Long- and Short-Term Cryptocurrency Volatility Components: A GARCH-MIDAS Analysis

1

Department of Economics, Heidelberg University, Bergheimer Strasse 58, 69115 Heidelberg, Germany

2

Department of Economics, University of North Carolina, Chapel Hill, NC 27599, USA

3

CEPR, Department of Finance, Kenan-Flagler School of Business, University of North Carolina, Chapel Hill, NC 27599, USA

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2018, 11(2), 23; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm11020023

Submission received: 10 April 2018

/

Revised: 5 May 2018

/

Accepted: 8 May 2018

/

Published: 10 May 2018

(This article belongs to the Special Issue Alternative Assets and Cryptocurrencies)

Abstract

:We use the GARCH-MIDAS model to extract the long- and short-term volatility components of cryptocurrencies. As potential drivers of Bitcoin volatility, we consider measures of volatility and risk in the US stock market as well as a measure of global economic activity. We find that S&P 500 realized volatility has a negative and highly significant effect on long-term Bitcoin volatility. The finding is atypical for volatility co-movements across financial markets. Moreover, we find that the S&P 500 volatility risk premium has a significantly positive effect on long-term Bitcoin volatility. Finally, we find a strong positive association between the Baltic dry index and long-term Bitcoin volatility. This result shows that Bitcoin volatility is closely linked to global economic activity. Overall, our findings can be used to construct improved forecasts of long-term Bitcoin volatility.

Keywords:

Baltic dry index; Bitcoin volatility; digital currency; GARCH-MIDAS; pro-cyclical volatility; volumeJEL Classifications:

C53; C58; F31; G15“After Lehman Brothers toppled in September 2008, it took 24 days for US stocks to slide more than 20 per cent into official bear market territory. Bitcoin, the new age cryptocurrency that has been breaking bull market records, did the same on Wednesday in just under six hours”Financial Times—30 November 2017—Bitcoin swings from bull to bear and back in one day

1. Introduction

Bitcoin is surely not short on publicity as its rise, subsequent decline and volatile swings have drawn the attention from academics and business leaders alike. There are many critics. For example, Nobel laureate Joseph Stiglitz said that Bitcoin ought to be outlawed whereas fellow Nobel laureate Robert Shiller said the currency appeals to some investors because it has an anti-government, anti-regulation feel. Many business leaders, including Carl Icahn and Warren Buffett, characterized its spectacular price increases as a bubble. Jamie Dimon, CEO of JP Morgan called it a fraud, and implicitly alluding to bubbles that ultimately burst, predicted that it eventually would blow up. Along similar lines, Goldman Sachs CEO Lloyd Blankfein is on the record for saying that the currency serves as a vehicle for perpetrating fraud, although he acknowledged that the currency could have potential if volatility drops.

Cryptocurrencies has its defenders and enthusiasts as well. The CME Group listed Bitcoin futures in mid-December 2017 and Nasdaq plans to launch Bitcoin futures this year. The currency also has many supporters in Silicon Valley. The listing of Bitcoin futures and the proliferation of cryptocurrencies in general has generated a growing literature on the topic.

Most of the existing studies focus on Bitcoin returns. For example, Baur et al. (2017) show that Bitcoin returns are essentially uncorrelated with traditional asset classes such as stocks or bonds, which points to diversification possibilities. Others investigate the determinants of Bitcoin returns. The findings of Li and Wang (2017), among others, suggest that measures of financial and macroeconomic activity are drivers of Bitcoin returns. Kristoufek (2015) considers financial uncertainty, Bitcoin trading volume in Chinese Yuan and Google trends as potential drivers of Bitcoin returns. The inclusion of Google trends as some sort of proxy for sentiment or interest is fairly common within the literature (see, for example, Polasik et al. (2015)). A recurrent theme in the literature is the question to which asset class Bitcoin belongs, with many comparing it to gold, others to precious metals or to speculative assets (see, among others, Baur et al. (2017); or Bouri et al. (2017)). Some have classified Bitcoin as something in between a currency and a commodity (see, for example, Dyhrberg (2016)). For other recent contributions, see Cheah et al. (2018); Khuntia and Pattanayak (2018); and Koutmos (2018).

A second strand of literature tries to model Bitcoin volatility. Among the first papers is Balcilar et al. (2017), who analyze the causal relation between trading volume and Bitcoin returns and volatility. They find that volume cannot help predict the volatility of Bitcoin returns. Dyhrberg (2016) explores Bitcoin volatility using GARCH models. The models estimated in Dyhrberg (2016) suggest that Bitcoin has several similarities with both gold and the dollar. Bouri et al. (2017) find no evidence for asymmetry in the conditional volatility of Bitcoins when considering the post December 2013 period and investigate the relation between the VIX index and Bitcoin volatility. Al-Khazali et al. (2018) consider a model for daily Bitcoin returns and show that Bitcoin volatility tends to decrease in response to positive news about the US economy. Finally, Katsiampa (2017) explores the applicability of several ARCH-type specifications to model Bitcoin volatility and selects an AR-CGARCH model as the preferred specification. Although Katsiampa (2017) suggests that Bitcoin volatility consists of long- and short-term components, he does not investigate the determinants of Bitcoin volatility.

