Intellectual Capital and Bank Risk in Vietnam—A Quantile Regression Approach

1

School of Banking & Finance, University of Economics and Law, Ho Chi Minh City 700000, Vietnam

2

Vietnam National University, Ho Chi Minh City 700000, Vietnam

3

Institute for Development & Research in Banking Technology, University of Economics and Law, Ho Chi Minh City 700000, Vietnam

*

Authors to whom correspondence should be addressed.

J. Risk Financial Manag. 2021, 14(1), 27; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14010027

Submission received: 10 December 2020

/

Revised: 23 December 2020

/

Accepted: 29 December 2020

/

Published: 7 January 2021

(This article belongs to the Section Banking and Finance)

Abstract

:This study empirically presents evidence of nonlinearity and heterogeneity relation between intellectual capital and risk-taking for the Vietnamese banking system. We used quantile regression methods on a data set of 30 Vietnamese banks from 2007 to 2019. The results showed that bank insolvency was positively affected by its value-added intellectual coefficient (VAIC) at the upper quantiles (i.e., 80th and 90th), while the opposite was true for credit risk (i.e., 10th and 20th quantiles). When observing the VAIC’s components, risk-taking behaviors were also significantly affected by HCE (Human Capital Efficiency), CEE (Capital Employed Efficiency) and SCE (Structural Capital Efficiency) at the 90th quantile of instability distribution and the 10th quantile of credit risk distribution. Furthermore, the results also emphasized that there was an inverse U-shaped association between intellectual capital and bank risk-taking. Therefore, this study provides important implications for policymakers, regulators, bank managers and academics that encourage increasing investment in knowledge assets to minimize bank risks in the long run.

1. Introduction

Since the late 20th century, Intellectual Capital (IC) has been received much attention from academics and practitioners because it is recognized as the hidden factors behind the significant gap between a firm’s market value and its book value (Lev 2001). Even though the idea of IC has been used for several years, there is still no clear-cut for its definition nor its classification (Sharabati et al. 2013). Nahapiet and Ghoshal (1998) define intellectual capital as the knowledge and knowing the capability of a social collectivity, such as an organization, intellectual community or professional practice. Despite no universal concept of IC, its definition still contains some common keywords, as accumulated knowledge, gained experience, intangible assets, maintaining good relationships, know-how and innovation, which help firms gain more sustainable competitive advantages and enhance their market value (Clarke et al. 2011).

There appear three main strands in the literature. Several studies have attempted to define IC from a theoretical perspective (Bontis 1998; Wu and Tsai 2005), while other have developed effective measures of IC-based performance (Pulic 2000) or explored the relationship between IC efficiency and some key characteristics of firms, industries and regions (El-Bannany 2008; Liang et al. 2011). The last common strand focuses on the effect of IC efficiency on financial performance, especially in the banking industry. Some studies confirm that banks should manage their IC as efficiently as possible because of its significant effects (Ozkan et al. 2017). Nevertheless, to the best of our knowledge, very few studies attempt to investigate the impact of IC on bank risk-taking.

Unfortunately, these studies provide mixed findings. One may argue that larger IC can help banks survive in financial distress (Curado et al. 2014; Kaupelytė and Kairytė 2016; Onumah and Duho 2019), while the other claims the negative effect of the IC’s component on bank stability (Onumah and Duho 2019). On the other hand, Ghosh and Maji (2014) emphasize that IC can reduce credit risk but there is not enough evidence to confirm its impact on bank insolvency. With regard to a certain business case, Chatzkel (2003) mentions three core issues affecting the role of intellectual capital that has been highlighted by Enron’s business failure. To be more specific, the effect of moving from a more traditional trading model to an intangible intensive trading model and the requirements for a viable intellectual capital are the main points. Because of the continuous disagreement, our study revisits this issue by examining the relationship in the Vietnamese banking system.

Vietnam’s economy has witnessed remarkable changes since entering the World Trade Organization (WTO) in 2007. Indeed, Vietnam is considered to become the next Asian dragon with an annual economic growth of approximately 6.2% from 2007 to 2009, compared to 8.36%1 of China over the same period. In which, the Vietnamese banking system is the backbone of the economy due to the fact that the capital market is still underdeveloped (Le 2019). In order to maintain healthy and sustainable stability, this requires the quality of management, shareholder’s behavior, bank’s competitive strategies, efficiency and risk management capacity. The recent banking reforms emphasize that IC is one of the increasingly important factors contributing to the success of banks; therefore, it is crucial to investigate whether IC has any effect on bank risk-taking in Vietnam.

This study contributes to the extant literature in several ways. Prior studies failed to indicate the turning point of the relationship between intellectual capital and bank performance given the non-linear relation between them due to the use of the conditional mean (Le and Nguyen 2020b). Therefore, our paper adds more evidence of the effects of IC on bank risk-taking in the context of Vietnam using a quantile regression approach. First, this approach allows us to report the full conditional distribution of bank risk-taking and to determine how IC affects banks on each quantile of the conditional distribution of risk-taking. Second, our study further determines where the turning point of the impact of IC on bank risk-taking is if the U-shaped relationship between them may exist. Last but not least, we also investigate the impact of IC’s components on bank risk-taking. It is evident that in addition to human capital, structural capital as banking information systems, databases, patents and copyrights along with keeping a good relationship with others, all play an important role in the process of risk management and enhancing the bank system solvency (Bayraktaroglu et al. 2019; Ghosh and Maji 2014). Therefore, we empirically investigate the IC and its components on bank risk-taking.

2. Literature Review

Although many studies have investigated whether IC significantly contributes to firms’ value creation (Bontis 1998; El-Bannany 2008; Liang et al. 2011; Pulic 2000; Wu and Tsai 2005), the concepts of IC and its components are still a subject of ongoing debate (Obeidat et al. 2017). There are several different definitions of IC across enormous disciplines and perspectives as economics, strategy, finance, accounting, human resources, reporting and disclosure, marketing and communication (Abhayawansa and Guthrie 2010; Bayraktaroglu et al. 2019). Based on the various definitions and the availability of data, researchers and practitioners thus have developed different measures and used them in different industries (Bontis 2001; Chen et al. 2004; Tayles et al. 2007). In more detail, they are divided into 4 sets: (1) Direct Intellectual Capital Methods (DIC); (2) Market Capitalization Methods (MCM); (3) Return on Assets Methods (ROA); and (4) Scorecard Methods (SC) (Sveiby 2010). In this study, we focus on the literature on the relationship between intellectual capital and bank risk-taking where IC is measured by the VAIC method, proposed by Pulic (2004). According to Sveiby (2010), this method is categorized into Return on Assets Methods.

Most of the studies concentrate on the impact of IC and its components on the bank performance (Buallay et al. 2019; El-Bannany 2008; Meles et al. 2016) by applying the Value-Added Intellectual Coefficient (VAIC) model and traditional accounting measures (i.e., bank profitability is proxied by Return on Asset (ROA) or Return on Equity (ROE), along with the bank market value). These studies figure out a significant influence of IC and its components on the banks’ financial performance in both developed and developing markets. Recently, Nazir et al. (2020) point out that intellectual capital efficiency has a significant and positive impact on the profitability of financial institutions in China, Taiwan and Hong Kong, while human capital and structural capital are significantly related to the performance of financial institutions only in China. Similarly, when investigating the Ghanaian banking industry, Duho (2020) concludes that intellectual capital has a positive impact on the slack-based technical efficiency of banks, in which human capital is the main driver.

Regarding bank risk-taking, mixed findings have been found in several studies. Notably, Ghosh and Maji (2014) indicate the impact of IC and its components on bank credit and insolvency risks. Their results show that IC is reciprocally associated with bank credit risk. Among the components, Human Capital Efficiency (HCE) is significant and negatively correlated with bank credit risk. However, they fail to draw a definite conclusion about the impact of IC on banks’ insolvency risk.

