Designing a Roadmap for Human Resource Management in the Banking 4.0

1

Institute of Finance, Faculty of Economics and Sociology, University of Lodz, POW 3/5, 90-255 Lodz, Poland

2

Department of Labour and Social Policy, Faculty of Economics and Sociology, University of Lodz, Rewolucji 1905 Street 41, 90-214 Lodz, Poland

*

Authors to whom correspondence should be addressed.

J. Risk Financial Manag. 2021, 14(12), 615; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14120615

Submission received: 22 October 2021

/

Revised: 10 December 2021

/

Accepted: 15 December 2021

/

Published: 18 December 2021

(This article belongs to the Special Issue Banking during the COVID-19 Pandemia)

Abstract

:The banking sector has been going through a rapid transformation due to digitalization, regulatory requirements, customer expectations, and demographic trends. The purpose of this paper is to provide an advanced overview of the practical applications of human resource management (HRM) in Banking 4.0. This study used quantitative and qualitative methods to present the results of good practice form inventory and a Delphi study. The results of a European study show that human resource management practices such as reskilling, upskilling, and redeployment are a solution to mitigate challenges in the Banking 4.0 era. The HRM roadmap for banks will be a major guide to ensure effective workforce management.

1. Introduction

Nowadays, more and more attention is paid to intangible resources, which are associated with the intellectual capital of organizations and the financial sector is no exception. Individuals’ information and knowledge resources, as well as their skills and competencies, build individual intellectual capital.

The most popular concept of an intellectual capital structure based on the value platform model consists of three components: human capital, relational capital (clients), and structural (organizational) capital (Wall 2007). According to the model of Saint-Onge (1996), human capital is the basis for raising an enterprise’s organizational capital and both cooperate to generate customer capital. Sveiby (1997), the creator of the intangible assets monitor, emphasizes that people are the most important asset in a company, determining its competitive position.

The literature indicates that in financial institutions, banks in particular, the most important intangible assets are the employees (human capital), customers, brands, and quality (Marcinkowska 2013). Human capital is understood as the capital that is inseparably integrated with a person (employee)—his knowledge, experience, presence, and the way he can act in a bank. Due to the objectives of the study, considerations in this area will be narrowed down to the role of human capital.

In the financial sector, research on the importance of this component of intellectual capital has been conducted since the 1990s. According to Canals (1993), the sources of a bank’s competitive advantage are the people who work in them. As a result of research conducted at the same time by Bharadway et al. (1993), the sources of competitive advantage in the service sector are: company culture, economies of scale, brand value, modern information technology, and the ability to implement it. In turn, Devlin and Ennew (1997) drew attention to the importance of reputation, image, and quality of service in building an advantage in the banking sector. The importance of the human factor in a bank’s competitive strategy was emphasized by Chen (1999), while Hitt et al. (2001) showed that human capital exhibits a curvilinear effect (u-shaped) and the leveraging of human capital has a positive effect on performance.

The twenty-first century brought new challenges that the banking sector had to face. Modern business models must take a much greater account of digitalization, new regulations, and changing customer expectations. Effectively building a competitive advantage in this virtual reality would not be possible without the human factor. There is a growing body of literature on human capital theory and strategic management theory that point to the relationship between human capital efficiency and bank performance.

Meles et al. (2016) found that human capital has a greater beneficial effect on bank profitability than the other components of intellectual capital (structural capital, and physical capital). Similar results were presented by Al-Musali and Ku Ismail (2016). Adesina (2021) investigated the influence of intellectual capital (and its components) on bank allocative, cost, and technical efficiencies and found that only human capital is positively related to all the three efficiency measures across the panel. Moreover, higher levels of human capital efficiency are positively associated with bank performance. Studies on the role of human capital in banking have found that to achieve a competitive edge, banks should invest in their human capital (Mohapara et al. 2019). When banks diversify away from interest-earning assets (loans) to non-interest income activities and non-earning assets, they need to have sophisticated human resources and skills to make efficient business decisions in these areas (Ahamed 2017; Nguyen 2018).

In recent decades, the increasing use of internet technologies in production and services called the fourth industrial revolution (Industry 4.0) has put high pressure on banks to create and maintain the interactions with their customers over time, adapting the nature of relationships from the physical environment associated with bank branches to the virtual environment linked to the use of digital platforms and technologies. The use of Industry 4.0 technologies for digitizing assets, creating a digital identity, providing special offers to customers, offering customization, etc., is one of Banking 4.0’s central strategies (Mehdiabadi et al. 2020).

Digital transformation in the banking sector covers the alternative distribution channels through which banks reach their customers—such as ATMs, Internet branches, and mobile branches. Banks are able to reach their customers on alternative platforms thanks to applications developed by these branches. Several routines and manual tasks that were previously performed by humans are now being replaced by automated machines with advanced technology (Kaur et al. 2020).

Regulatory compliance such as the Revised Payment Services Directive (PSD2; EU 2015) has accelerated the competition, and bringing payment systems out of the monopoly of the banks implies that the whole sector will be transformed (Premchand and Choudhry 2018). Fintech start-ups and tech giants as innovating and experimenting institutions with new products, delivery channels, and analytics are redefining how banking fits in the daily life of consumers. The COVID-19 crisis has fast-tracked innovation and the digitalization of processes in the financial sector (Demirgüç-Kunt et al. 2021). To survive, banks must develop new capabilities, new jobs, and new skills (King 2018). This future will require institutions to be agile and open, ready to explore different options in an uncertain world. Having coped with the numerous challenges of globalization, internationalization, tertiarization, informatization, the growth of competition and innovation, as well as changing consumption patterns and customs, organizations also face the impacts of the digitalization of society. Taking this into consideration, the purpose of the article is to recommend human resource practices that cover reskilling, upskilling, and redeployment as a solution to mitigate workforce challenges in the era of Banking 4.0. Reskilling can be defined as the procedure by which people learn a new skill to do a different job or give guidance to other people to do a different job; meanwhile, ‘upskilling’ refers to learning a new skill or training employees with new skills (Wahab et al. 2021). Redeployment, accompanied by a shortage of talent, is a consequence of some conventional jobs becoming redundant (Sima et al. 2020).

This paper is structured as follows. The first part of the paper focuses on the theoretical background of Banking 4.0 and the characteristics of the workforce in the banking sector. The second part describes the research methodology. The third part presents the results. The fourth part proposes a roadmap for HRM that can meet the challenges faced by the banking sector, while the fifth part focuses on discussion and the last part presents overall conclusions.

2. Banking 4.0 in the Context of Human Resource Management

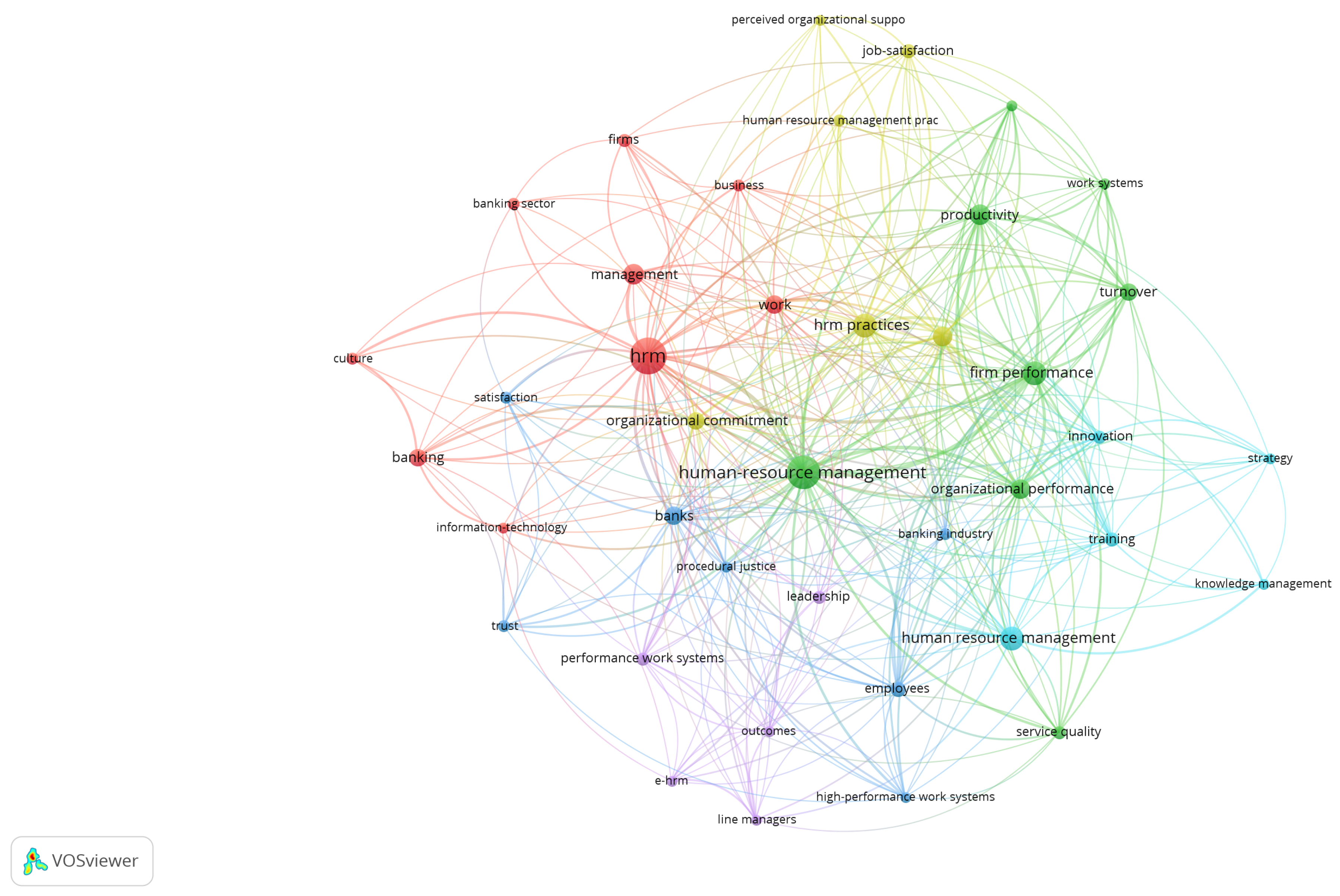

Human resource management (HRM) is a subject of interest on many levels, but the motivations for the interest and how it is manifested differ. This is a bibliometric study to shed light on the gap in the literature, which can contribute to the scientific demand and originality of the proposed study on HRM in Banking 4.0. To cover the relevant and extensive collection of scientific publications bibliometric data from two scientific research platforms were used: Scopus and Web of Science. VOSviewer (version 1.6.17), a freely available computer program, was used to construct and view bibliometric maps that consider keyword frequency and co-occurrence (Van Eck and Waltman 2010).

