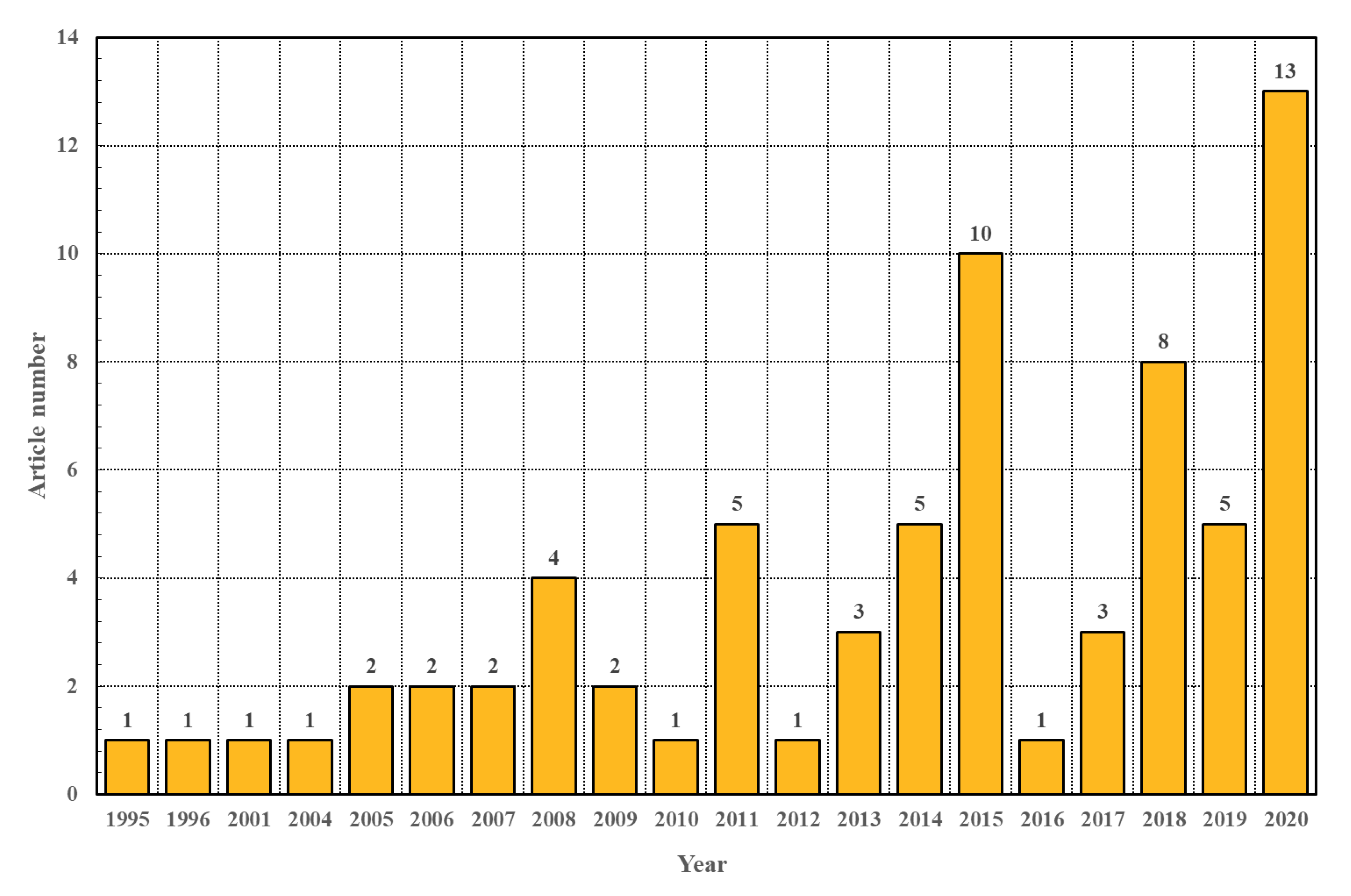

3.1. Publication Distribution

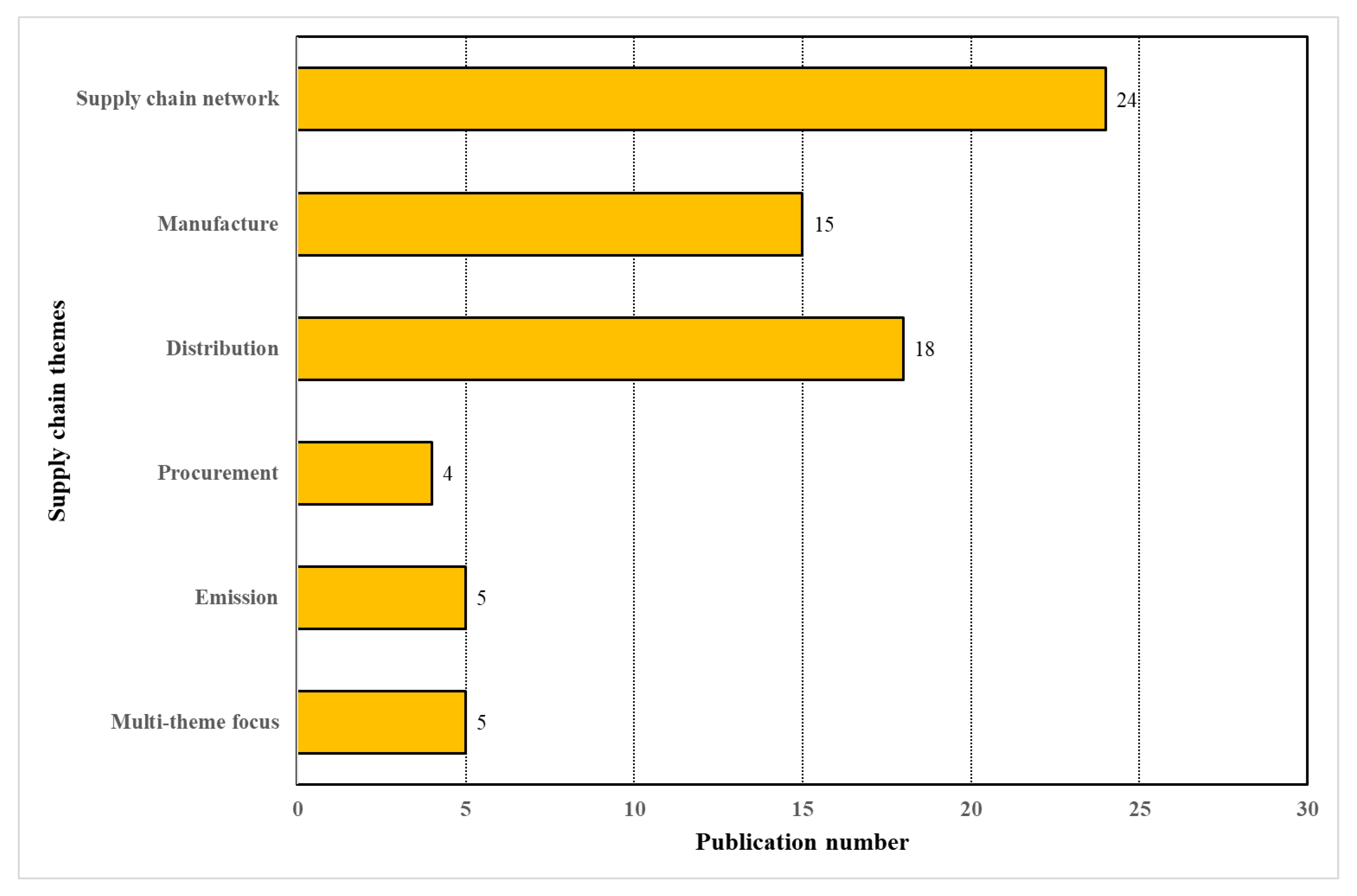

3.2. Supply Chain Themes Addressed

3.2.1. Supply Chain Network Category

3.2.2. Manufacturing Category

3.2.3. Distribution Category

3.2.4. Procurement Category

3.2.5. Emissions Category

3.2.6. Multi-Theme Category

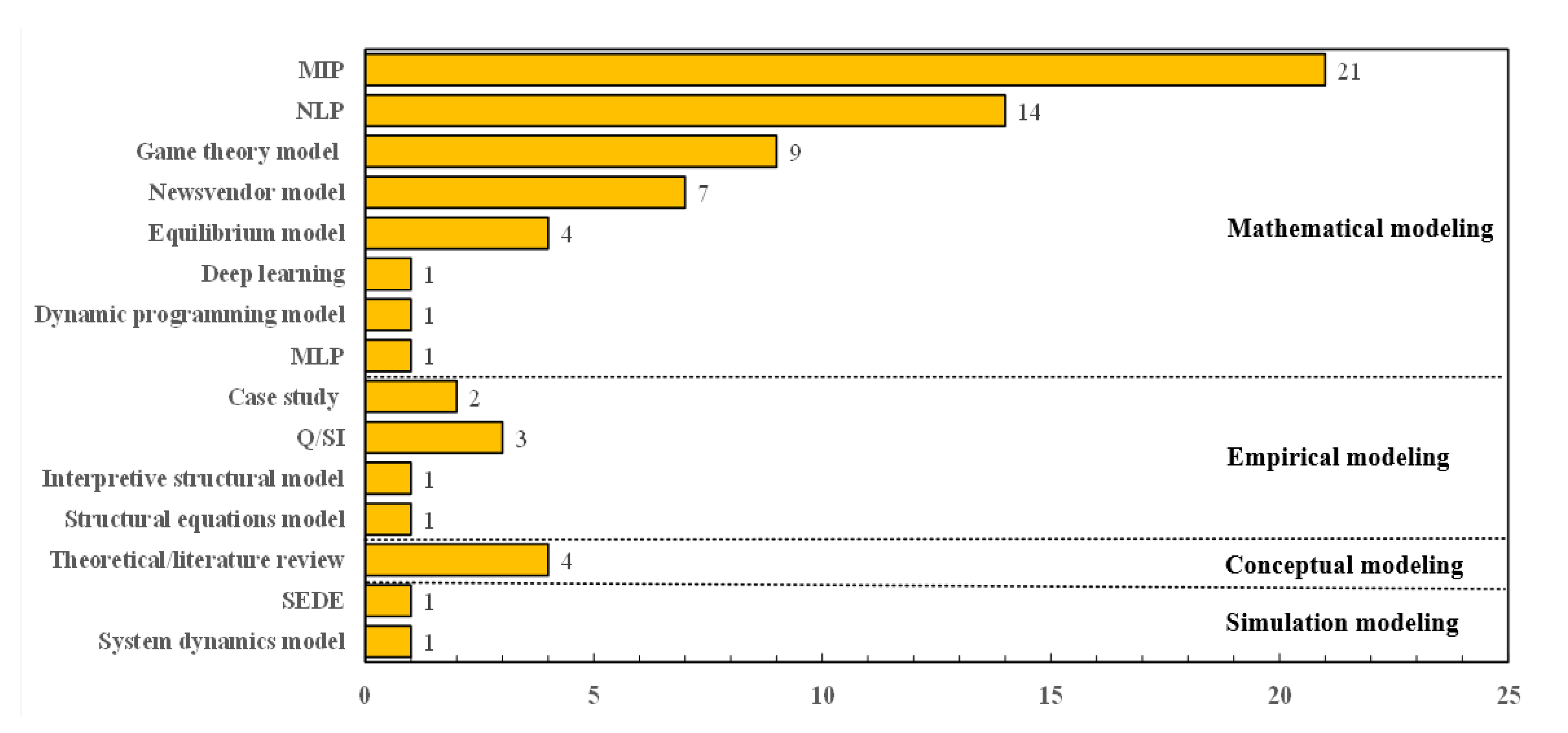

3.3. Research Methodology Dimension

3.3.1. Mathematical Modeling Category

3.3.2. Empirical Modeling Category

3.3.3. Conceptual Modeling Category

3.3.4. Simulation Modeling Category

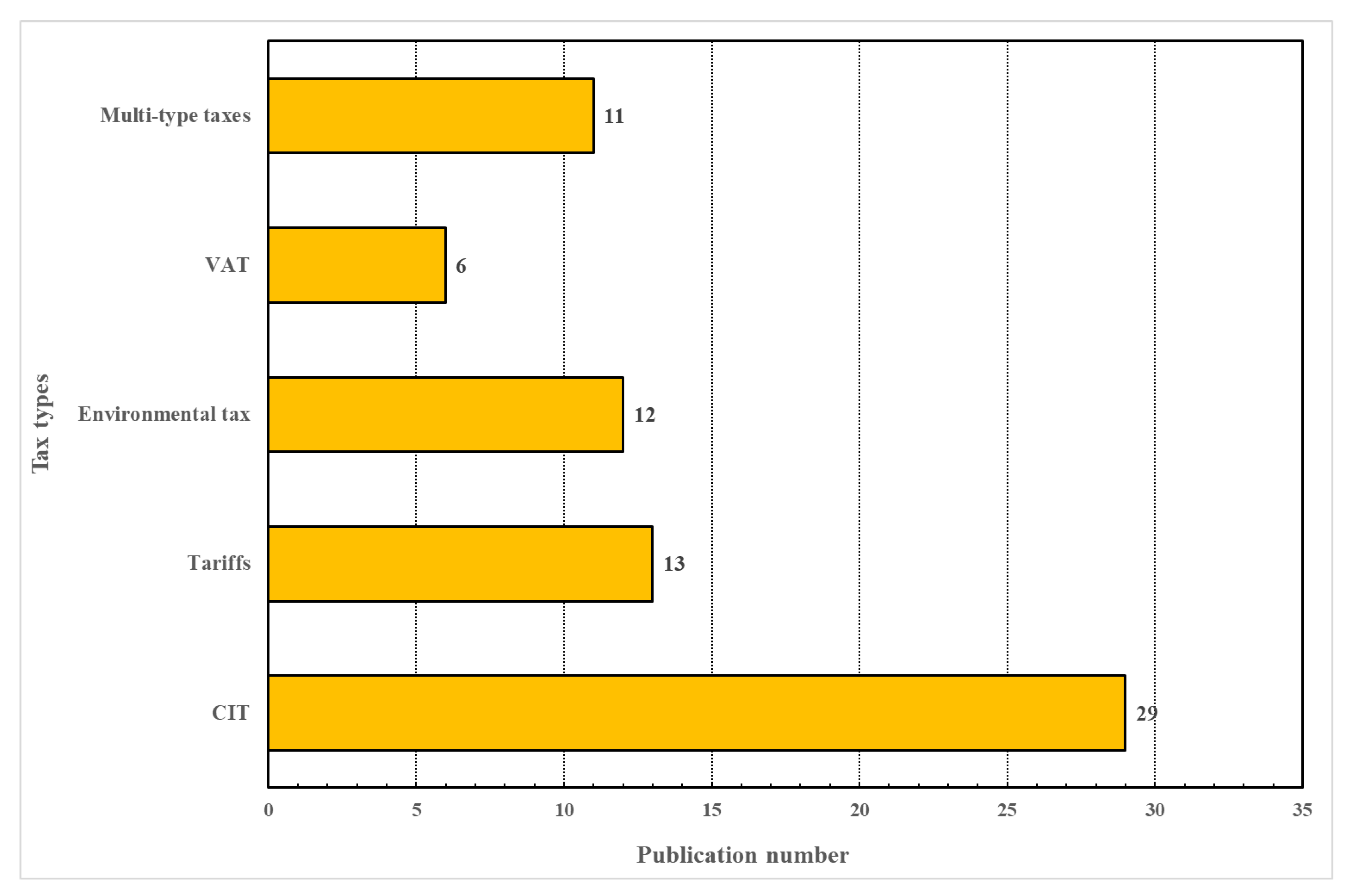

3.4. Tax Type Dimension

3.4.1. Corporate Income Tax Category

3.4.2. Tariffs Category

3.4.3. Environmental Tax Category

