Can Mandatory Disclosure Policies Promote Corporate Environmental Responsibility?—Quasi-Natural Experimental Research on China

Abstract

:1. Introduction

2. Research Design

2.1. Research Hypotheses

2.2. Model Setting

2.3. Variable Measurement and Explanation

2.3.1. Explained Variables

2.3.2. Policy Variables

2.3.3. Control Variables

2.3.4. Other Variables

2.4. Data Sources and Descriptive Analysis

3. Econometric Tests of the Impact of Mandatory CSR Disclosure on CER

3.1. Analysis of Regression Results

3.2. Robustness Test

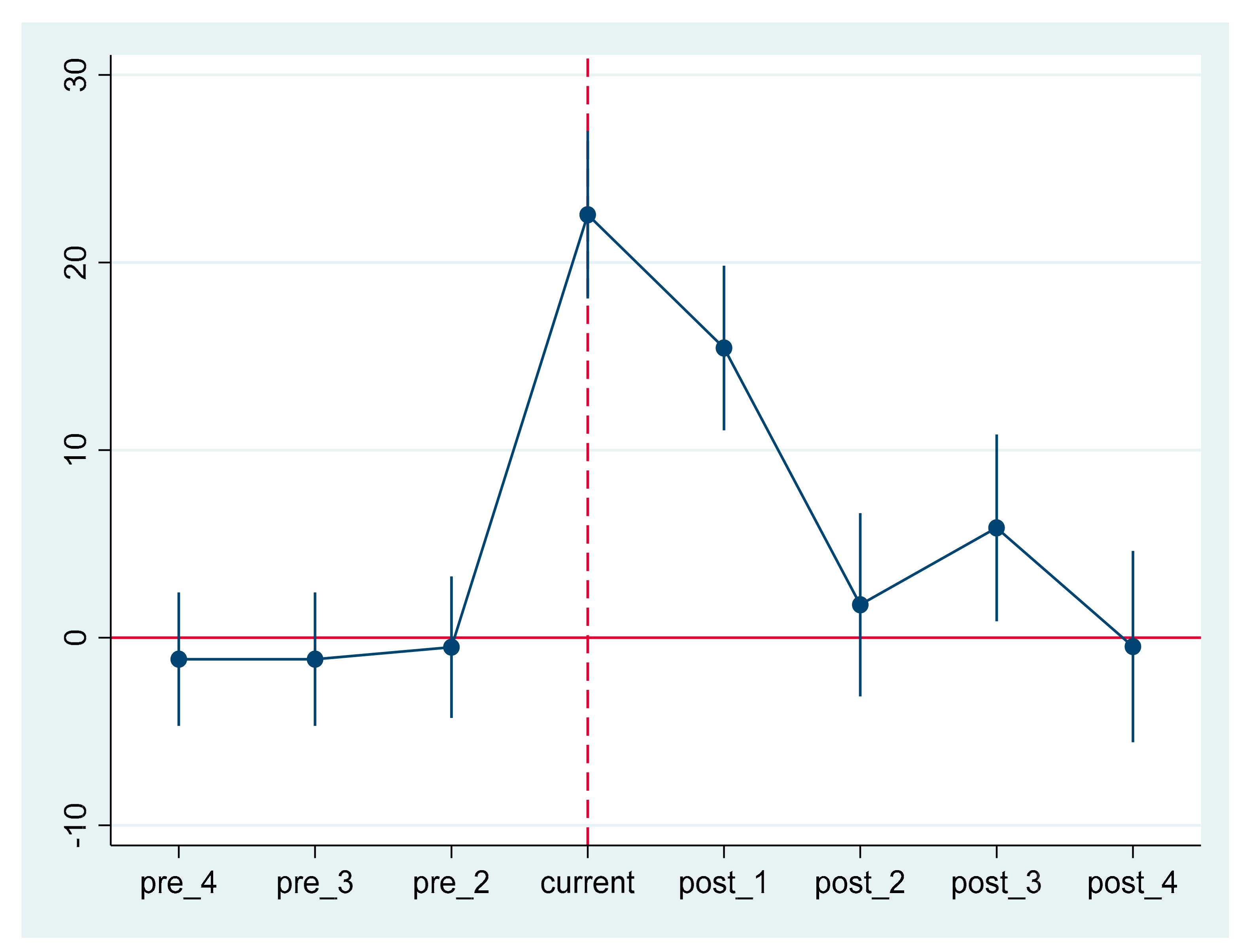

3.2.1. Parallel Trend Test

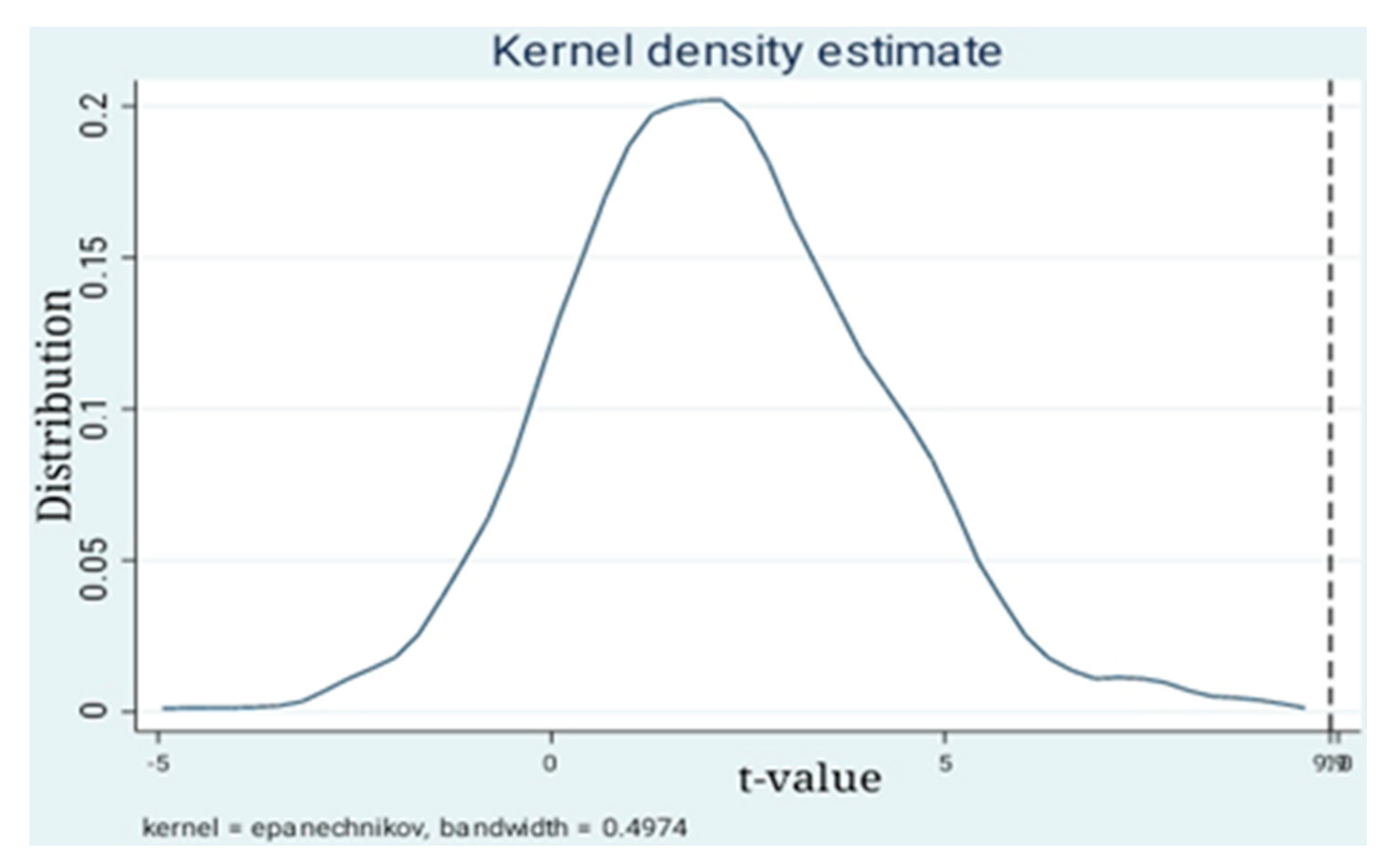

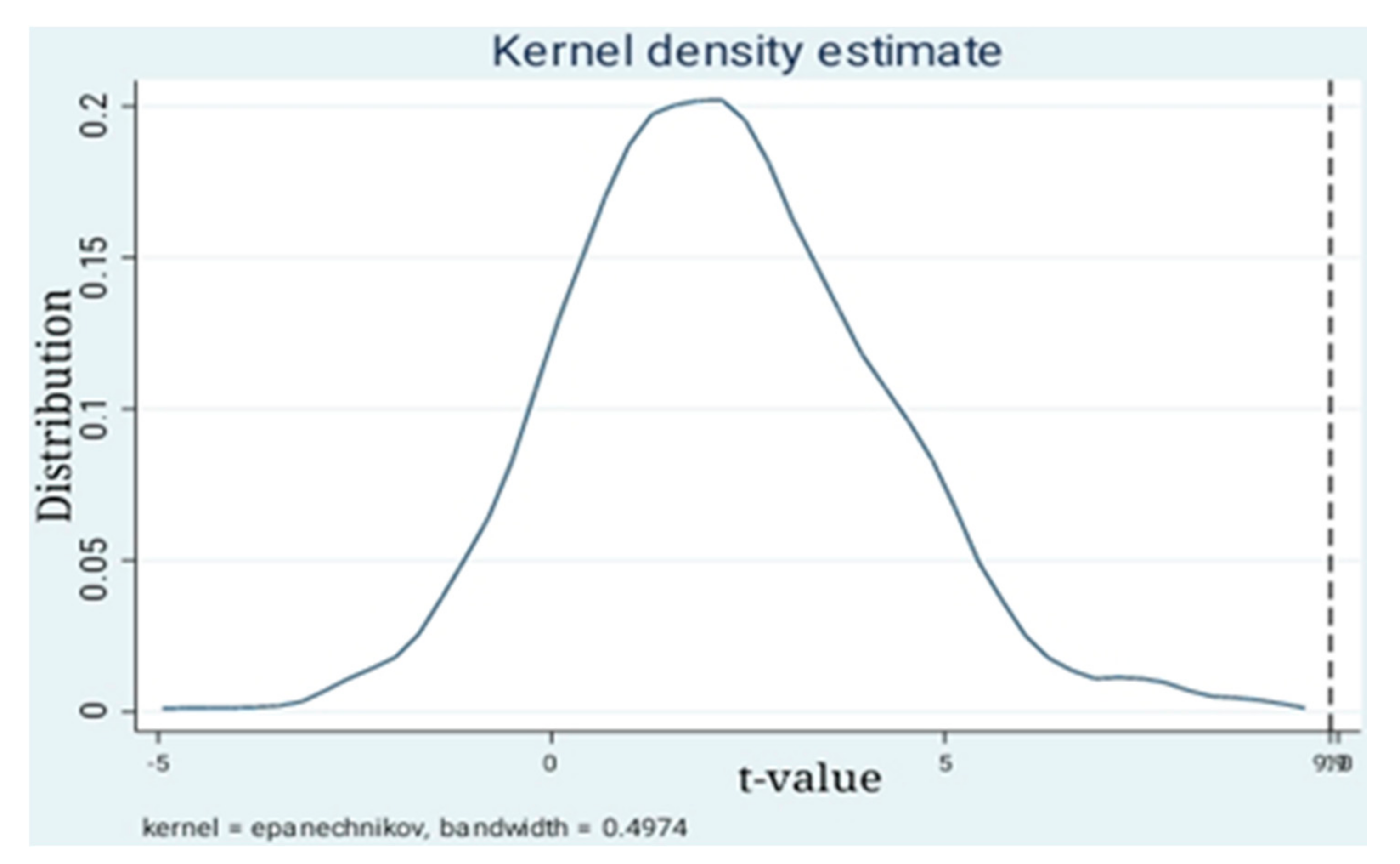

3.2.2. Placebo Test

4. The Influence Mechanism of Mandatory CSR Disclosure on CER

4.1. The Mediating Effect of the Quality of Environmental Management Disclosure

4.2. Mediating Effect of the Number of Patents Application

5. Heterogeneity Analysis

5.1. Heterogeneity Caused by Different CER Levels

5.2. Heterogeneity Caused by Different Corporate Scales

5.3. Heterogeneity Caused by XSD Different Property Rights Structure

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ilić, B.; Stojanovic, D.; Djukic, G. Green economy: Mobilization of international capital for financing projects of renewable energy sources. Green Financ. 2019, 1, 94–109. [Google Scholar] [CrossRef]

