How to Design Cryptocurrency Value and How to Secure Its Sustainability in the Market

Business Administration, Hansei University, Gunpo 15852, Korea

J. Risk Financial Manag. 2021, 14(5), 210; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050210

Submission received: 13 March 2021

/

Revised: 20 April 2021

/

Accepted: 23 April 2021

/

Published: 6 May 2021

(This article belongs to the Special Issue Sustainability of Business Ecosystems)

Abstract

:The purpose of this study is to analyze the contents of cryptocurrency value design based on adaptability to the current market. It is also intended to provide a method of issuing cryptocurrency before its creation, and an operation method afterwards. Activities before the creation of cryptocurrency must determine desirable behaviors and rewards to create value, and suggest countermeasures to prevent participants from engaging in undesirable behaviors. After the creation of a cryptocurrency, it is necessary to propose a method to induce scarcity and increase demand so that the value of the generated cryptocurrency can be sustained. To observe this, we looked at the contents of the value design of the eight types of cryptocurrencies currently in use in the market. Some cryptocurrencies, such as Bitcoin, are choosing mining as a reward, to secure scarcity for maintaining the value of cryptocurrency, limiting the amount of issuance, and burning the already issued cryptocurrency in the market. Also, increasing demand helps maintain the value of cryptocurrency. This study can contribute to supporting the growth of a healthy cryptocurrency market through cryptocurrency-related research.

1. Introduction

Blockchain technology is the biggest contributor to the growth of the cryptocurrency market, and Bitcoin was first introduced to the market through this technology. As of the current publication, various cryptocurrencies are simultaneously being created and disappearing in the market. Those who want to conduct business with cryptocurrency are highly interested in how to create and maintain the value of cryptocurrency. Therefore, this study observed how cryptocurrency was implemented to provide value, and how it provides persistence to survive in the market.

Firstly, this study investigated the value design stage for cryptocurrency and looked at desirable goals and actions to provide value before creating cryptocurrency. Also, countermeasures that limit undesirable behavior (e.g., hacking) were examined and discussed in order to implement an ecosystem that can survive in the market as well as sustain the value that emerges after the creation of cryptocurrency.

The purpose of this study is to analyze the value of cryptocurrency based on its adaptability to the market. We studied the issuance (activity before creation) and operation (activity after creation) required when creating cryptocurrency. This paper can contribute to the support and growth of a healthy cryptocurrency market as a reference on cryptocurrency creation and operation.

2. Literature Review

2.1. Cryptocurrency

A blockchain-based virtual asset is created as a cryptographically secure object (token). Depending on the nature of the token, when the token, commonly called cryptocurrency, generates the value of purchase and exchange, it retains a digital monetary character. Cryptocurrency is a type of digital asset designed to be used as a means of exchange, which increases transaction security, controls currency issuance, and certifies the transaction or movement of assets (Bakar et al. 2017).

Cryptocurrencies are the first pure digital assets to be included by asset managers. Even though they share some commonalities with more traditional assets, they have a separate nature of their own, and their behavior as an asset is still under the process of being understood. In Korea, it is generally referred to as “virtual currency”, but there is a conceptual difference between cryptocurrency and virtual currency.

Cryptocurrency is a compound word of crypto and currency. In this case, the prefix “crypto-“ refers to encrypted electronic information issued through a distributed network using blockchain technology.

Virtual currency refers to any currency used in a virtual environment and includes the concept of e-money, such as online game money or cyber money, online credit card payments, and bank balances. The expression “virtual currency” does not explain the characteristics of cryptocurrency’s encryption security technology, so there is a need to clearly separate cryptocurrency and virtual currency (Lee et al. 2018).

In this study, rather than the name of a token, the value design and persistence in terms of cryptocurrency that holds purchase and transactional value shall be presented.

We generally believe that holding an asset in scarcity (e.g., gold and diamonds) should yield a return. Therefore, in the case of a large number of public blockchain-based cryptocurrencies including Bitcoin, the number of coins to be mined is predetermined. In this case, one purchases cryptocurrency with the belief that the scarcity of cryptocurrency will be maintained.

The biggest problem with blockchain-based cryptocurrency is that the value of money lies not in social credit but in “shortage or scarcity.” In social credit, however, credit is defined objectively in social relationships, not in subjective beliefs. Therefore, researchers with more pessimistic views argue that cryptocurrency is a Ponzi scheme caused by the futile hopes of supporters of value by scarcity, such as outdated gold (Amadeo 2021).

On the other hand, advocates of cryptocurrency (e.g., Bitcoin) argue that money is viewed only as a means of personal transaction and credit. In addition, real credit money requires not only social institutions to supply credit in response to regular social demands, but also legal and institutional practices to support the operation of the institutions (Ciaian et al. 2016; Fang et al. 2020).

