Estimating Distributions of Parameters in Nonlinear State Space Models with Replica Exchange Particle Marginal Metropolis–Hastings Method

Abstract

:1. Introduction

2. Methods

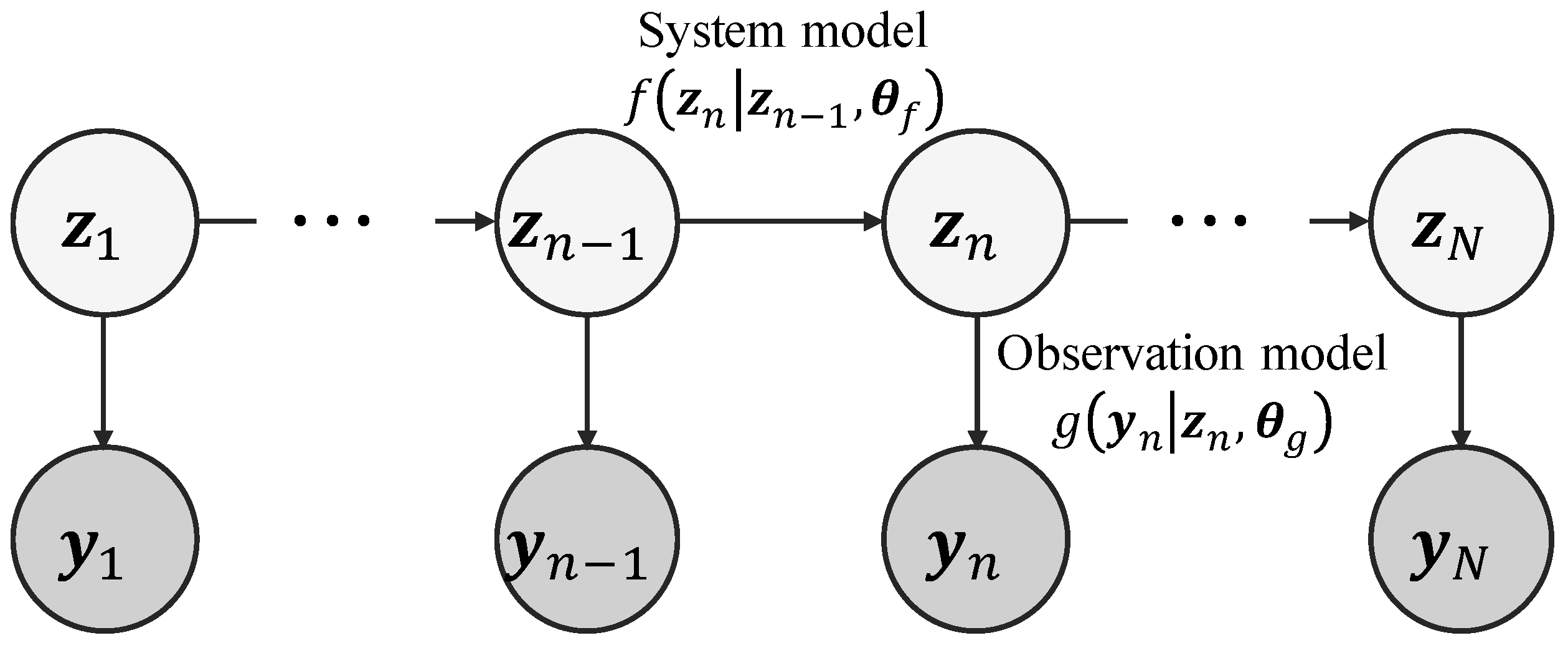

2.1. State Space Model

2.2. Particle Marginal Metropolis–Hastings Method

| Algorithm 1 Particle Marginal Metropolis–Hastings (PMMH) Method. |

|

2.3. Proposed Method

2.3.1. Brief Summary of Our Proposed Method

2.3.2. Introducing the Replica Exchange Method into the PMMH Method

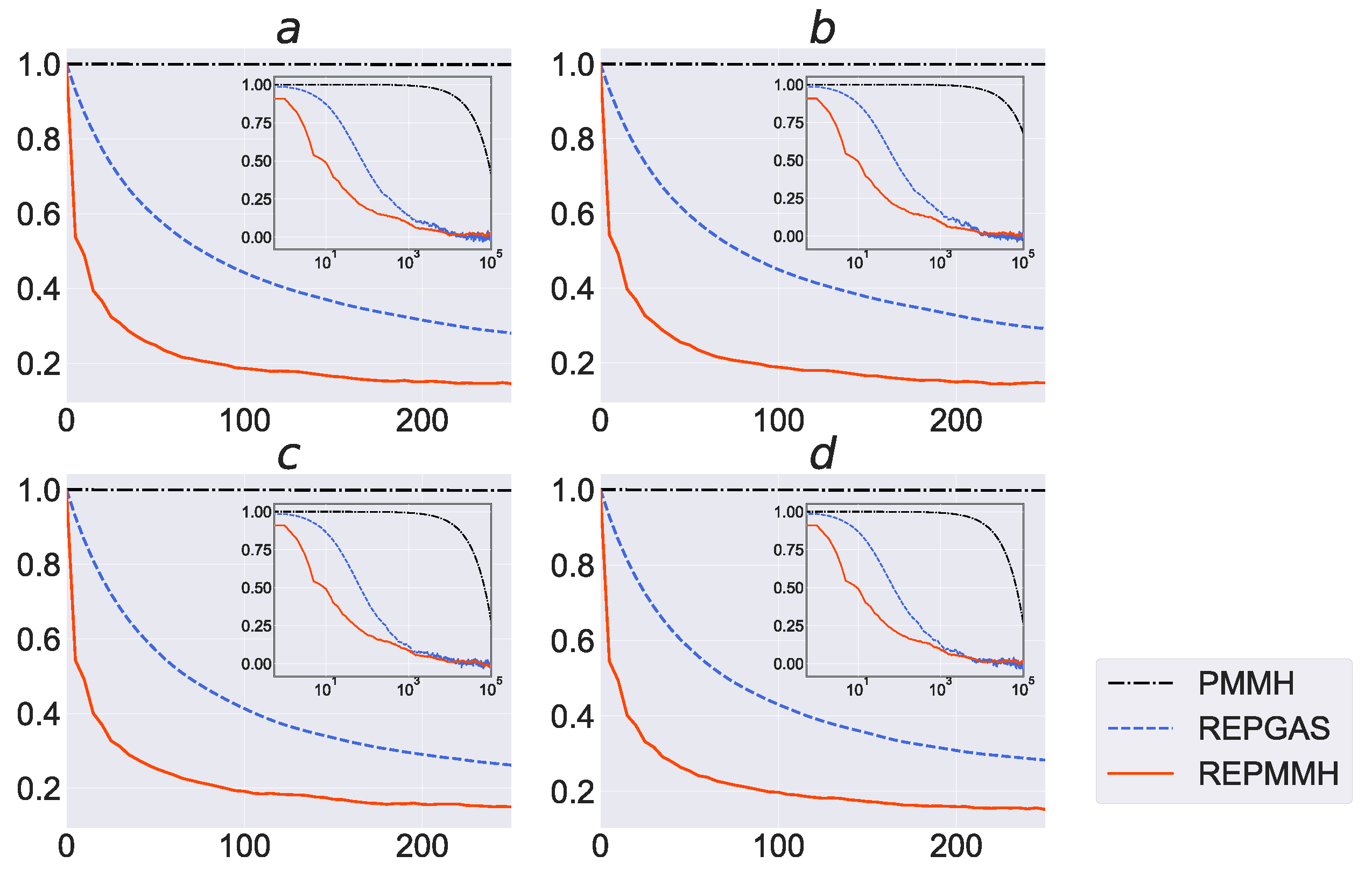

2.3.3. Relations among Particle Markov Chain Monte Carlo Methods

| Algorithm 2 Replica Exchange Particle Marginal Metropolis–Hastings (REPMMH) Method. |