- Li, T.; Liao, G. The Heterogeneous Impact of Financial Development on Green Total Factor Productivity. Front. Energy Res. 2020, 8, 9. [Google Scholar] [CrossRef] [Green Version]

- Li, T.; Zhong, J.; Huang, Z. Potential Dependence of Financial Cycles between Emerging and Developed Countries: Based on ARIMA-GARCH Copula Model. Emerg. Mark. Financ. Trade 2019, 56, 1237–1250. [Google Scholar] [CrossRef]

- Li, Z.H.; Huang, Z.H.; Dong, H. The Influential Factors on Outward Foreign Direct Investment: Evidence from the “The Belt and Road”. Emerg. Mark. Financ. Trade 2019, 55, 3211–3226. [Google Scholar] [CrossRef]

- Li, Z.; Wang, Y.; Huang, Z. Risk Connectedness Heterogeneity in the Cryptocurrency Markets. Front. Phys. 2020, 8, 13. [Google Scholar] [CrossRef]

- Yang, A.; Liu, W. Corporate Environmental Responsibility and Global Online Cross-sector Alliance Network: A Cross-national Study. Environ. Commun. 2016, 12, 99–114. [Google Scholar] [CrossRef]

- Chang, C.Y.; Shie, F.S.; Yang, S.L. The relationship between herding behavior and firm size before and after the elimination of short-sale price restrictions. Quant. Finance Econ. 2019, 3, 526–549. [Google Scholar] [CrossRef]

- Demirtaş, Y.E.; Keçeci, N.F. The efficiency of private pension companies using dynamic data envelopment analysis. Quant. Finance Econ. 2020, 4, 204–219. [Google Scholar] [CrossRef]

- Arena, C.; Liong, R.; Vourvachis, P. Carrot or stick: CSR disclosures by Southeast Asian companies. Sustain. Account. Manag. Policy J. 2018, 9, 422–454. [Google Scholar] [CrossRef]

- Joseph, C.; Nichol, E.O.; Janggu, T.; Madi, N. Environmental literacy and attitudes among Malaysian business educators. Int. J. Sustain. High. Educ. 2013, 14, 196–208. [Google Scholar] [CrossRef]

- Nair, R.; Muttakin, M.; Khan, A.; Subramaniam, N.; Somanath, V. Corporate social responsibility disclosure and financial transparency: Evidence from India. Pac. Basin Financ. J. 2019, 56, 330–351. [Google Scholar] [CrossRef]

- De Luca, F.; Cardoni, A.; Phan, H.-T.-P.; Kiseleva, E. Does Structural Capital Affect SDGs Risk-Related Disclosure Quality? An Empirical Investigation of Italian Large Listed Companies. Sustainability 2020, 12, 1776. [Google Scholar] [CrossRef] [Green Version]

- Nicolo, G.; Zanellato, G.; Tiron-Tudor, A. Integrated Reporting and European State-Owned Enterprises: A Disclosure Analysis Pre and Post 2014/95/EU. Sustainability 2020, 12, 1908. [Google Scholar] [CrossRef] [Green Version]

- Balluchi, F.; Lazzini, A.; Torelli, R. Credibility of environmental issues in non-financial mandatory disclosure: Measurement and determinants. J. Clean. Prod. 2021, 288, 125744. [Google Scholar] [CrossRef]

- Li, Z.H.; Zhong, J.H. Impact of economic policy uncertainty shocks on China’s financial conditions. Financ. Res. Lett. 2020, 35, 7. [Google Scholar] [CrossRef]

- Liu, Y.; Li, Z.; Xu, M. The Influential Factors of Financial Cycle Spillover: Evidence from China. Emerg. Mark. Financ. Trade 2019, 56, 1336–1350. [Google Scholar] [CrossRef]

- Xu, M.; Albitar, K.; Li, Z. Does corporate financialization affect EVA? Early evidence from China. Green Financ. 2020, 2, 392–408. [Google Scholar] [CrossRef]

- Zhong, J.; Li, T. Impact of Financial Development and Its Spatial Spillover Effect on Green Total Factor Productivity: Evidence from 30 Provinces in China. Math. Probl. Eng. 2020, 2020, 1–11. [Google Scholar] [CrossRef] [Green Version]

- Sedláček, J.; Popelková, V. Non-financial information and their reporting—Evidence of small and medium-sized enterprises and large corporations on the Czech capital market. Natl. Account. Rev. 2020, 2, 204–216. [Google Scholar] [CrossRef]