Nonetheless, Curado et al. (2014) state that banks with low IC score are likely to be failed in Portugal from 2005 to 2009. In the same vein, Onumah and Duho (2019) point out a positive relationship between IC and financial performance in Ghana from 2000 to 2015. Contrary to the study of Ghosh and Maji (2014), Onumah and Duho (2019) also figures out the positive and significant relationship between IC and financial stability. However, among the IC’s components, Structural Capital Efficiency (SCE) has a negative impact on both financial performance and stability while Capital Employed Efficiency (CEE) increases financial performance but reduces financial stability.

Following a similar methodology of Ghosh and Maji (2014), Kaupelytė and Kairytė (2016) investigate the impact of IC and its components on three different levels as bank profitability, effectiveness and risk management. The sample drawn in the study is based on an annual panel dataset of 118 European listed banks, covering the period of 2005–2014. The main findings of the estimated effect model show that the increase of SCE helps to increase the net interest margin in large banks. Further, an increase of HCE leads to stronger profitability ratios in small banks and better solvency ratios in large banks.

The consistency on the topic of IC and bank risk-taking is still a matter of debate. Further, the fact that banks are more opaque than other industrial firms, which leads to greater opportunities for risk-taking behaviors (Ashraf et al. 2016). From these standpoints, this study aims to provide more comprehensive evidence of the influence of IC and its components on bank risk-taking; therefore, the first hypothesis is formed as:

Hypothesis 1.

There is no impact of IC measures on bank risk-taking.

In addition, following Britto et al. (2014); Haris et al. (2019), this study is the first attempt to investigate whether a U-shaped relationship between IC measures (VAIC and its components) and bank risk-taking may exist. It is argued that when IC (and its components) goes beyond a certain threshold, it may have an inverse effect on bank risk-taking. Taken together, our second hypothesis is proposed as:

Hypothesis 2.

There is a non-existence of a non-linear relationship between IC measures and bank risk-taking.

3. Methodology and Data

3.1. Methodology

Following prior studies in banking such as Le and Nguyen (2020b), a quantile regression method as proposed by Koenker and Bassett (1978) is used. This approach is comprehensively discussed by Jiang et al. (2020) and Le and Nguyen (2020b). Also, we use the asymptotic normality of a two-step estimator as introduced by Canay (2011) to reduce intensive computation when utilizing Koenker’s technique. Hence, our quantile model is determined as follows:

where Qτ(RISKit|Xit) is the τ-th quantile-regression function. is risk-taking behavior of a bank i during year t and is measured by either credit risk or bank stability. Following Le et al. (2019), Le et al. (2020), Le (2020), bank stability is measured as where is the return on assets, is the ratio of total equity to total assets and is the standard deviation of return on assets over the examined period. A higher value of implies a greater bank stability. Moreover, credit risk is proxied by the growth rate of the ratio of non-performing loans to total loan () (Alihodžić and Ekşï 2018; Le and Ngo 2020). It is noticeable that, in our study, an inverse of Z-score is used as a proxy of bank insolvency, denoted by Z. Hence, a greater value of both and implies a higher level of risk-taking or less bank stability.

The literature suggests several alternative approaches to measure IC (Bayraktaroglu et al. 2019). Due to the unavailability of data used to measure IC, we use the conventional VAIC methodology since it provides a standardized and consistent measure (Shiu 2006) and considered innovative both theoretically and methodologically (Iazzolino and Laise 2013). Following prior studies such as Pulic (2004), Ozkan et al. (2017), Tran and Vo (2018) and others, VAIC is calculated as where represents the value added intellectual coefficient; is the capital employed efficiency; is the human capital efficiency; and represents the structural capital efficiency. To estimate the VAIC’s components, it is necessary to calculate the total value added as follows: where is operating profit of a bank; represents personnel expenses (salaries, wages and other benefits); refers to the amortization and depreciation of the bank. Then, these components of VAIC are estimated as follows where is capital employed by a bank and is measured as the book value of equity. where refers to personnel expenses. where represents structural capital and is measured as .

The literature proposes that increasing the efficiency of intellectual capital is the cheapest and safest way to ensure the sustainable operation of banks, thereby preventing banks from risk-taking. However, it can be difficult to use intangible resources efficiently. Also, higher investment in human and structural capital could reduce bank stability if management does not produce more efficiency. Therefore, we include the quadratic terms of VAIC (VAIC2) and its components (SCE2, HCE2 and CEE2) to investigate the existence of a U-shaped relationship between them and bank risk-taking.

Bit is a set of bank-specific and market-specific variables. These variables chosen in the study are similar but not identical to those adopted in prior studies, so as to better reflect the Vietnamese institutional and regulatory framework. For instance, LERN, the Lerner index to measure bank market power by price (or marginal cost to price) (Koetter et al. 2008). The higher the market power a bank has, the fewer incentives for it to take risky projects. LOAN, the ratio of total loans to total assets, is used to control for the effect of lending specialization (Le 2018). Several studies show a positive impact of bank loans on bank profitability. Ben Naceur and Goaied (2008) and Saona (2016) suggest that risk-averse shareholders seek higher earnings to compensate for higher risk because loans have higher operational costs as they need to be originated, serviced and monitored. Bank inefficiency is measured by a cost-to-income ratio ( (Le 2017). More efficient banks may control operating or monitor borrowers efficiently thus having lower risk. Alternatively, banks may skimp on operating costs by relaxing the procedure of credit monitoring and collateral valuation to accomplish short-run economic efficiency. These activities may in turn reduce loan quality, thus leading to higher risk Ghosh and Maji (2010).

For market-specific conditions, the Herfindahl-Hirschman concentration index () in terms of total assets is used to account for the effect of bank concentration (García-Herrero et al. 2009). HHI is estimated by the sum of squared of banks’ market share in total assets. A greater value of implies greater market concentration. An increase in bank profits and the franchise value is related to a highly concentrated market due to reduced competitive pressure and higher market power. Therefore, bank managers are less incentive to take more risky investments.

Finally, we also incorporate two variables annual economic growth rate () and annual inflation rate (), represented by Mt (a set of time-varying macroeconomic control variables), in the model to capture the possible effect of the business cycle on bank risk-taking.

3.2. Data

The data was manually gathered from the audited financial reports of individual banks from 2007 to 2019 on a consolidated basis according to Vietnamese Accounting Standards. It is worth noting that only 30 domestic commercial banks were considered in our study since 100% foreign-owned banks, joint-venture banks and foreign affiliates have faced some limitations on operating activities in the Vietnamese financial market. These banks together account for approximately 80% of total assets in the whole banking system. Due to several merger and acquisition activities in the examined period, an unbalanced panel data of 353 observations were obtained.2 Furthermore, the data on macroeconomic conditions were collected from the World Bank database. Table 1 provides the descriptive statistics of the variables used in this study.

The data shown in Table 1 indicate that among the three components of VAIC, HCE accounts for the highest proportion of VAIC. This is comparable with those of Ozkan et al. (2017) in Turkey and Tran and Vo (2018) in Thailand. Because there appear some negative HCE values, this arrives at some negative VAIC values due to negative HCE values. Negative HCE value is explained by the fact that banks make a loss while still paying salaries (Le and Nguyen 2020a). The same reasons are also used to explain the negative values of CEE and SCE.

Table 1 also shows that the 10th and 90th quantiles of Z are approximately 0.0% and 4.2%, while these figures of NPL are −55% and 86.1%, respectively. This indicates risk-taking, measured by bank insolvency, varies a lot from lower quantile to higher quantile. Moreover, the histogram of Z and NPL (presented in Figure 1) illustrates the skewed and heavily right-tail distribution. Such fact further reinforces the necessity of a quantile approach. Though the standard conditional mean method can be appropriate to model average risk, it cannot provide an accurate description of risk spread (Le and Nguyen 2020b; Pires et al. 2015). Additionally, we also examine whether multicollinearity among independent variables may exist. Table 2 and Table 3 present the results of the correlation matrix and variance inflation factor (VIF) values, respectively. Although there is a relatively high correlation between LERN and INF, their VIF values are less than 10, suggesting that there is no multicollinearity among them.3 Furthermore, we run the same model when including LERN and INF separately and then the same results are obtained.4

4. Results

4.1. Quantile Regression Analysis

Early studies suggest that the ordinary least squares (OLS) regression might have seriously under or overestimate effects in heterogeneous distributions (Cade and Noon 2003; Le and Nguyen 2020b). Therefore, the results of pooled OLS and panel OLS with fixed effects are not presented here due to the length restriction.