|

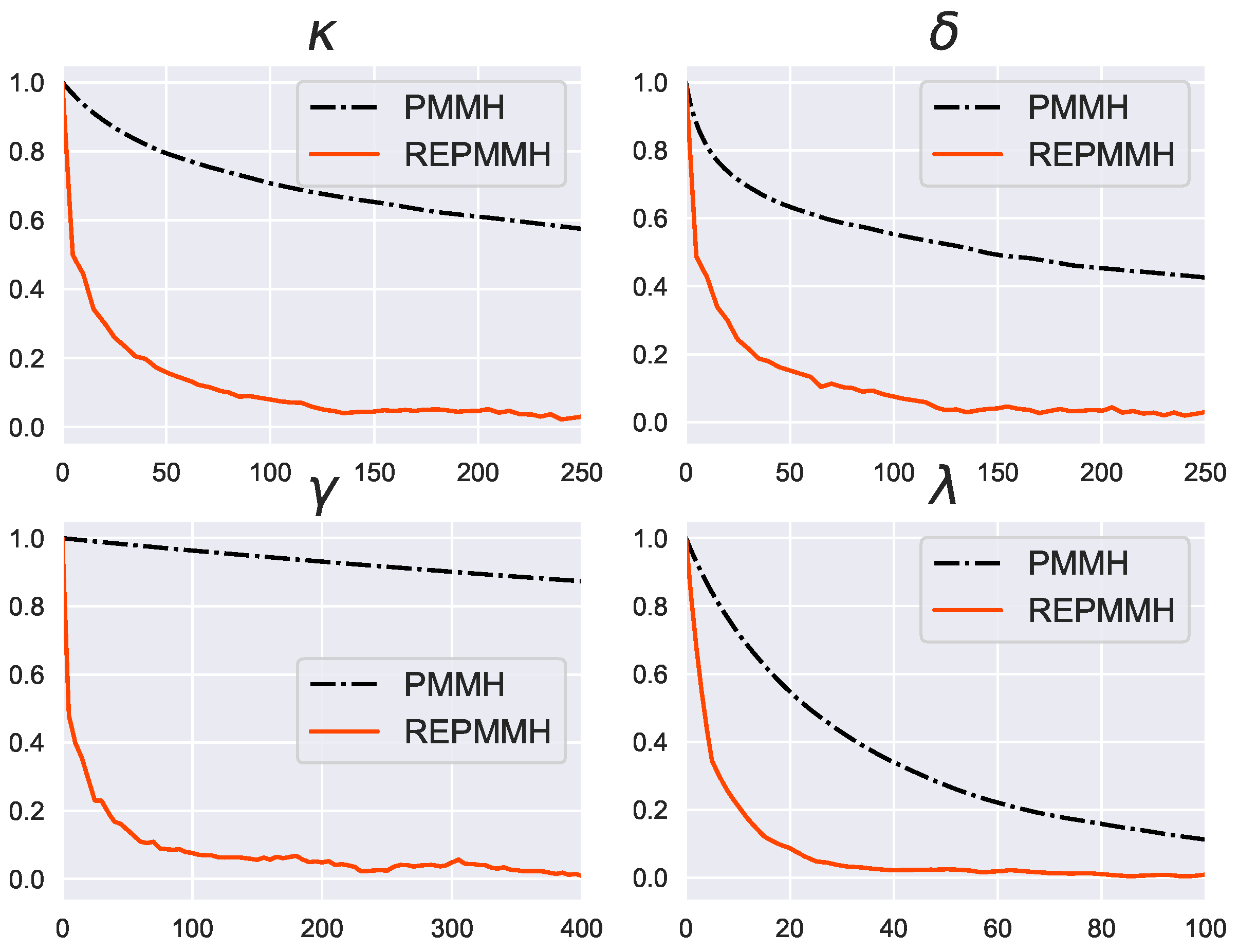

3. Results

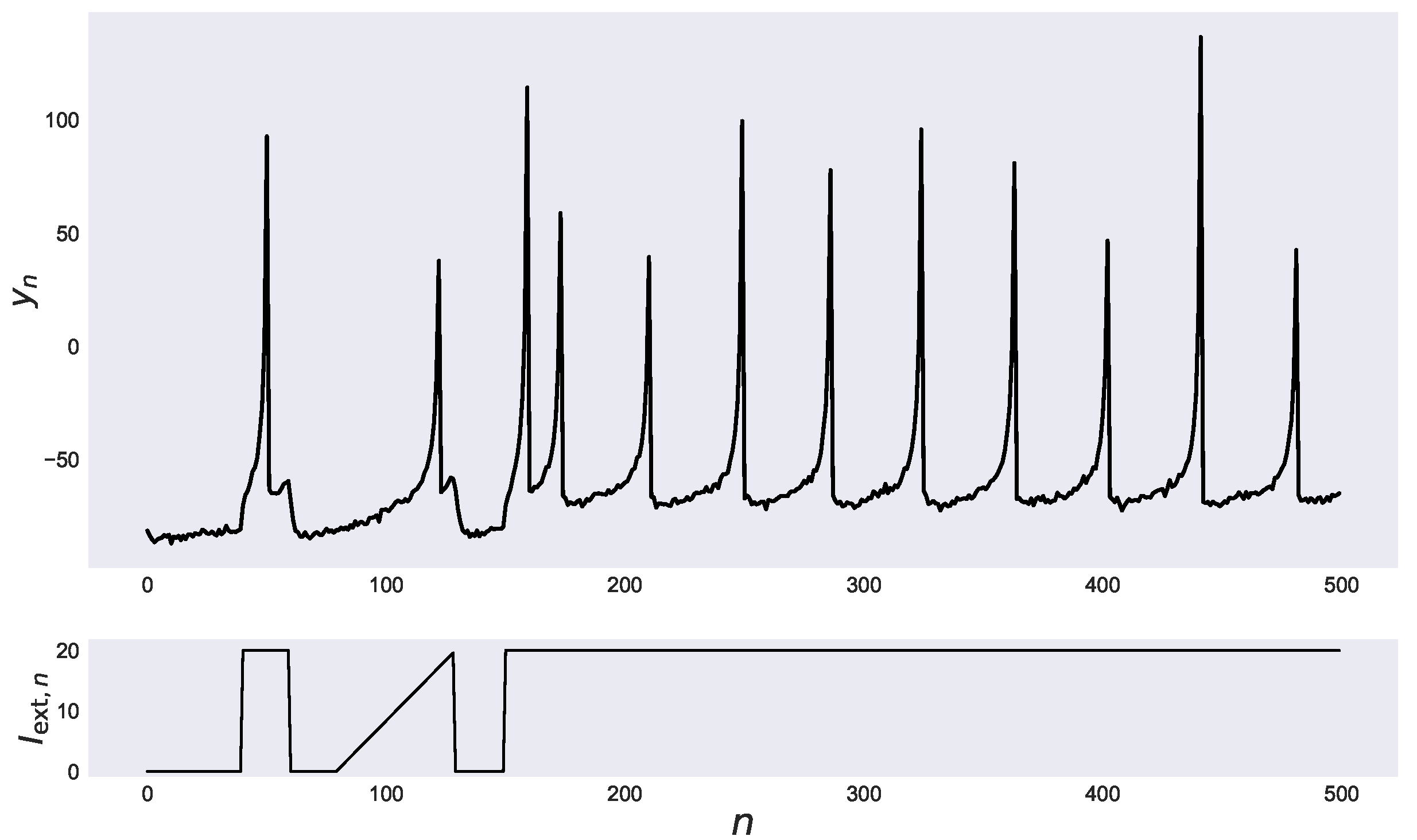

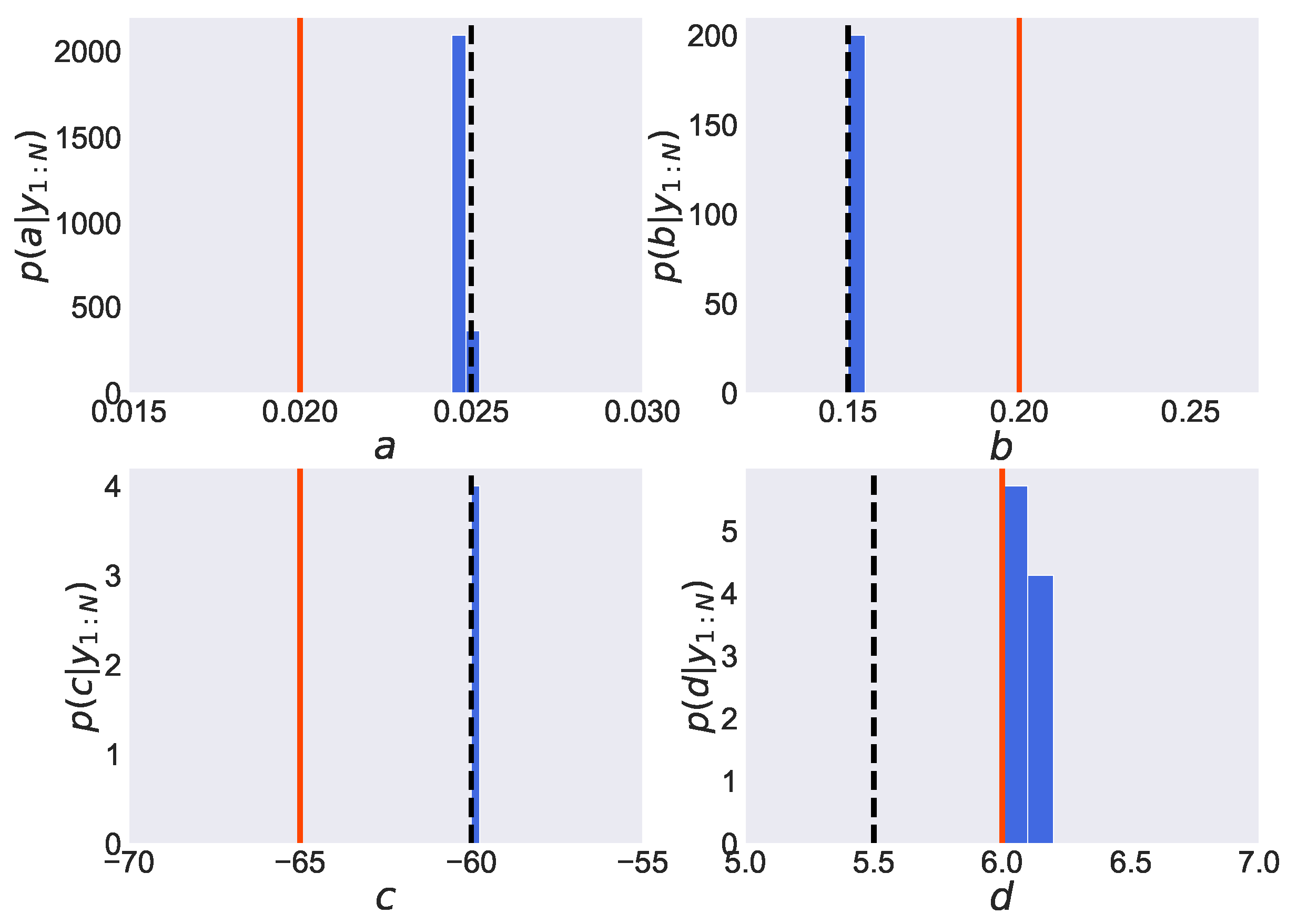

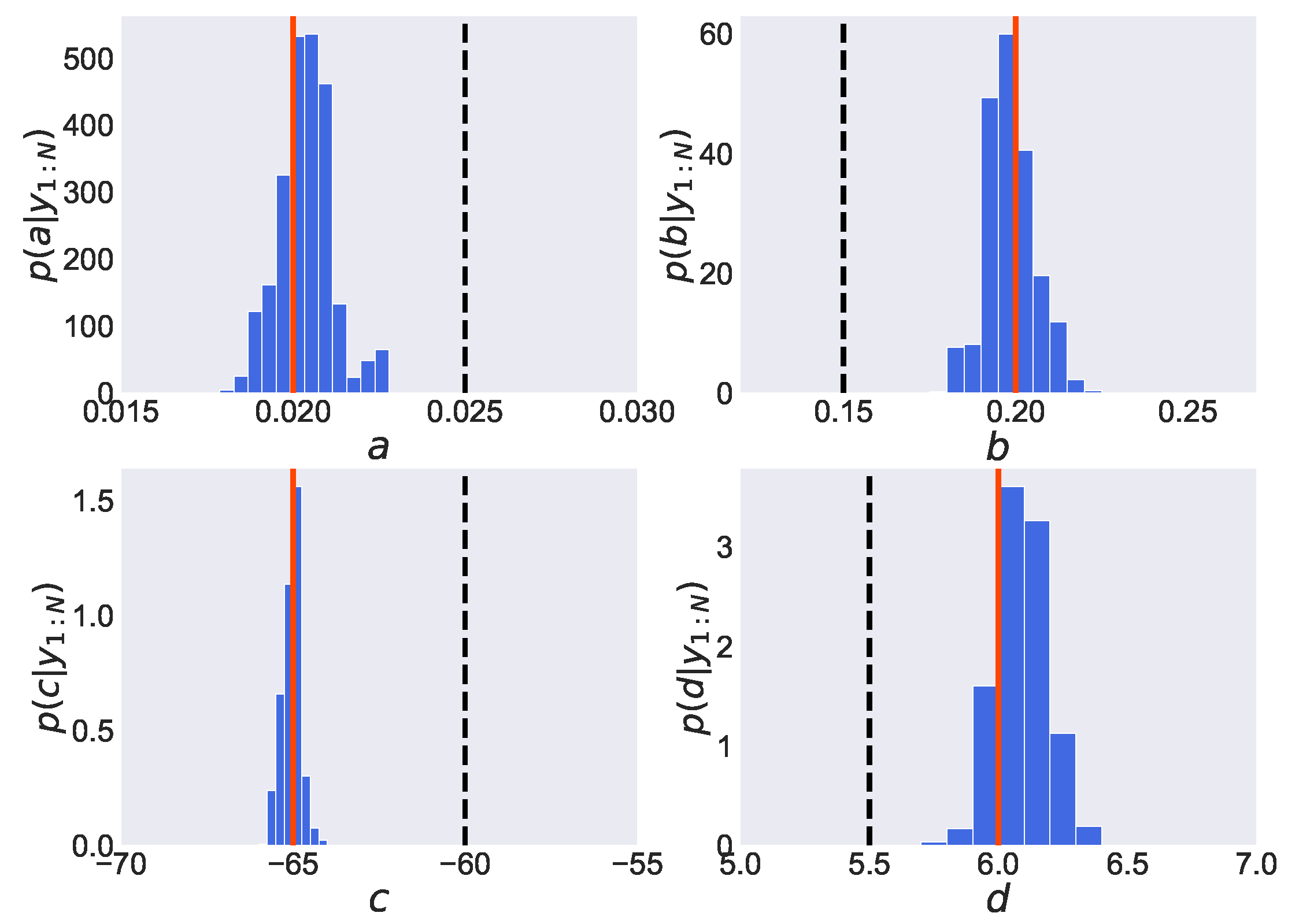

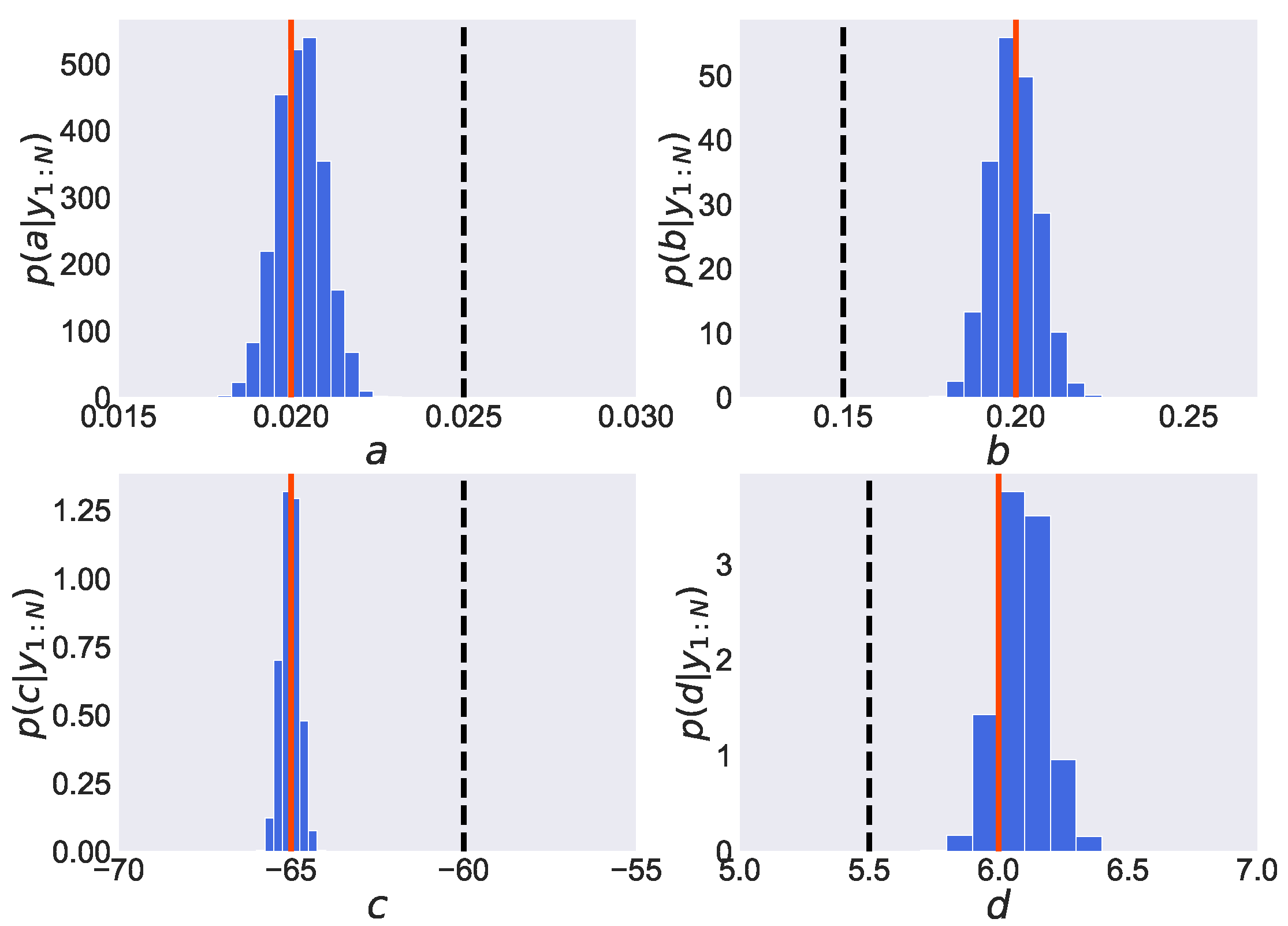

3.1. Izhikevich Neuron Model

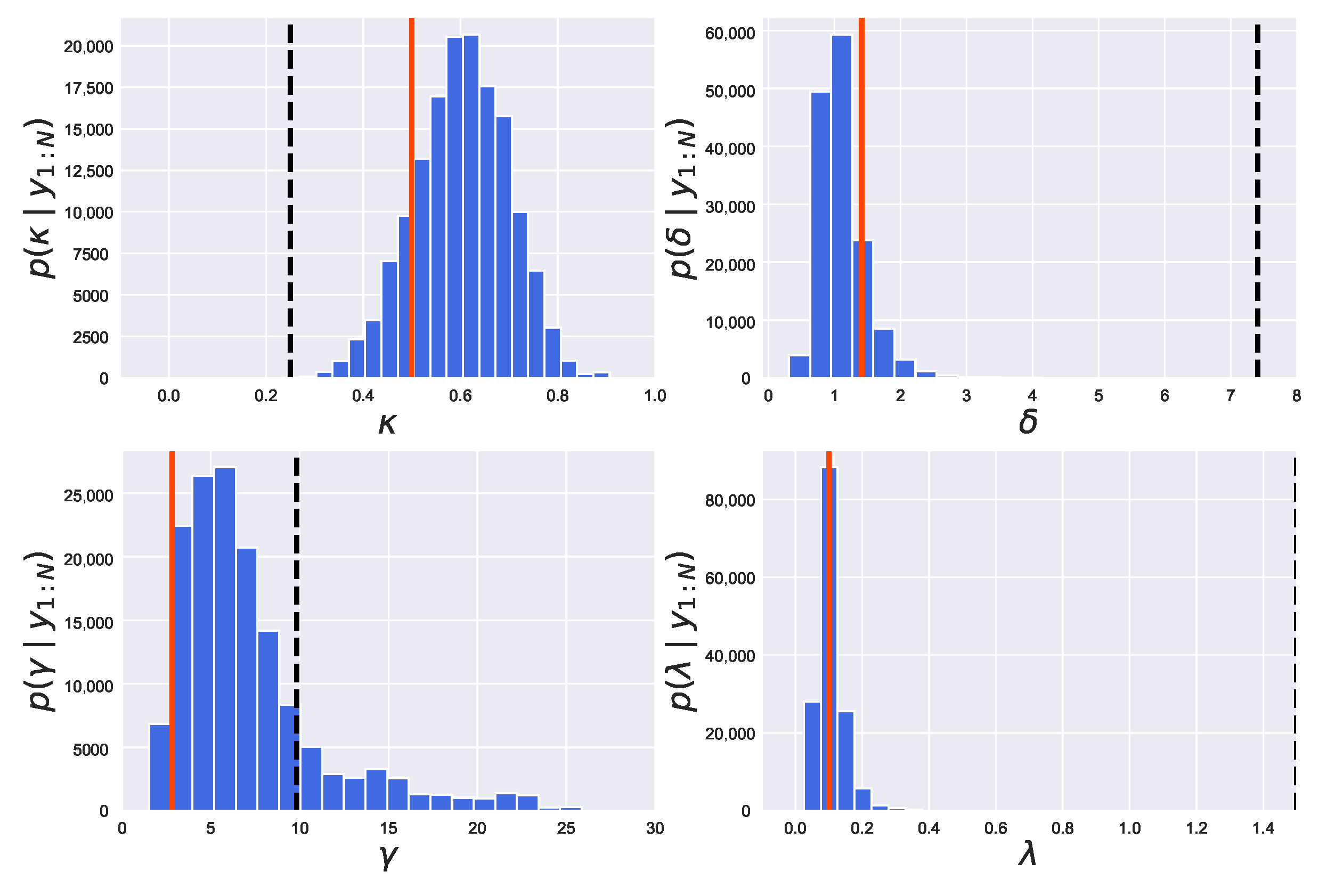

