1. Introduction

The International Monetary Fund (IMF), established in 1948, is an independent international organization. The IMF is a cooperative of 190 member countries, working on a mission of providing financial assistance to member countries, when needed, to tackle balance-of-payment problems, restore stability, and sustainable economic growth (

Bird and Rowlands 2017). The purpose of the IMF is outlined in its Article of Agreement (

Iseringhausen et al. 2019):

1. To give hope to member countries by making financial resources temporarily available under adequate safeguards, thereby helping them to overcome balance-of-payment crises and prevent them implementing policies that are destructive to economic prosperity by associating conditionality measures with the fund program.

2. To reduce the duration and shorten the period of disequilibrium in balance of payment. Any member country experiencing financial trouble, whether rich, middle-income, or poor, can turn to the IMF for financing. To tackle current account deficits, the IMF offers several concessional and non-concessional instruments to its member countries. The IMF-supported programs not only involve financial assistance, but there is also a policy advice and policy conditionality associated with it (

Marchesi and Sabani 2007). These policy adjustments serve as a condition for an IMF loan. It includes macroeconomic and structural policies and specific tools used to monitor the progress of a country towards its goals, defined by the country in collaboration with the IMF. The purpose of policy adjustment is to overcome balance-of-payment deficits without resorting to measures that are harmful to the country’s stability, and to ensure that the country will be able to pay back its loan (

Unigovskaya and Mercer-Blackman 2000). The participating country is responsible for implementing adjustment policies adequately to make the IMF-supported program successful.

To understand why a country may choose an IMF lending program is an important step towards determining overall economic performance and the stability of the participating country. There is extensive literature investigating the main drivers of the IMF lending program. Poor macroeconomic conditions and distorted current account balance are the prime reasons for a country to choose the IMF program (

Joyce 1992;

Knight and Santaella 1997;

Bird and Rowlands 2017). In addition, mismanagement of fiscal and monetary policies can lead to large economic imbalances, e.g., large current account deficit and high level of external and public debt (

Bird 2007). The purpose of the IMF program is to help such countries restore current account deficits and implement adjustment policies to achieve a stable economy and sustainable growth (

Conway 1994;

Gylfason 1987).

The IMF is responsible for helping member countries during both domestic and global crises. During the global crisis of 2008, the IMF strengthened its lending capacity and approved various financial support mechanisms for participating countries. These steps adopted by the IMF during the crisis helped in mitigating the instability, and allowed it to tailor the instruments to meet the financial needs of a participating country (

Hutchison 2004). At the same time, the IMF enhanced its capacity to provide concessional loans to low-income countries. The average limit under the IMF loan facilities were doubled (

Conway 2010). Similarly, a large number of low- and upper middle-income countries turned to the IMF for financing during the oil crisis of the 1970s and debt crisis of the 1980s (

Conway 2010). Currently, the IMF is engaged in lending programs with more than 50 countries and has allocated more than USD 325 billion to its member countries since the beginning of the financial crisis. We obtained this details from the official website of IMF, by using the following link

https://www.imf.org/external/about/lending.htm (assessed on 10 January 2021).

However, many countries have repeatedly chosen the IMF support program over the years due to deep-rooted structural and macroeconomic problems. In most cases, a successor program is implemented shortly after quitting the initial program (

Dreher 2006). This raises a question of the credibility of the IMF support program amid unresolved balance-of-payment problems of most participating countries. However, the interruption of the fund program and non-compliance with the conditionality measures may restrain a country from gaining macroeconomic stability (

Dreher 2006). The IMF has always faced huge criticism for its institutional structure and lending practices. Some studies argue that the IMF is a non-transparent institution, claiming that its programs have no impact in stabilizing the economy of participant countries (

Goldstein and Montiel 2017;

Przeworski and Vreeland 2000;

Bordo and Schwartz 2000;

Hutchison 2004).

In light of the above discussion, some policy questions can be raised: what are the reasons for a persistent stay under the IMF program, and why do countries seek IMF financial assistance for so long? Keeping these questions in mind, this study first attempts to investigate the determinants behind a persistent stay under the IMF program using panel survival analysis. We use cross-country panel data, consisting of 70 countries, over the period 1980–2018. Survival analysis, also known as duration analysis, was originally applied by bio-statisticians in medical research, but now it can be implemented in socio-economic research to investigate complex phenomena. Survival analysis includes the modeling of time to event data, and in this context, years under the IMF is considered to be time. Time involves a risk factor, i.e., what are the chances that an event will happen over time, and will it repeat itself? We assume that that event is probabilistic. This risk is a relationship between the chances that an event will happen given that it has not happened yet, measured as a probability of failure to survive. In comparison to the existing literature, we use a different methodology to find determinants behind persistent stays under the IMF program.

Secondly, we explore the impact of IMF program on participating countries. For instance,

Fidrmuc and Kostagianni (

2015) suggested that existing literature on effectiveness of IMF program encounters endogeneity bias. However, to overcome the issue of endogeneity, we use instrumental variables. We implement panel instrumental fixed effects using a two-stage least squares (2SLS) model. We observe that some countries in our sample show transition from lower middle-income level and become upper middle-, and high-income countries over the sample period of our study. Hence, we investigate the impact of the IMF program by dividing countries in our sample into two groups, i.e., the countries which show transition and become upper middle- and high-income, until 2018, as well as the countries which do not show transition and remain at low- or lower middle-income level, until 2018. The existing literature on the effectiveness of IMF program does not differentiate between countries based on their income level.

Bird and Rowlands (

2017) observed that most studies do not distinguish between low- and middle-income countries, even though there are substantial reasons to believe that the conditions under which they select IMF program are different. Therefore, we tried to identify the effectiveness of IMF program by differentiating between these categories.

Based on empirical analysis, our results are the following: (i) weak economic conditions increased risk for a country to adopt and stay under IMF program, i.e., low GDP, high current account deficit, high debt to service ratio. This study also attempts to find the risk for a country to implement the International Monetary Fund (IMF) program with regard to its income level and concludes that hazard rate for low-income countries to stay under IMF program is relatively greater as compared to lower middle- and upper middle-income countries. The existing literature does not take into account this effect. (ii) Our analysis depicts a positive picture of the IMF program. We conclude that the impact of the IMF fund program is positive to upper middle-income countries from the very first year of participating in it and remain positive and significant for all the subsequent three years. For low-income countries, IMF impact remains insignificant during first two years of participation in it. However, its impact becomes positive and significant during the third and fourth year.