We use the GARCH-MIDAS model of Engle et al. (2013) for investigating the economic determinants of long-term Bitcoin volatility. While all the previous studies considered Bitcoin returns/volatility as well as their potential determinants at the same (daily) frequency, the MIxed Data Sampling (MIDAS) technique offers a unique framework to investigate macroeconomic and financial variables that are sampled at a lower (monthly) frequency than the Bitcoin returns as potential drivers of Bitcoin volatility. Specifically, the two-component GARCH-MIDAS model consists of a short-term GARCH component and a long-term component. The model allows explanatory variables to enter directly into the specification of the long-term component.

As potential drivers of Bitcoin volatility, we consider macroeconomic and financial variables, such as the Baltic dry index and the VIX, but also Bitcoin specific variables, such as trading volume. In addition, we analyze the drivers of the volatility of the S&P 500, the Nikkei 225, gold and copper. This allows for a comparison of the effects on the different assets and provides further useful insights for a classification of Bitcoin as an asset class.

Our main findings can be summarized as follows: First, Bitcoin volatility is negatively related to US stock market volatility. This observation is consistent with investors who consider Bitcoin as a safe-haven. Second, in contrast to stock market volatility, Bitcoin volatility behaves pro-cyclical, i.e., increases with higher levels of global economic activity. Third, the response of Bitcoin volatility to higher levels of US stock market volatility is the opposite of the response of gold volatility. This questions the meaningfulness of comparisons between Bitcoin and gold. Finally, while most previous studies focused on short-term relationships using exclusively daily data, our results highlight the importance of also investigating the relationship between long-term Bitcoin volatility and its economic drivers.

2. Model

We model Bitcoin volatility as a GARCH-MIDAS processs. Engle et al. (2013) discuss the technical details of this class of models where the conditional variance is multiplicatively decomposed into a short-term (high-frequency) and a long-term (low-frequency) component. The long-term component is expressed as a function of observable explanatory variables. This allows us to investigate the financial and macroeconomic determinants of Bitcoin volatility. In the empirical application, we consider daily Bitcoin returns and monthly explanatory variables.

We define daily Bitcoin returns as , where denotes the monthly frequency and the number of days within month t. We assume that the conditional mean of Bitcoin returns is constant, i.e.,

with

The innovation is assumed to be i.i.d. with mean zero and variance one. and denote the short- and long-term component of the conditional variance, respectively. The short-term component varies at the daily frequency and follows a unit-variance GARCH(1,1) process

where , and . The long-term component varies at the monthly frequency and is given by

where denotes the explanatory variable and a certain weighting scheme. We opt for the Beta weighting scheme, which is given by

By construction, the weights , , sum to one. In the empirical application, we impose the restriction that , which implies that the weights are monotonically declining. Following Conrad and Loch (2015), we employ three MIDAS lag years, i.e., we choose for the monthly explanatory variables. Our empirical results show that this choice is appropriate in the sense that the estimated weights approach zero before lag 36. As in Engle et al. (2013), we estimate the GARCH-MIDAS models by quasi-maximum likelihood and construct heteroscedasticity and autocorrelation consistent (HAC) standard errors.

3. Data

Our analysis utilizes cryptocurrency specific data, measures of financial conditions, and measures of macroeconomic activity from May 2013 to December 2017. Data are collected from a number of sources and are described in more detail in what follows.

3.1. Data Descriptions

Daily Bitcoin prices and trading volumes were taken from bitcoinity.1 The monthly realized volatility for Bitcoin was constructed using daily squared returns. The Bitcoin (BTC) trading volume by currency is simply the sum of all BTC traded in a selected period in specific currencies. It is worth noting, however, that traders are able to trade in any currency they choose, regardless of geographic location.

The financial measures used consist of the following: commodity ETFs, a luxury goods index, monthly realized volatility and daily returns for the S&P 500 and the Nikkei 225, the VIX index, and the Variance Risk Premium. For the luxury goods index, we use the S&P Global Luxury Index (Glux). This offers exposure to over 80 luxury brands in a number of countries. For our commodities, we use SPDR Gold Shares ETF (GLD) and iPath Bloomberg Copper ETF (JJC).

The S&P 500 monthly realized volatility is constructed using the daily realized variances, , based on 5-min intra-day returns from the Oxford-Man Institute of Quantitative Finance. The daily realized variances are then used to construct annualized monthly realized volatility as . The Nikkei 225 monthly realized volatility is constructed analogously. The VIX index, from the Chicago Board of Options Exchange (Cboe), is computed from a panel of options prices and is a “risk-neutral” implied volatility measure of the stock market. It is frequently referred to as a “fear index” and is a gauge of perceived volatility, in both directions. The Variance Risk Premium, , is calculated as the difference between the squared VIX and the expected realized variance. Assuming the realized variance is a random walk, this is then a purely data-driven measure of the risk premium.

The measure of macroeconomic activity used consists of the Baltic dry index (BDI), retrieved from Quandl.2 BDI is an economic indicator issued by the Baltic Exchange based in London and was first released in January 1985. The BDI is a composite of the following four different Baltic indices: the Capesize, Handysize, Panamax, and Supramax. Everyday, a panel submits current freight cost estimates on various routes. These rates are then weighted by size to create the BDI. The index covers a range of carriers who transport a number of commodities and provides a cost assessment of moving raw materials by water. It is frequently thought of as a good indicator of future economic growth and production.

Since Bitcoin has been receiving more attention in the news, we follow Kristoufek (2015) and utilize Google Trend data to see how this may contribute to the volatility of Bitcoin. We use monthly indexes constructed by Google Trends for all web searches and monthly indexes for news searches only. The spikes in the indices coincide with big events, both positive and negative. Moreover, we were able to match large weekly swings in the index to specific events throughout the sample period. Periods in the sample where Bitcoin did not have any major events take place had low, constant interest index values. Hence, we believe that the Google Trends index is a fair proxy for large events, both positive and negative, that may affect the volatility of Bitcoin.