- Li, Z.; Chen, L.; Dong, H. What are bitcoin market reactions to its-related events? Int. Rev. Econ. Financ. 2021, 73, 1–10. [Google Scholar] [CrossRef]

- Li, Z.H.; Dong, H.; Floros, C.; Charemis, A.; Failler, P. Re-examining Bitcoin Volatility: A CAViaR-based Approach. Emerg. Mark. Financ. Trade 2021. [Google Scholar] [CrossRef]

- Kasych, A.; Suler, P.; Rowland, Z. Corporate Environmental Responsibility through the Prism of Strategic Management. Sustainability 2020, 12, 9589. [Google Scholar] [CrossRef]

- Cave, A.H. Environmentally responsible management in international business: A literature review. Multinatl. Bus. Rev. 2014, 22, 78–102. [Google Scholar] [CrossRef]

- Tuzcuoğlu, T. The impact of financial fragility on firm performance: An analysis of BIST companies. Quant. Financ. Econ. 2020, 4, 310–342. [Google Scholar] [CrossRef]

- Peng, B.H.; Chen, S.L.; Elahi, E.; Wan, A.X. Can corporate environmental responsibility improve environmental perfor-mance? An inter-temporal analysis of Chinese chemical companies. Environ. Sci. Pollut. Res. 2021, 28, 12190–12201. [Google Scholar] [CrossRef] [PubMed]

- Huang, Z.; Liao, G.; Li, Z. Loaning scale and government subsidy for promoting green innovation. Technol. Forecast. Soc. Chang. 2019, 144, 148–156. [Google Scholar] [CrossRef]

- Zhang, Y.Y.; Ouyang, Z. Doing well by doing good: How corporate environmental responsibility influences corporate financial performance. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 54–63. [Google Scholar] [CrossRef]

- Dögl, C.; Holtbrügge, D. Corporate environmental responsibility, employer reputation and employee commitment: An empirical study in developed and emerging economies. Int. J. Hum. Resour. Manag. 2013, 25, 1739–1762. [Google Scholar] [CrossRef]

- Bhuiyan, M.B.U.; Hooks, J. Operational “problem” directors and environmental performance. Sustain. Account. Manag. Policy J. 2016, 7, 268–294. [Google Scholar]

- Wong, C.W.Y.; Miao, X.; Cui, S.; Tang, Y. Impact of Corporate Environmental Responsibility on Operating Income: Moderating Role of Regional Disparities in China. J. Bus. Ethics 2016, 149, 363–382. [Google Scholar] [CrossRef]

- Lin, Y. Legitimation strategies in corporate discourse: A comparison of UK and Chinese corporate social responsibility re-ports. J. Pragmat. 2021, 177, 157–169. [Google Scholar] [CrossRef]

- Li, Z.; Liao, G.; Albitar, K. Does corporate environmental responsibility engagement affect firm value? The mediating role of corporate innovation. Bus. Strat. Environ. 2019, 29, 1045–1055. [Google Scholar] [CrossRef]

- Li, Y.H.; Zhang, J.; Foo, C.T. Towards a theory of social responsibility reporting Empirical analysis of 613 CSR reports by listed corporations in China. Chin. Manag. Stud. 2013, 7, 519–534. [Google Scholar] [CrossRef]

- Jung, H.; Song, S.; Song, C.-K. Carbon Emission Regulation, Green Boards, and Corporate Environmental Responsibility. Sustainability 2021, 13, 4463. [Google Scholar] [CrossRef]

- Dana, L.-P.; Rounaghi, M.M.; Enayati, G.; Researcher, M.I. Increasing productivity and sustainability of corporate performance by using management control systems and intellectual capital accounting approach. Green Financ. 2021, 3, 1–14. [Google Scholar] [CrossRef]

- Hong, M.; Drakeford, B.; Zhang, K. The impact of mandatory CSR disclosure on green innovation: Evidence from China. Green Financ. 2020, 2, 302–322. [Google Scholar] [CrossRef]

- Testa, M.; D’Amato, A. Corporate environmental responsibility and financial performance: Does bidirectional causality work? Empirical evidence from the manufacturing industry. Soc. Responsib. J. 2017, 13, 221–234. [Google Scholar] [CrossRef]

