Sustaining Economic Growth in Sub-Saharan Africa: Do FDI Inflows and External Debt Count?

1

Department of Economic, Federal University Lokoja, Lokoja 1154, Nigeria

2

Nord University Business School (HHN), Post Box 1490, 8049 Bodø, Norway

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2021, 14(4), 146; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14040146

Submission received: 3 March 2021

/

Revised: 20 March 2021

/

Accepted: 24 March 2021

/

Published: 29 March 2021

(This article belongs to the Special Issue Foreign Direct Investment – Under the Sign of Profit or Sustainable Development?)

Abstract

:The quest for the attainment of economic development is sought after by all global economies, which by effect is expected to transcend to improving livelihoods and standard of living. However, several factors hinder the process of achieving sustained economic development, especially in developing countries. In this regard, assessing the extent of economic expansion orchestrated by foreign direct investment (FDI) inflows in vulnerable economies such as Sub-Saharan Africa (SSA), particularly in the face of the significant fall in global FDI inflow, is worthwhile. In essence, this study ascertains the impact of FDI inflows and external debt on economic growth amidst decline in FDI inflows and excessive foreign borrowings. The mixed order of integration from the stationarity test underpins the adoption of autoregressive distributed lag (ARDL) approach for data covering the period 1990 to 2018. The empirical results found FDI inflows play a crucial role in achieving economic expansion in the region. On average, FDI inflows, external debt, and foreign aids are more useful in expanding the economy compared to trade openness and exchange rate. Thus, this study recommends the need for SSA to open its economic borders for external capital, viz. FDI. A peaceful economic and political environment is a pre-condition to attract and maintain potential foreign investors. Stability in exchange rates is critical in achieving growth in FDI and other foreign resources. However, caution is required, especially in administration of external resources. Particularly, contracting external debt must strictly be driven by economic reasons rather than political motivation. Borrowed funds could be injected mainly into productive streams with the highest investment returns to boost economic development.

JEL Code:

F15; F43; F3; 0141. Introduction

It is on record that the 2015 global economic recession heavily affected vulnerable economies including Sub-Saharan Africa, as many foreign investors withdrew their investment from the region. This action was presumed to be in connection with the fall in investment profit and global oil shock particularly for oil-producing economies like Nigeria, Angola, Gabon, and Egypt (UNCTAD 2018). However, despite the continuous fall in global FDI inflows, the region recorded a positive increase in 2018 where FDI inflow to the region increased by 6%. According to United Nations Conference on Trade and Development (UNCTAD 2018), FDI inflows in 2017 stood at $US38 billion, increasing to $US40 billion in 2018, spreading disproportionately across the region. The natural resources dominated economies, such as Nigeria and Angola, suffered more serious setbacks in FDI inflows than diversified economies including Egypt and South Africa, which witnessed stable increase in FDI inflows. For instance, UNCTAD (2018), further reveals that the Northern sub-region registered growth in FDI inflows from $US13.4 billion in 2017 to $US13.9 billion in 2018. Egypt, the biggest economy in the Northern region received the largest share of FDI flows increasing by 7% in 2018, viz. $US7.9 billion compared to $US7.4 billion recorded in 2017. The growth in FDI to the continent could be attributed to the oil and gas sector of the economy, food processing, investment in real estate, and renewable energy technologies. Similarly, the Southern sub-region registered a drastic increase in FDI inflow from $US1 billion in 2017 to $US4.5 billion in 2018. South Africa, the hub of FDI inflows in the Southern region, suffered a sharp fall in FDI inflows from 2014, recording a significant recovery amounting to $US7.1 billion in 2018 relative to $US1.3 billion achieved in 2017. This huge achievement was driven by investments in mining, renewable energy, information and communications technology (ICT), and petroleum refining. Apart from the Northern and the Southern sub-region, the rest of the sub-region experienced sharp fall in FDI inflow in 2018 compared to the previous year. West Africa recorded a 20% drop in FDI inflows, followed by East Africa (14%), and Central (6%), respectively. In West Africa, Nigeria witnessed a fall in FDI inflow by 36% ($US2.2 billion), losing its leading position to Ghana, which registered the highest achievement in the sub-region amounting to $US3.3 billion. Ethiopia tops FDI flows in East Africa irrespective of the fall recorded in the economy. The economy achieved the equivalent of $US3.1 billion FDI inflows, indicating a fall of 24% compared to the previous year. Angola, the biggest recipient in Central Africa, recorded only $US5.1 billion relative to the previous year.

However, the reciprocal impact of FDI shocks on economic growth remains contentious although theoretically proven. The modernization theory developed by Max Weber (1864–1920) and popularized by Talcott Parsons (1902–1979) asserts that FDI inflows into recipient countries drive economic growth. The theory maintains that FDI inflows can facilitate economic structural change in the host economy. This theory is reputed by the dependency theory, which posits that FDI inflows serve as a medium of exploiting developing economies by their developed counterpart. The Harrod–Domar model is one of the early models that described economic growth as a function of saving and productivity of capital. Although the model is mostly applicable to the experience of developed nations, it described the rate of income growth necessary to keep consistent and smooth economic development (Olajide 2004). The model emphasizes investment, which includes FDI inflows. Similarly, the Solow growth model, a modification of Harrod–Domar’s version, is a simple growth model showing how savings, population growth, and technical progress affect the level of gross national product (GNP) and growth over time. Empirically, Kalai and Zghidi (2019) found that FDI has a complementary influence on home investment which by extension induces economic expansion in the Middle East and North Africa economies. This claim is consistent with existing studies including Pradhan et al. (2019) and Sarkodie and Strezov (2019). Contrary to this view, Goh et al. (2017) and Khobai et al. (2018) state that FDI inflow is exploitative and could be regarded as a non-catalyst to economic development. Goh et al. (2017) and Khobai et al. (2018) concluded that the perceived impact of FDI inflow is more of a fallacy rather than a reality. However, the recent unexpected fluctuation in FDI and the extent to which it impacts sub-Saharan Africa (SSA) countries require empirical investigation. This prompts the research question, viz. do FDI inflows impact economic development in SSA countries? This question is examined to ascertain the role of long-term FDI inflows on economic growth in the region. Secondly, it is imperative to know that the impact of external debt on economic growth is still arguable in the existing literature. For instance, Joshua et al. (2020a) examined the impact of external debt on economic growth across global income clusters and found a positive impact of external debt on economic growth across countries. Joshua et al. (2020a) supported the presumed positive impact of external debt on the South African economy. However, several studies contend with the positive impact of external debt on economic development, rejecting the outlined hypothesis (See Moh’d AL-Tamimi and Mohammad 2019; Umaru et al. 2013). Nonetheless, the global economic recession affecting emerging economies has forced most SSA economies to seek alternate financial resources by borrowing from overseas to meet their national budget expenditure. Many of these nations, including Nigeria, keep borrowing excessively, particularly from China to finance government budgets to boost economic growth. Unfortunately, some of these economies failed to pay back their debt, leading to threats of losing their sovereignty to creditors. The salient question that demands an empirical response is, how impactful are these resources on economies in the region? This also calls for empirical examination.