The modern capitalist credit currency system, led by governments, banks, and corporations, has emerged as a problem in that monopolies and an uneven distribution of credit continue while many individuals are economically alienated—the world of cryptocurrency has not created a traditional credit system to cope with this (see Table 1). However, those who prefer cryptocurrency believe that if an organization changes the algorithm that records transactions, maintains security, and maintains only the scarcity of coins, it can return economic power to individuals in social activities. Various cryptocurrencies are still emerging, and through this, its proponents are making many attempts to create value in new markets.

2.2. Factors That Create Value of Cryptocurrency

Cryptocurrency now is available as a form of payment for retail goods, as an instrument for a wholesale international transaction, and as a means of exchange for whatever goods that are available through ATM (Asynchronous Transfer Mode)’s (Limba et al. 2019).

The Wonik Park (2019) study explored whether cryptocurrencies that emerged after Bitcoin, also known as Altcoins, showed differential price movements in the exchange market. For this purpose, the study conducted a time series analysis of cryptocurrency prices through a Johansen Cointegration Test and Vector Error Correction Model. The results showed that prices of Ethereum, Ripple, Bitcoin-Cash, and Litecoin, which were among the top 5 of the market capitalization value, have revealed some price impact with Bitcoin (Jang and Kim 2017; Jun and Yeo 2014; Wonik Park 2019).

Another study examined the performance of cryptocurrency issued by the initial coin offering (ICO) for three years after the initial exchange listing. The median ICO fell by 30% during the one-to-24 months’ retention period. This clearly showed that there is a significant amount of distortion in the cryptocurrency market. In addition, large-scale ICOs are expensive in the long term and have low economic value due to the size effect shown by empirical regularity in the data (Momtaz 2019).

The research investigated the identification of possible determinants of cryptocurrency value formation, including Bitcoin. As a result, they used cross-sectional empirical data to estimate the regression model that points to the competitive level, unit production rate, and difficulty of the producer network—three main drivers of cryptocurrency value. They reveal that the cost of producing digital currencies varies depending on the algorithm used to “mine” cryptocurrency (Al-Htaybat et al. 2019).

Altcoins tend to be vulnerable to 51% attacks, defined as when a miner or a group of miners try to control more than 50% of a network’s mining power, computing power, or hash rate, which significantly reduces its value on the day of the attack. Vulnerable Altcoins use task-proof blockchains with low market capitalization and low hash rates. Additionally, if the price of a particular Altcoin suddenly falls without a clear explanation, it is a sign that an attack may have occurred. The rate of depreciation due to 51% attacks is typically much greater than the stock price drops that typically occur when an entity experiences data leakage or other cybersecurity attacks (Shanaev et al. 2019).

As seen above, research is still being conducted on various ways to maintain the value of a generated cryptocurrency. Therefore, this study aims to examine how to the value design can keep the value of cryptocurrency sustainable.

