A Systematic and Critical Review on the Research Landscape of Finance in Vietnam from 2008 to 2020

,

,

,

,  and

and

Abstract

:1. Introduction

2. Data and Methods

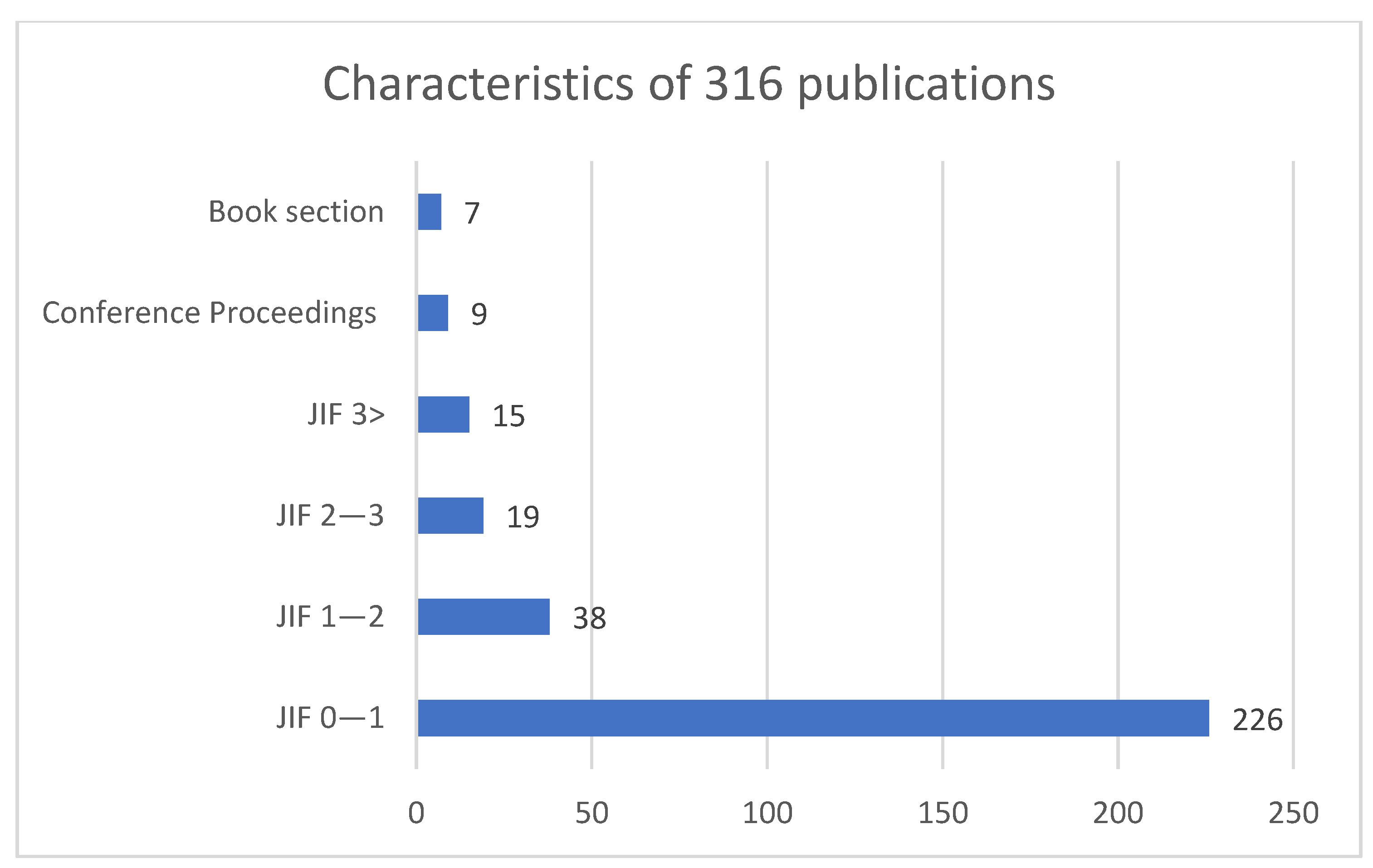

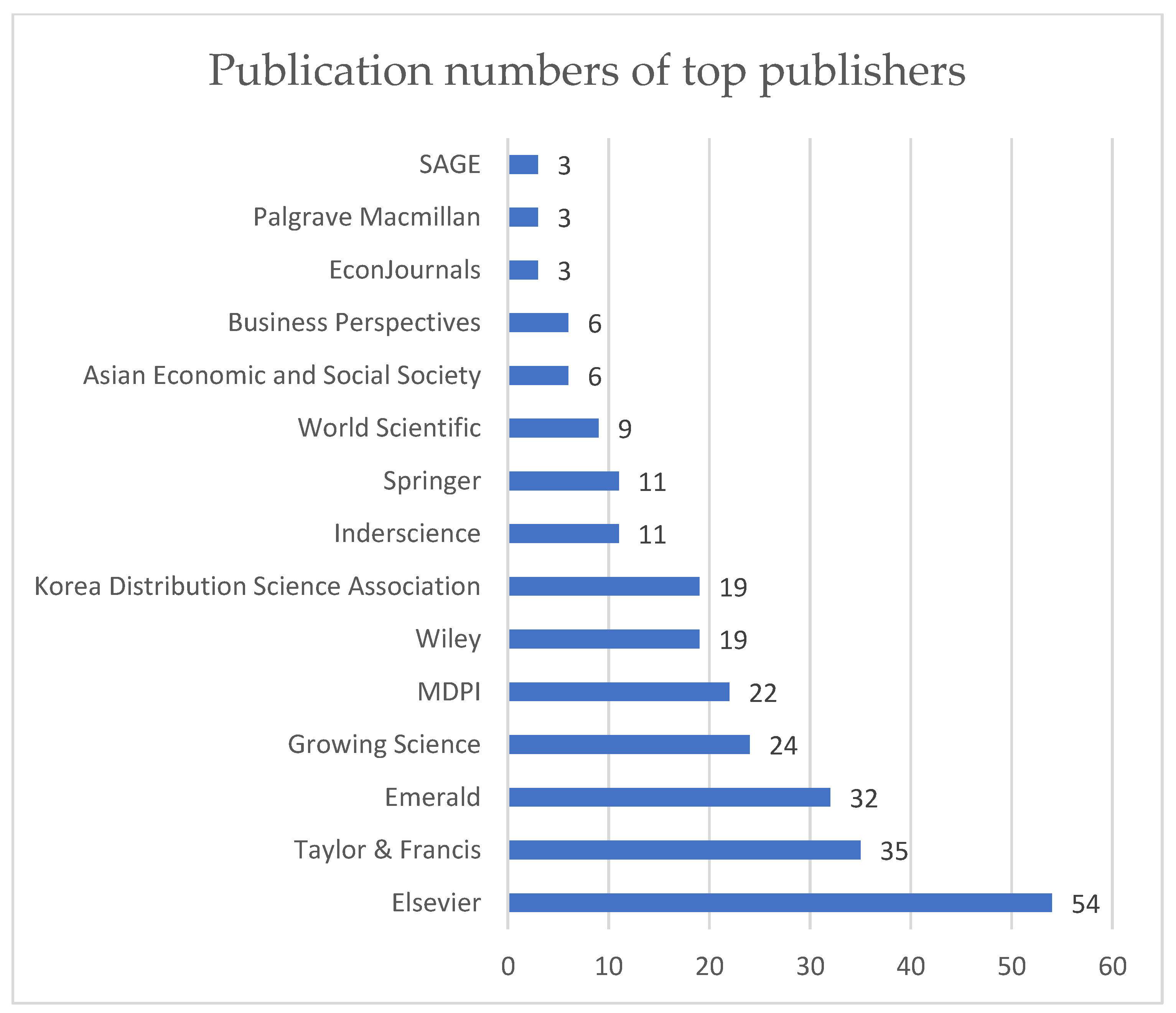

2.1. The SSHPA Database

2.2. Data Extraction and Filtering Process

- (1)

- The database is collected from Vietnam or regions in which the Vietnamese market is included or strongly influenced.

- (2)

- The research topic of the paper is either partially related to or focused on finance in multiple fields, notably the financial market structure, financial policy, or corporate finance.

- (3)

- The research coherently presents its results and implications for topics such as systematic corporate governance or policies implementations.