3.2. Summary Statistics

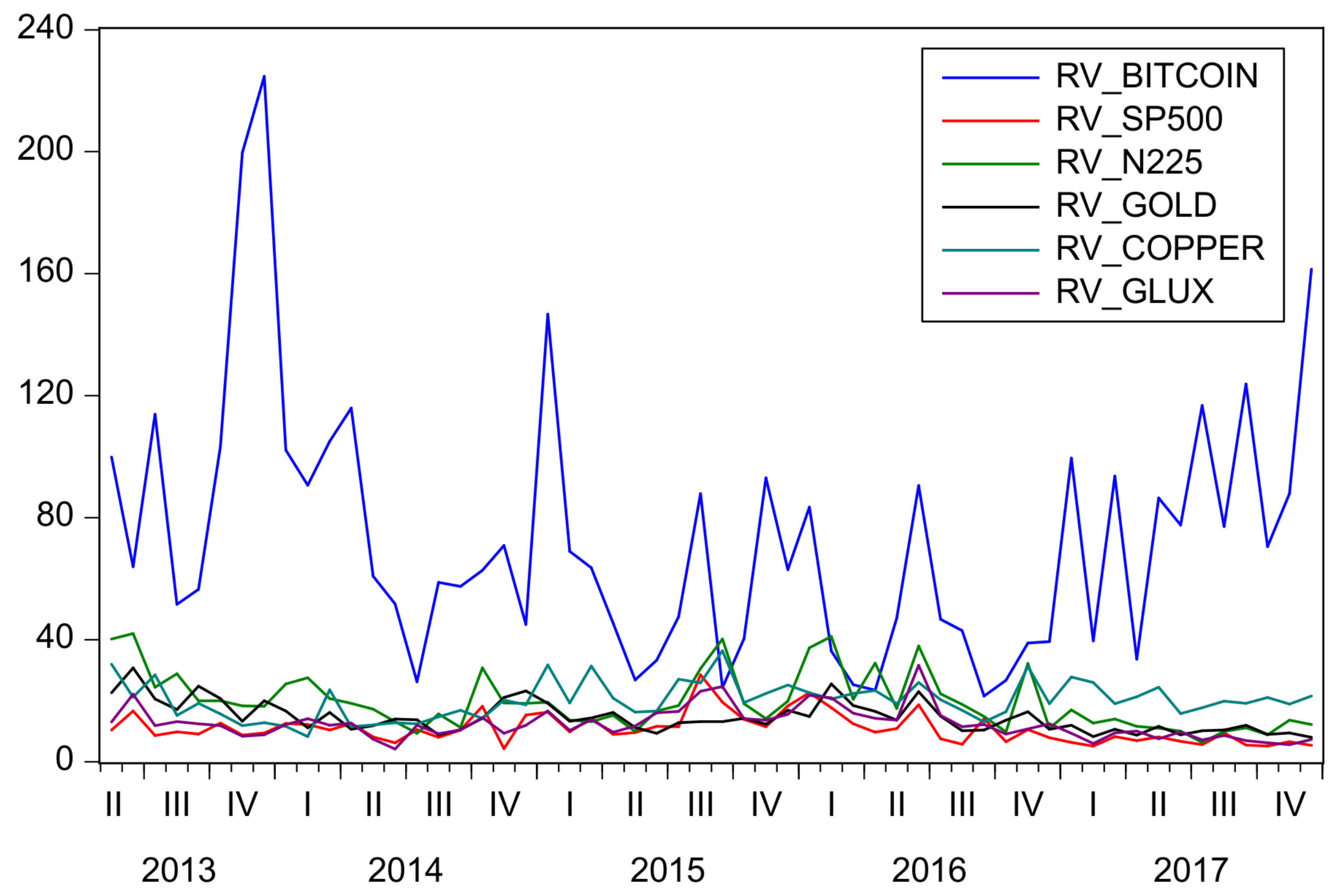

Table 1 provides summary statistics. Panel A presents descriptive statistics for the Bitcoin returns as well as returns on the S&P 500, Nikkei 225, Gold and Copper. The average daily Bitcoin return is 0.271% during our sample period. On an annualized basis, this corresponds to a return of approximately 68%, which is much higher than for the other assets (e.g., 11.34% for the S&P 500). However, the minimum and maximum of daily Bitcoin returns are also much more extreme than for the other assets. This is also reflected in a kurtosis of 11.93 (vs. 5.99 for the S&P 500). Note that Bitcoins are traded seven days per week while the other assets are not traded over the weekend or on bank holidays, which explains the variation in the number of observations across the assets. The extraordinary price development of the Bitcoin is depicted in Figure 1. In particular, the price action in 2017 is dramatic: from January 2017 to December 2017 the Bitcoin price increased by 1318%!

The monthly realized volatilities (RV) are presented in Panel B. Clearly, Bitcoin realized volatility stands out as by far the highest. The average annualized Bitcoin RV is 73% as compared to 11% for the S&P 500. Figure 2 shows the times series of annualized monthly realized volatilities. During the entire sample period Bitcoin realized volatility by far exceeds realized volatility in all other assets. Specifically, the year 2017 was characterized by unusually low volatility in stock markets: in 2017, the Cboe’s volatility index, VIX, fell to the lowest level during the last 23 years and realized volatility in US stock markets was the lowest since the mid-1990s. In sharp contrast, Bitcoin volatility was increasing over almost the entire year.