2. Literature Review

Scholars are yet to agree on the FDI-induced growth hypothesis. Although several studies support the outlined hypothesis, yet some remain contentious about its reality. For instance, Joshua et al. (2020a) examined the influence of external factors on economic expansion in South Africa and confirmed that FDI inflows promote economic expansion. The study recommends the need for authorities to adopt policies that promote business environment (both political and economic) through stable exchange rates and other macroeconomic variables to boost the confidence of existing foreign firms and to woo new ones. In contrast, Joshua et al. (2020b), through the causality method found FDI does not drive economic growth in Nigeria. Tsaurai (2018) found that FDI promotes stock market improvement through its influence on human capital, which induces economic expansion. A closely related study for OECD indicates FDI inflows to both ITC-base and non-ICT base do not induce economic progress (Gönel and Aksoy 2016). The finding further showed FDI influence on ICT-base could be felt only if the economy has achieved the minimum threshold of its absorptive capacity.

Additionally, Joshua (2019) and Gungor and Katircioglu (2010) investigated the FDI-led growth nexus and validated the existence of the FDI-led growth hypothesis in Nigeria and Turkey. In a related study, Gungor and Ringim (2017) found the inducing influence of FDI in Nigeria and concluded that FDI is potent for economic transformation. Kalai and Zghidi (2019) studied the relationship between FDI, trade, and economic advancement in the Middle East and North Africa (MENA) region and revealed that FDI inflows significantly promote economic advancement. Similarly, Sokhanvar (2019) examined the nexus between FDI, tourism, and economic advancement in European countries. The result validated the efficacy of FDI inflows as subscribed by Omri and Kahouli (2014). A study on financial development, export, FDI inflow, and economic growth in Pakistan (Shahbaz and Rahman 2012) agreed with previous studies where FDI inflows improve economic expansion, similar to Almfraji and Almsafir (2014). Similarly, Sarkodie and Strezov (2019) found that FDI positively drives economic growth in transition economies. Pradhan et al. (2019) examined the interaction between FDI, stock market depth, economic growth, and openness in the Association of Southeast Asian Nations (ASEAN) economies and found that FDI positively drives economic expansion. Sunde (2017) found a similar outcome where FDI was found as agent of economic expansion, corroborating results presented in Gungor et al. (2014). Abdouli and Hammami (2017) examined the impact of FDI inflows on economic growth in MENA countries and confirmed that FDI is a determinant of economic expansion. Khobai et al. (2018) showed FDI inflows contribute negatively to the path of economic growth in South Africa. Pandya and Sisombat (2017) examined the nexus between FDI and economic advancement in Australia and revealed FDI plays a key role in promoting economic advancement. Similarly, Zandile and Phiri (2019) examined the FDI-led growth hypothesis and found a devastating effect of FDI inflows on economic expansion. A similar study for Asian economies by Goh et al. 2017 showed the influence of FDI inflows in the region is uncertain. Similarly, Joshua et al. (2020c) revealed that external debt is a key determinant of global economic growth. Joshua et al. (2020c) indicated that external debt exhibits a positive and significant impact on economic growth. In contrast, the existing literature found a negative impact of external debt on economic growth (See Moh’d AL-Tamimi and Mohammad 2019; Umaru et al. 2013).

3. Materials and Method

3.1. Data Source

In the literature, several studies have assessed the interaction between economic expansion and FDI (Joshua 2019; Joshua et al. 2020c). In line with the Sustainable Development Goals, we utilize six data series from the World Bank (World Bank 2020) from 1990 to 2018 for the Sub-Saharan countries. Data include Economic growth (RGDP, measured in constant 2010 US$) and FDI (measured in BoP, current US$) as the key variables of the model, which was augmented by Long-term External debt stocks (DBT, measured in DOD, current US$), Official exchange rate (EXR, measured in LCU per US$, period average), Net official development assistance received (ODA, measured in constant 2015 US$), and Trade Openness (TRO, measured in % of GDP).

3.2. Model Specification

We adopted a logarithmic transformation of all variables to ensure that the variance remains constant across all the series where LRGDP, LFDI, LTRO, LDBT, LODA, and LEXR represent the logarithmic transformation of all variables and and βs represent the stochastic, intercept, and partial slope coefficients, respectively. The linear representation of the proposed model can be expressed as:

Going further, the study reinvestigates the neoclassical growth model adjusted to include external growth factors. For brevity, the generic panel estimation model can be presented as:

where is the error term and β’s denotes the estimated parameters across countries in time .

The model specification of the fixed (FE) and random (RE) effects can be expressed as:

where denotes unobserved country-specific fixed-effects that capture time-constant country-specific heterogeneity, , , , , and are the contemporaneous regressors, and represents the idiosyncratic error varying across countries over time . For the RE model in Equation (4), denotes the intercept, and represent between and within uncorrelated entity errors that allow time-invariant variables as regressors. The panel is subdivided into four sub-regions: West Africa, South Africa, Central Africa, and East Africa, to enable comparison across the sub-regions. (2) To effectively establish the significance of FDI inflow on economic growth, the study utilizes both static and dynamic models. The static models include the pooled ordinary least squares (POLS) which do not account for heterogeneities across countries, whereas the fixed-effects (FE) model allows for panel heterogeneities. On the other hand, the dynamic model used is the System Generalized Method of Moments (sys-GMM).