3. Thematic Review

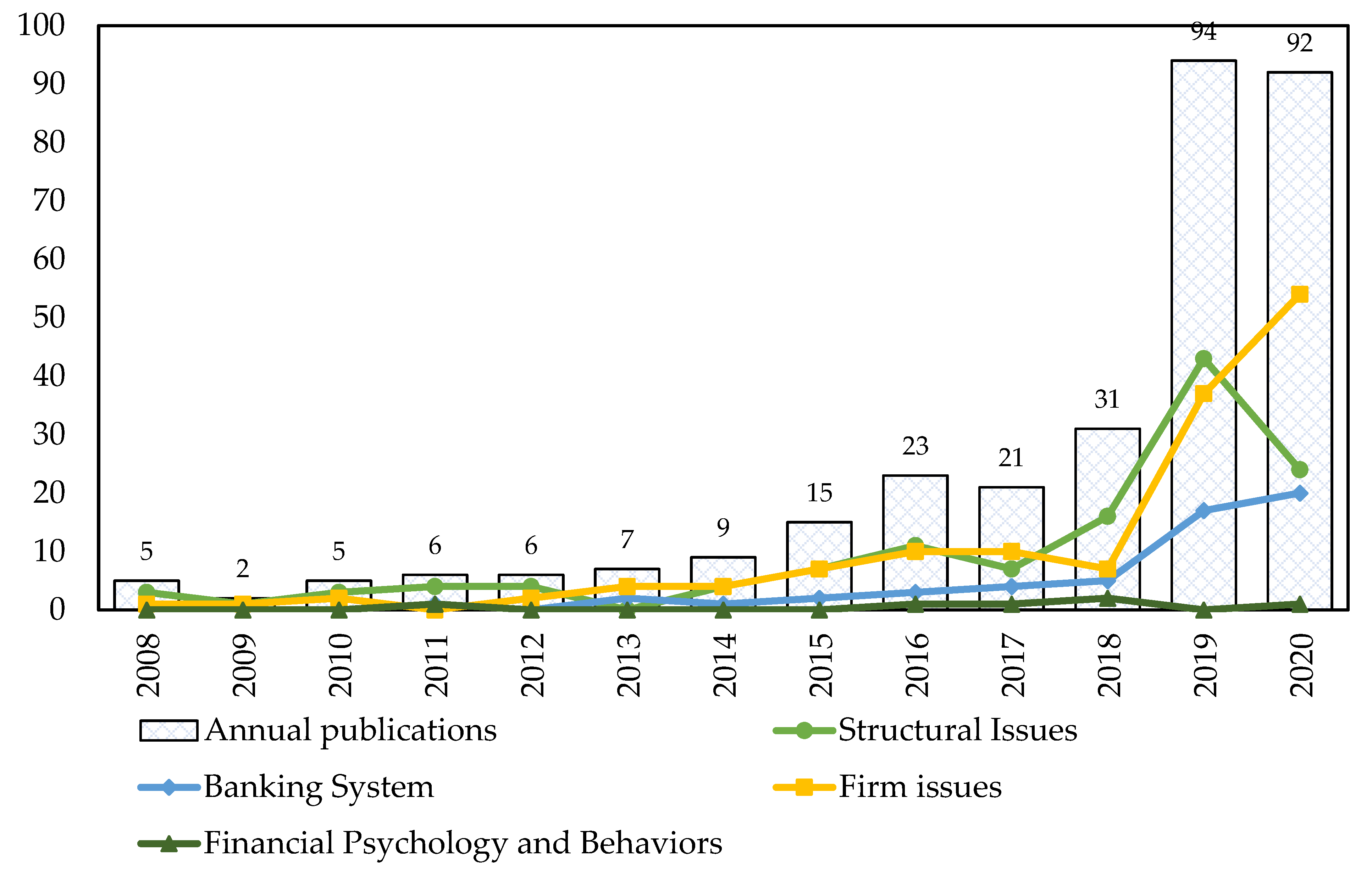

3.1. Vietnam’s Financial Publication Output Trends

3.2. Vietnam’s Finance Research Landscape

3.2.1. Structure Issues

Stock Market

Foreign Investment

Financial Inclusion Promotion

Rural Credit and Microcredit

IFRS Adoption

3.2.2. Banking System

Risks

- A bank holding public capital in Vietnam will positively affect the other banks.

- Contagion risk in the banking system emerges when banks are cross-owned, such as Vietnam Commercial Joint Stock Export-Import Bank A Chau Bank (ACB) and Joint Stock Commercial Bank for Investment and Development of Vietnam (BID).

- A commercial bank with state-owned capital may lead to contagion risk if they operate inefficiently or invest in a weak bank.

- Banks with a high ratio of NPL can cause a high contagion risk.

Bank Structure

Banking Performance

Bank Policies

3.2.3. Firm Issues

Capital Structure

Corporate Governance

Ownership

SMEs Financing

3.2.4. Financial Psychology and Behaviors

4. Discussion

4.1. Continued Interests in International Integration Post-COVID-19

4.2. Financial Technology Research

4.3. Green Bank

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Anwar, Sajid, and Lan Phi Nguyen. 2010. Foreign direct investment and economic growth in Vietnam. Asia Pacific Business Review 16: 183–202. [Google Scholar] [CrossRef] [Green Version]

- Anwar, Sajid, and Lan Phi Nguyen. 2011. Foreign direct investment and trade: The case of Vietnam. Research in International Business and Finance 25: 39–52. [Google Scholar] [CrossRef]

- Archer, Lan Thanh. 2019. Formality and Financing Patterns of Small and Medium-Sized Enterprises in Vietnam. Emerging Markets Finance and Trade, 1–18. [Google Scholar] [CrossRef]

- Archer, Lan Thanh, Parmendra Sharma, and Jen-Je Su. 2020. Do credit constraints always impede innovation? Empirical evidence from Vietnamese SMEs. Applied Economics 52: 4864–80. [Google Scholar] [CrossRef]

- Arnoud, W. A. Boot, Anjan V. Thakor, and Gregory F. Udell. 1991. Secured lending and default risk: Equilibrium analysis, policy implications and empirical results. The Economic Journal 101: 458–72. [Google Scholar] [CrossRef]

- Bai, Yuwen, Michael Faure, and Jing Liu. 2013. The Role of China’s Banking Sector in Providing Green Finance. Duke Environmental Law & Policy Forum 24: 89–140. [Google Scholar]

- Batten, Jonathan A., and Xuan Vinh Vo. 2015. Foreign ownership in emerging stock markets. Journal of Multinational Financial Management 32–33: 15–24. [Google Scholar] [CrossRef]

- Batten, Jonathan A., and Xuan Vinh Vo. 2016. Bank risk shifting and diversification in an emerging market. Risk Management 18: 217–35. [Google Scholar] [CrossRef]

- Batten, Jonathan, and Xuan Vinh Vo. 2019. Determinants of Bank Profitability—Evidence from Vietnam. Emerging Markets Finance and Trade 55: 1417–28. [Google Scholar] [CrossRef]

- Bekaert, Geert, Kenton Hoyem, Wei-Yin Hu, and Enrichetta Ravina. 2017. Who is internationally diversified? Evidence from the 401(k) plans of 296 firms. Journal of Financial Economics 124: 86–112. [Google Scholar] [CrossRef]