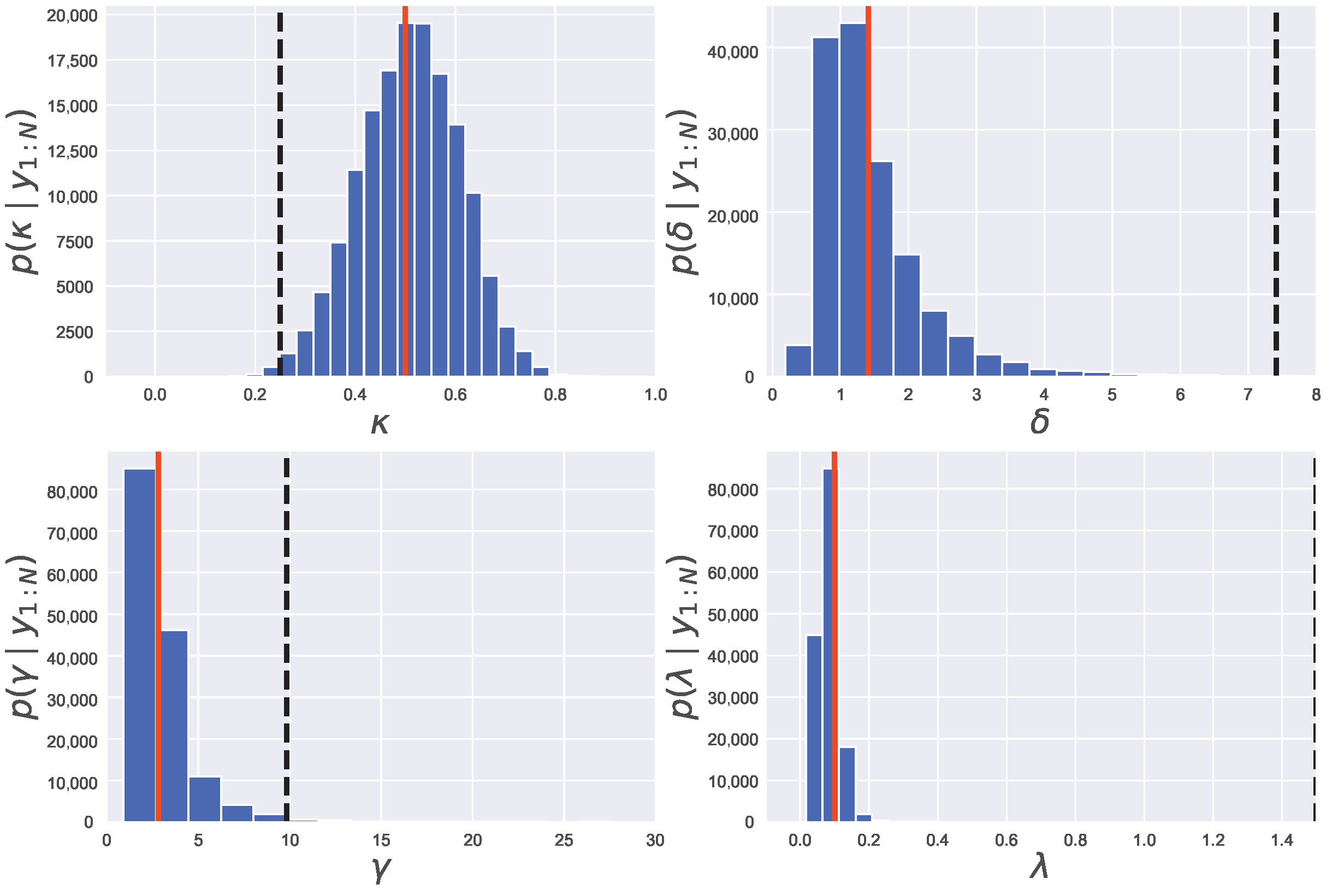

3.2. Lévy-Driven Stochastic Volatility Model

4. Concluding Remarks

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| PMMH | Particle Marginal Metropolis–Hastings |

| REPMMH | Replica Exchange Particle Marginal Metropolis–Hastings |

| SMC | Sequential Monte Carlo |

| EM | Expectation–Maximization |

| MCMC | Markov Chain Monte Carlo |

| PMCMC | Particle Markov Chain Monte Carlo |

| MH | Metropolis–Hastings |

| PG | Particle Gibbs |

| PGAS | Particle Gibbs with Ancestor Sampling |

| REPGAS | Replica Exchange Particle Gibbs with Ancestor Sampling |

References

- Netto, M.A.; Gimeno, L.; Mendes, M.J. A new spline algorithm for non-linear filtering of discrete time systems. IFAC Proc. Vol. 1978, 11, 2123–2130. [Google Scholar] [CrossRef]

- Doucet, A.; Godsill, S.; Andrieu, C. On sequential Monte Carlo sampling methods for Bayesian filtering. Stat. Comput. 2000, 10, 197–208. [Google Scholar] [CrossRef]

- Ghahramani, Z.; Hinton, G.E. The EM Algorithm for Mixtures of Factor Analyzers; Technical Report CRG-TR-96-1; Department of Computer Science, University of Toronto: Toronto, ON, USA, 1996. [Google Scholar]