In order to obtain high-quality data mining, the search reliably reflects the research topic, the study objectives, and the limits of research fields. The search used the Topic (TS) “HRM in banking”, “Human resource management in banking”, HRM in the bank” and “Human resource management in the bank” and was limited to articles written in English between 1997–2021, included articles, proceedings papers, book chapters, and early access. In total, 139 publications were identified in the WoS database and 176 in Scopus. According to WoS, there were 96 (90.04%) papers, and according to Scopus, there were 101 (57.38%) papers. Most of the papers from both platforms pertain to Management, Business, and Economic.

Citations for the articles were moved to a marked list. This complete record list was then exported as a Windows Tab-delimited file for processing in VOSviewer for further analysis. Keywords provided by authors of the paper, which occurred more than 5 times in the WoS core database were enrolled in the final analysis. Of the 805 keywords, 54 met the threshold. Technical terms were removed, reducing the list to 50. For each of the 50 keywords, the total strength of the co-occurrence links with other keywords was calculated (Figure 1).

The 50 keywords are divided into 6 clusters. If keywords are grouped into the same cluster, they are more likely to reflect identical topics (Waltman et al. 2010). The cluster analysis indicates that the research fields of human resource management in banking are varied. Only one of the clusters covered keywords connected with banking and technology but the context of the article concentrated on high involvement work practice (HIWP) as a crucial way of improving technology adaptation among the employees in the organization (Rubel et al. 2020).

The most cited publication examines the relationships between HRM and organizational performance in the bank (Bartel 2004) adding work climate (Gelade and Ivery 2003) or linking high-performance work systems (HPWS) and performance outcomes at the individual and organizational levels of analyses (Aryee et al. 2012). Practice and training development is recognized as the most critical part of banking financial performance (Huynh et al. 2020). There are publications that consider the effectiveness of separate HRM practices (mostly training) that are limited to separate countries or even banks and confirm that training and development in organizations positively affects the employee and improves his/her performance and development (Cherif 2020; Alsafadi and Altahat 2021; Jeni et al. 2021). The bibliometric analysis shows that there is a gap in HRM in the context of Banking 4.0.

We are believed to be at the beginning of the Fourth Industrial Revolution. The digitalization of the banking sector is at maximum capacity, as this process also includes other parts of Industry 4.0, such as blockchain networks, artificial intelligence, IoT, biometrics, the cooperation of banks with FinTech companies, the preparation of the platform, and other services for Generation Z and others (Mekinjić 2019). The most significant drivers of change for the banking sector are connected with technology (World Economic Forum 2020), and according to an Accenture (2021a) report, the following changes have taken place in the banking sector:

- −

- removing barriers to customer service,

- −

- the use of Big Data, advanced analytics, and artificial intelligence,

- −

- improving integrated omnichannel support by implementing open API technologies,

- −

- building collaboration between banks and FinTechs,

- −

- mobile payment expansion,

- −

- adapting to regulatory changes,

- −

- exploring modern technologies (Internet of Things, voice forwarding, blockchain),

- −

- the emergence of new challenger banks

- −

- investing in innovations.

During the COVID-19 pandemic, electronic banking has proved its value to society. The pandemic has disrupted every aspect of how societies function, forcing governments, businesses, educators, and regular citizens to adopt online activities (Demirgüç-Kunt et al. 2021). The banking sector was expected to play a key role in absorbing the shock, by supplying much-needed funding (Acharya et al. 2021). The banking sector, which already boasted the highest proportion of digital users in Europe, has recorded an increase of 23% in first-time digital users since the onset of COVID-19, while globally, remote digital payments shot up by about 50% when physical distancing measures were introduced (Auer et al. 2020).

The literature emphasizes that the digitalization of banking products and services will have to reduce their operating costs, resulting in layoffs and fewer employees in the banking sector. The overview shows that banks have continued to scale back their physical presence across Europe as the importance of having a widespread network of bank branch falls. The structural financial indicators show a further decline in the number of bank branches in the EU, averaging 8.62% across the member states. Contractions were observed in 24 of the 27 countries, ranging from −2.28% to −30.66%. Fewer bank employees is a trend that has been observed in most countries since 2008. The number of employees in the EU has declined from 3,233,000 in 2010 to 2,622,723 in 2020 (ECB 2021). Digitalization is also changing the nature of the work in the banking and financial industry (both from qualitative and quantitative perspectives), similar to the current trends in manufacturing.

Digitalization results not only in leveraging technology and innovative tools to improve the efficiency and efficacy of products, but it has also transformed consumer habits. It has shifted customer expectations, resulting in a new kind of consumer who is constantly connected, app-native, and well-aware of the potential and opportunities offered by technology.

The digital society appreciates real-time experience, and usefulness, and it turns to the convenience of online banking and cashless payments (Mbama and Ezepue 2018). According to a KPMG (2020) report, banking customers expect banks to be integrated into their lifestyle, offered automated, intuitive, and user-friendly processes of interacting as well as cyber safety and personalized customer’s finance management. Implementing new technologies should always correspond with the need to have a workforce that will take time to meet the requirements.

The main direct impacts of EU regulation are increased capital requirements and new positions in compliance, data protection, and IT departments. The European Commission has adopted the AML/CFT RULES as the robust legislation to fight money laundering and financing of terrorists. It has resulted in the increased importance of Know-Your-Customer (KYC), and the workforce responsible for identifying KYC (EU 2018). EU (2019) supports the principle of equal pay for male and female workers for equal work or work of equal value. Meanwhile, the PSD2 regulation (EU 2015) has increased cost pressures, leading to agile working and desk sharing. Regarding the indirect impact of EU regulation, there has been a downsizing, mainly in commercial functions. At the same time, there has been an increase in workload due to reporting requirements and a need for specific IT and consulting support.

The accelerating pace of technological, regulation, and socioeconomic disruption is transforming industries and business models, changing the skills that employers need and shortening the shelf-life of employees’ existing skill sets in the process (CEDEFOP 2015). The expected level of skills stability in the banking sector is 57% (Industries Overall—67%).

As companies strive to become more agile and customer-focused, organizations are shifting their structures from traditional, functional models toward interconnected, flexible teams. The most important human capital future trends are workforce management, digital HR, people analytics, changing skills of the HR organization, design thinking, learning, engagement, culture, leadership, and organizational design (Deloitte 2019).