As the previous traditional regressions have not strongly explained the impacts of IC on bank insolvency though they can provide a good estimation of the bank credit risk. Moreover, neither of them can capture the whole distribution of conditional bank stability. Hence, we employ quantile regression to address the heterogeneity effects among variables along with the quantile distribution. For ease of exposition, we only focus on interpreting our main interest variables.

Table 4, Table 5, Table 6 and Table 7 present baseline results using panel quantile regression methods when bank risk-taking is proxied by both Z and NPL, respectively. Estimated coefficients are reported for the 10th, 20th, 25th, 50th, 75th, 80th and 90th percentiles of the conditional distribution of bank risk-taking. From these tables, some interesting findings can be drawn as the following.

Regarding the insolvency of the bank (Z), the coefficient of VAIC in Table 4 is generally positive and significant at the 80th and 90th quantiles. However, the sign of VAIC2 becomes negative, which verifies the nonlinearity U-shaped character of the impact of VAIC. The signs of VAIC imply that increasing investment in intellectual capital is likely to increase bank instability; however, this effect is reversed when VAIC investment reaches a certain threshold. These findings are consistent with Onumah and Duho (2019). Further, the same results are also found in credit risk (NPL), at the 10th and 20th quantiles.

When observing VAIC’s components (CEE, HCE, SCE), Table 6 shows the significant impact of HCE and SCE on Z at the 90th quantiles, while that of CEE is at 75th and 90th quantiles. A positive relationship between HCE and Z is in the line with the results of Ghosh and Maji (2014), demonstrating that investment entering HCE will increase bank insolvency because banks are too confident in participating in risky projects in short-term periods. However, we find an inverse U-shaped relationship between these variables, demonstrating a higher investment in human capital can enhance bank stability in the long run. On the other hand, the negative relationship between SCE and Z indicates that a bank, with well-controlled databases of policies and procedures, is less risky and more stable. This finding is consistent with the study of Ghosh and Maji (2014) but is in contrast to Onumah and Duho (2019). Nevertheless, too many investments in SCE may inversely impact bank risk-taking. Moreover, Table 7 also shows the significant relationship between NPL and HCE at the 10th quantile, while other components, unfortunately, show insignificant coefficients. Again, the results of HCE and NPL are the same as those of Z.

Additionally, the results from these tables also figure out several interesting points. First, we find that the coefficients of VAIC (and VAIC2) are statistically significant in higher quantiles (i.e., 80th and 90th) of Z, while the opposite is true for NPL (i.e., 10th and 20th). Second, the absolute values of estimated coefficients are different for each quantile. The magnitude is increasing from lower to higher quantiles in the distribution. Such variation validates our concerns of heterogeneity among coefficients. For the case of bank stability, Table 4 shows the estimated coefficient of VAIC at the 90th quantile is 0.032, higher than that of the 80th quantile (0.028). Similarly, the estimated coefficient of VAIC2 at the 90th quantile is −0.024, while that of the 80th quantile is −0.019. Similar findings are also found in Table 5 in regard to the relationship between VAIC and NPL.

In order to provide further insights into the non-linear relationship between IC measures and bank risk-taking, we need to estimate the turning points. It should be noted that evidence would support the inverted U-shaped relationship at the τ quantile if and where and denote the coefficients of linear and quadratic terms of VAIC at τ quantile, respectively. The turning point level of VAIC is calculated as .

More specifically, the value of turning points of the U-shaped relationship tends to be relatively small at lower quantiles and then start to increase at higher quantiles. For instance, when conditional bank insolvency is high at the 80th quantile, the turning point is 73.6%. This argues that the effect of investment in intellectual capital on bank instability will turn from positive to negative when VAIC exceeds about 73.6%. This critical level will reduce to 66.6% at the 90th quantile, implying that investments in IC may initially induce higher risk but then will gradually stabilize banks. For the VAIC’s components, the turning point of HCE is 69.0% and SCE is 26.4% at the 90th quantile.

For the 10th quantile of the credit risk (NPL), the turning point of VAIC is 50%, suggesting that the impact of investment in intellectual capital on a bank’s risk appetite will turn from negative to positive when VAIC exceeds about 50%. For banks in the 20th quantile of NPL conditional distribution, the number is up to about 100%. When breaking down, the turning point of HCE is also 50% at the 10th quantile.

4.2. Inter-Quantile Difference

Our findings specify that the impact of VAIC and its components on bank risk-taking is heterogeneous across the distributions of Z and NPL. To test whether or not these differences are statistically significant, following Koenker and Bassett (1978), the inter-quantile regressions are utilized to check for slope equality throughout the quantiles. The estimated coefficients of inter-quantile regressions are exactly the difference in coefficients of two quantiles regressions estimated separately and the estimated variance-covariance matrixes are obtained using bootstrapping methods with 200 bootstrap replications. We only present statistically significant results between upper quantiles (the 90th, 80th and 75th quantiles) and the lower quantiles (the 10th, 20th and 25th quantiles).

Table 8 indicates that heterogeneity among coefficients does exist even when controlling bank-specific and macro factors. Regarding bank insolvency, banks in upper quantiles generally have greater estimated coefficients in absolute of VAIC and VAIC2. For example, the difference between the upper quantile and the lower quantile Q(90/10) for VAIC and VAIC2 are 0.009 and −0.001, respectively, which are statistically significant at the 1% level. Table 9, on the other hand, shows only the differences in for HCE and HCE2, at 0.017 and −0.009.

In terms of credit risk, in Q (90/10) for VAIC and VAIC2, the figures are 0.004 and −0.001 and are statistically significant at 5% and 10%, respectively. Meanwhile, the difference in Q (90/10) for HCE is 0.001. Unfortunately, the coefficients of HCE2 and other components are not statistically significant.

Overall, our empirical results indicate that the influence of intellectual capital on bank risk-taking is not only U-shape but also heterogeneous across the risk-taking distribution.

Regarding the other variables, we only concentrate on interpreting those with their significant coefficients in inter-quantile regression. Accordingly, is only positively and significantly associated with Z at the higher quantiles, thus the skimp costs hypothesis may hold. Accordingly, banks may skip on operating costs through a lax approach to credit monitoring and collateral valuation to achieve short-run economic efficiency, which, in turn, reduces loan quality and thus leading to higher insolvency (Le 2018). Besides, a positive relationship between and bank risk-taking points out that a more competitive banking system is related to lower bank risk-taking. This confirms the early view of Le et al. (2020); Mirzaei et al. (2013). Finally, a negative impact of GDP on Z supports the traditional opinion that there appears an increasing demand for banks’ services and products during the cyclical upswings of the economy, which results in higher bank profitability.

4.3. Robustness Checks

It may be concerned that our study on the relationship between IC measures (VAIC and its components) and bank risk-taking may be affected by latency and indigenousness. More specifically, omitted variables and reverse causality are the most important and common problems that can lead to biased inconsistent parameter estimates. Therefore, we re-estimate the model under the two-step system General Moment Method (GMM) and the explanatory variables change with time delay in one year to avoid concurrency. For the sake of brevity, we only report our main interest variables. The results, as shown in Table 10, again confirm our above findings.