- Berg, Sigbjørn Atle, Finn R. Førsund, Eilev S. Jansen, Sigbjorn Atle Berg, and Finn R. Forsund. 1992. Malmquist indices of productivity growth during the deregulationof Norwegian banking, 1980–1989. The Scandinavian Journal of Economics 94: S211. [Google Scholar] [CrossRef]

- Bester, Helmut. 1985. Screening vs. rationing in credit markets with imperfect information. The American Economic Review 75: 850–55. [Google Scholar]

- Boudriga, Abdelkader, Neila Boulila Taktak, and Sana Jellouli. 2009. Banking supervision and nonperforming loans: A cross-country analysis. Journal of Financial Economic Policy 1: 286–318. [Google Scholar] [CrossRef] [Green Version]

- Brooks, Chris, and Lisa Schopohl. 2018. Topics and trends in finance research: What is published, who publishes it and what gets cited? The British Accounting Review 50: 615–37. [Google Scholar] [CrossRef]

- Cao, Nguyet Thi Khanh. 2019. What factors determine whether small and medium enterprises obtain credit from the formal credit market? The case of Vietnam. Asian Economic Journal 33: 191–213. [Google Scholar] [CrossRef]

- Chinh, Pham Minh, and Quan-Hoang Vuong. 2009a. Kinh tế Việt Nam: Thăng trầm và đột phá. Hà Nội: Nxb Chính trị Quốc gia. [Google Scholar]

- Chinh, Pham Minh, and Quan-Hoang Vuong. 2009b. Bối cảnh tài chính Việt Nam 1997–1998 và 2007–2008: khoảng cách và biến đổi. Nghiên cứu Kinh tế 48: 3–24. [Google Scholar]

- Cuong, Nguyen Viet. 2008. Is a governmental micro-credit program for the poor really pro-poor? Evidence from Vietnam. The Developing Economies 46: 151–87. [Google Scholar] [CrossRef]

- Dang, Van Dan. 2019. The effects of loan growth on bank performance: Evidence from Vietnam. Management Science Letters, 899–910. [Google Scholar] [CrossRef]

- Dang, Van Dan. 2020. Do non-traditional banking activities reduce bank liquidity creation? Evidence from Vietnam. Research in International Business and Finance 54: 101257. [Google Scholar] [CrossRef]

- Dang, Ha V., and Mi Lin. 2016. Herd mentality in the stock market: On the role of idiosyncratic participants with heterogeneous information. International Review of Financial Analysis 48: 247–60. [Google Scholar] [CrossRef]

- Dang, Tung Lam, Nguyen Trang Phuong Doan, Thi Minh Hue Nguyen, Thanh Thao Tran, and Xuan Vinh Vo. 2019. Analysts and stock liquidity—Global evidence. Cogent Economics & Finance 7: 1625480. [Google Scholar] [CrossRef]

- Dang, Ngoc Hung, Duc Cuong Pham, Xuan Thang Nguyen, and Thi Thanh Hoa Nguyen. 2020. Effects of corporate governance and earning quality on listed Vietnamese firm value. The Journal of Asian Finance, Economics and Business 7: 71–80. [Google Scholar] [CrossRef]

- De Buysere, Kristof, Oliver Gajda, Ronald Kleverlaan, and Dan Marom. 2012. A Framework for European Crowdfunding. Available online: http://eurocrowd.org (accessed on 1 May 2021).

- Diamond, Douglas W. 1991. Debt maturity structure and liquidity risk. The Quarterly Journal of Economics 106: 709–37. [Google Scholar] [CrossRef]

- Dinh, The Hung, and Trung Tuan Tran. 2019. Factors affecting the effectiveness of internal control in joint stock commercial banks in Vietnam. Management Science Letters, 1799–812. [Google Scholar] [CrossRef]

- Dinh, Trang Thi-Huyen, Duc Hong Vo, Anh The Vo, and Thang Cong Nguyen. 2019. Foreign direct investment and economic growth in the short run and long run: Empirical evidence from developing countries. Journal of Risk and Financial Management 12: 176. [Google Scholar] [CrossRef] [Green Version]

- Do, Xuan Luan. 2015. Microcredit and poverty reduction: A case study of microfinance fund for community development in Northern Vietnam. Journal of Agricultural Science 7. [Google Scholar] [CrossRef] [Green Version]

- Do, Hoai Linh. 2019. Impacts of Founder on The Success of Crowdfunding in Vietnam. Journal of Economics and Business 2: 356–62. [Google Scholar] [CrossRef] [Green Version]

- Doumpos, Michael, Chrysovalantis Gaganis, and Fotios Pasiouras. 2016. Bank diversification and overall financial strength: International evidence. Financial Markets, Institutions & Instruments 25: 169–213. [Google Scholar] [CrossRef] [Green Version]

- Elyasiani, Elyas, and Seyed Mehdian. 1995. The comparative efficiency performance of small and large US commercial banks in the pre- and post-deregulation eras. Applied Economics 27: 1069–79. [Google Scholar] [CrossRef]

- Faber, André, and Quan Hoang Vuong. 2004. New empirical results on anomalies and herd behavior: Vietnam stock market 2000–2004. Economic Studies 44: 55–59. [Google Scholar]

- Färe, Rolf, and Shawna Grosskopf. 2010. Directional distance functions and slacks-based measures of efficiency. European Journal of Operational Research 200: 320–22. [Google Scholar] [CrossRef]

- Fatima, Tajjali, and Amir Shehzad. 2014. An analysis of impact of merger and acquisition of financial performance of banks: A case of Pakistan. Journal of Poverty, Investment and Development 5: 29–36. [Google Scholar]

- Gopinath, Gita. 2020. The Great Lockdown: Worst Economic Downturn Since the Great Depression. Available online: https://blogs.imf.org/2020/04/14/the-great-lockdown-worst-economic-downturn-since-the-great-depression/ (accessed on 1 May 2021).