- Zhang, C. Political connections and corporate environmental responsibility: Adopting or escaping? Energy Econ. 2017, 68, 539–547. [Google Scholar] [CrossRef]

- Imbens, G.W.; Wooldridge, J.M. Recent Developments in the Econometrics of Program Evaluation. J. Econ. Lit. 2009, 47, 5–86. [Google Scholar] [CrossRef] [Green Version]

- Feng, Y.; Chen, S.; Failler, P. Productivity Effect Evaluation on Market-Type Environmental Regulation: A Case Study of SO2 Emission Trading Pilot in China. Int. J. Environ. Res. Public Health 2020, 17, 8027. [Google Scholar] [CrossRef] [PubMed]

- Yang, J.; Luo, P.; Tan, Y. Contingent Decision of Corporate Environmental Responsibility Based on Uncertain Economic Policy. Sustainability 2020, 12, 8839. [Google Scholar] [CrossRef]

- Penfold, R.B.; Zhang, F. Use of Interrupted Time Series Analysis in Evaluating Health Care Quality Improvements. Acad. Pediatr. 2013, 13, S38–S44. [Google Scholar] [CrossRef]

- Liu, W.; Wei, Q.; Huang, S.Q.; Tsai, S.B. Doing Good Again? A Multilevel Institutional Perspective on Corporate Environ-mental Responsibility and Philanthropic Strategy. Int. J. Environ. Res. Public Health 2017, 14, 1283. [Google Scholar] [CrossRef] [Green Version]

- Chang, C.-H. The Determinants of Green Product Innovation Performance. Corp. Soc. Responsib. Environ. Manag. 2014, 23, 65–76. [Google Scholar] [CrossRef]

- Li, F.; Yang, C.Y.; Li, Z.H.; Failler, P. Does Geopolitics Have an Impact on Energy Trade? Empirical Research on Emerging Countries. Sustainability 2021, 13, 5199. [Google Scholar] [CrossRef]

- Yang, C.Y.; Li, T.H.; Albitar, K. Does energy efficiency affect ambient PM2.5? The moderating role of energy investment. Front. Environ. Sci. 2021, 1. [Google Scholar] [CrossRef]

- Hatmanu, M.; Sandu, C.B.; Jaba, E. A Comparative Study on Drivers for Corporate Environmental Responsibility, EU15 vs. EU-NMS13. Sustainability 2019, 11, 6397. [Google Scholar] [CrossRef] [Green Version]

- Dang, C.; Li, Z.; Yang, C. Measuring firm size in empirical corporate finance. J. Bank. Financ. 2018, 86, 159–176. [Google Scholar] [CrossRef]

- Coles, J.L.; Li, Z.F. An Empirical Assessment of Empirical Corporate Finance. SSRN Electron. J. 2011. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1787143 (accessed on 18 March 2011).

- Coles, J.L.; Li, Z. Managerial Attributes, Incentives, and Performance. Rev. Corp. Financ. Stud. 2020, 9, 256–301. [Google Scholar] [CrossRef]

- Fortunati, S.; Morea, D.; Mosconi, E.M. Circular economy and corporate social responsibility in the agricultural system: Cases study of the Italian agri-food industry. Agric. Econ. 2020, 66, 489–498. [Google Scholar] [CrossRef]

- Zhang, J.; Xiang, X.; Liu, Y. Political Connection, Institutional Environment and Corporate Social Responsibility; St Plum-Blossom Press Pty Ltd: Melbourne, Australia, 2016; pp. 203–209. [Google Scholar]

- Fortunati, S.; Martiniello, L.; Morea, D. The Strategic Role of the Corporate Social Responsibility and Circular Economy in the Cosmetic Industry. Sustainability 2020, 12, 5120. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Dimensions | Indicators |

|---|---|

| Legal awareness (10%) | 1. Whether following the GRI “Sustainability Reporting Guidelines” (1, 0); 2. Whether disclosing environment and sustainable development (1, 0); 3. Whether Environmental penalties are imposed (0, 1) |

| Social assessment (15%) | 1. Whether receiving environmental recognition (1, 0); 2. Whether having environmental advantages (1, 0) |

| Environment- friendly outputs (25%) | 1. Whether having a circular economy (1, 0); 2. Whether having environmentally beneficial products (1, 0); 3. Whether having pollution emissions (0, 1) |