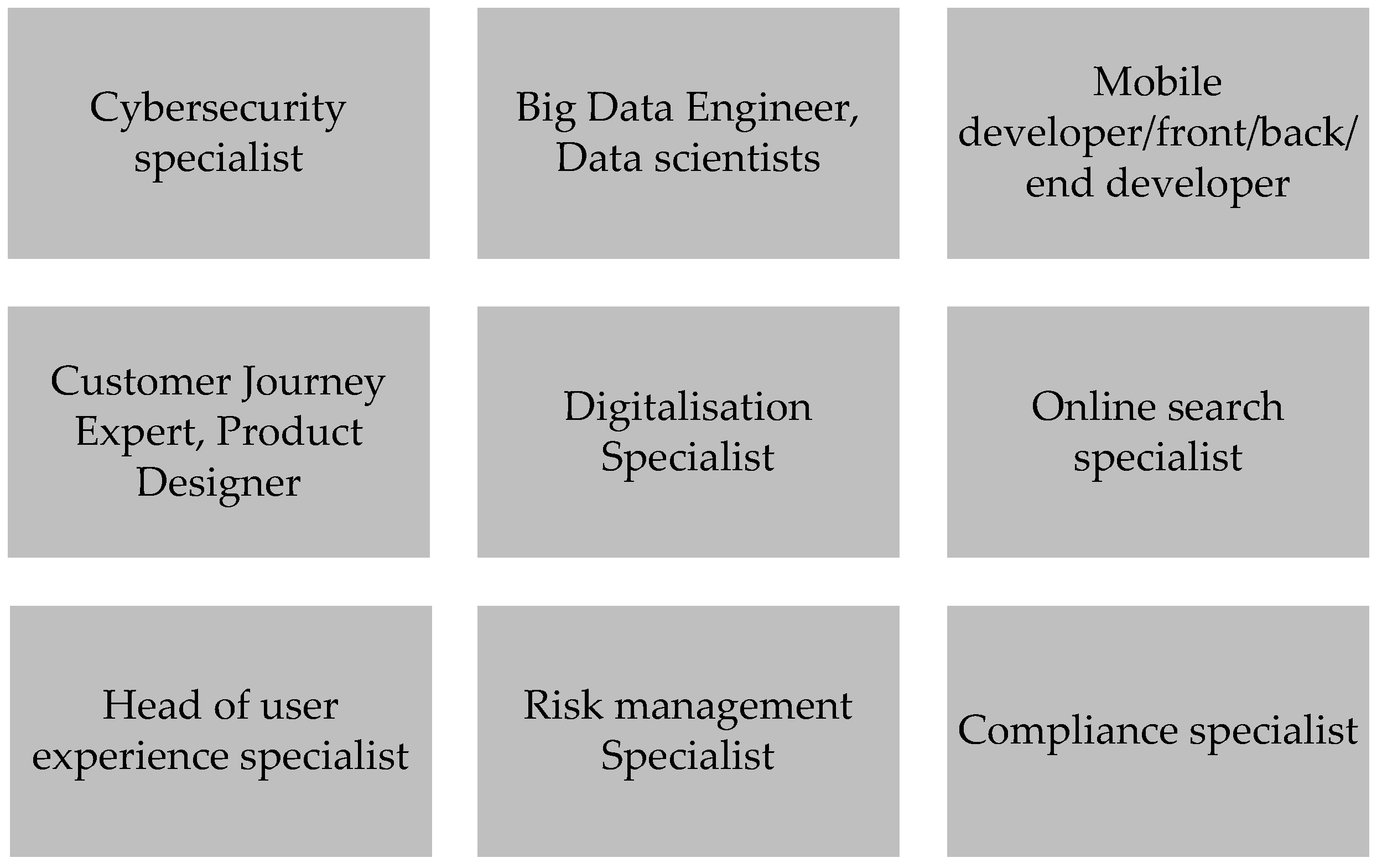

Concerning the overall scale of demand for various skills, in 2020, all jobs across the banking sector were expected to require complex problem-solving as one of their core skills, as well as an increase in technical skills and cognitive abilities. An increasing number of financial institutions will be looking for workers for new posts that arise on the basis of the trends observable in the banking sector (Figure 2).

A significant proportion of these posts are related to the increasing digitization of society, and the work carried out on data possessing positions. It is becoming increasingly popular to bring people together to work in one team that is involved separately in sales, design, marketing and financing. Interdisciplinarity will create products and solutions faster, but it will also require common competencies of the team members. This situation results in a large difference between the present level of competence in the banking sector and the desired level. Banks recognize this gap. The biggest gaps concern conceptual thinking, analytical abilities, and searching for information (Accenture 2021b). Thus, the solution might be to rethink the employment strategy. Financial sector CEOs recognize that while technology can create greater connectivity and transparency, concerns over how data are used and the sector’s vulnerability to cyber breaches have led to increasing levels of mistrust. Financial sector CEOs are rethinking their people strategies to meet these evolving skills demands. This includes moving talent around and seeking the best people, no matter who or where they are (we look at diversity and inclusion further on).

This is the scope of talent management, understood as a systematic process carried out by the company in finding, selecting, improving, and maintaining the best talents of its employees for meeting the needs of the company today and in the future (Wolor et al. 2019). The CEOs we spoke to highlighted the importance of adaptability and regularly updating skills to keep pace with market events or changes in the business model. They also recognized that their changing skills demands and the underlying issues of education, labor inclusion, and employment in an ever more automated world are areas that their organizations cannot tackle alone. This underlines the importance of collaborating more closely with governments and other stakeholders to develop solutions. Examples include working with universities to update curricula and develop more work-related capabilities (PwC 2017).

Finally, with regard to rethinking the employment strategy, it might be a good idea to pay greater attention to training. The industry professionals questioned by the Fintech Circle Institute felt that a lack of training within financial services organizations was the biggest factor that prevents some employees from developing their digital and FinTech skills, with 69% making this claim. Meanwhile, 22% said financial services professionals delay developing their digital skills for fear that it is already too late to catch up with existing FinTech experts (Fintech Circle 2017). Regardless of the financial sector’s size and structure, it is affected by problems related to digitization, consolidation, regulatory changes, and customer expectations. The thesis is as follows:

HR practices including reskilling, upskilling, and redeployment are a solution that helps to mitigate challenges in the era of Banking 4.0.

3. Data and Methods

The article presents the results of a three-stage study that used both quantitative and qualitative methods. First, a review of the scientific literature and thematic reports was carried out. Additionally, statistical data were analyzed, including Eurostat data and quantitative branch reports. The result of this preliminary research phase were three partial desk research reports as well as the methodology for the second phase, including a “code of good practice form”, which was applied during the second phase of the research.

The aim of the code of good practice form was to gather examples of the implementation of programs from the HRM area of a financial institution. Aware of two necessary and sufficient conditions that must be met by the method of best practice (Bretschneider et al. 2015), the good practice form was completed by members of financial institutions from the nine EU countries (Greece, Finland, Hungary, Italy, France, Malta, Poland, Romania, and Spain). Additionally, we conducted a web query analysis of thematic source texts for the banking sector.

Based on the collected forms, a catalog of good practices was prepared. They assessed the popularity of human resource management in the financial sector, indicated the scale of the tools used, and assessed their effectiveness from an organizational point of view. The structure of a good practice form lets an organization have general information about the time frame of realizing the good practices, the number of employees covered by the support, the source of financing activities within the framework of the good practice, and how to spread information about the good practice.

The second part of the good practice form describes the good practice, the activities provided within the framework of the good practice, the objective of the activities carried out within the framework of this good practice, the measures used, the results, the involvement of social partners in implementing the good practice, and transferability.

The third part of the research was a Delphi study using the Computer Assisted Web Interviewing (CAWI) method in two rounds of the study. The respondents were chosen using convenience sampling. Experts (n = 11) were invited to contribute to the study by providing feedback on the first and second versions. The sample included a limited number of individuals, but this shortcoming is balanced by the status of the individuals, and their valuable opinions, due to their professional standing, i.e., they represent leading organizations from the banking sector. The sample included trade union representatives of different roles and countries of practice i.e., 3–4 negotiators from national organizations, 2–3 professionals from Eurocadres, 2–3 experts from Uni-Europa. The respondents represented Uni Europa, Eurocadres, Nordic Financial Unions (Denmark), GPA-djp (Germany—national level sectoral collective bargaining), Unicredit group (Austria and Germany—national and company-level collective bargaining), Royal Bank of Scotland (company-level collective bargaining), Sindicato dos Bancarios do Sul e Ilhas (Portugal—international officer), CCOO Commissiones Obreras (Spain) and BNP Paribas European Works Council. The CAWI semi-structured questionnaire was organized in four sections: (1) preliminary considerations (four questions), (2) digitalization and skills disruption (nine questions), (3) final remarks and best practices, (4) organization profile. The last step was applying Qualitative Comparative Analysis (QCA) launched in the late 1980s by Charles Ragin (1987) to the Delphi results.

This multiapproach perspective covered the literature review, the inventory of the good practice forms, and the Delphi study results with QCA analysis on the proposed roadmap of how banks should build a workforce to mitigate challenges in the era of Banking 4.0.

4. Results

4.1. Good Practice form Analysis

The good practices forms were analyzed and thematically grouped. The analyzed result found ten main activities covered by separate initiatives (Table 1):

- Development practices, mentoring and reverse mentoring; training, lifelong learning practices

- Practices focused on employees’ health and wellbeing

- An information campaign targeted at employees, promoting of intergeneration co-operation

- Recruitment, selection, and adaptation of employees and apprentices

- Organization of work, job-sharing, e-work, temporary work

- Inclusion culture

- Agreement/dialog

- Motivational aspects

- Retirement plan based on resource analysis

- Talent management

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Good practice form inventory results.

| Name of the Organization | Country/Headquarters | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Barclays | Great Britain | ||||||||||

| Deutsche Bank | Germany | ||||||||||

| Bank of France | France | ||||||||||

| Nordea Bank | Denmark | ||||||||||

| Axa | France | ||||||||||

| KBC | Belgium | ||||||||||

| ING-DIBA | Denmark/Germany | ||||||||||

| Unicredit | Italy | ||||||||||

| Credit Industriel at Commercial | France | ||||||||||

| Groupama | France | ||||||||||

| Rabobank | Denmark | ||||||||||

| Wij(s) Rabo | Netherland | ||||||||||

| Achmea Holding NV | Belgium/Netherland/Luxemburg | ||||||||||

| Dekabank Deutche Girozentrale | Germany | ||||||||||

| Danske Bank A/S Finland Branch | Denmark | ||||||||||

| Fondo Banche Assicurazioni | Italy | ||||||||||

| CIB Bank | Hungary | ||||||||||

| Bank Generational Relay | Italy | ||||||||||

| National Bank of Greece | Greece | ||||||||||

| Dikete | Greece/Cyprus | ||||||||||

| Santander Group | Spain | ||||||||||

| Towarzystwo Ubezpieczeń Wzajemnych | Poland | ||||||||||

| Credit Agricole Bank Polska SA | Poland |

Source: Kozar et al. (2020).

The inventory and analysis of the good practice form demonstrated that although banks are aware of emerging job categories and functions that they expect to become critical to their industry, they introduced only some partial initiatives. Most of them were associated with lifelong development (including mentoring, reverse mentoring, and training activities) and flexible working methods (including job-sharing, e-work, and temporary work). In line with Park and Kim (2020), rapid technological development makes skills depreciate faster than in the past, while new technologies generate gaps in workers’ skills and call for the acquisition of proper skills and lifelong learning.

4.2. Delphi Results Analysis

The respondents confirmed that the financial sector is affected by digital skills imbalances and that digitalization will have an influence on the qualifications required by financial sector workers. They also indicated that in the last five years, the financial sector introduced digital technologies such as Big Data, Analytics, and Cybersecurity, simulation, the Internet of Things, Augmented Reality, virtual reality, and blockchain. In our opinion, most of the respondents’ workplaces will be under tremendous pressure from digitalization. During the past five years, the technological factor is believed to have been the main driver of change in EU financial sector workplaces. Other drivers, which the participants of the first round listed, included organizational models, the legal framework, the aging of the workforce, product services and environmental changes. Other answers that were listed included “(seeking) new business models” and “cost-cutting, short term focus on shareholders’ value, and globalization”.