Panels C and D provide summary statistics for the macro/financial and Bitcoin specific explanatory variables. Prior to the estimation, all explanatory variables are standardized.

Table 2 presents the contemporaneous correlations between the realized volatilities of the different assets. While there is a strong co-movement between the realized volatilities of the S&P 500 and the Nikkei 225 as well as a very strong correlation of both RVs with the realized volatility of the luxury goods index, Bitcoin realized volatility is only weakly correlated with the RV of all other assets. Although the contemporaneous correlations are close to zero, the correlation between and is −0.1236 and between and is −0.2623. This suggests that lagged S&P 500 realized volatility may be a useful predictor for future Bitcoin volatility.

In the empirical analysis, we use the explanatory variables in levels. This is justified because the persistence of the explanatory variables is not too strong at the monthly frequency. For example, the first order autocorrelation of the Baltic dry index and trading volume in US dollars is 0.79 and 0.48, respectively. Nevertheless, we also estimated GARCH-MIDAS models using the first difference of the explanatory variables. All our results were robust to this modification.

4. Empirical Results

4.1. Macro and Financial Drivers of Long-Term Bitcoin Volatility

In this section, we analyze the determinants of long-term Bitcoin volatility. In general, once the long-term component is accounted for, the short-term volatility component is well described by a GARCH(1,1) process. As potential drivers of Bitcoin volatility, we consider measures of volatility and risk in the US stock market as well as a measure of global economic activity. These measures have been shown to be important drivers of US stock market volatility in previous studies (see, among others, (Engle et al. 2013; Conrad and Loch 2015; and Conrad and Kleen 2018)). Bouri et al. (2017) found only weak evidence for a relation between US stock market volatility and Bitcoin volatility. However, their analysis was based on daily data and focused on short-term effects. In contrast, the GARCH-MIDAS model allows us to investigate whether US stock market volatility has an effect on long-term Bitcoin volatility. For comparison, we also present how these measures are related to the volatility of the S&P 500, the Nikkei 225 and the volatility of gold and copper.3

As a benchmark model, we estimate a simple GARCH(1,1) for the Bitcoin returns. The parameter estimates are presented in the first line of Table 3. The constant in the mean as well as the two GARCH parameters are highly significant. The sum of the estimates of and is slightly above one. Therefore, the estimated GARCH model does not satisfy the condition for covariance stationarity. This result is likely to be driven by the extreme swings in Bitcoin volatility and suggests that a two-component model may be more appropriate.4 We also estimated a GJR-GARCH and—in line with Bouri et al. (2017)—found no evidence for asymmetry in the conditional volatility.

The remainder of Table 3 presents the parameter estimates for the GARCH-MIDAS models. For those models, the estimates of and satisfy the condition for covariance stationarity, i.e., accounting for long-term volatility reduces persistence in the short-term component. First, we use S&P 500 realized volatility as an explanatory variable for long-term Bitcoin volatility. Interestingly, we find that has a negative and highly significant effect on long-term Bitcoin volatility. Since the estimated weighting scheme puts a weight of 0.09 on the first lag, our parameter estimates imply that a one standard deviation increase in this month predicts a decline of 17% in long-term Bitcoin volatility next month. The finding that is negatively related to Bitcoin volatility is in contrast to the usual findings for other markets. For comparison, Table 4 and Table 5 present parameters estimates for GARCH-MIDAS models applied to the S&P 500 and the Nikkei 225. As expected, higher levels of predict increases in S&P 500 long-term volatility as well as increases in the long-term volatility of the Nikkei 225.

Second, we find that the VIX and RV-Glux are negatively related to long-term Bitcoin volatility. Since both measures are positively related to (see Table 2), this finding is not surprising. Again, Table 4 and Table 5 show that the opposite effect is true for the two stock markets.

Third, Table 3 implies that the VRP has a significantly positive effect on long-term Bitcoin volatility. A high VRP is typically interpreted either as a sign of high aggregate risk aversion (Bekaert et al. (2009)) or high economic uncertainty (Bollerslev et al. (2009)). We observe the same effect for the Nikkei 225 (see Table 5) but no such effect for the S&P 500 (see Table 4).

Fourth, we find a strong positive association between the Baltic dry index and long-term Bitcoin volatility. The finding of a pro-cyclical behavior of Bitcoin volatility is noteworthy, since it contrasts with the counter-cyclical behavior usually observed for financial volatility (see Schwert (1989); or Engle et al. (2013)).

