The Frantic Seeking of Credit during Poker Machine Problem Gambling: A Public Health Perspective

Abstract

:1. Introduction

2. Materials and Methods

3. Results

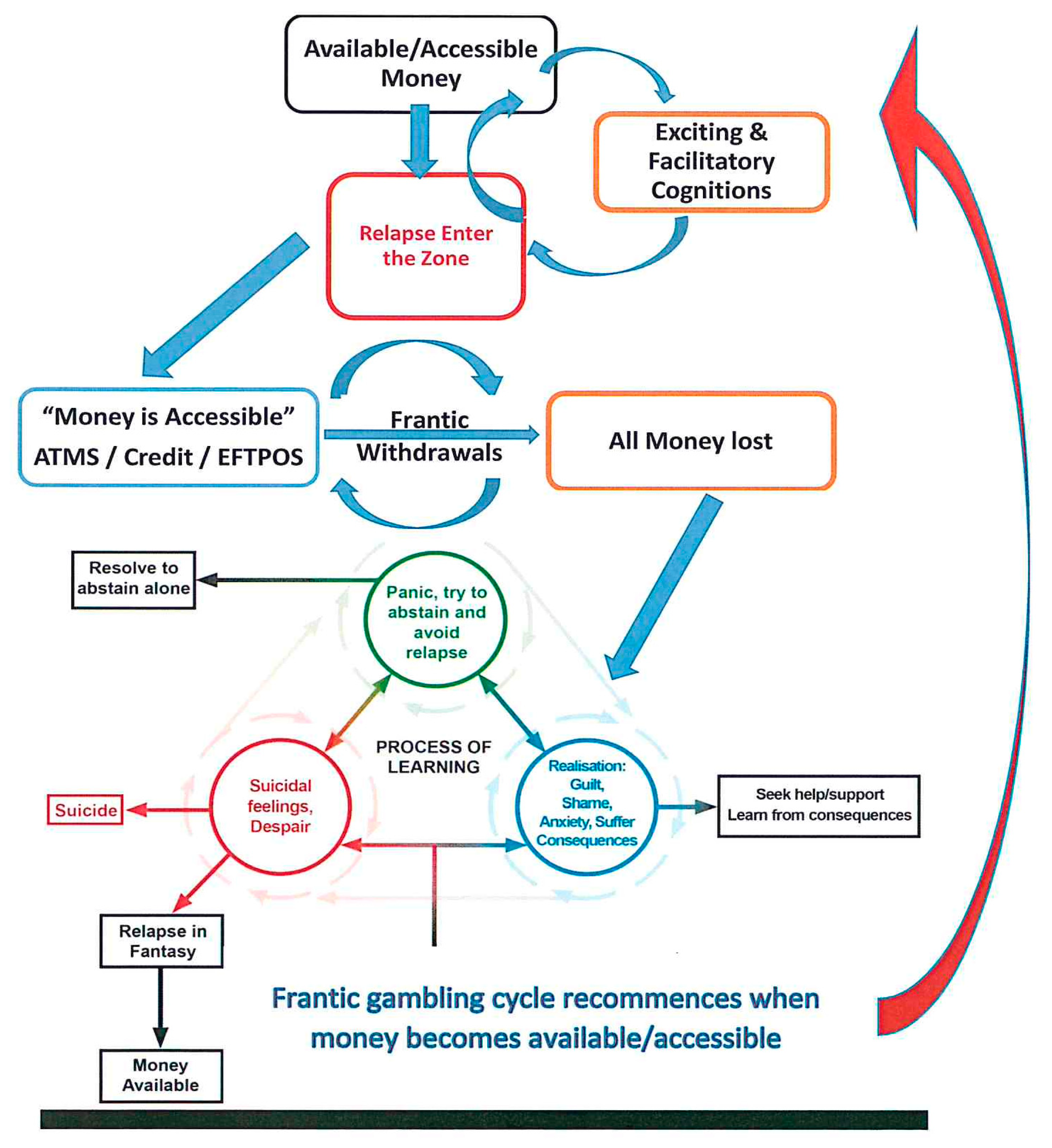

3.1. Frantic Accessing of Credit While Gambling

I wasn’t aware of my surroundings or anything, just back and forth to the ATM—$50, 50, 50, 50, 50—desperate in the end. Yeah, that ugly ‘zone’; a dangerous place to be. The ‘zone’ is when you lose rational thinking, and you don’t have the power or the thought process to be able to leave.

