Financial Inclusion Paradigm Shift in the Postpandemic Period. Digital-Divide and Gender Gap

Abstract

:1. Introduction

- 1.

- Identifying the factors that influence the increase of access to use digitization facilities for payments and savings.

- 2.

- Analysis of the evolution of bank account holders, as the main form of facilitating the expansion of current online payments, respectively the degree of banking of the payment system, and presentation of differences depending on various attributes—level of economic development, population categories, including gender approach.

- 3.

- Establishing the impact of the pandemic crisis on the demand and supply of online payments, respectively of financial inclusion, after a year of pandemic, and some estimates of the increase of postpandemic bank account holders.

- 4.

- Identifying the potential for increasing financial inclusion through companies’ social responsibility (CSR) in small and medium private companies in emerging economies.

- 5.

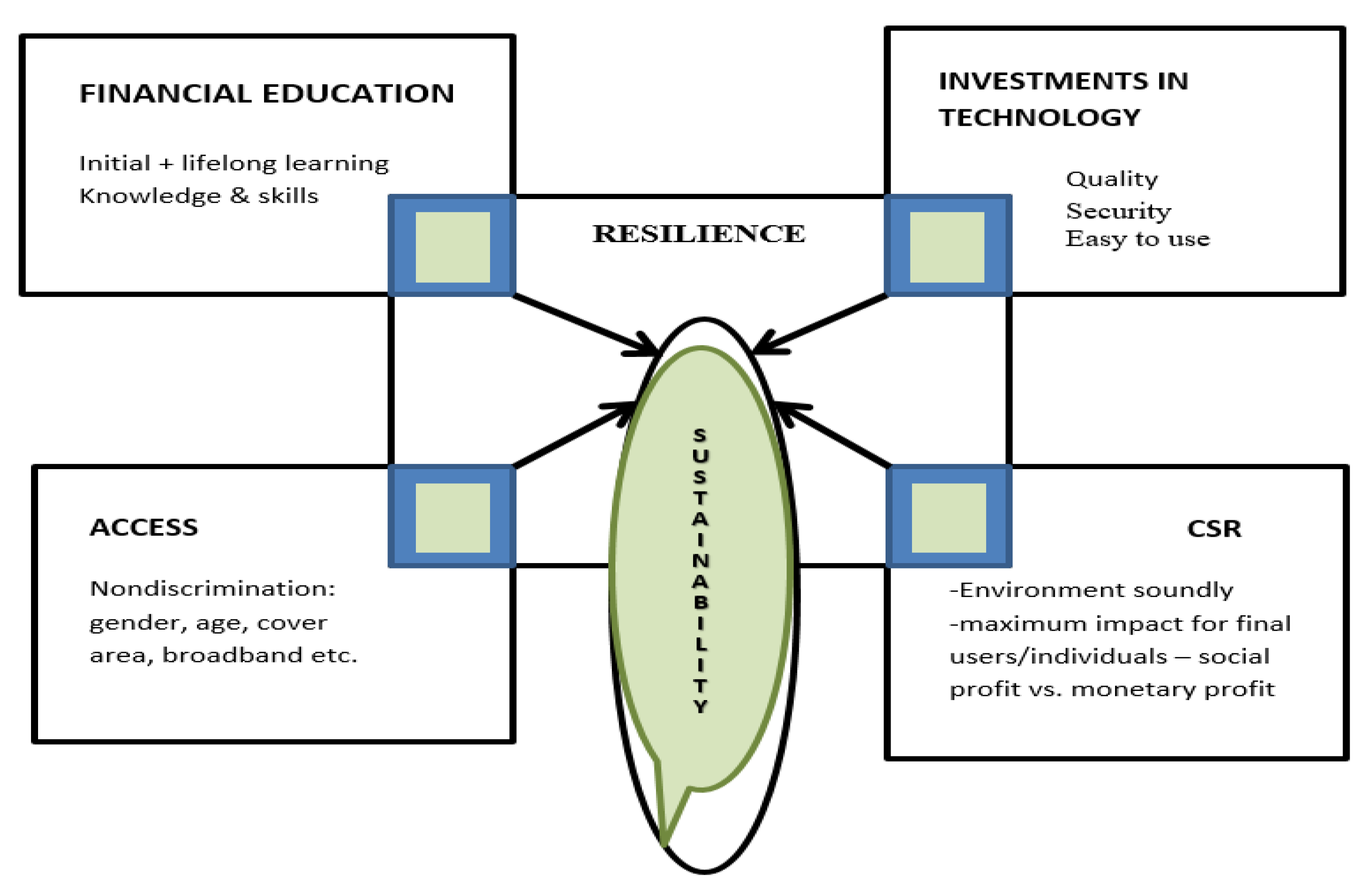

- Establishing the minimum coordinates necessary for the wide promotion of financial inclusion, as a pillar of the quality of life after the pandemic. Starting from the analysis of inequality of access to financial instruments in recent years, of use of specific products/services, from the information asymmetry to support financial inclusion and from the challenges of the pandemic period, we identified the main coordinates of changing the model of financial inclusion—based on five pillars—access, education, support tools, CSR and resilience.