3. Cryptocurrency Value Design

3.1. Cryptocurrency Value Design

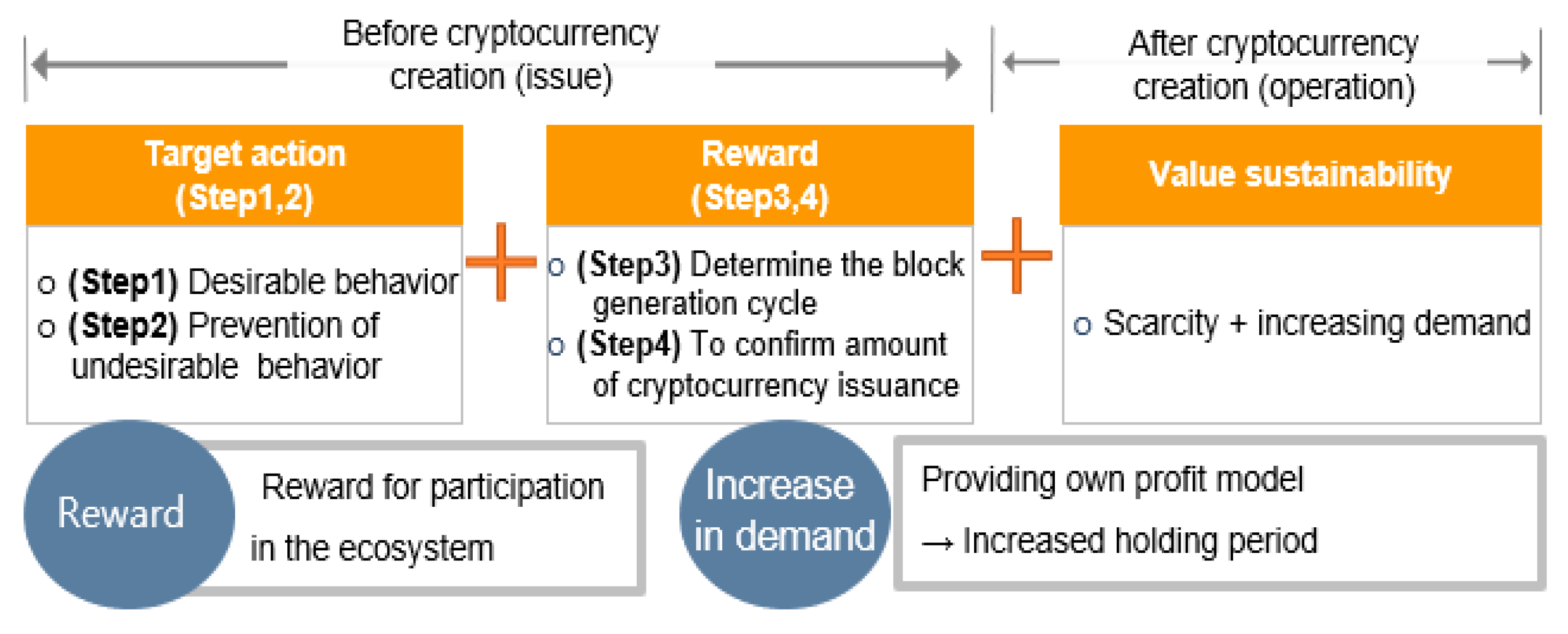

There are many considerations in designing cryptocurrency, but the principles of issuance and operation are simple. Issuance is a pre-creation activity of cryptocurrency and should produce a concept of target behavior and its compensation. As a process after issuance of cryptocurrency, operation is to provide a principle to continuously secure value of cryptocurrency in the market. The ‘open blockchain’ initially proposed by Bitcoin is system open to the public and requires a reliable method of application by participants. What emerged to solve this problem is compensation through cryptocurrency represented by mining. The most important way to grow cryptocurrency is the principle of compensation.

Cryptocurrency should be basically given as a reward for ecosystem participation, and demand should be maintained by creating its own profit model or increasing the period that it is held by participants. Without these considerations, a sustainable cryptocurrency ecosystem cannot be created, but may only be recklessly distributed primarily in the form of “sales” to investors and may respond to increases in demand only through inflation (Wonik Park 2019).

According to Figure 1, the first step (step 1) in generating a cryptocurrency should define a clear purpose of issuance. Usually, in cryptocurrency white papers, cryptocurrency issuers, or platform developers present the “problems” that they want to solve through this token and subsequently determine the user group that will benefit from its issuance. One needs to consider how they will participate, how much they will be involved, or how much reward will be needed to be able to drive participation (Al-Htaybat et al. 2019).

In step 2, in the reward-based system for participants, desirable behaviors should be defined and ways to prevent undesirable behaviors should be suggested. In many cases, undesirable behaviors occur such as ‘form of enterprise-type mining participation’, which is defined as when participants behave analogously to that of corporate miners with large equipment, mining excessively. The general public’s access to computing power (e.g., through smartphones) is generally unable to compete with the computing power of a corporate entity. As such, some appropriate solutions to limit the disparity of computing power should be prepared.

In step 3, the block generation cycle must be determined. The block generation cycle can be determined in consideration of the average computing power of the block producer as well as network and equipment processing speed. In addition, various factors of the applied market must be considered.

In step 4, the amount of cryptocurrency issuance is confirmed. In this case, mechanism design, incentive design, and reverse incentive design are required.

Although many services and goods providers must enter the cryptocurrency ecosystem, cryptocurrency can operate similarly to fiat currency, but it is ultimately difficult to apply the actual market.