The remainder of this paper is structured as follows:

Section 2 reviews the existing literature.

Section 3 discusses the research methodology and data collection.

Section 4 introduces empirical estimation and

Section 5 presents conclusion.

2. Literature Review

The International Monetary Fund (IMF) was designed as a result of an international conference which took place in 1944 in Bretton Woods, (USA). There were 44 countries participating in this conference, and the main objective was to provide a sustainable restructuring solution at the financial and currency nexus. International Monetary Fund (IMF) officially debuted on 27 December 1945 and initiated its financial operations in 1947. The main aim of IMF is based on international monetary cooperation by providing a global monitoring agency that supervises, consults, and collaborates on monetary problems,

Dammasch (

2006). Currently, the International Monetary Fund includes 190 countries. Moreover, according to the IMF’s official website, its main objective is “to ensure the stability of the international monetary system, i.e., the system of exchange rates and international payments that enables countries, but also their citizens, to transact with each other.” The IMF activity is focused on certain major directions, such as: to guarantee global monetary cooperation, to encourage sustainable economic growth and employment, to ensure financial stability, to support international trade and poverty alleviation. Moreover,

Spulbar et al. (

2020) suggested that sustainable economic growth plays an essential role in achieving major goals such as social justice, poverty alleviation and natural environment protection.

As a common perception, it is believed that IMF is an institution which provides resurrection or revives the nations from crises situations if such nations somehow get into turmoil either due to negligence, poor monetary and financial policies or just from inevitable outside situations. As a result of such a situation, the troubled nations more often choose to knock on the door of the IMF (

Nasir 2020). There is an extensive research study that looked at the motives which measure the reasons for repeated use of the IMF program, its determinants and effectiveness of the IMF program (

Iseringhausen et al. 2019). Most of the existing literature use the IMF program as binary choice logit or probit model or extreme bound analysis, frequently describing political and economic determinants of the IMF program. A few research studies use discriminant and descriptive statistics to determine the demand for the IMF program. Recurrent use of the IMF program has increased rapidly since 1970s in both middle- and low-income countries (

Marchesi and Sabani 2007). Most likely determinants for recurrent use of the IMF program are weak macro-economic determinants such as: low international reserves, large current account balance and low real growth and poor quality of institutions (

Iseringhausen et al. 2019;

Bird 2007;

Bird et al. 2004).

Economic and political factors represent the most consistent determinants in order to sign the IMF arrangement (

Orăștean et al. 2016;

Joyce 1992;

Gündüz 2009).

Knight and Santaella (

1997) observe 91 developing countries over a period of 1973–1991 by executing a probit model to find factors which determine the probability of a country to opt for the IMF program. Their findings suggest that rising demand of IMF funding program is based on the following: low level of international reserves, low GDP per capita, higher debt service ratio, low rate of domestic investment, movements in the real exchange rate and high ratio of external debt service to export earnings that increase probability of a country to seek IMF arrangement.

Cerutti (

2007) applied a probit model on 59 developing countries which are ineligible for PRGT program over a time period of 1982–2005. He found that low levels of international reserves and low GDP growth are the most significant reasons to influence the chances of a country to select the International Monetary Fund (IMF) program. Furthermore, the effect of world GDP growth becomes most significant during the crisis of 1980s.

Joyce (

1992) implemented a logit model on a sample of 45 low-per-capita-income countries over a period of 1980–1984 in order to find the determinants of the International Monetary Fund (IMF) program. He concluded that distorted economic policies, poor performance and lack of effective utilization of resources are increasingly contributing in forcing a country towards International Monetary Fund (IMF) relief packages. His findings suggested that countries which requested the IMF program were dealing with rapid expansion in case of domestic credit, severe balance of payment deficit, low- income level, large government sector and small reserve adequacy as compared to those countries which do not choose IMF assistance. Moreover, inequality of chance among the citizens of a country inevitably leads to economic and social imbalances based on the inefficient allocation of resources (

Birau et al. 2019).

Elekdağ (

2006) established the relationship between global economic factors and Stand-By Agreements (SBAs) by applying a probit model. The author concluded that higher oil prices, higher world real interest rate and harsh global recession increases the probability of an emerging country opting for an SBA program. He also interprets that when these variables are adversely shocked by one standard deviation, the probability of a country to request an SBA program doubles.

Berg et al. (

2015) demonstrate that whether a country is efficient or inefficient, the increase in its public spending does not affect its economic growth which contrasts the study of

Pritchett et al. (

2013) and common policy analysis view.

Gündüz (

2009) also concludes that global conditions play a significant role in determining the demand for the IMF program. He interprets that the IMF program requested by low-income countries is cyclical depending upon the intensity of global shock.

Orăștean et al. (

2016) developed a Z score function by using descriptive analysis to find economic factors behind IMF participation program for 153 emerging countries for both concession and non-concessional loans. A methodological based contribution in the literature is provided by

Orăștean et al. (

2016).

Many studies have concluded that the there is a linkage between the IMF program and the likelihood of conflicts and instability whether social or political (

Casper 2017;

Abouharb and Cingranelli 2007). According to

Hartzell et al. (

2010), there is a technical constraint in IMF programs because implementation of such programs involves limiting the macroeconomic policy discretion of the host nation that potentially can bring harmful distributional consequences. It becomes difficult for the governments to take hard decisions and to choose which societal group will bear the adjustment costs. Given the economic circumstances at that time, it becomes even more difficult and the ability of government to moderate economic costs becomes inhibited. In such situations, the response from the people or society may come in the form of violence and strikes which may harm the state further. However, costs of such programs vary drastically among democracies and autocracies and its imposed restraints over the government spending (

Nooruddin and Simmons 2006). In a landmark study,

Anton (

2016) highlights that the IMF lending program directly affects the foreign direct investment negatively especially in the emerging economies by providing a clear message of the uncertain economic situations of such economies.

