Impact of Medical Debt on the Financial Welfare of Middle- and Low-Income Families across China

, , ,

, , ,

Abstract

:1. Introduction

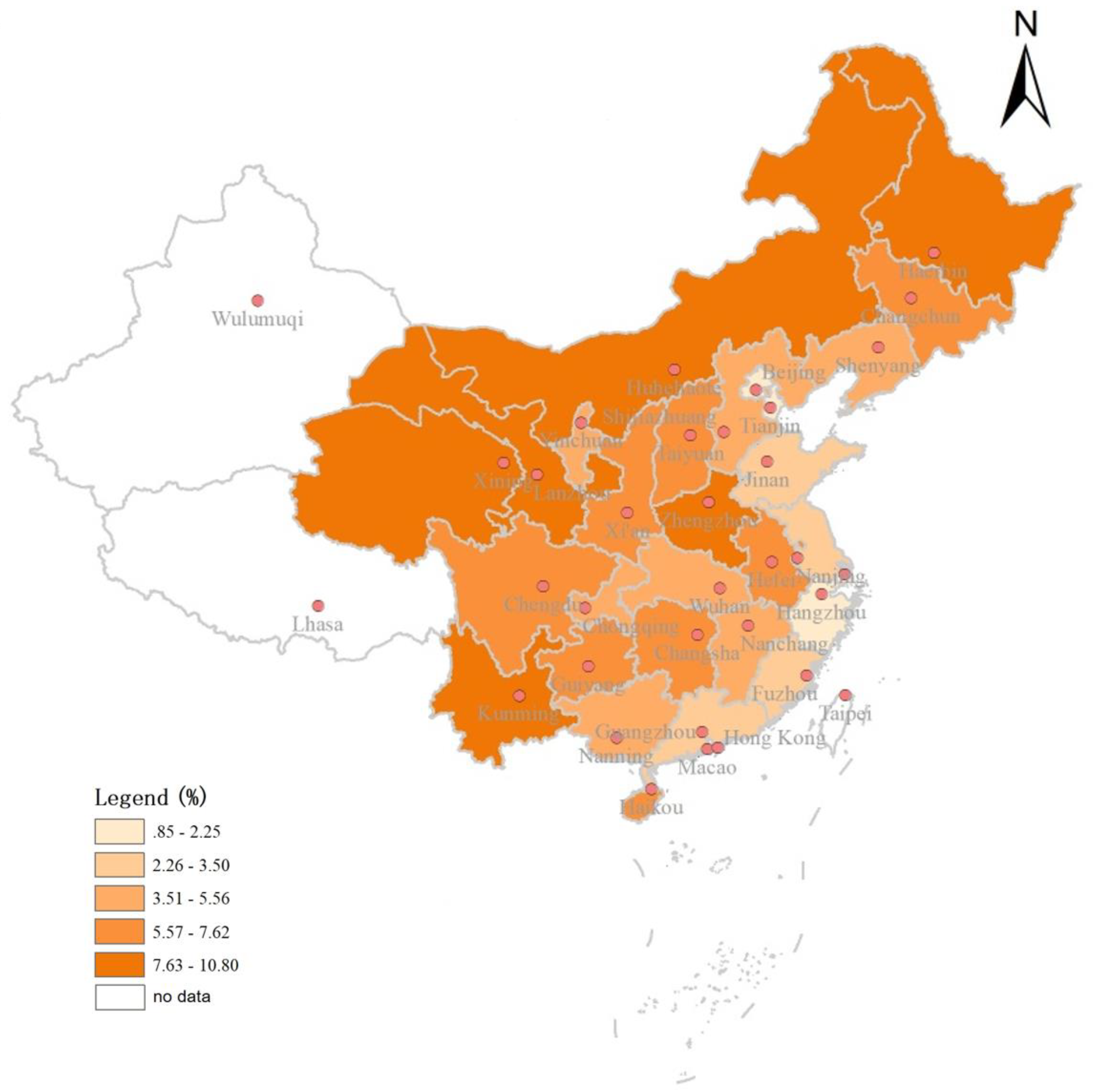

2. Materials and Methods

2.1. Materials

2.2. Variables

2.3. Methods

3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Ethics Approval and Consent to Participate

