Stacking Subsidies in Factor Markets: Evidence from Market Experiments

Abstract

:1. Introduction

2. Literature Review

2.1. Subsidy Incidence: Theoretical Consideration

2.2. Empirical Analyses of Subsidy Incidence

2.3. Behavioral Issues on Tax and Subsidy Incidence

2.4. Demand and Supply in Ethanol Market

3. Structure of Agriculture and Energy Markets

4. Experimental Design

5. Data and Econometric Model

6. Results

6.1. Prices

6.2. Trades

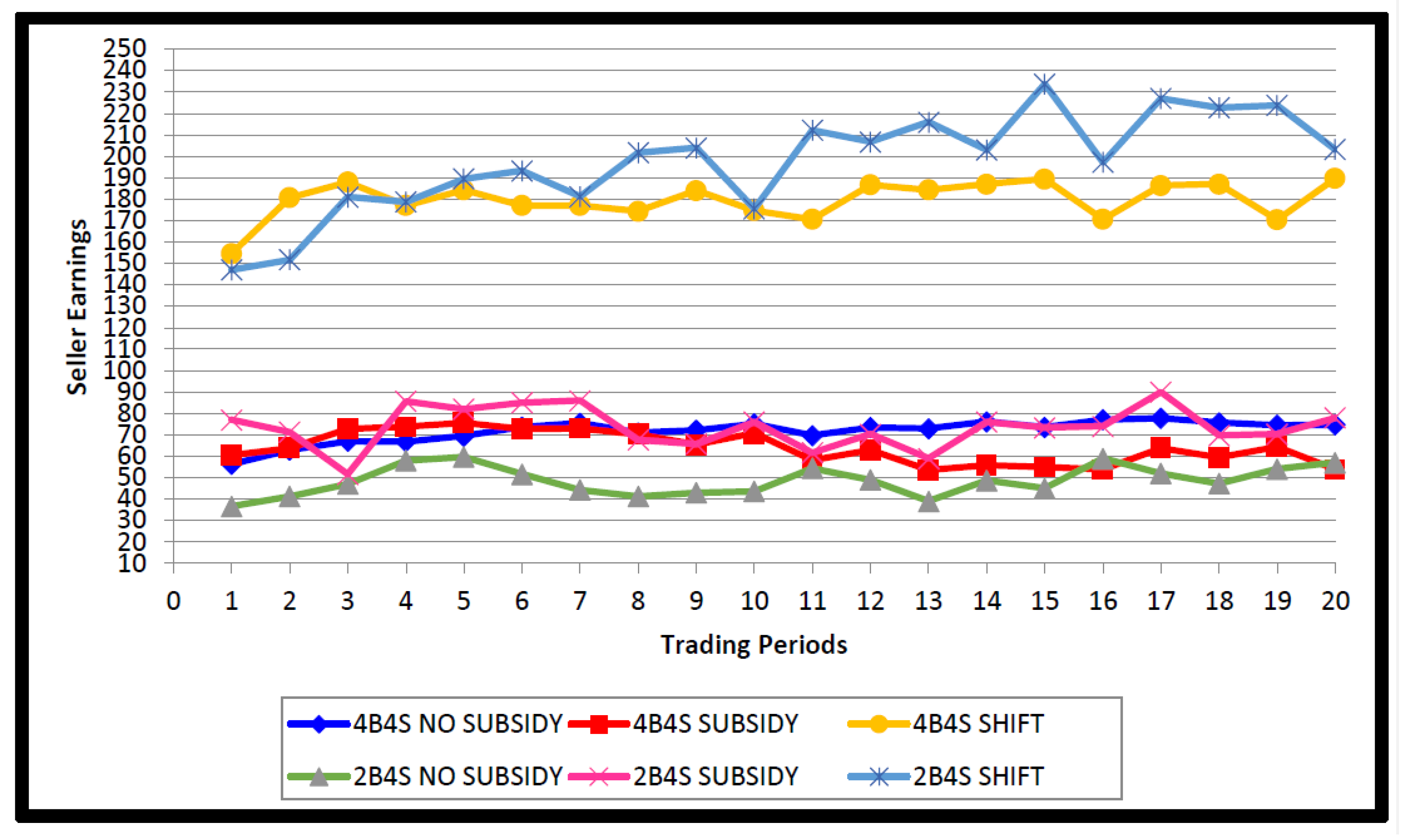

6.3. Seller Earnings

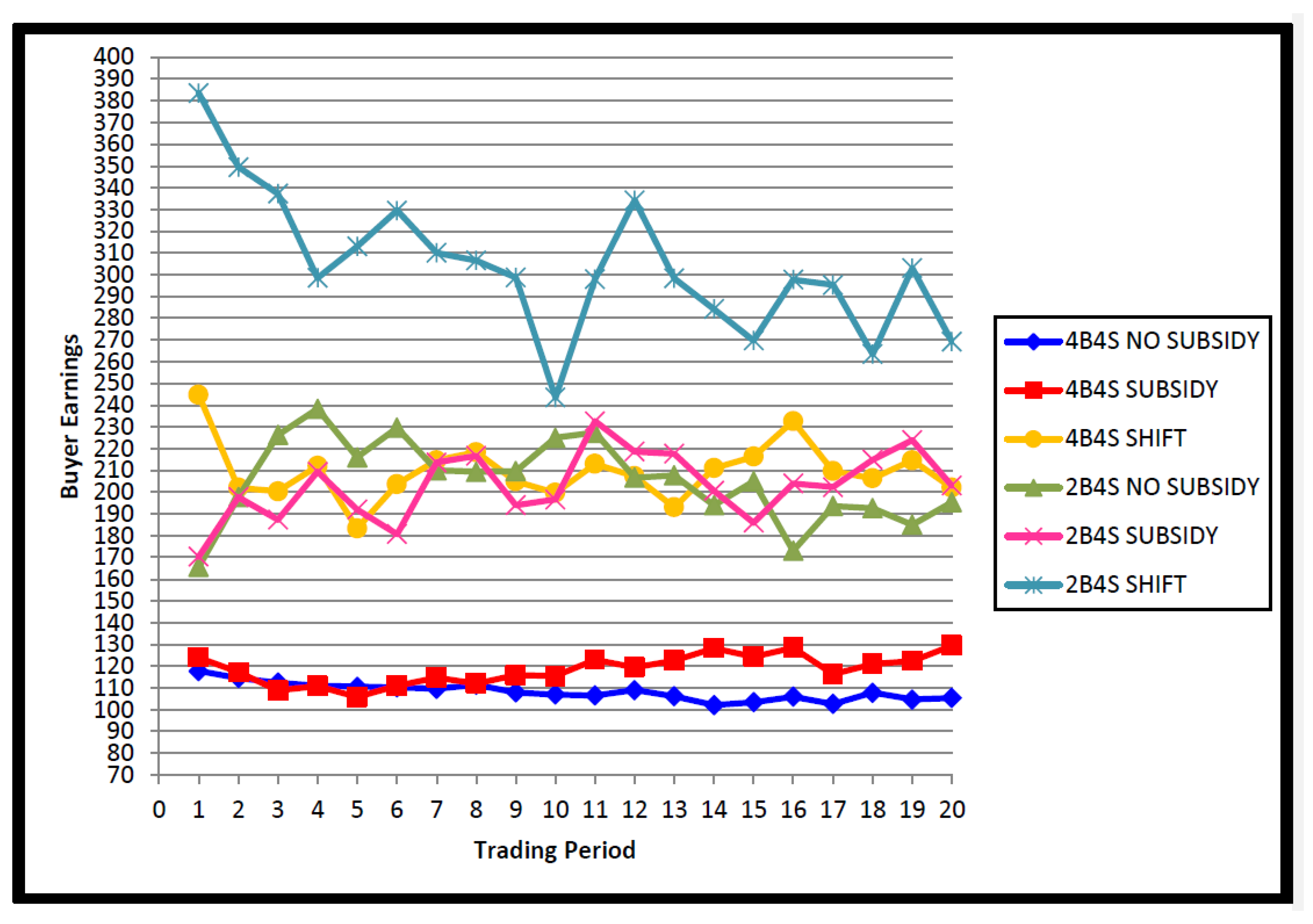

6.4. Buyer Earnings

6.5. Total Earnings

7. Estimates from the Convergence Model

7.1. Prices

7.2. Trades

7.3. Total Earnings

7.4. Seller Earnings

7.5. Buyer Earnings

7.6. Relative Earnings

8. Discussion

9. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Example PowerPoint Instructions and Screenshots for 20 Token per Unit Subsidy to Buyer and Seller Treatment