4. Results and Discussion

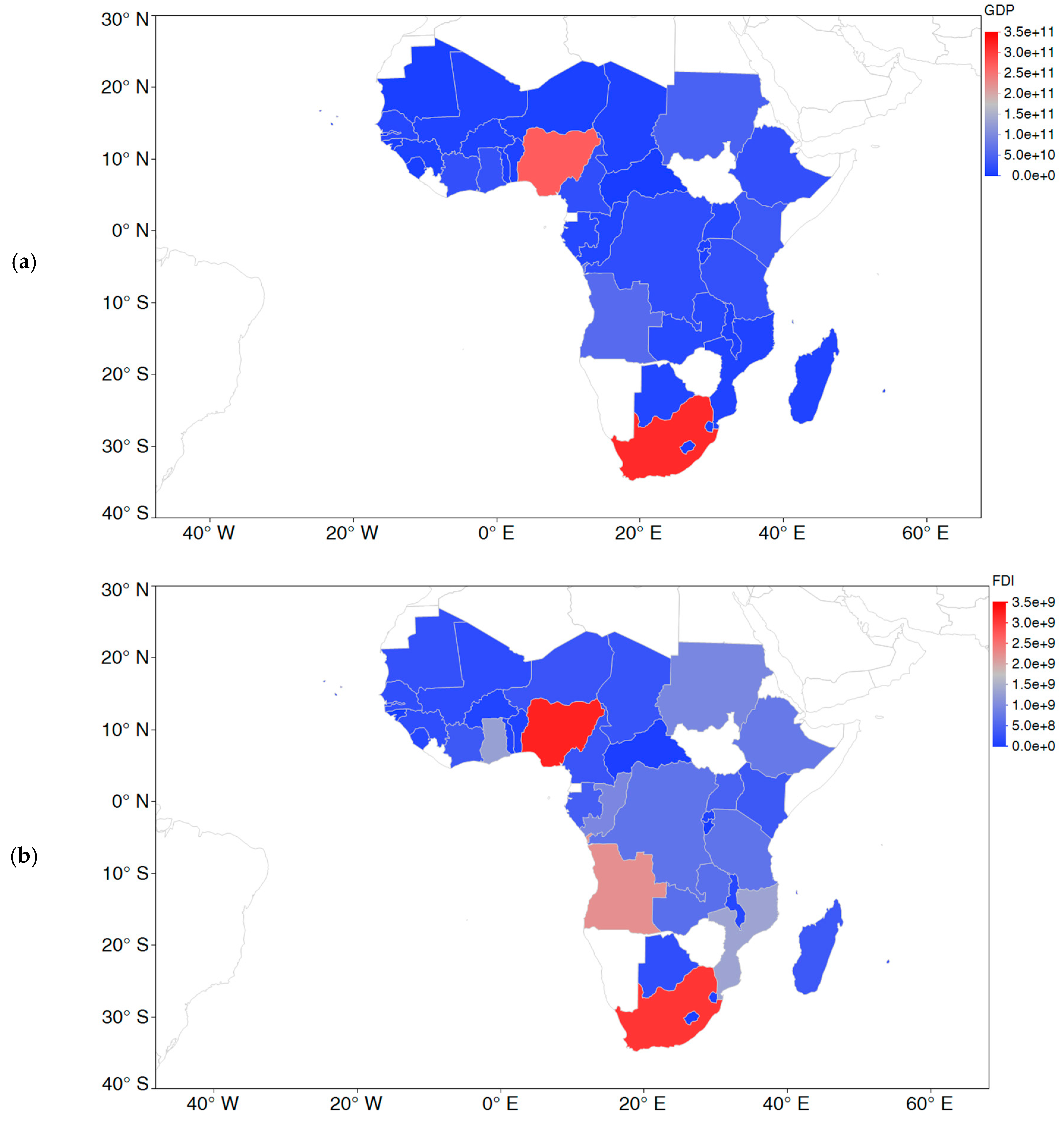

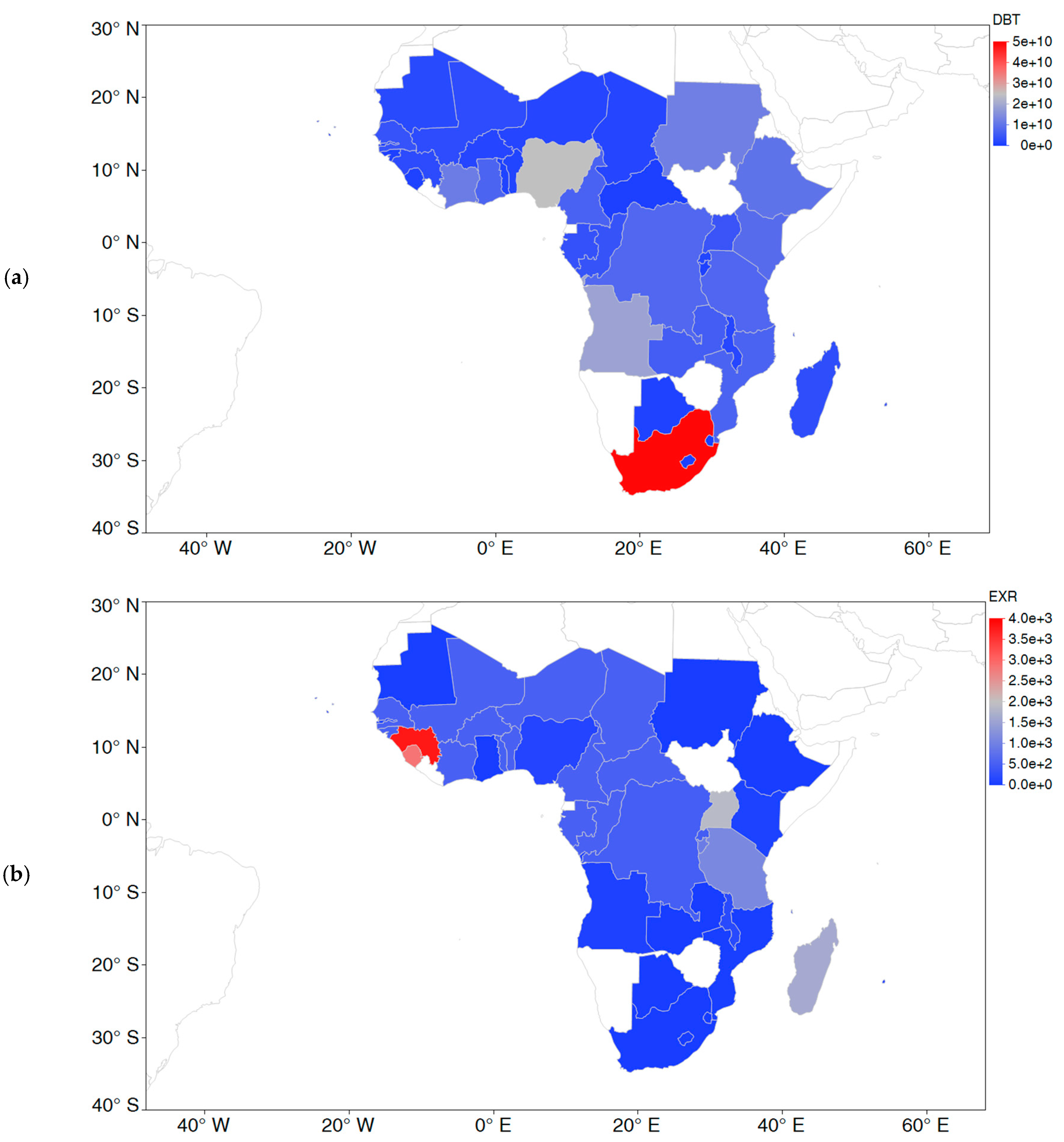

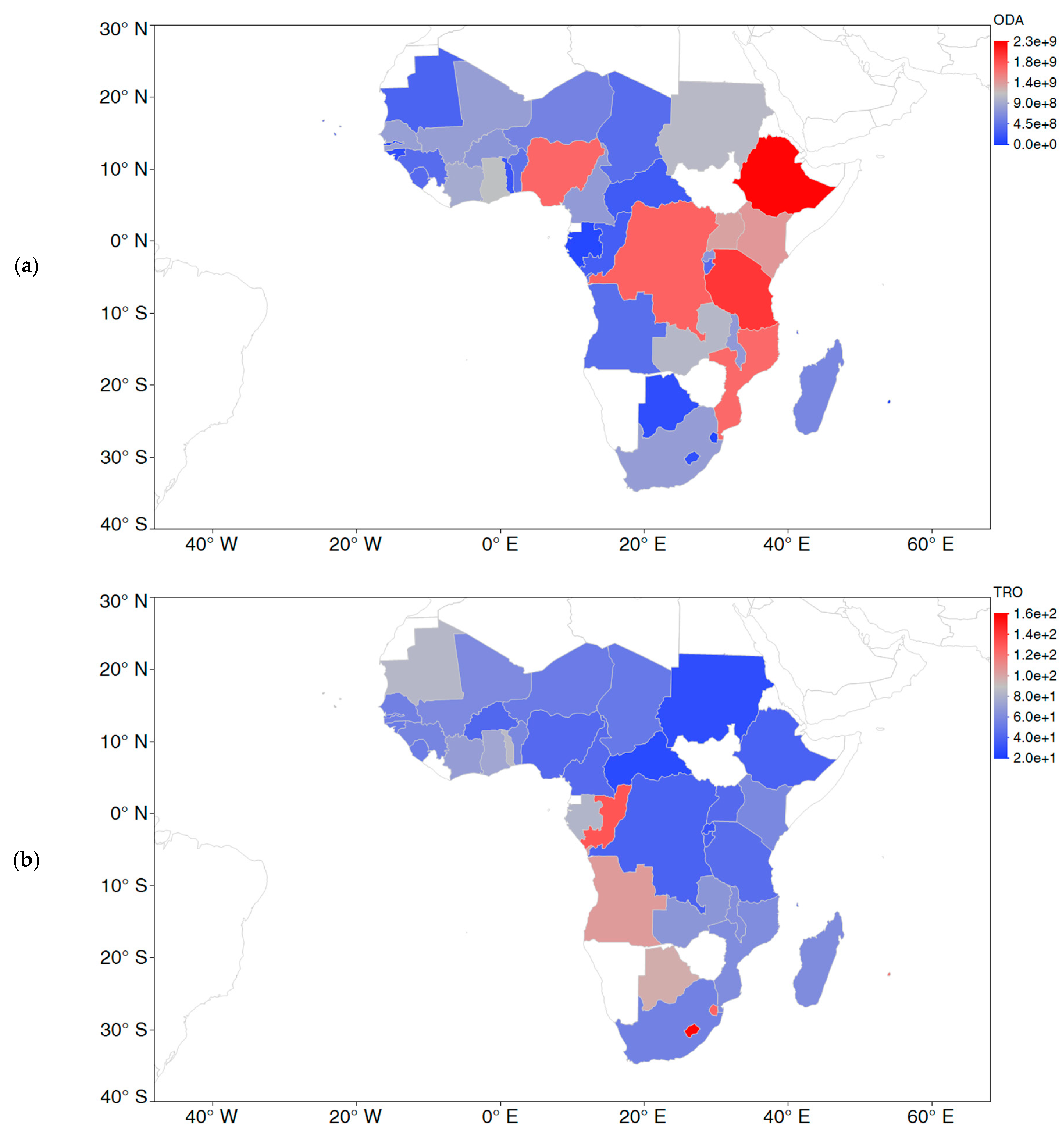

We examined the geographical distribution of the data series across Sub-Saharan Africa presented in Figure 1, Figure 2 and Figure 3. It can be observed that South Africa has the highest average economic growth of about US$0.32 trillion (constant 2010), followed closely by Nigeria of about US$0.27 trillion (constant 2010). Nigeria receives the highest average FDI of almost US$3.24 billion, followed by South Africa and Angola with about US$3.06 billion and US$2.23 billion, respectively. Again, South Africa has the highest average long-term external debt stocks of about US$49.49 billion. Guinea has the highest 29-year average exchange rate of about 3796.4 local currency unit per US$, followed by Sierra Leone of about 2854.16 local currency unit per US$. Ghana ranks as the best country in Sub-Saharan Africa based on the 29-year average exchange rate of about 1.26 local currency unit per US$. Ethiopia ranks first in terms of the average net official development assistance received, of almost US$2.31 billion. This is followed closely by Tanzania, Congo (Kinshasa), Nigeria, and Mozambique, of almost US$1.97 billion, US$1.71 billion, US$1.69 billion, and US$1.67 billion, respectively. Lesotho has the highest average contribution of trade openness to economic growth of about 161.24%, followed by Congo and Eswatini of about 131.09% and 126.20%, respectively.

The least-square dummy variable (LSDV) estimates presented in Table 1 show that FDI exhibits a positive and significant impact across all regions, signifying that an increase in physical investments in SSA is important to growth in the region. The impact is intensive in Southern Africa where a unit change in FDI leads to 33% rise in economic growth, 15% in West Africa, 3.5% in Central Africa, and 6.9% in