Availability of Data and Materials

List of Abbreviations

| OOP | Out-Of-Pocket |

| CHE | Catastrophic Health Expenditure |

| NCMS | New Cooperative Medical Scheme |

| UEBMI | Urban Employee Basic Medical Insurance |

| URBMI | Urban Resident Basic Medical Insurance |

| CII | Critical Illness Insurance |

| CI | Concentration Index |

| CHFS | China Household Finance Survey |

| NCD | Non-Communicated Disease |

References

- Herman, P.M.; Rissi, J.J.; Walsh, M.E. Health insurance status, medical debt, and their impact on access to care in Arizona. Am. J. Public Health 2011, 101, 1437–1443. [Google Scholar] [CrossRef] [PubMed]

- Himmelstein, D.U.; Woolhandler, S.; Sarra, J.; Guyatt, G. Health Issues and Health Care Expenses in Canadian Bankruptcies and Insolvencies. Int. J. Health Serv. 2014, 44, 7–23. [Google Scholar] [CrossRef] [PubMed]

- Damme, W.V.; Leemput, L.V.; Por, I.; Hardeman, W.; Meessen, B. Out-of-pocket health expenditure and debt in poor households: Evidence from Cambodia. Trop. Med. Int. Health 2004, 9, 273–280. [Google Scholar] [CrossRef] [Green Version]

- Seifert, R.W.; Rukavina, M. Bankruptcy Is the Tip of a Medical-Debt Iceberg. Health Affair 2006, 25, w89–w92. [Google Scholar] [CrossRef]

- Dranove, D.; Millenson, M.L. Medical Bankruptcy: Myth Versus Fact. Health Affair 2006, 25, w74–w83. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Doty, M.M.; Edwards, J.N.; Holmgren, A.L. Seeing red: Americans driven into debt by medical bills. Results from a National Survey. Issue Brief 2005, 837, 1–12. [Google Scholar]

- Siddalingappa, H.; Harshith, G.C.; Narayana Murthy, M.R.; Kulkarni, P.; Sunil Kumar, D. Health insurance coverage and healthcare expenditure pattern in rural Mysore. Ind. J. Med. Spec. 2015, 6, 151–154. [Google Scholar] [CrossRef]

- Masic, I.; Hadziahmetovic, M.; Donev, D.; Pollhozani, A.; Ramadani, N.; Skopljak, A.; Pasagic, A.; Roshi, E.; Zunic, L.; Zildzic, M. Public Health Aspects of the Family Medicine Concepts in South Eastern Europe. Mater. Soc. Med. 2014, 26, 277. [Google Scholar] [CrossRef] [Green Version]

- Thomas, T.K. Role of health insurance in enabling universal health coverage in India: A critical review. Health Serv. Manag. Res. 2016, 29, 99–106. [Google Scholar] [CrossRef]

- Ensor, T.; San, P.B. Access and payment for health care: The poor of Northern Vietnam. Int. J. Health Plann. Manag. 1996, 11, 69–83. [Google Scholar] [CrossRef]

- Sun, X.; Jackson, S.; Carmichael, G.; Sleigh, A.C. Catastrophic medical payment and financial protection in rural China: Evidence from the New Cooperative Medical Scheme in Shandong Province. Health Econ. 2009, 18, 103–119. [Google Scholar] [CrossRef] [PubMed]

- Zhu Wei, X.Y. An Analysis on Household Consumption-Fueled Borrowing in China. J. Finance Econ. 2018, 44, 67–81. [Google Scholar]

- Leng, A.; Jing, J.; Nicholas, S.; Wang, J. Catastrophic Health Expenditure of Cancer Patients at the End-of-Life: A Retrospective Observational Study in China. BMC Palliat Care 2019, 18, 43. [Google Scholar] [CrossRef] [PubMed]

- Gan, L.; Yin, Z.; Jia, N.; Xu, S.; Ma, S.; Zheng, L. Data You Need to Know about China. Research Report of China Household Finance Survey 2012; Springer: Berlin, Germany, 2014. [Google Scholar]

- Hao, Y.; Wu, Q.; Zhang, Z.; Gao, L.; Ning, N.; Jiao, M.; Zakus, D. The impact of different benefit packages of Medical Financial Assistance Scheme on health service utilization of poor population in Rural China. BMC Health Serv. Res. 2010, 10, 170. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Li, X.; Lu, J.; Hu, S.; Cheng, K.K.; De Maeseneer, J.; Meng, Q.; Mossialos, E.; Xu, D.R.; Yip, W.; Zhang, H.; et al. The primary health-care system in China. Lancet 2017, 390, 2584–2594. [Google Scholar] [CrossRef]