2. Literature Review

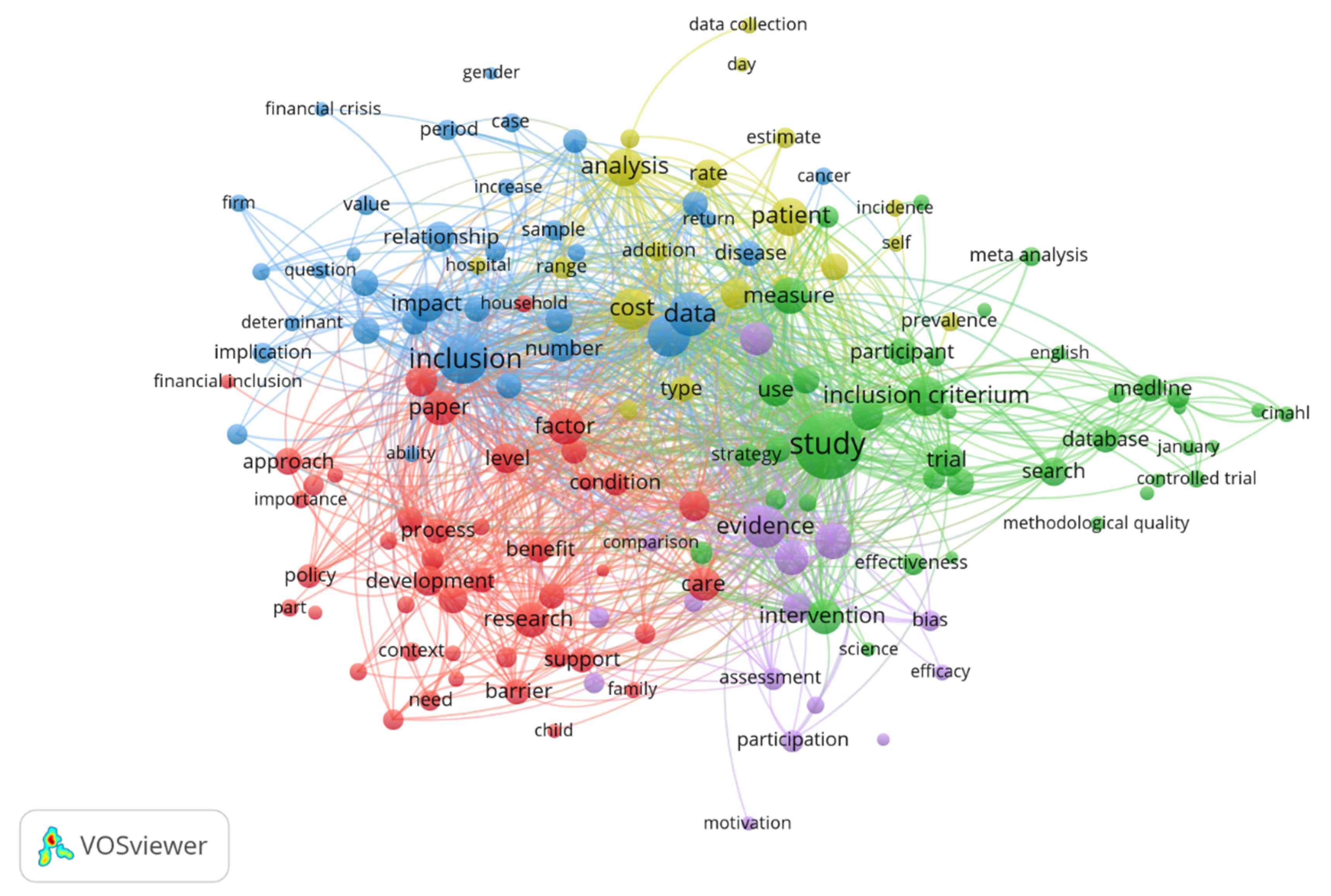

3. A Bibliometric Analysis on Financial Inclusion

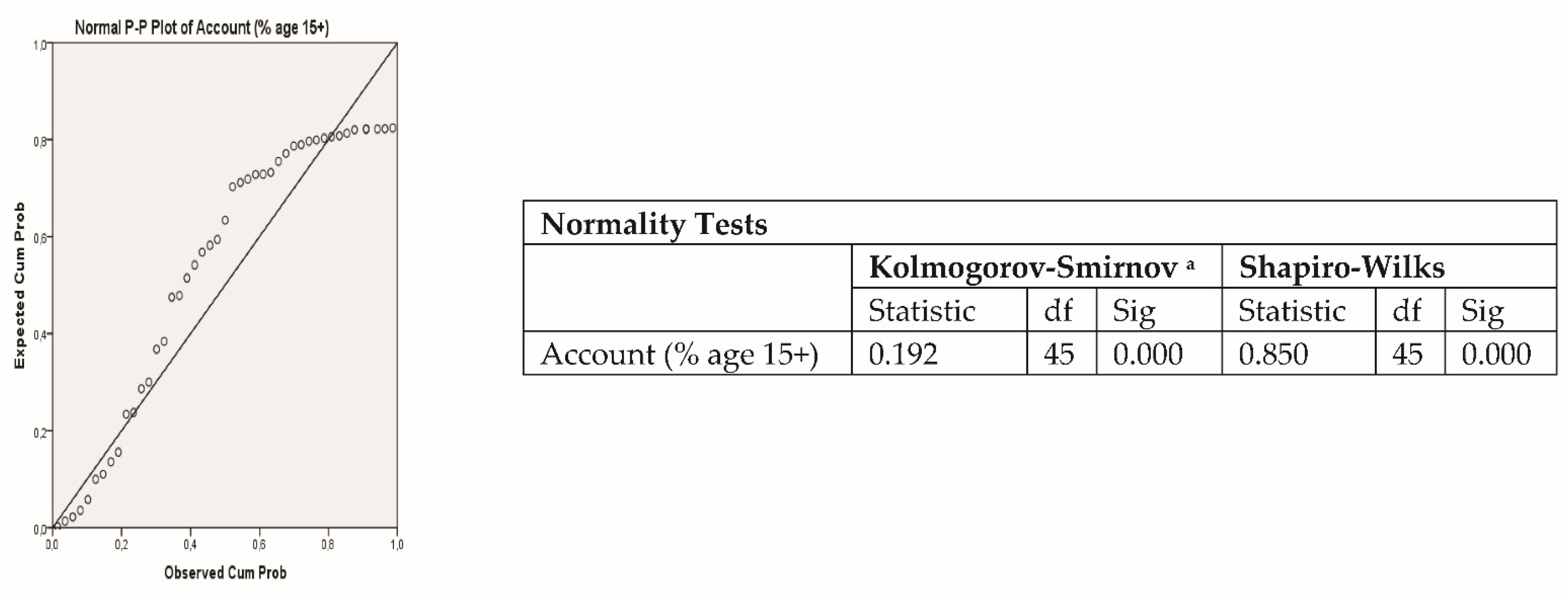

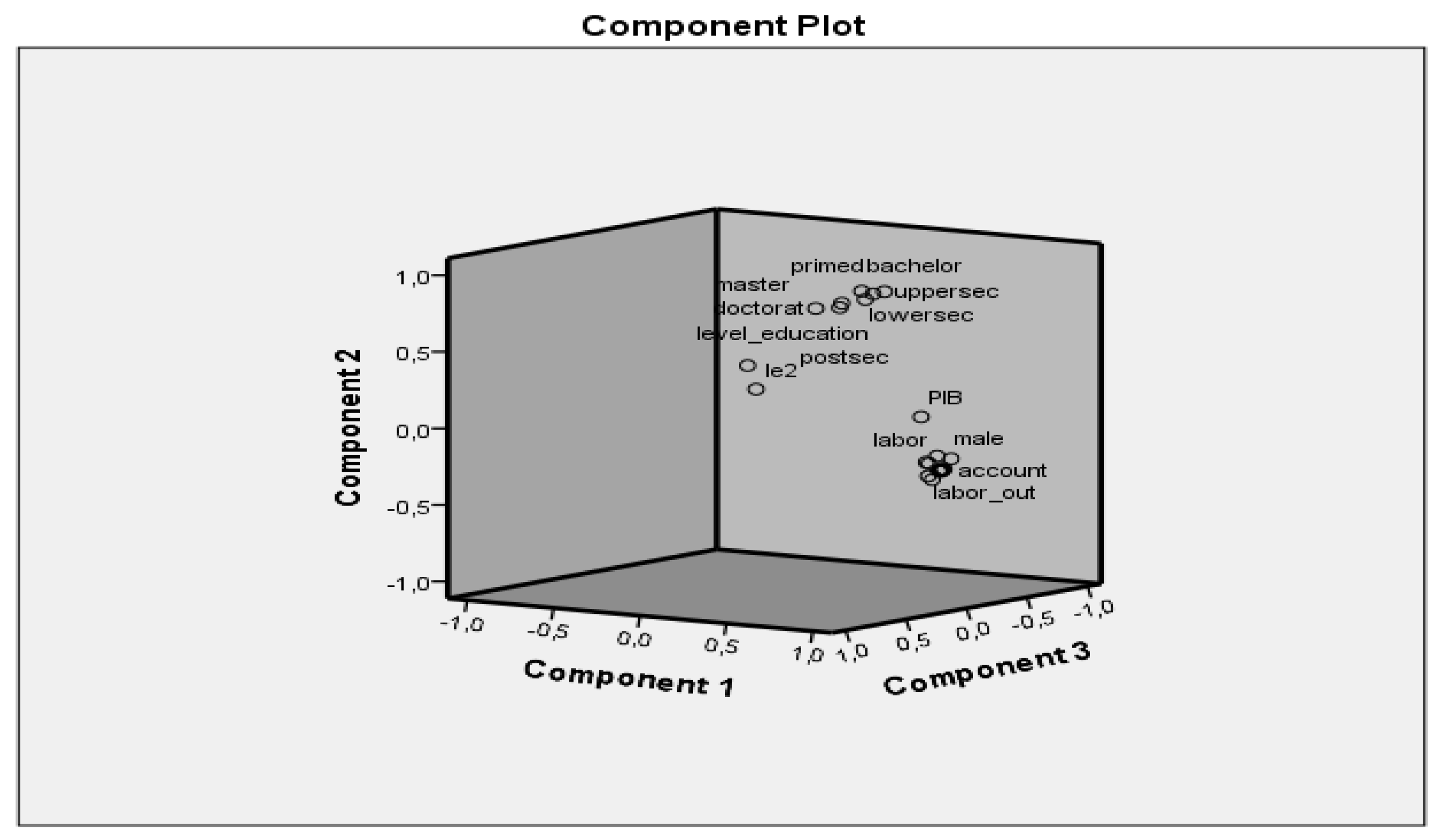

4. Data and Methodology

- The way PCA separates information and reduces the size of the data;

- That PCA is a versatile and handy method [95]:

- That PCA is a powerful technique for data transformation;

- That this method is useful wherever high-dimensional data sets are encountered it before further analytical work.

5. Results

5.1. Dynamics of Financial Inclusion in the Last Decade, Based on Transaction Banking and Digitization, Using the Findex Database

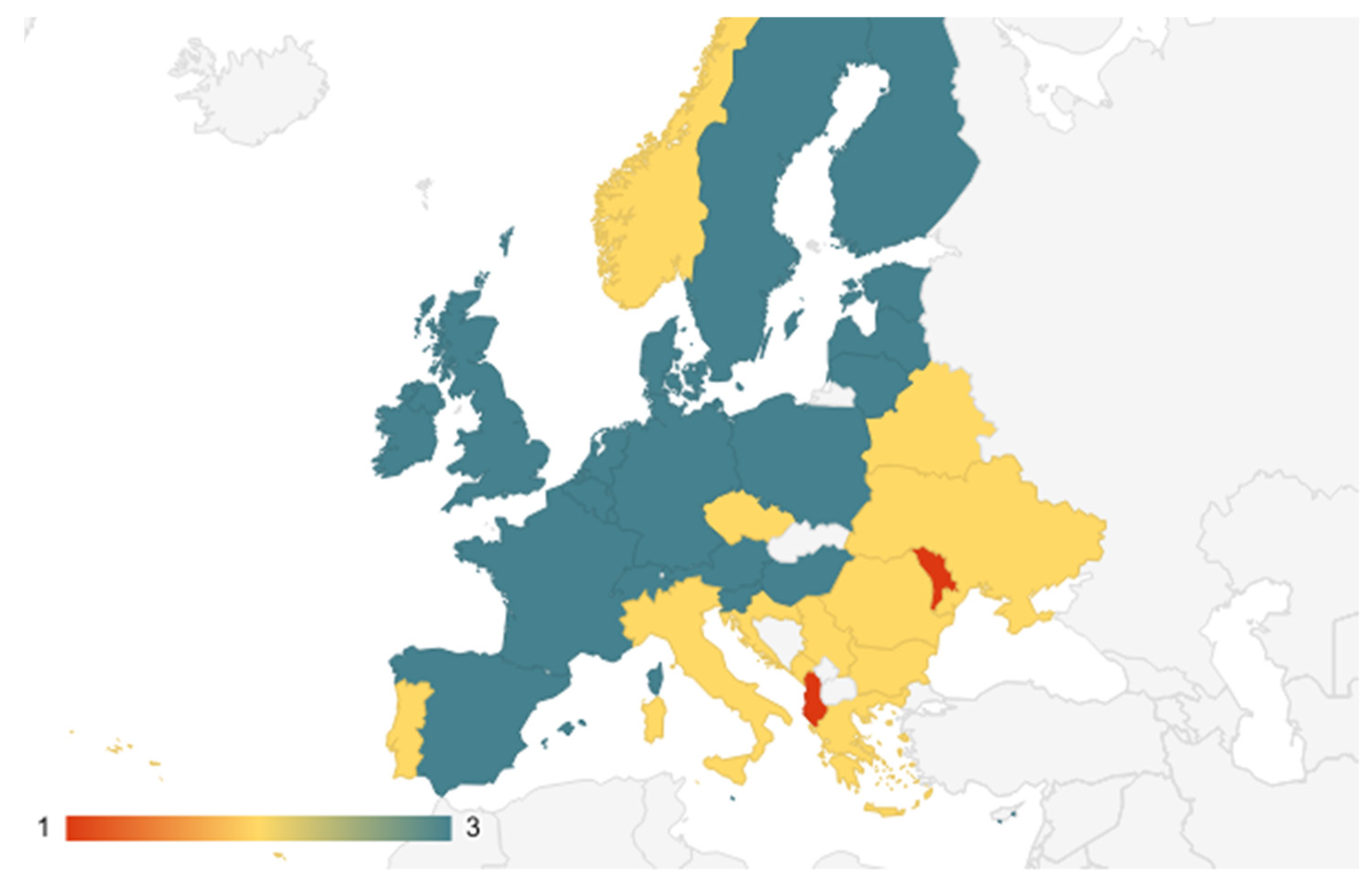

- Cluster 1: Albania, Azerbaijan, Moldova;

- Cluster 2: Armenia, Bulgaria, Bosnia, Belarus, Georgia, Croatia, Macedonia, Montenegro, Romania, Russia, Turkey, Ukraine, Kosovo, Czech Republic, Italy, Norway, Portugal;

- Cluster 3: Austria, Belgium, Switzerland, Cyprus, Germany, Denmark, Spain, Estonia, Finland, France, UK, Hungary, Ireland, Israel, Lithuania, Luxembourg, Latvia, Malta, the Netherlands, Poland, Slovak Republic, Slovenia, Sweden (Figure 5).