East Africa. This implies that the increase in FDI creates an opportunity for growth in national output for the host country, as additional economic resources are committed. The presence of foreign firms in host countries encourages healthy competition whereby local firms can manage their resources more efficiently and improve their productivity in the process, as supported by Joshua (2019).

The coefficient of LDBT is positive and significant across the four regions. This means that external debt is an important contributor to economic growth across the sub-regions. This signifies the importance of debt in boosting economic growth in Sub-Saharan Africa, confirmed by Jayaraman and Lau (2009) in six Pacific Island countries. The results show the impact of debt is greater in Central, Western, and Eastern Africa with 5% level of significance than Southern Africa with 10%. Specifically, a unit change in LDBT leads to ~73%, 81%, 68%, and 57% increase in GDP per capita in Central, Western, Eastern, and Southern Africa, respectively.

Change in exchange rate leads to a negative and significant influence on growth in all four regions, except for Central Africa where it has a significantly positive impact. The behavior of the exchange rate can be linked to the stability of the Francs, which is tied to the stable French economy and is used widely by all countries in Central Africa. A rise in the exchange rate of various currencies used in the other regions limits growth. This outcome can be attributed to the heavily dependent import of goods and services by Sub-Saharan economies, which are more expensive when indigenous currencies depreciate against global currencies like the US dollar and the Euro. This situation exposes the disadvantage faced by African economies due to unstable currencies that are prone to global economic shocks and hurt economic growth across the sub-continent (Vieira et al. 2013).