- Li, L.; Fu, H. China’s health care system reform: Progress and prospects. Int. J. Health Plan. Manag. 2017, 32, 240–253. [Google Scholar] [CrossRef] [PubMed]

- Zhou, Z.; Zhu, L.; Zhou, Z.; Li, Z.; Gao, J.; Chen, G. The effects of China’s urban basic medical insurance schemes on the equity of health service utilisation: Evidence from Shaanxi Province. Int. J. Equity Health 2014, 13, 23. [Google Scholar] [CrossRef] [Green Version]

- General Department of Poverty Alleviation Office of the State Council. Achievements and Experiences of Poverty Alleviation in the 70 Years since the Founding of New China. Available online: http://www.cpad.gov.cn/art/2019/9/18/art_624_103441.html (accessed on 18 September 2019).

- Zeng, Y.; Li, J.; Yuan, Z.; Fang, Y. The effect of China’s new cooperative medical scheme on health expenditures among the rural elderly. Int. J. Equity Health 2019, 18, 27. [Google Scholar] [CrossRef] [Green Version]

- China Health and Family Planning Statistical Yearbook Committee. Health Statistics Yearbook of China. Available online: http://www.yearbookchina.com/navibooklist-n3018112802-1.html (accessed on 18 September 2018).

- Hongbo, C.; Shi, P. Research on Social Capital and Urban Household Debt Behavior—Based on the Empirical Analysis of 3011 Families in Cities. Finance Econ. 2017, 2, 88–98. [Google Scholar]

- Zhiqiang, J. The Medical Burden of Urban and Rural Poor Families and Strategy Advices for Improving the Medical Assistance—Based on the Survey Data from “the Social Policy Support System Project of Urban and Rural Poor Family”. Soc. Secur. Stud. 2018, 4, 48–55. [Google Scholar]

- Jiang, J.; Chen, S.; Xin, Y.; Wang, X.; Zeng, L.; Zhong, Z.; Xiang, L. Does the critical illness insurance reduce patients’ financial burden and benefit the poor more: A comprehensive evaluation in rural area of China. J. Med. Econ. 2019, 22, 455–463. [Google Scholar] [CrossRef]

- Batty, M.; Gibbs, C.; Ippolito, B. Unlike Medical Spending, Medical Bills in Collections Decrease with Patients’ Age. Health Affair 2018, 37, 1257–1264. [Google Scholar] [CrossRef] [PubMed]

- Finkelstein, A.; Taubman, S.; Wright, B.; Bernstein, M.; Gruber, J.; Newhouse, J.P.; Allen, H.; Baicker, K. The Oregon Health Insurance Experiment: Evidence from the First Year. Q. J. Econ. 2012, 127, 1057–1106. [Google Scholar] [CrossRef] [Green Version]

- McCarthy, M. TV comedian writes off $15m in US medical debt. BMJ Brit. Med. J. 2016, 353, i3228. [Google Scholar] [CrossRef] [PubMed]

- Thompson, O. The long-term health impacts of Medicaid and CHIP. J. Health Econ. 2017, 51, 26–40. [Google Scholar] [CrossRef]

- Richard, P.; Walker, R.; Alexandre, P. The burden of out of pocket costs and medical debt faced by households with chronic health conditions in the United States. PLoS ONE 2018, 13, e199598. [Google Scholar] [CrossRef] [Green Version]

- Andreescu, C.; Whyte, E.M.; Mazumdar, S.; Pollock, B.G.; Houck, P.R.; Dombrovski, A.Y.; Reynolds, C.F.; Mulsant, B.H. Empirically Derived Decision Trees for the Treatment of Late-Life Depression. Am. J. Psychiatry 2008, 165, 855–862. [Google Scholar] [CrossRef] [Green Version]

- Carlson, M.J.; DeVoe, J.; Wrigbt, B.J. Short-term impacts of coverage loss in a Medicaid population: Early results from a prospective cohort study of the Oregon Health Plan. Ann. Fam. Med. 2006, 4, 391–398. [Google Scholar] [CrossRef] [Green Version]