The second strand of literature deals with the effectiveness of the IMF program. Most of the studies take three routes to determine the effectiveness of the IMF program. All of them include calculation of estimated propensity score.

The first approach evaluates the impact of the IMF program by estimating separate macroeconomic models for the participant and non-participant country samples. The estimated propensity score is used to calculate inverse Mills ratio for the two samples which are then used as separate regressors in the estimation equation to remove bias. The participation effect is then calculated from the difference in predicted values.

Przeworski and Vreeland (

2000) and

Vreeland (

2003) follow this approach.

The second approach estimates propensity score to match observations. The two observations are matched if they have nearly the same propensity score but a different participation decision then difference in participation is estimated. An average of many such matches will provide the effectiveness of the IMF program.

Hardoy (

2003) and

Hutchison (

2003) used this approach.

The third approach estimates structural equation through 2SLS model and bias is controlled by introducing an instrumental variable.

Fidrmuc and Kostagianni (

2015) used this approach.

Studies given on the bases of these three approaches are surprisingly different in their conclusions. Critics consider that the policy proposed by the IMF program is not suitable for the developing countries to retrieve stability and it only suppresses domestic demand. Therefore, impact of compliance with conditionality is quantitatively small on economic growth (

Dreher 2006;

Dollar and Svensson 2000).

Bird and Rowlands (

2017) interpret that the scope of successful implementation decreases when countries with sound policies negotiate a fund program with the IMF because it may instead reduce market confidence which thereby reduces economic growth.

Mehdiabadi et al. (

2020) argued that the banking system constitutes an essential element of the economic growth and macroeconomic stability.

Many research papers conclude that far from promoting development by stimulating economic growth, the IMF program impacts growth negatively (

Goldstein and Montiel 2017;

Przeworski and Vreeland 2000;

Bordo and Schwartz 2000;

Hardoy 2003;

Hutchison 2003;

Hutchison and Noy 2003;

Vreeland 2003;

Barro and Lee 2005).

Evrensel (

2002) predicts that the IMF program provides temporary improvement in balance of payment and international reserves to a developing country and this relief cannot be sustained in the post-program period. He interprets that, on average, each developing country implements a successive fund program with worse macroeconomic instability.

Hutchison’s (

2003) findings suggest that the cost of implementing the IMF program is 0.6–0.8% of GDP.

Przeworski and Vreeland (

2000) use all the programs offered by the IMF and estimate a growth model. Their findings suggest that IMF program reduces growth rate and there are no useful impacts of program implementation in the long run.

Haque and Khan (

1998) findings suggest negative impact on growth in the short run particularly due to demand compressing nature of conditionality proposed by IMF while long run shows evidence of positive growth rate.

Mussa and Savastano (

2000) suggested that ineffectiveness of the IMF program is the result of expansion in its scope. They claimed that reduction in poverty and achievement of high output growth rate is not a responsibility of the IMF program and disjunction between its core responsibilities and wider objective is the result of criticism against the IMF program.

Fundamental research studies report positive effects of the IMF lending fund program, i.e., (

Gylfason 1987;

Khan 1990;

Conway 1994;

Mireaux et al. 2000;

Hutchison 2004;

Atoyan and Conway 2006).

Gylfason (

1987) examined the relationship between credit creation in countries participating in the IMF program and current account balance thereby drawing an analogy with non participating developing countries. His findings suggest a reduction in credit creation and improvement in balance of payment of participating countries as compared to reference group countries whilst they found an insignificant effect on output growth and inflationary pressure.

Mireaux et al. (

2000) implemented an Enhanced Structural Adjustment Facility (ESAF) selected by low-income countries and by using Modified Control Group methodology, they conclude the positive effect of the program on growth.

Khan (

1990) observe that in the short run, there is significant improvement in balance of payment and current account, decrease in inflation and a reduction in growth of developing countries who choose the IMF program while in the long run, stability of macroeconomic indicators becomes strengthened and growth is also retained.

Conway (

1994) predicts an improvement in current account balance, positive economic growth and increased investment, when developing countries implement the IMF fund program.

Butkiewicz and Yanikkaya (

2005) investigated the effect of the IMF fund program by using empirical growth models that control for other growth determinants. However, the authors used value of loans instead of number of programs and conclude that fund lending stimulates growth, particularly by accelerating public investment.

According to

IMF (

2019a), the median public debt among a cluster of 59 countries included in the category of low-income developing economies increased from 38.7% of GDP for the sample period 2010–2014, up to 46.5% in 2017 and subsequently had a constant dynamic that stagnated. Moreover, low-income countries exhibit a high level of exposure regarding profit shifting and tax competition, but on the other hand they have a small number of options for increasing revenue (

IMF 2019b).

3. Research Methodology and Data Collection

We are using a panel data, consisting of 70 countries covering a very long specified time period from 1980 to 2018. Our variable of interest is “Years Under IMF program”. It is measured as binary variable, taking the value of 1 when the country is under the IMF program and 0 otherwise. The information about the IMF program is retrieved from IMF (see the official website:

https://www.imf.org/external/np/fin/tad/extarr1.aspx (assessed on 10 January 2021)). As we are concerned with reasons behind persistent and long use of the IMF program, the methodology adopted is Panel Survival Analysis. Survival analysis is a time to event analysis. It measures the length of time from origin until the event (failure) occurs. In case of our analysis, the

failure is when a country opts for the IMF support program. The superiority of survival analysis, sometimes also known as Duration Analysis, over the other econometric techniques for the analysis of such data is censoring minimum assumptions, and taking into account the time elapsed (see

Cleves et al. 2004).

