New Ways of Working through Emerging Technologies: A Meta-Synthesis of the Adoption of Blockchain in the Accountancy Domain

Abstract

:1. Introduction

2. Theoretical Framework

3. Method

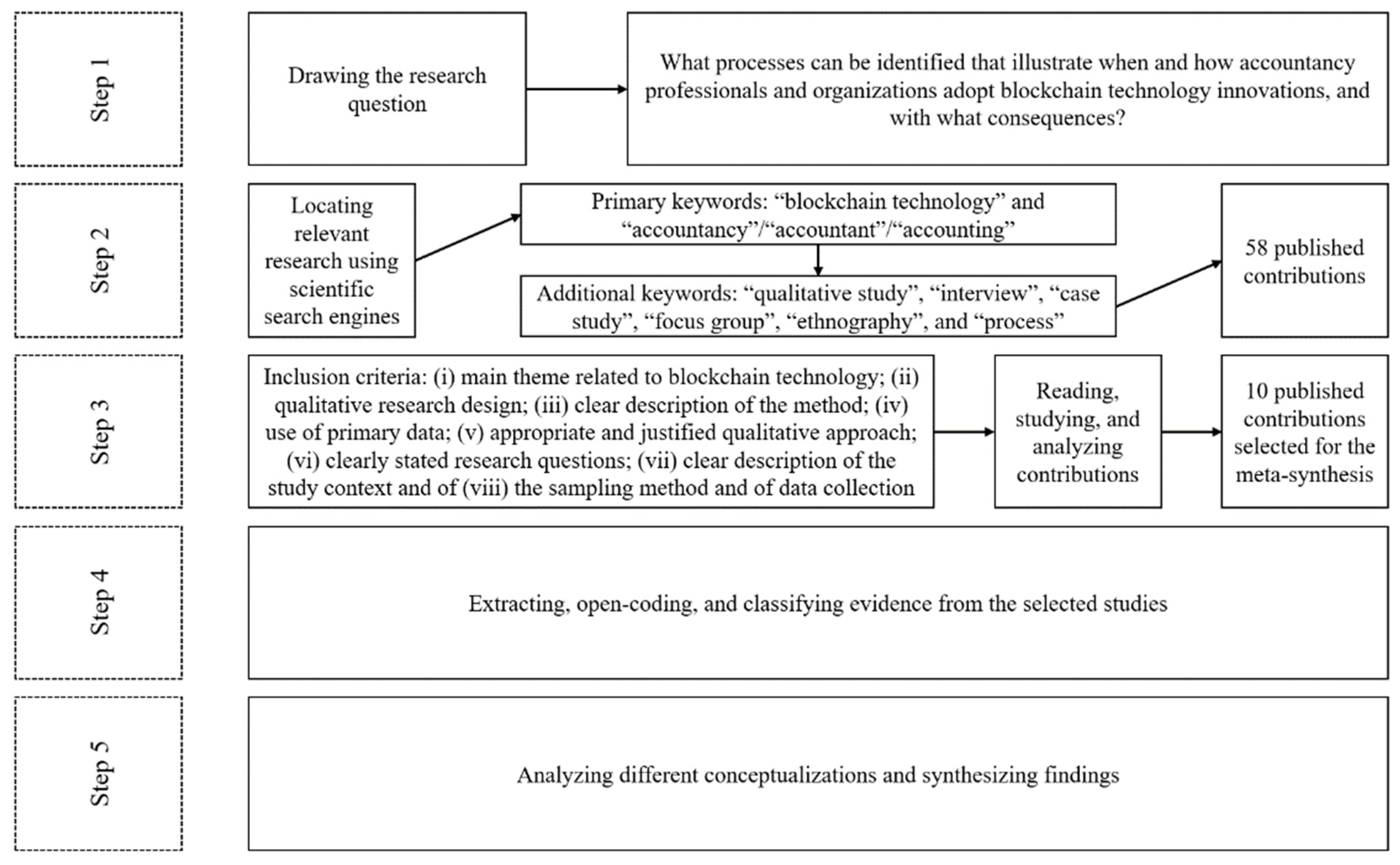

3.1. Formulating the Research Question

3.2. Locating Relevant Research

3.3. Establishing Inclusion and Exclusion Criteria

3.4. Extracting and Coding Data

3.5. Analyzing Different Conceptualizations and Synthesizing Findings

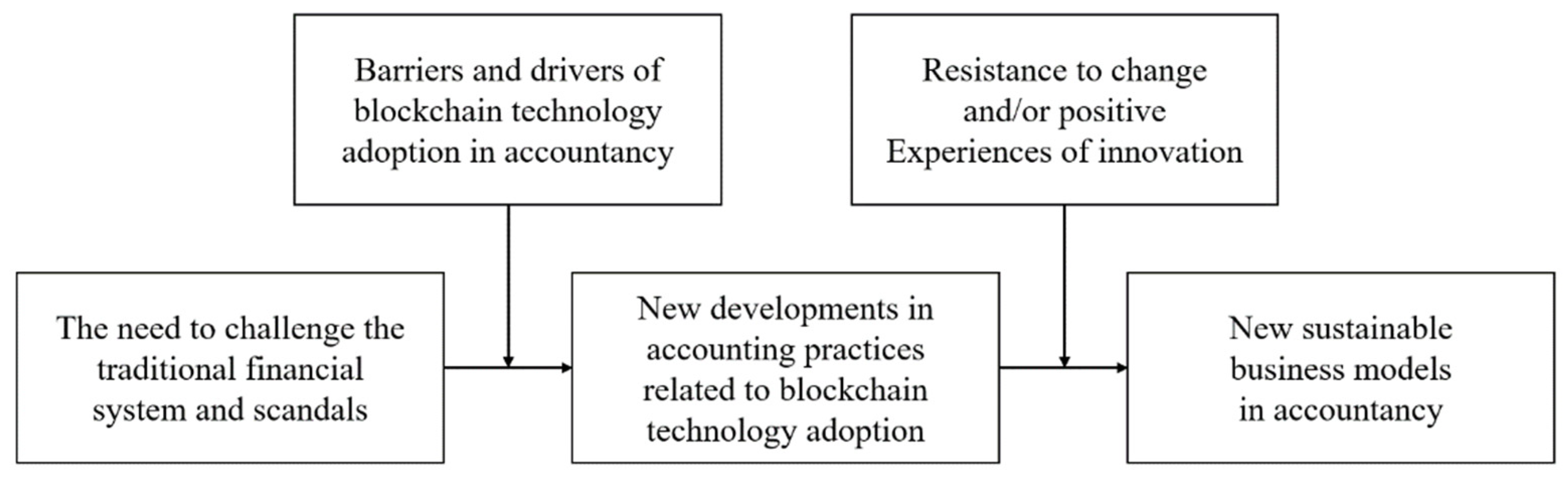

4. Results: A Process Model for Blockchain Adoption in Accountancy

4.1. The Need to Challenge the Traditional Financial System and Scandals

4.2. Barriers and Drivers of Blockchain Technology Adoption in Accountancy

4.3. New Developments in Accounting Practices Related to Blockchain Technology Adoption

4.4. Resistance to Change and/or Positive Experiences of Innovation

4.5. New Sustainable Business Models in Accountancy

5. Discussion and Conclusions

5.1. Contributions to the Literature

5.2. Practical Implications

5.3. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Nakamoto, S. Bitcoin: A peer-to-peer electronic cash system. White Paper. Available online: http://www.bitcoin.org/bitcoin.pdf (accessed on 1 February 2022).

- Natarajan, H.; Krause, S.; Gradstein, H. Distributed ledger technology and blockchain. In FinTech Note; World Bank: Washington, DC, USA, 2017. [Google Scholar]

- Kakarlapudi, P.V.; Mahmoud, Q.H. A systematic review of blockchain for consent management. In Healthcare; Multidisciplinary Digital Publishing Institute: Basel, Switzerland, 2021. [Google Scholar] [CrossRef]

- Niranjanamurthy, M.; Nithya, B.N.; Jagannatha, S. Analysis of blockchain technology: Pros, cons and SWOT. Clust. Comput. 2019, 22, 14743–14757. [Google Scholar] [CrossRef]

- Wang, Y.; Han, J.H.; Beynon-Davies, P. Understanding blockchain technology for future supply chains: A systematic literature review and research agenda. Int. J. Supply Chain Manag. 2019, 24, 62–84. [Google Scholar] [CrossRef]