| 1 | The study of tax incidence assesses distribution of taxes. |

| 2 | A decoupled payment as one that is not dependent upon production or price in the year in which it is made. |

| 3 | As we previously mentioned, this is evident in biofuels markets, where both ethanol producers and corn growers received subsidy. |

| 4 | Induced-value theory indicates that in an experimental session, which provides the proper reward to participants, and meets the conditions of monotonicity, dominance, and salience, the innate characteristics of subjects becomes irrelevant (Friedman et al. 1994). As long as the potential reward is high relative to the opportunity cost of the participant, students should make reasonable subjects for our experiment. A review of the literature comparing various experiments testing differences across subject pools reported by Fréchette (2015) concludes that results across different subject pools are generally consistent, lending further support to the use of students as subjects. Nagler et al. (2013) conduct market experiments similar to those we utilize with students and agricultural professionals as subject pools. They find the same treatment effect across students versus agricultural professionals. Moreover, they do not find statistically significant differences in price levels and relative earnings levels between students and agricultural professionals. Bastian (2019) further examines these data and finds no statistical difference in various bargaining behavior indicators between students and agricultural professionals. Given induced-value theory and the reported subject pool findings in this literature, we use students as subjects in our study. |

| 5 | Given we employ a random stop, individual experimental sessions typically have between 20 and 24 trading periods in an individual experimental session. To maintain a balanced sample, we truncate the data at 20 periods. Moreover, the Parks method requires that the number of cross-sections be less than the time-series length. As we have 3 to 9 replications per treatment for this research, the number of individual cross-sections would be 28 when using all the individual sessions. By averaging across the sessions in each treatment we avoid this issue and reduce the potential contemporaneous correlation across sessions within treatments. Research has tested different estimation procedures for the convergence model in other laboratory market research and finds that while standard errors can be wider, magnitude and significance of parameter estimates is generally not altered given the panel corrections taken when using the Parks method compared to estimation with all individual data (Cook 2010). |

| 6 | Since the observations are over multiple trading periods and the error terms may be serially correlated, contemporaneously correlated or heteroscedastic, we use the Parks method (Parks 1967; SAS 2008) to estimate the model as it accounts for the unique statistical properties resulting from panel data sets. This model allows for simultaneous testing of differences in asymptote or starting levels across treatments. Analyses are conducted in SAS using the PANEL procedure (SAS 2008). |

| 7 | An example of subsidization via a shifted demand curve exists in biofuel markets given blend mandates requiring gasoline to have a certain percentage of ethanol in it (De Gorter and Just 2010). |

References

- Alm, James. 2010. Testing Behavioral Public Economics Theories in the Laboratory. National Tax Journal 63: 635–58. [Google Scholar] [CrossRef] [Green Version]

- Andreoni, J., and John Miller. 2002. Giving According to GARP: An Experimental Test of the Consistency of Preferences for Altruism. Econometrica 70: 737–53. [Google Scholar] [CrossRef] [Green Version]

- Ashenfelter, Orley C., Janet Currie, Henry S. Farber, and Matthew Spiegel. 1992. An Experimental Comparison of Dispute Rates in Alternative Arbitration Systems. Econometrica 60: 1407–33. [Google Scholar] [CrossRef]

- Bastian, Christopher T. 2019. Evolution toward Private Negotiation as a Dominant Institution in Agribusiness Supply Chains: Implications, Challenges, and Opportunities. Journal of Agricultural and Resource Economics 44: 457–73. [Google Scholar]