- Altice, C.K.; Banegas, M.P.; Tucker-Seeley, R.D.; Yabroff, K.R. Financial Hardships Experienced by Cancer Survivors: A Systematic Review. JNCI J. Natl. Cancer I 2017, 109, djw2052. [Google Scholar] [CrossRef]

- Banegas, M.P.; Guy, G.P.; de Moor, J.S.; Ekwueme, D.U.; Virgo, K.S.; Kent, E.E.; Nutt, S.; Zheng, Z.; Rechis, R.; Yabroff, K.R. For Working-Age Cancer Survivors, Medical Debt and Bankruptcy Create Financial Hardships. Health Affair 2016, 35, 54–61. [Google Scholar] [CrossRef]

- Xu, K.; Evans, D.B.; Kawabata, K.; Zeramdini, R.; Klavus, J.; Murray, C.J. Household catastrophic health expenditure: A multicountry analysis. Lancet 2003, 362, 111–117. [Google Scholar] [CrossRef]

- Sun, J.; Liabsuetrakul, T.; Fan, Y.; McNeil, E. Protecting patients with cardiovascular diseases from catastrophic health expenditure and impoverishment by health finance reform. Trop. Med. Int. Health 2015, 20, 1846–1854. [Google Scholar] [CrossRef] [Green Version]

- Xu, K.; Aguilarmahecha, A.; Carrin, G.; Evans, D.; Hanvoravongchai, P.; Kawabata, K.; Klavus, J.; Knaul, F.; Murray, C.; Ortiz, J. Distribution of Health Payments and Catastrophic Expenditures: Methodology; WHO: Geneva, Switzerland, 2005. [Google Scholar]

- Kakwani, N.; Wagstaff, A.; van Doorslaer, E. Socioeconomic inequalities in health: Measurement, computation, and statistical inference. J. Econom. 1997, 77, 87–103. [Google Scholar] [CrossRef] [Green Version]

- Wagstaff, A. The bounds of the concentration index when the variable of interest is binary, with an application to immunization inequality. Health Econ. 2005, 14, 429–432. [Google Scholar] [CrossRef]

- Petrov, M.E.; Goodin, B.R.; Cruz-Almeida, Y.; King, C.; Glover, T.L.; Bulls, H.W.; Herbert, M.; Sibille, K.T.; Bartley, E.J.; Fessler, B.J.; et al. Disrupted Sleep Is Associated with Altered Pain Processing by Sex and Ethnicity in Knee Osteoarthritis. J. Pain 2015, 16, 478–490. [Google Scholar] [CrossRef] [Green Version]

- Amemiya, T. Tobit Models: A Survey. J. Econom. 1984, 24, 3–61. [Google Scholar] [CrossRef]

- Johnson, P.T.; Alvin, M.D.; Ziegelstein, R.C. Transitioning to a High-Value Health Care Model: Academic Accountability. Acad. Med. 2018, 93, 850–855. [Google Scholar] [CrossRef]

- O’toole, T.P.; Arbelaez, J.J.; Lawrence, R.S. Baltimore Community Health Consortium. Medical Debt and Aggressive Debt Restitution Practices. J. Gen. Intern Med. 2004, 19, 772–778. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Richard, P. The Burden of Medical Debt Faced by Households with Dependent Children in the United States: Implications for the Affordable Care Act of 2010. J. Fam. Econ. Issue 2016, 37, 212–225. [Google Scholar] [CrossRef]

- Lu, L.; O’Sullivan, E.; Sharp, L. Cancer-related financial hardship among head and neck cancer survivors: Risk factors and associations with health-related quality of life. Psycho Oncol. 2019, 28, 863–871. [Google Scholar] [CrossRef]

- Scott, J.W.; Raykar, N.P.; Rose, J.A.; Tsai, T.C.; Zogg, C.K.; Haider, A.H.; Salim, A.; Meara, J.G.; Shrime, M.G. Cured into Destitution: Catastrophic Health Expenditure Risk Among Uninsured Trauma Patients in the United States. Ann. Surg. 2018, 267, 1093–1099. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

| Variable | Low-Income Households | Middle-Income Households | ||

|---|---|---|---|---|

| n | Median or Proportion | n | Median or Proportion | |

| Median medical debt (US$) | 487 | 3268.51 | 301 | 4085.63 |

| Median per capita income (US$) | 12435 | 738.03 | 12433 | 3757.88 |

| Median years to pay medical debt (years) | 487 | 2.49 | 301 | 0.56 |

| CI for medical debt incidence | 12435 | −0.070 (p = 0.007) | 12433 | −0.306 (p = 0.000) |