- Gordon, Lawrence A., Martin P. Loeb, and Wenjie Zhu. 2012. The impact of IFRS adoption on foreign direct investment. Journal of Accounting and Public Policy 31: 374–98. [Google Scholar] [CrossRef]

- Ha, Dao, Mai Nguyen, and Kim Nguyen. 2016. Accessibility to credit of small medium enterprises in Vietnam. Afro-Asian Journal of Finance and Accounting 6: 241. [Google Scholar] [CrossRef]

- Han, Jianlei, Jing He, Zheyao Pan, and Jing Shi. 2018. Twenty years of accounting and finance research on the Chinese capital market. Abacus 54: 576–99. [Google Scholar] [CrossRef]

- Haughton, Jonathon, and Shahidur R. Khandker. 2016. Microcredit in Viet Nam: Does It Matter? Washington, DC: International Food Policy Research Institute, p. 33. [Google Scholar]

- Hoang, Thi Thanh Hang, Kieu Trinh Vo, and Nguyen Tuong Vy Ha. 2019a. Analysis of the factors affecting credit risk of commercial banks in Vietnam. In Paper presented at the ECONVN 2019: Beyond Traditional Probabilistic Methods in Economics, 14–16 January, Ho Chi Minh City, Vietnam. Cham: Springer. [Google Scholar]

- Hoang, Thi Viet Ha, Ngoc Hung Dang, Manh Dung Tran, Thi Thuy Van Vu, and Quang Trung Pham. 2019b. Determinants influencing financial performance of listed firms: Quantile regression approach. Asian Economic and Financial Review 9: 78–90. [Google Scholar] [CrossRef] [Green Version]

- Hu, Ying. 2015. Regulation of equity crowdfunding in Singapore. Singapore Journal of Legal Studies 2015: 46–76. [Google Scholar]

- Hu, Yingyi, Tiao Zhao, and Lin Zhang. 2018. Does low price synchronicity mean more informativeness in stock prices? Empirical evidence on information integration speed in the Chinese stock market. Emerging Markets Finance and Trade 55: 1014–33. [Google Scholar] [CrossRef]

- Hung, Dang, Manh Tran, and Thi Nguyen. 2018. Investigation of the impact of financial information on stock prices: The case of Vietnam. Academy of Accounting and Financial Studies Journal 22: 1–12. [Google Scholar]

- Huynh, Toan Luu Duc, Sang Phu Nguyen, and Duy Duong. 2018. Pricing assets with higher co-moments and value-at-risk by quantile regression approach: Evidence from Vietnam stock market. In Paper presented at the Econometrics for Financial Applications, Ho Chi Minh City, Vietnam, January 15–16. Cham: Springer. [Google Scholar]

- Huynh, Toan Luu Duc, Muhammad Ali Nasir, Sang Phu Nguyen, and Duy Duong. 2020. An assessment of contagion risks in the banking system using non-parametric and Copula approaches. Economic Analysis and Policy 65: 105–16. [Google Scholar] [CrossRef]

- International Monetary Fund. 2020. World Economic Outlook, April 2020: The Great Lockdown. Washington: International Monetary Fund, Available online: https://www.imf.org/en/Publications/WEO/Issues/2020/04/14/weo-april-2020 (accessed on 1 May 2021).

- Kabir, Rezaul, and Hanh Minh Thai. 2017. Does corporate governance shape the relationship between corporate social responsibility and financial performance? Pacific Accounting Review 29: 227–58. [Google Scholar] [CrossRef]

- Kallinterakis, Vasileios. 2007. Herding and the thin trading bias in a start-up market: Evidence from Vietnam. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Kasman, Adnan, and Saadet Kasman. 2016. Bank size, competition and risk in the Turkish banking industry. Empirica 43: 607–31. [Google Scholar] [CrossRef]

- Khoi, Phan Dinh, and Christopher Gan. 2016. Rural credit market and microfinance in Vietnam. In Microfinance in Asia. Singapore: World Scientific, pp. 23–46. [Google Scholar]

- Kopf, Dan. 2018. Vietnam Is the Most globalIzed Populous Country in Modern History. Available online: https://www.weforum.org/agenda/2018/10/vietnam-is-the-most-globalized-populous-country-in-modern-history/ (accessed on 1 May 2021).