- Bastian, Christopher T., Dale J. Menkhaus, Amy M. Nagler, and Nicole S. Ballenger. 2008. Ex Ante Evaluation of Alternative Agricultural Policies in Laboratory Posted Bid Markets. American Journal of Agricultural Economics 90: 1208–15. [Google Scholar] [CrossRef]

- Brown, James Dean. 1997. Questions and Answers about Language Testing Statistics: Skewness and Kurtosis. Shiken: JALT Testing & Evaluation SIG Newsletter 1: 20–23. [Google Scholar]

- Charness, Gary, Uri Gneezy, and Michael A. Kuhn. 2012. Experimental Methods: Between-subject and Within-subject Design. Journal of Economic Behavior & Organization 81: 1–8. [Google Scholar]

- Cook, Benjamin R. 2010. Essays on Carbon Policy and Enhanced Oil Recovery. Ph.D. dissertation, Economics Department, University of Wyoming, Laramie, WY, USA. [Google Scholar]

- De Gorter, Harry, and David R. Just. 2010. The Social Costs and Benefits of Biofuels: The Intersection of Environmental, Energy and Agricultural Policy. Applied Economic Perspectives and Policy 31: 4–32. [Google Scholar] [CrossRef] [Green Version]

- Demmel, Laura. 2008. State Policies in the North Central Region Promotion Ethanol. Available online: https://digitalcommons.unl.edu/cgi/viewcontent.cgi?article=1001&context=ageconundergrad (accessed on 1 October 2021).

- Fischer, Charles C. 1997. What Can Economics Learn from Marketing’s Market Structure Analysis? Business Quest. Journal of Applied Topics in Business and Economics. Available online: http://www.westga.edu/~bquest/1997 (accessed on 1 October 2021).

- Fréchette, Guillaume R. 2015. Chapter 7: Experimental Economics across Subject Populations. In The Handbook of Experimental Economics, 2nd ed. Edited by Alvin E. Roth and John H. Kagel. Princeton: Princeton University Press. [Google Scholar]

- Friedman, Sunder, Daniel Friedman, and Shyam Sunder. 1994. Experimental Methods: A Primer for Economists. New York: Cambridge University Press. [Google Scholar]

- Gamage, David, Andrew T. Hayashi, and Brent K. Nakamura. 2010. Experimental Evidence of Tax Framing Effects on the Work/Leisure Decision. SSRN Working Paper. Rochester: Social Science Research Network. [Google Scholar]

- Goodhue, Rachael E., and Carlo Russo. 2012. Modeling Processor Market Power and the Incidence of Agricultural Policy: A Nonparametric Approach. In The Intended and Unintended Effects of US Agricultural and Biotechnology Policies. Edited by Joshua S. Graff Zivin and Jeffrey M. Perloff. Chicago: University of Chicago Press. [Google Scholar]

- Goodwin, Barry K., Ashok K. Mishra, and François N. Ortalo-Magné. 2003a. Explaining Regional Difference in the Capitalization of Policy Benefits into Agricultural Land Values. In Government Policy and Farmland Markets—The Maintenance of Farmer Wealth. Edited by Charles Moss and Andrew Schmitz. Ames: Iowa State Press, pp. 3–14. [Google Scholar]

- Goodwin, Barry K., Ashok K. Mishra, and François N. Ortalo-Magné. 2003b. What’s Wrong with Our Models of Agricultural Land Values? American Journal of Agricultural Economics 85: 744–52. [Google Scholar] [CrossRef]

- Goodwin, Barry K., Ashok K. Mishra, and François Ortalo-Magné. 2012. The Buck Stops Where? The Distribution of Agricultural Subsidies. In The Intended and Unintended Effects of S.US Agricultural and Biotechnology Policies. Edited by Joshua S. Graff Zivin and Jeffrey M. Perloff. Chicago: University of Chicago Press, pp. 15–50. [Google Scholar]

- Hurt, C., W. Tyner, and O. Doering. 2006. Economics of Ethanol. Extension Publication No. 339. West Lafayette: Purdue University. [Google Scholar]

- Isola, Wakeel A. 2012. An Analysis of Electricity Market Structure and Its Implications for Energy Sector Reforms and Management in Nigeria. Global Advanced Research Journal of Management and Business Studies 5: 141–49. [Google Scholar]

