Small Water Enterprise in Rural Rwanda: Business Development and Year-One Performance Evaluation of Nine Water Kiosks at Health Care Facilities

,

,

Abstract

:1. Introduction

2. Materials and Methods

2.1. Market Analysis and Demand Estimation

2.2. Production Cost Estimation and Implementation

2.3. Monitoring of Kiosk Operation, Consumer Demand, and Evaluation of Financial Performance

2.4. Ethical Approval

3. Results

3.1. Market Analysis and Demand Estimation

3.1.1. Market Analysis

3.1.2. Demand Estimation

3.2. Cost Model and Implementation

3.3. Kiosk Operation and Financial Performance

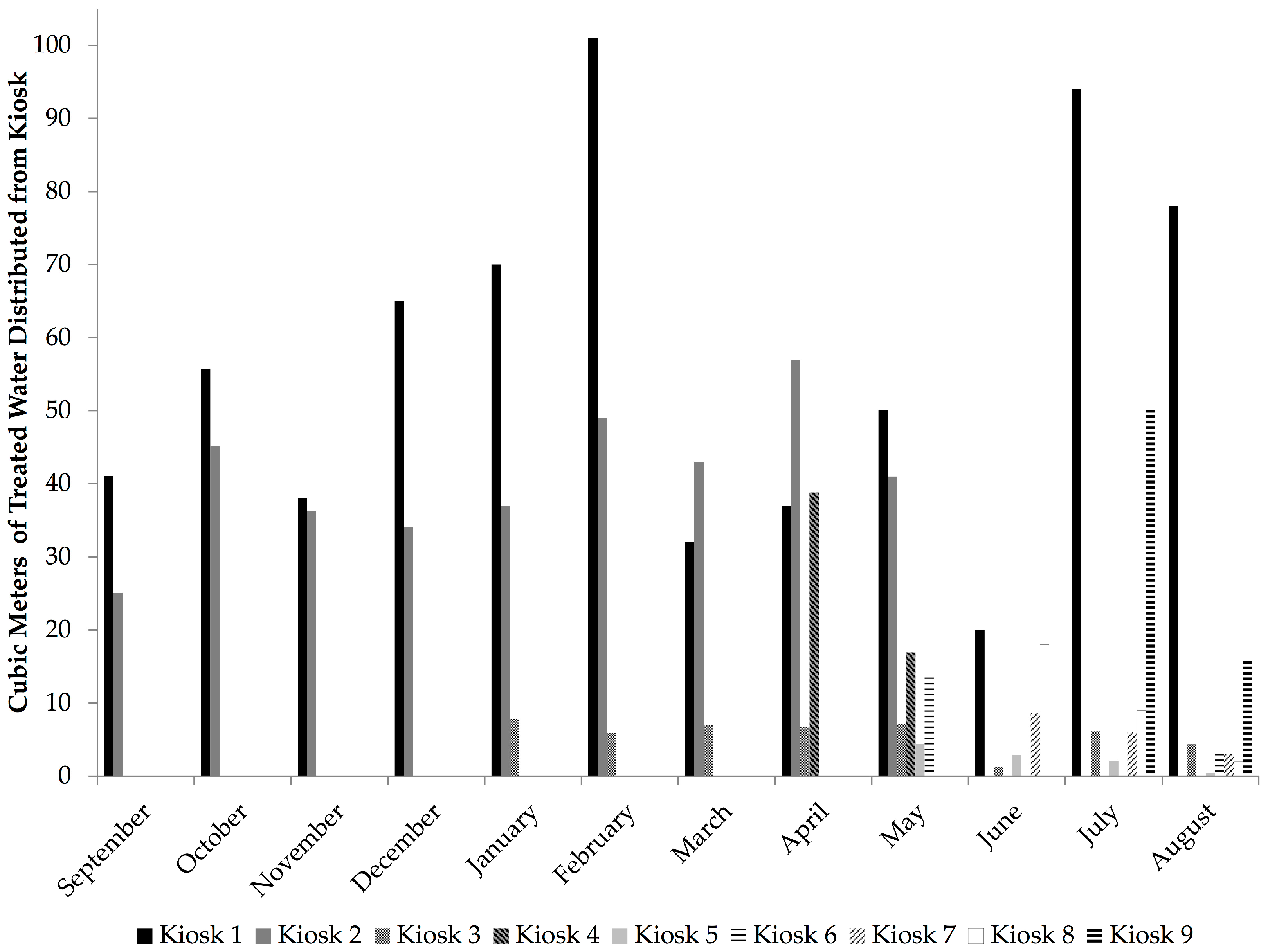

3.3.1. Kiosk Operation

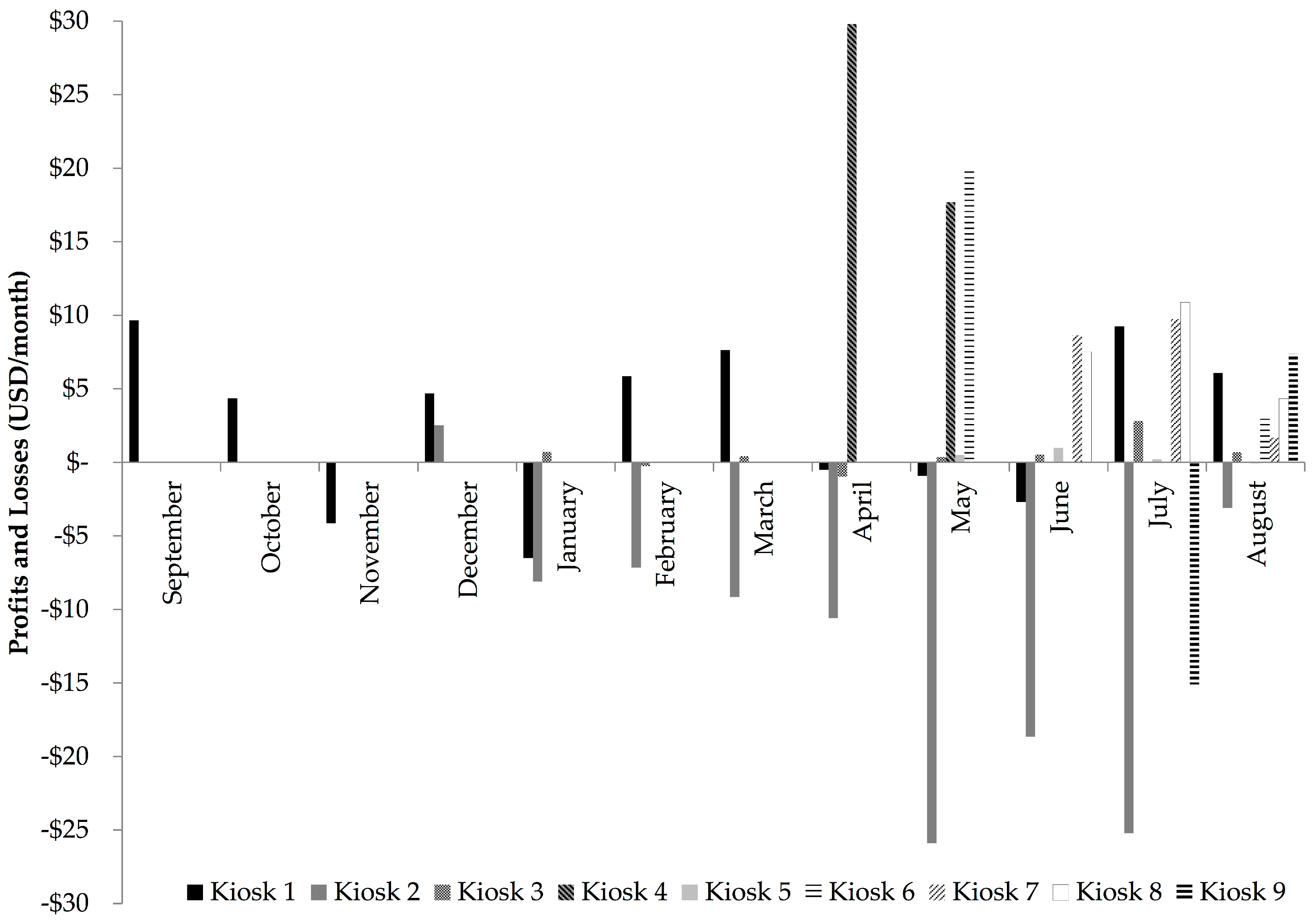

3.3.2. Consumer Demand and Financial Performance

3.3.3. Measures of Correlation

4. Discussion

5. Conclusions

Supplementary Materials

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Opryszko, M.C.; Huang, H.; Soderlund, K.; Schwab, K.J. Data Gaps in Evidence-based Research on Small Water Enterprises in Developing Countries. J. Water Health 2009, 7, 609–622. [Google Scholar] [CrossRef] [PubMed]