5. Conclusions

This study investigated the impact of VAIC and its components on the risk-taking behaviors of the Vietnamese banking system from 2007 to 2019 using the quantile regression method. Our study contributes to the literature by uncovering a non-linear U-shaped feature of intellectual capital (and its components) that is previously unidentified. Our main results also highlight the heterogeneity of sensitivity to intellectual capital across banks with different risk-taking levels. These results pass a robustness test of potential endogeneity, hence, provide strong evidence for our claim that there exists pronounced nonlinear heterogeneous intellectual capital impact among Vietnamese banks.

This study provides several directions for policymakers and bank managers to target at preventing banks from taking the disproportional risk. First, intellectual capital may hamper bank stability in the short term, however, investments in intellectual capital would increase stability at a certain threshold. Second, among three components of intellectual capital, structural capital (i.e., a well-controlled database of policies and procedures), however, should be moderately invested because they may threaten the bank stability if they are excessively financed.

The study has some limitations. The alternative measures of intellectual capital and risk-taking may be used to confirm our main findings. Furthermore, our study covers one emerging market and a limited period of study, suggesting that the need for future research in other emerging nations that have similar banking structure for the robustness of the results.

Author Contributions

Methodology: T.D.Q.L.; software: D.T.N.; formal analysis: T.H.H. and D.T.N.; investigation: T.D.Q.L. and D.T.N.; writing-original draft preparation: T.H.H. and D.T.N.; writing-review and editing: T.D.Q.L.; funding acquisition: T.H.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by University of Economics and Law, Vietnam National University, Ho Chi Minh City, Vietnam.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abhayawansa, Subhash, and James Guthrie. 2010. Intellectual capital and the capital market: A review and synthesis. Journal of Human Resource Costing & Accounting 14: 196–226. [Google Scholar] [CrossRef]

- Alihodžić, Almir, and İbrahim Halil Ekşï. 2018. Credit growth and non-performing loans: Evidence from Turkey and some Balkan countries. Eastern Journal of European Studies 9: 229–49. [Google Scholar]

- Arellano, Manuel, and Olympia Bover. 1995. Another look at the instrumental variable estimation of error-components models. Journal of Econometrics 68: 29–51. [Google Scholar] [CrossRef] [Green Version]

- Ashraf, Badar Nadeem, Changjun Zheng, and Sidra Arshad. 2016. Effects of national culture on bank risk-taking behavior. Research in International Business and Finance 37: 309–26. [Google Scholar] [CrossRef]

- Bayraktaroglu, Ayse Elvan, Fethi Calisir, and Murat Baskak. 2019. Intellectual capital and firm performance: An extended VAIC model. Journal of Intellectual Capital 20: 406–25. [Google Scholar] [CrossRef]

- Ben Naceur, Sami, and Mohamed Goaied. 2008. The determinants of commercial bank interest margin and profitability: Evidence from Tunisia. Frontiers in Finance and Economics 5: 106–30. [Google Scholar] [CrossRef] [Green Version]

- Bontis, Nick. 1998. Intellectual capital: An exploratory study that develops measures and models. Management Decision. [Google Scholar] [CrossRef] [Green Version]

- Bontis, Nick. 2001. Assessing knowledge assets: A review of the models used to measure intellectual capital. International Journal of Management Review 3: 41–60. [Google Scholar] [CrossRef]

- Britto, Daniel Pitelli, Eliane Monetti, and da Rocha Lima Jao Jr. 2014. Intellectual capital in tangible intensive firms: The case of Brazilian real estate companies. Journal of Intellectual Capital. [Google Scholar] [CrossRef] [Green Version]

- Buallay, Amina, Richard Cummings, and Allam Hamdan. 2019. Intellectual capital efficiency and bank’s performance: A comparative study after the global financial crisis. Pacific Accounting Review. [Google Scholar] [CrossRef]

- Cade, Brian S., and Barry R. Noon. 2003. A gentle introduction to quantile regression for ecologists. Frontiers in Ecology and the Environment 1: 412–20. [Google Scholar] [CrossRef]

- Canay, Ivan A. 2011. A simple approach to quantile regression for panel data. The Econometrics Journal 14: 368–86. [Google Scholar] [CrossRef]

- Chatzkel, Jay. 2003. The collapse of Enron and the role of intellectual capital. Journal of Intellectual Capital 4: 127–43. [Google Scholar] [CrossRef]

- Chen, Jin, Zhaohui Zhu, and Hong Yuan Xie. 2004. Measuring intellectual capital: A new model and empirical study. Journal of Intellectual Capital 5: 195–212. [Google Scholar] [CrossRef] [Green Version]

- Clarke, Martin, Dyna Seng, and Rosalind H. Whiting. 2011. Intellectual capital and firm performance in Australia. Journal of Intellectual Capital. [Google Scholar] [CrossRef] [Green Version]

- Curado, Carla, Maria João Coelho Guedes, and Nick Bontis. 2014. The Financial Crisis of Banks (before, during and after): An Intellectual Capital Perspective. Knowledge and Process Management 21. [Google Scholar] [CrossRef]

- Duho, King Carl Tornam. 2020. Intellectual capital and technical efficiency of banks in an emerging market: A slack-based measure. Journal of Economic Studies 47: 1711–32. [Google Scholar] [CrossRef]

- El-Bannany, Magdi. 2008. A study of determinants of intellectual capital performance in banks: The UK case. Journal of Intellectual Capital 9: 487–98. [Google Scholar] [CrossRef]

- García-Herrero, Alicia, Sergio Gavilá, and Daniel Santabárbara. 2009. What explains the low profitability of Chinese banks? Journal of Banking & Finance 33: 2080–92. [Google Scholar] [CrossRef] [Green Version]

- Ghosh, and Maji. 2010. Credit growth, bank soundness and financial fragility: Evidence from Indian banking sector. South Asia Economic Journal 11: 69–98. [Google Scholar] [CrossRef] [Green Version]

- Ghosh, and Maji. 2014. The impact of intellectual capital on bank risk: Evidence from Indian banking sector. IUP Journal of Financial Risk Management 11: 18. [Google Scholar]

- Hair, Joseph F., William C. Black, Barry J. Babin, and Rolph E. Anderson. 2010. Multivariate Data Analysis, 7th ed. Upper Saddle River: Prentice Hall. [Google Scholar]

- Haris, Muhammad, HongXing Yao, Gulzara Tariq, Ali Malik, and Hafiz Mustansar Javaid. 2019. Intellectual capital performance and profitability of banks: Evidence from Pakistan. Journal of Risk and Financial Management 12: 56. [Google Scholar] [CrossRef] [Green Version]

- Iazzolino, Gianpaolo, and Domenico Laise. 2013. Value added intellectual coefficient (VAIC): A methodological and critical review. Journal of Intellectual Capital 14: 547–63. [Google Scholar] [CrossRef]

- Jiang, Hai, Jinyi Zhang, and Chen Sun. 2020. How does capital buffer affect bank risk-taking? New evidence from China using quantile regression. China Economic Review 60: 101300. [Google Scholar] [CrossRef]

- Kaupelytė, Dalia, and Deimantė Kairytė. 2016. Intellectual Capital Efficiency Impact on European Small and Large Listed Banks Financial Performance. International Journal of Management, Accounting and Economics 3: 367–77. [Google Scholar]

- Koenker, Roger, and Gilbert Bassett Jr. 1978. Regression quantiles. Econometrica: Journal of the Econometric Society, 33–50. [Google Scholar] [CrossRef]

- Koetter, Michael, James Kolari, and Laura Spierdijk. 2008. Efficient competition? Testing the ‘quiet life’ of US banks with adjusted Lerner indices. Paper presented at the 44th ‘Bank Structure and Competition’ Conference, Federal Reserve Bank of Chicago, Chicago, IL, USA, May 14–15. [Google Scholar]

- Le, Tu D. Q. 2017. The efficiency effects of bank mergers: An analysis of case studies in Vietnam. Risk Governance & Control: Financial Markets & Institutions 7: 61–70. [Google Scholar] [CrossRef] [Green Version]

- Le, Tu D. Q. 2018. Bank risk, capitalisation and technical efficiency in the Vietnamese banking system. Australasian Accounting, Business and Finance Journal 12: 41–61. [Google Scholar] [CrossRef]