Official Development Assistance (ODA) has a positive and significant coefficient for the sub-regions of Africa. This entails that ODA induces growth in Sub-Saharan Africa, indicating that a unit change in ODA will boost growth by 30%, 27%, 14%, and 12% in Western Africa, Southern Africa, Central Africa, and Eastern Africa, respectively. This revelation is in line with Burhop (2005) for 45 developing countries. However, the Central African region was significant at 10% level.

Trade openness has a negative and significant coefficient at 10% and 5% level for Western and Eastern Africa. Central Africa recorded a positive and significant impact at 10% level. There was no evidence of significance for the Southern region of Africa. It is evident that openness slows growth in both Western and Eastern Africa regions because a unit change in openness leads to 51% and 8.4% shrink in growth, respectively. On the other hand, the coefficient for openness has a positive impact on growth among other variables in Central Africa. Implying that a unit rise in openness leads to an increase in growth by 70% in line with Chang et al. (2009).

The results in Table 2 are based on the inclusion of heterogeneities of the variables via the Fixed-Effects and Random Effect Estimators. Results from both the Fixed Effect (FE) and Random Effect (RE) show that FDI has a significantly positive effect on growth in all the regions at 5% significance level, except for RE in Southern Africa with 10% significance level. As earlier indicated, FDI leads to the transfer of technology and resultant productivity from foreign countries to host countries, thereby increasing the productive capacity of the host countries as justified by the positive coefficient of FDI for the regions in Sub-Saharan Africa as supported by Joshua et al. (2020c)

Consequently, the R-squared statistic is high and does suggest that the model contains variables that explain the changes in the dependent variable real per capita income.

Furthermore, the coefficients of debt are positive and significant on growth for all the sub-regions, both for the FE and RE estimates, except for Southern Africa where the positive effect was insignificant. This result affirms the importance of debt as a determinant of growth in Sub-Saharan Africa and explains the growing debt to GDP ratio in the region. This discovery is in line with Jayaraman and Lau (2009) for six countries in the Pacific Islands.

The exchange rate has effects on growth in all the regions using the FE. The positive effects outweigh the negative effect, which shows that exchange rate has a negative effect on growth only in the Eastern region of African, while other regions indicated positive relationships. Based on the RE estimate, results indicate that exchange rate has negative effects on growth both in Western and Eastern Africa, while in Central Africa, exchange rate has a significantly positive relationship with growth. There was no evidence of significant relationship between growth and exchange rate in the Southern African region. A positive coefficient in exchange rate in the Central Africa region means that a depreciation in the domestic currency will make domestic goods cheaper, thereby increasing exports, which will boost economic growth in the process.

Results from the FE estimates for LODA show two levels of relationships. One, positive and significant relationships exist for Western and Central Africa at 5% and 10% significance levels, respectively. Second, the impacts on Southern and Eastern regions are negative at 5% significance level. Consequently, RE estimate shows that LODA has a positive and significant impact on growth in Western, Central, and Eastern regions of Africa. RE results in Southern Africa show a negative and insignificant impact between LODA and growth. A rise in development assistance means that more funds are available for the execution of recurrent and capital expenditures, which can be used to grow economic activities in the regions.

The coefficients for trade openness are positive for all regions at 10%, except for Southern Africa with insignificant positive and negative impacts as shown by the FE and RE estimates, respectively. The mixed impact of trade openness across the regions could be due to differences in random economic characteristics captured in the RE estimator, such as differences in trade policies adopted by countries in the various regions.

The main results of the panel estimation using pooled OLS, Fixed, and Random Effects and GMM are presented in Table 3.

4.1. LFDI Estimates

Results from all estimates (Pooled OLS, Fixed Effects, Random Effects, and System GMM) indicate LFDI has positive and significant effects on growth, as shown in previous studies. This means the flow of investments into Sub-Saharan African countries contributes positively to economic growth. A unit change in FDI leads to about 15% growth in the region, which is a substantial influence on economic expansion. This outcome tallies with Athukorala (2003) for Sri Lanka.

4.2. LDBT Estimates

Estimates of Pooled OLS, Fixed Effects, and Random Effects (in Table 3) indicate that the coefficients of debt stock are positive and significant at 5% significance level in line with Jayaraman and Lau (2009) for six Pacific Island countries. This confirms that debt is a good source of economic growth for countries in Sub-Saharan Africa. However, the System GMM estimate shows a negative and significant effect of LDBT on growth at 1% level, indicating a very strong negative impact on economic growth. This finding is in line with Siddique et al. (2016) for 40 Highly Indebted Poor Countries. Similarly, high external debt stock entails that the burden of debt servicing could hurt economic activities. Large funds that should have been used to boost economic growth are used to fulfil debt servicing obligations. In meeting debt obligations, governments often adopt high taxation and lesser subsidies, which could transcend to reducing productivity by harming the small-scale industries that should have contributed immensely to increased economic output.

4.3. LEXR Estimates

Revelation from the Pooled OLS estimate indicates that exchange rate has a negative impact on growth, further confirming the prevalent evidence on the negative effect suffered by economic growth in times of exchange rate crisis. In the case of global exchange rate shocks, Sub-Saharan African countries experience a slowdown in economic growth. However, estimates of FE, RE, and System GMM show that exchange rate has a positive impact on economic growth, implying that currency depreciation and or appreciation in the Sub-Saharan countries does significantly affect economic growth.

4.4. LODA Estimates

Additionally, results for LODA from the four estimates were found to be all positive and significant on growth at 5% level for Pooled OLS, Fixed Effects, Random Effects, and 10% for System GMM. This result affirms the importance of development assistance in sustaining and boosting economic activities in Sub-Saharan Africa. Apart from providing funds for the development of economy and stimulating infrastructure, ODA also comes in the form of partnership that involves training of manpower in receiving countries that improve economic productivity. This finding is in line with Burhop (2005) for 45 developing countries and Burnside and Dollar (2000) for 56 developing countries.

4.5. LTRO Estimates

The results from the Pooled OLS estimate for trade openness indicate a negative and significant link with economic growth, which signifies that an increase in openness results in a slowdown in economic growth. Specifically, a unit change in openness shrinks growth by 11% in Sub-Saharan Africa. However, similar findings were found by Rigobon and Rodrik (2005) for 242 countries. For Sub-Saharan Africa, the negative relationship between openness and growth could be attributed to the several decades of liberal economic policies dating back to the policies of Structural Adjustment Program in the 1980s. The economic adjustments were accompanied by currency devaluations, which made the importation of intermediate goods difficult for indigenous firms leading to the closedown of several economic ventures across the continent. On the other hand, an increasing level of openness exposes Sub-Saharan African firms to compete with more technologically advantaged firms from developed countries, thereby losing out their share of the African market to foreign firms. Contrarily, trade openness has a positive impact on growth in Sub-Saharan Africa, as shown by the FE and RE and System GMM estimates. These results show that countries in Sub-Saharan Africa have the potential to benefit greatly from globalization.