- Opryszko, M.C.; MacDonald, L.; Schwab, K.J.; Kiihl, S.; Guo, Y.; MacDonald, L. Impact of Water-Vending Kiosks and Hygiene Education on Household Drinking Water Quality in Rural Ghana. Am. J. Trop. Med. Hyg. 2013, 88, 651–660. [Google Scholar] [CrossRef] [PubMed]

- Kariuki, M.; Schwartz, J. Small-Scale Private Service Providers of Water Supply and Electricity: A Review of Incidence, Structure, Pricing and Operating Characteristics. Policy Research Working Paper No. 3727; World Bank: Washington, DC, USA, 2005. [Google Scholar]

- Nijru, C. WELL Factsheet: How Small Water Enterprises Can Contribute to MDGs for Water; Water Engineering and Development Centre (WEDC), Loughborough University: Leicestershire, UK, 2005. [Google Scholar]

- McGranahan, G.; Mitlin, D.; Albu, M.; Smith, M.; Njiru, C. How Small Water Enterprises Can Contribute to the Millennium Development Goals: Evidence from Dar es Salaam, Nairobi, Khartoum and Accra; Water Engineering and Development Centre (WEDC), Loughborough University: Leicestershire, UK, 2006. [Google Scholar]

- Brown, J.; Clasen, T.; Outlaw, T.; Sobsey, M.D.; Wu, J. Safe Water for All: Harnessing the Private Sector to Reach the Underserved; World Bank: Washington, DC, USA, 2011. [Google Scholar]

- Foster, T. Private Sector Provision of Rural Water Services: A Desk Study for Water for People; Water for People: Denver, CO, USA, 2012. [Google Scholar]

- Sima, L.C.; Elimelech, M. More than a Drop in the Bucket: Decentralized Membrane-based Drinking Water Refill Stations in Southeast Asia. Environ. Sci. Technol. 2013, 47, 7580–7588. [Google Scholar] [CrossRef] [PubMed]

- Bhatt, J. Comparison of Small-scale Providers and Utility Performance in Urban Water Supply: The Case of Maputo, Mozambique. Water Policy 2014, 16, 102–123. [Google Scholar] [CrossRef]

- Jeuland, M.; McClatchey, M.; Patil, S.; Poulos, C.; Pattanayak, S.K.; Yang, J.-C. Do Decentralized Community Treatment Plants Provide Better Water? Evidence from Andhra Pradesh; Nicholas Institute for Environmental Policy Solutions and Duke University Energy Initiative, Duke University: Durham, NC, USA, 2015. [Google Scholar]

- Collignon, B.; Vezina, M. Independent Water and Sanitation Providers in African Cities: Full Report of a Ten-Country Study; World Bank Water and Sanitation Program (WSP): Washington, DC, USA, 2000. [Google Scholar]

- Lang, B.; Khush, R. Water Business Kit—Kenya—A Guide to Starting Your Own Water Treatment and Vending Business; International Finance Corporation: Nairobi, Kenya, 2012. [Google Scholar]

- Decentralized Safe Water Kiosks: Working toward a Sustainable Model in Ghana; Safe Water Network: New York, NY, USA, 2012.