- Kosmidou, Kyriaki, and Constantin Zopounidis. 2008. Measurement of bank performance in Greece. South-Eastern Europe Journal of Economics 6: 79–95. [Google Scholar]

- Le, Quoc Hoi. 2016. Foreign direct investment into real estate and macroeconomic instability in Vietnam. Afro-Asian J. of Finance and Accounting 6: 258. [Google Scholar] [CrossRef]

- Le, Thi Thuy Van. 2017. Xử lý nợ xấu ở Việt Nam: Thực trạng và những vấn đề đặt ra. Available online: https://www.mof.gov.vn/webcenter/portal/vclvcstc/r/m/ncvtd/ncvtd_chitiet?dDocName=MOFUCM108229&dID=112489&_afrLoop=9700893825530014 (accessed on 1 May 2021).

- Le, Tu. 2019. The interrelationship between liquidity creation and bank capital in Vietnamese banking. Managerial Finance 45: 331–47. [Google Scholar] [CrossRef]

- Le, Ngoc, and Thang Nguyen. 2009. The impact of networking on bank financing: The case of small and medium-sized enterprises in Vietnam. Entrepreneurship Theory and Practice 33. [Google Scholar] [CrossRef]

- Le, Thai-Ha, Anh Tu Chuc, and Farhad Taghizadeh-Hesary. 2019a. Financial inclusion and its impact on financial efficiency and sustainability: Empirical evidence from Asia. Borsa Istanbul Review 19: 310–22. [Google Scholar] [CrossRef]

- Le, Thi Tu Oanh, Thi Ngoc Bui, and Anh Tu Chuc. 2019b. Relationship between experts and enterprises viewed via the IFRS application: An empirical study in Vietnam. Asian Economic and Financial Review 9: 946–63. [Google Scholar] [CrossRef]

- Le, Thi Tu Oanh, Thi Ngoc Bui, and Anh Tu Chuc. 2019c. Benefits and difficulties of adopting IFRSS. Creativity and Innovation Management 10: 205. [Google Scholar]

- Le, Xuan Quynh, Ngoc Tien Nguyen, and Thy Ha Van Le. 2019d. The impact of corporate social responsibility on the cost of equity: An analysis of Vietnamese listed companies. Investment Management and Financial Innovations 16: 87–96. [Google Scholar] [CrossRef]

- Le, Minh, Viet-Ngu Hoang, Clevo Wilson, and Thanh Ngo. 2020a. Risk-adjusted efficiency and bank size in a developing economy: An analysis of Vietnamese banks. Journal of Economic Studies 47: 386–404. [Google Scholar] [CrossRef]

- Le, Minh, Viet-Ngu Hoang, Clevo Wilson, and Thanh Ngo. 2020b. The implication of applying IFRS in Vietnamese enterprises from an expert perspective. Management Science Letters, 551–64. [Google Scholar] [CrossRef]

- Lee, Yen Nee. 2021. This Is Asia’s Top-Performing Economy in the Covid pandemic—It’s Not China. Available online: https://www.cnbc.com/2021/01/28/vietnam-is-asias-top-performing-economy-in-2020-amid-covid-pandemic.html (accessed on 1 May 2021).

- Lee, Jeong Yeon, and Doyeon Kim. 2013. Bank performance and its determinants in Korea. Japan and the World Economy 27: 83–94. [Google Scholar] [CrossRef]

- Lensink, Robert, and Thi Thu Tra Pham. 2011. The impact of microcredit on self-employment profits in Vietnam. Economics of Transition 20: 73–111. [Google Scholar] [CrossRef]

- Linnenluecke, Martina K., Xiaoyan Chen, Xin Ling, Tom Smith, and Yushu Zhu. 2016. Emerging trends in Asia-Pacific finance research: A review of recent influential publications and a research Agenda. Pacific-Basin Finance Journal 36: 66–76. [Google Scholar] [CrossRef] [Green Version]

- Locus Bulletin. 2019. Vietnam Tops the Chart of the World’s Fastest-Growing Economies. Available online: https://locus.sh/resources/bulletin/vietnams-economic-growth/ (accessed on 1 May 2021).

- Luu, Hiep Ngoc, Loan Quynh Thi Nguyen, Quynh Huong Vu, and Quoc Tuan Le. 2019. Income diversification and financial performance of commercial banks in Vietnam. Review of Behavioral Finance 12: 185–99. [Google Scholar] [CrossRef]

- Merton, Robert C. 1974. On the pricing of corporate debt: The risk structure of interest rates. The Journal of Finance 29: 449–70. [Google Scholar]

- Ministry of Finance. 2017. Thu hút FDI hậu WTO: Tăng cao cả lượng và chất. Available online: https://mof.gov.vn/webcenter/portal/tttc/r/m/cochechinhsach/cochechinhsach_chitiet?dDocName=MOFUCM095331&dID=98672&_afrLoop=1223614006738808#%40%3FdID%3D98672%26_afrLoop%3D1223614006738808%26dDocName%3DMOFUCM095331%26_adf.ctrl-state%3Dwgp65cej8_4 (accessed on 1 May 2021).