- Kirwan, Barrett E. 2009. The Incidence of US Agricultural Subsidies on Farmland Rental Rates. Journal of Political Economy 117: 138–64. [Google Scholar] [CrossRef] [Green Version]

- Komives, Kristin, Jon Halpern, Vivien Foster, Quentin Wodon, and Roohi Abdullah. 2007. Utility Subsidies as Social Transfers: An Empirical Evaluation of Targeting Performance. Development Policy Review 25: 659–79. [Google Scholar] [CrossRef]

- Kumar, Radika, Ronald Ravinesh Kumar, Peter Josef Stauvermann, and Pallavi Arora. 2020. Effect of Fisheries Subsidies Negotiations on Fish Production and Interest Rate. Journal of Risk and Financial Management 13: 297. [Google Scholar] [CrossRef]

- Menkhaus, Dale J., Owen R. Phillips, and Chris T. Bastian. 2003. Impacts of Alternative Trading Institutions and Methods of Delivery on Laboratory Market Outcomes. American Journal of Agricultural Economics 85: 1323–29. [Google Scholar] [CrossRef]

- Menkhaus, Dale J., Owen R. Phillips, Christopher T. Bastian, and Lance B. Gittings. 2007. The Matching Problem (and Inventories) in Private Negotiation. American Journal of Agricultural Economics 89: 1073–84. [Google Scholar] [CrossRef]

- Nagler, Amy M., Dale J. Menkhaus, Christopher T. Bastian, Mariah D. Ehmke, and Kalyn T. Coatney. 2013. Subsidy Incidence in Factor Markets: An Experiment al Approach. Journal of Agricultural and Applied Economics 45: 17–33. [Google Scholar] [CrossRef] [Green Version]

- Nechyba, Thomas. 2011. Microeconomics: An Intuitive Approach with Calculus, 1st ed. Mason: Cengage Learning. [Google Scholar]

- Neter, John, William Wasserman, and Michael H. Kutner. 1985. Applied Linear Statistical Models: Regression, Analysis of Variance, and Experimental Design, 2nd ed. Homewood: Richard D. Irwin, Inc. [Google Scholar]

- Parks, Richard W. 1967. Efficient Estimation of a System of Regression Equations when Disturbances are Both Serially and Contemporaneously Correlated. Journal of the American Statistical Association 62: 500–9. [Google Scholar] [CrossRef]

- Patton, Myles, Philip Kostov, Seamus McErlean, and Joan Moss. 2008. Assessing the Influence of Direct Payments on the Rental Value of Agricultural Land. Food Policy 33: 397–405. [Google Scholar] [CrossRef]

- Qiu, Feng, Jean-Philippe Gervais, and Barry K. Goodwin. 2010. An Empirical Investigation of the Agricultural Subsidy Incidence on Farmland Rental Rates. Paper Presented at Selected Paper Prepared for Presentation at the Agricultural & Applied Economics Association 2010 AAEA, CAES, & WAEA Joint Annual Meeting, Denver, CO, USA, July 25–27. [Google Scholar]

- Rahman, Mohammad Maksudur, Christopher T. Bastian, Chian Jones Ritten, and Owen R. Phillips. 2019. Subsidy Incidence in Privately Negotiated Spot Markets: Experimental Evidence. Journal of Agricultural and Applied Economics 51: 219–34. [Google Scholar] [CrossRef] [Green Version]

- Rasul, Imran, Andrew Leicester, and Peter Levell. 2012. Tax and Benefit Policy: Insights from Behavioral Economics. London: The Institute for Fiscal Studies. [Google Scholar]

- Ruffle, Bradley J. 2005. Tax and Subsidy Incidence Equivalence Theories: Experimental Evidence from Competitive Markets. Journal of Public Economics 89: 1519–42. [Google Scholar] [CrossRef]

- Saitone, Tina L., Richard J. Sexton, and Steven E. Sexton. 2008. Market Power in the Corn Sector: How Does It Affect the Impacts of the Ethanol Subsidy? Journal of Agricultural and Resource Economics 33: 169–94. [Google Scholar]

- SAS. 2008. SAS/ETS 9.2 User’s Guide. Cary: SAS Institute Inc, Available online: http://support.sas.com/documentation/cdl/en/etsug/60372/PDF/default/etsug.pdf (accessed on 2 July 2013).