- Ampadu-Boakye, J.; Hebert, R.; Crooks, H.; Awais, M. Remote Kiosks: A Cost-Effective Approach to Increasing Safe Water Consumption in Ghana; Safe Water Network: New York, NY, USA, 2014. [Google Scholar]

- Cherunya, P.C.; Janezic, C.; Leuchner, M. Sustainable Supply of Safe Drinking Water for Underserved Households in Kenya: Investigating the Viability of Decentralized Solutions. Water 2015, 7, 5437–5457. [Google Scholar] [CrossRef]

- Nzengya, D.M. Exploring the Challenges and Opportunities for Master Operators and Water Kiosks under Delegated Management Model (DMM): A Study in Lake Victoria Region, Kenya. Cities 2015, 46, 35–43. [Google Scholar] [CrossRef]

- Wutich, A.; Beresford, M.; Carvajal, C. Can Informal Water Vendors Deliver on the Promise of a Human Right to Water? Results From Cochabamba, Bolivia. World Dev. 2016, 79, 14–24. [Google Scholar] [CrossRef]

- Solo, T.M. Small-scale Entrepreneurs in the Urban Water and Sanitation Market. Environ. Urban. 1999, 11, 117–132. [Google Scholar] [CrossRef]

- London, T.; Anupindi, R.; Sheth, S. Creating Mutual Value: Lessons Learned from Ventures Serving Base of the Pyramid Producers. J. Bus. Res. 2010, 63, 582–594. [Google Scholar] [CrossRef]

- Bauer, S. Guidelines for User Fees and Cost Recovery for Rural, Non-Networked, Water and Sanitation Delivery; African Development Bank: Abijan, Côte d’Ivoire, 2010. [Google Scholar]

- Brockelhurst, C.; Harvey, P.; Danert, K.; Baumann, E.; Casey, V.; Gichuru, W.; Aleobua, B.; Sutton, S. Myths of the Rural Water Supply Sector. RWSN Perspectives No. 4; Rural Water Supply Network (RWSN): St. Gallen, Switzerland, 2010. [Google Scholar]

- Community Safe Water Solutions: India Sector Review; Safe Water Network: New York, NY, USA, 2014; p. 68.

- Joint Monitoring Program (WHO and UNICEF). Progress on Sanitation and Drinking Water—2015 Update and MDG Assessment; WHO Press: Geneva, Switzerland, 2015. [Google Scholar]

- Klawitter, S.; Lorek, S.; Schaefer, D.; Lammerding, A. Case Study: Water Kiosks. How the Combination of Low-Cost Technology, Pro-Poor Financing and Regulation Leads to the Scaling Up of Water Supply Service Provision to the Poor; Deutsche Gesellschaft fuür Internationale Zusammenarbeit (GIZ): Eschborn, Germany, 2009. [Google Scholar]

- Opere, M.; Lerise, F.; Gronemeier, K. Kiosk Service Options for Water Utilities in Tanzania. Experiences; Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ): Eschborn, Germany, 2013. [Google Scholar]

- Brirner, S.; van Zadelhoff, R.; Mohrmann, B. Bringing Water to Where It Is Needed Most: Innovative Private Sector Participation in Water & Sanitation; World Bank: Washington, DC, USA, 2011. [Google Scholar]

- The Market for Water Treatment and Vending Enterprises in Kenya, Sanitation and Safe Water for All Program Marketing Brief Issue No. 2; International Finance Corportation and Aquaya: Nairobi, Kenya, 2011.

- The Decentralized Water Market, Assessing and Overcoming the Hurdles to Scale in Kenya, Sanitation and Safe Water for All Program: Marketing Brief Issue No. 3; International Finance Corportation and Safe Water Network: Nairobi, Kenya, 2013.

- Oyo, A. Spare Part Supplies for Handpumps in Africa: Success Factors for Sutainability, in Rural Water Supply Field Notes; Stanford, M., Ed.; The World Bank; Water and Sanitation Program (WSP) and Rural Water Supply Network (RWSN): St. Gallen, Switzerland, 2006. [Google Scholar]

- Meierhofer, R.; Fluckiger, A.C.; Gebauer, H. Do Sales Models Influence the Purchase and Use of Ceramic Filters in Rural Areas of Kenya and Bolivia? J. Water Supply Res. Technol. AQUA 2016, 65, 87–102. [Google Scholar] [CrossRef]

- Huttinger, A.; Dreibelbis, R.; Roha, K.; Ngabo, F.; Kayigamba, F.; Mfura, L.; Moe, C. Evaluation of Membrane Ultrafiltration and Residual Chlorination as a Decentralized Water Treatment Strategy for Ten Rural Healthcare Facilities in Rwanda. Int. J. Environ. Res. Public Health 2015, 12, 13602–13623. [Google Scholar] [CrossRef] [PubMed]

- World Currency Exchange Rates and Currency Exchange Rate History, US Dollars (USD) to Rwanda Francs (RWF) Exchange Rate for 31 December 2014. Available online: https://www.exchange-rates.org/Rate/USD/RWF/12-31-2014 (accessed on 13 November 2017).