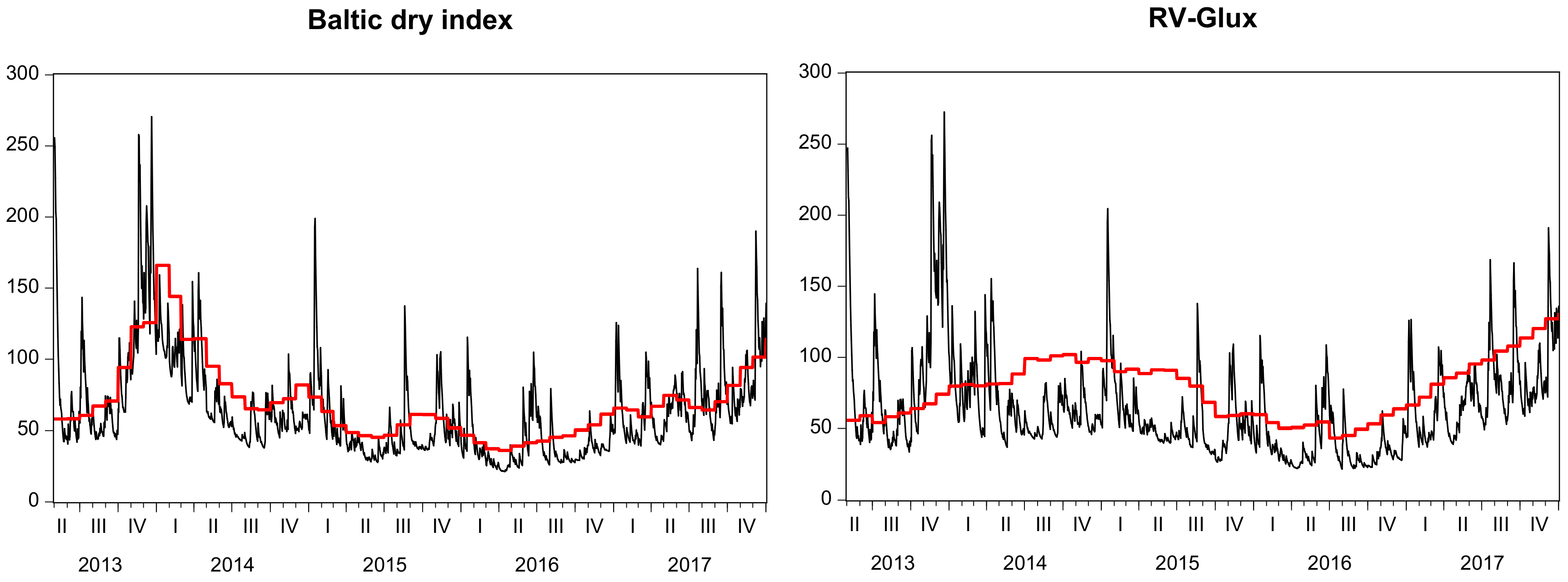

According to the Akaike and Bayesian information criteria, the preferred GARCH-MIDAS model for Bitcoin volatility is based on the Baltic dry index (see Table 3). The left panel of Figure 3 shows the estimated long- and short-term components from this specification. About 65% percent of the variation in the monthly conditional volatility can be explained by movements in long-term volatility. For comparison, the right panel shows the long- and short-term components for the model based on the volatility of the luxury goods index. Clearly, the comparison of graphs confirms that the Baltic dry index has more explanatory power for Bitcoin volatility than RV-Glux.

Finally, Table 6 presents the GARCH-MIDAS estimates for gold and copper. In the table, we include only explanatory variables for which the estimate of is significant. We find that the GARCH persistence parameter, , is high for both Gold and Copper across all models. Long-term gold volatility is positively related to realized volatility in the S&P 500, the VIX and realized volatility in the luxury goods index. Interestingly, there is a strongly negative relation between long-term copper volatility and the baltic dry index. Elevated levels of global economic activity go along with high demand for copper and, hence, an increasing copper price and low volatility.

In summary, we find that the behavior of long-term Bitcoin volatility is rather unusual. Unlike volatility in the two stock markets and volatility of gold/copper, Bitcoin volatility decreases in response to higher realized or expected volatility in the US stock market. A potential explanation might be that Bitcoin investors may have lost faith in institutions such as governments and central banks and consider Bitcoin as a safe-haven.5 Furthermore, while stock market volatility and copper volatility behave counter-cyclically, Bitcoin volatility appears to behave strongly pro-cyclically. This is an interesting result that distinguishes Bitcoin from stocks but also from commodities or precious metals. Since Bitcoin neither has an income stream (as compared to stocks) nor an intrinsic value (as compared to commodities), it is often compared to precious metals such as gold. However, our results suggest that the link between Bitcoin volatility and macro/financial variables is very different from the link between those variables and stocks/copper/gold.

4.2. Bitcoin Specific Explanatory Variables

Next, we consider Bitcoin specific explanatory variables. The parameter estimates are presented in Table 7. As expected, we find that both Google Trend measures (all web searches and monthly news searches) are significantly positively related to Bitcoin volatility. That is, more attention in terms of Google searches predicts higher levels of long-term volatility.6 Finally, we estimate two models that include Bitcoin trading volume in US dollar (US-TV) and Chinese yuan (CNY-TV), respectively. In both cases, we find a significantly negative effect of trading volume. We conjecture that increasing trading volume goes along with higher levels of “trust” or “confidence” in Bitcoin as a payment system and, hence, predicts lower Bitcoin volatility. Recall that Balcilar et al. (2017) analyze the causal relation between trading volume and Bitcoin returns and volatility. They find that volume cannot help predict the volatility of Bitcoin returns. It appears therefore that separating out long-term components is important in finding significant patterns between volatility and trading volume.

5. Conclusions

Cryptocurrency is a relatively unexplored area of research and the fluctuations of Bitcoin prices are still poorly understood. As cryptocurrencies appear to gain interest and legitimacy, particularly with the establishment of derivatives markets, it is important to understand the driving forces behind market movements. We tried to tease out what are the drivers of long-term volatility in Bitcoin. We find that S&P 500 realized volatility has a negative and highly significant effect on long-term Bitcoin volatility and that the S&P 500 volatility risk premium has a significantly positive effect on long-term Bitcoin volatility. Moreover, we find a strong positive association between the Baltic dry index and long-term Bitcoin volatility and report a significantly negative effect of Bitcoin trading volume.