- Le, Tu D. Q. 2019. The interrelationship between liquidity creation and bank capital in Vietnamese banking. Managerial Finance 45: 331–47. [Google Scholar] [CrossRef]

- Le, Tu D. Q. 2020. The interrelationship among bank profitability, bank stability and loan growth: Evidence from Vietnam. Cogent Business & Management 7: 1–18. [Google Scholar] [CrossRef]

- Le, Tu D. Q., and Thanh Ngo. 2020. The determinants of bank profitability: A cross-country analysis. Central Bank Review 20: 65–73. [Google Scholar] [CrossRef]

- Le, Tu D. Q., and Dat T. Nguyen. 2020a. Intellectual capital and bank profitability: New evidence from Vietnam. Cogent Business & Management 7. [Google Scholar] [CrossRef]

- Le, Tu D. Q., and Dat T. Nguyen. 2020b. Capital Structure and Bank Profitability in Vietnam: A Quantile Regression Approach. Journal of Risk and Financial Management 13: 168. [Google Scholar] [CrossRef]

- Le, Tu D. Q., Son. H. Tran, and Liem T. Nguyen. 2019. The impact of multimarket contacts on bank stability in Vietnam. Pacific Accounting Review 31: 336–57. [Google Scholar] [CrossRef]

- Le, Tu D. Q., Van T. H. Nguyen, and Son H. Tran. 2020. Geographic loan diversification and bank risk: A cross-country analysis. Cogent Economics & Finance 8: 1809120. [Google Scholar] [CrossRef]

- Lev, Baruch. 2001. Intangibles: Management. Washington, DC: Measurement and Reporting. [Google Scholar]

- Liang, Chiung Ju, Tzu Tsang Huang, and Wen Cheng Lin. 2011. Does ownership structure affect firm value? Intellectual capital across industries perspective. Journal of Intellectual Capital 12: 552–70. [Google Scholar] [CrossRef]

- Meles, Antonio, Claudio Porzio, Gabriele Sampagnaro, and Vincenzo Verdoliva. 2016. The impact of the Intellectual Capital Efficiency on Commercial Banks Performance: Evidence from the US. Journal of Multinational Financial Management 36: 64–74. [Google Scholar] [CrossRef]

- Mirzaei, Ali, Tomoe Moore, and Guy Liu. 2013. Does market structure matter on banks’ profitability and stability? Emerging vs. advanced economies. Journal of Banking & Finance 37: 2920–37. [Google Scholar] [CrossRef]

- Nahapiet, and Ghoshal. 1998. Social capital, intellectual capital and the organizational advantage. Academy of Management Review 23: 242–66. [Google Scholar] [CrossRef]

- Nazir, Muhammad Imran, Tan Yong, and Muhammad Rizwan Nazir. 2020. Intellectual capital performance in the financial sector: Evidence from China, Hong Kong and Taiwan. International Journal of Finance and Economics. [Google Scholar] [CrossRef]

- Obeidat, Bader Y., Ali Tarhini, Ra’Ed. Masa’deh, and Noor Aqqad. 2017. The impact of intellectual capital on innovation via the mediating role of knowledge management: A structural equation modelling approach. International Journal of Knowledge Management Studies 8: 273–98. [Google Scholar] [CrossRef]

- Onumah, Joseph Mensah, and King Carl Tornam Duho. 2019. Intellectual capital: Its impact on financial performance and financial stability of Ghanaian banks. Athens Journal of Business and Economics 5: 243–68. [Google Scholar] [CrossRef]

- Ozkan, Nasif, Sinan Cakan, and Murad Kayacan. 2017. Intellectual capital and financial performance: A study of the Turkish banking sector. Borsa Istanbul Review 17: 190–98. [Google Scholar] [CrossRef] [Green Version]

- Pires, Pedro, Pedro Pereira João, and Filipe Martins Luis. 2015. The Empirical Determinants of Credit Defaut Swap Spreads: A Quantile Regression Approach. European Financia Management 21: 556–89. [Google Scholar] [CrossRef]

- Pulic, Ante. 2000. VAIC™—An accounting tool for IC management. International Journal of Technology Management 20: 702–14. [Google Scholar] [CrossRef]

- Pulic, Ante. 2004. Intellectual capital—Does it create or destroy value? Measuring Business Excellence. [Google Scholar] [CrossRef] [Green Version]

- Saona, Paolo. 2016. Intra-and extra-bank determinants of Latin American Banks’ profitability. International Review of Economics & Finance 45: 197–214. [Google Scholar] [CrossRef] [Green Version]

- Sharabati, Abdel-Aziz Ahmad, Abdulnaser Ibrahim Nour, and Yacoub Adel N. Eddin. 2013. Intellectual capital development: A case study of middle east university. Jordan Journal of Business Administration 153: 1–72. [Google Scholar] [CrossRef]

- Shiu, Huei-Jen. 2006. The application of the value added intellectual coefficient to measure corporate performance: Evidence from technological firms. International Journal of Management 23: 356–65. [Google Scholar]

- Sveiby, Karl Erik. 2010. Methods for Measuring Intangible Assets. Available online: https://www.sveiby.com/article/Methods-for-Measuring-Intangible-Assets (accessed on 23 December 2020).

- Tayles, Mike, Richard H. Pike, and Saudah Sofian. 2007. Intellectual capital, management accounting practices and corporate performance: Perceptions of managers. Accounting Auditing & Accountability Journal 20: 522–48. [Google Scholar] [CrossRef]

- Tran, Dai Binh, and Duc Hong Vo. 2018. Should bankers be concerned with Intellectual capital? A study of the Thai banking sector. Journal of Intellectual Capital 19: 897–914. [Google Scholar] [CrossRef]

- Wu, Wann-Yih, and Hsin-Ju Tsai. 2005. Impact of social capital and business operation mode on intellectual capital and knowledge management. International Journal of Technology Management 30: 147–71. [Google Scholar] [CrossRef]

| 1 | As reported by the National Bureau of Statistics of China. |

| 2 | |

| 3 | Any VIF exceeding 10 indicates a problem of multicollinearity (Hair et al. 2010). |

| 4 | The table of results cannot be presented here due to the length restriction. However, they are available upon request. |

Figure 1.

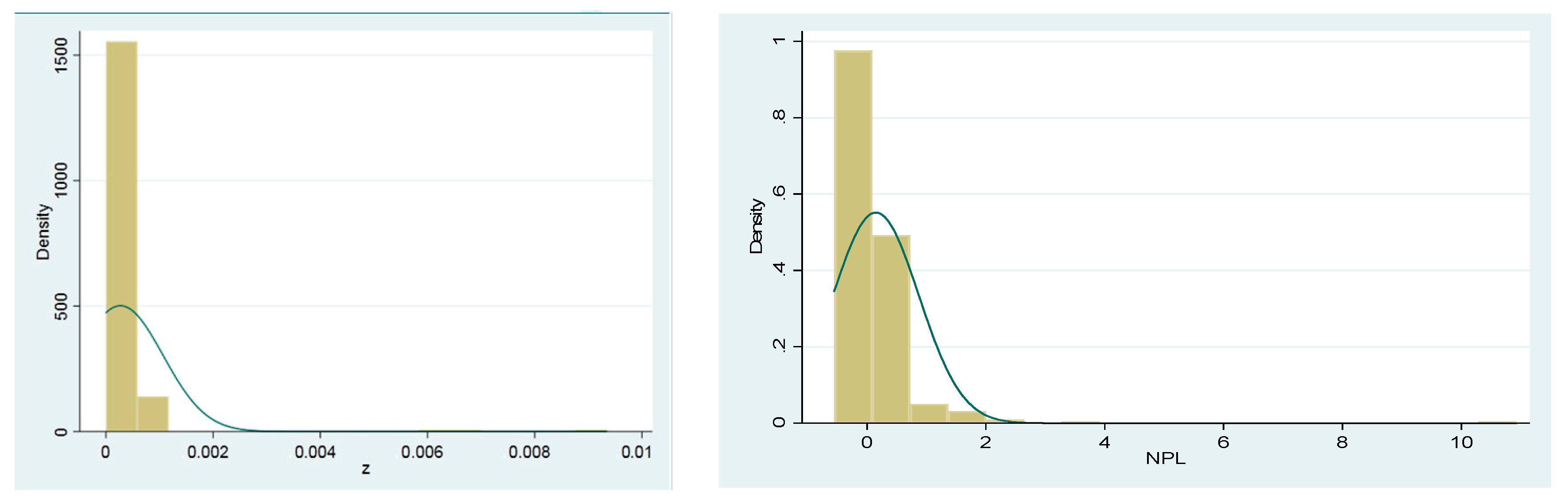

Histogram for Z and NPL.