- Economic Development and Poverty Reduction Strategy; Government of the Republic of Rwanda: Kigali, Rwanda, 2007.

- Rwanda Interim Demographic and Health Survey 2007–2008; National Institute of Statistics of Rwanda: Kigali, Rwanda, 2009.

- Rwanda Water and Sanitation Profile; USAID Advancing the Blue Revolution Initiative (ABRI): Washington, DC, USA, 2010.

- Dusabe, G.; Raobelison, A.; Nzabonimpa, J.P.; Wilson, M. Scaling Up Point-of-Use Water Treatment through Multiple Channels in Rwanda, Country Brief; Population Services International: Bethesda, MD, USA, 2010. [Google Scholar]

- National Policy and Strategy for Water Supply and Sanitation Services; Ministry of Infrastructure, Government of the Republic of Rwanda: Kigali, Rwanda, 2010.

- Integrated Household Living Conditions Survey (EICV3 2010/11) District Profile East-Bugesera; National Institute of Statistics of Rwanda, Government of the Republic of Rwanda: Kigali, Rwanda, 2011; p. 92.

- WASH Survey for Households, Schools and Health Centres in the Districts of Burera, Musanze, Nyabihu & Rubavu Final Results; Republic of Rwanda Ministry of Health, Environmental Health Desk and UNICEF Rwanda: Kigali, Rwanda, 2011.

- Integrated Household Living Conditions Survey (EICV3 2010/11) District Profile North-Musanze; National Institute of Statistics of Rwanda: Kigali, Rwanda, 2011; p. 104.

- Population and Housing Census, Provisional Results; National Institute of Statistics of Rwanda: Kigali, Rwanda, 2012.

- Alcorn, T.E.; Opryszko, M.C.; Schwab, K.J. Formative Ethnographic Research to Improve Evaluation of a Novel Water System in Ghana. Am. J. Trop. Med. Hyg. 2011, 84, 801–805. [Google Scholar] [CrossRef] [PubMed]

- Ampadu-Boakye, J.; Yeboah, C.; Tetteh-Zomayi, F.; Gimble, A.; Crooks, H.; Stea, B.; Hebert, R. Ghana Market Assessment: Market-Based Provision of Water at the Community Level, Executive Summary; Safe Water Network: New York, NY, USA, 2016. [Google Scholar]

- Chawla, G.; Sewak, R.; Handa, I.; Gupta, J.C.C.S.; Arora, S. Financial Drivers of Reverse Osmosis (RO) Water Systems in Rural India; Safe Water Network: New York, NY, USA, 2015. [Google Scholar]

- Herbert, R. Improving Financial Viability through Cost-Effective Delivery Services; Safe Water Network: New York, NY, USA, 2013. [Google Scholar]

- National Water Tariffs Energy Water Sanitation and Energy Corporation of Rwanda (WASAC). 2014. Available online: http://www.wasac.rw/index.php/customer-information/tariffs-charges (accessed on 2 April 2014).

- Huttinger, A.; Emory University, Atlanta, GA, USA; Communications Office of Water Sanitation and Energy Corportation (WASAC) Kigali, Rwanda. Personal communication, 2013.

{kind=link}

{kind=link}

| Characteristic | Mean | Range | rs † | p Value |

|---|---|---|---|---|

| Observed demand for water per kiosk per month (m3) | 21 | (2–57) | (Ref.) | |

| Size of population within 1 km of kiosk | 1967 | (609–4045) | 0.41 | 0.24 |

| National utility water sources within 2 km of kiosk | 9 | (2–23) | 0.81 | 0.02 |

| National utility water sources within 500 m of kiosk | 3 | (0–5) | 0.27 | 0.48 |

| Increase in price of water from national utility sources to kiosk (%) 1 | 83 | (−38–214) | −0.65 | 0.08 |