5. Conclusions

This study investigated the FDI-led growth hypothesis in Sub-Saharan Africa amidst noticeable fluctuation in FDI inflows. The findings show that FDI inflow and external debt are important growth driving factors as confirmed by all estimation techniques (Pooled OLS, Fixed Effects, Random Effects, and System GMM) used in the study. This means that despite the significant fluctuation in FDI inflow, its influence on economic growth and that of external debt simultaneously remain positive and significant. This is in line with the a priori expectation and objective of the study, proving that despite the fall in FDI inflows and excessive external borrowing, the impact on economic growth is still positive for SSA. While exchange rates exhibit a negative and significant influence on growth with the Pooled OLS estimator, their impact is positive and significant when included in the FE, RE, and GMM models. Official development assistance is dominantly positive and significant in the study. Hence, this implies that foreign aid is an important contributor to economic advancement in the region. The influence of trade openness on growth in this study is mixed. While openness demonstrates a negative and significant influence on economic expansion in the POLS estimation, it appears to be positively significant when included in the other three estimation techniques.

This study has policy implications for consideration. First, we established the leading role of foreign FDI and external debt in driving growth in SSA. The case of debt has been a subject of debate in the region for a while, and emphasis has often been laid on the need for sustainable debt. Having established the importance of FDI inflow in boosting growth in SSA, this study recommends the adoption of policies that assist in stabilizing FDI inflow to ensure continuous growth through free license of operation, exchange rate stability, an improved business environment, strong/stable macroeconomic performance, and political stability guarantee. This will attract fresh foreign investors as well as boosting the confidence of existing ones, thereby boosting investment opportunities and, by extension, increasing growth in the region. Similarly, although debt is found to be of benefit to economic growth, the governments must take precautions to avoid unfavorable costs imposed by debt servicing, which instead of boosting the economy may hamper it. Secured external debt must strictly be utilized for long-term developmental and productive projects in the economies of the region, which will in turn boost economic growth.

On the other hand, the role of the exchange rate in this study is mixed with negative and positive significant impact. However, we must not ignore the fact that oil-dependent countries in the region like Nigeria and Angola are often exposed to exchange rate crises in times of global oil price meltdown. To mitigate this crisis, diversification from mining-based to manufacturing-based and from low tech to high-tech economies should be taken seriously. This will help SSA countries to achieve stable exchange rate and steady economic growth simultaneously. The Africa Continental Free Trade Area (AfCFTA) agreement which was unanimously endorsed by several African countries is commendable and if properly implemented will develop indigenous sectors like manufacturing, service, and technology. This will help protect the Sub-Saharan African economies from external shocks. The findings from this study will help the region strategize for the attraction of more foreign capital like FDI inflows and external loans. Although the positive impact of external debt is evident, recommendations from this study will guide SSA economies to borrow for economic reasons rather than for non-economic reasons.

Author Contributions

Conceptualization, U.J.; methodology, U.J.; software, U.J.; validation, U.J.; formal analysis, U.J.; data curation, U.J.; writing—original draft preparation, U.J., D.B., and S.A.S.; writing—review and editing, S.A.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Publicly available datasets were analyzed in this study. This data can be found here: https://data.worldbank.org/ (accessed on 2 January 2021).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abdouli, Mohamed, and Sami Hammami. 2017. The impact of FDI inflows and environmental quality on economic growth: An empirical study for the MENA countries. Journal of the Knowledge Economy 8: 254–78. [Google Scholar] [CrossRef] [Green Version]

- Almfraji, Mohammad Amin, and Mahmoud Khalid Almsafir. 2014. Foreign direct investment and economic growth literature review from 1994 to 2012. Procedia-Social and Behavioral Sciences 129: 206–13. [Google Scholar] [CrossRef] [Green Version]

- Athukorala, Wasantha. 2003. The impact of foreign direct investment for economic growth: A case study in Sri Lanka. Paper presented at 9th International Conference on Sri Lanka Studies, Matara, Sri Lanka, 28–30 November; vol. 92, pp. 1–21. [Google Scholar]

- Burhop, Carsten. 2005. Foreign assistance and economic development: A re-evaluation. Economics Letters 86: 57–61. [Google Scholar] [CrossRef]

- Burnside, Craig, and David Dollar. 2000. Aid, policies, and growth. American Economic Review 90: 847–68. [Google Scholar] [CrossRef] [Green Version]

- Chang, Roberto, Linda Kaltani, and Norman V. Loayza. 2009. Openness can be good for growth: The role of policy complementarities. Journal of Development Economics 90: 33–49. [Google Scholar] [CrossRef] [Green Version]

- Goh, Soo Khoon, Chung Yan Sam, and Robert McNown. 2017. Re-examining foreign direct investment, exports, and economic growth in asian economies using a bootstrap ARDL test for cointegration. Journal of Asian Economics 51: 12–22. [Google Scholar] [CrossRef]

- Gönel, Feride, and Tolga Aksoy. 2016. Revisiting FDI-led growth hypothesis: The role of sector characteristics. The Journal of International Trade & Economic Development 25: 1144–66. [Google Scholar]

- Gungor, Hasan, and Salih Turan Katircioglu. 2010. Financial development, FDI and real income growth in Turkey: An empirical investigation from the bounds tests and causality analysis. Actual Problems of Economics 11: 215–25. [Google Scholar]

- Gungor, Hasan, and Salim Hamza Ringim. 2017. Linkage between foreign direct investment, domestic investment and economic growth: Evidence from Nigeria. International Journal of Economics and Financial 7: 97. [Google Scholar]

- Gungor, Hasan, Salih Katircioglu, and Mehmet Mercan. 2014. Revisiting the nexus between financial development, FDI, and growth: New evidence from second generation econometric procedures in the Turkish context. Acta Oeconomica 64: 73–89. [Google Scholar] [CrossRef]

- Jayaraman, Tiruvalangadu K., and Evan Lau. 2009. Does external debt lead to economic growth in Pacific island countries. Journal of Policy Modeling 31: 272–88. [Google Scholar] [CrossRef]

- Joshua, Udi, Festus Fatai Adedoyin, and Samuel Asumadu Sarkodie. 2020a. Examining the external-factors-led growth hypothesis for the South African economy. Heliyon 6: e04009. [Google Scholar] [CrossRef]

- Joshua, Udi, Festus Victor Bekun, and Samuel Asumadu Sarkodie. 2020b. New insight into the causal linkage between economic expansion, FDI, coal consumption, pollutant emissions and urbanization in South Africa. Environmental Science and Pollution Research 27: 18013–24. [Google Scholar] [CrossRef] [Green Version]