Well, what would happen is that you’d play all your money, empty your bank book, empty that out because they’ve got the ATMs virtually next door to you. Then you try to chase it up, and then I keep trying to chase and chase and chase it up, going back and forth to the auto bank.

I’d blown $300, or two or $300, from the credit card …..I said to myself ‘look if I ever go back to the ATM and withdraw from the credit card then I’m going to have to go and see ‘somebody’’ so I sort of – and that happened for quite some time.

Oh my God, I’m taking more money out. I’ve gone back to the ATM three times in a night, so at each point, there’s a level of – did pride come into it? I don’t know; I’m trying to recall the feelings. Towards the end – I suppose scared is not quite the right word. I can’t think of how I’d feel at the ATM.

I just kept losing. I kept going to the ATM – and, worse, I kept going to the ATM, getting more money out and going back and spending it.

Yeah, more than I had. I’d bleed the bank dry. Not good; not good but then I’d think ‘oh okay, a few dollars or $50 I might win some of that back’ so I guess at the time you – yeah I was – I mean I didn’t feel good because I’d be watching the bank account go down and down and down.

I, you put your money through and think ‘oh I need some more money’ so you go and grab some more money, you use your EFTPOS card and you go and grab some more money, and then you put more money in. You’re going ‘these free games have got to come up’ so you go and get more money and put it in the machine… sometimes I’ve gone overboard, and I might have had to get a credit advance or something like that on a Bankcard.

3.2. Financial Statements Tell the Gambler What They Have Done

I got a bank statement which showed me what I’d earned and what I still had in the account, and it was like ‘oh my God, I can’t possibly have earned that amount of money and spent that amount of money and I did’.

I had that bank statement sitting in front of me going ‘oh my God, you did lose that amount of money’.

I could have my bank statements now you’d see that I was going back and forth taking out $20, not wanting to spend the whole lot but eventually spending the whole lot. When the receipt came out, there was no money left; it felt so bad.

3.3. Inability to Make Rational Financial Decisions

I would say ‘quick I need more money’. I couldn’t get it into the machine quick enough but now to lose that particular amount of money in one day to me, I can’t even understand how my cognitive processes were going at that time. It seems insane.

No; no, until afterwards, until I realised all that money’s gone. Shocking isn’t it? That was all I had basically, so I had to stop.

4. Discussion

4.1. The Frantic Use of Credit during the Gambling Episode

4.2. Model of Financial Destruction

4.3. Do Financial Institutions Have a Duty of Care to Intervene?

4.4. Recommendations

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Armstrong, A.; Carroll, M. Gambling Activity in Australia. Australian Gambling Research Centre; Australian Institute of Family Studies: Melbourne, Australia, 2017. [Google Scholar]

- Connelly, J.; Luckett, W.; Knox, K. Enhancing Recovery Prospects of Gamblers Through In-Depth Financial Counselling: An Integrated Approach. In Proceedings of the National Association of Gambling Studies Sixth National Conference, Freemantle, Western Australia, 28–30 September 1995. [Google Scholar]

- Productivity Commission. Australia’s Gambling Industries (Report No. 10); AusInfo: Canberra, Australia, 1999. Available online: https://www.pc.gov.au/inquiries/completed/gambling/report/gambling1.pdf (accessed on 12 July 2020).

- Browne, M.; Greer, N.; Rawat, V.; Rockloff, M.A. A Population-Level Metric for Gambling-Related Harm. Int. Gambl. Stud. 2017, 2, 163–167. [Google Scholar] [CrossRef]

- Delfabbro, P.; King, D.L. Challenges in the Conceptualisation and Measurement of Gambling-Related Harm. J. Gambl. Stud. 2019, 35, 743–755. [Google Scholar] [CrossRef] [PubMed]

- Langham, E.; Thorne, H.; Browne, M.; Donaldson, P.; Rose, J.; Rockloff, M. Understanding Gambling-Related Harm: A Proposed Definition, Conceptual Framework, and Taxonomy of Harms. BMC Public Health 2015, 1, 80–102. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Swanton, T.B.; Gainsbury, S.M.; Blaszczynski, A. The Role of Financial Institutions in Gambling. Int. Gambl. Stud. 2019, 3, 377–398. [Google Scholar] [CrossRef]