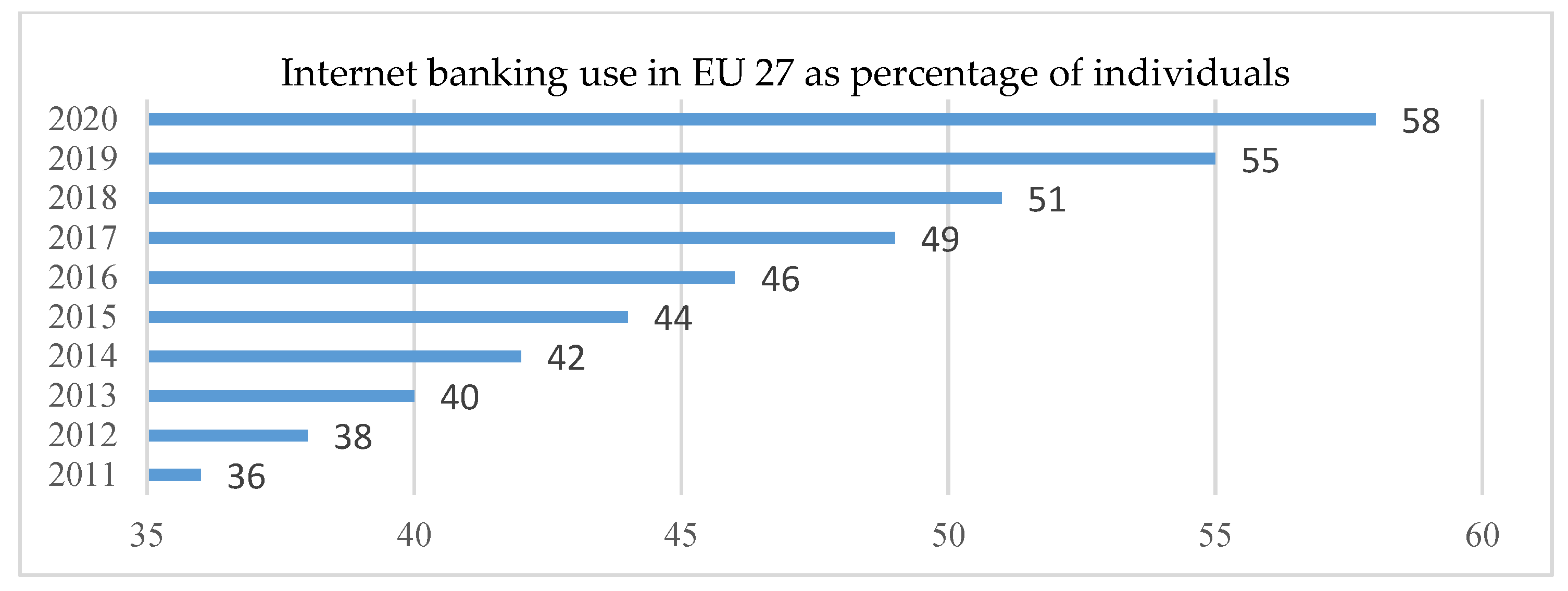

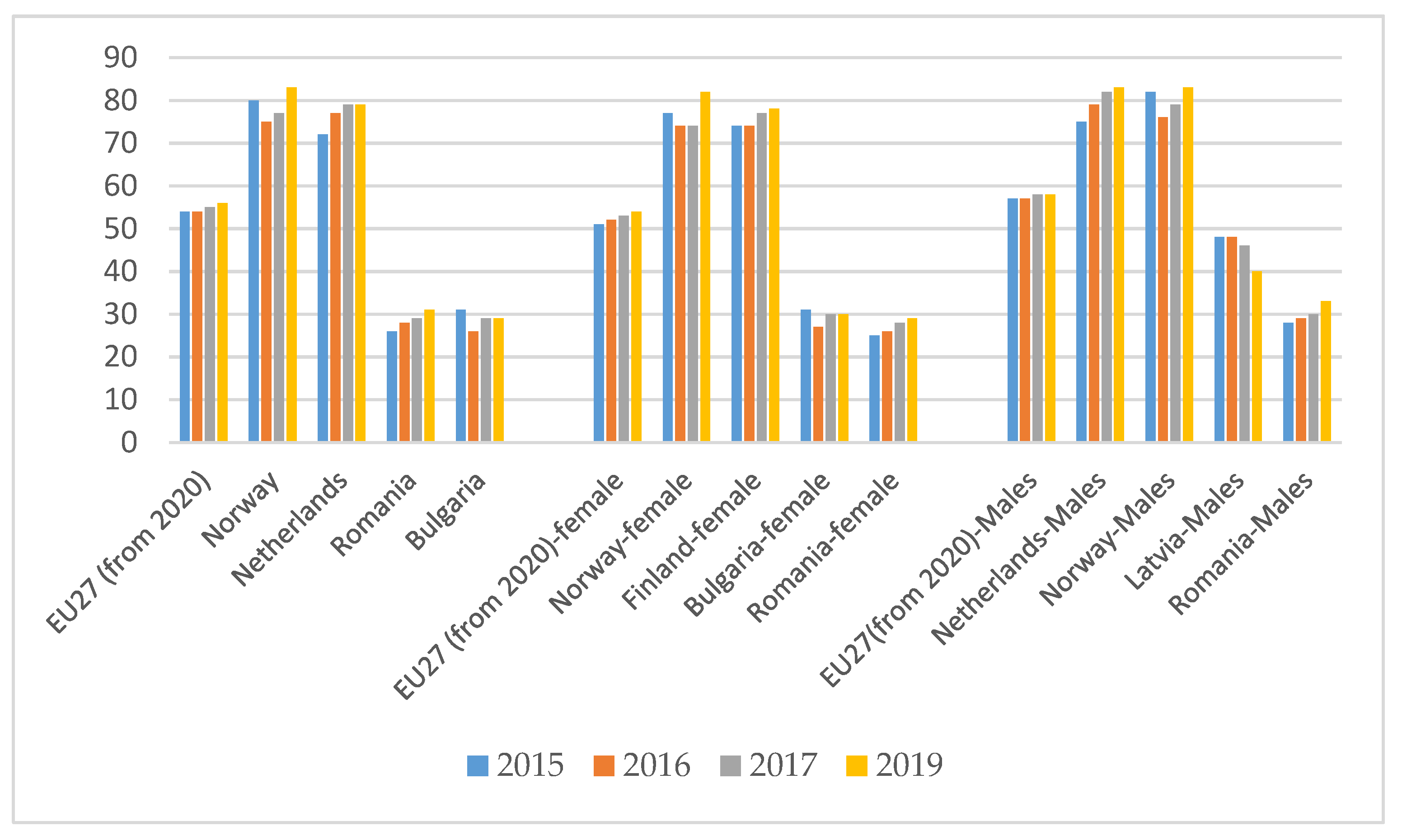

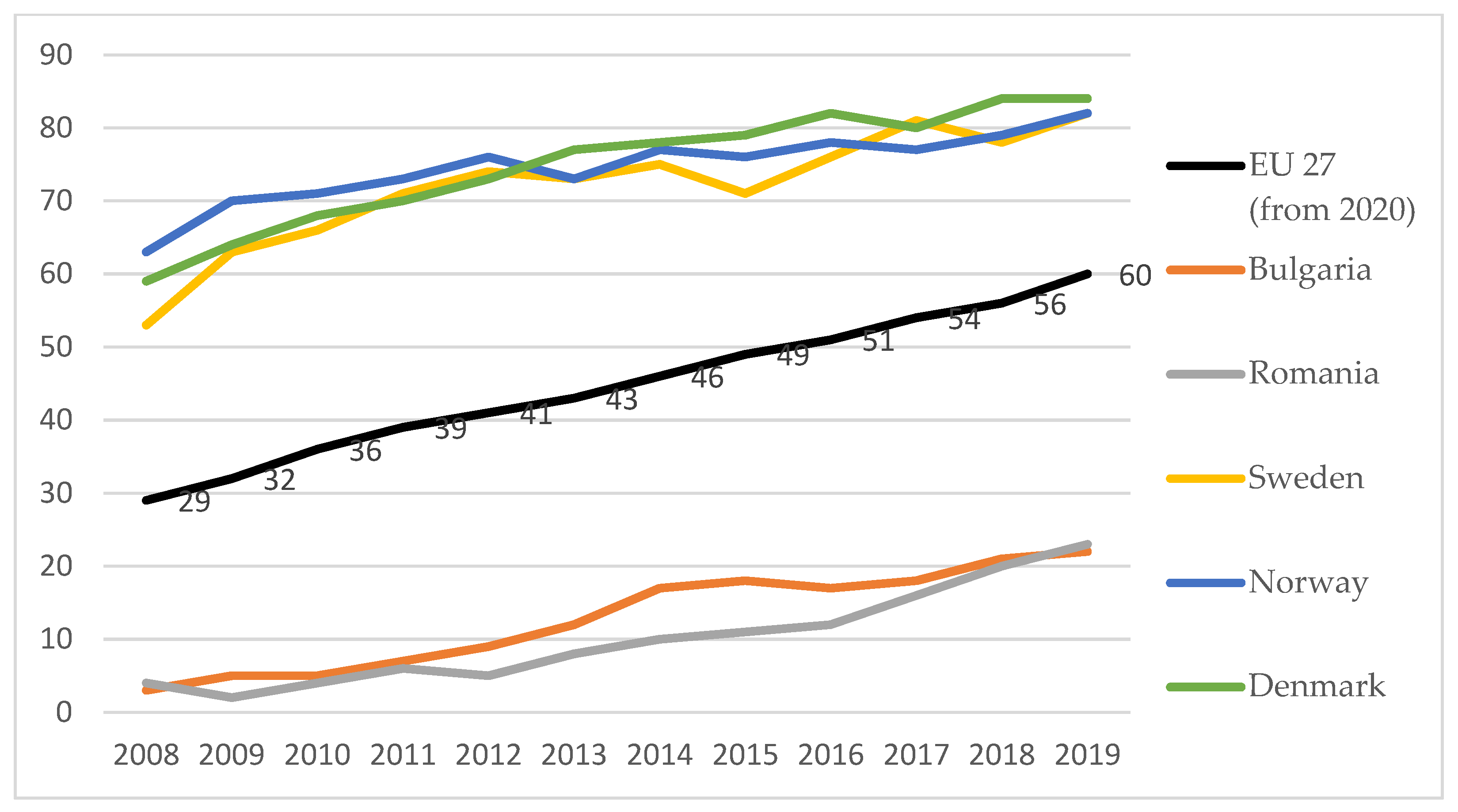

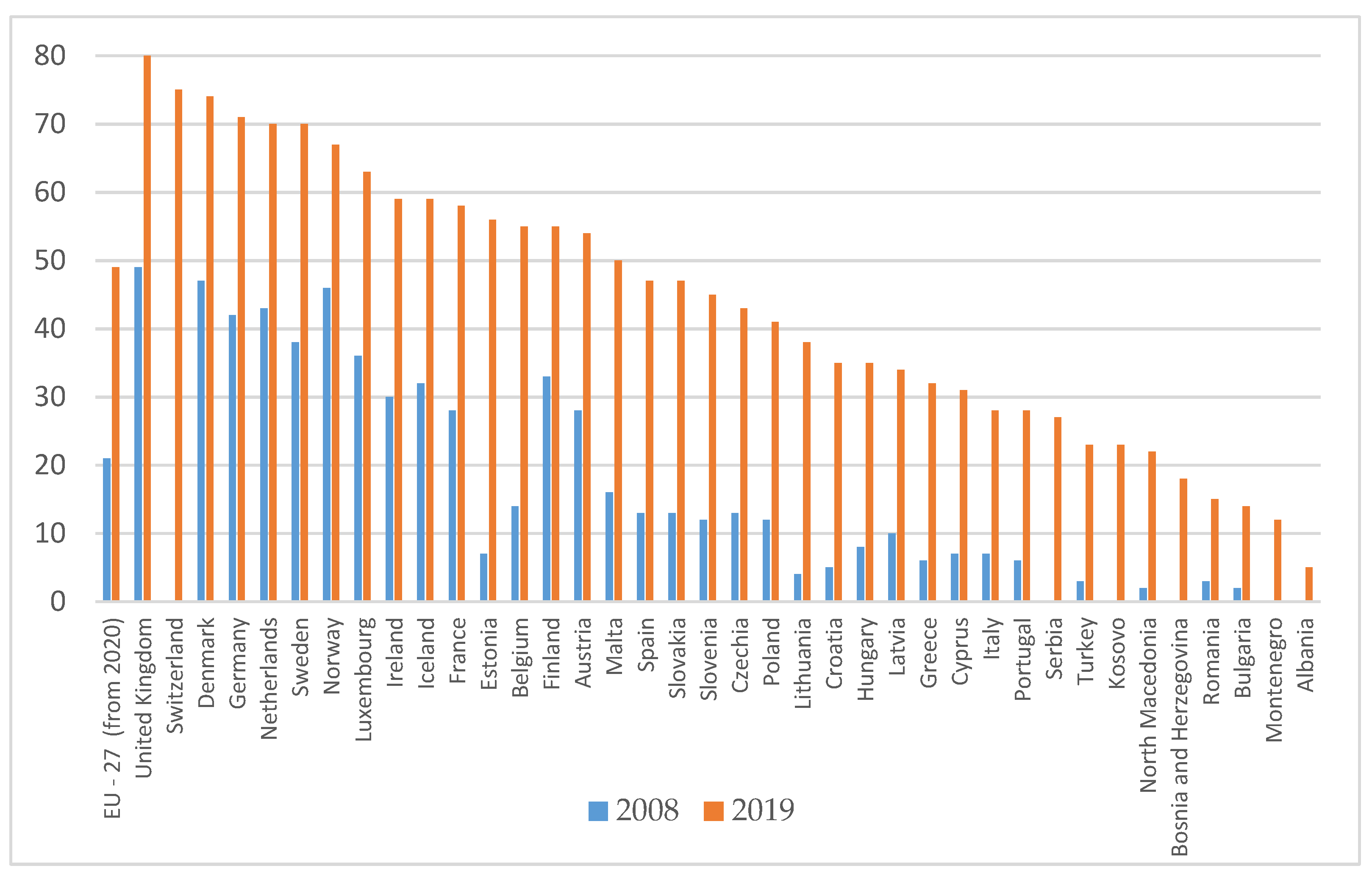

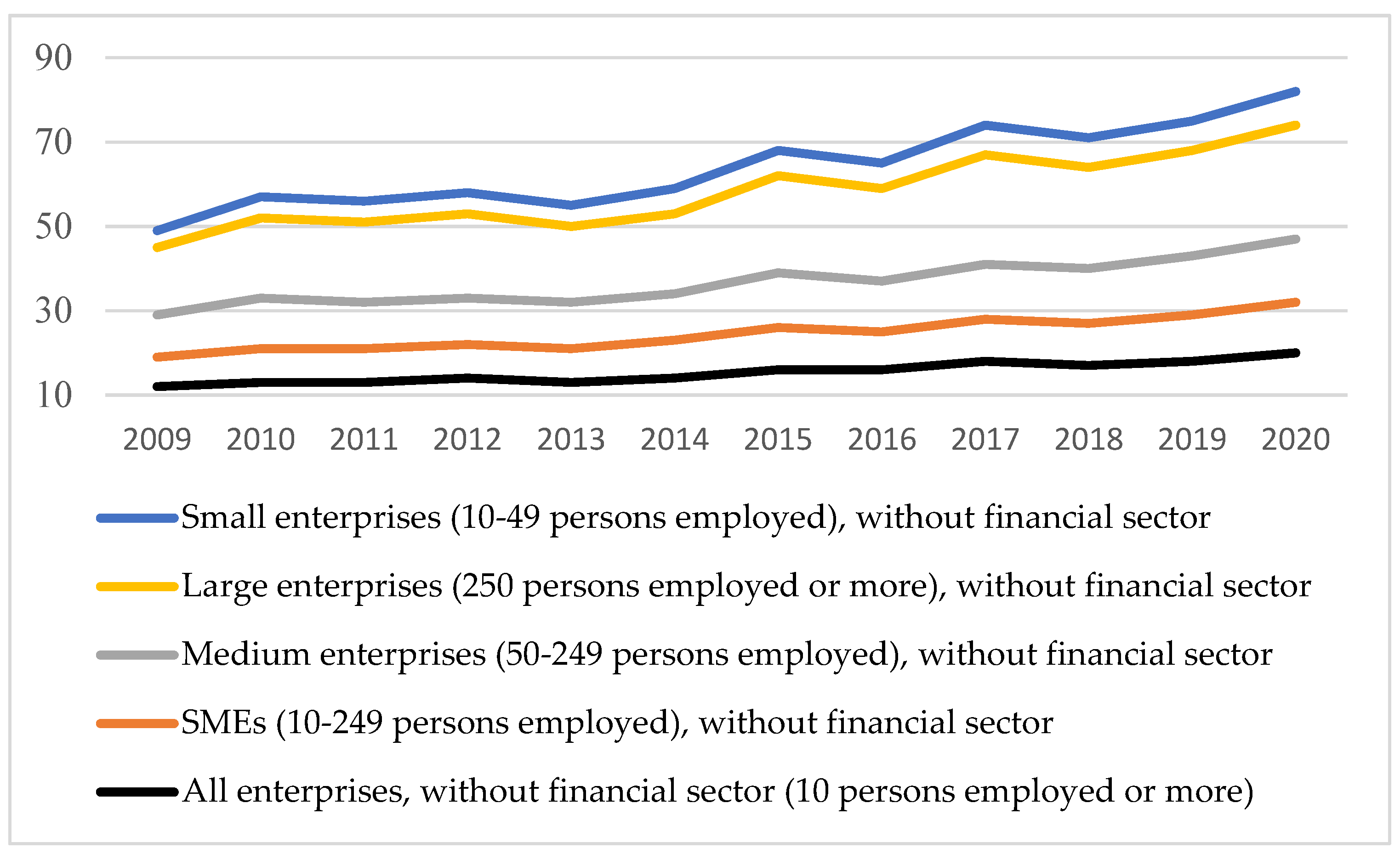

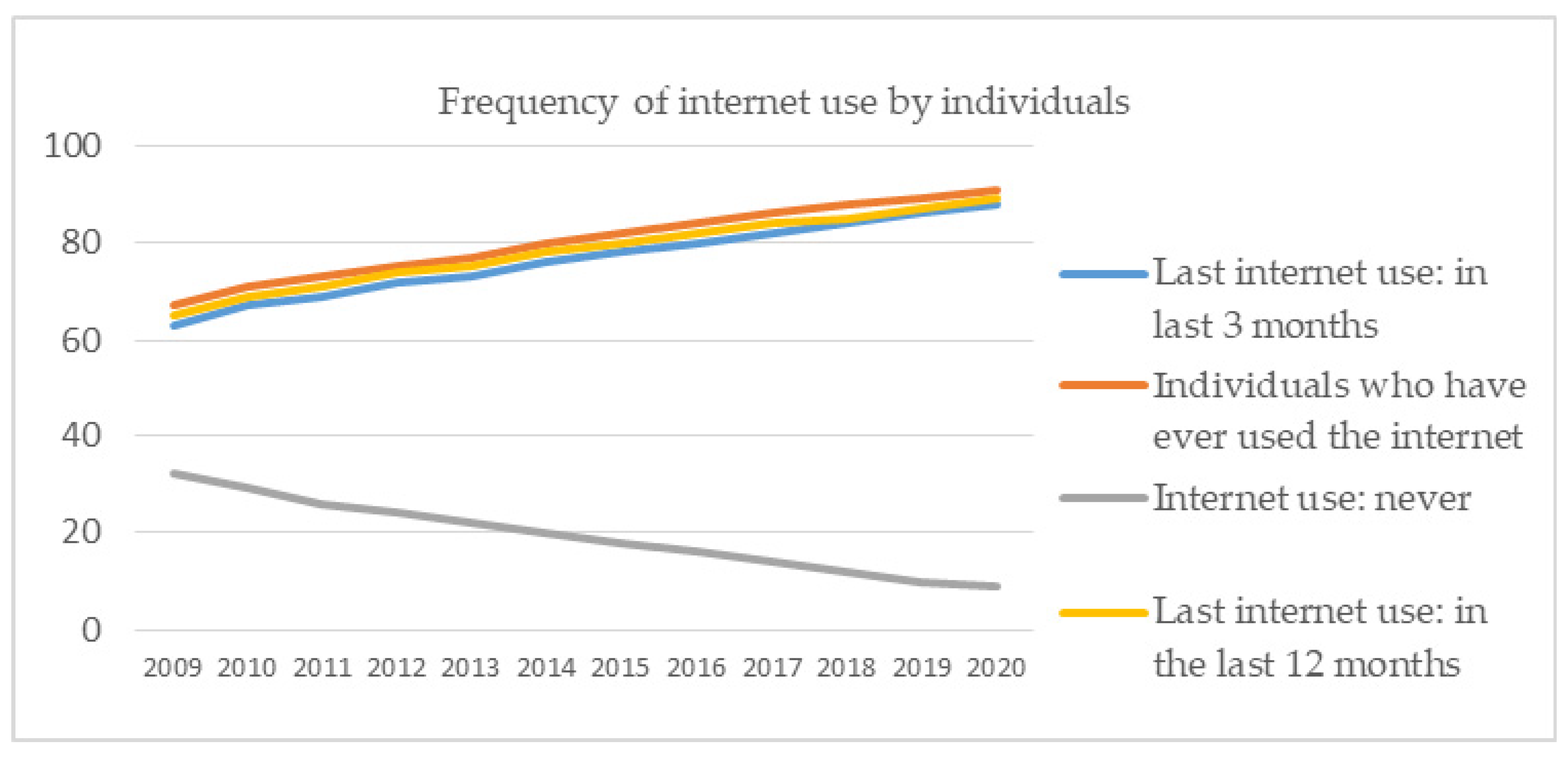

5.2. Aspects of Forced Digital Financial Inclusion in the First Year of the Pandemic. The Gaps Persist. An Analysis Using Eurostat Data

6. Discussion

6.1. Some General Outcomes

- The social responsibility of corporations (banks) that carry out financial education programs and have an ethical behavior towards consumers. We have in mind the social ethics that aims to increase citizens’ access to digital financial services by attracting as many citizens as possible to the formal economy and the official banking system;

- The institutional social responsibility of central banks and consumer protection authorities, which creates the necessary legal framework for increasing citizens’ access to banking services and products and sanctions the unethical behavior of banks towards customers;

- The social responsibility of consumers who show openness to the accumulation of new knowledge and skills given the major changes in the financial market under the sign of financial innovation and digitalization. The need to increase the degree of financial inclusion should not turn into a favored factor for money laundering and terrorist financing. For this reason, the different categories of stakeholders involved (consumers, financial institutions, public authorities) have a common responsibility to create a sound framework, promote secure financial products and use banking products and services in good faith [15,17,21]. Promoting social responsibility can also take the form of partnerships (1) between credit institutions and companies to provide financial education programs for employees of large companies (these programs may target savings and investment programs to ensure financial comfort in old age, with retirement from professional life), and (2) between banks and educational institutions to lay the foundations of responsible financial behavior from childhood.