| Low-carbon technologies (25%) | 1. Whether conserving energy (1, 0); 2. Whether having measures to reduce processing wastes (1, 0) |

| Green management (25%) | 1. Whether there is a third-party inspection (1, 0); 2. Whether adopting green office (1, 0) |

| Variable | Observations | Mean Value | Standard Deviation | Minimum Value | Maximum Value |

|---|---|---|---|---|---|

| CER | 4140 | 18.94975 | 23.11495 | 0 | 92.50000 |

| Corporate scale | 4140 | 22.25129 | 1.30309 | 16.18471 | 27.85198 |

| Corporate age | 4140 | 12.52278 | 4.43182 | 2.00000 | 31.00000 |

| Fixed asset ratio | 4140 | 0.29179 | 0.19889 | 0 | 0.93634 |

| Capital structure | 4140 | 0.52593 | 0.22456 | 0.02910 | 3.88615 |

| Return on assets | 4140 | 0.04371 | 0.11799 | −4.16097 | 2.14273 |

| Capital labor density | 4140 | 2069.40000 | 1202.84100 | 1.00000 | 4153.00000 |

| Number of patents application | 4140 | 50.41715 | 278.21780 | 0 | 6437 |

| Quality of environmental management disclosure | 4140 | 0.17343 | 0.80909 | 0 | 8 |

| Changes in CER mean before and after policy | Full sample | ||||

| Treated group | Control group | Difference | |||

| +40.44510 | +32.63288 | 7.81222 | |||

| Changes in CER mean before and after policy | State-owned enterprises | ||||

| Treated group | Control group | Difference | |||

| +39.56243 | +31.91209 | 7.65033 | |||

| Changes in CER mean before and after policy | Non-State-owned enterprises | ||||