| Estimated demand for water per kiosk per month (m3) | 116 | (57–205) | - | |

| Estimated demand met per month (% observed/estimated) | 20 | (3–49) | - |

| Kiosk | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | Mean |

|---|---|---|---|---|---|---|---|---|---|---|

| Months of observation | 12 | 9 | 8 | 5 | 4 | 4 | 3 | 3 | 2 | 5.5 |

| Percent of observation period when kiosk was closed | 10 | 0 | 10 | 70 | 60 | 70 | 0 | 50 | 0 | 30 |

| Percent of closure time due to water shortage | 80 | 0 | 90 | 100 | 83 | 86 | 0 | 80 | 0 | 86 |

| Percent of closure time due to offline water treatment system | 10 | 0 | 0 | 0 | 17 | 0 | 0 | 0 | 0 | 7 |

| Percent of closure time due to lack of manpower | 10 | 0 | 10 | 0 | 0 | 14 | 0 | 20 | 0 | 7 |

| Kiosk | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | Mean | rs † | p Value |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Profit margin per m3 sold (%) | 3 | −34 | 10 | 54 | 7 | 74 | 56 | 47 | 4 | 25 | (Ref.) | |

| Volume distributed (m3) | 57 | 41 | 6 | 28 | 3 | 8 | 6 | 10 | 33 | 21 | −0.51 | <0.01 |

| Rainwater used (%) | 7 | 22 | 0 | 41 | 0 | 30 | 14 | 22 | 0 | 23 | 0.21 | 0.25 |

| Production cost (USD/m3) | 1.03 | 1.11 | 1.14 | 0.78 | 1.27 | 0.53 | 0.79 | 1.24 | 1.09 | 1.00 | −0.52 | <0.01 |

| Water loss per m3 sold (%) | 19 | 53 | 5 | 15 | 30 | 10 | 8 | 6 | 12 | 18 | −0.66 | <0.01 |

| Kiosk | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| Total m3 of treated water distributed to kiosk and HCF | 1383 | 1137 | 541 | 93 | 124 | 168 | 280 | 178 | 132 |

| Total production cost (USD) of treated water distributed to kiosk and HCF | 1430 | 1224 | 644 | 80 | 167 | 135 | 271 | 220 | 155 |

| Total m3 treated water distributed to kiosk (% total volume) | 739 (53) | 367 (32) | 46 (9) | 56 (60) | 1 (1) | 16 (10) | 18 (6) | 29 (16) | 66 (50) |

| Total production cost of treated water distributed to kiosk (USD) * | 766 | 416 | 54 | 47 | 12 | 7 | 13 | 35 | 81 |

| Total kiosk revenue (USD) | 802 | 310 | 59 | 95 | 14 | 30 | 33 | 58 | 73 |

| Total kiosk profit (USD) | 36 | −106 | 5 | 48 | 2 | 23 | 20 | 23 | −8 |

| Average kiosk profit * (USD/month) (range) | 3 (−7–10) | −12 (−26–3) | 1 (−1–3) | 24 (0–68) | 0 (0–1) | 12 (0–20) | 7 (2–10) | 8 (4–11) | −4 (−15–7) |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huttinger, A.; Brunson, L.; Moe, C.L.; Roha, K.; Ngirimpuhwe, P.; Mfura, L.; Kayigamba, F.; Ciza, P.; Dreibelbis, R. Small Water Enterprise in Rural Rwanda: Business Development and Year-One Performance Evaluation of Nine Water Kiosks at Health Care Facilities. Int. J. Environ. Res. Public Health 2017, 14, 1584. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph14121584

Huttinger A, Brunson L, Moe CL, Roha K, Ngirimpuhwe P, Mfura L, Kayigamba F, Ciza P, Dreibelbis R. Small Water Enterprise in Rural Rwanda: Business Development and Year-One Performance Evaluation of Nine Water Kiosks at Health Care Facilities. International Journal of Environmental Research and Public Health. 2017; 14(12):1584. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph14121584

Chicago/Turabian StyleHuttinger, Alexandra, Laura Brunson, Christine L. Moe, Kristin Roha, Providence Ngirimpuhwe, Leodomir Mfura, Felix Kayigamba, Philbert Ciza, and Robert Dreibelbis. 2017. "Small Water Enterprise in Rural Rwanda: Business Development and Year-One Performance Evaluation of Nine Water Kiosks at Health Care Facilities" International Journal of Environmental Research and Public Health 14, no. 12: 1584. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph14121584