- Digitalization will be accentuated insofar as the security of transactions increases and in the trust towards the transaction partners;

- The financial education of the individuals will change the business model of the banks and, in general, of the financiers or of the suppliers of goods and services, obliging towards social responsibility, in its various forms;

- Resilience will be the basic component in building the development strategies of companies and households;

- Discrimination in access will be reduced—whether it is discrimination of territorial area, costs, vulnerability (involvement of young people, women, low-income people, etc.).

6.2. Theoretical and Practical Implications

- −

- Improving the digital competencies of consumers considering the separation of black swan type events (such as the COVID-19 crisis) which requires the use of home banking services;

- −

- Modeling the behavior of consumers who face, on the one hand, the increase in the complexity of specific products as a result of the intensification of financial innovation and, on the other hand, with technical challenges generated by digitalization;

- −

- Increasing the responsibility of credit institutions towards consumers who should be treated as equal partners, despite the asymmetry of information and financial power specific to the banking market;

- −

- Limiting the threats posed by cyberattacks, money laundering and terrorist financing.

7. Conclusions

- Significant differences between countries from the perspective of the degree of banking transactions at the level of individuals, caused by both financial education and support infrastructure (access to digitization facilities, offer of financial services, cost of banked transactions, etc.).

- The preponderance of SMEs in the business environment and the CSR weaknesses at their level or the lack of concerns in this respect, with direct effects on the financial inclusion of employees.

- The main factors influencing the increase of access to the use of digitization facilities for payments and savings identified by the analysis were access to internet, level of studies, gender, employment characteristics and level of development.

- The limitation of some activities during the pandemic period reorganized the model of consumer transactions, both for individuals and for a large part of companies. After a year of pandemic, the bank account holders rescued, but limited, depending on the accessibility to the online banking system. Likewise, many small and medium-sized companies have digitized their collection and payment operations with the development of online commerce.

- The financial education in the pandemic represented especially a fortuitous information and options for adapting to online payments, according to the current offer, without the possibility of options based on rational choices of financial efficiency. Banks and companies have promoted their “adaptation” offers and the population has had few alternatives to choose from. Likewise, the employees of the small private firms, accustomed to cash payments in the relationship with the employer, were forced to switch to the use of debit cards, and for banking operations to access the online services of saving, payments, credit.

- From the perspective of promoting financial inclusion through CSR in SMEs we can identify some major changes at the company level, namely (a) greater use of social support tools for employees, e.g., accessing the financing of pandemic employment from special funds, developed at national level, flexibility of working time, use of banking instruments for payment of salaries, etc., and (b) computerization of production and distribution processes and hence change of job requirements including digital skills, use online communication devices, teleworking, etc.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- UFA. 2020 Overview: Universal Financial Access by 2020, World Bank. Available online: https://www.worldbank.org/en/topic/financialinclusion/brief/achieving-universal-financial-access-by-2020 (accessed on 8 June 2021).

- World Bank. World Development Report 2021: Data for Better Lives; License: CC BY 3.0 IGO; World Bank: Washington, DC, USA, 2021; Available online: https://openknowledge.worldbank.org/handle/10986/35218 (accessed on 9 June 2021).

- Khera, P.; Ng, S.; Ogawa, S.; Sahay, R. Is digital financial inclusion unlocking growth? IMF Work. Pap. 2021, 2021, 167. Available online: https://www.imf.org/en/Publications/WP/Issues/2021/06/11/Is-Digital-Financial-Inclusion-Unlocking-Growth-460738 (accessed on 7 June 2021).

- Moore, D.; Niazi, Z.; Rouse, R.; Kramer, B. Building Resilience through Financial Inclusion: A Review of Existing Evidence and Knowledge Gaps. Innovations for Poverty Action. 2019. Available online: https://www.poverty-action.org/publication/building-resilience-through-financial-inclusion-review-existing-evidence-and-knowledge (accessed on 5 June 2021).

- FATF. Anti-Money Laundering and Terrorist Financing Measures and Financial Inclusion. 2017. Available online: https://www.fatf-gafi.org/media/fatf/content/images/Updated-2017-FATF-2013-Guidance.pdf (accessed on 25 June 2021).

- Barajas, A.; Beck, T.; Belhaj, M.; Naceur, S.B.; Cerra, V.; Qureshi, M.S. Financial inclusion: What have we learned so far? What do we have to learn? IMF Work. Pap. 2020, 157, 51. [Google Scholar] [CrossRef]

- Mhlanga, D. Artificial intelligence in the industry 4.0, and its impact on poverty, innovation, infrastructure development, and the sustainable development goals: Lessons from emerging economies? Sustainability 2021, 13, 5788. [Google Scholar] [CrossRef]

- Arunachalam, R.S.; Crentsil, G.L. Financial Inclusion in the Era of COVID-19. In An Online Participative Conference for Central Bankers, Ministries of Finance, Financial Sector Development & Financial Inclusion Professionals, Commercial & Microfinance Bankers, NBFIs, DFIs, MFIs, Consultants, FINTECH & RegTech Companies, Investors, Ins; The Financial Inclusion Advocacy Centre: Kent, UK, 2020. [Google Scholar]

- Lutfi, A.; Al-Okaily, M.; Alshirah, M.H.; Alshira’h, A.F.; Abutaber, T.A.; Almarashdah, M.A. Digital financial inclusion sustainability in Jordanian context. Sustainability 2021, 13, 6312. [Google Scholar] [CrossRef]

- Lotfi, A.; Salehi, M.; Dashtbayaz, M.L. The effect of intellectual capital on fraud in financial statements. TQM J. 2021. Available online: https://0-www-emerald-com.brum.beds.ac.uk/insight/content/doi/10.1108/TQM-11-2020-0257/full/html?casa_token=5vXDtJJydkUAAAAA:JuBf0bsEZ869BuPaP9FubM-rhpMNDHcOVZ7P44_Sq0rVAU8wael3OUcOupSLHTOrilzoRnEprLiJMdgxQCaxqxycgunz9VURWoge-Cu9wDcuK0DGJdE (accessed on 22 June 2021).

- CGAP. Annual Report. 2020. Available online: https://www.cgap.org/sites/default/files/minisites/annualReport_2020/index.html (accessed on 22 June 2021).

- Gerard, F.; Imbert, C.; Orkin, K. Social protection response to the COVID-19 crisis: Options for developing countries. Oxf. Rev. Econ. Policy 2020, 36, S281–S296. [Google Scholar] [CrossRef]

- Aidukaite, J.; Saxonberg, S.; Szelewa, D.; Szikra, D. Social policy in the face of a global pandemic: Policy responses to the COVID-19 crisis in Central and Eastern Europe. Soc. Policy Adm. 2021, 55, 358–373. [Google Scholar] [CrossRef] [PubMed]

- Cantillon, B.; Seeleib-Kaiser, M.; van der Veen, R. The COVID-19 crisis and policy responses by continental European welfare states. Soc. Policy Adm. 2021, 55, 326–338. [Google Scholar] [CrossRef] [PubMed]

- Panait, M.; Radulescu, I.; Brezoi, A. Financial markets—Under the sign of CSR. Some evidences regarding financial education. LUMEN Proc. 2020, 11, 96–106. [Google Scholar]

- Loo, M.K.L. Enhancing financial inclusion in ASEAN: Identifying the best growth markets for fintech. J. Risk Financ. Manag. 2019, 12, 181. [Google Scholar] [CrossRef] [Green Version]

- Ma’ruf, A.; Aryani, F. Financial inclusion and achievements of sustainable development goals (SDGs) in ASEAN. J. Bus. Econ. Rev. 2020, 4, 147–155. [Google Scholar] [CrossRef]

- Siano, A.; Raimi, L.; Palazzo, M.; Panait, M. Mobile banking: An innovative solution for increasing financial inclusion in Sub-Saharan African countries. evidence from Nigeria. Sustainability 2020, 12, 10130. [Google Scholar] [CrossRef]

- Grazioli, J.; Lloyd, G.; Panziera, L.; Hoyle, C.R.; Connolly, P.J.; Henneberger, J.; Berne, A. Polarimetric radar and in situ observations of riming and snowfall microphysics during CLACE 2014. Atmos. Chem. Phys. 2015, 15, 13787–13802. [Google Scholar] [CrossRef] [Green Version]

- Kim, D.W.; Yu, J.S.; Hassan, M.K. Financial inclusion and economic growth in OIC countries. Res. Int. Bus. Financ. 2018, 43, 1–14. [Google Scholar] [CrossRef]

- Voica, M.C. Financial inclusion as a tool for sustainable development. Rom. J. Econ. 2017, 44, 121–129. [Google Scholar]

- Abor, J.Y.; Amidu, M.; Issahaku, H. Mobile telephony, financial inclusion and inclusive growth. J. Afr. Bus. 2018, 19, 430–453. [Google Scholar] [CrossRef]

- Bayar, Y.; Gavriletea, M.D.; Paun, D. Impact of mobile phones and internet use on financial inclusion: Empirical evidence from the EU post-communist countries. Technol. Econ. Dev. Econ. 2018, 27, 722–741. [Google Scholar] [CrossRef]

- Iacovoiu, V.; Stancu, A. Competition and consumer protection in the romanian banking sector. Amfiteatru Econ. 2017, 19, 381. [Google Scholar]