- Zhang, L.; Xie, Y.; Zheng, Y.; Xue, W.; Zheng, X.; Xu, X. The challenges and countermeasures of blockchain in finance and economics. Syst. Res. Behav. Sci. 2020, 37, 691–698. [Google Scholar] [CrossRef]

- Pennino, D.; Pizzonia, M.; Vitaletti, A.; Zecchini, M. Blockchain as IoT Economy enabler: A review of architectural aspects. J. Sens. Actuator Netw. 2022, 11, 20. [Google Scholar] [CrossRef]

- Yuan, Y.; Wang, F.Y. Blockchain and cryptocurrencies: Model, techniques, and applications. IEEE Trans. Syst. Man Cybern. Syst. 2018, 48, 1421–1428. [Google Scholar] [CrossRef]

- Secinaro, S.; Dal Mas, F.; Brescia, V.; Calandra, D. Blockchain in the accounting, auditing and accountability fields: A bibliometric and coding analysis. Account. Audit. Account. J. 2021. ahead-of-print. [Google Scholar] [CrossRef]

- Kokina, J.; Davenport, T.H. The emergence of artificial intelligence: How automation is changing auditing. J. Emerg. Technol. Account. 2017, 14, 115–122. [Google Scholar] [CrossRef]

- Schmitz, J.; Leoni, G. Accounting and auditing at the time of blockchain technology: A research agenda. Aust. Account. Rev. 2019, 29, 331–342. [Google Scholar] [CrossRef]

- Bonsón, E.; Bednárová, M. Blockchain and its implications for accounting and auditing. Meditari Account. Res. 2019, 27, 725–740. [Google Scholar] [CrossRef]

- Guthrie, J.; Parker, L.D.; Dumay, J.; Milne, M.J. What counts for quality in interdisciplinary accounting research in the next decade: A critical review and reflection. Account. Audit. Account. J. 2019, 32, 2–25. [Google Scholar] [CrossRef] [Green Version]

- Tiron-Tudor, A.; Deliu, D. Reflections on the human-algorithm complex duality perspectives in the auditing process. Qual. Res. Account. Manag. 2021, 19, 255–285. [Google Scholar] [CrossRef]

- Spence, C.; Toh, D. Reaching up and out: The audit society. Qual. Res. Account. Manag. 2021, 19, 101–106. [Google Scholar] [CrossRef]

- Kosmarski, A. Blockchain adoption in academia: Promises and challenges. J. Open Innov. Technol. Mark. Complex. 2020, 6, 117. [Google Scholar] [CrossRef]

- Creswell, J.W.; Poth, C.N. Qualitative Inquiry and Research Design: Choosing among Five Approaches; Sage Publications: London, UK, 2016. [Google Scholar]

- Saunders, M.; Lewis, P.; Thornhill, A. Research Methods for Business Students; Pearson Education: London, UK, 2009. [Google Scholar]

- Mathilda, G.; Karin, D.J. Will Blockchain Save the World?: A Qualitative Study of How the Implementation of Blockchain Technology in Supply Chains Enables Sustainable Practices; Umeå School of Business and Economics: Umeå, Sweden, 2021. [Google Scholar]

- Crosby, M.; Pattanayak, P.; Verma, S.; Kalyanaraman, V. Blockchain technology: Beyond bitcoin. Appl. Syst. Innov. 2016, 2, 71. [Google Scholar]

- Xu, M.; Chen, X.; Kou, G. A systematic review of blockchain. Financ. Innov. 2019, 5, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Pilkington, M. Blockchain technology: Principles and applications. In Research Handbook on Digital Transformations; Edward Elgar Publishing: London, UK, 2016. [Google Scholar]

- Agrifoglio, R.; Metallo, C.; Rossignoli, C. Blockchain nella pubblica amministrazione: Benefici attesi e implicazioni organizzative. Prospett. Organ. 2021, 14, 1–14. [Google Scholar]

- Casey, M.J.; Vigna, P. In blockchain we trust. MIT Technol. Rev. 2018, 121, 10–16. [Google Scholar]

- Coyne, J.G.; McMickle, P.L. Can blockchains serve an accounting purpose? J. Emerg. Technol. Account. 2017, 14, 101–111. [Google Scholar] [CrossRef]