- Joshua, Udi, Mathew Ekundayo Rotimi, and Samuel Asumadu Sarkodie. 2020c. Global FDI Inflow and Its Implication across Economic Income Groups. Journal of Risk and Financial Management 13: 291. [Google Scholar] [CrossRef]

- Joshua, Udi. 2019. An ARDL approach to the government expenditure and economic growth nexus in Nigeria. Academic Journal of Economic Studies 5: 152–60. [Google Scholar]

- Kalai, Maha, and Nahed Zghidi. 2019. Foreign direct investment, trade, and economic growth in MENA countries: Empirical analysis using ARDL bounds testing approach. Journal of the Knowledge Economy 10: 397–421. [Google Scholar] [CrossRef]

- Khobai, Hlalefang, Nicolene Hamman, Thando Mkhombo, Simba Mhaka, Nomahlubi Mavikela, and Andrew Phiri. 2018. The FDI-growth nexus in South Africa: A re-examination using quantile regression approach. Studia Universitatis Babes-Bolyai Oeconomica 63: 33–55. [Google Scholar] [CrossRef] [Green Version]

- Moh’d AL-Tamimi, Khaled Abdalla, and Sulieman Jaradat Mohammad. 2019. Impact of external debt on economic growth in Jordan for the period (2010–2017). International Journal of Economics and Finance 11: 114–18. [Google Scholar] [CrossRef] [Green Version]

- Olajide, O. T. 2004. Theories of Economic Development and Planning. Lagos: Punmark Nigeria Limited, vol. 6. [Google Scholar]

- Omri, Anis, and Bassem Kahouli. 2014. Causal relationships between energy consumption, foreign direct investment and economic growth: Fresh evidence from dynamic simultaneous-equations models. Energy Policy 67: 913–22. [Google Scholar] [CrossRef] [Green Version]

- Pandya, Viral, and Sommala Sisombat. 2017. Impacts of foreign direct investment on economic growth: Empirical evidence from Australian economy. International Journal of Economics and Finance 9: 121–31. [Google Scholar] [CrossRef]

- Pradhan, Rudra P., Mak B. Arvin, and John H. Hall. 2019. The nexus between economic growth, stock market depth, trade openness, and foreign direct investment: The case of ASEAN countries. The Singapore Economic Review 64: 461–93. [Google Scholar] [CrossRef]

- Rigobon, Roberto, and Dani Rodrik. 2005. Rule of law, democracy, openness, and income: Estimating the interrelationships. Economics of Transition 13: 533–64. [Google Scholar] [CrossRef]

- Sarkodie, Samuel Asumadu, and Vladimir Strezov. 2019. Effect of foreign direct investments, economic development and energy consumption on greenhouse gas emissions in developing countries. Science of the Total Environment 646: 862–71. [Google Scholar] [CrossRef] [PubMed]

- Shahbaz, Muhammad, and Mohammad Mafizur Rahman. 2012. The dynamic of financial development, imports, foreign direct investment and economic growth: Cointegration and causality analysis in Pakistan. Global Business Review 13: 201–19. [Google Scholar] [CrossRef] [Green Version]

- Siddique, Abu, E. A. Selvanathan, and Saroja Selvanathan. 2016. The impact of external debt on growth: Evidence from highly indebted poor countries. Journal of Policy Modeling 38: 874–94. [Google Scholar] [CrossRef]

- Sokhanvar, Amin. 2019. Does foreign direct investment accelerate tourism and economic growth within Europe? Tourism Management Perspectives 29: 86–96. [Google Scholar] [CrossRef]

- Sunde, Tafirenyika. 2017. Foreign direct investment, exports and economic growth: ADRL and causality analysis for South Africa. Research in International Business and Finance 41: 434–44. [Google Scholar] [CrossRef]

- Tsaurai, Kunofiwa. 2018. FDI led financial development hypothesis in emerging markets: The role of human capital development. International Journal of Education Economics and Development 9: 109–23. [Google Scholar] [CrossRef]

- Umaru, Aminu, Ahmad Hamidu, and Salihu Musa. 2013. External debt and domestic debt impact on the growth of the Nigerian economy. International Journal of Educational Research 1: 70–85. [Google Scholar]

- UNCTAD. 2018. FDI/MNE Database. Available online: https://unctad.org/webflyer/world-investment-report-2018 (accessed on 2 January 2020).

- Vieira, Falvio V., Marcio Holland, C. Gomes Da Silva, and Luiz C. Bottecchia. 2013. Growth and exchange rate volatility: A panel data analysis. Applied Economics 45: 3733–41. [Google Scholar] [CrossRef]

- World Bank. 2020. Available online: http://databank.worldbank.org (accessed on 2 January 2020).

- Zandile, Zezethu, and Andrew Phiri. 2019. FDI as a contributing factor to economic growth in Burkina Faso: How true is this? Global Economy Journal 19: 1950004. [Google Scholar] [CrossRef]

Figure 1.

Country-wise average distribution of (a) Economic growth (GDP, measured in constant 2010 US$), (b) Foreign direct investment net inflows (FDI, measured in BoP, current US$).

Figure 1.

Country-wise average distribution of (a) Economic growth (GDP, measured in constant 2010 US$), (b) Foreign direct investment net inflows (FDI, measured in BoP, current US$).

Figure 2.

Country-wise average distribution of (a) Long-term External debt stocks (DBT, measured in DOD, current US$), (b) Official exchange rate (EXR, measured in LCU per US$, period average).

Figure 2.

Country-wise average distribution of (a) Long-term External debt stocks (DBT, measured in DOD, current US$), (b) Official exchange rate (EXR, measured in LCU per US$, period average).

Figure 3.

Country-wise average distribution of (a) Net official development assistance received (ODA, measured in constant 2015 US$), (b) Trade Openness (TRO, measured in % of GDP).

Figure 3.

Country-wise average distribution of (a) Net official development assistance received (ODA, measured in constant 2015 US$), (b) Trade Openness (TRO, measured in % of GDP).

{kind=link}

{kind=link}

{kind=link}

Table 1.

Pooled ordinary least squares (OLS or LSDV) for comparative analysis across 4 sub-regions in SSA from 1990–2018.

Table 1.