{kind=link}

Table 1.

The descriptive statistics of variables.

| Variables | Obs. | Mean | SD | Min | Q (10) | Median | Q (90) | Max |

|---|---|---|---|---|---|---|---|---|

| Z | 353 | 0.024 | 0.117 | 0.001 | 0.002 | 0.005 | 0.042 | 1.732 |

| NPL | 353 | 0.149 | 0.722 | −0.550 | −0.243 | 0.020 | 0.861 | 10.927 |

| VAIC | 353 | 4.783 | 2.278 | −2.452 | 2.893 | 4.439 | 6.804 | 19.452 |

| CEE | 353 | 0.289 | 0.138 | −0.045 | 0.145 | 0.276 | 0.488 | 0.826 |

| HCE | 353 | 3.775 | 2.147 | −0.737 | 2.100 | 3.407 | 5.651 | 18.636 |

| SCE | 353 | 0.668 | 0.279 | −2.767 | 0.533 | 0.706 | 0.823 | 2.356 |

| LERN | 353 | 0.105 | 0.033 | 0.069 | 0.071 | 0.101 | 0.158 | 0.169 |

| LOAN | 353 | 0.547 | 0.137 | 0.113 | 0.365 | 0.566 | 0.713 | 0.851 |

| CIR | 353 | 0.154 | 0.076 | 0.040 | 0.080 | 0.140 | 0.220 | 0.640 |

| HHI | 353 | 0.087 | 0.014 | 0.072 | 0.077 | 0.081 | 0.117 | 0.119 |

| GDP | 353 | 0.062 | 0.007 | 0.052 | 0.054 | 0.062 | 0.071 | 0.084 |

| INF | 353 | 0.076 | 0.062 | 0.006 | 0.026 | 0.065 | 0.186 | 0.231 |

Table 2.

Correlation matrix.

| Z | NPL | VAIC | CEE | HCE | SCE | LOAN | LERN | CIR | HHI | GDP | INF | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Z | 1.000 | |||||||||||

| NPL | −0.040 | 1.000 | ||||||||||

| VAIC | 0.089 | 0.105 | 1.000 | |||||||||

| CEE | 0.279 | −0.101 | 0.207 | 1.000 | ||||||||

| HCE | 0.067 | 0.115 | 0.320 | 0.130 | 1.000 | |||||||

| SCE | 0.070 | 0.047 | 0.586 | 0.176 | 0.507 | 1.000 | ||||||

| LOAN | 0.043 | −0.169 | −0.129 | 0.326 | −0.149 | −0.124 | 1.000 | |||||

| LERN | 0.104 | 0.132 | 0.305 | −0.059 | 0.308 | 0.220 | −0.367 | 1.000 | ||||

| CIR | −0.006 | −0.058 | −0.171 | −0.002 | −0.157 | −0.240 | 0.038 | −0.288 | 1.000 | |||

| HHI | 0.026 | −0.069 | −0.007 | 0.417 | −0.039 | 0.004 | 0.391 | 0.018 | 0.158 | 1.000 | ||

| GDP | −0.106 | −0.149 | −0.094 | 0.188 | −0.107 | −0.068 | 0.264 | −0.469 | 0.082 | −0.046 | 1.000 | |

| INF | 0.084 | 0.127 | 0.298 | −0.013 | 0.296 | 0.224 | −0.335 | 0.959 | −0.280 | 0.014 | −0.361 | 1.000 |

Table 3.

Variance Inflation Factor (VIF) results.

| Variable | VIF (Z) | VIF (NPL) | VIF (Z) | VIF (NPL) |

|---|---|---|---|---|

| VAIC | 1.11 | 1.14 | - | - |

| CEE | - | - | 1.40 | 1.42 |

| HCE | - | - | 1.42 | 1.39 |

| SCE | - | - | 1.43 | 1.41 |

| LOAN | 1.48 | 1.41 | 1.53 | 1.45 |

| LERN | 8.03 | 5.46 | 7.06 | 5.50 |

| CIR | 1.16 | 1.22 | 1.20 | 1.32 |

| HHI | 1.30 | 1.32 | 1.50 | 1.58 |

| GDP | 1.99 | 1.49 | 2.03 | 1.51 |

| INF | 6.57 | 4.16 | 5.60 | 4.18 |

| Mean VIF | 3.09 | 2.31 | 2.57 | 2.20 |

Table 4.

Baseline results for Z and VAIC: Quantile regression.

| Quantiles | 0.10 | 0.20 | 0.25 | 0.50 | 0.75 | 0.80 | 0.90 |

|---|---|---|---|---|---|---|---|

| VAIC | 0.000 | 0.000 | 0.005 | 0.014 | 0.021 | 0.028 ** | 0.032 ** |

| (0.000) | (0.002) | (0.005) | (0.012) | (0.018) | (0.022) | (0.025) | |

| VAIC2 | −0.000 | −0.000 | −0.001 | −0.008 | −0.013 | −0.019 ** | −0.024 ** |

| (0.000) | (0.001) | (0.000) | (0.004) | (0.006) | (0.010) | (0.016) | |

| LERN | 0.000 | 0.000 | 0.000 | 0.155 | 0.292 | 0.475 | 0.281 |

| (0.000) | (0.000) | (0.011) | (0.169) | (0.250) | (0.333) | (0.482) | |

| LOAN | 0.000 | 0.000 | 0.000 | 0.021 * | 0.059 *** | 0.054 ** | 0.021 * |

| (0.000) | (0.000) | (0.001) | (0.012) | (0.180) | (0.022) | (0.034) | |

| CIR | 0.000 | −0.000 | −0.000 | 0.011 | 0.009 | −0.007 | 0.045 |

| (0.000) | (0.000) | (0.001) | (0.020) | (0.029) | (0.037) | (0.056) | |

| HHI | 0.000 | −0.000 | −0.000 | 0.123 | −0.716 ** | −0.939 ** | −1.090 |

| (0.000) | (0.001) | (0.017) | (0.248) | (0.417) | (0.457) | (0.691) | |

| GDP | 0.000 | −0.000 | −0.000 | −0.059 | −0.515 | −0.578 | −0.653 |

| (0.000) | (0.001) | (0.015) | (0.255) | (0.387) | (0.425) | (0.642) | |

| INF | 0.000 | −0.000 | −0.000 | −0.047 | −0.036 | −0.010 | −0.067 |

| (0.000) | (0.000) | (0.002) | (0.034) | (0.056) | (0.061) | (0.093) | |

| Constant | 0.000 | 0.000 | 0.000 | −0.025 | −0.026 | 0.004 | −0.028 |

| (0.000) | (0.000) | (0.001) | (0.025) | (0.037) | (0.032) | (0.072) | |

| No. Obs | 320 | 320 | 320 | 320 | 320 | 320 | 320 |

| Pseudo R2 | 0.000 | 0.000 | 0.000 | 0.065 | 0.071 | 0.082 | 0.102 |

Note: This table presents pooled quantile regression for the 10th, 20th, 25th, 50th, 75th, 80th and 90th quantiles. The dependent variable is Z. Standard errors are in parentheses. *, ** and *** denote statistical significance at 10%, 5% and 1%, respectively.