More than 50% of the experts claimed that the loss of traditional jobs is one of the most evident effects of technological innovation. Some (28%) believed that, because of digitalization, new tasks were added to existing jobs in the financial sector. Finally, a few respondents (14%) argued in favor of creating new jobs as a result of technological innovation.

Taking into consideration technological progress, there are expected changes in skills demand, as modern workplaces require workers to perform different tasks, thus improving their versatility (Kuchciak and Wiktorowicz 2020). The most requested digital skills in the financial sector are data analytics, software development, and maintenance, and digital marketing, and social media. Fewer than half of the respondents indicated digital ICT, basic digital competencies, and cybersecurity, as well as soft and relational skills (Kuchciak et al. 2020).

In the question about digitalization versus workers’ skills in the age context, the respondents emphasize that completely new technical skills are required to deal with new technologies. In their opinion, tackling the lack of digital skills is just one part of the solution, which needs to be complemented with the development of other technical and behavioral skills. According to the respondent’s opinion, over the past five years the introduction of new technologies has affected employment rates among older workers (i.e., 55–64) in the finance sector. On the other hand, for younger workers (i.e., 18–30) the main risk associated with their increasing inclusion in companies (in terms of the ratio over the other age groups) is the loss of soft skills at the company and sector level.

A significant proportion of these posts are related to the increasing role of the digitization of society, and the work carried out in data possessing positions. It is becoming increasingly common to bring people together to work in one team that is involved separately in sales, design, marketing, and financing (Munjuri and Maina 2013; Mgiba 2019). Interdisciplinarity will create products and solutions faster, but it will also require common competencies of the team members. One respondent also claimed that the financial sector is responding to workers’ lack of necessary technical and/or soft skills to deal with the changes in their tasks and responsibilities by using training programs or selecting new professional figures, inter-mentoring, relocation, and offshoring. The respondents argued that the lack of soft skills in a particular group of employees (considering age, sex, position, etc.) is related to the way the finance companies are introducing new workers.

Most of the panelists confirmed the significance of the benefits of age management and intergenerational solidarity within organizations as an essential part of HRM. They mentioned the culture of sharing experience, including the transfer of skills (often soft skills), retaining older workers in the workforce, and mentoring programs, where older workers share their knowledge of services, etc., while younger workers do the same regarding e-skills. At the same time, the respondents confirmed existing barriers to adopting measures and policy instruments that deal with HRM.

In the second round of the Delphi survey, some of the aspects investigated in the first stage of the analysis were examined in more detail. While in Round 1 the experts were asked to identify the most important digital skills that workers should have, round 2 was concerned with assessing their relevance. Relevant skills included those related to ‘data analytics’, followed by ‘digital marketing and social media management. The panel, which consisted of privileged observers, stated that back-office functions and accountancy tasks are at the greater risk of becoming automated.

Regarding the drivers of change—technology, organizational models, and products and services—and the importance of developing training schemes, experts were asked to evaluate the effectiveness of some training approaches based on adaptation in the financial sector. On this aspect, group learning was regarded as a valuable strategy, while different views were recorded regarding training provided under the supervision of a mentor or a senior worker. This heterogeneity might be caused by doubts about the effectiveness of a top-down approach for skills transfer. Preference was given to strategies such as “e-learning, with digital tools used to transfer knowledge remotely. It is possible to use the platform in real-time, interacting with the instructor and other participants at a convenient time” and to “methods based on temporary changes in workers’ positions, which enable one to develop more qualifications, and raise motivation by lowering monotony”.

For the next step, authors used QCA, combining qualitative and quantitative methods, which solves the problem of comparative analysis when the number of cases is small or medium size. The steps of QCA and results are shown below (Figure 3).

The aim of necessity analysis is to identify those conditions that are necessary to produce the expected result, while the sufficiency analysis determines those conditions that are sufficient to produce the expected result presented on Table 2, Table 3, Table 4, Table 5, Table 6, Table 7 and Table 8.

The QCA describe factors affecting positive and negative perception of practices based on age management and intergenerational solidarity. The necessity analysis clearly confirms that the necessary conditions are TECH, MULT and SOFT, while sufficiency analysis determines DIG and lacking job substitution as those conditions that are sufficient to produce the expected result. These results support the thesis that HR practices that include reskilling, upskilling, and redeployment are a solution that helps to mitigate challenges in the era of Banking 4.0.

5. Proposed Roadmap for Human Resource Management in Banking 4.0

A bank’s value competitive position, and market power are determined primarily by the knowledge and skills of its employees and managerial staff, and its ability to motivate them to use their competencies to develop that institution (Capiga et al. 2016). Cost-based competition, the technology used, or the products offered, seem to be less effective due to the ease with which they can be copied (Bharadway et al. 1993).

Flexibility, responsiveness, the ability to learn, and the use of employees’ competencies are currently goals for human resource management in banks. Therefore, human capital, based on the knowledge of bank employees, seems to be the most important part of intellectual capital. It is an indispensable starting point when creating a bank’s organizational capital (including knowledge in a system of specific norms, which, while remaining in the bank, teaches the other employees), relational and social capital.

In light of a number of challenges that the banking sector will face, the key to developing its potential is to systematically build the professionalism of the sector’s employees by usage of a wide range of HRM practices, while literature often emphasises insufficient diversified practices of HRM (Ray et al. 2021).

This strategy is conditioned by the company’s business strategy, its organizational structure and culture, and its philosophy (Shahnawaz and Juyal 2006). Most often, HRM is based on functions that correspond to the employee life cycle, from his entry into the organization to his exit. It includes the following areas: recruitment and leaving work, training, development, and promotion, work organization, health protection, termination of employment and retirement (Kołodziejczyk-Olczak 2014).

Apart from the more traditional, functional orientation, it is worth recommending an approach based on practices that bring equal benefits to the workers and the employers:

- −

- managing competencies, including knowledge,

- −

- increasing the motivation to work, commitment, and well-being,

- −

- work-life balance programs (Warwas 2017).

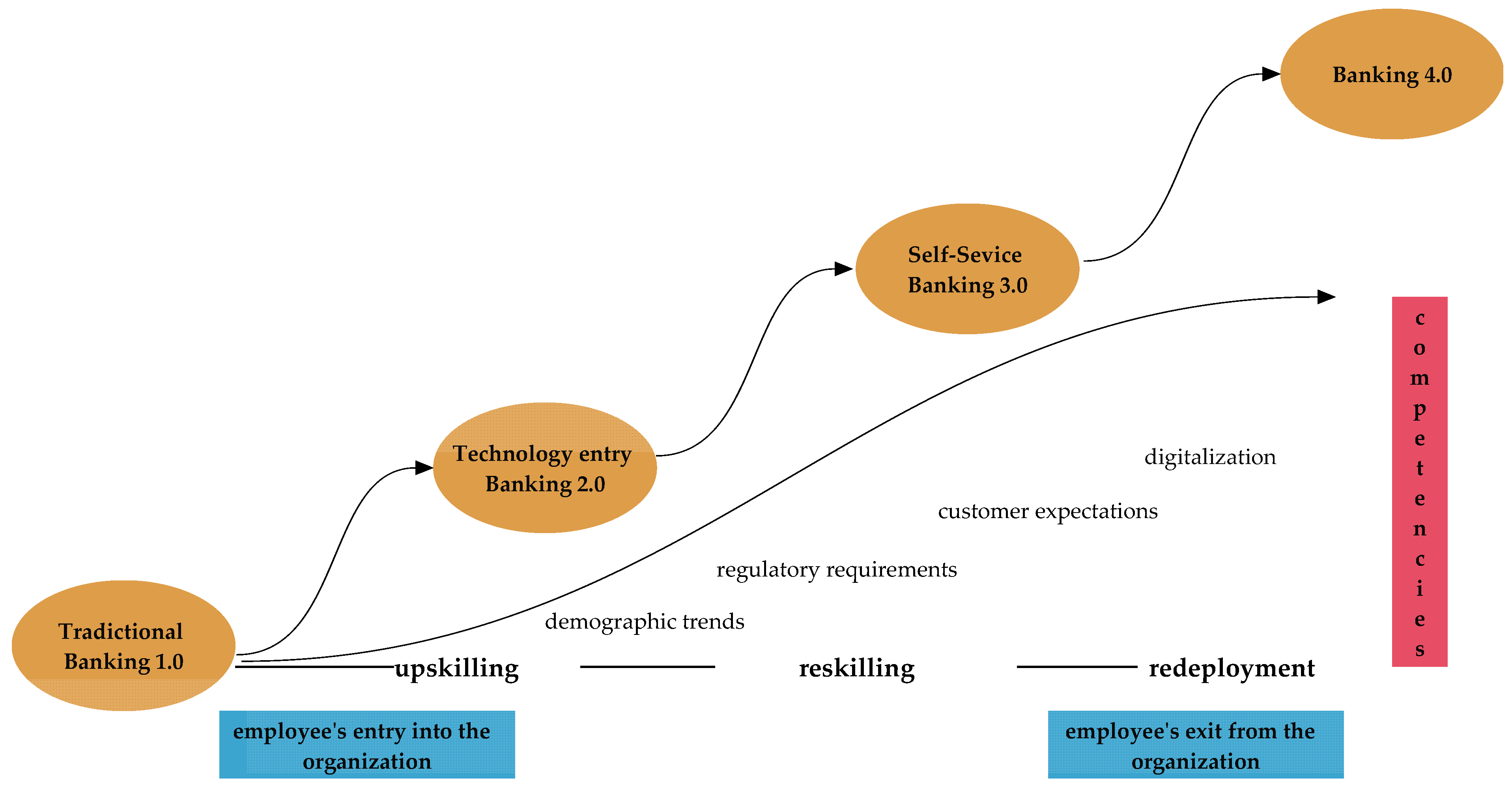

Banks depend largely on the quality and competence of its employees. Therefore, organizations have to pay more attention to their human resources, because implementation of human resource practices supports maximizing employees’ competences in the organization (Saleem and Khurshid 2014). Thereby, for banks to attract new competent employees and maintain those existing talented ones, consistent human resource management practices, employee job satisfaction, and organizational commitment should be achieved by a coherent range of HRM practices. As can be seen from Figure 4, the activities mentioned in the European research can be grouped into three main areas: reskilling (training an employee for a new job), upskilling (giving an employee additional skills in an existing job), and redeployment (assigning an employee to a new task). Our findings support the thesis (see Figure 4).