It is worth noting that there are a number of series we considered—such as crime-related statistics—which did not really seem to explain Bitcoin volatility, despite the popular press coverage on the topic. We also experimented with a flight-to-safety indictor suggested in Engle et al. (2012) and found that long-term Bitcoin volatility tends to decrease during flight-to-safety periods. This result squares with our finding of a negative relation between Bitcoin volatility and risks in the US stock market.

Since our findings suggest that Bitcoin volatility forecasts based on the GARCH-MIDAS model are superior to forecasts based on simple GARCH models, our results can be used, for example, to construct improved time-varying portfolio weights when building portfolios of Bitcoins and other assets such as stocks and bonds. Our results may also be useful for the pricing of Bitcoin futures, since they allow us to anticipate changes in Bitcoin volatility at longer horizons. Finally, the GARCH-MIDAS model can be used to simulate Bitcoin volatility based on alternative scenarios for the development of the US stock market or global economic activity. We look forward to sort out these possibilities in future research.

Nevertheless, we would like to emphasize that all our results are based on a relatively short sample period. It will be interesting to see whether our results still hold in longer samples and when the Bitcoin currency has become more mature.

Author Contributions

C.C., A.C. and E.G. have contributed jointly to all of the sections of the paper. The authors analyzed the data and wrote the paper jointly.

Acknowledgments

We thank Christian Hafner for inviting us to write on the topic of cryptocurrency. We thank Peter Hansen and Steve Raymond for helpful comments.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Al-Khazali, Osamah, Bouri Elie, and David Roubaud. 2018. The impact of positive and negative macroeconomic news surprises: Gold versus Bitcoin. Economics Bulletin 38: 373–82. [Google Scholar]

- Balcilar, Mehmet, Elie Bouri, Rangan Gupta, and David Roubaud. 2017. Can volume predict Bitcoin returns and volatility? A quantiles-based approach. Economic Modelling 64: 74–81. [Google Scholar] [CrossRef]

- Baur, Dirk G., Kihoon Hong, and Adrian D. Lee. 2017. Bitcoin: Medium of Exchange or Speculative Assets? Available online: https://ssrn.com/abstract=2561183 (accessed on 25 April 2018). [CrossRef]

- Bekaert, Geert, Eric Engstrom, and Yuhang Xing. 2009. Risk, uncertainty, and asset prices. Journal of Financial Economics 91: 59–82. [Google Scholar] [CrossRef]

- Bollerslev, Tim, George Tauchen, and Hao Zhou. 2009. Expected stock returns and variance risk premia. Review of Financial Studies 22: 4463–92. [Google Scholar] [CrossRef]

- Bouri, Elie, Georges Azzi, and Anne Haubo Dyhrberg. 2017. On the return-volatility relationship in the Bitcoin market around the price crash of 2013. Economics 11: 1–16. [Google Scholar] [CrossRef]

- Chen, Cathy Y. H., Wolfgang Karl Härdle, Ai Jun Hou, and Weining Wang. 2018. Pricing Cryptocurrency Options: The Case of CRIX and Bitcoin. IRTG 1792 Discussion Paper 2018-004. Berlin: Humboldt-Universität zu Berlin. [Google Scholar]

- Cheah, Eng-Tuck, Tapas Mishra, Mamata Parhi, and Zhuang Zhang. 2018. Long memory interdependency and inefficiency in Bitcoin markets. Economics Letters 167: 18–25. [Google Scholar] [CrossRef]

- Conrad, Christian, and Onno Kleen. 2018. Two Are Better Than One: Volatility Forecasting Using Multiplicative Component GARCH Models. Available online: https://ssrn.com/abstract=2752354 (accessed on 15 October 2017).

- Conrad, Christian, and Karin Loch. 2015. Anticipating long-term stock market volatility. Journal of Applied Econometrics 30: 1090–114. [Google Scholar] [CrossRef]

- D’Amuri, Francesco, and Juri Marcucci. 2017. The predictive power of Google searches in forecasting US unemployment. International Journal of Forecasting 33: 801–16. [Google Scholar] [CrossRef]

- Dyhrberg, Anne Haubo. 2016. Bitcoin, gold and the dollar—A GARCH volatility analysis. Finance Research Letters 16: 85–92. [Google Scholar] [CrossRef]

- Engle, Robert, Michael Fleming, Eric Ghysels, and Giang Nguyen. 2012. Liquidity, Volatility, and Flights to Safety in the U.S. Treasury Market: Evidence from a New Class of Dynamic Order Book Models. FRB of New York Staff Report No. 590. Available online: http://0-dx-doi-org.brum.beds.ac.uk/10.2139/ssrn.2195655 (accessed on 9 October 2017).