- Dai, J.; Vasarhelyi, M.A. Toward blockchain-based accounting and assurance. J. Inf. Syst. 2017, 31, 5–21. [Google Scholar] [CrossRef]

- Ferri, L.; Spanò, R.; Ginesti, G.; Theodosopoulos, G. Ascertaining auditors’ intentions to use blockchain technology: Evidence from the Big 4 accountancy firms in Italy. Meditari Account. Res. 2020, 29, 1063–1087. [Google Scholar] [CrossRef]

- Sheldon, M.D. Using blockchain to aggregate and share misconduct issues across the accounting profession. Curr. Issues Audit. 2018, 12, A27–A35. [Google Scholar] [CrossRef] [Green Version]

- Tiron-Tudor, A.; Deliu, D.; Farcane, N.; Dontu, A. Managing change with and through blockchain in accountancy organizations: A systematic literature review. J. Organ. Chang. Manag. 2021, 34, 477–506. [Google Scholar] [CrossRef]

- Wu, J.; Xiong, F.; Li, C. Application of Internet of Things and blockchain technologies to improve accounting information quality. IEEE Access 2019, 7, 100090–100098. [Google Scholar] [CrossRef]

- Estabrooks, C.A.; Field, P.A.; Morse, J.M. Aggregating qualitative findings: An approach to theory development. Qual. Health Res. 1994, 4, 503–511. [Google Scholar] [CrossRef]

- Neuman, W.L. Social Research Methods: Qualitative and Quantitative Approaches, 6th ed.; Allyn and Bacon: Boston, MA, USA, 2006. [Google Scholar]

- Mahmoud, Q.H.; Lescisin, M.; AlTaei, M. Research challenges and opportunities in blockchain and cryptocurrencies. Internet Technol. Lett. 2019, 2, e93. [Google Scholar] [CrossRef] [Green Version]

- Dixon-Woods, M.; Booth, A.; Sutton, A.J. Synthesizing qualitative research: A review of published reports. Qual. Res. 2007, 7, 375–422. [Google Scholar] [CrossRef]

- Hoon, C. Meta-synthesis of qualitative case studies: An approach to theory building. Organ. Res. Methods 2013, 16, 522–556. [Google Scholar] [CrossRef] [Green Version]

- Lazazzara, A.; Tims, M.; de Gennaro, D. The process of reinventing a job: A meta–synthesis of qualitative job crafting research. J. Vocat. Behav. 2020, 116, 103267. [Google Scholar] [CrossRef] [Green Version]

- Walsh, D.; Downe, S. Meta-synthesis method for qualitative research: A literature review. J. Adv. Nurs. 2005, 50, 204–211. [Google Scholar] [CrossRef]

- Kisamore, J.L.; Brannick, M.T. An illustration of the consequences of meta-analysis model choice. Organ. Res. Methods 2008, 11, 35–53. [Google Scholar] [CrossRef]

- Al-Htaybat, K.; Hutaibat, K.; von Alberti-Alhtaybat, L. Global brain-reflective accounting practices: Forms of intellectual capital contributing to value creation and sustainable development. J. Intellect. Cap. 2019, 20, 733–762. [Google Scholar] [CrossRef]

- Boulianne, E.; Fortin, M. Risks and Benefits of Initial Coin Offerings: Evidence from impak Finance, a Regulated ICO. Account. Perspect. 2020, 19, 413–437. [Google Scholar] [CrossRef]

- Cai, C.W. Triple-entry accounting with blockchain: How far have we come? Account. Financ. 2021, 61, 71–93. [Google Scholar] [CrossRef]

- Dal Mas, F.; Dicuonzo, G.; Massaro, M.; Dell’Atti, V. Smart contracts to enable sustainable business models. A case study. Manag. Decis. 2020, 58, 1601–1619. [Google Scholar] [CrossRef]

- Helliar, C.V.; Crawford, L.; Rocca, L.; Teodori, C.; Veneziani, M. Permissionless and permissioned blockchain diffusion. Int. J. Inf. Manag. 2020, 54, 102136. [Google Scholar] [CrossRef]

- Massaro, M.; Dal Mas, F.; Chiappetta Jabbour, C.J.; Bagnoli, C. Crypto-economy and new sustainable business models: Reflections and projections using a case study analysis. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 2150–2160. [Google Scholar] [CrossRef]