3.4.4. Value-Added Tax Category

3.4.5. Multi-Type Taxes Category

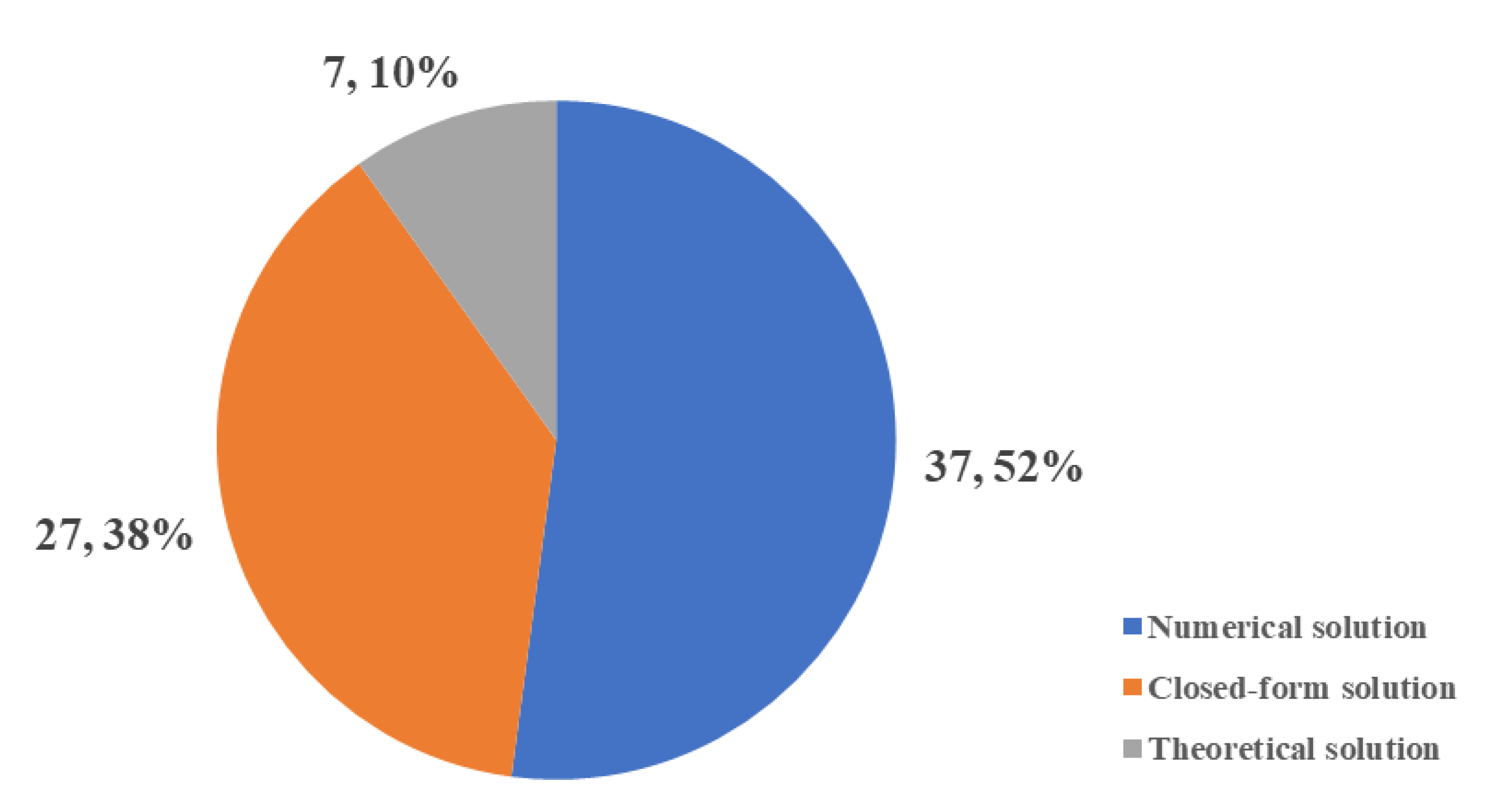

3.5. Illustration Type Dimension

3.5.1. Numerical Solution Category

3.5.2. Closed-Form Solution Category

3.5.3. Theoretical Solution Category

4. Discussion

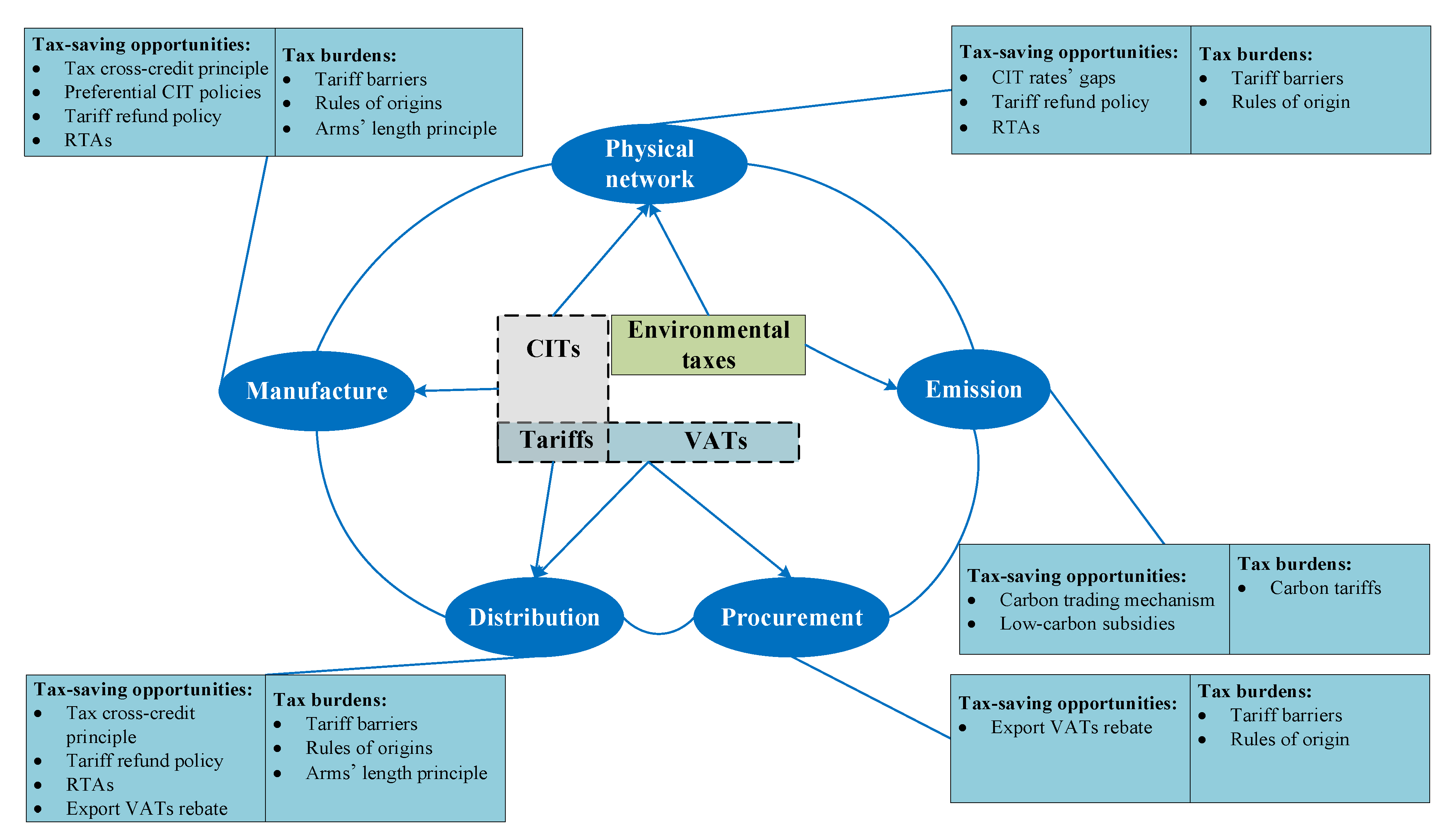

4.1. The Interface between CBSC Operations and Taxes

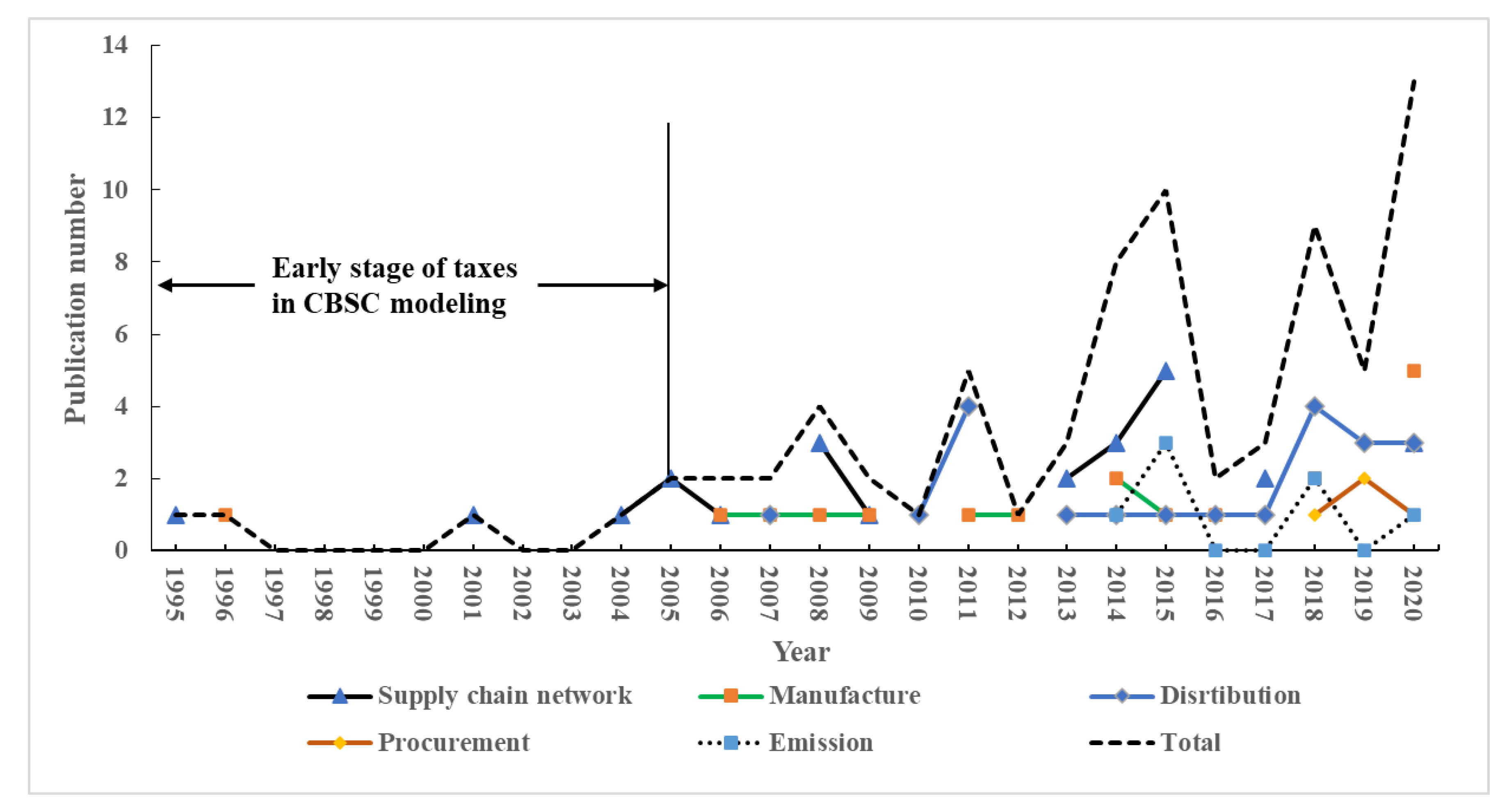

4.2. The Evolution of Supply Chain Themes

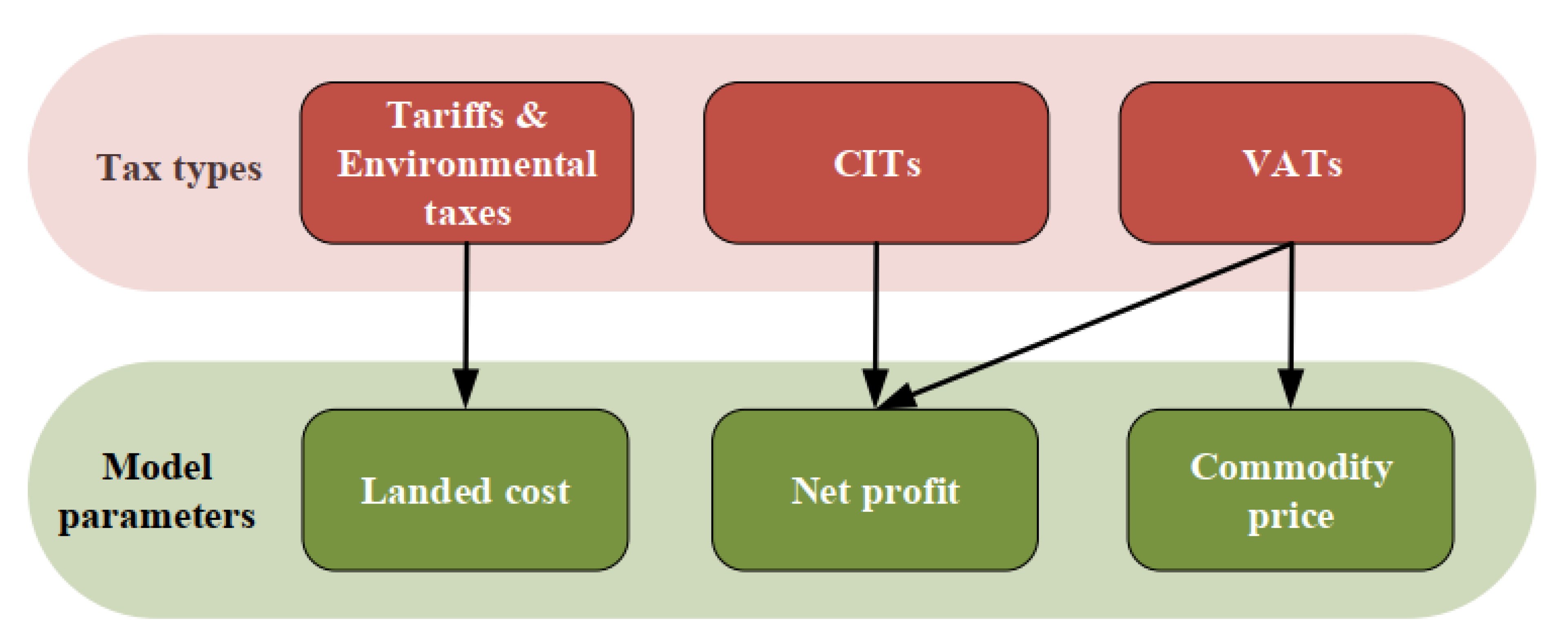

4.3. The Impacts of Different Taxes

4.4. New Trade-Offs

5. Research Opportunities

5.1. Modeling the Tax-Related Risks

5.2. Modifying Existing CBSC Models to Include Tax Conventions

5.3. Exploring the Conflicts among Different Tax Types