- Pentland, J.; Drosten, P. Financial Counselling and Problem Gambling Counselling: Exploration of a Service Model. Aust. J. Prim. Health 1996, 2, 54–62. [Google Scholar] [CrossRef]

- Financial Counselling Australia. Problem Gambling Financial Counselling Survey and Case Studies; Financial Counselling Australia 2016: Level 6/179 Queen Street Melbourne, VIC, Australia, 5000; Available online: https://www.financialcounsellingaustralia.org.au/docs/problem-gambling-financial-counselling-survey-and-case-studies-2/ (accessed on 12 July 2020).

- Slutske, W.S. Natural Recovery and Treatment-Seeking in Pathological Gambling: Results of Two Us National Surveys. Am. J. Psychiatry 2006, 2, 297–302. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Tavares, H.; Zilberman, M.L.; Beites, F.J.; Gentil, V. Brief Communications: Gender Differences in Gambling Progression. J. Gamb. Stud. 2001, 2, 151–159. [Google Scholar]

- Hing, N.; Russell, A.; Tolchard, B.; Nower, L. Risk Factors for Gambling Problems: An Analysis by Gender. J. Gambl. Stud. 2016, 2, 511–534. [Google Scholar] [CrossRef] [Green Version]

- Evans, L.; Delfabbro, P. Motivators for Change and Barriers to Help-Seeking in Australian Problem Gamblers. J. Gambl. Stud. 2005, 2, 133–155. [Google Scholar] [CrossRef]

- Schüll, N.D. Addiction by Design: Machine Gambling in Las Vegas; Princeton University Press: Princeton, NJ, USA, 2014. [Google Scholar]

- Oakes, J.; Pols, R.; Lawn, S. The “Merry-Go-Round” of Habitual Relapse: A Qualitative Study of Relapse in Electronic Gaming. Int. J. Environ. Res. Public Health 2019, 16, 2858–2872. [Google Scholar] [CrossRef] [Green Version]

- Oakes, J.; Pols, R.G.; Lawn, S.; Battersby, M.W.; Lubman, D. “I’ll Just Pay The Rent Next Month”: An Exploratory Study Examining Facilitatory Cognitions among EGM Problem Gamblers. Int. J. Ment. Health Addict. 2019, 6, 1564–1579. [Google Scholar] [CrossRef]

- Oakes, J.; Pols, R.; Lawn, S.; Battersby, M. The “Zone”: A Qualitative Exploratory Study of an Altered State of Awareness in Electronic Gaming Machine Problem Gambling. Int. J. Ment. Health Addict. 2020, 1, 177–194. [Google Scholar] [CrossRef]

- Oakes, J.; Pols, R.; Battersby, M.; Lawn, S.; Pulvirenti, M.; Smith, D. A Focus Group Study of Predictors of Relapse in Electronic Gaming Machine Problem Gambling, Part 1: Factors That ‘Push ‘Towards Relapse. J. Gambl. Stud. 2012, 3, 451–464. [Google Scholar] [CrossRef] [PubMed]

- Oakes, J.; Pols, R.; Battersby, M.; Lawn, S.; Pulvirenti, M.; Smith, D. A Focus Group Study of Predictors of Relapse in Electronic Gaming Machine Problem Gambling, Part 2: Factors That ‘Pull ‘The Gambler Away From Relapse. J. Gambl. Stud. 2012, 28, 465–479. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ritchie, J.; Lewis, J. Qualitative Research Practice: A Guide for Social Science Students and Researchers; Sage: London, UK, 2003. [Google Scholar]

- Smith, J. Qualitative Psychology: A Practical Guide to Methods, Interpretative Phenomenological Analysis, 2nd ed.; Sage Publications: London, UK, 2008. [Google Scholar]

- Lewis, R.; Lewis, J. (Eds.) The Applications of Qualitative Methods to Social Research. In Qualitative Research Practice: A Guide for Social Science Students and Researchers; Publications: London, UK, 2003; Chapter 2.23. [Google Scholar]

- Douglas, D. Grounded Theories of Management: A Methodological Review. Manag. Res. News 2003, 26, 44–52. [Google Scholar] [CrossRef]