Pooled ordinary least squares (OLS or LSDV) for comparative analysis across 4 sub-regions in SSA from 1990–2018.

| West Africa | Southern Africa | Central Africa | Eastern Africa | |

|---|---|---|---|---|

| Pooled OLS Results for Sub-Regions (Dep. Variable: RGDP, log) | ||||

| LFDI | 0.149 ** | 0.333 ** | 0.0352 ** | 0.0692 ** |

| (0.0215) | (0.0381) | (0.0233) | (0.0155) | |

| LDBT | 0.810 ** | 0.578 * | 0.680 ** | 0.725 ** |

| (0.0347) | (0.0520) | (0.0258) | (0.0350) | |

| LEXR | −0.0326 *** | −0.0695 ** | 0.00690 *** | −0.0239 *** |

| (0.00872) | (0.0275) | (0.00774) | (0.00623) | |

| LODA | 0.300 ** | −0.271 * | 0.144 ** | 0.121 ** |

| (0.0384) | (0.0663) | (0.0236) | (0.0268) | |

| LTRO | −0.510 * | −0.531 | 0.697 * | −0.0839 ** |

| (0.0715) | (0.226) | (0.0790) | (0.0426) | |

| Constant | −1.371 | 12.08 | 1.959 | 3.646 |

| (0.605) | (2.150) | (0.640) | (0.502) | |

| Observations | 435 | 227 | 171 | 285 |

| R-squared | 0.904 | 0.773 | 0.950 | 0.925 |

| Year Dummies | Yes | Yes | Yes | Yes |

Notes: Robust standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

Table 2.

Fixed and Random Effects Estimates for comparative analysis across 4 sub-regions in SSA (Dep. Variable: LRGDP, log) from 1990–2018.

Table 2.

Fixed and Random Effects Estimates for comparative analysis across 4 sub-regions in SSA (Dep. Variable: LRGDP, log) from 1990–2018.

| West Africa | Southern Africa | Central Africa | Eastern Africa | West Africa | Southern Africa | Central Africa | Eastern Africa | |

|---|---|---|---|---|---|---|---|---|

| Fixed Effects | Random Effects | |||||||

| LFDI | 0.0259 ** | 0.0210 ** | 0.0265 ** | 0.0293 ** | 0.0293 ** | 0.333 * | 0.0352 ** | 0.0358 ** |

| (0.0116) | (0.0163) | (0.0141) | (0.0108) | (0.0116) | (0.0729) | (0.0158) | (0.0118) | |

| LDBT | 0.154 ** | 0.0253 * | 0.307 ** | 0.137 * | 0.189 ** | 0.578 | 0.680 ** | 0.207 * |

| (0.0434) | (0.0676) | (0.0416) | (0.0511) | (0.0378) | (0.186) | (0.0281) | (0.0596) | |

| LEXR | 0.00922 ** | 0.0490 ** | 0.0128 *** | −0.0257 *** | −0.00345 ** | −0.0695 | 0.00690 *** | −0.0289 *** |

| (0.0311) | (0.0492) | (0.00330) | (0.00825) | (0.0204) | (0.104) | (0.00938) | (0.00571) | |

| LODA | 0.0888 ** | −0.0215 ** | 0.0540 * | −0.0254 ** | 0.109 ** | −0.271 | 0.144 ** | 0.0122 ** |

| (0.0276) | (0.0187) | (0.0562) | (0.0357) | (0.0299) | (0.212) | (0.0304) | (0.0471) | |

| LTRO | 0.0790 * | 0.202 | 0.234 * | 0.109 * | 0.0669 * | −0.531 | 0.697 * | 0.0937 * |

| (0.0695) | (0.105) | (0.0957) | (0.0580) | (0.0685) | (0.429) | (0.0510) | (0.0583) | |

| Constant | 16.18 | 20.84 | 13.74 | 19.31 | 15.08 | 12.08 | 1.959 | 16.96 |

| (1.256) | (1.450) | (1.932) | (1.412) | (1.192) | (4.015) | (1.301) | (2.108) | |

| Observations | 435 | 227 | 171 | 285 | 435 | 227 | 171 | 285 |

| R-squared | 0.923 | 0.930 | 0.899 | 0.896 | - | - | - | - |

| Number of country ID | 15 | 8 | 6 | 10 | 15 | 8 | 6 | 10 |

| Year Dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Notes: Robust standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

Table 3.

Results for Main Model Estimation across several techniques compared with System GMM from 1990–2018.

Table 3.

Results for Main Model Estimation across several techniques compared with System GMM from 1990–2018.

| Pooled OLS | Fixed Effects | Random Effects | System GMM | |

|---|---|---|---|---|

| Main Results (Dep. Variable: RGDP, log) | ||||

| VARIABLES | LRGDP | LRGDP | LRGDP | LRGDP |

| LFDI | 0.149 ** | 0.116 *** | 0.118 *** | 0.00721 *** |

| (0.0138) | (0.00956) | (0.00970) | (0.00275) | |

| LDBT | 0.747 ** | 0.241 ** | 0.274 ** | −0.00607 *** |

| (0.0212) | (0.0399) | (0.0362) | (0.00285) | |

| LEXR | −0.0258 *** | 0.0212 ** | 0.0175 ** | 0.00115 *** |

| (0.00423) | (0.0246) | (0.0230) | (0.00125) | |

| LODA | 0.0297 ** | 0.119 ** | 0.131 ** | 0.00986 *** |

| (0.0215) | (0.0410) | (0.0409) | (0.00248) | |

| LTRO | −0.107 ** | 0.102 * | 0.0917 * | 0.00407 *** |

| (0.0490) | (0.0670) | (0.0669) | (0.00825) | |

| Southern Africa | 0.275 * | - | 0.414 | - |

| (0.0645) | - | (0.428) | - | |

| Central Africa | 0.165 ** | - | 0.523 | - |

| (0.0484) | - | (0.356) | - | |

| Eastern Africa | 0.157 ** | - | 0.386 | - |

| (0.0426) | - | (0.320) | - | |

| L.LRGDP | - | - | - | 0.994 *** |

| - | - | - | (0.00462) | |

| Constant | 3.682 | 12.61 | 11.41 | −0.0427 * |

| (0.425) | (1.111) | (1.015) | (0.0843) | |

| Year Dummies | Yes | Yes | Yes | - |

| Observations | 1118 | 1118 | 1118 | 1081 |

| R-squared | 0.837 | 0.613 | - | - |

| Instruments/Groups | - | - | - | 762/39 |

| Hansen p-value | - | - | - | 1 |

| AR(2) p-value | - | - | - | 0.163 |

| Hausman (p-value) | - | 0.0000 | 1 | |

| Number of Country ID | - | 39 | 39 | 39 |

Notes: Robust standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Joshua, U.; Babatunde, D.; Sarkodie, S.A. Sustaining Economic Growth in Sub-Saharan Africa: Do FDI Inflows and External Debt Count? J. Risk Financial Manag. 2021, 14, 146. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14040146

AMA Style

Joshua U, Babatunde D, Sarkodie SA. Sustaining Economic Growth in Sub-Saharan Africa: Do FDI Inflows and External Debt Count? Journal of Risk and Financial Management. 2021; 14(4):146. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14040146

Chicago/Turabian StyleJoshua, Udi, David Babatunde, and Samuel Asumadu Sarkodie. 2021. "Sustaining Economic Growth in Sub-Saharan Africa: Do FDI Inflows and External Debt Count?" Journal of Risk and Financial Management 14, no. 4: 146. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14040146