5.4. Modeling Different Tax Incentives in CBSC Operations

5.5. Embedding Tax Policies in Cross-Border E-Commerce Models

6. Conclusions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Durbhakula, V.K.; Kim, D.J. E-business for Nations: A Study of National Level Ebusiness Adoption Factors Using Country Characteristics-Business-Technology-Government Framework. J. Theor. Appl. Electron. Commer. Res. 2011, 6, 1–12. [Google Scholar] [CrossRef] [Green Version]

- Knol, A.; Tan, Y.H. The Cultivation of Information Infrastructures for International Trade: Stakeholder Challenges and Engagement Reasons. J. Theor. Appl. Electron. Commer. Res. 2018, 13, 106–117. [Google Scholar] [CrossRef] [Green Version]

- Navaretti, G.B.; Venables, A.J. Multinational Firms in the World Economy; Princeton University Press: Princeton, NJ, USA, 2020. [Google Scholar]

- Cohen, M.A.; Lee, H.L. Designing the right global supply chain network. MSOM-Manuf. Serv. Oper. Manag. 2020, 22, 15–24. [Google Scholar] [CrossRef] [Green Version]

- Cerrillo, R.A.; Rodriguez, M.G.L. Tax Implications of Selling Electronic Books in the European Union. J. Theor. Appl. Electron. Commer. Res. 2016, 11, 28–40. [Google Scholar] [CrossRef] [Green Version]

- Henkow, O.; Norrman, A. Tax aligned global supply chains: Environmental impact illustrations, legal reflections and crossfunctional flow charts. Int. J. Phys. Distrib. Logist. Manag. 2011, 41, 878–895. [Google Scholar] [CrossRef]