- Kitagawa, G. A self-organizing state-space model. J. Am. Stat. Assoc. 1998, 93, 1203–1215. [Google Scholar] [CrossRef]

- Meyer, R.; Christensen, N. Fast Bayesian reconstruction of chaotic dynamical systems via extended Kalman filtering. Phys. Rev. E 2001, 65, 016206. [Google Scholar] [CrossRef] [Green Version]

- Doucet, A.; De Freitas, N.; Gordon, N. An introduction to sequential Monte Carlo methods. In Sequential Monte Carlo Methods in Practice; Doucet, A., De Freitas, N., Gordon, N., Eds.; Springer: New York, NY, USA, 2001; pp. 3–14. [Google Scholar]

- Hyndman, R.J.; Koehler, A.B.; Snyder, R.D.; Grose, S. A state space framework for automatic forecasting using exponential smoothing methods. Int. J. Forecast. 2002, 18, 439–454. [Google Scholar] [CrossRef] [Green Version]

- Bishop, C.M. Pattern Recognition and Machine Learning; Springer: New York, NY, USA, 2006. [Google Scholar]

- Vogelstein, J.T.; Watson, B.O.; Packer, A.M.; Yuste, R.; Jedynak, B.; Paninski, L. Spike inference from calcium imaging using sequential Monte Carlo methods. Biophys. J. 2009, 97, 636–655. [Google Scholar] [CrossRef] [Green Version]

- Vogelstein, J.T.; Packer, A.M.; Machado, T.A.; Sippy, T.; Babadi, B.; Yuste, R.; Paninski, L. Fast nonnegative deconvolution for spike train inference from population calcium imaging. J. Neurophysiol. 2010, 104, 3691–3704. [Google Scholar] [CrossRef] [Green Version]

- Tsunoda, T.; Omori, T.; Miyakawa, H.; Okada, M.; Aonishi, T. Estimation of intracellular calcium ion concentration by nonlinear state space modeling and expectation-maximization algorithm for parameter estimation. J. Phys. Soc. Jpn. 2010, 79, 124801. [Google Scholar] [CrossRef]

- Andrieu, C.; Doucet, A.; Holenstein, R. Particle Markov chain Monte Carlo methods. J. R. Stat. Soc. B 2010, 72, 269–342. [Google Scholar] [CrossRef] [Green Version]

- Meng, L.; Kramer, M.A.; Eden, U.T. A sequential Monte Carlo approach to estimate biophysical neural models from spikes. J. Neural Eng. 2011, 8, 065006. [Google Scholar] [CrossRef]

- Paninski, L.; Vidne, M.; DePasquale, B.; Ferreira, D.G. Inferring synaptic inputs given a noisy voltage trace via sequential Monte Carlo methods. J. Comput. Neurosci. 2012, 33, 1–19. [Google Scholar] [CrossRef]

- Snyder, R.D.; Ord, J.K.; Koehler, A.B.; McLaren, K.R.; Beaumont, A.N. Forecasting compositional time series: A state space approach. Int. J. Forecast. 2017, 33, 502–512. [Google Scholar] [CrossRef] [Green Version]

- Lindsten, F.; Schön, T.B.; Jordan., M.I. Ancestor sampling for particle Gibbs. In Proceedings of the Advances in Neural Information Processing Systems, Stateline, NV, USA, 3–8 December 2012; pp. 2600–2608. [Google Scholar]

- Henriksen, S.; Wills, A.; Schön, T.B.; Ninness, B. Parallel implementation of particle MCMC methods on a GPU. IFAC Proc. Vol. 2012, 45, 1143–1148. [Google Scholar] [CrossRef] [Green Version]

- Frigola, R.; Lindsten, F.; Schön, T.B.; Rasmussen, C.E. Bayesian inference and learning in Gaussian process state-space models with particle MCMC. In Proceedings of the Advances in Neural Information Processing Systems, Stateline, NV, USA, 5–10 December 2013; pp. 3181–3189. [Google Scholar]

- Lindsten, F.; Jordan, M.I.; Schön, T.B. Particle Gibbs with ancestor sampling. J. Mach. Learn. Res. 2014, 15, 2145–2184. [Google Scholar]

- Omori, T.; Kuwatani, T.; Okamoto, A.; Hukushima, K. Bayesian inversion analysis of nonlinear dynamics in surface heterogeneous reactions. Phys. Rev. E 2016, 94, 033305. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Omori, T.; Sekiguchi, T.; Okada, M. Belief propagation for probabilistic slow feature analysis. J. Phys. Soc. Jpn. 2017, 86, 084802. [Google Scholar] [CrossRef]

- Rangapuram, S.S.; Seeger, M.W.; Gasthaus, J.; Stella, L.; Wang, Y.; Januschowski, T. Deep state space models for time series forecasting. In Proceedings of the Advances in Neural Information Processing Systems, Montreal, QC, Canada, 2–8 December 2018; pp. 7785–7794. [Google Scholar]

- Wang, P.; Yang, M.; Peng, Y.; Zhu, J.; Ju, R.; Yin, Q. Sensor control in anti-submarine warfare—A digital twin and random finite sets based approach. Entropy 2019, 21, 767. [Google Scholar] [CrossRef] [Green Version]

- Inoue, H.; Hukushima, K.; Omori, T. Replica exchange particle-Gibbs method with ancestor sampling. J. Phys. Soc. Jpn. 2020, 89, 104801. [Google Scholar] [CrossRef]

- Shapovalova, Y. “Exact” and approximate methods for Bayesian inference: Stochastic volatility case study. Entropy 2021, 23, 466. [Google Scholar] [CrossRef]

- Gregory, P. Bayesian Logical Data Analysis for the Physical Sciences; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

- Andrieu, C.; Doucet, A.; Punskaya, E. Sequential Monte Carlo methods for optimal filtering. In Sequential Monte Carlo Methods in Practice; Doucet, A., De Freitas, N., Gordon, N., Eds.; Springer: New York, NY, USA, 2001; pp. 79–95. [Google Scholar]

- Wu, C.J. On the convergence properties of the EM algorithm. Annal. Stat. 1983, 11, 95–103. [Google Scholar] [CrossRef]