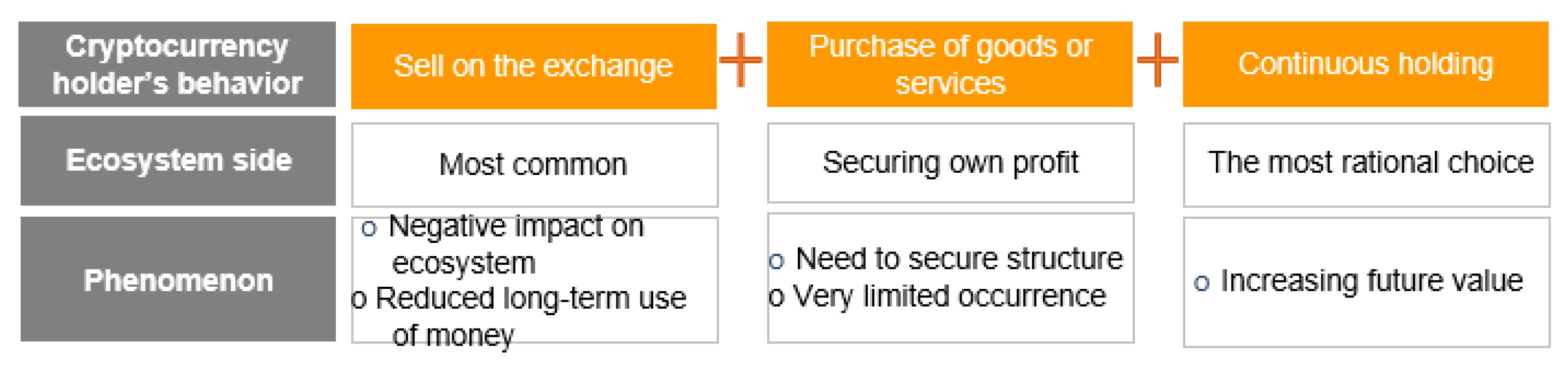

In order to maintain a sound ecosystem of issued cryptocurrency, participants should consider countermeasures. There are three choices in the behavior of those who receive cryptocurrency after issuing it: to sell to the exchange, to buy goods or services, or to retain the currency. Of these, selling on an exchange is the worst choice for cryptocurrency operators (see Figure 2).

Selling the cryptocurrency as soon as it is received by the participants means that there is very little long-term demand for money. Therefore, it does not have a self-sustaining profit structure (Limba et al. 2019). This is because most blockchain projects distribute cryptocurrencies to participants as rewards or investments, but purchasing goods and services with cryptocurrency is difficult in such an environment. In fact, even in the case of highly versatile Bitcoin, the goods and services that can be directly purchased in real life and for practical purposes are very limited.

For the operation community using issued cryptocurrency, the most realistic and desirable action is to keep the cryptocurrencies that participants received. Holding cryptocurrency comes from the belief that the intrinsic value will increase in the future, and this belief can provide trust in a cryptocurrency. In terms of fiat currency circulation, it is desirable to minimize the amount of circulation in the market with the supply and demand of money.

It is not easy to lower the liquidity of a cryptocurrency. Firstly, there are few places where cryptocurrency can be used, and secondly, most people recognize cryptocurrency for speculative purposes, so they often sell it according to market fluctuations.

To prevent this, various ideas have been suggested, such as maintaining a protection period for the issued currency, issuing a currency that can be sold on exchanges and currency used inside the ecosystem separately like Steemit, or airdrops (the act of distributing coins to existing cryptocurrency holders for free) when holding a currency for a long time.

3.2. Before Creating Cryptocurrency: Purposive Behavior and Compensation for Issue

3.2.1. Desirable Target Behavior and Reward

In terms of the cryptocurrency economy, the criteria for desirable and undesirable behaviors are not short-term profits of individuals, but long-term co-prosperity in which the entire ecosystem can grow and individuals can benefit. It is not a moral or ethical issue whether a particular behavior is considered desirable or undesirable in a cryptocurrency-related economy, but rather strictly economic and profit-oriented. What is desirable is to increase the value of cryptocurrency in the long term, and what is undesirable is to lower the value of cryptocurrency.

A desirable action is to optimize not only one’s own interests but also the interests of the entire ecosystem of participants by allowing them to create value through continuous participation by individuals or organizations and also by receiving appropriate rewards from the ecosystem. Therefore, the developers of a protective currency must take steps to define what is a desirable action before issuing it.

For example, if the desired behavior using a consensus algorithm in the way of proof of work is “mining,” it is necessary to consider who should participate and how they can do so. Many factors should be considered, such as deciding whether or not to impose restrictions on users.

In particular, it is imperative to consider whether efficiency or fairness is more important at this stage. As a related thread, EOS (a blockchain-based, decentralized system) is designed to focus on efficiency and limit the desired behavior of only 21 nodes as block generators.

In the real-world economy, monetary rewards often lead to better products and services; however, the digital world economy has a completely different way of working. Some economies work well without monetary compensation, some do not work well even if they are compensated, and some ecosystems that have been working well fail after introducing a compensation system.

3.2.2. Preventing Undesirable Behavior

Cryptocurrency economists should consider what are undesirable behaviors that reduce the value of the ecosystem. For example, if you look at Bitcoin, an undesirable behavior could be spam attacks or 51% percent attacks. If 51% attacks had occurred over times, the value of Bitcoin would be far lower than it is today; however, Bitcoin has effectively defended against these attacks and is maintaining a relatively high value at present. Looking at another example, we can consider exploiting funds through the smart contract vulnerabilities of Ethereum. From the attacker’s point of view, it may be the pursuit of maximizing profit, uncaring that the value of the entire network naturally declines.

In the case of Steem coin, its creators have defined creating content as a desirable behavior. Specifically, Steem coin defined writing articles on blogs and posting them as desirable activities, i.e., when bloggers write, users select excellent articles and reward them accordingly.

Steem’s attempt to compensate for content drew enthusiastic responses from many early users. It received much praise from those who wanted to write in early cyberspace. However, as the so-called “whale” group with the power of selection formed their own league, an unreasonable reward system was formed and the general participants began to ignore it. In other words, there was a disadvantage in that the ecosystem was damaged as it moved away from voluntary participation, which is a basic condition in sustainability. Nonetheless, Steem’s attempt is regarded as an innovative in that it defined content creation as a desirable behavior.