The three basic approaches to model survival analysis are descriptive, semi-parametric and parametric. In this study, we take into account a parametric and descriptive framework in order to estimate our model. A non-parametric approach does not involve the distribution of failure times and how variation in independent variables impact the survival chance (

Cleves et al. 2004). Additionally, the application of a non-parametric approach is limited in scope because non-parametric methods are not good in dealing with censoring data and other data-related issues. As stated earlier, the duration analysis takes into account the duration of data until the happening of event (failure). An important measure used is hazard ratio. Hazard ratio is the unconditional probability that an event will occur given the probability that “up until now” the event has not yet occurred. Whilst cumulative hazard ratio is also cumulative risk at time t and can be written as follows:

Cumulative hazard represents the total amount of risk of experiencing the event, summed up to time t. Hazard function is the most useful estimator employed in survival analysis. It represents the probability of an event to occur at time t. It is measured as a derivative of cumulative hazard function. The shape of hazard function differs from one situation to another. If hazard rate is increasing over time, i.e., , then the chances of experiencing an event is increase over time and vice versa.

This indicates that the probability to experience an event varies in different situations. There are complex forms of hazard function, i.e., flat, monotone and non-monotone. The parametric model assumes a particular shape of hazard function. Some of the common parametric models include, i.e., Exponential Weibull, Lognormal, Loglogistic and Gompertz. Here, it is assumed that hazard function (

Hesketh and Skrondal 2012) is not only a function of time but it also varies with the characteristics of individual unit under observation (we used the following official website:

https://www.stata.com/manuals14/xtxtstreg.pdf assessed on 10 January 2021). So, here hazard function is represented as:

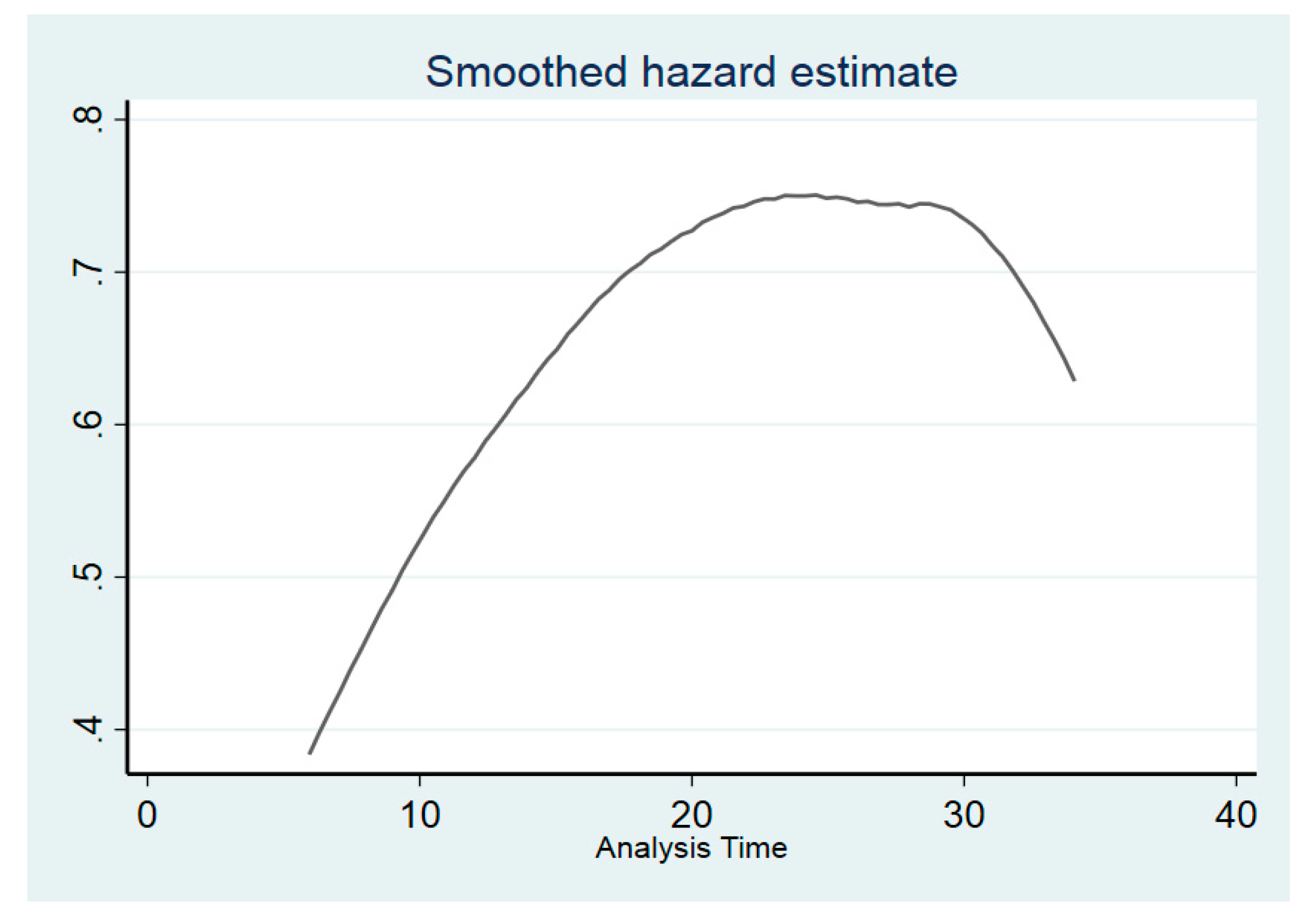

Appendix A represents the smooth hazard estimate (

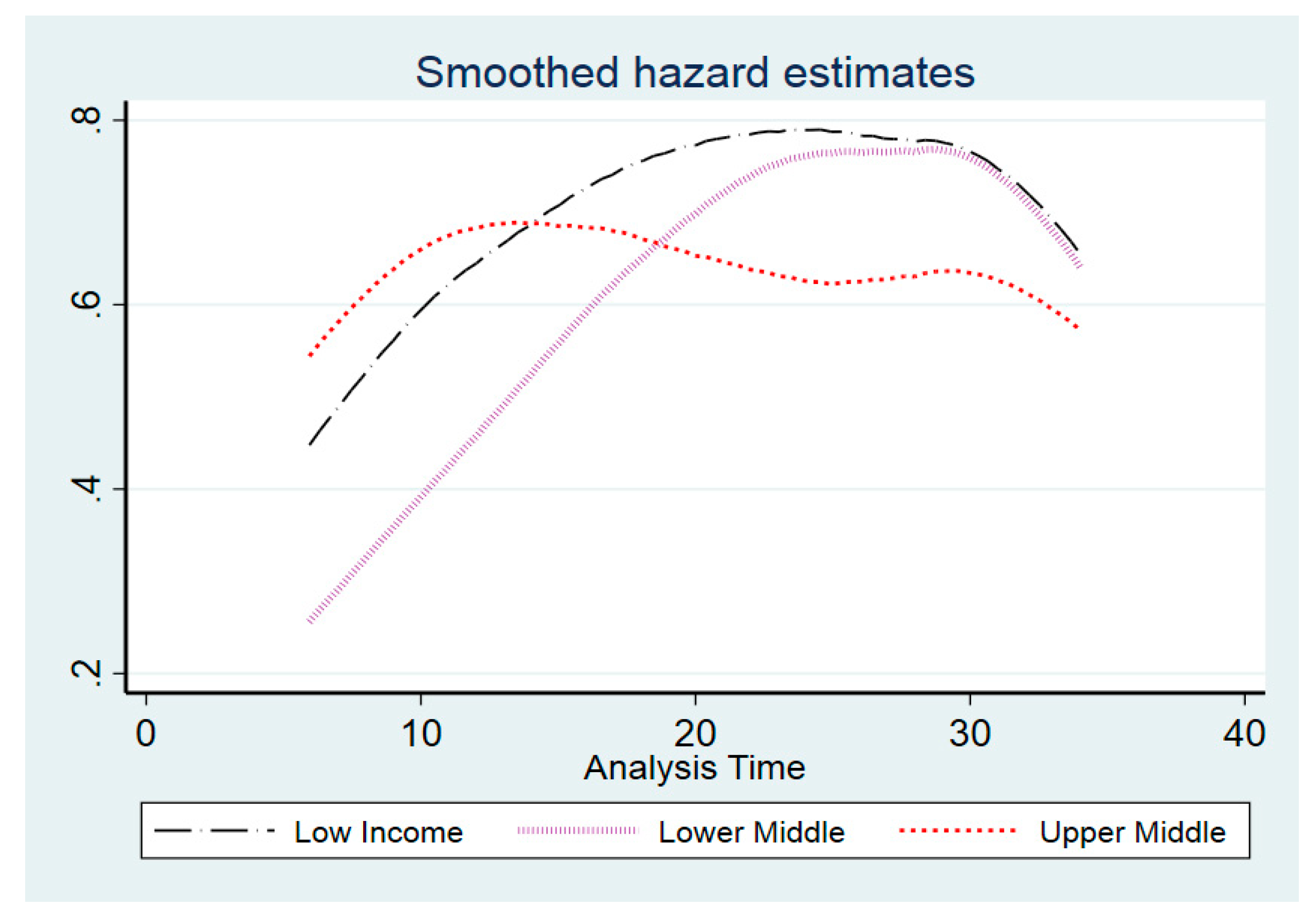

Figure A2) of our analysis. It shows that probability of experiencing the event for the subjects in our sample increases initially and then decreases over time, hence, confirming a non-monotone shape. Similarly, when we break down our analysis on the basis of the income level of countries, we get an overall similar trend for low-, middle- and upper middle-income countries (see

Figure A1 and

Figure A3).