Before initiating any upskilling or reskilling effort, it is essential to base them on forecasts of shifts in the role mix and to focus on critical skills for specific roles in the banking sector. The reskilling tool can help match employees to new roles for when the bank needs to hire internally. Based on the requirements of the new role, the tool can help select targeted trainees and assign them to the proper training, taking into consideration their skills, background, education, and experience (Meyer and Smith 2009).

Based on forecasts of shifts in the role mix, banks have focused on critical skills for specific roles (for example, remote skills for advisers) and for general needs across roles (for instance, adaptability skills). Banks that want to meet the competition, have to design a parallel upskilling and reskilling process. Banks have offered training on new skills that employees can use in their current jobs (upskilling) or for new jobs (reskilling). Banks have redeployed talent from surplus to shortage areas to help save costs and bolster reputations. Selected processes, based on those mentioned above, are detailed in Table 9 (Alhajjar et al. 2018).

The above-developed complex “cafeteria” of possible solutions shows the entire spectrum of activities. Considering that in the banking sector, the trend is to reduce employment, the stress now and in the near future will be on updating employees’ competencies and retaining key knowledge. Managing competencies contains all those practices that relate to updating knowledge and raising competencies. With today’s challenges, this process can occur as an intergenerational transfer. It was mentioned earlier that the demand for certain positions is changing in the banking sector. Positions such as cybersecurity specialist, big data engineer, mobile developer, or digitalization specialist will probably be the domain of employees mainly from younger generations, generations Y and C. This is due to the characteristics of these generations. Young employees are computer natives, while the process of accepting and adopting technology among seniors takes longer (Vulpe and Crăciun 2019).

Nevertheless, mentoring and reverse mentoring can be recommended. As part of multigeneration teams, the transfer of ICT competencies is possible for older employees, while soft skills related to communication, empathy, cooperation or problem-solving, may be transferred to the younger employees (Nagarajan et al. 2019). Equipped with technological competencies, older employees are efficient at work, and younger employees can serve their bank’s clients better. It is possible to build long-term relationships based on substantive and, above all, soft competencies.

Cooperation in intergenerational teams strengthens their interdisciplinary nature, which is highly desired in the banking sector. Positions such as customer journey expert, product design specialist, head of user experience, or banking analyst are not only useful, but they are available to employees of all ages because the recipients of banking services are customers of all ages. In accordance with the silver economy concept, the banking sector should focus on mature customers and seniors, monitoring their needs and expectations, and modifying their products and services accordingly (Naegele and Walker 2006). In addition, in certain segments and certain types of transactions, the employee’s age raises confidence due to their life experience. Positions where a risk or specialist assessment takes place (risk management specialist, compliance specialist) require trust, balance, and multi-criteria decision-making skills.

Mismatches are noted, however. The biggest gap is noticed with conceptual thinking, analytical abilities, searching for information (banking), and self-confidence in selling insurance. The answer to these complex mismatched processes is in the area of employee competencies in training (Motlokoa et al. 2018). If they are to result in the desired outcome, the management of the banking sector institutions should be open, fostering a “culture of training”. Training is an investment, so, like any investment, it involves risks. Young employees want to learn and develop, but they may want to quickly leave the organization, and turnover among young employees is noticeable. In turn, not all older employees will want to train, and some will not achieve the expected results (Afroz 2018). However, human capital is still the leverage of development, and the strategy of investing in human capital brings better results, not only in the economic sense (Paul and Anantharaman 2004; Schröder et al. 2014). While undergoing training, employee morale is built, and attachment to the organization and feelings of engaging with the employer and the team are born, based on effective and normative engagement. In the long run, this improves banks’ profitability and is particularly important when interest rates are low.

Regarding skills, vital ICT competencies can be acquired at any age. People employed in ICT positions will be required to solve problems, so programming, logical thinking, critical thinking, and creative skills (World Economic Forum 2020) to cope with problems, as well as selected aspects of the cognitive process, can be perfectly developed in intergenerational teams. Creativity is a meta competence that can be developed throughout life. Analytical and problem-solving abilities, as well as creativity, and the ability to work across disciplines, are the skills that will keep employees important to the company even as AI and automation take over their job functions (Rotatori et al. 2020).

In addition, the analysis of the profiles of the most popular workplaces in the banking sector (including analyst, corporate client advisor, operational risk specialist, managerial staff) show that social competencies are an integral component of each position. When it comes to maintaining the quality of work, the most critical competencies include accuracy, readiness to work in accordance with applicable procedures, duty, responsibility, compliance with the code of ethics, banking secrecy and confidentiality, independence, the ability to cooperate with an internal client, communication skills, and flexibility in action. The above cafeteria seems to be the domain of mature employees, who are also carriers of values that result from the organizational culture.

Stabilizing the skills of desired employees will facilitate the fight for talent. The main objective of talent management is to develop skills and retain the workforce, which consists of highly skilled and committed employees (Alhajjar et al. 2018). The competency requirements set by the banking sector include people skills, ability to work with clients, and interpersonal communication (39%), knowledge and professional experience (28%), and responsibility, discipline, honesty, diligence, and reliability (24%), (Górniak et al. 2018). In other words, competencies that grow with age. These requirements are also a prerequisite for the design and implementation of human resources strategies.

Working in conditions of uncertainty, the stress associated with the need to learn or a change in the employment structure, and, in particular, an intense pressure to achieve results and fulfill plans, leave room to develop programs in the banking sector that allow a healthy balance between work and life. Sustainable jobs create well-being at work, which in turn is linked to the creation of high-quality jobs. Employees tend not to leave such workplaces, and thus, latent knowledge does not flow out of the organization with departing employees. Furthermore, the increasing number of older employees in modern organizations and the potential negative attitudes of younger employees toward them create the need for better understanding between generations (Rožman et al. 2020).

6. Discussion

Digitality affects people and gives them new abilities for expression and for shaping society. Thus, the banking sector requires a successful HR strategy to cope with the transformation challenges of Industry 4.0 (Wolor et al. 2019). Fixed assets, land, and capital are no longer key resources for an organization to maintain its competitiveness in the current changing environment (Kumar and Mathimaran 2017).

Most authors conclude that digitalization is the most powerful driver of changes in the banking sector (Beck et al. 2016; Puschmann 2017), although only a few authors are concerned by human resources (Kitsios et al. 2021; Bastari et al. 2020). It is, therefore, true that digital technology dominates in replacing human roles in banking. The result is a resizing of the branch and agent networks and a reorganizing of their channel management towards hybrid client interaction and more customer self-services (Kusumawati 2019). This affects the range of services offered in modern bank branches (Nüesch et al. 2015), especially those focused on professional advice, but we should not forget about other factors.

Digitalization has increased competition in the banking sector. Banks reach for competitive advantages based not only on technological solutions but on service quality, trust-building, and ensuring professionalism in customer service, i.e., building and managing customer relationships. Therefore, the reaction to digitization should not only be a quantitative approach to the number of facilities and employees, but should also be qualitative, based on the need for systematic training and even retraining of some staff (Kitsios et al. 2021). Banks believe that training increases employees’ job skills and training reduces employee turnover (Anusara et al. 2019). It is a process of building human capital that can be developed as a source of competitive advantage, although it does not guarantee this advantage (Wright and McMahan 2011).

Digitization has also changed the way customers use banking products. Now they expect increased personalization of products and services, omnichannel service, universal availability of products, and ease of use (Zhao et al. 2019; Ananda et al. 2020). Faced with a better informed and more competent customer, advisers are thus required to be professionals (Dubois et al. 2011). This requires banks to have specialists not only from the IT department but also those responsible for obtaining information about customers and analyzing them, to create new products better suited to their needs. As a result, banks are struggling to keep up with the growing need for new skills and capabilities in the workforce. Ensuring high-quality service to customers in a highly competitive banking environment can harm the psychological well-being of employees, so in human resources management, they cannot fail to care for their workforce. The importance of IT competencies is increasing, but so are those that promote the transfer of knowledge within the bank and build relationships with customers, i.e., interpersonal competencies (especially communicativeness), cognitive skills, and responsibility. In the development of this type of competence, intergenerational transfer can be very useful.

From the authors’ point of view in human resource management, the impact of legal regulations on the banking sector cannot be underestimated. Regulations such as the Payment Service Direction II create a huge drive for the transformation of finance. Open banking generates benefits for the customers but, at the same time, it results in greater competition in the financial sector (Deng et al. 2019). The European regulation grants Fintech access to customer data that was previously under the sole possession of banks; however, the incumbents maintain the market power over the standards that enable Fintech to gain access to customer information (Haddad and Hornuf 2019). Banks should offer the highest convenience, while simultaneously being the most trusted by customers (Dratva 2020). It is worth stressing that legal regulations impose specific requirements on banks related to the quality of services provided and their security, resulting in the need to have a highly qualified and professional workforce.