It is worth noting that the use of selection as the basis of the compensation system has “failed” by creating an inadequate compensation system that potentially operates unfairly and is not sustainable in the long run.

It could be looked at in terms of cost and profit as a way to prevent such undesirable behavior. As in the case of cryptocurrencies that have emerged, if the profit is not greater than the cost, the motivation for undesirable behaviors shall disappear. If the expected return from doing any undesirable behavior is less than that of doing the desirable behavior, or the difference is not substantial, there is no disincentive in doing so. In terms of cost, the basic design approach is to avoid undesirable behavior due to the cost increases. A representative case related to this is an environment in which more fees are required for spam attacks. And there are things that require more investments in stakes or mining hashes in order to do a 51% attack. Therefore, some miners could perform a 51% attack if desired, but a rational actor would not choose this method because it would be more profitable in the long run to grow the market as a good actor. Additionally, even if the attack were successful, it would come at a high cost—rumors may spread throughout the market, and the attacker may earn less than the expected return due to the fall of the cryptocurrency’s price.

The cryptocurrency economy, which is based on blockchain, cannot adapt quickly enough to control every continuously changing situation; therefore, semi-centralized or centralized solutions have been emerging recently as potential solutions.

Examples include allowing only certain accounts to exert influence through a licensing system based on reputation and many pros and cons, or introducing a certification and blocking system in a blockchain company and empowering only those who meet their ecosystem growth philosophy.

This method is criticized by those who aim at decentralization, but we believe that this centralized solution is a transitional factor that is needed to facilitate the connection between blockchain and the real world, and may be a variable that can be chosen from full decentralization to full centralization, depending on the token economy designer.

3.3. After Creating Cryptocurrency: Securing Value Sustainability for Operation

3.3.1. How to Maintain the Value of Cryptocurrency

After issuance of cryptocurrency, it is necessary to devise a plan for the ecosystem to secure self-sustainability in consideration of self-evolution and innovation. Ideally, all evolution or innovation should be made automatically, but in reality, governance structures can be created to ensure self-sustainment.

In addition, in the case of a network server, it is necessary to calculate the network maintenance cost according to the scale of how many users there are and how quickly to process and reflect this in the block generating node (see Table 2).

There are three ways to consider how to stably maintain the value created by cryptocurrency. The first is a way to maintain scarcity by controlling the absolute amount. The second is a method to induce demand by continuously using it in the market. The third option is to utilize the above two methods simultaneously. Currently, the cryptocurrency ecosystem is a combination of scarcity and increasing demand.

3.3.2. Scarcity Application

An example of applying scarcity is as follows. As in the case of XRP (formerly Ripple), one way to secure scarcity is to issue the total amount of cryptocurrency, store it in escrow, and supply only a certain amount to the market every month. And, in the case of applying scarcity, Bitcoin exists as a way to control the absolute amount of cryptocurrency. Ethereum uses a method that allows the increasing number of cryptocurrencies in the market to increase indefinitely but decreases the relative increase. In addition, Guinea National Coin (cryptocurrency) uses a method of adjusting the quantity by absorbing the cryptocurrency existing in the market (see Table 3).

3.3.3. Increased Demand Application Cases

The increase in demand for cryptocurrency is a major factor in increasing the value of cryptocurrency. Therefore, due diligence should paid to increasing demand. As a representative example, there are cases where the value of cryptocurrency appears as an alternative to the inconvenience of the existing fiat currency. As an example, the demand for cryptocurrency in emerging markets is increasing due to the worldwide dollar shortage. Billions of individuals outside the U.S. spend U.S. dollars every day, but the supply is insufficient. In the case of emerging markets, the dollar is difficult to find. But for those who do not trust their own currency, Bitcoin and Stablecoin can be used as a hedge against future inflation and as a useful means for settlement or remittance.

This is a case that has been emerging in situations where it is not easy to move funds between countries due to the current COVID-19 environment. In particular, countries that use U.S. dollars officially or unofficially are experiencing many difficulties. In these countries, many prefer using U.S. dollars for larger transactions such as B2B transactions, savings, and rent because they do not trust their currencies. Nigeria, a crude oil exporter, also experienced a serious dollar crisis due to a worldwide dollar shortage along with a plunge in crude oil prices. In Nigeria, Africa’s largest economy, bitcoin-to-person transactions surged, leading to an increase in transactions across the African region.

A similar phenomenon occurred in Venezuela. As the value of its currency, the Venezuelan Bolivar, plummeted and people could not pay with cash even when they went shopping, the authoritarian regime of the government effectively withdrew its restrictions on the use of U.S. dollars. But recently, due to the COVID-19 pandemic, Venezuelans are not getting the dollars they demand for daily usage. In this situation, Bitcoin has been provided as an alternative (Shutterstock 2020).

What many Venezuelans want is U.S. dollars rather than Bitcoin. Therefore, if they have assets similar to U.S. dollars, they will have found a solution. As shown in the impact of the increase in demand, an increase in demand for cryptocurrency can lead to an increase and persistence of cryptocurrency value.