| Treated group | Control group | Difference | |||

| +44.55052 | +28.14369 | 16.40683 | |||

| Items | (1) | (2) | (3) |

|---|---|---|---|

| CER | CER | CER | |

| Treat × PL | 25.33 *** (25.25) | 9.726 *** (9) | 9.522 *** (8.67) |

| _cons | 16.32 *** (45.24) | 10.02 ** (2.26) | −59.23 *** (−3.99) |

| Control variables | no | no | yes |

| Time fixed effects | no | yes | yes |

| Individual fixed effects | no | yes | yes |

| N | 4140 | 4140 | 4140 |

| R-sq | 0.110 | 0.667 | 0.670 |

| Items | (1) | (2) |

|---|---|---|

| CER | CER | |

| Treat × year2004 | −1.140 | −1.002 |

| (−0.630) | (−0.560) | |

| Treat × year2005 | −1.140 | −0.919 |

| (−0.63) | (−0.52) | |

| Treat × year2006 | −0.502 | −0.564 |

| (−0.26) | (−0.30) | |

| Treat × year2007 | omitted | omitted |

| Treat × year2008 | 22.550 *** | 22.420 *** |

| (9.90) | (9.88) | |

| Treat × year2009 | 15.450 *** | 15.340 *** |

| (6.900) | (6.850) | |

| Treat × year2010 | 1.760 | 1.587 |

| (0.71) | (0.64) | |

| Treat × year2011 | 5.860 * | 5.662 * |

| (2.31) | (2.27) | |

| Treat × year2012 | −0.468 | −0.579 |

| (−0.18) | (−0.23) | |

| Constant term | 10.800 * | −48.390 *** |

| (2.13) | (−4.20) | |

| Control variables | no | yes |

| Time fixed effects | yes | yes |

| Individual fixed effects | yes | yes |

| N | 4140 | 4140 |

| R-sq | 0.679 | 0.682 |

| Items | (1) | (2) | (3) |

|---|---|---|---|

| CER | MNG | CER | |

| Treat × PL | 9.357 *** | 0.281 *** | 9.046 *** |

| (8.52) | (4.36) | (8.25) | |

| MNG | 1.110 *** | ||

| (2.97) | |||

| Constant term | −62.360 *** | −0.282 | −62.050 *** |

| (−4.19) | (−0.37) | (−4.18) | |

| Control variables | yes | yes | yes |

| Time fixed effects | yes | yes | yes |

| Individual fixed effects | yes | yes | yes |

| N | 4140 | 4140 | 4140 |

| R-sq | 0.672 | 0.277 | 0.673 |

| Items | (1) | (2) | (3) |

|---|---|---|---|

| CER | Patent | CER | |

| Treat × PL | 9.357 *** | 79.980 *** | 8.997 *** |

| (8.52) | (3.76) | (8.15) | |

| Patent | 0.005 *** | ||

| (3.21) | |||

| Constant term | −62.360 *** | −843.900 *** | −56.020 *** |

| (−4.19) | (−5.98) | (−4.76) | |

| Control variables | Yes | yes | yes |

| Time fixed effects | Yes | yes | yes |

| Individual fixed effects | Yes | yes | yes |

| N | 4140 | 4140 | 4140 |

| R-sq | 0.672 | 0.707 | 0.673 |

| Items | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) |

|---|---|---|---|---|---|---|---|---|---|

| 10th CER | 20th CER | 30th CER | 40th CER | 50th CER | 60th CER | 70th CER | 80th CER | 90th CER | |

| Treat × PL | 15.00 *** | 27.50 *** | 35.00 *** | 33.52 *** | 23.27 *** | 17.9 *** | 13.44 *** | 9.56 *** | 10.99 *** |

| (0.416) | (0.129) | (0.133) | (1.544) | (2.042) | (1.672) | (1.842) | (1.888) | (1.977) | |

| Constant term | 0 | 0 | 0 | −23.63 ** | −90.50 *** | −126.80 *** | −144.70 *** | −142.50 *** | −111.50 *** |

| (2.124) | (0.659) | (0.676) | (7.881) | (10.420) | (8.532) | (9.402) | (9.639) | (10.090) | |

| Control variables | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Time fixed effects | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| Individual fixed effects | yes | yes | yes | yes | yes | yes | yes | yes | yes |

| N | 4140 | 4140 | 4140 | 4140 | 4140 | 4140 | 4140 | 4140 | 4140 |

| Pseudo R2 | 0.0149 | 0.0658 | 0.0982 | 0.1242 | 0.2028 | 0.2608 | 0.2337 | 0.1885 | 0.1489 |

| Items | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| 20th Scale | 40th Scale | 60th Scale | 80th Scale | 100th Scale | |

| Treat × PL | 4.578 | 3.403 | 7.706 *** | 11.48 *** | 1.69 |

| (0.81) | (0.77) | (3.55) | (5.71) | (0.83) | |

| Constant term | 2.318 | −10.29 * | −2.53 | 7.578 | 8.182 ** |

| (0.56) | (−1.77) | (−0.57) | (1.27) | (2.06) | |

| Control variables | yes | yes | yes | yes | yes |

| Time fixed effects | yes | yes | yes | yes | yes |

| Individual fixed effects | yes | yes | yes | yes | yes |

| N | 828 | 828 | 828 | 828 | 828 |

| R-sq | 0.543 | 0.65 | 0.668 | 0.703 | 0.767 |

| Items | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| CER (SOEs) | CER (SOEs) | CER (NSOEs) | CER (NSOEs) | |

| Treat× PL | 7.499 *** | 6.911 *** | 16.300 *** | 15.290 *** |

| (6.03) | (5.61) | (6.15) | (5.87) | |

| Constant term | 10.410 * | −80.470 *** | 4.050 | −71.060 *** |

| (2.25) | (−5.34) | (0.80) | (−3.90) | |

| Control variables | no | yes | no | yes |

| Time fixed effects | yes | yes | yes | yes |

| Individual fixed effects | yes | yes | yes | yes |

| N | 3080 | 3080 | 1060 | 1060 |

| R-sq | 0.674 | 0.681 | 0.672 | 0.677 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, Y.; Failler, P.; Chen, L. Can Mandatory Disclosure Policies Promote Corporate Environmental Responsibility?—Quasi-Natural Experimental Research on China. Int. J. Environ. Res. Public Health 2021, 18, 6033. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph18116033

Liu Y, Failler P, Chen L. Can Mandatory Disclosure Policies Promote Corporate Environmental Responsibility?—Quasi-Natural Experimental Research on China. International Journal of Environmental Research and Public Health. 2021; 18(11):6033. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph18116033

Chicago/Turabian StyleLiu, Yue, Pierre Failler, and Liming Chen. 2021. "Can Mandatory Disclosure Policies Promote Corporate Environmental Responsibility?—Quasi-Natural Experimental Research on China" International Journal of Environmental Research and Public Health 18, no. 11: 6033. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph18116033