It is also necessary to take into account demographic trends that affect employment policy. Demographic trends affect not only the demand side by increasing the popularity of electronic banking, but also the age structure of banking employees. Regarding age, the authors focused on selected human resource management tools, and the issue often addressed is talent management in the organization. The banking sector is now facing many challenges, especially with high turnover and workforce engagement, both of which can be due to deficiencies in the talent management (Mawlawi and El Fawal 2018). Banks are facing stiff competition for talent, and retaining the right people is becoming a competitive advantage and a must for survival. In line with Elia et al. (2017), employee performance is positively correlated with the implementation of Talent Management Initiatives. Bank talent initiatives should refer to acquired soft skills, learning ability, flexibility, and technology adaptability of high performers/potentials (Dang et al. 2020).

The literature review and the Delphi studies with QCA analysis confirm that it was valuable to introduce age management and intergenerational solidarity within organizations. The experts especially appreciate and recommend incorporating and promoting practices in banks such as a mentoring program where older workers share knowledge of services, etc., while the younger ones do the same regarding e-skills, creating a culture of sharing experiences.

In conclusion, the multitude and diversity of factors that affect the banking sector call for a more coherent approach by human resources departments to using upskilling, reskilling, and redeployment in parallel. Taking into account the specifics of the sector, in which employees’ knowledge and human capital play an important role, and dynamic changes force a change in their competence profile, this approach takes into account digitization, the impact of legal regulations, and changes in consumer expectations. In response to these challenges, banking entities must combine substantial financial capital with human capital that is highly qualified in both knowledge and abilities.

7. Conclusions and Contributions

The study revealed that human resource management is very significant to the survival of the banking sector in today’s highly competitive business environment. Banking 4.0 forces employees to develop skills related to new technologies, cybersecurity, the digitization of processes, and data analysis. Increasing interdisciplinarity is required of employees, and the key competencies include digital, analytical, and mathematical competencies, high sales/consulting skills, problem-solving, creativity, and openness: and honesty, responsibility, reliability. The challenge is to combine extensive expertise in the area of finance and modern digital tools with communication skills, relationship management, and the need to maintain good customer relations, as well as critical thinking and teamwork.

Our contribution to the theory and practice is threefold. First, it extends human resource management to the context of Banking 4.0. Secondly, this study also contributes to human resources management research in the era of Banking 4.0 thanks to a multiapproach perspective, the literature review, the inventory of good practice form and the Delphi study results support by QCA analysis. Therefore, based on quantitative and qualitative methods this study provides a comprehensive view of the challenges that are shaping human resources management today. It provides a roadmap for human resource management that can help banks manage the main challenges related to digitalization, regulations, and client expectations. The research confirms the hypothesis that only a coherent perception of human resource practices including reskilling, upskilling, and redeployment is a solution that can help to mitigate the challenges in the era of Banking 4.0.

Finally, the global COVID-19 pandemic has accelerated those trends and has added urgency to the discussion. The pandemic has led to many significant innovations in the way banking services operate and has undoubtedly accelerated the digital transformation agenda beyond all predictions. It has required banks to respond with agility, placing a greater focus on their most important asset: their workforce. In light of this, sustainable human resource management, with an even greater focus on designing, implementing, and monitoring employee well-being, will become important. There is a particularly strong voice now for prioritizing practices aimed at improving well-being and positive employee relations over performance improvement, according to the mutual gains model of HRM (Guest 2017).

Author Contributions

Data curation, I.K. and I.W.; Formal analysis, I.K. and I.W.; Methodology, I.W. and I.K.; Writing—original draft, I.K. and I.W. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data is available upon request.

Acknowledgments

This research received no external funding. This study was carried out as a part of an international project from DG Employment, Social Affairs and Inclusion entitled, The European social dialogue and the development of the solidarity between generations of workers: focus on “over 55” and young workers in the finance sector. Sustainable Growth and generation gap (VS/2018/0040) and thanks to financing from the Polish Ministry of Science and Higher Education (4031/GRANT KE/2018/2). We cordially thank Justyna Wiktorowicz, who is a member of the research team, for her support in developing the concept of the article and the methodological part. We also wish to thank Łukasz Kozar, a member of the research team, for his special engagement in desk research.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Accenture. 2021a. Digital Banking Redefined in 2021. Available online: https://www.deloittedigital.com/us/en/offerings/next-gen-digital-banking/digital-banking-redefined-in-2021.html (accessed on 11 October 2021).

- Accenture. 2021b. The Future of Work: Productive Anywhere. Available online: https://www.accenture.com/_acnmedia/PDF-155/Accenture-Future-Of-Work-Global-Report.pdf#zoom=40 (accessed on 11 October 2021).

- Acharya, Viral V., Robert Engle, and Steffen Sascha. 2021. Why Did Bank Stocks Crash during COVID-19? CEPR Discussion Papers 15901. C.E.P.R. Discussion Papers. Cambridge: NBER. [Google Scholar] [CrossRef]

- Adesina, Kolade Sunday. 2021. How diversification affects bank performance: The role of human capital. Economic Modelling 94: 303–19. [Google Scholar] [CrossRef]

- Afroz, Nushrat N. 2018. Effects of Training on Employee Performance—A Study on Banking Sector, Tangail Bangladesh. Global Journal of Economic and Business 4: 111–24. [Google Scholar] [CrossRef]

- Ahamed, Mostak M. 2017. Asset quality, non-interest income, and bank profitability: Evidence from Indian banks. Economic Modelling 63: 1–14. [Google Scholar] [CrossRef]

- Alhajjar, Anas A., Rezian-na Muhammed Kassim, Valliappan Raju, and Tarek Alnachef. 2018. Driving Industry 4.0 Business Through Talent Management of Human Resource System: The Conceptual Framework for Banking Industry. World Journal of Research and Review 7: 53–57. [Google Scholar]

- Al-Musali, M. A., and K. N. I. Ku Ismail. 2016. Cross-country comparison of intellectual capital performance and its impact on financial performance of commercial banks in GCC countries. International Journal of Islamic and Middle Eastern Finance and Management 9: 512–31. [Google Scholar] [CrossRef]

- Alsafadi, Yousef, and Shadi Altahat. 2021. Human Resource Management Practices and Employee Performance: The Role of Job Satisfaction. Journal of Asian Finance, Economics and Business 8: 519–29. [Google Scholar] [CrossRef]

- Ananda, S. Upadhyaya, Devesh Sonal, and Anis Moosa Al Lawati. 2020. What factors drive the adoption of digital banking? An empirical study from the perspective of Omani retail banking. Journal of Financial Services Marketing 25: 14–24. [Google Scholar] [CrossRef]

- Anusara, Jhensanam, Md Rasel, Ayrin Sultana, Bouasone Chanthamith, Md Humayun Kabir, and Md Arafatul Hasan. 2019. Comparative Study on Human Resource Management Practices in Banking Sector. American Journal of Marketing Research 5: 36–41. [Google Scholar]

- Aryee, Samuel, Fred O. Walumbwa, Emmanuel Y. M. Seidu, and Lilian Otaye. 2012. Impact of high-performance work systems on individual- and branch-level performance: Test of a multilevel model of intermediate linkages. The Journal of Applied Psychology 97: 287–300. [Google Scholar] [CrossRef] [PubMed]

- Auer, Raphael, Giulio Cornelli, and Jon Frost. 2020. COVID-19, Cash, and the Future of Payments. BIS Bulletin No 3. Available online: https://www.bis.org/publ/bisbull03.pdf (accessed on 12 October 2021).

- Bartel, Ann P. 2004. Human Resource Management and Organizational Performance: Evidence from Retail Banking. ILR Review 57: 181–203. [Google Scholar] [CrossRef]

- Bastari, Ary, Anis Eliyana, Agus Syabarrudin, Zainal Arief, and Alvin Permana Emur. 2020. Digitalization in Banking Sector: The Role of Intrinsic Motivation. Heliyon 6: e05801. [Google Scholar] [CrossRef]

- Beck, Thorsten, Tao Chen, Chen Lin, and Frank Song. 2016. Financial innovation: The bright and the dark sides. Journal of Banking and Finance 72: 28–51. [Google Scholar] [CrossRef]

- Bharadway, Sundar G., P. Rajan Varadarajan, and John Fahy. 1993. Sustainable Competitive Advantage in Service Industries: A Conceptual Model and Research Propositions. Journal of Marketing 57: 83–99. [Google Scholar] [CrossRef]

- Bretschneider, Stuart, Frederick J. Marc-Aurele, and Jiannan Wu. 2015. Best Practices. Research: A Methodological Guide for the Perplexed. Journal of Public Administration Research and Theory: J-PART 15: 307–23. [Google Scholar] [CrossRef]

- Canals, Jordi. 1993. Competitive Strategies in European Banking. Oxford: Clarendon Press. [Google Scholar]

- Capiga, Mirosława, Witold Gradoń, and Grażyna Szustak. 2016. Kreowanie Wartości Banku. Warszawa: Wydawnictwo CeDeWu. [Google Scholar]

- CEDEFOP. 2015. National Qualifications Framework Developments in Europe Analysis and Overview 2015–16. Available online: http://www.cedefop.europa.eu/files/5565_en.pdf (accessed on 10 October 2021).