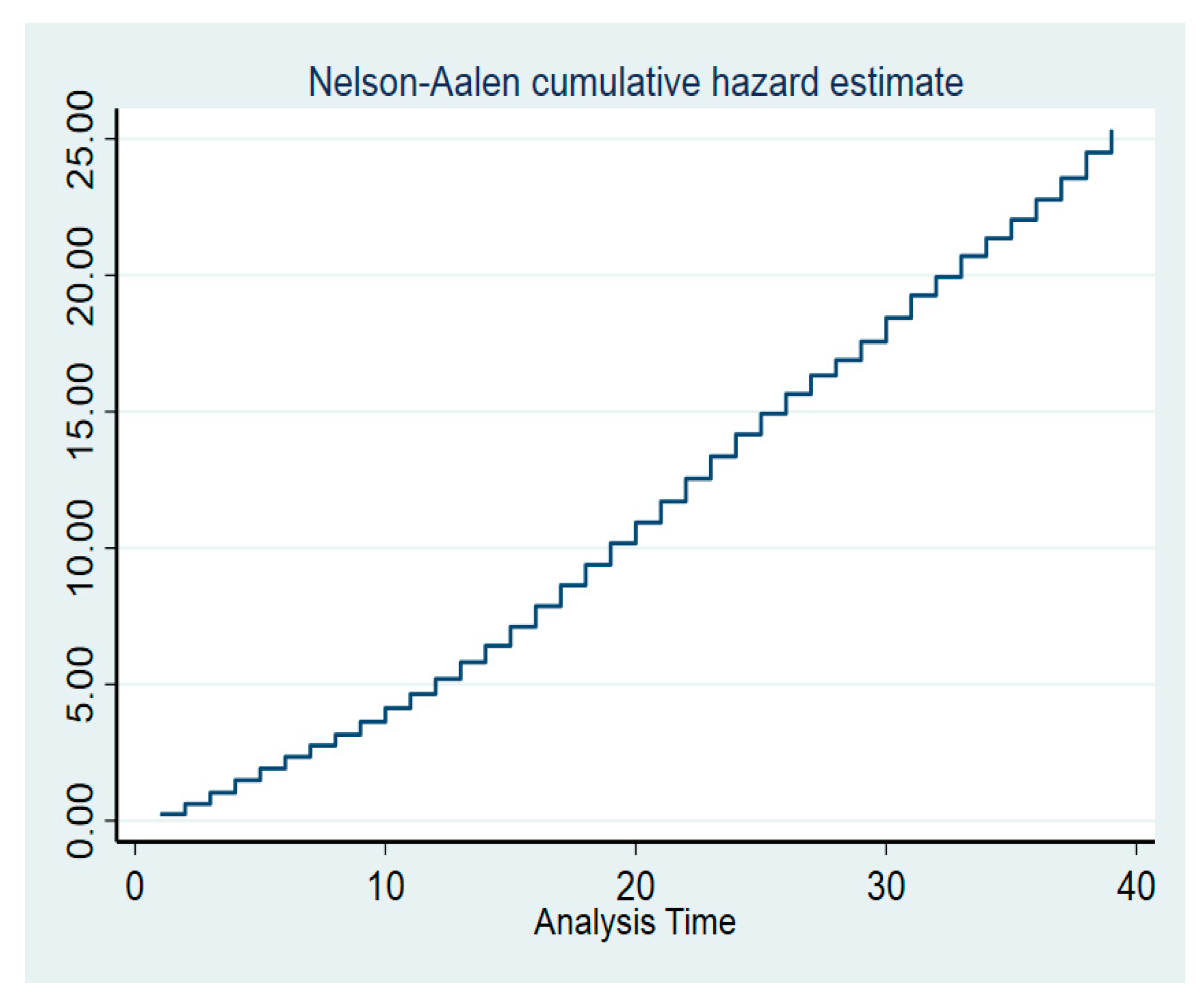

Figure A4 represents the cumulative hazard function. It represents total number (a sum-up) of expected failures within estimated period. It shows that probability to experience event (to opt IMF program) is increasing over the time and chances to survive is decreasing.

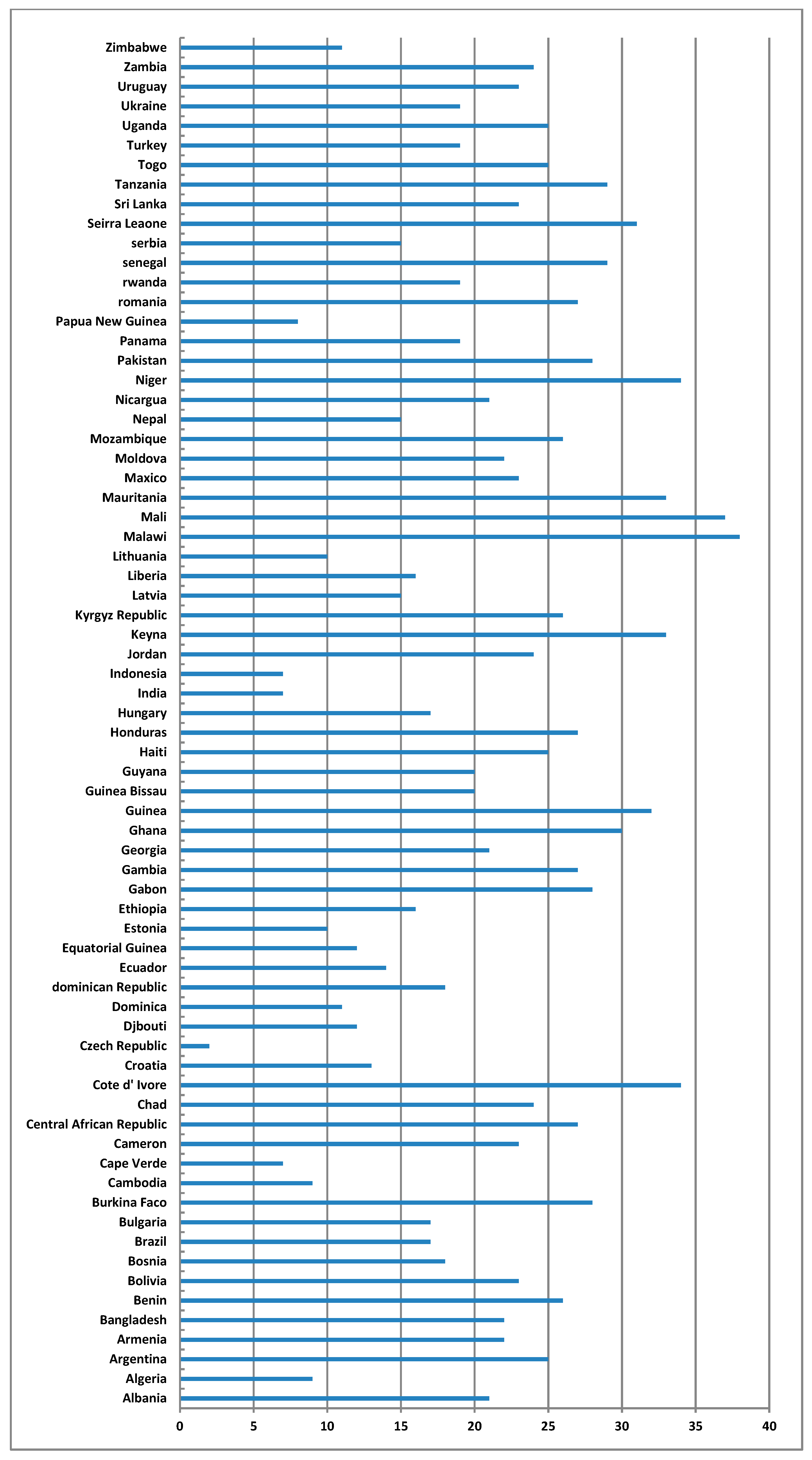

Figure A5 demonstrates number of years each country in the sample remains under IMF support program within estimated period.

Based on the distribution of hazard graph, we implement Weibull Distribution parametric model. For the Weibull model, hazard function is represented as follows:

where:

The survival function for the Weibull model is given as:

The density function is as follows:

It is easy to construct the likelihood for the Weibull model after getting hazard, survival and density function.

Our variables for the analysis of duration under the IMF program are GDP growth (% annual), broad money (% of GDP), debt service (% of exports of goods, services and income), country status (low-, lower middle-, upper middle-income countries), real exchange rate (REER), autocracy index, effective federal funds rate, current account (% of GDP) and remittances (% of GDP). All variables are continuous except for country status. Country status is a categorical variable. It is divided into three categories, i.e., low-income, lower middle-income and upper middle/high-income countries. All variables are obtained from World Development Indicator (WDI) except for effective federal funds rate and country status. Effective federal funds rate is retrieved from IMF and country status data are obtained from World Bank. We investigate the determinants for multiple times of participation in an IMF support program during the sample time period, from 1980 to 2018, generally irrespective of specific fund program.