- Engle, Robert F., Eric Ghysels, and Bumjean Sohn. 2013. Stock market volatility and macroeconomic fundamentals. Review of Economics and Statistics 95: 776–97. [Google Scholar] [CrossRef]

- Fang, Libing, Baizhu Chen, Honghai Yu, and Yichuo Qian. 2018. The importance of global economic policy uncertainty in predicting gold futures market volatility: A GARCH-MIDAS approach. Journal of Futures Markets 38: 413–22. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi. 2017. Volatility estimation for Bitcoin: A comparison of GARCH models. Economics Letters 158: 3–6. [Google Scholar] [CrossRef]

- Kristoufek, Ladislav. 2015. What are the main drivers of the Bitcoin price? Evidence from Wavelet coherence analysis. PLoS ONE 10: e0123923. [Google Scholar] [CrossRef] [PubMed]

- Khuntia, Sashikanta, and J. K. Pattanayak. 2018. Adaptive market hypothesis and evolving predictability of Bitcoin. Economics Letters 167: 26–28. [Google Scholar] [CrossRef]

- Koutmos, Dimitrios. 2018. Bitcoin returns and transaction activity. Economics Letters 167: 81–85. [Google Scholar] [CrossRef]

- Li, Xin, and Chong Alex Wang. 2017. The technology and economic determinants of cryptocurrency exchange rates: The case of Bitcoin. Decision Support Systems 95: 49–60. [Google Scholar] [CrossRef]

- Polasik, Michal, Anna Iwona Piotrowska, Tomasz Piotr Wisniewski, Radoslaw Kotkowski, and Geoffrey Lightfoot. 2015. Price Fluctuations and the Use of Bitcoin: An Empirical Inquiry. International Journal of Electronic Commerce 20: 9–49. [Google Scholar] [CrossRef]

- Schwert, G. William. 1989. Why does stock market volatility change over time? The Journal of Finance 44: 1115–53. [Google Scholar] [CrossRef]

| 1. | All data on data.bitcoinity.org is retrieved directly from exchanges through their APIs and is regularly updated for accuracy. |

| 2. | Note, Quandl’s data source for the BDI is Lloyd’s List. |

| 3. | Fang et al. (2018) investigate whether global economic policy uncertainty predicts long-term gold volatility. We are not aware of any applications of the GARCH-MIDAS to copper returns. |

| 4. | Similarly, Katsiampa (2017) estimates a non-stationary GARCH(1,1) for Bitcoin returns (see his Table 1). See also Chen et al. (2018) for GARCH estimates of Bitcoin volatility. |

| 5. | For example, in a Reuters article from 11 April 2013, it is argued that the Bitcoin “currency has gained in prominence amid the euro zone sovereign debt crisis as more people start to question the safety of holding their cash in the bank. Bitcoins shot up in value in March when investors took fright at Cyprus’ plans to impose losses on bank deposits.” |

| 6. | There is already some evidence that Google searches can be used to forecast macroeconomic variables such as the unemployment rate (see D’Amuri and Marcucci (2017)). |

Figure 1.

Bitcoin price development in the 2013:M5 to 2017:M12 period.

Figure 2.

Annualized monthly realized volatilities.

Figure 3.

The figure shows the annualized long-term (bold red line) and short-term (black line) volatility components as estimated by the GARCH-MIDAS models with the Baltic dry index (left) and the realized volatility of the luxury goods index (right) as explanatory variables.

Figure 3.

The figure shows the annualized long-term (bold red line) and short-term (black line) volatility components as estimated by the GARCH-MIDAS models with the Baltic dry index (left) and the realized volatility of the luxury goods index (right) as explanatory variables.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Descriptive statistics.

| Variable | Mean | Min | Max | SD | Skew. | Kurt. | Obs. |

|---|---|---|---|---|---|---|---|

| Panel A: Daily return data | |||||||

| Bitcoin | 0.271 | −26.620 | 35.745 | 4.400 | −0.139 | 11.929 | 1706 |

| S&P 500 | 0.045 | −4.044 | 3.801 | 0.748 | −0.423 | 5.985 | 1176 |

| Nikkei 225 | 0.043 | −8.253 | 7.426 | 1.389 | −0.391 | 7.817 | 1145 |

| Gold | −0.012 | −5.479 | 4.832 | 0.967 | 0.022 | 5.873 | 1177 |

| Copper | −0.004 | −5.126 | 6.594 | 1.323 | 0.018 | 4.812 | 1177 |

| Panel B: Monthly realized volatilities (annualized) | |||||||

| RV-Bitcoin | 73.063 | 21.519 | 224.690 | 42.349 | 1.414 | 5.472 | 56 |

| RV-S&P 500 | 10.879 | 4.219 | 28.435 | 4.825 | 1.263 | 4.909 | 56 |

| RV-Nikkei 225 | 19.701 | 6.336 | 41.969 | 9.328 | 0.981 | 3.039 | 56 |

| RV-Gold | 14.519 | 8.026 | 30.734 | 5.014 | 1.052 | 3.735 | 56 |

| RV-Copper | 20.132 | 8.265 | 36.396 | 6.037 | 0.493 | 2.930 | 56 |

| RV-Glux | 12.469 | 4.087 | 31.537 | 5.114 | 1.359 | 5.536 | 56 |

| Panel C: Monthly explanatory variables | |||||||

| VIX | 14.684 | 9.510 | 28.430 | 3.602 | 1.424 | 5.832 | 56 |

| VRP | 9.819 | −8.337 | 20.299 | 5.837 | −0.463 | 4.538 | 56 |

| Baltic dry index | 983.150 | 306.905 | 2178.059 | 383.597 | 0.774 | 3.613 | 56 |

| RV-Glux | 12.469 | 4.087 | 31.537 | 5.114 | 1.359 | 5.536 | 56 |

| Panel D: Monthly Bitcoin specific explanatory variables | |||||||

| Google Trends (all) | 7.661 | 2.000 | 100.000 | 14.395 | 5.156 | 32.147 | 56 |

| Google Trends (news) | 10.625 | 2.000 | 100.000 | 15.304 | 4.056 | 22.532 | 56 |

| US-TV | 2,308,314 | 603,946 | 4,947,777 | 1,047,524 | 0.573 | 2.686 | 56 |

| CNY-TV | 24,897,595 | 4693 | 173,047,579 | 42,509,087 | 2.180 | 7.056 | 56 |

Notes: The sample covers the 2013M05–2017M12 period. The reported statistics include the mean, the minimum (Min) and maximum (Max), standard deviation (SD), Skewness (Skew.), Kurtosis (Kurt.), and the number of observations (Obs.).