- Stef van Weeghel, A.P.; Dane, T.; Ramalho, R.; Croci, S.; Nasr, J. Paying Taxes 2020; PwC, the World Bank and International Finance Corporation: Washington, NY, USA, 2020; pp. 1–11. [Google Scholar]

- Feng, C.M.; Wu, P.J. A tax savings model for the emerging global manufacturing network. Int. J. Prod. Econ. 2009, 122, 534–546. [Google Scholar] [CrossRef]

- Hsu, V.N.; Zhu, K.J. Tax-effective supply chain decisions under China’s export-oriented tax policies. MSOM-Manuf. Serv. Oper. Manag. 2011, 13, 163–179. [Google Scholar] [CrossRef]

- Xu, J.Y.; Hsu, V.N.; Niu, B.Z. The impacts of markets and tax on a multinational firm’s procurement strategy in China. Prod. Oper. Manag. 2018, 27, 251–264. [Google Scholar] [CrossRef]

- WTO. Regional Trade Agreements; World Trade Organization: Geneva, Switzerland, 2020. [Google Scholar]

- Singh, S.; Haldar, N.; Bhattacharya, A. Offshore manufacturing contract design based on transfer price considering green tax: A bilevel programming approach. Int. J. Prod. Res. 2018, 56, 1825–1849. [Google Scholar] [CrossRef]

- Schenker, O.; Koesler, S.; Löschel, A. On the effects of unilateral environmental policy on offshoring in multi-stage production processes. Can. J. Econ. 2018, 51, 1221–1256. [Google Scholar] [CrossRef]

- Hsu, V.; Hu, Q.H. Global sourcing decisions for a multinational firm with foreign tax credit planning. IISE Trans. 2020, 52, 688–702. [Google Scholar] [CrossRef]

- Hammami, R.; Frein, Y. Integration of the profit-split transfer pricing method in the design of global supply chains with a focus on offshoring context. Comput. Ind. Eng. 2014, 76, 243–252. [Google Scholar] [CrossRef]

- Handfield, R.B.; Graham, G.; Burns, L. Corona virus, tariffs, trade wars and supply chain evolutionary design. Int. J. Oper. Prod. Manag. 2020, 40, 1649–1660. [Google Scholar] [CrossRef]

- Baldenius, T.; Reichelstein, S. External and internal pricing in multidivisional firms. J. Account. Res. 2006, 44, 1–28. [Google Scholar] [CrossRef]

- Baldenius, T.; Melumad, N.D.; Reichelstein, S. Integrating managerial and tax objectives in transfer pricing. Account. Rev. 2004, 79, 591–615. [Google Scholar] [CrossRef]

- Pfeiffer, T.; Schiller, U.; Wagner, J. Cost-based transfer pricing. Rev. Account. Stud. 2011, 16, 219–246. [Google Scholar] [CrossRef]

- Mayring, P. Qualitative content analysis. A Companion Qual. Res. 2004, 1, 159–176. [Google Scholar]

- Van Mieghem, J.A. Commissioned paper: Capacity management, investment, and hedging: Review and recent developments. Manuf. Serv. Oper. Manag. 2003, 5, 269–302. [Google Scholar] [CrossRef] [Green Version]

- Snyder, L.V.; Shen, Z.J.M. Introduction. In Fundamentals of Supply Chain Theory; John Wiley & Sons: Hoboken, NJ, USA, 2019; pp. 1–4. [Google Scholar]

- Ghadimi, P.; Wang, C.; Lim, M.K. Sustainable supply chain modeling and analysis: Past debate, present problems and future challenges. Resour. Conserv. Recycl. 2019, 140, 72–84. [Google Scholar] [CrossRef]

- Meixell, M.J.; Waller, M.; Norbis, M. A review of the transportation mode choice and carrier selection literature. Int. J. Logist. Manag. 2008, 19, 183–211. [Google Scholar] [CrossRef]

- Wilhelm, W.; Liang, D.; Rao, B.J.; Warrier, D.; Zhu, X.Y.; Bulusu, S. Design of international assembly systems and their supply chains under NAFTA. Transp. Res. Part E Logist. Transp. Rev. 2005, 41, 467–493. [Google Scholar] [CrossRef]

- Rebs, T.; Brandenburg, M.; Seuring, S. System dynamics modeling for sustainable supply chain management: A literature review and systems thinking approach. J. Clean. Prod. 2019, 208, 1265–1280. [Google Scholar] [CrossRef]

- Cronbach, L.J. Coefficient alpha and the internal structure of tests. Psychometrika 1951, 16, 297–334. [Google Scholar] [CrossRef] [Green Version]

- Arntzen, B.C.; Brown, G.G.; Harrison, T.P.; Trafton, L.L. Global supply chain management at Digital Equipment Corporation. Interfaces 1995, 25, 69–93. [Google Scholar] [CrossRef] [Green Version]

- Prataviera, L.B.; Norrman, A.; Melacini, M. Global distribution network design: Exploration of facility location driven by tax considerations and related cross-country implications. Int. J. Logist.-Res. Appl. 2020, 1–24. [Google Scholar] [CrossRef]

- Sabet, E.; Yazdani, B.; Kian, R.; Galanakis, K. A strategic and global manufacturing capacity management optimisation model: A Scenario-based multi-stage stochastic programming approach. Omega-Int. J. Manag. Sci. 2020, 93, 1–20. [Google Scholar] [CrossRef]

- Mariel, K.; Minner, S. Benders decomposition for a strategic network design problem under NAFTA local content requirements. Omega-Int. J. Manag. Sci. 2017, 68, 62–75. [Google Scholar] [CrossRef]

- Urata, T.; Yamada, T.; Itsubo, N.; Inoue, M. Global Supply Chain Network Design and Asian Analysis with Material-Based Carbon Emissions and Tax. Comput. Ind. Eng. 2017, 113. [Google Scholar] [CrossRef]

- de Matta, R.; Miller, T. Formation of a strategic manufacturing and distribution network with transfer prices. Eur. J. Oper. Res. 2015, 241, 435–448. [Google Scholar] [CrossRef]

- Fernandes, R.; Pinho, C.; Gouveia, B. Supply chain networks design and transfer-pricing. Int. J. Logist. Manag. 2015, 26, 128–146. [Google Scholar] [CrossRef]

- Hasani, A.; Zegordi, S.H.; Nikbakhsh, E. Robust closed-loop global supply chain network design under uncertainty: The case of the medical device industry. Int. J. Prod. Res. 2015, 53, 1596–1624. [Google Scholar] [CrossRef]

- Mariel, K.; Minner, S. Strategic capacity planning in automotive production networks under duties and duty drawbacks. Int. J. Prod. Econ. 2015, 170, 687–700. [Google Scholar] [CrossRef]

- Zhou, Y.; Gong, D.C.; Huang, B.; Peters, B.A. The Impacts of Carbon Tariff on Green Supply Chain Design. IEEE Trans. Autom. Sci. Eng. 2015, 14, 1542–1555. [Google Scholar] [CrossRef]

- Hamad, R.; Gualda, N.D.F. Global Sourcing Approach to Improve Cash Flow of Agribusiness Companies in Brazil. Interfaces 2014, 44, 317–327. [Google Scholar] [CrossRef]

- Hammami, R.; Frein, Y. Redesign of global supply chains with integration of transfer pricing: Mathematical modeling and managerial insights. Int. J. Prod. Econ. 2014, 158, 267–277. [Google Scholar] [CrossRef]

- Bassett, M.; Gardner, L. Designing optimal global supply chains at Dow AgroSciences. Ann. Oper. Res. 2013, 203, 187–216. [Google Scholar] [CrossRef]

- Fahimnia, B.; Parkinson, E.; Rachaniotis, N.P.; Mohamed, Z.; Goh, M. Supply chain planning for a multinational enterprise: A performance analysis case study. Int. J. Logist.-Res. Appl. 2013, 16, 349–366. [Google Scholar] [CrossRef]

- Hamad, R.; Gualda, N.D.F. Model for facilities or vendors location in a global scale considering several echelons in the Chain. Netw. Spat. Econ. 2008, 8, 297–307. [Google Scholar] [CrossRef]