We further extend our analysis in order to find the effectiveness of the IMF program. In the spirit of

Bird and Rowlands (

2017) who suggest that the conditions under which middle- and low-income countries select the IMF program vary, we therefore divide our countries into two groups: countries which face transition from lower middle to upper middle/high-income countries until 2018, consisting of a panel of 26 countries, and the countries which do not show transition and remain low/lower middle-income, consisting of a panel of 44 countries. In this way, we tried to separate low/lower middle-income and upper middle-income/high-income countries. We follow World Bank’s classification of countries. World Bank used GNI per capita to divide countries based on their income level by Atlas methodology. The complete list of countries along with their status of income in 2018 is included in

Table A4.

Our analysis is based on augmented Solow growth model (1956). By employing GDP per capita, as a dependent variable, we used labor force and capital accumulation as our independent variables. Mortality rate is used as a proxy for labor force in the case of low-income countries and population growth is used as a proxy for labor force in the case of high-income countries. Investment (% of GDP) is employed as proxy for capital accumulation in both cases. In addition to this, we also use IMF loan (% of GDP) as our endogenous independent variable.

Fidrmuc and Kostagianni (

2015) pointed out that methods implemented so far, in order to determine the effectiveness of the IMF program, represent an issue of endogeneity. Countries choose the IMF program when they are already experiencing economic instability or are about to face it in the foreseeable future. They suspect that there might be reverse causality between economic growth and the IMF loan. Moreover, there are variables which are not included in our model but they can affect economic growth, i.e., trade deficit, inflation and debt service ratio. Being part of the error term, these variables might be strongly correlated with the IMF loan package. This indicates that there might be an issue of endogeneity in our model.

To overcome the issue of endogeneity, we introduce suitable tools. An instrument must be independent from the error term but strongly correlated with the endogenous variable. We ensure that the included instrument is not correlated with the economic hardships that a country is experiencing at the time of participating in the IMF program. However, a self-selection based on economic conditions may cause bias in our results that we want to eliminate. In order to find whether the instrument is identified or not, we execute the Anderson Canon statistic. A significant value of less than 5% suggests that the equation is completely identified. In the case of low-income countries, we choose “polity index” (see the official website:

https://www.systemicpeace.org/polityproject.html assessed on 10 January 2021) as instrument for IMF loan (% of GDP). Polity index is divided into three categories. A value of −10 to −6 represents autocracies, a value of −5 to 5 represents anocracies and a value of 6 to 10 is regarded as democracies. For upper middle-income countries, we introduced the concepts of: “accountability” and “rule of law” as instruments for IMF loan (% of GDP). Accountability and rule of law are retrieved from World Governance Indicators (WGI). Since, we have introduced instruments in our analysis, a two-stage panel fixed effect model would be most suitable for our analysis.

Visible effects of loan allocated to a country may appear in the same year or subsequent year. In some cases, the main effects of a loan cannot be visible in one year because a loan is disbursed late in a year. Due to the austerity measures which were implemented, the outcome of the IMF program might be negative in the initial years and become visible in the upcoming years. Therefore, a possible shape of the outcome of the IMF program may be J shaped. To explore impact of the IMF program in subsequent years, we will also introduce lags of IMF credit (% of GDP) in our model up to three years maximum.

4. Empirical Results

Table A1 represents the regression results obtained by estimating seven equations under panel survival analysis. The first equation represent the baseline equations. they includes two variables, i.e., debt service and money supply (% of GDP). Money supply is negatively associated with years under IMF program. Money growth can be an indicator of inflation. In contradiction with

Goldstein and Montiel (

2017), our analysis indicates that higher money supply, as a percentage of GDP, reduces the hazard rate by 8% approximately. We can support our findings in terms of the monetarist view. Monetarists (the monetarist doctrine promoted starting in the year 1967) were of the view that government can foster economic growth by targeting the money supply. They suggest that an increased money supply in the economy stimulates aggregate demand for goods and services thereby encourages job creation. Unemployment will gradually decrease over time and economic growth will be achieved. Debt service is positively associated with the duration under IMF program. One percent increase in debt service ratio results in 3.3% increase in risk rate.

Knight and Santaella (

1997) suggest that high debt service ratio reduces the fiscal space of the government.

Two additional variables are included in the second equation, i.e., GDP and country status. Both variables are significant. In line with the empirical findings of

Orăștean et al. (

2016), our empirical analysis also demonstrates that GDP is negatively related to the stay under IMF program and a 1% increase in GDP reduces the risk of remaining under the IMF program by 3.6%. For variable country status, we have introduced the low-income category as the base category. It clearly demonstrates that demand for the IMF program is relatively less for lower middle- and upper middle-income countries as compared to low-income countries. Past experiences have revealed that low-income countries are at greater risk of experiencing current account deficit and are more prone to structural and macroeconomic imbalances. During the financial crisis of 2008, many low-income countries turn to IMF support program to tackle current account deficit (

Conway 2010).

Going further, real exchange rate is positively related to years under IMF program. A 1% increase in real exchange rate increases the chance to reach IMF program by 0.1%. An increase in real exchange rate will make imported goods cheaper as compared to domestic goods. On the other hand, exports will become more expensive with the rise in real exchange rate. As a result, net exports will reduce which can cause a widening of the current account deficit and can force a country to reach out to the IMF. In order to check if dictatorship is significantly associated with demand for IMF program, we introduce autocracy index. Our analysis demonstrates that autocracy is positively linked with demand for IMF program.

Olson (

1993) suggests that increased tenure of dictatorship is increasingly associated with economic downfall and implementation of less successful and repressive policies. These policies may eventually lead to economic disaster. We introduce the federal funds rate variable to investigate the impact of global conditions on demand for IMF program. We find federal funds rate is positively related with years under the IMF program. An increase in federal funds rate by 1% will increase the risk of requiring a funding program by 4.1%. An increased US interest rate can affect the world through two channels. A higher US interest rate leads to capital outflow from other countries, which can negatively impact their economic growth. On the other hand, if a country is holding dollar-denominated debt, a rise in US interest rate may lead to deterioration of the domestic balance sheet (

Iacoviello and Navarro 2019).