Table 5.

Baseline results for NPL and VAIC: Quantile regression.

| Quantiles | 0.10 | 0.20 | 0.25 | 0.50 | 0.75 | 0.80 | 0.90 |

|---|---|---|---|---|---|---|---|

| VAIC | 0.001 ** | 0.002 * | 0.004 | −0.002 | −0.008 | −0.001 | −0.003 |

| (0.005) | (0.007) | (0.005) | (0.007) | (0.011) | (0.001) | (0.002) | |

| VAIC2 | −0.001 *** | −0.001 * | −0.003 ** | 0.001 | 0.007 | 0.005 | 0.006 |

| (0.000) | (0.000) | (0.005) | (0.003) | (0.000) | (0.000) | (0.000) | |

| LERN | 0.000 | 0.000 | 0.000 | 0.143 | 0.281 | 0.475 | 0.281 |

| (0.000) | (0.000) | (0.011) | (0.169) | (0.250) | (0.333) | (0.482) | |

| LOAN | 0.000 | 0.000 * | 0.000 | 0.021 * | 0.046 | 0.034 | 0.021 ** |

| (0.000) | (0.000) | (0.001) | (0.012) | (0.180) | (0.022) | (0.034) | |

| CIR | 0.000 | −0.000 | −0.000 | 0.011 | 0.009 | −0.007 | 0.045 |

| (0.000) | (0.000) | (0.001) | (0.020) | (0.029) | (0.037) | (0.056) | |

| HHI | 0.000 | −0.000 | −0.000 | 0.123 | −0.716 | −0.939 | −1.090 * |

| (0.000) | (0.001) | (0.017) | (0.248) | (0.417) | (0.457) | (0.691) | |

| GDP | 0.000 | −0.000 | −0.000 | −0.059 | −0.515 | −0.578 | −0.653 |

| (0.000) | (0.001) | (0.015) | (0.255) | (0.387) | (0.425) | (0.642) | |

| INF | 0.000 | −0.000 | −0.000 | −0.047 | −0.036 | −0.010 | −0.067 |

| (0.000) | (0.000) | (0.002) | (0.034) | (0.056) | (0.061) | (0.093) | |

| Constant | 0.033 | 0.034 | 0.028 | 0.044 | 0.065 | 0.089 | 0.131 |

| (0.009) | (0.007) | (0.008) | (0.011) | (0.016) | (0.020) | (0.035) | |

| No. Obs. | 367 | 367 | 367 | 367 | 367 | 367 | 367 |

| Pseudo R2 | 0.125 | 0.105 | 0.126 | 0.178 | 0.253 | 0.277 | 0.346 |

Note: This table presents pooled quantile regression for the 10th, 20th, 25th, 50th, 75th, 80th and 90th quantiles. The dependent variable is NPL. Standard errors are in parentheses. *, ** and *** denote statistical significance at 10%, 5% and 1%, respectively.

Table 6.

Baseline results for Z and VAIC’s components: Quantile regression.

| Quantiles | 0.10 | 0.20 | 0.25 | 0.50 | 0.75 | 0.80 | 0.90 |

|---|---|---|---|---|---|---|---|

| CEE | 0.000 | −0.000 | −0.000 | 0.029 | 0.103 * | 0.067 | 0.202 * |

| (0.000) | (0.005) | (1.180) | (0.044) | (0.057) | (0.082) | (0.108) | |

| CEE2 | −0.000 | 0.000 | 0.000 | 0.038 | −0.021 | 0.007 | −0.168 |

| (0.000) | (0.007) | (1.510) | (0.058) | (0.075) | (0.108) | (0.141) | |

| HCE | −0.000 | −0.000 | 0.000 | 0.006 | 0.015 | 0.024 | 0.029 * |

| (0.000) | (0.000) | (0.062) | (0.002) | (0.008) | (0.015) | (0.020) | |

| HCE2 | 0.000 | −0.000 | −0.000 | −0.003 | −0.009 | −0.015 | −0.021 * |

| (0.000) | (0.000) | (0.003) | (0.002) | (0.008) | (0.012) | (0.015) | |

| SCE | 0.000 | −0.000 | −0.000 | −0.003 | −0.005 | −0.006 | −0.070 * |

| (0.000) | (0.002) | (0.422) | (0.017) | (0.021) | (0.031) | (0.040) | |

| SCE2 | 0.000 | 0.000 | 0.000 | 0.003 | 0.009 | 0.009 | 0.037 * |

| (0.000) | (0.001) | (0.220) | (0.009) | (0.011) | (0.016) | (0.021) | |

| LERN | 0.000 | 0.000 | 0.000 | 0.200 | 0.502 ** | 0.553 * | 0.395 |

| (0.000) | (0.000) | (0.040) | (0.169) | (0.220) | (0.315) | (0.413) | |

| LOAN | 0.000 ** | 0.000 | 0.000 | 0.012 | 0.036 ** | 0.050 ** | 0.046 |

| (0.000) | (0.001) | (0.516) | (0.012) | (0.016) | (0.023) | (0.030) | |

| CIR | −0.000 * | −0.000 | −0.000 | −0.007 | 0.032 | 0.052 | 0.103 |

| (0.000) | (0.002) | (0.503) | (0.020) | (0.026) | (0.037) | (0.049) | |

| HHI | −0.000 | −0.000 | −0.000 | −0.205 | −1.080 *** | −1.221 ** | −1.725 *** |

| (0.000) | (0.035) | (6.607) | (0.265) | (0.344) | (0.493) | (0.647) | |

| GDP | −0.000 *** | −0.000 *** | −0.000 | −0.215 | −0.302 | −0.203 | −1.044 * |

| (0.000) | (0.031) | (5.903) | (0.258) | (0.335) | (0.480) | (0.629) | |

| INF | −0.000 | −0.000 | −0.000 | −0.117 | −0.312 ** | −0.305 | −0.171 |

| (0.000) | (0.004) | (0.832) | (0.106) | (0.138) | (0.198) | (0.259) | |

| Constant | 0.000 | 0.000 | 0.000 | −0.009 | −0.046 | −0.062 | −0.003 |

| (0.000) | (0.002) | (0.557) | (0.025) | (0.033) | (0.047) | (0.062) | |

| No. Obs | 320 | 320 | 320 | 320 | 320 | 320 | 320 |

| Pseudo R2 | 0.000 | 0.000 | 0.000 | 0.118 | 0.152 | 0.158 | 0.189 |

Note: This table presents pooled quantile regression for the 10th, 20th, 25th, 50th, 75th, 80th and 90th quantiles. The dependent variable is Z. Standard errors are in parentheses. *, ** and *** denote statistical significance at 10%, 5% and 1%, respectively.

Table 7.