- McLachlan, G.J.; Krishnan, T. The EM Algorithm and Extensions; Wiley: Hoboken, NY, USA, 1996. [Google Scholar]

- Geman, S.; Geman, D. Stochastic relaxation, Gibbs distributions, and the Bayesian restoration of images. IEEE Trans. Pattern Anal. Mach. Intell. 1984, 6, 721–741. [Google Scholar] [CrossRef]

- Metropolis, N.; Rosenbluth, A.W.; Rosenbluth, M.N.; Teller, A.H.; Teller, E. Equation of state calculations by fast computing machines. J. Chem. Phys. 1953, 21, 1087–1092. [Google Scholar] [CrossRef] [Green Version]

- Hastings, W.K. Monte Carlo sampling methods using Markov chains and their applications. Biometrika 1970, 57, 97–109. [Google Scholar] [CrossRef]

- Cunningham, N.; Griffin, J.E.; Wild, D.L. ParticleMDI: Particle Monte Carlo methods for the cluster analysis of multiple datasets with applications to cancer subtype identification. Adv. Data Anal. Classif. 2020, 14, 463–484. [Google Scholar] [CrossRef]

- Wang, S.; Wang, L. Particle Gibbs sampling for Bayesian phylogenetic inference. Bioinformatics 2021, 37, 642–649. [Google Scholar] [CrossRef]

- Jasra, A.; Persing, A.; Beskos, A.; Heine, K.; De Iorio, M. Bayesian inference for duplication–mutation with complementarity network models. J. Comput. Biol. 2015, 22, 1025–1033. [Google Scholar] [CrossRef] [PubMed]

- Du, D.; Hu, Z.; Du, Y. Model Identification and Physical Exercise Control using Nonlinear Heart Rate Model and Particle Filter. In Proceedings of the 2019 IEEE 15th International Conference on Automation Science and Engineering, Vancouver, BC, Canada, 22–26 August 2019; pp. 405–410. [Google Scholar]

- Osmundsen, K.K.; Kleppe, T.S.; Liesenfeld, R.; Oglend, A. Estimating the Competitive Storage Model with Stochastic Trends in Commodity Prices. Econometrics 2021, 9, 40. [Google Scholar] [CrossRef]

- Hukushima, K.; Nemoto, K. Exchange Monte Carlo method and application to spin glass simulations. J. Phys. Soc. Jpn. 1996, 65, 1604–1608. [Google Scholar] [CrossRef] [Green Version]

- Urano, R.; Okamoto, Y. Designed-walk replica-exchange method for simulations of complex systems. Comput. Phys. Commun. 2015, 196, 380–383. [Google Scholar] [CrossRef] [Green Version]

- Motonaka, K.; Miyoshi, S. Connecting PM and MAP in Bayesian spectral deconvolution by extending exchange Monte Carlo method and using multiple data sets. Neural Netw. 2019, 118, 159–166. [Google Scholar] [CrossRef]

- Izhikevich, E.M. Simple model of spiking neurons. IEEE Trans. Neural Netw. 2003, 14, 1569–1572. [Google Scholar] [CrossRef] [Green Version]

- Izhikevich, E.M. Which model to use for cortical spiking neurons? IEEE Trans. Neural Netw. 2004, 15, 1063–1070. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, O.E.; Shephard, N. Non-Gaussian Ornstein–Uhlenbeck-based models and some of their uses in financial economics. J. R. Stat. Soc. B 2001, 63, 167–241. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, O.E.; Shephard, N. Normal modified stable processes. Theor. Probab. Math. Stat. 2001, 65, 1–19. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Method | Target Distribution | Overview |

|---|---|---|

| PG | Sample parameters and latent variables alternately with Gibbs sampling for targeting the joint posterior distribution Note that the SMC method is used for sampling latent variables . The SMC method used in the PG method is called the conditional SMC method and uses the previous sample of latent variables as a particle in the SMC method [12]. | |

| PGAS | Sample latent variables not only in the forward direction but also in the backward direction in the PG method [16,18,19]. | |

| REPGAS | Improve the problem of initial value dependence in the PGAS method by combining the replica exchange method and the PGAS method [24]. | |

| PMMH | Sample parameters with the MH algorithm for targeting directly the marginal posterior distribution marginalization over the distribution of latent variables . Note that the SMC method is used to calculate the marginal likelihood [12]. | |

| REPMMH | Improve the problem of initial value dependence in the PMMH method by combining the replica exchange method and the PMMH method. |

| Parameter | |||||

|---|---|---|---|---|---|

| Mode | |||||

| Std | |||||

| ACF | |||||

| Mode | |||||

| Std | |||||

| ACF | |||||

| Mode | |||||

| Std | |||||

| ACF | |||||

| Mode | |||||

| Std | |||||

| ACF |

| Parameter | ||||||

|---|---|---|---|---|---|---|

| Mode | ||||||

| Std | ||||||

| ACF | ||||||

| Mode | ||||||

| Std | ||||||

| ACF | ||||||

| Mode | ||||||

| Std | ||||||

| ACF | ||||||

| Mode | ||||||

| Std | ||||||

| ACF |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Inoue, H.; Hukushima, K.; Omori, T. Estimating Distributions of Parameters in Nonlinear State Space Models with Replica Exchange Particle Marginal Metropolis–Hastings Method. Entropy 2022, 24, 115. https://0-doi-org.brum.beds.ac.uk/10.3390/e24010115

Inoue H, Hukushima K, Omori T. Estimating Distributions of Parameters in Nonlinear State Space Models with Replica Exchange Particle Marginal Metropolis–Hastings Method. Entropy. 2022; 24(1):115. https://0-doi-org.brum.beds.ac.uk/10.3390/e24010115

Chicago/Turabian StyleInoue, Hiroaki, Koji Hukushima, and Toshiaki Omori. 2022. "Estimating Distributions of Parameters in Nonlinear State Space Models with Replica Exchange Particle Marginal Metropolis–Hastings Method" Entropy 24, no. 1: 115. https://0-doi-org.brum.beds.ac.uk/10.3390/e24010115