- Chen, Tser-yieth. 1999. Critical Success Factors for Various Strategies in the Banking. International Journal of Bank Marketing 17: 83–92. [Google Scholar] [CrossRef]

- Cherif, Fatma. 2020. The role of human resource management practices and employee job satisfaction in predicting organizational commitment in Saudi Arabian banking sector. International Journal of Sociology and Social Policy 40: 529–41. [Google Scholar] [CrossRef]

- Dang, Nhan Truong Thanh, Quynh Thi Nguyen, Raymund Habaradas, Van Dung HA, and Van Thuy Nguyen. 2020. Talent Conceptualization and Talent Management Approaches in the Vietnamese Banking Sector. Journal of Asian Finance, Economics and Business 7: 453–62. [Google Scholar] [CrossRef]

- Deloitte. 2019. What Is the Future of Work? Redefining Work, Workforces, and Workplaces. Available online: https://www2.deloitte.com/us/en/insights/focus/technology-and-the-future-of-work/redefining-work-workforces-workplaces.html (accessed on 5 October 2021).

- Demirgüç-Kunt, Asli, Alvaro Pedraza, and Claudia Ruiz-Ortega. 2021. Banking sector performance during the COVID-19 crisis. Journal of Banking & Finance 133: 106305. [Google Scholar] [CrossRef]

- Deng, Xiang, Zhi Huang, and Xiang Cheng. 2019. FinTech and Sustainable Development: Evidence from China Based on P2P Data. Sustainability 11: 6434. [Google Scholar] [CrossRef] [Green Version]

- Devlin, Jim, and Christine Ennew. 1997. Understanding competitive advantage in retail financial services. International Journal of Bank Marketing 15: 73–82. [Google Scholar] [CrossRef]

- Dratva, Richard. 2020. Is open banking driving the financial industry towards a true electronic market? Electronic Markets 30: 65–67. [Google Scholar] [CrossRef]

- Dubois, Michel, Marc-Eric Bobillier Chaumon, and Didier Retour. 2011. The impact of development of customer online banking skills on customer adviser skills. New Technology, Work and Employment 26: 156–73. [Google Scholar] [CrossRef]

- ECB. 2021. EU Structural Financial Indicators. Available online: https://www.ecb.europa.eu/press/pr/date/2021/html/ecb.pr210526_annex~b5ce7a6554.en.pdf (accessed on 10 October 2021).

- Elia, Pamela T., Kalil Ghazzawi, and Badih Arnaout. 2017. Talent Management Implications in the Lebanese Banking Industry. Human Resource Management Research 7: 83–89. [Google Scholar] [CrossRef]

- EU. 2015. Directive (EU) 2015/2366 of the European Parliament and of the Council of 25 November 2015 on payment services in the internal market, amending Directives 2002/65/EC, 2009/110/EC and 2013/36/EU and Regulation (EU) No 1093/2010, and repealing Directive 2007/64/EC. OJ L 337: 35–127. [Google Scholar]

- EU. 2018. Directive (EU) 2018/843 of the European Parliament and of the Council of 30 May 2018 amending Directive (EU) 2015/849 on the prevention of the use of the financial system for the purposes of money laundering or terrorist financing, and amending Directives 2009/138/EC and 2013/36/EU. OJ L 156: 43–74. [Google Scholar]

- EU. 2019. Directive (EU) 2019/878 of the European Parliament and of the Council of 20 May 2019 amending Directive 2013/36/EU as regards exempted entities, financial holding companies, mixed financial holding companies, remuneration, supervisory measures and powers and capital conservation measures. OJ L 150: 253–95. [Google Scholar]

- Fintech Circle. 2017. 94% of People in Financial Services Suspect Colleagues Are Bluffing about Their Fintech Knowledge. Available online: https://www.finextra.com/pressarticle/70717/94-of-people-in-financial-services-suspect-colleagues-are-bluffing-about-their-fintech-knowledge (accessed on 22 August 2021).

- Gelade, Garry A., and Mark Ivery. 2003. The impact of human resource management and work climate on organizational performance. Personnel Psychology 56: 383–404. [Google Scholar] [CrossRef]

- Górniak, Jarosław, Kocór Marcin, Kwinta Odrzywołek Joanna, Maźnica Łukasz, Worek Barbara, and Jakub Wróblewski. 2018. Centrum Ewaluacji i Analiz Polityk Publicznych Uniwersytetu Jagiellońskiego. Available online: https://www.parp.gov.pl/storage/publications/pdf/37-RAPORT-sektor-finansowy-210x270-inter_200511.pdf (accessed on 9 October 2021).

- Guest, David E. 2017. Human resource management and employee well-being: Towards a new analytic framework. Human Resource Management Journal 27: 22–38. [Google Scholar] [CrossRef] [Green Version]

- Haddad, Christian, and Lars Hornuf. 2019. The emergence of the global fintech market: Economic and technological determinants. Small Business Economics 53: 81–105. [Google Scholar] [CrossRef] [Green Version]

- Hitt, Michael A., Leonard Bierman, Katsuhiko Shimizu, and Rahul Kochhar. 2001. Direct and Moderating Effects of Human Capital on Strategy and Performance in Professional Service Firms: A Resource-Based Perspective. The Academy of Management Journal 44: 13–28. [Google Scholar] [CrossRef]

- Huynh, Quang Linh, Thanh Thuy Nguyen Thi, Tan Khuong Huynh, Tuyet Anh Duong Thi, and Thuy Lan Le Thi. 2020. Comparative significance of human resource management practices on banking financial performance with analytic hierarchy process. Accounting 6: 1323–28. [Google Scholar] [CrossRef]

- Jeni, Fatema Akter, Momota, and Md. Al-Amin. 2021. The Impact of Training and Development on Employee Performance and Productivity: An Empirical Study on Private Bank of Noakhali Region in Bangladesh. South Asian Journal of Social Studies and Economics 9: 1–18. [Google Scholar] [CrossRef]

- Kaur, Navleen, Supriya Lamba Sahdev, Monika Sharma, and Laraibe Siddiqui. 2020. Banking 4.0: ‘The Influence of Artificial Intelligence on the Banking Industry & How AI Is Changing the Face of Modern Day Banks. International Journal of Management 11: 577–85. [Google Scholar] [CrossRef]

- King, Brett. 2018. Bank 4.0, Banking Everywhere, Never at a Bank. Singapore: Marshall Cavendish International (Asia) Pte Ltd. [Google Scholar]

- Kitsios, Fotis, Ioannis Giatsidis, and Maria Kamariotou. 2021. Digital Transformation and Strategy in the Banking Sector: Evaluating the Acceptance Rate of E-Services. Journal of Open Innoation: Technology, Market, and Complexity 7: 204. [Google Scholar] [CrossRef]

- Kołodziejczyk-Olczak, Izabela. 2014. Zarządzanie Pracownikami w Dojrzałym Wieku. Wyzwania i Problemy. Lodz: Lodz University Press. [Google Scholar]

- Kozar, Łukasz, Justyna Wiktorowicz, Izabela Warwas, and Iwa Kuchciak. 2020. Solidarity between Generations in the Financial Sector. Inventory of the Best Practices. Łódź (Internal Project Materials). Łódź: University of Lodz. [Google Scholar]

- KPMG. 2020. Digitalization in Banking Beyond Covid-19. Available online: https://assets.kpmg/content/dam/kpmg/be/pdf/2021/Digitalization-in-banking-beyond-Covid-19.pdf (accessed on 9 October 2021).

- Kuchciak, Iwa, and Justyna Wiktorowicz. 2020. Individual Determinants for the Transfer of Knowledge in the Financial Sector. Intergenerational Human Capital Management in Organizations 2: 81–87. [Google Scholar] [CrossRef]

- Kuchciak, Iwa, Justyna Wiktorowicz, and Izabela Warwas. 2020. Chapter 3: Age Management in the Financial Sector: Opportunities and Challenges. In Intergenerational Divide and Employee Solidarity. Inclusive Bargaining as a Drive for Change in the Digital Era. Edited by Domenico Iodice. Bergamo: Adapt University Press. [Google Scholar]

- Kumar, Ananda, and Balaji K. Mathimaran. 2017. Employee Retention Strategies. An Empirical Research. Global Journal of Management and Business 17. Available online: https://journalofbusiness.org/index.php/GJMBR/article/view/2243 (accessed on 9 October 2021).

- Kusumawati, Rizqi Adhyka. 2019. The change of human resources role in the banking digitalization era. The European Proceedings of Social & Behavioural Sciences. Available online: https://www.europeanproceedings.com/files/data/article/94/5421/article_94_5421_pdf_100.pdf (accessed on 9 October 2021).

- Marcinkowska, Monika. 2013. Kapitał Relacyjny Banków. Łódź: Wydawnictwo Uniwersytetu Łódzkiego. [Google Scholar]

- Mawlawi, Allam, and Abir El Fawal. 2018. Talent Management in the Lebanese Banking Sector. Management 8: 80–85. [Google Scholar] [CrossRef]

- Mbama, Cajetan I., and Patrick O. Ezepue. 2018. Digital banking, customer experience and bank financial performance: UK customers’ perceptions. International Journal of Bank Marketing 36: 230–55. [Google Scholar] [CrossRef]

- Mehdiabadi, Amir, Mariyeh Tabatabeinasab, Cristi Spulbar, Amir Karbassi Yazdi, and Ramona Birau. 2020. Are We Ready for the Challenge of Banks 4.0? Designing a Roadmap for Banking Systems in Industry 4.0. International Journal of Financial Studies 8: 32. [Google Scholar] [CrossRef]

- Mekinjić, Boško. 2019. The impact of Industry 4.0 on the transformation of the banking sector. Journal of Contemporary Economics 1. [Google Scholar] [CrossRef]

- Meles, Antonio, Claudio Porzio, Gabriele Sampagnaro, and Vincenzo Verdoliva. 2016. The impact of the intellectual capital efficiency on commercial banks performance: Evidence from the US. Journal of Multinational Financial Management 36: 64–74. [Google Scholar] [CrossRef]

- Meyer, John P., and Catherine A. Smith. 2009. HRM practices and organizational commitment: Test of a mediation model. Canadian Journal of Administrative Sciences 17: 319–31. [Google Scholar] [CrossRef]

- Mgiba, Freddy. 2019. Merger, Upskilling, and Reskilling of the Sales—Marketing Personnel in the Fourth Industrial Revolution Environment: A Conceptual Paper. Global Journal of Management and Business Research: E Marketing 19: 12–23. [Google Scholar]

- Mohapara, Suryanarayan, Sangram Keshari Jena, Amarnath Mitra, and Aviral Kumar Tiwari. 2019. Intellectual capital and firm performance: Evidence from Indian banking sector. Applied Economics 51: 6054–67. [Google Scholar] [CrossRef]

- Motlokoa, Mamofokeng Eliza, Lira Peter Sekantsi, and Rammuso Paul Monyolo. 2018. The Impact of Training on Employees’ Performance: The Case of Banking Sector in Lesotho. International Journal of Human Resource Studies 8: 16–46. [Google Scholar] [CrossRef]

- Munjuri, Mercy Gacheri, and Rachael Muthoni Maina. 2013. Workforce diversity management and employee performance in the banking sector in Kenya. DBA Africa Management Review 3: 1–21. Available online: http://journals.uonbi.ac.ke/damr/article/view/1088 (accessed on 7 October 2021).