Baseline results for NPL and VAIC’s components: Quantile regression.

| Quantiles | 0.10 | 0.20 | 0.25 | 0.50 | 0.75 | 0.80 | 0.90 |

|---|---|---|---|---|---|---|---|

| CEE | 0.050 | 0.044 | 0.045 | 0.035 | −0.045 | −0.067 | −0.168 |

| (0.015) | (0.015) | (0.017) | (0.020) | (0.035) | (0.040) | (0.068) | |

| CEE2 | −0.050 ** | −0.045 | −0.044 | −0.041 | 0.045 | 0.063 | 0.172 |

| (0.020) | (0.020) | (0.023) | (0.027) | (0.048) | (0.054) | (0.092) | |

| HCE | 0.001 ** | 0.005 | 0.004 | −0.005 | −0.003 | −0.003 | −0.001 |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.001) | (0.001) | (0.003) | |

| HCE2 | −0.001 ** | −0.000 | −0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |

| SCE | −0.003 | 0.009 | 0.009 | 0.015 | 0.017 | 0.016 | 0.012 |

| (0.002) | (0.002) | (0.002) | (0.002) | (0.005) | (0.00) | (0.010) | |

| SCE2 | 0.002 | 0.003 | 0.003 | 0.004 | 0.003 | 0.002 | −0.001 |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.002) | (0.003) | (0.004) | |

| LERN | 0.000 | 0.000 | 0.000 | 0.200 | 0.502 | 0.553 * | 0.395 |

| (0.000) | (0.000) | (0.040) | (0.169) | (0.220) | (0.315) | (0.413) | |

| LOAN | 0.000 ** | 0.000 | 0.000 | 0.012 | 0.036 | 0.050 ** | 0.046 |

| (0.000) | (0.001) | (0.516) | (0.012) | (0.016) | (0.023) | (0.030) | |

| CIR | −0.000 * | −0.000 | −0.000 | −0.007 | 0.032 | 0.052 | 0.103 |

| (0.000) | (0.002) | (0.503) | (0.020) | (0.026) | (0.037) | (0.049) | |

| HHI | −0.000 | −0.000 | −0.000 | −0.205 | −1.080 | −1.221 ** | −1.725 * |

| (0.000) | (0.035) | (6.607) | (0.265) | (0.344) | (0.493) | (0.647) | |

| GDP | −0.000 * | −0.000 ** | −0.000 | −0.215 | −0.302 | −0.203 | −1.044 * |

| (0.000) | (0.031) | (5.903) | (0.258) | (0.335) | (0.480) | (0.629) | |

| INF | −0.000 | −0.000 | −0.000 | −0.117 | −0.312 ** | −0.305 | −0.171 |

| (0.000) | (0.004) | (0.832) | (0.106) | (0.138) | (0.198) | (0.259) | |

| Constant | 0.004 | 0.009 | 0.006 | 0.006 | 0.020 | 0.026 | 0.131 |

| (0.003) | (0.003) | (0.003) | (0.004) | (0.007) | (0.008) | (0.035) | |

| No. Obs. | 367 | 367 | 367 | 367 | 367 | 367 | 367 |

| Pseudo R2 | 0.101 | 0.062 | 0.059 | 0.072 | 0.099 | 0.118 | 0.139 |

Note: This table presents pooled quantile regression for the 10th, 20th, 25th, 50th, 75th, 80th and 90th quantiles. The dependent variable is NPL. Standard errors are in parentheses. * and ** denote statistical significance at 10% and 5%, respectively.

Table 8.

The results of inter-quantile regression VAIC.

| Z | NPL | |||

|---|---|---|---|---|

| Inter-Quantile | (90–10) | (80–20) | (75–25) | (90–10) |

| VAIC | 0.009 *** | 0.019 *** | 0.028 *** | 0.004 ** |

| (0.004) | (0.002) | (0.002) | (0.004) | |

| VAIC2 | −0.001 *** | −0.012 *** | −0.015 ** | −0.001 * |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| LERN | 0.003 | 0.476 | 0.292 | 0.001 |

| (0.004) | (0.323) | (0.309) | (0.003) | |

| LOAN | 0.059 | 0.053 | 0.059 *** | 0.021 |

| (0.052) | (0.030) | (0.013) | (0.032) | |

| CIR | 0.081 | −0.001 * | 0.009 | 0.031 |

| (0.105) | (0.049) | (0.031) | (0.027) | |

| HHI | −0.167 | −0.744 *** | −0.863 *** | −0.005 ** |

| (0.716) | (0.259) | (0.238) | (0.012) | |

| GDP | −0.213 | −0.380 | −0.466 | 0.032 |

| (0.602) | (0.409) | (0.381) | (0.235) | |

| INF | −0.125 | −0.249 | −0.138 | 0.013 |

| (0.346) | (0.202) | (0.188) | (0.032) | |

| Constant | −0.034 | −0.037 | −0.027 | 0.097 |

| (0.108) | (0.041) | (0.037) | (0.037) | |

| No. Obs | 320 | 320 | 320 | 367 |

Notes: This table shows the difference in quantile regression estimates for an inter-quantile regression: , . The bootstrapped cluster standard errors (in parentheses) are obtained with 200 bootstrap replications. *, ** and *** denote statistical significance at 10%, 5% and 1%, respectively.

Table 9.

The results of inter-quantile regression VAIC’s components.

| Z | NPL | |

|---|---|---|

| Inter Quantile | (90–10) | (90–10) |

| CEE | 0.202 | 0.216 |

| (0.083) | (0.083) | |

| CEE2 | −0.168 | −0.242 |

| (0.113) | (0.122) | |

| HCE | 0.017 ** | 0.001 * |

| (0.022) | (0.004) | |

| HCE2 | −0.009 * | −0.000 |

| (0.002) | (0.000) | |

| SCE | −0.070 | −0.014 |

| (0.062) | (0.044) | |

| SCE2 | 0.037 | 0.002 ** |

| (0.083) | (0.001) | |

| LERN | 0.395 | 0.247 |

| (0.362) | (0.432) | |

| LOAN | 0.103 * | 0.012 |

| (0.055) | (0.028) | |

| CIR | −1.725 * | 0.023 |

| (0.311) | (0.012) | |

| HHI | −1.044 *** | −0.143 * |

| (0.564) | (0.023) | |

| GDP | −0.171 * | −0.176 |

| (0.233) | (0.132) | |

| INF | −0.003 | −0.005 |

| (0.053) | (0.032) | |

| Constant | 0.202 | 0.082 |

| (0.083) | (0.030) | |

| No. Obs | 320 | 367 |

Notes: This table shows the difference in quantile regression estimates for an inter-quantile regression: . The bootstrapped cluster standard errors (in parentheses) are obtained with 200 bootstrap replications. *, ** and *** denote statistical significance at 10%, 5% and 1%, respectively.

Table 10.

VAIC, VAIC’s components and Z, using system GMM.

| Z | NPL | |||

|---|---|---|---|---|

| VAIC | VAIC’s Components | VAIC | VAIC’s Components | |

| πt−1 | 0.170 *** | 0.069 ** | 0.076 *** | 0.075 *** |

| (0.005) | (0.028) | (0.020) | (0.017) | |

| VAIC | 0.135 *** | 0.133 *** | ||

| (0.026) | (0.045) | |||

| CEE | 4.248 *** | −0.363 | ||

| (0.641) | (0.820) | |||

| HCE | 0.053 ** | 0.092 ** | ||

| (0.024) | (0.044) | |||

| SCE | −1.725 *** | −0.331 | ||

| (0.454) | (0.204) | |||

| Constant | 2.053 | 3.773 | −2.112 | −1.546 |

| (0.223) | (0.629) | (0.478) | (0.294) | |

| No. Obs. | 291 | 291 | 309 | 309 |

| No. of Groups | 30 | 30 | 30 | 30 |

| AR1 (p-value) | 0.056 | 0.064 | 0.001 | 0.002 |

| AR2 (p-value) | 0.377 | 0.336 | 0.558 | 0.348 |

| Hansen test (p-value) | 0.883 | 0.956 | 0.239 | 0.837 |

Notes: The table contains the results estimated using the system GMM estimator. Variables in italics are instrumented through the GMM procedure following Arellano and Bover (1995). Robust standard errors are in parentheses. ** and ***Significant at 5 and 1 per cent levels, respectively.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Nguyen, D.T.; Le, T.D.Q.; Ho, T.H. Intellectual Capital and Bank Risk in Vietnam—A Quantile Regression Approach. J. Risk Financial Manag. 2021, 14, 27. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14010027

AMA Style

Nguyen DT, Le TDQ, Ho TH. Intellectual Capital and Bank Risk in Vietnam—A Quantile Regression Approach. Journal of Risk and Financial Management. 2021; 14(1):27. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14010027

Chicago/Turabian StyleNguyen, Dat T., Tu D. Q. Le, and Tin H. Ho. 2021. "Intellectual Capital and Bank Risk in Vietnam—A Quantile Regression Approach" Journal of Risk and Financial Management 14, no. 1: 27. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14010027