- Schechinger, Anne. 2021. Under Trump, Farm Subsidies Soared and the Rich Got Richer Biden and Congress Must Reform a Wasteful and Unfair System. Available online: https://www.ewg.org/interactive-maps/2021-farm-subsidies-ballooned-under-trump (accessed on 1 October 2021).

- US Grains Council. 2021. Ethanol Production and Exports. Available online: https://grains.org/buying-selling/ethanol-2/ethanol/ (accessed on 1 October 2021).

- Zelinsky, Edward A. 2005. Do Tax Expenditures Create Framing Effects? Volunteer Firefighters, Property Tax Exemptions, and the Paradox of Tax Expenditure Analysis. Virginia Tax Review 24: 797–834. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Treatments | Number of Buyers | Number of Sellers | Number of Replications | ||

|---|---|---|---|---|---|

| 1 | 4 | Buyers with no subsidy | 4 | Sellers with no subsidy | 9 Replications |

| 2 | 4 | Buyers with subsidy | 4 | Sellers with subsidy | 5 Replications |

| 3 | 4 | Buyers shift RV | 4 | Sellers shift cost | 3 Replications |

| 4 | 2 | Buyers with no subsidy | 4 | Sellers with no subsidy | 3 Replications |

| 5 | 2 | Buyers with subsidy | 4 | Sellers with subsidy | 3 Replications |

| 6 | 2 | Buyers shift RV | 4 | Sellers shift cost | 5 Replications |

| Treatments | Price | Trades | Total | Buyer | Seller | Relative |

|---|---|---|---|---|---|---|

| (Tokens) | Levels | Earnings | Earnings | Earnings | Earnings | |

| 4 Buyers and | ||||||

| 4 Sellers | ||||||

| No Subsidy | 74.81 | 13.93 | 725.16 | 104.72 | 75.69 | −29.34i |

| (−29.29) a–c,f | ||||||

| Subsidy | 73.38 a | 19.57 *,a | 731.97 a | 118.76 *,a | 63.53 *,a,c | −55.41i * |

| 77.28 *,b,c | 20.93 *,b | 1555.55 *,b | 203.33 *,b,c | 183.54 *,b | (−64.44) b–e | |

| Shift R.V./Cost | −20.30 i | |||||

| (−32.26) c | ||||||

| 2 Buyers and | ||||||

| 4 Sellers | 71.53 *,a | 11.71 *,c | 632.01 *,c | 211.54 *,c,d | 51.28 *,a | −159.42 i,* |

| No subsidy | ||||||

| [105.77] | (−134.07) d,e | |||||

| Subsidy | 79.48 *,c | 15.85 *,d | 718.37 a | 209.94 *,d,b | 73.80 c | −136.76i * |

| [104.97] | (−133.27) e,f | |||||

| Shift R.V./Cost | 83.78 *,d | 18.45 *,e | 1338.44 *,d | 303.42 *,e | 182.94 *,b | −120.49 i,* |

| [151.71] | (−117.20) f,b |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Baffoe-Bonnie, A.; Bastian, C.T.; Menkhaus, D.J.; Phillips, O.R. Stacking Subsidies in Factor Markets: Evidence from Market Experiments. J. Risk Financial Manag. 2021, 14, 608. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14120608

Baffoe-Bonnie A, Bastian CT, Menkhaus DJ, Phillips OR. Stacking Subsidies in Factor Markets: Evidence from Market Experiments. Journal of Risk and Financial Management. 2021; 14(12):608. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14120608

Chicago/Turabian StyleBaffoe-Bonnie, Anthony, Christopher T. Bastian, Dale J. Menkhaus, and Owen R. Phillips. 2021. "Stacking Subsidies in Factor Markets: Evidence from Market Experiments" Journal of Risk and Financial Management 14, no. 12: 608. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14120608