- Naegele, Gerhard, and Alan Walker. 2006. A Guide to Good Practice in Age Management. Office for Official Publications of the European Communities. Available online: https://www.eurofound.europa.eu/sites/default/files/ef_publication/field_ef_document/ef05137en_1.pdf (accessed on 13 October 2021).

- Nagarajan, Renuga, Mineko Wanda, Mei Lan Fang, and Andrew Sixmith. 2019. Defining organizational contributions to sustaining an ageing workforce: A bibliometric review. European Journal of Ageing 9: 1–25. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, Thi Lam Anh. 2018. Diversification and bank efficiency in six ASEAN countries. Global Finance Journal 37: 57–78. [Google Scholar] [CrossRef]

- Nüesch, Rebecca, Rainer Alt, and Thomas Puschmann. 2015. Hybrid customer interaction. Business & Information Systems Engineering. The International Journal of Wirtschaftsinformatik 57: 73–78. [Google Scholar] [CrossRef]

- Park, Cyn-Young, and Jinyoung Kim. 2020. Education, Skill Training, and Lifelong Learning in the Era of Technological Revolution. Asian Development Bank Economics Working Paper Series 606; Mandaluyong: Asian Development Bank. [Google Scholar] [CrossRef]

- Paul, Achandy Kuriappan, and R. N. Anantharaman. 2004. Influence of HRM practices on organizational commitment: A study among software professionals in India. Human Resource Development Quarterly 15: 77–88. [Google Scholar] [CrossRef]

- Premchand, Anshu, and Anurag Choudhry. 2018. Open Banking & APIs for Transformation in Banking. Paper presented at 2018 International Conference on Communication, Computing and Internet of Things (IC3IoT), Chennai, India, February 15–17. [Google Scholar] [CrossRef]

- Puschmann, Thomas. 2017. Fintech. Business & Information Systems Engineering. The International Journal of Wirtschaftsinformatik 59: 69–76. [Google Scholar] [CrossRef]

- PwC. 2017. 20th CEO Survey, Key Talent Findings in the Financial Services Industry. Available online: https://www.pwc.com/gx/en/ceo-agenda/ceosurvey/2018/gx/industries/financial-services.html (accessed on 14 August 2021).

- Ragin, Charles C. 1987. The Comparative Method: Moving beyond Qualitative and Quan-Titative Strategies. Berkeley, Los Angeles and London: University of California Press. [Google Scholar]

- Ray, Shimul, Sraboni Bagchi, Md. Shahbub Alam, and Umme Salma Luna. 2021. Human Resource Management Practices in Banking Sector of Bangladesh: A Critical Review. OSR Journal of Business and Management 23: 1–7. [Google Scholar] [CrossRef]

- Rihoux, Benoît, and Charles C. Ragin. 2009. Configurational Comparative Methods: Qualitative Comparative Analysis (QCA) and Related Techniques. Thousand Oaks: SAGE Publications, Inc. [Google Scholar] [CrossRef]

- Rotatori, Denise, Eun Jeong Lee, and Sheryl Sleeva. 2020. The evolution of the workforce during the fourth industrial revolution. Human Resource Development International 24: 92–103. [Google Scholar] [CrossRef]

- Rožman, Maja, Sonja Treven, and Vesna Čančer. 2020. The impact of promoting intergenerational synergy on the work engagement of older employees in Slovenia. Journal of East European Management Studies 25: 9–34. [Google Scholar] [CrossRef]

- Rubel, Mohammad Rabiul Basher, Daisy Mui Hung Kee, and Nadia Newaz Rim. 2020. Matching People with Technology: Effect of HIWP on Technology Adaptation. South Asian Journal of Human Resources Management 7: 9–33. [Google Scholar] [CrossRef]

- Saint-Onge, Hubert. 1996. Tacit Knowledge: The key to the strategic alignment of intellectual capital. Planning Review 24: 10–16. [Google Scholar] [CrossRef]

- Saleem, Irfan, and Aitzaz Khurshid. 2014. Do human resource practices affect employee performance? Pakistan Business Review 15: 669–88. [Google Scholar]

- Schröder, Heike, Michael Muller-Camen, and Matthew Flynn. 2014. The management of an ageing workforce: Organisational policies in Germany and Britain. Journal of Human Resource Management 24: 394–409. [Google Scholar] [CrossRef]

- Shahnawaz, Muhhamed, and Rakesh C. Juyal. 2006. Human resource management practices and organizational commitment in different organizations. The Journal of the Indian Academy of Applied Psychology 32: 267–74. [Google Scholar]

- Sima, Violeta, I. G. Gheorghe, J. Subić, and D. Nancu. 2020. Influences of the Industry 4.0 Revolution on the Human Capital Development and Consumer Behavior: A Systematic Review. Sustainability 12: 4035. [Google Scholar] [CrossRef]

- Sveiby, Karl Erik. 1997. The Intangible Assets Monitor. Journal of Human Resource Costing and Accounting 2: 73–97. [Google Scholar] [CrossRef]

- Van Eck, Nees Jan, and Ludo Waltman. 2010. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 84: 523–38. [Google Scholar] [CrossRef] [Green Version]

- Vulpe, Simona, and Andrei Crăciun. 2019. Silver surfers from a European perspective: Technology communication usage among European seniors. European Journal of Ageing 17: 125–34. [Google Scholar] [CrossRef] [PubMed]

- Wahab, Siti Norida, Salini Devi Rajendran, and Swee Pin Yeap. 2021. Upskilling and reskilling requirement in logistics and supply chain industry for the fourth industrial revolution. Scientific Journal of Logistics 17: 399–410. [Google Scholar]

- Wall, Anthony. 2007. The Measurement and Management of Intellectual Capital in the Public Sector. Public Management Review 7: 289–303. [Google Scholar] [CrossRef]

- Waltman, Ludo, Nees Jan van Eck, and Ed C.M. Noyons. 2010. A unified approach to mapping and clustering of bibliometric networks. Journal of Informetrics 4: 629–35. [Google Scholar] [CrossRef] [Green Version]

- Warwas, Izabela. 2017. Zarządzanie Wiekiem w Polsce—Stan i Perspektywy Rozwoju. Polityka Społeczna 4: 33–38. [Google Scholar]

- Wolor, Christian Wiradendi, Hera Khairunnisa, and Dedi Purwana. 2019. Implementation Talent Management to Improve Organization’s Performance in Indonesia To Fight Industrial Revolution 4.0. International Journal of Scientific and Technology Research 9: 1243–47. [Google Scholar]

- World Economic Forum. 2020. The Future of Jobs Report. October. Available online: https://www3.weforum.org/docs/WEF_Future_of_Jobs_2020.pdf (accessed on 5 October 2021).

- Wright, Patrick M., and Gary C. McMahan. 2011. Exploring human capital: Putting ‘human’ back into strategic human resource management. Human Resource Management Journal 21: 93–104. [Google Scholar] [CrossRef]

- Zhao, Qun, Pei-Hsuan Tsai, and Jin-Long Wang. 2019. Improving financial service innovation strategies for enhancing China’s banking industry competitive advantage during the fintech revolution: A Hybrid MCDM model. Sustainability 11: 1419. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Co-occurrence relationships among keywords. Source: own elaboration based on VOSviewer version 1.6.17.

Figure 1.

Co-occurrence relationships among keywords. Source: own elaboration based on VOSviewer version 1.6.17.

Figure 2.

Most valued positions in the banking sector. Source: own elaboration.

Figure 3.

Steps in QCA analysis. Source: based on Rihoux and Ragin (2009).

Figure 3.

Steps in QCA analysis. Source: based on Rihoux and Ragin (2009).

Figure 4.

The roadmap for HRM in the Banking 4.0. Source: own elaboration.

Table 2.

Truth table explaining factors affecting positive and negative perception of HR practices based on age management and intergenerational solidarity. Source: own elaboration.

Table 2.

Truth table explaining factors affecting positive and negative perception of HR practices based on age management and intergenerational solidarity. Source: own elaboration.

| EDU07 | FLEX07 | LMP07 | TEMCYC07 | OUT | n | incl | Cases |

|---|---|---|---|---|---|---|---|

| 0 | 1 | 1 | 0 | 1 | 4 | 1.00 | Belgium, Denmark, Ireland, Netherlands |

| 1 | 0 | 0 | 1 | 1 | 3 | 1.00 | Czech Republic, Estonia, Slovenia |

| 1 | 1 | 0 | 1 | 1 | 3 | 1.00 | Latvia, Hungary, Slovakia |