- Morgan, Peter J., and Trinh Quang Long. 2020. Financial literacy, financial inclusion, and savings behavior in Laos. Journal of Asian Economics 68: 101197. [Google Scholar] [CrossRef]

- Ngo, Thanh, and David Tripe. 2017. Measuring efficiency of Vietnamese banks. Pacific Accounting Review 29: 171–82. [Google Scholar] [CrossRef]

- Nguyen, Tho. 2011. US macroeconomic news spillover effects On Vietnamese stock market. The Journal of Risk Finance 12: 389–99. [Google Scholar] [CrossRef]

- Nguyen, Chu V. 2015a. The Vietnamese lending rate, policy-related rate, and monetary policy post-1997 Asian Financial Crisis. Cogent Economics & Finance 3: 1007808. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, Nhung. 2015b. Credit Accessibility and Small and Medium Sized Enterprises Growth in Vietnam. Doctoral dissertation, Lincoln University, Lincoln, New Zealand. [Google Scholar]

- Nguyen, Ngoc Thuy. 2017a. Crowdfunding in Vietnam: The Impact of Project and Founder Quality on Funding Success. Master’s thesis, University of Twente, Enschede, The Netherlands. [Google Scholar]

- Nguyen, V. Chu. 2017b. Asymmetries in responses of commercial banks to monetary policy: The case of Thailand. Southeast Asia Review Of Economics and Business 1: 10–12. [Google Scholar]

- Nguyen, Ngoc. 2019. Revenue diversification, risk and bank performance of Vietnamese commercial banks. Journal of Risk and Financial Management 12: 138. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, Huy Hoang. 2020. Việt Nam: Ước tính xuất siêu kỷ lục 19.1 tỷ USD năm 2020, cao nhất trong 5 năm qua. Available online: https://commoditytrading.vn/viet-nam-uoc-tinh-xuat-sieu-ky-luc-19-1-ty-usd-nam-2020-cao-nhat-trong-5-nam-qua/ (accessed on 1 May 2021).

- Nguyen, Dat. 2021. VN-Index Hits New Peak as Trading Value Surges. Available online: https://e.vnexpress.net/news/business/economy/vn-index-hits-new-peak-as-trading-value-surges-4260081.html (accessed on 1 May 2021).

- Nguyen, Thi Thanh Phuong, and Ngoc Hung Dang. 2020. Impact Of corporate governance on corporate value: Research in Vietnam. Research in World Economy 11: 161–70. [Google Scholar] [CrossRef]

- Nguyen, Minh Ha, and Minh Tai Le. 2017. Impact of capital structure and cash holdings on firm value: Case of firms listed on the Ho Chi Minh stock exchange. International Journal of Economics and Financial Issues 7: 24–30. [Google Scholar]

- Nguyen, An Khoa Truong, and Khuong Mai Ngoc. 2020. Building a Conceptual Framework of Corporate Social Responsibility: An Experience of Qualitative Approach in Vietnam. Journal of Asia-Pacific Business 21: 39–56. [Google Scholar] [CrossRef]

- Nguyen, Hieu Thanh, and Anh Huu Nguyen. 2020a. The Impact of capital structure on firm performance: Evidence from Vietnam. The Journal of Asian Finance, Economics and Business 7: 97–105. [Google Scholar] [CrossRef]

- Nguyen, Thanh Hieu, and Anh Huu Nguyen. 2020b. Capital structure and firm performance of non-financial listed companies: Cross-sector empirical evidences from Vietnam. Accounting 6: 137–50. [Google Scholar] [CrossRef]

- Nguyen, Phong Hoang, and Duyen Thi Bich Pham. 2020. The cost efficiency of Vietnamese banks—The difference between DEA and SFA. Journal of Economics and Development 22: 209–27. [Google Scholar] [CrossRef]

- Nguyen, Minh Ha, and Hiep Phan. 2019. The effect of institutional ownership on listed companies’ performance in Vietnam. International Journal of Economics and Business Research 17: 317. [Google Scholar] [CrossRef]

- Nguyen, Lisa-Uyen, and Asheq Rahman. 2019. From totalitarianism to capitalism—The case of IFRS adoption in Vietnam. Accounting & Finance 59: 1649–80. [Google Scholar] [CrossRef]

- Nguyen, Thi Nhung, and Thi Van Anh Tran. 2019. Has merger and acquisition been considered as a method of dealing with weak banks? Evidence from the third bank restructuring process in Vietnam. Banks and Bank Systems 14: 193–210. [Google Scholar] [CrossRef]

- Nguyen, Xuan-Hung, and Hiep-Thien Trinh. 2020. Corporate social responsibility and the non-linear effect on audit opinion for energy firms in Vietnam. Cogent Business & Management 7: 1757841. [Google Scholar] [CrossRef]

- Nguyen, Tuan, Stuart Locke, and Krishna Reddy. 2015. Ownership concentration and corporate performance from a dynamic perspective: Does national governance quality matter? International Review of Financial Analysis 41: 148–61. [Google Scholar] [CrossRef]

- Nguyen, V. Chu, LeBon Caroline, Miller Stephen, and B. Lloyd Cynthia. 2017a. The Russian landing rate, central bank’s policy related rate and intermediation premium. Journal of Eastern European and Central Asian Research (JEECAR) 4. [Google Scholar] [CrossRef]

- Nguyen, Vinh, Anh Tran, and Richard Zeckhauser. 2017b. Stock splits to profit insider trading: Lessons from an emerging Market. Journal of International Money and Finance 74: 69–87. [Google Scholar] [CrossRef]