4. Comparison of Blockchain-Based Cryptocurrency Value Design

In the case of Bitcoin, which was the first cryptocurrency ever created, it is provided by solving the hash function, which is a mining method as a target action and reward, and the quantity of 21 million is limited to apply the principle of scarcity. It is one of the cryptocurrencies that can purchase and trade goods as well as maintain scarcity in terms of value sustainability. Additionally, the coin supply has been decreasing exponentially every four years (half-life) according to the principle of scarcity (see Table 4).

Ethereum, like Bitcoin, uses a similar mining method and a scarcity-based exchange medium. However, as it is unlimited, the maximum issuance of Ethereum remains undecided, and verification of its sustainability is still underway in the market.

XRP, a cryptocurrency issued by banks when transferring money through legalization, is used as a means of service for the ‘real’ economy through a batch generation process. It is a currency that controls volume by locking up 55 billion XRPs, nearly half of its maximum issuance.

In the case of EOS, one billion coins were initially generated and provided to the market, and two million coins were distributed over 350 times. To secure the scarcity of its cryptocurrency, the company has been using the process of incinerating based on commission.

The maximum issuance of Dash is 19 million (some claim 22.5 million), and the end of issuance is known as 2075. Target behavior and rewards include mining compensation (45%), the master node (45%), and governance (10%). In addition, anonymous transmission implementations are made through a PoS system called a Master node, and 1000 Dash is required for master node construction. Looking at the price change factors, the effect of tying large amounts of Dqsh increases the transaction price, which results in higher returns. This increases the demand for master nodes and makes them suggestive and actionable through governance. However, if the market price falls for a long period, the volume tied to the master node can affect the price in the short term.

Steem was provided through the creation of social media content and was developed in conjunction with real-life services. However, regarding sustainability in the marketplace, the emergence of some distorted compensation schemes has become a problem.

Links is a cryptocurrency that can be paid as incentives through user-reward-based content and distributed application activities being developed on Line. Line is a Mobile messenger service (such as Kakao Talk in Korea) in Japan that was developed in NHN Japan (later renamed to ‘Line Corporation’). So, it has developed 5 types of Dapps (Decentralized applications) including future predictions, knowledge sharing, product reviews, restaurant reviews, and travel destination reviews. It is proceeding with an exclusive listing on the Bitbox Exchange (a global cryptocurrency exchange) operated by the Line Corporation subsidiary, Line Tech Plus, and is also considering linking various online and offline services to payment and compensation means. Line was developed with its own blockchain technology and aims to create a Link ecosystem that can be practically utilized.

Medibloc is a blockchain-based health information open platform that allows the safe integration and management of all medical information produced by smartphones and other devices, as well as medical information scattered across institutions. This allows healthcare consumers to exercise full ownership and management of their medical information. It is a certification support service that allows individuals to freely provide their medical information to other medical institutions for treatment purposes without issuing data from the relevant institution as in the existing method.

Medical providers may record or obtain medical information for research purposes, with the consent of medical consumers. Medibloc will issue MED (Medi token), a cryptocurrency that will be used on the platform, and participants will receive compensation by using MED according to their contributions. Medical consumers as well as healthcare providers who have contributed to the production of medical information are entitled to due compensation according to these contributions. MEDs can also be used as a means to pay for medical expenses, medications, insurance premiums, etc. in various institutions associated with Medibloc (MediBloc 2021).

5. Conclusions

There are many considerations in designing cryptocurrency, but the principle of issuance and operation is simple. Issuance is a pre-creation activity of cryptocurrency and should produce a concept of the target behavior and compensation. The operation, which is the process of issuing cryptocurrency, provides the principle in which cryptocurrency can be continuously valued in the market.

If one observes the design stage of value before cryptocurrency creation, the following steps are taken: step one should define a clear purpose of issuance; step two should define desirable behaviors and also prevent undesirable behaviors for participants using compensation as a driver; step three should determine the block generation cycle; step four should confirm the amount of cryptocurrency issued.

The most realistic and best action for the community is to hold the cryptocurrency received by the participants. Holding cryptocurrency comes from the belief that intrinsic value will increase over time, and this belief increases trust in the currency. In the case of general fiat currency, it is desirable to minimize the amount of circulation in the market due to supply and demand.

In terms of the cryptocurrency economy, the standard for what is desirable and undesirable is not an individual’s pursuit of short-term profits, but rather a long-term win-win growth in which the entire ecosystem can grow and individuals can also benefit. It is not a moral or ethical issue whether a particular behavior is considered desirable or undesirable in a cryptocurrency-related economy, but rather strictly economic and profit-oriented. What is desirable is to increase the value of cryptocurrency in the long term, and what is undesirable is to lower its value. A desirable action is to optimize the interests of not only one’s interests but also of the entire ecosystem by enabling the creation of value through continuous participation of individuals or organizations and by receiving appropriate rewards from the ecosystem.