| Median OOP payment (US$) | 9409 | 244.19 | 9336 | 325.58 |

| CHE incidence (%) | 12435 | 36.92 | 12433 | 25.54 |

| CHE forcing households into poverty (%) | 62.75 | 41.80 | ||

| Variables | Households in Poverty | Non-Poverty Households | χ2 | ||

|---|---|---|---|---|---|

| n | Median or Proportion | n | Median or Proportion | ||

| CHE incidence | 9470 | 44.44% | 15398 | 23.11% | p < 0.001 |

| The proportion of families with medical debt | 9470 | 3.50% | 15398 | 2.95% | p = 0.017 |

| median medical debt (US$) | 331 | 1953.51 | 457 | 4069.81 | |

| median OOP payment (US$) | 7250 | 162.79 | 11525 | 325.58 | |

| Variables | Impoverished Households | Non-Impoverished Households | χ2 | ||

|---|---|---|---|---|---|

| n | Median or Proportion | n | Median or Proportion | ||

| CHE incidence | 1534 | 79.01% | 13864 | 16.76% | p < 0.001 |

| The proportion of families with medical debt | 1534 | 11.08% | 13864 | 2.05% | p < 0.001 |

| median medical debt (US$) | 170 | 4069.81 | 284 | 4232.60 | |

| median OOP payment (US$) | 1534 | 1627.92 | 9991 | 325.58 | |

| Variable | Low-Income Households | Middle-Income Households | ||

|---|---|---|---|---|

| b | p | b | p | |

| per capita income (RMB 10 thousand≈US$1645.25) | - | - | –2.391 | 0.000 |

| OOP payment (RMB 10 thousand≈US$1645.25) | 0.524 | 0.000 | 0.886 | 0.000 |

| CHE | 0.254 | 0.000 | 0.286 | 0.011 |

| Household asset (RMB 10 thousand≈US$1645.25) | - | - | –0.054 | 0.000 |

| householder age | –0.009 | 0.002 | - | - |

| householder education | –0.101 | 0.000 | - | - |

| householder working status | 0.121 | 0.082 | 0.128 | 0.065 |

| householder health status | 0.173 | 0.000 | 0.208 | 0.000 |

| middle-age members with NCD | 0.220 | 0.000 | - | - |

| middle-age members insured by NCMS | - | - | 0.346 | 0.000 |

| middle-age members uninsured | - | - | 0.182 | 0.128 |

| middle-age members hospitalized ever | 0.145 | 0.050 | 0.115 | 0.127 |

| children under 5 uninsured | –0.512 | 0.000 | –0.221 | 0.134 |

| children under 5 hospitalized ever | 0.294 | 0.117 | - | - |

| children under 5 insured by URBMI | - | - | 0.454 | 0.019 |

| students hospitalized ever | 0.717 | 0.000 | - | - |

| students insured by URBMI | –0.290 | 0.145 | - | - |

| the elderly insured by URBMI | - | - | –0.301 | 0.037 |

| the elderly hospitalized ever | 0.200 | 0.066 | 0.228 | 0.050 |

| constant | –1.606 | 0.000 | –2.158 | 0.000 |

| uncensored | 483 | 301 | ||

| Log pseudo likelihood | –0.957 | –0.309 | ||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, J.; Jiao, C.; Nicholas, S.; Wang, J.; Chen, G.; Chang, J. Impact of Medical Debt on the Financial Welfare of Middle- and Low-Income Families across China. Int. J. Environ. Res. Public Health 2020, 17, 4597. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph17124597

Li J, Jiao C, Nicholas S, Wang J, Chen G, Chang J. Impact of Medical Debt on the Financial Welfare of Middle- and Low-Income Families across China. International Journal of Environmental Research and Public Health. 2020; 17(12):4597. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph17124597

Chicago/Turabian StyleLi, Jiajing, Chen Jiao, Stephen Nicholas, Jian Wang, Gong Chen, and Jinghua Chang. 2020. "Impact of Medical Debt on the Financial Welfare of Middle- and Low-Income Families across China" International Journal of Environmental Research and Public Health 17, no. 12: 4597. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph17124597