- Miller, T.; de Matta, R. A global supply chain profit maximization and transfer pricing model. J. Bus. Logist. 2008, 29, 175–199. [Google Scholar] [CrossRef]

- Tsiakis, P.; Papageorgiou, L.G. Optimal production allocation and distribution supply chain networks. Int. J. Prod. Econ. 2008, 111, 468–483. [Google Scholar] [CrossRef]

- Vila, D.; Martel, A.; Beauregard, R. Designing logistics networks in divergent process industries: A methodology and its application to the lumber industry. Int. J. Prod. Econ. 2006, 102, 358–378. [Google Scholar] [CrossRef]

- Chakravarty, A.K. Global plant capacity and product allocation with pricing decisions—Production, manufacturing and logistics. Eur. J. Oper. Res. 2005, 165, 157–181. [Google Scholar] [CrossRef]

- Fandel, G.; Stammen, M. A general model for extended strategic supply chain management with emphasis on product life cycles including development and recycling. Int. J. Prod. Econ. 2004, 89, 293–308. [Google Scholar] [CrossRef]

- Vidal, C.J.; Goetschalckx, M. A global supply chain model with transfer pricing and transportation cost allocation. Eur. J. Oper. Res. 2001, 129, 134–158. [Google Scholar] [CrossRef]

- Niu, B.Z.; Li, Q.Y.; Liu, Y.Q. Conflict management in a multinational firm’s production shifting decisions. Int. J. Prod. Econ. 2020, 230, 107880. [Google Scholar] [CrossRef] [PubMed]

- Prataviera, L.B.; Perotti, S.; Melacini, M.; Moretti, E. Postponement strategies for global downstream supply chains: A conceptual framework. J. Bus. Logist. 2020, 41, 94–110. [Google Scholar] [CrossRef]

- Turken, N.; Carrillo, J.; Verter, V. Strategic supply chain decisions under environmental regulations: When to invest in end-of-pipe and green technology. Eur. J. Oper. Res. 2020, 283, 601–613. [Google Scholar] [CrossRef]

- Lu, X.Y.; Wu, Z.Q. How taxes impact bank and trade financing for Multinational Firms. Eur. J. Oper. Res. 2020, 286, 218–232. [Google Scholar] [CrossRef]

- Xiao, W.Q.; Hsu, V.N.; Hu, Q.H. Manufacturing capacity decisions with demand uncertainty and tax cross-crediting. MSOM-Manuf. Serv. Oper. Manag. 2015, 17, 384–398. [Google Scholar] [CrossRef] [Green Version]

- Choi, K.; Narasimhan, R.; Kim, S.W. Postponement strategy for international transfer of products in a global supply chain: A system dynamics examination. J. Oper. Manag. 2012, 30, 167–179. [Google Scholar] [CrossRef]

- Bogataj, D.; Bogataj, M. The role of free economic zones in global supply chains-a case of reverse logistics. Int. J. Prod. Econ. 2011, 131, 365–371. [Google Scholar] [CrossRef]

- Hameri, A.P.; Hintsa, J. Assessing the drivers of change for cross-border supply chains. Int. J. Phys. Distrib. Logist. Manag. 2009, 39, 741–761. [Google Scholar] [CrossRef]

- Lu, C.S.; Liao, C.H.; Yang, C.C. Segmenting manufacturers’ investment incentive preferences for international logistics zones. Int. J. Oper. Prod. Manag. 2008, 28, 106–129. [Google Scholar] [CrossRef]

- Kazmer, D.; Roser, C. Analysis of design for global manufacturing guidelines. In Proceedings of the ASME 2007 International Design Engineering Technical Conferences and Computers and Information in Engineering Conference, Las Vegas, NV, USA, 4–7 September 2007. [Google Scholar]

- Lu, C.S.; Yang, C.C. Comparison of investment preferences for international logistics zones in Kaohsiung, Hong Kong, and Shanghai ports from a Taiwanese manufacturer’s perspective. Transp. J. 2006, 45, 30–51. [Google Scholar]

- Huchzermeier, A.; Cohen, M.A. Valuing operational flexibility under exchange rate risk. Oper. Res. 1996, 44, 100–113. [Google Scholar] [CrossRef]

- Dong, L.X.; Kouvelis, P. Impact of tariffs on global supply chain network configuration: Models, predictions, and future research. MSOM-Manuf. Serv. Oper. Manag. 2020, 22, 25–35. [Google Scholar] [CrossRef]

- Gao, L.; Zhao, X. Determining intra-company transfer pricing for multinational corporations. Int. J. Prod. Econ. 2015, 168, 340–350. [Google Scholar] [CrossRef]

- Wang, X.H.; Xie, J.C.; Fan, Z.P. B2C cross-border E-commerce logistics mode selection considering product returns. Int. J. Prod. Res. 2021, 59, 3841–3860. [Google Scholar] [CrossRef]

- Nagurney, A.; Besik, D.; Nagurney, L.S. Global supply chain networks and tariff rate quotas: Equilibrium analysis with application to agricultural products. J. Glob. Optim. 2019, 75, 439–460. [Google Scholar] [CrossRef]

- Niu, B.Z.; Liu, Y.Q.; Liu, F.; Lee, C.K.M. Transfer pricing and channel structure of a multinational firm under overseas retail disruption risk. Int. J. Prod. Res. 2019, 57, 2901–2925. [Google Scholar] [CrossRef]

- Niu, B.Z.; Xu, J.W.; Lee, C.K.M.; Chen, L. Order timing and tax planning when selling to a rival in a low-tax emerging market. Transp. Res. Part E Logist. Transp. Rev. 2019, 123, 165–179. [Google Scholar] [CrossRef]

- Kim, B.; Park, K.S.; Jung, S.Y.; Park, S.H. Offshoring and outsourcing in a global supply chain: Impact of the arm’s length regulation on transfer pricing. Eur. J. Oper. Res. 2018, 266, 88–98. [Google Scholar] [CrossRef]

- Wu, Z.Q.; Lu, X.Y. The effect of transfer pricing strategies on optimal control policies for a tax-efficient supply chain. Omega-Int. J. Manag. Sci. 2018, 80, 209–219. [Google Scholar] [CrossRef]

- Zhang, X.B.; Huang, S.; Wan, Z. Stochastic programming approach to global supply chain management under random additive demand. Oper. Res. 2018, 18, 389–420. [Google Scholar] [CrossRef]

- Shunko, M.; Do, H.T.; Tsay, A.A. Supply chain strategies and international tax arbitrage. Prod. Oper. Manag. 2017, 26, 231–251. [Google Scholar] [CrossRef]

- Huh, W.T.; Park, K.S. Impact of transfer pricing methods for tax purposes on supply chain performance under demand uncertainty. Nav. Res. Logist. 2013, 60, 269–293. [Google Scholar] [CrossRef]

- Kumar, S.; Sosnoski, M. Decision framework for the analysis and selection of appropriate transfer pricing for a resilient global SME manufacturing operation—A business case. Int. J. Prod. Res. 2011, 49, 5431–5448. [Google Scholar] [CrossRef]

- Matsui, K. Intrafirm trade, arm’s-length transfer pricing rule, and coordination failure. Eur. J. Oper. Res. 2011, 212, 570–582. [Google Scholar] [CrossRef]

- Perron, S.; Hansen, P.; Le Digabel, S.; Mladenovic, N. Exact and heuristic solutions of the global supply chain problem with transfer pricing. Eur. J. Oper. Res. 2010, 202, 864–879. [Google Scholar] [CrossRef]

- Shunko, M.; Gavirneni, S. Role of transfer prices in global supply chains with random demands. J. Ind. Manag. Optim. 2007, 3, 99–117. [Google Scholar] [CrossRef]

- Cui, S.L.; Lu, L.X. Optimizing local content requirements under technology gaps. MSOM-Manuf. Serv. Oper. Manag. 2019, 21, 213–230. [Google Scholar] [CrossRef]

- Niu, B.Z.; Mu, Z.H.; Chen, K.L. Quality spillover, tariff, and multinational firms’ local sourcing strategies. Int. Trans. Oper. Res. 2019, 26, 2508–2530. [Google Scholar] [CrossRef]

- Fang, Y.; Yu, Y.G.; Shi, Y.; Liu, J. The effect of carbon tariffs on global emission control: A global supply chain model. Transp. Res. Part E Logist. Transp. Rev. 2020, 133, 101818. [Google Scholar] [CrossRef]