- Patiño, O.A.; Patiño Gutiérrez, L.M. Financial education and inclusion: The role of banks. Int. J. Sustain. Entrep. Corp. Soc. Responsib. 2019, 4, 57–72. [Google Scholar] [CrossRef]

- Yue, H.; Chang, L.; Jiangang, P. Financial inclusion and agricultural total factor productivity growth in China. Econ. Model. 2021, 96, 68–82. [Google Scholar]

- Manta, O.; Gouliamos, K.; Kong, J.; Li, Z.; Ha, N.M.; Mohanty, R.P.; Yang, H.; Pu, R.; Yue, X.G. The architecture of financial networks and models of financial instruments according to the “Just transition mechanism” at the European level. J. Risk Financ. Manag. 2020, 13, 235. [Google Scholar] [CrossRef]

- Sevim, N.; Temizel, F.; Sayılır, O. The effects of financial literacy on the borrowing behaviour of Turkish financial consumers. Int. J. Consum. Stud. 2012, 36, 573–579. [Google Scholar] [CrossRef]

- Fidrmuc, J.; Hake, M.; Stix, H. Households’ foreign currency borrowing in Central and Eastern Europe. J. Bank. Financ. 2013, 37, 1880–1897. [Google Scholar] [CrossRef] [Green Version]

- Kundid, N.A. Troubles with the CHF loans in Croatia: The story of a case still waiting to be closed. J. Risk Financ. Manag. 2021, 14, 75. [Google Scholar] [CrossRef]

- Apiors, E.K.; Suzuki, A. Mobile money, individuals’ payments, remittances, and investments: Evidence from the Ashanti region, Ghana. Sustainability 2018, 10, 1409. [Google Scholar] [CrossRef] [Green Version]

- Trașcă, D.L.; Ștefan, G.M.; Sahlian, D.N.; Hoinaru, R.; Șerban-Oprescu, G.L. Digitalization and business activity. The struggle to catch up in CEE countries. Sustainability 2019, 11, 2204. [Google Scholar] [CrossRef] [Green Version]

- Aguayo, F.Z.; Ślusarczyk, Z. Risks of banking services’ digitalization: The practice of diversification and sustainable development goals. Sustainability 2020, 12, 4040. [Google Scholar] [CrossRef]

- Pearce, C.; Manz, C.C. Leadership centrality and corporate social irresponsibility (CSIR): The potential ameliorating effects of self and shared leadership on CSIR. J. Bus. Ethics 2011, 102, 563–579. [Google Scholar] [CrossRef]

- Zhao, J.L.; Fan, S.; Yan, J. Overview of business innovations and research opportunities in blockchain and introduction to the special issue. Financ. Innov. 2016, 2, 28. [Google Scholar] [CrossRef] [Green Version]

- Shao, F.; Murrell, A.J.; Zhao, X.; Zhang, K.; Hart, T.A. Understanding the dynamic relationships between CSR and CSIR. J. Strategy Manag. 2021. ahead of print. [Google Scholar] [CrossRef]

- Matei, M.; Voica, M.C. Social responsibility in the financial and banking sector. Econ. Insights Trends Chall. 2013, 65, 115–123. [Google Scholar]

- Raimi, L. Understanding theories of corporate social responsibility in the Ibero-American hospitality industry. Corp. Soc. Responsib. Corp. Gov. Dev. Corp. Gov. Responsib. 2017, 11, 65–88. [Google Scholar]

- Gurtu, A. Recent Advancements in Sustainable Entrepreneurship and Corporate Social Responsibility; IGI Global: Hershey, PA, USA, 2020. [Google Scholar]

- Pérez, A.; Rodríguez-del-Bosque, I. Corporate social responsibility and customer loyalty: Exploring the role of identification, Satisfaction and type of company. J. Serv. Mark. 2015, 29, 15–25. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; García-Meca, E. CSR engagement and earnings quality in banks. The moderating role of institutional factors. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 145–158. [Google Scholar] [CrossRef]

- Boachie, C. Corporate social responsibility and financial performance in the banking industry in Ghana. Int. J. Sustain. Entrep. Corp. Soc. Responsib. 2020, 5, 1121–1133. [Google Scholar] [CrossRef]

- Palazzo, M.; Deigh, L.; Foroudi, P.; Siano, A. How to boost place branding leveraging on community relations: An exploration of the banking sector in Ghana. Qual. Mark. Res. 2020, 23, 933–960. [Google Scholar] [CrossRef] [Green Version]

- Stoian, A.; Vintilă, N.; Iorgulescu, F.; Ciobanu, R.; Cepoi, C.; Manolache, A.E.D.; Draghia, A.E. Financial literacy, risk aversion and financial behaviours: What shapes the preference for capital market participation? In Proceedings of the 3rd International Conference on Economics and Social Sciences, Bucharest, Romania, 15–16 October 2020; pp. 877–884. [Google Scholar]

- Voica, M.C.; Stancu, A. Corporate Social Responsibility Reporting: Background, Evolution and Sustainability Promoter. Sustainable Management for Managers and Engineers; Machado, C.F.J., Davim, P., Eds.; Wiley: Hoboken, NJ, USA, 2021. [Google Scholar]

- Deliema, M.; Shadel, D.; Pak, K. Profiling victims of investment fraud: Mindsets and risky behaviors. J. Consum. Res. 2020, 46, 904–914. [Google Scholar] [CrossRef]

- Lusardi, A.; Hasler, A.; Yakoboski, P. Building up financial literacy and financial resilience. Mind Soc. 2020, 20, 181–187. [Google Scholar] [CrossRef]

- Bălan, M.; Vasile, V. Cultural determinants of economic performance in Romania. Procedia Soc. Behav. Sci. 2015, 188, 290–296. [Google Scholar] [CrossRef] [Green Version]

- Forcadell, F.J.; Aracil, E.; Úbeda, F. The impact of corporate sustainability and digitalization on international banks’ performance. Contemp. Issues Bank. 2020, 11, 18–27. [Google Scholar] [CrossRef]

- Kwilinski, A.; Vyshnevskyi, O.; Dzwigol, H. Digitalization of the EU economies and people at risk of poverty or social exclusion. J. Risk Financ. Manag. 2020, 13, 142. [Google Scholar] [CrossRef]

- Niemand, T.; Rigtering, J.C.; Kallmunzer, A.; Kraus, S.; Maalooui, A. Digitalization in the financial industry: A contingency approach of entrepreneurial orientation and strategic vision on digitalization. Eur. Manag. J. 2020, 39, 317–326. [Google Scholar] [CrossRef]

- Kanungo, R.P.; Gupta, S. Financial inclusion through digitalisation of services for well-being. Technol. Forecast. Soc. Chang. 2021, 167, 120721. [Google Scholar] [CrossRef]

- Lee, H.; Fridlind, A.M.; Ackerman, A.S. An evaluation of size-resolved cloud microphysics scheme numerics for use with radar observations. Part II: Condensation and evaporation. J. Atmos. Sci. 2021, 78, 1629–1645. [Google Scholar]

- Swacha-Lech, M. The main challenges facing the retail banking industry in the era of digitalization. Rozpr. Ubezpieczeniowe Konsument Na Rynk. Usl. Finans. 2017, 4, 94–116. [Google Scholar]

- Calliess, C.; Baumgarten, A. Cybersecurity in the EU the example of the financial sector: A legal perspective. Ger. Law J. 2020, 21, 1149–1179. [Google Scholar] [CrossRef]

- Uddin, A.; Ashraful, M.; Chowdhury, F.; Sajib, S.D.; Masih, M. Revisiting the impact of institutional quality on post-GFC bank risk-taking: Evidence from emerging countries. Emerg. Mark. Rev. 2020, 42, 100659. [Google Scholar] [CrossRef]

- Aldasoro, I.; Eren, E.; Huang, W. Dollar funding of non-US banks through Covid-19. BIS Q. Rev. 2021, March 2021, 31–40. [Google Scholar]

- Yartey, C.A. Financial development, the structure of capital markets, and the global digital divide. Inf. Econ. Policy 2008, 20, 208–227. [Google Scholar] [CrossRef] [Green Version]

- Horne, D.R. Financial Exclusion, Technology, the Digital Divide and Poverty in Responsible Management Education and the Challenge of Poverty; Routledge: Abingdon on Thames, UK, 2016. [Google Scholar]

- Lupo-Pasini, F. Financial inclusion and the ‘War for Cash’. Law Contemp. Probl. 2021, 84, 17–33. Available online: https://ssrn.com/abstract=3801581 (accessed on 13 June 2021).

- Ene, C.; Panait, M. The financial education—Part of corporate social responsibility for employees and customers. Rev. Romana Econ. 2017, 44, 145–154. [Google Scholar]

- Grohmann, A. Financial literacy and financial behavior: Evidence from the emerging Asian middle class. Pac. Basin Financ. J. 2018, 48, 129–143. [Google Scholar] [CrossRef] [Green Version]

- Iacovoiu, V.B. An empirical analysis of some factors influencing financial literacy. Econ. Insights Trends Chall. 2018, 70, 23–31. [Google Scholar]

- Castro, R.; Enríquez-Diaz, J.; García, B. The Role of Financial Education in the Path towards Sustainable Development: A Practical Experience with Students of Secondary Education. In Financial Management and Risk Analysis Strategies for Business Sustainability; IGI Global: Hershey, PA, USA, 2021; pp. 1–19. [Google Scholar]

- Valenzuela, M.; Martínez-Martínez, S.; Soto, J. Financial Literacy and Innovation Performance in SMEs: The Mediating Effect of Risk-Taking. In Financial Management and Risk Analysis Strategies for Business Sustainability; IGI Global: Hershey, PA, USA, 2021; pp. 58–81. [Google Scholar]

- Ansari, A.; Riasi, A. Modelling and evaluating customer loyalty using neural networks: Evidence from startup insurance companies. Future Bus. J. 2016, 2, 15–30. [Google Scholar] [CrossRef] [Green Version]

- Ghazanfari, Z.; Niknami, S.; Ghofranipour, F.; Larijani, B.; Agha-Alinejad, H.; Montazeri, A. Determinants of glycemic control in female diabetic patients: A study from Iran. Lipids Health Dis. 2010, 9, 83. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Zeithaml, V.A.; Rust, R.T.; Lemon, K.N. The customer pyramid: Creating and serving profitable customers. Calif. Manag. Rev. 2001, 43, 118–142. [Google Scholar] [CrossRef]

- Gough, O.; Sozou, P.D. Pensions and retirement savings: Cluster analysis of consumer behaviour and attitudes. Int. J. Bank Mark. 2005, 23, 558–570. [Google Scholar] [CrossRef]

- Neal, A.G. National Trauma and Collective Memory: Major Events in the American Century; M.E. Sharpe: Armonk, NY, USA, 1998. [Google Scholar]