- Strauss, A.; Corbin, J. Basics of Qualitative Research. Grounded Theory Procedures and Techniques; Sage Publications: South Oaks, CA, USA, 1990. [Google Scholar]

- Guba, E.G. Criteria for Assessing the Trustworthiness of Naturalistic Inquiries. Ectj 1981, 2, 75–91. [Google Scholar]

- Swanton, T.; Gainsbury, S. Gambling-Related Consumer Credit Use and Debt Problems: A Brief Review. Curr. Opin. Behav. Sci. 2020, 31, 21–31. [Google Scholar] [CrossRef]

- Hayne, K. Final Report: Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry; Commonwealth of Australia: Canberra, Australia, 2019. Available online: https://treasury.gov.au/publication/p2019-fsrc-final-report (accessed on 10 July 2020).

- Chamberlain, E.; Simpson, R.; Smith, G. When Should Casinos Owe a Duty of Care toward Their Patrons. Alta. L. Rev. 2018, 56, 963–989. [Google Scholar] [CrossRef] [Green Version]

- Australian Banking Association. Australian Banking Association Banking Code of Practice Setting the Standards of Practice for Banks, Their Staff and Their Representative; Australian Banking Association: 6-10 O’Connell St, Sydney NSW 2000, 2019; Available online: https://www.ausbanking.org.au/wp-content/uploads/2020/03/Banking-Code-of-Practice-2019-web.pdf (accessed on 12 July 2020).

- Davis, K. The Hayne Royal Commission and Financial Sector Misbehaviour: Lasting Change or Temporary fix? Econ. Labour Relat. Rev. 2019, 30, 200–221. [Google Scholar] [CrossRef]

- Boardman, B.; Perry, J. Access to Gambling and Declaring Personal Bankruptcy. J. Socio-Econ. 2007, 36, 789–801. [Google Scholar] [CrossRef]

- Grant, J.; Schreiber, L.; Odlaug, B.; Kim, S. Pathologic Gambling and Bankruptcy. Compr. Psychiatry 2010, 51, 115–120. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Sacco, P.; Frey, J.; Callahan, C.; Hochheimer, M.; Imboden, R.; Hyde, D. Feasibility of Brief Screening for at-Risk Gambling In Consumer Credit Counseling. J. Gambl. Stud. 2019, 35, 1423–1439. [Google Scholar] [CrossRef] [PubMed]

- Riley, B.; Lawn, S.; Crisp, B. ‘When I’m Not Angry I Am Anxious’: The Lived Experiences of Individuals in a Relationship with a Non-Help-Seeking Problem Gambler. J. Soc. Pers. Relatsh. 2020; In press. [Google Scholar] [CrossRef]

- Greene, R. Carl Rogers and the Person-Centered Approach. In Human Behavior Theory and Social Work Practice; Transaction Publishers: New Brunswick, NJ, USA, 2017; pp. 145–165. [Google Scholar]

- Goyder, E.; Blank, L.; Baxter, S.; van Schalkwyk, M. Tackling Gambling Related Harms as a Public Health Issue. Lancet Pub. Health 2020, 1, e14–e15. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Focus Groups | Title |

|---|---|

| Participants | n = 10 |

| Clients who completed CBT | 5 |

| Pokies Anonymous members | 5 |

| In-Depth Interviews | Title |

|---|---|

| Participants | n = 19 |

| Treatment Seekers Total | 7 |

| Female | 2 |

| Male | 5 |

| Pokies Anonymous Total | 6 |

| Female | 4 |

| Male | 2 |

| Non treatment Seekers Total | 6 |

| All female | 6 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oakes, J.; Pols, R.; Lawn, S. The Frantic Seeking of Credit during Poker Machine Problem Gambling: A Public Health Perspective. Int. J. Environ. Res. Public Health 2020, 17, 5216. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph17145216

Oakes J, Pols R, Lawn S. The Frantic Seeking of Credit during Poker Machine Problem Gambling: A Public Health Perspective. International Journal of Environmental Research and Public Health. 2020; 17(14):5216. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph17145216

Chicago/Turabian StyleOakes, Jane, Rene Pols, and Sharon Lawn. 2020. "The Frantic Seeking of Credit during Poker Machine Problem Gambling: A Public Health Perspective" International Journal of Environmental Research and Public Health 17, no. 14: 5216. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph17145216