It can be looked at in terms of cost and revenue as a way to prevent undesirable behavior. As in the case of current cryptocurrency, if the profit is not greater than the cost, the motivation for the behavior will disappear. Therefore, people who want to acquire cryptocurrency through undesirable behavior should encounter sufficient risk in to disincentivize undesirable behavior.

There are three ways to keep the value of cryptocurrency permanently stable: maintaining scarcity by controlling absolute quantities, generating demand by allowing continuous use in the market, and the above two methods being used simultaneously.

The cryptocurrency ecosystem is a combination of scarcity and increased demand so that the current eight types of cryptocurrency value design provided to the market and the current status of market operation were compared. Each cryptocurrency such as Bitcoin and Ethereum provides desirable behavior and clear compensation. Also, the value management aspect is progressing according to the scarcity of cryptocurrency and the control of demand. However, even now, some cryptocurrencies are disappearing because they cannot create value in the market, and new cryptocurrencies are being created.

This study should contribute to the growth of new services and cryptocurrency markets in the future by presenting design and value creation aspects for cryptocurrency.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The author declares no conflict of interest.

References

- Al-Htaybat, Khaldoon, Khaled Hutaibat, and Larissa von Alberti-Alhtaybat. 2019. Global brain-reflective accounting practices: Forms of intellectual capital contributing to value creation and sustainable development. Journal of Intellectual Capital 20: e733. [Google Scholar] [CrossRef]

- Amadeo, Kimberly. 2021. Ponzi Scheme, What It Is and How It Works with Examples. Available online: https://www.thebalance.com/what-is-a-ponzi-scheme-history-examples-vs-pyramid-scheme-3305877 (accessed on 11 March 2021).

- Bakar, Nashirah Abu, Sofian Rosbi, and Kiyotaka Uzaki. 2017. Cryptocurrency Framework Diagnostics from Islamic Finance Perspective: A New In-sight of Bitcoin System Transaction. International Journal of Management Science and Business Administration 4: 19–28. [Google Scholar] [CrossRef]

- Ciaian, Pavel, Miroslava Rajcaniova, and d’Artis Kancs. 2016. The Economics of Bitcoin Price Formation. Applied Economics 48: 1799–815. [Google Scholar] [CrossRef] [Green Version]

- Fang, Fan, Carmine Ventre, Michail Basios, Hoiliong Kong, Leslie Kanthan, Lingbo Li, David Martinez-Regoband, and Fan Wu. 2020. Cryptocurrency Trading: A Comprehensive Survey. arXiv arXiv:2003.11352. [Google Scholar]

- Jang, Seong Il, and Jeong Yeon Kim. 2017. A Study on The Asset Characterization of Bitcoin. The Journal of Society for e-Business Studies 22: 117–28. [Google Scholar]

- Jun, J. Y., and E. J. Yeo. 2014. Understanding Bitcoin: From the Perspective of Monetary Economics. Korea Business Review 18: 211–39. [Google Scholar]

- Lee, Junsik, Gunwoo Kim, and Dohyung Park. 2018. Empirical Analysis of Bitcoin Price Changes: Focusing on Consumers, Indus-tries, and Macro Variables. Intelligence Information Research 24: 195–220. [Google Scholar]

- Limba, Tadas, Andrius Stankevičius, and Antanas Andrulevičius. 2019. Towards sustainable cryptocurrency: Risk mitigations from a perspective of national security. Risk Mitigations from a Perspective of National Security 9: 375–89. [Google Scholar] [CrossRef]

- MediBloc. 2021. Available online: https://kr.investing.com/crypto/medibloc (accessed on 11 March 2021).

- Momtaz, Paul P. 2019. The pricing and performance of cryptocurrency. The European Journal of Finance 27: 367–80. [Google Scholar] [CrossRef]

- Shanaev, Savva, Arina Shuraeva, Mikhail Vasenin, and Maksim Kuznetsov. 2019. Cryptocurrency Value and 51% Attacks: Evidence from Event Studies. The Journal of Alternative Investments 22: 65–77. [Google Scholar] [CrossRef]

- Shutterstock. 2020. Current Crisis Sparks Crypto Awakening in Developing Countries. Available online: https://www.hebergementwebs.com/blockchain/current-crisis-sparks-crypto-awakening-in-developing-countries (accessed on 11 March 2021).

- Wonik Park, Byunggil Min. 2019. Available online: https://www.dbpia.co.kr/Journal/articleDetail?nodeId=NODE09252730 (accessed on 11 March 2021).

Figure 1.

Cryptocurrency value design structure.

Figure 2.

Behavior of cryptocurrency holders.

{kind=link}

{kind=link}

Table 1.

Views on cryptocurrency.

| Item | Negative View | Positive View |

|---|---|---|

| Contents | Starting from the scarcity of money, it is vulnerable to Ponzi-like scams | It is a means of personal transactions and credit and a method of providing integrated economic management authority to individuals |

Table 2.