- Cheng, C.H.; Chen, Y.S. Classifying the segmentation of customer value via RFM model and RS theory. Expert Syst. Appl. 2009, 36, 4176–4184. [Google Scholar] [CrossRef]

- Khajvanda, M.; Tarokh, M.J. Estimating customer future value of different customer segments based on adapted RFM model in retail banking context. Procedia Comput. Sci. 2010, 3, 1327–1332. [Google Scholar] [CrossRef] [Green Version]

- Mccarty, J.; Hastak, M. Segmentation approaches in data-mining: A comparison of RFM, CHAID, and logistic regression. J. Bus. Res. 2007, 60, 656–662. [Google Scholar] [CrossRef]

- Wei, L.H.; Keto, E.; Ho, L.C. Two populations of molecular clouds in the Antennae galaxies. Astrophys. J. 2012, 750, 136. [Google Scholar] [CrossRef]

- Dehghanpour, A.; Rezvani, Z. The profile of unethical insurance customers: A European perspective. Int. J. Bank Mark. 2015, 33, 298–315. [Google Scholar] [CrossRef]

- Wang, Y.; Lin, X.; Lin, W.; Wenji, Z.; Qing, Z. Exploiting correlation consensus: Towards subspace clustering for multi-modal data. In Proceedings of the 22nd ACM International Conference on Multimedia, Orlando, FL, USA, 3–7 November 2014; pp. 981–984. [Google Scholar]

- Newstead, S.; D’Elia, A. Does vehicle colour influence crash risk? Saf. Sci. 2010, 48, 1327–1338. [Google Scholar] [CrossRef]

- Olawale, F.; Garwe, D. Obstacles to the growth of the SMEs in South Africa: A principal components approach. Afr. J. Bus. Manag. 2010, 4, 729–738. [Google Scholar]

- Leech, N.L.; Barrett, K.C.; Morgan, G.A. SPSS for Intermediate Statistics: Use and Interpretation; Psychology Press: Hove, UK, 2005. [Google Scholar]

- Ringim, K.J.; Yussof, I.M. Perception, awareness and understanding of muslim account holders in conventional banks with respect to patronizing Islamic banking products in Nigeria. Ilorin J. Econ. Policy 2014, 1, 41–52. [Google Scholar]

- Bruce, N.; Pope, D.; Stanistreet, D. Quantitative Methods for Health Research: A Practical Interactive Guide to Epidemiology and Statistics; Wiley-Blackwell: Hoboken, NJ, USA, 2008. [Google Scholar]

- Adler, R.F.; Huffman, G.H.; Chang, A.; Ferraro, R.; Xie, P.P.; Janowiak, J.; Rudolf, B.; Schneider, U.; Curtis, S.; Bolvin, D.; et al. The version-2 global precipitation climatology project (GPCP) monthly precipitation analysis (1979–present). J. Hydrometeorol. 2017, 4, 1147–1167. [Google Scholar] [CrossRef]

- Shanmugam, K.R.; Chilakala, R.; Korivi, M.; Reddy, K.S. Protective effect of ginger against alcohol-induced renal damage and antioxidant enzymes in male albino rats. Indian J. Exp. Biol. 2010, 48, 143–149. [Google Scholar]

- Yaghoubi, A.; Bashiri, M. Proposing a mixed model based on stochastic data envelopment analysis and principal component analysis to predict efficiency. J. Basic Appl. Sci. Res. 2012, 2, 12031–12043. [Google Scholar]

- The Global Findex Database. Available online: https://globalfindex.worldbank.org/ (accessed on 3 June 2021).

- Eurostat Database. Available online: https://ec.europa.eu/eurostat (accessed on 3 June 2021).

- Abdi, H.; Williams, L.J. Principal component analysis. WIREs Comput. Stat. 2010, 2, 433–459. [Google Scholar] [CrossRef]

- Groth, C.; Sasamura, T.; Khanna, M.R.; Whitley, M.; Fortini, M.E. Protein trafficking abnormalities in Drosophila tissues with impaired activity of the ZIP7 zinc transporter Catsup. Development 2013, 140, 3018–3027. [Google Scholar] [CrossRef] [Green Version]

- Wold, S.; Esbensen, K.; Geladi, P. Principal component analysis. Chemom. Intell. Lab. Syst. 1987, 2, 37–52. [Google Scholar] [CrossRef]

- Jolliffe, D. Whose education matters in the determination of household income? Evidence from a developing country. Econ. Dev. Cult. Chang. 2002, 50, 287–312. [Google Scholar] [CrossRef]

- Forkman, J.; Josse, J.; Piepho, H. Hypothesis tests for principal component analysis when variables are standardized. J. Agric. Biol. Environ. Stat. 2019, 24, 289–308. [Google Scholar] [CrossRef] [Green Version]

- Forkman, J.; Piepho, H.P. Parametric bootstrap methods for testing multiplicative terms in GGE and AMMI models. Biometrics 2014, 70, 639–647. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Yochmowitz, M.G.; Cornell, R.G. Stepwise tests for multiplicative components of interaction. Technometrics 1978, 20, 79–84. [Google Scholar] [CrossRef]

- Chen, N. Sparse Decentralized Principal Components Analysis for Dimensionality Reduction. Available online: https://rc.library.uta.edu/uta-ir/bitstream/handle/10106/25774/CHEN-THESIS-2016.pdf?sequence=1&isAllowed=y (accessed on 12 June 2021).

- Wilks, D.S. Statistical Methods in the Atmospheric Sciences, 3rd ed.; Academic Press: Oxford, UK, 2011. [Google Scholar]

- Boccard, J.; Rudaz, S. Mass Spectrometry Metabolomic Data Handling for Biomarker Discovery; Academic Press: Cambridge, MA, USA, 2013. [Google Scholar] [CrossRef]

- Milligan, G.W.; Cooper, M.C. Methodology review: Clustering methods. Appl. Psychol. Meas. 1987, 11, 329–354. [Google Scholar] [CrossRef] [Green Version]

- Sokal, R.R.; Michener, C.D. A Statistical methods for evaluating relationships. Univ. Kans. Sci. Bull. 1958, 38, 1409–1448. [Google Scholar]

- Eisen, M.B.; Spellman, P.T.; Brown, P.O.; Botstein, D. Cluster analysis and display of genome-wide expression patterns. Proc. Natl. Acad. Sci. USA 1998, 95, 14863–14868. [Google Scholar] [CrossRef] [Green Version]

- Steinbach, M.; Ertöz, L.; Kumar, V. The challenges of clustering high dimensional data. In New Directions in Statistical Physics; Wille, L.T., Ed.; Springer: Berlin/Heidelberg, Germany, 2004. [Google Scholar] [CrossRef] [Green Version]

- Almeida, B.; Sampaio-Marques, B.; Carvalho, J.; Silva, M.T.; Leão, C.; Rodrigues, F.; Ludovico, P. An atypical active cell death process underlies the fungicidal activity of ciclopirox olamine against the yeast Saccharomyces cerevisiae. FEMS Yeast Res. 2007, 7, 404–412. [Google Scholar] [CrossRef] [Green Version]

- McHugh, M.L. Multiple comparison analysis testing in ANOVA. Biochem. Med. 2011, 21, 203–209. Available online: https://hrcak.srce.hr/index.php?id_clanak_jezik=108599&show=clanak (accessed on 2 June 2021). [CrossRef]

- Maxwell, S.E.; Delaney, H.D.; Kelley, K. Designing Experiments and Analyzing Data. A Model Comparison Perspective, 3rd ed.; Routledge: Abingdon on Thames, UK, 2018. [Google Scholar]

- Brown, M.B.; Forsythe, A.B. Robust tests for the equality of variances. J. Am. Stat. Assoc. 1974, 69, 364–367. [Google Scholar] [CrossRef]

- Foroudi, P.; Melewar, T.C.; Gupta, S. Linking corporate logo, corporate image, and reputation: An examination of consumer perceptions in the financial setting. J. Bus. Res. 2014, 67, 2269–2281. [Google Scholar] [CrossRef]

- Qi, J.Y.; Qu, Q.X.; Zhou, Y.P. How does customer self-construal moderate CRM value creation chain? Electron. Commer. Res. Appl. 2014, 13, 295–304. [Google Scholar] [CrossRef]

- Ageeva, E.; Melewar, T.C.; Foroudi, P.; Dennis, C. Cues adopted by consumers in examining corporate website favorability: An empirical study of financial institutions in the UK and Russia. J. Bus. Res. 2019, 98, 15–32. [Google Scholar] [CrossRef]

- Akram, U.; Fülöp, M.T.; Tiron-Tudor, A.; Topor, D.I.; Căpușneanu, S. Impact of digitalization on customers’ well-being in the pandemic period: Challenges and opportunities for the retail industry. Int. J. Environ. Res. Public Health 2021, 18, 7533. [Google Scholar] [CrossRef]

- Wang, H.; Ding, J.; Akram, U.; Yue, X.; Chen, Y. An empirical study on the impact of e-commerce live features on consumers’ purchase intention: From the perspective of flow experience and social presence. Information 2021, 12, 324. [Google Scholar] [CrossRef]

- Cheng, M.; Liu, J.; Qi, J.; Wan, F. Differential effects of firm generated content on consumer digital engagement and firm performance: An outside-in perspective. Ind. Mark. Manag. 2021, 98, 41–58. [Google Scholar] [CrossRef]

- Demirguc-Kunt, A.; Klapper, L. Measuring Financial Inclusion: The Global Findex Database. The World Bank. 2012. Available online: https://elibrary.worldbank.org/doi/abs/10.1596/1813-9450-6025 (accessed on 21 June 2021).

- Demirguc-Kunt, A.; Klapper, L.; Singer, D.; Ansar, S.; Hess, J. The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution. The World Bank. 2018. Available online: http://0-mr-crossref-org.brum.beds.ac.uk/iPage?doi=10.1596%2F978-1-4648-1259-0 (accessed on 25 June 2021).

- WIEGO. Informal Workers in the COVID-19 Crisis: A Global Picture of Sudden Impact and Long-Term Risk; WIEGO: Manchester, UK, 2020; Available online: https://www.wiego.org/sites/default/files/resources/file/Informal%20Workers%20in%20the%20COVID-19%20Crisis_WIEGO_July_2020.pdf (accessed on 22 June 2021).

- Von Allmen, U.E.; Purva, K.; Sumiko, O.; Ratna, S. Digital Financial Inclusion in the Times of COVID-19, IMFBlog, 1 July 2020. Available online: https://blogs.imf.org/2020/07/01/digital-financial- (accessed on 19 June 2021).