Table 2.

Contemporaneous correlations between monthly realized volatilities.

| RV-Bitcoin | RV-S&P 500 | RV-Nikkei 225 | RV-Gold | RV-Copper | RV-Glux | |

|---|---|---|---|---|---|---|

| RV-Bitcoin | 1.000 | −0.074 | −0.048 | 0.059 | −0.080 | −0.179 |

| RV-S&P 500 | 1.000 | 0.636 | 0.369 | 0.252 | 0.818 | |

| RV-Nikkei 255 | 1.000 | 0.634 | 0.333 | 0.743 | ||

| RV-Gold | 1.000 | 0.220 | 0.469 | |||

| RV-Copper | 1.000 | 0.367 | ||||

| RV-Glux | 1.000 |

Notes: The sample covers the 2013M05-2017M12 period. The table reports the contemporaneous correlations between the various realized volatilities.

Table 3.

GARCH-MIDAS for Bitcoin: financial and macroeconomic explanatory variables.

| Variable | m | LLF | AIC | BIC | |||||

|---|---|---|---|---|---|---|---|---|---|

| GARCH(1,1) | - | - | 5.4608 | 5.4734 | |||||

| RV-S&P 500 | 5.4182 | 5.4374 | |||||||

| VIX | 5.4285 | 5.4477 | |||||||

| RV-Glux | 5.4208 | 5.4399 | |||||||

| VRP | 5.4126 | 5.4317 | |||||||

| Baltic | 5.3935 | 5.4127 |

Notes: The table reports estimation results for the GARCH-MIDAS-X models including 3 MIDAS lag years () of a monthly explanatory variable X. The sample period is 2013M05-2017M12. The conditional variance of the GARCH(1,1) is specified as . The numbers in parentheses are HAC standard errors. , , indicate significance at the 1%, 5%, and 10% level. LLF is the value of the maximized log-likelihood function. AIC and BIC are the Akaike and Bayesian information criteria.

Table 4.

GARCH-MIDAS for S&P 500.

| Variable | m | LLF | AIC | BIC | |||||

|---|---|---|---|---|---|---|---|---|---|

| RV-S&P 500 | 2.0371 | 2.0630 | |||||||

| VIX | 2.0270 | 2.0529 | |||||||

| RV-Glux | 2.0425 | 2.0684 | |||||||

| VRP | 2.0405 | 2.0664 | |||||||

| Baltic | 2.0455 | 2.0714 |

Notes: See Table 3.

Table 5.

GARCH-MIDAS for Nikkei 225.

| Variable | m | LLF | AIC | BIC | |||||

|---|---|---|---|---|---|---|---|---|---|

| RV-N225 | 3.2489 | 3.2753 | |||||||

| RV-S&P 500 | 3.2335 | 3.2599 | |||||||

| VIX | 3.2265 | 3.2530 | |||||||

| RV-Glux | 3.2425 | 3.2689 | |||||||

| VRP | 3.2437 | 3.2701 | |||||||

| Baltic | 3.2480 | 3.2745 |

Notes: See Table 3.

Table 6.

GARCH-MIDAS for Gold and Copper.

| Variable | m | LLF | AIC | BIC | |||||

|---|---|---|---|---|---|---|---|---|---|

| Panel A: Gold | |||||||||

| RV-S&P 500 | 2.6732 | 2.6990 | |||||||

| VIX | 2.6691 | 2.6949 | |||||||

| RV-Glux | 2.6788 | 2.7046 | |||||||

| Panel B: Copper | |||||||||

| RV-S&P 500 | 3.3494 | 3.3753 | |||||||

| Baltic | 3.3493 | 3.3752 | |||||||

Notes: See Table 3.

Table 7.

GARCH-MIDAS for Bitcoin specific explanatory variables

| Variable | m | LLF | AIC | BIC | |||||

|---|---|---|---|---|---|---|---|---|---|

| Google Trends (all) | 5.4295 | 5.4486 | |||||||

| Google Trends (news) | 5.4140 | 5.4331 | |||||||

| US-TV | 5.4234 | 5.4431 | |||||||

| CNY-TV | 5.1774 | 5.2011 |

Notes: See Table 3.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Conrad, C.; Custovic, A.; Ghysels, E. Long- and Short-Term Cryptocurrency Volatility Components: A GARCH-MIDAS Analysis. J. Risk Financial Manag. 2018, 11, 23. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm11020023

AMA Style

Conrad C, Custovic A, Ghysels E. Long- and Short-Term Cryptocurrency Volatility Components: A GARCH-MIDAS Analysis. Journal of Risk and Financial Management. 2018; 11(2):23. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm11020023

Chicago/Turabian StyleConrad, Christian, Anessa Custovic, and Eric Ghysels. 2018. "Long- and Short-Term Cryptocurrency Volatility Components: A GARCH-MIDAS Analysis" Journal of Risk and Financial Management 11, no. 2: 23. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm11020023