- Ozlanski, M.E.; Negangard, E.M.; Fay, R.G. Kabbage: A fresh approach to understanding fundamental auditing concepts and the effects of disruptive technology. Issues Account. Educ. 2020, 35, 26–38. [Google Scholar] [CrossRef]

- Roszkowska, P. Fintech in financial reporting and audit for fraud prevention and safeguarding equity investments. J. Account. Organ. Chang. 2020, 17, 164–196. [Google Scholar] [CrossRef]

- Sandner, P.; Lange, A.; Schulden, P. The role of the CFO of an industrial company: An analysis of the impact of blockchain technology. Future Internet 2020, 12, 128. [Google Scholar] [CrossRef]

- Zheng, Y.; Boh, W.F. Value drivers of blockchain technology: A case study of blockchain-enabled online community. Telemat. Inform. 2021, 58, 101563. [Google Scholar] [CrossRef]

- Easterby-Smith, M.; Golden-Biddle, K.; Locke, K. Working with pluralism: Determining quality in qualitative research. Organ. Res. Methods 2008, 11, 419–429. [Google Scholar] [CrossRef] [Green Version]

- Artstein, R.; Poesio, M. Inter-coder agreement for computational linguistics. J. Comput. Linguist. 2008, 34, 555–596. [Google Scholar] [CrossRef] [Green Version]

- Card, R.F. Individual responsibility within organizational contexts. J. Bus. Ethics 2005, 62, 397–405. [Google Scholar] [CrossRef]

- Sezer, O.; Gino, F.; Bazerman, M.H. Ethical blind spots: Explaining unintentional unethical behavior. Curr. Opin. Psychol. 2015, 6, 77–81. [Google Scholar] [CrossRef]

- ICAEW. Auditor Independence Approach. Available online: www.icaew.com/technical/ethics/auditor-independence/auditor-independence-approach (accessed on 12 March 2022).

- Tönnissen, S.; Teuteberg, F. Analysing the impact of blockchain-technology for operations and supply chain management: An explanatory model drawn from multiple case studies. J. Inf. Manag. 2020, 52, 101953. [Google Scholar] [CrossRef]

- Frizzo-Barker, J.; Chow-White, P.A.; Adams, P.R.; Mentanko, J.; Ha, D.; Green, S. Blockchain as a disruptive technology for business: A systematic review. J. Inf. Manag. 2020, 51, 102029. [Google Scholar] [CrossRef]

- Dunne, T.; Helliar, C.; Lymer, A.; Mousa, R. Stakeholder engagement in internet financial reporting: The diffusion of XBRL in the UK. Br. Account. Rev. 2013, 45, 167–182. [Google Scholar] [CrossRef]

- Kamble, S.S.; Gunasekaran, A.; Sharma, R. Modeling the blockchain enabled traceability in agriculture supply chain. J. Inf. Manag. 2020, 52, 101967. [Google Scholar] [CrossRef]

- Hanson, R.; Reeson, A.; Staples, M. Distributed Ledgers: Scenarios for the Australian Economy over the Coming Decades; CSIRO: Canberra, Australia, 2017. [Google Scholar]

- Caiazza, R. A cross-national analysis of policies affecting innovation diffusion. J. Technol. Transf. 2016, 41, 1406–1419. [Google Scholar] [CrossRef]

- Queiroz, M.M.; Wamba, S.F. Blockchain adoption challenges in supply chain: An empirical investigation of the main drivers in India and the USA. J. Inf. Manag. 2019, 46, 70–82. [Google Scholar] [CrossRef]

- Broadbent, B. Central Banks and Digital Currencies; Speech at the London School of Economics: London, UK, 2016. [Google Scholar]

- Denning, S. The Age of Agile: How Smart Companies are Transforming the Way Work Gets Done; Amacom: New York, NY, USA, 2018. [Google Scholar]

- Heylighen, F.; Lenartowicz, M. The Global Brain as a model of the future information society: An introduction to the special issue. Technol. Forecast. Soc. Chang. 2017, 114, 1–6. [Google Scholar] [CrossRef]

- Moll, J.; Yigitbasioglu, O. The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. Br. Account. Rev. 2019, 51, 100833. [Google Scholar] [CrossRef]