Remittance (% of GDP) is negatively related to the request for IMF support program. Large and steady inflow of remittances improves the international reserves holdings of a country.

Bugamelli and Paternò (

2009) suggest that worker’s remittances can help in overcoming current account deficit. This estimation is in line with

Orăștean et al. (

2016). Equation (7) involves current account balance (% of GDP). Our estimation results demonstrate that current account deficit is negatively related to the demand for IMF program. A number of empirical studies support this finding (see

Iseringhausen et al. 2019;

Orăștean et al. 2016). One percent increase in current account decreases the hazard rate by 4.2%.

Turning towards the effectiveness of the IMF program,

Table A2 reports the results of a panel instrumental fixed effect model for low-income countries, with the introduction of IMF lag up to 3 years. Since IMF loan (% of GDP) is an endogenous variable, we have introduced an instrument “polity index” for IMF loan. Democracy is completely identified and is positively related to IMF loan (% of GDP). This demonstrates that democracies have a greater chance to receive the IMF funding program as compared to non-democracies. The two exogenous variables, i.e., infant mortality and investment (% of GDP), seem uncorrelated with IMF loan (% of GDP) (see first-stage analysis of

Table A2). Second-stage analysis suggests that the contemporaneous effect of IMF support program on economic growth is insignificant. The impact remains insignificant during the second year after participation in the IMF program. However, the magnitude of the impact of the IMF program becomes significant and positive as we introduce more lags. With the introduction of second and third lag, the impact of the IMF program becomes positive on economic growth of low-income countries. Average growth improves by 5.15% for the last two years of our estimation analysis. The other two independent variables, i.e., investment and infant mortality, executed in second-stage analysis of

Table A2, remain significant at 1% in each of the four equations. Investment is positively related with the economic growth and infant mortality is negatively associated with economic growth.

Table A3 presents the results of a panel instrumental fixed effect model for upper middle-income countries. In order to find the impact of the IMF fund program on the economic growth of a participating country, we introduced lags of IMF from one to three years. To tackle the endogeneity of IMF loan program, we introduced two instruments, i.e., accountability and rule of law. The first analysis of

Table A3 shows that both the instruments are negatively related to the IMF loan program. This indicates that a county that adheres strictly to the principles of supremacy of law, equality before the law and accountability towards the law, is less likely to opt for the IMF loan program. The insignificant relation of exogenous variables with IMF loan program shows absence of correlation (see first-stage analysis of

Table A3). The first-stage F-statistics have always been greater than 10, indicating that a variation in IMF loan (% of GDP) has been well explained by our instruments. Equation (1) of second-stage analysis demonstrates that the contemporaneous impact of IMF program is clearly visible from the very first year of participation in the IMF program. The magnitude of its impact remains significant and positive for the next three years after participating in the IMF program. The insignificant value of Sargan test for all the four equations suggests that our instruments are valid. The second-stage analysis involved the addition of two independent variables, i.e., investment and population growth. Investment is significant at 1% and is positively related with economic growth whilst population growth remains an insignificant determinant in all four equations.

Figure A1 represents in a graphic manner the countries under IMF Program, while

Figure A2 examines the Smooth Hazard Estimate. Moreover,

Figure A3 reflects the Smooth Hazard Estimate by income level, while

Figure A4 reveals Nelson–Aalen Cumulative Hazard Estimate (see

Appendix A section).

Figure A5 provides a representative framework on multiple instances of participation in IMF program.

5. Conclusions

The IMF is an international financial assistance organization, to help countries experiencing economic instability. It provides temporary support for member countries, addresses their balance of payment issues and provides policy advice to protect the country from the measures that are harmful for economic stability. This paper attempts to investigate major determinants that induce a country to seek and stay under the IMF program. An understanding of factors behind multiple persistent stay under an IMF-supported program is required from a policy point of view. We implement survival analysis to explore these factors. Our analysis demonstrates that weak economic conditions, i.e., low economic growth, current account deficit, high debt service ratio and high real exchange rate, are major reasons that cause a country to deal with the IMF. The limitations of this study are that: (i) it observed 70 countries during a time span of 1980–2018. The successive studies can widen the scope of their study by considering a panel of more than 70 countries and observing them for a much longer duration. (ii) The survival analysis can also be executed on countries separately, based on their income level, to get a better understanding of the severity of determinants for a country, belonging to a specific category (low income, lower middle income and upper middle income), that force it to opt for the IMF program.

In the past, many countries have repeatedly chosen the IMF program. In most cases, a participant country implements a successor program shortly after the end of the initial program. Many empirical studies claim that the IMF program has negative or no impact on economic growth of the participant country. In this study, we also investigate the impact of IMF program on economic growth, since most of the countries in our sample show transition based on their income level. We therefore determine the effectiveness of the IMF fund program by dividing our sample countries into two groups, i.e., the countries that show transition and become upper middle/high income until 2018 and the countries which do not show much transition and remain at low/lower middle-income level. By employing, a 2SLS panel instrumental fixed effect model, our results demonstrate a positive picture of the IMF program. We conclude that the IMF fund program positively affects upper middle-income countries from the very first year of participating in it and remain positive and significant for all of the subsequent three years. For low-income countries, IMF impact remains insignificant during first two years of participation in it. However, IMF impact become positive and significant during the third year.

This study can help the leadership of a country to develop a better understanding of major economic factors that can force their country to reach out to the IMF fund program. They can get the idea of what needs to be done to avoid the IMF fund program, i.e., sound macroeconomic policies, economic growth, sustainable current account, stable currency value and low budget deficit. Sound macroeconomic policies are required that can help a country to withstand domestic and external crisis without causing instability in the country and distortion in current account balance. Our second analysis on the effectiveness of the IMF program, demonstrates a positive approach of the IMF fund program to economic stability and soundness. It contradicts all those studies which claim that IMF programs bring unnecessary damage to economic growth and harm to the poor, and probably can help the leadership of a country to restore their confidence in IMF policy advice. So, when a country experiences persistent current account deficit and economic challenges, it can turn to the IMF program, believing that the program will be able to cope with its balance-of-payments needs, and policy measures associated with it can better address the changing needs of a participant country.

and

and

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}