Ways to increase the value of cryptocurrency and maintain its value.

| Items | Contents |

|---|---|

| Value change factors (issued volume according to issuance cycle) | Coin value changes according to the issuance volume The amount of issuance according to the issuance cycle is proportional to the amount of mining speed (when mining) |

| Value increase (method to increase coin value) | As the value changes according to the amount of issuance, it is necessary to manage the amount of issuance. Mechanism of determining supply quantity - Gold Type: Supplied in proportion to the amount of gold mined (gold production increases by 2% annually in the world supply) - Bitcoin Type: Fixed maximum issuance amount - Ethereum Type: The maximum issuance is undecided, and the issuance is decreasing - EOS Type: Initially increasing supply and recovering and burning in case of price drop - Medibloc Type: Expectation of initial speculative capital inflow (ex. Money supply increased by 1.5%, 2%, 2.5%) |

| Value maintenance (methods to maintain the value of cryptocurrency) | Provide means of mining and value inflow Building a business model that can secure profitability Buy back cryptocurrency (tokens) based on commercialization Algorithm-based stable coins Contents protocol |

Table 3.

Examples of scarcity application.

| Item | Contents |

|---|---|

| Bitcoin Type | Fixed maximum issuance - Gold is supplied to the market according to the amount of mined, and the world’s gold production increases by about 2% every year. - In the case of gold, the amount of growth is small, so the impact on the market is insignificant. It can be considered that gold issuance is fixed. |

| Ethereum type | The maximum issuance amount is undecided, and is responding to changes by reducing the issuance amount. |

| EOS Type | (Incineration utilization type) Plan to increase supply in the early stage and burn it after collecting if price falls |

| Mediblock Type | (Investment cost supply type) Expectation of initial speculative capital inflow and money supply increased by 1.5% 2% 2.5% |

Table 4.

The contents of the value design of the eight types of cryptocurrencies currently in use in the market.

Table 4.

The contents of the value design of the eight types of cryptocurrencies currently in use in the market.

| Item | Target Action and Reward | Sustainability of Values | Maximum Issuance | Issued Quantity | Feature |

|---|---|---|---|---|---|

| Bitcoin | Solving the hash function, as a mining method | Scarcity, means of exchange | 21 million (number of bitcoins) | 15,730,250 Bitcoins were issued (4 July 2017) 18,090,137 issued (8 December 2019) | Coin supply decreases exponentially every 4 years (half-life) |

| Ethereum | A type of consensus mechanism by which a cryptocurrency blockchain network achieves distributed consensus | Scarcity, means of exchange | Currently, the maximum issuance of Ethereum remains undecided. | 120 million Ethereums were issued (3 April 2018) | Cryptocurrency Media Trust Node reported that ETH issuance could decrease by 10 times by 2021, citing a timeline released by Justin Drake, an Ethereum 2.0 developer. |

| XRP | Issued for bank transfer transactions | Batch creation method Intermediate means for service utilization | 110 billion | 43 billion units are in circulation (28 November 2019) | The quantity is controlled by escrow lockup of 55 billion XRP, which is half of the maximum issuance |

| EOS | Batch issuance | Scarcity-based Burning of fees | 1 billion (to raise $4.2 billion) | 1.30 billion (Source: eosflare.io) (21 January 2019) | 0th: 200 million issued 2 million units distributed in 350 times |

| Dash | Mining compensation (45%) Master node (45%) Governance (10%) | Scarcity Means of exchange | The maximum issuance is 19 million (some claim 22.5 million) | 9.1 Million | Issuance ends in 2075 |

| Steem | Writing social media content | Provide real service | Has an infinite maximum number of issues | Issue volume:360,125,980 Steem (31 August 2019) | Unconfirmed at the end of issuance |

| Link | Incentive payment through user reward-based content and distributed application activities | Available only in the Line business ecosystem | 1 billion | 3.6 million | Link distribution event started (16 October 2018) |

| Med (Medibloc) | Compensation for medical information production and operation in medical information open platform | Used as a means of payment for medical expenses | 10 billion | 4.1 billion | 4.1 billion (13 November 2017) |

Line is Mobile messenger service such as Kakao Talk that was developed NHN Japan (later renamed to ‘Line Corporation’).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Yoo, S. How to Design Cryptocurrency Value and How to Secure Its Sustainability in the Market. J. Risk Financial Manag. 2021, 14, 210. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050210

AMA Style

Yoo S. How to Design Cryptocurrency Value and How to Secure Its Sustainability in the Market. Journal of Risk and Financial Management. 2021; 14(5):210. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050210

Chicago/Turabian StyleYoo, Soonduck. 2021. "How to Design Cryptocurrency Value and How to Secure Its Sustainability in the Market" Journal of Risk and Financial Management 14, no. 5: 210. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050210