- Dicuonzo, G.; Donofrio, F.; Fusco, A.; Dell’Atti, V. Blockchain technology: Opportunities and challenges for small and large banks during COVID-19. Int. J. Innov. Technol. Manag. 2021, 18, 2140001. [Google Scholar] [CrossRef]

- Schmidt, C.G.; Wagner, S.M. Blockchain and supply chain relations: A transaction cost theory perspective. J. Purch. Supply Manag. 2019, 25, 100552. [Google Scholar] [CrossRef]

- Roeck, D.; Schöneseiffen, F.; Greger, M.; Hofmann, E. Analyzing the potential of DLT-based applications in smart factories. In Blockchain and Distributed Ledger Technology Use Cases; Springer: Cham, Switzerland, 2020; pp. 245–266. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Authors | Year of Publication | Title | Journal/Book | Doi |

|---|---|---|---|---|

| Al-Htaybat, K., Hutaibat, K., von Alberti-Alhtaybat, L. [39] | 2019 | Global brain-reflective accounting practices: Forms of intellectual capital contributing to value creation and sustainable development | Journal of Intellectual Capital | 10.1108/JIC-01-2019-0016 |

| Boulianne, E., Fortin, M. [40] | 2020 | Risks and Benefits of Initial Coin Offerings: Evidence from impak Finance, a Regulated ICO | Accounting Perspectives | 10.1111/1911-3838.12243 |

| Cai, C.W. [41] | 2021 | Triple-entry accounting with blockchain: How far have we come? | Accounting and Finance | 10.1111/acfi.12556 |

| Dal Mas, F., Dicuonzo, G., Massaro, M., Dell’Atti, V. [42] | 2020 | Smart contracts to enable sustainable business models. A case study | Management Decision | 10.1108/MD-09-2019-1266 |

| Helliar, C.V., Crawford, L., Rocca, L., Teodori, C., Veneziani, M. [43] | 2020 | Permissionless and permissioned blockchain diffusion | International Journal of Information Management | 10.1016/j.ijinfomgt.2020.102136 |

| Massaro, M., Dal Mas, F., Chiappetta Jabbour, C.J., Bagnoli, C. [44] | 2020 | Crypto-economy and new sustainable business models: Reflections and projections using a case study analysis | Corporate Social Responsibility and Environmental Management | 10.1002/csr.1954 |

| Ozlanski, M.E., Negangard, E.M., Fay, R.G. [45] | 2020 | Kabbage: A fresh approach to understanding fundamental auditing concepts and the effects of disruptive technology | Issues in Accounting Education | 10.2308/issues-16-076tn |

| Roszkowska, P. [46] | 2020 | Fintech in financial reporting and audit for fraud prevention and safeguarding equity investments | Journal of Accounting and Organizational Change | 10.1108/JAOC-09-2019-0098 |

| Sandner, P., Lange, A., Schulden, P. [47] | 2020 | The role of the CFO of an industrial company: An analysis of the impact of blockchain technology | Future Internet | 10.3390/fi12080128 |

| Zheng, Y., Boh, W.F. [48] | 2021 | Value drivers of blockchain technology: A case study of blockchain-enabled online community | Telematics and Informatics | 10.1016/j.tele.2021.101563 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Agrifoglio, R.; de Gennaro, D. New Ways of Working through Emerging Technologies: A Meta-Synthesis of the Adoption of Blockchain in the Accountancy Domain. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 836-850. https://0-doi-org.brum.beds.ac.uk/10.3390/jtaer17020043

Agrifoglio R, de Gennaro D. New Ways of Working through Emerging Technologies: A Meta-Synthesis of the Adoption of Blockchain in the Accountancy Domain. Journal of Theoretical and Applied Electronic Commerce Research. 2022; 17(2):836-850. https://0-doi-org.brum.beds.ac.uk/10.3390/jtaer17020043

Chicago/Turabian StyleAgrifoglio, Rocco, and Davide de Gennaro. 2022. "New Ways of Working through Emerging Technologies: A Meta-Synthesis of the Adoption of Blockchain in the Accountancy Domain" Journal of Theoretical and Applied Electronic Commerce Research 17, no. 2: 836-850. https://0-doi-org.brum.beds.ac.uk/10.3390/jtaer17020043