- Micheli, G.J.L.; Mantella, F. Modelling an environmentally-extended inventory routing problem with demand uncertainty and a heterogeneous fleet under carbon control policies. Int. J. Prod. Econ. 2018, 204, 316–327. [Google Scholar] [CrossRef]

- Bonilla, D.; Keller, H.; Schmiele, J. Climate policy and solutions for green supply chains: Europe’s predicament. Supply Chain Manag. 2015, 20, 249–263. [Google Scholar] [CrossRef] [Green Version]

- Fahimnia, B.; Sarkis, J.; Choudhary, A.; Eshragh, A. Tactical supply chain planning under a carbon tax policy scheme: A case study. Int. J. Prod. Econ. 2015, 164, 206–215. [Google Scholar] [CrossRef] [Green Version]

- Hammami, R.; Nouira, I.; Frein, Y. Carbon emissions in a multi-echelon production-inventory model with lead time constraints. Int. J. Prod. Econ. 2015, 164, 292–307. [Google Scholar] [CrossRef]

- Soysal, M.; Bloemhof-Ruwaard, J.M.; van der Vorst, J. Modelling food logistics networks with emission considerations: The case of an international beef supply chain. Int. J. Prod. Econ. 2014, 152, 57–70. [Google Scholar] [CrossRef]

- Masha Shunko, L.D.; Gavirneni, S. Transfer pricing and sourcing strategies for multinational firms. Prod. Oper. Manag. 2014, 23, 2043–2057. [Google Scholar] [CrossRef]

- Wang, Z.P.; Gao, W.L.; Mukhopadhyay, S.K. Impact of taxation on international transfer pricing and offshoring decisions. Ann. Oper. Res. 2016, 240, 683–707. [Google Scholar] [CrossRef]

- Zhen, L. A three-stage optimization model for production and outsourcing under China’s export-oriented tax policies. Transp. Res. Part E Logist. Transp. Rev. 2014, 69, 1–20. [Google Scholar] [CrossRef]

- Allevi, E.; Gnudi, A.; Konnov, I.V.; Oggioni, G. Evaluating the effects of environmental regulations on a closed-loop supply chain network: A variational inequality approach. Ann. Oper. Res. 2018, 261, 1–43. [Google Scholar] [CrossRef]

- Cohen, M.; Lee, H. Resource deployment analysis of global manufacturing and distribution network. J. Manuf. Oper. Manag. 1989, 2, 81–104. [Google Scholar]

- Reddy, K.N.; Kumar, A.; Sarkis, J.; Tiwari, M.K. Effect of carbon tax on reverse logistics network design. Comput. Ind. Eng. 2020, 139, 106184. [Google Scholar] [CrossRef]

- Dou, G.W.; Cao, K.Y. A joint analysis of environmental and economic performances of closed-loop supply chains under carbon tax regulation. Comput. Ind. Eng. 2020, 146, 106624. [Google Scholar] [CrossRef]

- Madani, S.R.; Rasti-Barzoki, M. Sustainable supply chain management with pricing, greening and governmental tariffs determining strategies: A game-theoretic approach. Comput. Ind. Eng. 2017, 105, 287–298. [Google Scholar] [CrossRef]

- Gao, J.Z.; Xiao, Z.D.; Wei, H.X.; Zhou, G.H. Dual-channel green supply chain management with eco-label policy: A perspective of two types of green products. Comput. Ind. Eng. 2020, 146, 106613. [Google Scholar] [CrossRef]

- Guo, L. Cross-border e-commerce platform for commodity automatic pricing model based on deep learning. Electron. Commer. Res. 2020. [Google Scholar] [CrossRef]

- Du, J.; Sun, Y.; Ren, H. The relationship of delivery frequency with the cost and resource operational efficiency: A case study of jingdong logistics. Math. Comput. Sci. 2018, 3, 129–140. [Google Scholar]

- Drtina, R.; Correa, H.L. How transfer prices can affect a supply chain strategic decision. Int. J. Logist. Syst. Manag. 2011, 8, 363–376. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Dimension and Categories | References |

|---|---|

| Dimension 1: Themes | Van Mieghem [21]; Snyder L V [22] Inductively deduced |

| ● Supply chain network | |

| ● Manufacture | |

| ● Distribution ● Procurement ● Emission | |

| Dimension 2: Research methodologies | Ghadimi et al. [23]; Meixell et al. [24] Inductively deduced |

| ● Mathematical modeling | |

| ● Empirical modeling | |

| ● Simulation modeling | |

| ● Conceptual modeling | |

| Dimension 3: Tax types | Henkow and Norrman [6] Inductively deduced |

| ● Corporate income tax category | |

| ● Tariffs category | |

| ● Environmental tax category | |

| ● Value-added tax category | |

| ● Multi-type tax category | |

| Dimension 4: illustration types | Ghadimi et al. [23] Inductively deduced |

| ● Numerical solution | |

| ● Closed-form solution | |

| ● Theoretical solution |

| Themes Category | Publications |

|---|---|

| Supply chain network (24) | Cohen and Lee [4]; Prataviera et al. [29]; Sabet et al. [30]; Mariel and Minner [31]; Tomoyuki Urata [32]; de Matta and Miller [33]; Fernandes et al. [34]; Hasani et al. [35]; Mariel and Minner [36]; Yuan Zhou [37]; Hamad and Gualda [38]; Hammami and Frein [39]; Bassett and Gardner [40]; Fahimnia et al. [41]; Feng and Wu [8]; Hamad and Gualda [42]; Miller and de Matta [43]; Tsiakis and Papageorgiou [44]; Vila et al. [45]; Chakravarty [46]; Wilhelm et al. [25]; Fandel and Stammen [47]; Vidal and Goetschalckx [48]; Arntzen et al. [28]. |

| Manufacture (15) | Handfield et al. [16]; Niu et al. [49]; Prataviera et al. [50]; Turken et al. [51]; Lu and Wu [52]; Oliver Schenker [13]; Singh et al. [12]; Xiao et al. [53]; Choi et al. [54]; Bogataj and Bogataj [55]; Hameri and Hintsa [56]; Lu et al. [57]; Kazmer and Roser [58]; Lu and Yang [59]; Huchzermeier and Cohen [60]. |

| Distribution (18) | Dong and Kouvelis [61]; Gao [62]; Wang et al. [63]; Nagurney et al. [64]; Niu et al. [65]; Niu et al. [66]; Kim et al. [67]; Wu and Lu [68]; Zhang et al. [69]; Shunko et al. [70]; Gao and Zhao [62]; Huh and Park [71]; Henkow and Norrman [6]; Kumar and Sosnoski [72]; Matsui [73]; Hsu and Zhu [9]; Perron et al. [74]; Shunko and Gavirneni [75]. |

| Procurement (4) | Hsu and Hu [14]; Cui and Lu [76]; Niu et al. [77]; Xu et al. [10]. |

| Emission (5) | Fang et al. [78]; Micheli and Mantella [79]; Bonilla et al. [80]; Fahimnia et al. [81]; Hammami et al. [82]. |

| Multi-theme focus (5) | |

| Network design & Emission | Soysal et al. [83]. |

| Manufacture & Distribution | Masha Shunko [84]; Wang et al. [85]. |

| Manufacture & Procurement | Zhen [86]. |

| Emission & Distribution | Allevi et al. [87]. |

| Method Category | Methodology Approach | Publications |

|---|---|---|

| Mathematical modeling (58) | Mixed integer programming model (MIP) (21) | Sabet et al. [30]; Micheli and Mantella [79]; Tomoyuki Urata [32]; de Matta and Miller [33]; Hammami et al. [82]; Hasani et al. [35]; Mariel and Minner [36]; Yuan Zhou [37]; Hamad and Gualda [38]; Bassett and Gardner [40]; Fahimnia et al. [41]; Perron et al. [74]; Feng and Wu [8]; Hamad and Gualda [42]; Miller and de Matta [43]; Tsiakis and Papageorgiou [44]; Vila et al. [45]; Wilhelm et al. [25]; Fandel and Stammen [47]; Vidal and Goetschalckx [48]; Arntzen et al. [28]. |