- ILO. A Global Call to Action for a Human-Centred Recovery from the COVID-19 Crisis That Is Inclusive, Sustainable and Resilient, Resolution. 17 June 2021. Available online: https://www.ilo.org/wcmsp5/groups/public/---ed_norm/---relconf/documents/meetingdocument/wcms_806092.pdf (accessed on 12 July 2021).

- IFC. A Strategy for Creating Markets, Annual Report. 2020. Available online: https://www.ifc.org/wps/wcm/connect/5e9c14ca-5ed2-4310-9aa3-a7e24e48fe6a/IFC-AR20-Strategy-in-Action.pdf?MOD=AJPERES&CVID=nteydr8 (accessed on 22 June 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Communalities | ||

|---|---|---|

| Initial | Extraction | |

| Account (% age 15+) | 1.000 | 0.996 |

| Account. male (% age 15+) | 1.000 | 0.979 |

| Account. in labor force (% age 15+) | 1.000 | 0.799 |

| Account. out of labor force (% age 15+) | 1.000 | 0.937 |

| Account. female (% age 15+) | 1.000 | 0.973 |

| Account. young adults (% ages 15–24) | 1.000 | 0.774 |

| Account. older adults (% ages 25+) | 1.000 | 0.978 |

| Account. primary education or less (% ages 15+) | 1.000 | 0.842 |

| Account. secondary education or more (% ages 15+) | 1.000 | 0.945 |

| Account. income. poorest 40% (% ages 15+) | 1.000 | 0.982 |

| Account. income. richest 60% (% ages 15+) | 1.000 | 0.979 |

| Account. rural (% age 15+) | 1.000 | 0.985 |

| Account. urban (% age 15+) | 1.000 | 0.982 |

| Paired Samples Statistics | |||||||

|---|---|---|---|---|---|---|---|

| Statistic | Bootstrap a | ||||||

| Bias | Std. Error | 95% Confidence Interval | |||||

| Lower | Upper | ||||||

| Pair 1 | Account. male (% age 15+) | Mean | 0.835763 | −0.000268 | 0.027687 | 0.774476 | 0.886354 |

| N | 45 | ||||||

| Std. Deviation | 0.1811504 | −0.0033037 | 0.0224393 | 0.1300994 | 0.2188548 | ||

| Std. Error Mean | 0.0270043 | ||||||

| Account. female (% age 15+) | Mean | 0.808915 | −0.000258 | 0.030886 | 0.739922 | 0.866169 | |

| N | 45 | ||||||

| Std. Deviation | 0.2029120 | −0.0030470 | 0.0211476 | 0.1536688 | 0.2370336 | ||

| Std. Error Mean | 0.0302483 | ||||||

| Pair 2 | Account. out of labor force (% age 15+) | Mean | 0.731848 | −0.000044 | 0.038549 | 0.645534 | 0.802501 |

| N | 45 | ||||||

| Std. Deviation | 0.2522961 | −0.0039937 | 0.0267163 | 0.1937517 | 0.3020290 | ||

| Std. Error Mean | 0.0376101 | ||||||

| Account. in labor force (% age 15+) | Mean | 0.872829 | −0.000563 | 0.030224 | 0.806876 | 0.927699 | |

| N | 45 | ||||||

| Std. Deviation | 0.2006518 | −0.0071103 | 0.0457540 | 0.1047057 | 0.2837053 | ||

| Std. Error Mean | 0.0299114 | ||||||

| Pair 3 | Account. young adults (% ages 15–24) | Mean | 0.670945 | 0.000340 | 0.037899 | 0.593027 | 0.742627 |

| N | 45 | ||||||

| Std. Deviation | 0.2483807 | −0.0037557 | 0.0166311 | 0.2124366 | 0.2771743 | ||

| Std. Error Mean | 0.0370264 | ||||||

| Account. older adults (% ages 25+) | Mean | 0.849378 | −0.000369 | 0.027906 | 0.787047 | 0.901535 | |

| N | 45 | ||||||

| Std. Deviation | 0.1829446 | −0.0029490 | 0.0217086 | 0.1324199 | 0.2182820 | ||

| Pair 4 | Account. primary education or less (% ages 15+) | Std. Error Mean | 0.0272718 | ||||

| Mean | 0.698118 | −0.000174 | 0.040618 | 0.613800 | 0.775433 | ||

| N | 45 | ||||||

| Std. Deviation | 0.2684567 | −0.0034275 | 0.0165081 | 0.2286634 | 0.2967826 | ||

| Std. Error Mean | 0.0400192 | ||||||

| Account. secondary education or more (% ages 15+) | Mean | 0.863027 | −0.000127 | 0.025887 | 0.806171 | 0.909260 | |

| N | 45 | ||||||

| Std. Deviation | 0.1689842 | −0.0036587 | 0.0242915 | 0.1150508 | 0.2100197 | ||

| Std. Error Mean | 0.0251907 | ||||||

| Pair 5 | Account. income. poorest 40% (% ages 15+) | Mean | 0.764705 | −0.000159 | 0.036263 | 0.685704 | 0.832916 |

| N | 45 | ||||||

| Std. Deviation | 0.2378667 | −0.0034492 | 0.0232048 | 0.1848892 | 0.2764515 | ||

| Std. Error Mean | 0.0354591 | ||||||

| Account. income. richest 60% (% ages 15+) | Mean | 0.8599 | −0.0003 | 0.0247 | 0.8044 | 0.9045 | |

| N | 45 | ||||||

| Std. Deviation | 0.16136 | −0.00295 | 0.02081 | 0.11415 | 0.19546 | ||

| Std. Error Mean | 0.02405 | ||||||

| Pair 6 | Account. rural (% age 15+) | Mean | 0.806723 | −0.000239 | 0.032130 | 0.736557 | 0.866465 |

| N | 45 | ||||||

| Std. Deviation | 0.2097440 | −0.0034435 | 0.0241283 | 0.1558651 | 0.2513515 | ||

| Std. Error Mean | 0.0312668 | ||||||

| Account. urban (% age 15+) | Mean | 0.8371 | −0.0003 | 0.0264 | 0.7777 | 0.8846 | |

| N | 45 | ||||||

| Std. Deviation | 0.17348 | −0.00273 | 0.01906 | 0.12937 | 0.20446 | ||

| Std. Error Mean | 0.02586 | ||||||

| Paired Samples Test | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Paired Differences | t | df | Sig. (2-Tailed) | ||||||

| Mean | Std. Deviation | Std. Error Mean | 95% Confidence Interval of the Difference | ||||||

| Lower | Upper | ||||||||

| Pair 1 | Account. male (% age 15+)—Account. female (% age 15+) | 0.0268480 | 0.0587885 | 0.0087637 | 0.0091860 | 0.0445100 | 3.064 | 44 | 0.004 |

| Pair 2 | Account. out of labor force (% age 15+)—Account. in labor force (% age 15+) | −0.1409812 | 0.1302340 | 0.0194141 | −0.1801078 | −0.1018546 | −7.262 | 44 | 0.000 |

| Pair 3 | Account. young adults (% ages 15–24)—Account. older adults (% ages 25+) | −0.1784335 | 0.1473078 | 0.0219593 | −0.2226896 | −0.1341773 | −8.126 | 44 | 0.000 |

| Pair 4 | Account. primary education or less (% ages 15+)—Account. secondary education or more (% ages 15+) | −0.1649091 | 0.1615661 | 0.0240848 | −0.2134489 | −0.1163693 | −6.847 | 44 | 0.000 |

| Pair 5 | Account. income. poorest 40% (% ages 15+)—Account. income. richest 60% (% ages 15+) | −0.0951613 | 0.0904219 | 0.0134793 | −0.1223270 | −0.0679955 | −7.060 | 44 | 0.000 |

| Pair 6 | Account. rural (% age 15+)—urban | −0.0303414 | 0.0553019 | 0.0082439 | −0.0469560 | −0.0137269 | −3.680 | 44 | 0.001 |

| Sum of Squares | df | Mean Square | F | Sig. | ||

|---|---|---|---|---|---|---|

| GDP/capita | Between Groups | 46,993.387 | 2 | 23,496.693 | 12.310 | 0.000 |

| Within Groups | 80,169.595 | 42 | 1908.800 | |||

| Total | 127,162.981 | 44 | ||||

| Primary education | Between Groups | 2,027,438,281,546.901 | 2 | 1,013,719,140,773.451 | 1.963 | 0.153 |

| Within Groups | 21,693,324,235,317.900 | 42 | 516,507,719,888.521 | |||

| Total | 23,720,762,516,864.800 | 44 | ||||

| Secondary education | Between Groups | 1,892,076,989,138.040 | 2 | 946,038,494,569.020 | 0.964 | 0.390 |

| Within Groups | 58,502,013,437,693.070 | 42 | 1,392,905,081,849.835 | |||

| Total | 60,394,090,426,831.110 | 44 | ||||

| Bachelor | Between Groups | 458,514,789,598.221 | 2 | 229,257,394,799.111 | 0.423 | 0.658 |

| Within Groups | 22,785,515,704,173.426 | 42 | 542,512,278,670.796 | |||

| Total | 23,244,030,493,771.650 | 44 | ||||

| Master | Between Groups | 134,536,861,533.269 | 2 | 67,268,430,766.635 | 1.077 | 0.350 |

| Within Groups | 2,623,512,022,946.375 | 42 | 62,464,571,974.914 | |||

| Total | 2,758,048,884,479.644 | 44 | ||||

| Doctorate | Between Groups | 1,078,417,221.561 | 2 | 539,208,610.780 | 1.297 | 0.284 |

| Within Groups | 17,463,923,954.439 | 42 | 415,807,713.201 | |||

| Total | 23,720,762,516,864.800 | 44 | ||||

| Sum of Squares | df | Mean Square | F | Sig. | |

|---|---|---|---|---|---|

| Between Groups | 1.298 | 2 | 0.649 | 91.507 | 0.000 |

| Within Groups | 0.298 | 42 | 0.007 | ||

| Total | 1.596 | 44 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vasile, V.; Panait, M.; Apostu, S.-A. Financial Inclusion Paradigm Shift in the Postpandemic Period. Digital-Divide and Gender Gap. Int. J. Environ. Res. Public Health 2021, 18, 10938. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph182010938

Vasile V, Panait M, Apostu S-A. Financial Inclusion Paradigm Shift in the Postpandemic Period. Digital-Divide and Gender Gap. International Journal of Environmental Research and Public Health. 2021; 18(20):10938. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph182010938

Chicago/Turabian StyleVasile, Valentina, Mirela Panait, and Simona-Andreea Apostu. 2021. "Financial Inclusion Paradigm Shift in the Postpandemic Period. Digital-Divide and Gender Gap" International Journal of Environmental Research and Public Health 18, no. 20: 10938. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph182010938