| Non-linear programming model (NLP) (14) | Dong and Kouvelis [61]; Turken et al. [51]; Kim et al. [67]; Singh et al. [12]; Zhang et al. [69]; Mariel and Minner [31]; Shunko et al. [70]; Wang et al. [85]; Fahimnia et al. [81]; Gao and Zhao [62]; Hammami and Frein [39]; Masha Shunko [84]; Zhen [86]; Chakravarty [46]. | |

| Game theory model (9) | Fang et al. [78]; Niu et al. [49]; Cui and Lu [76]; Niu et al. [77]; Niu et al. [65]; Niu et al. [66]; Wu and Lu [68]; Xu et al. [10]; Matsui [73]. | |

| Newsvendor model (7) | Hsu and Hu [14]; Lu and Wu [52]; Wang et al. [63]; Xiao et al. [53]; Huh and Park [71] Hsu and Zhu [9]; Shunko and Gavirneni [75]. | |

| Equilibrium model (4) | Nagurney et al. [64]; Allevi et al. [87]; Oliver Schenker [13]; Bogataj and Bogataj [55]. | |

| Multi-objective linear programming model (MLP) (1) | Soysal et al. [83]. | |

| Dynamic programming model (1) | Huchzermeier and Cohen [60]. | |

| Deep learning (1) | Guo [62]. | |

| Empirical modeling (7) | Structural equations model (1) | Bonilla et al. [80]. |

| Interpretive structural model (1) | Kumar and Sosnoski [72]. | |

| Questionnaire surveys/Semi-structured interviews (3) | Henkow and Norrman [6]; Lu et al. [57]; Lu and Yang [59]. | |

| Case study (2) | Prataviera et al. [29]; Kazmer and Roser [58]. | |

| Conceptual modeling (4) | Theoretical/literature review (4) | Cohen and Lee [4]; Handfield et al. [16]; Prataviera et al. [50]; Hameri and Hintsa [56]. |

| Simulation modeling (2) | System dynamics model (1) | Choi et al. [54]. |

| Simulation experiment based on discrete events (1) | Fernandes et al. [34]. |

| Tax Types Category | Publications |

|---|---|

| Corporate income tax (29) | Hsu and Hu [14]; Lu and Wu [52]; Prataviera et al. [29]; Cui and Lu [76]; Niu et al. [65]; Niu et al. [66]; Kim et al. [67]; Wu and Lu [68]; Zhang et al. [69]; Shunko et al. [70]; Wang et al. [85]; de Matta and Miller [33]; Fernandes et al. [34]; Gao and Zhao [62]; Xiao et al. [53]; Hamad and Gualda [38]; Hammami and Frein [39]; Masha Shunko [84]; Huh and Park [71]; Kumar and Sosnoski [72]; Matsui [73]; Perron et al. [74]; Hameri and Hintsa [56], Lu et al. [57]; Miller and de Matta [43]; Shunko and Gavirneni [75]; Lu and Yang [59]; Vidal and Goetschalckx [48]; Huchzermeier and Cohen [60]. |

| Tariffs (13) | Dong and Kouvelis [61]; Handfield et al. [16]; Prataviera et al. [50]; Lu and Wu [52]; Nagurney et al. [64]; Niu et al. [77]; Mariel and Minner [31]; Mariel and Minner [36]; Bassett and Gardner [40]; Fahimnia et al. [41]; Choi et al. [54]; Tsiakis and Papageorgiou [44]; Kazmer and Roser [58]. |

| Environmental tax (12) | Fang et al. [78]; Turken et al. [51]; Allevi et al. [87]; Micheli and Mantella [79]; Oliver Schenker [13]; Singh et al. [12]; Tomoyuki Urata [32]; Bonilla et al. [80]; Fahimnia et al. [81]; Hammami et al. [82]; Yuan Zhou [37]; Soysal et al. [83]. |

| Value-added tax (6) | Niu et al. [49]; Hamad and Gualda [42]; Xu et al. [10]; Zhen [86]; Bogataj and Bogataj [55]; Hsu and Zhu [9]. |

| Multi-type taxes (11) | |

| Hasani et al. [35]; Vila et al. [45]; Chakravarty [46]; Wilhelm et al. [25]; Fandel and Stammen [47]; Arntzen et al. [28]. |

| Guo [62]; Cohen and Lee [4]; Sabet et al. [30]; Henkow and Norrman [6]; Feng and Wu [8]. |

| Illustration Types Category | Publications |

|---|---|

| Numerical solution (37) | Guo [62]; Sabet et al. [30]; Nagurney et al. [64]; Allevi et al. [87]; Micheli and Mantella [79]; Oliver Schenker [13]; Singh et al. [12]; Zhang et al. [69]; Mariel and Minner [31]; Tomoyuki Urata [32]; Bonilla et al. [80]; de Matta and Miller [33]; Fahimnia et al. [81]; Hammami et al. [82]; Hasani et al. [35]; Mariel and Minner [36]; Yuan Zhou [37]; Hamad and Gualda [38]; Hammami and Frein [39]; Soysal et al. [83]; Bassett and Gardner [40]; Fahimnia et al. [41]; Choi et al. [54]; Bogataj and Bogataj [55]; Perron et al. [74]; Feng and Wu [8]; Lu et al. [57]; Hamad and Gualda [42]; Miller and de Matta [43]; Tsiakis and Papageorgiou [44]; Kazmer and Roser [58]; Lu and Yang [59]; Vila et al. [45]; Wilhelm et al. [25]; Fandel and Stammen [47]; Vidal and Goetschalckx [48]; Arntzen et al. [28]. |

| Closed-form solution (27) | Dong and Kouvelis [61]; Fang et al. [78]; Niu et al. [49]; Turken et al. [51]; Hsu and Hu [14]; Wang et al. [63]; Lu and Wu [52]; Cui and Lu [76]; Niu et al. [65]; Niu et al. [77]; Niu et al. [66]; Kim et al. [67]; Wu and Lu [68]; Xu et al. [10]; Shunko et al. [70]; Wang et al. [85]; Fernandes et al. [34]; Gao and Zhao [62]; Xiao et al. [53]; Masha Shunko [84]; Zhen [86]; Huh and Park [71]; Matsui [73]; Hsu and Zhu [9]; Shunko and Gavirneni [75]; Chakravarty [46]; Huchzermeier and Cohen [60]. |

| Theoretical solution (7) | Handfield et al. [16]; Cohen and Lee [4]; Prataviera et al. [29]; Prataviera et al. [50]; Henkow and Norrman [6]; Kumar and Sosnoski [72]; Hameri and Hintsa [56]. |

| Supply Chain Network | Manufacture | Distribution | Procurement | Emission | |

|---|---|---|---|---|---|

| MIP model | √ | √ | √ | ||

| NLP model | √ | √ | √ | √ | |

| Game theory model | √ | √ | √ | √ | |

| Newsvendor model | √ | √ | √ | ||

| Equilibrium model | √ | √ | |||

| MLP model | √ | √ | |||

| Dynamic programming model | √ | ||||

| Deep learning | √ | ||||

| Structural equations model | √ | ||||

| Interpretive structural model | √ | ||||

| Questionnaire surveys/Semi-structured interviews | √ | √ | |||

| Case study | √ | ||||

| Theoretical/literature review | √ | √ | |||

| System dynamics model | √ | ||||

| Simulation experiment based on discrete events | √ |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mu, D.; Ren, H.; Wang, C. A Literature Review of Taxes in Cross-Border Supply Chain Modeling: Themes, Tax Types and New Trade-Offs. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 20-46. https://0-doi-org.brum.beds.ac.uk/10.3390/jtaer17010002

Mu D, Ren H, Wang C. A Literature Review of Taxes in Cross-Border Supply Chain Modeling: Themes, Tax Types and New Trade-Offs. Journal of Theoretical and Applied Electronic Commerce Research. 2022; 17(1):20-46. https://0-doi-org.brum.beds.ac.uk/10.3390/jtaer17010002

Chicago/Turabian StyleMu, Dong, Huanyu Ren, and Chao Wang. 2022. "A Literature Review of Taxes in Cross-Border Supply Chain Modeling: Themes, Tax Types and New Trade-Offs" Journal of Theoretical and Applied Electronic Commerce Research 17, no. 1: 20-46. https://0-doi-org.brum.beds.ac.uk/10.3390/jtaer17010002