- Nguyen, Danh, Thanh Ngo, Ron Nguyen, Huy Cao, and Huy Pham. 2019a. Corporate social responsibility, balanced scorecard system and financial performance in the service sector: The case of Vietnam. Management Science Letters 9: 2215–28. [Google Scholar] [CrossRef]

- Nguyen, Hang Thu, Thuy Thu Nguyen, Xuan Le Phuong Dang, and Hiep Manh Nguyen. 2019b. Informal financing choice In SMEs: Do the types of formal credit constraints matter? Journal of Small Business & Entrepreneurship, 1–20. [Google Scholar] [CrossRef]

- Nguyen, Lan Thanh, Jen-Je Su, and Parmendra Sharma. 2019c. SME credit constraints In Asia’s rising economic star: Fresh empirical evidence from Vietnam. Applied Economics 51: 3170–83. [Google Scholar] [CrossRef]

- Nguyen, To Hong-Kong, To Viet-Ha Nguyen, Thu-Trang Vuong, Manh-Tung Ho, and Quan-Hoang Vuong. 2019d. The new politics of debt In the transition economy of Vietnam. Austrian Journal of South-East Asian Studies 12: 91–110. [Google Scholar] [CrossRef]

- Nguyen, Hang Thu, Hiep Manh Nguyen, Michael Troege, and Anh T. H. Nguyen. 2020a. Debt aversion, education, and credit self-rationing in SMEs. Small Business Economics. [Google Scholar] [CrossRef]

- Nguyen, Thai Vu Hong, Tra Thi Thu Pham, Canh Phuc Nguyen, Thanh Cong Nguyen, and Binh Thanh Nguyen. 2020b. Excess liquidity and net interest margins: Evidence from Vietnamese banks. Journal of Economics and Business 110: 105893. [Google Scholar] [CrossRef]

- Nguyen, Tran Thai Ha, Massoud Moslehpour, Thi Thuy Van Vo, and Wing-Keung Wong. 2020c. State ownership and risk-taking behavior: An empirical approach to get better profitability, investment, and trading strategies for listed corporates in Vietnam. Economies 8: 46. [Google Scholar] [CrossRef]

- Nguyen, Minh-Hoang, Thanh-Hang Pham, Manh-Toan Ho, Huyen Thanh T. Nguyen, and Quan-Hoang Vuong. 2021a. On the social and conceptual structure of the 50-year research landscape in entrepreneurial finance. SN Business & Economics 1: 2. [Google Scholar] [CrossRef]

- Nguyen, Minh-Hoang, Le Tam-Tri, Nguyen T. Hong-Kong, Ho Manh-Toan, Nguyen T. Thanh-Huyen, and Vuong Quan-Hoang. 2021b. Alice in Suicideland: Exploring the Suicidal Ideation Mechanism through the Sense of Connectedness and Help-Seeking Behaviors. International Journal of Environmental Research and Public Health 18: 3681. [Google Scholar] [CrossRef]

- Nisar, Shoaib, Ke Peng, Susheng Wang, and Badar Ashraf. 2018. The impact of revenue diversification on bank profitability and stability: Empirical evidence From South Asian countries. International Journal of Financial Studies 6: 40. [Google Scholar] [CrossRef] [Green Version]

- Pham, Thi Hoang Anh. 2017. Are global shocks leading indicators of currency crisis In Viet Nam? Research in International Business and Finance 42: 605–15. [Google Scholar] [CrossRef] [Green Version]

- Pham, Tra, and Robert Lensink. 2008. The Determinants of Loan Contracts to Business Firms: Empirical Evidence from a Private Bank in Vietnam. London: Palgrave Macmillan, pp. 229–64. [Google Scholar]

- Pham, Tho, and Oleksandr Talavera. 2018. Discrimination, social capital, and financial constraints: The case Of Vietnam. World Development 102: 228–42. [Google Scholar] [CrossRef] [Green Version]

- Pham, Thach Ngoc, Vuong Minh Nguyen, and Duc Hong Vo. 2018a. The Cross-section of expected stock returns: New evidence from an emerging market. Emerging Markets Finance and Trade 54: 3566–76. [Google Scholar] [CrossRef]

- Pham, Thi Thu Tra, Thai Vu Hong Nguyen, and Kien Son Nguyen. 2018b. Does bank competition promote financial inclusion? A cross-country evidence. Applied Economics Letters 26: 1133–37. [Google Scholar] [CrossRef]

- Phan, Duc Hong Thi. 2014. What factors are perceived to influence consideration of IFRS adoption by Vietnamese policymakers? Journal of Contemporary Issues in Business and Government 20: 27. [Google Scholar] [CrossRef]

- Phan, Quynh Trang. 2018. Corporate debt and investment with financial constraints: Vietnamese listed firms. Research in International Business and Finance 46: 268–80. [Google Scholar] [CrossRef]

- Phan, Duc Hong Thi, and Bruno Mascitelli. 2014. Optimal approach and timeline for IFRS adoption in Vietnam: Perceptions from accounting professionals. Research in Accounting Regulation 26: 222–29. [Google Scholar] [CrossRef]

- Phan, Duc, Mahesh Joshi, and Bruno Mascitelli. 2018. What influences the willingness of Vietnamese accountants to adopt International Financial Reporting Standards (IFRS) by 2025? Asian Review of Accounting 26: 225–47. [Google Scholar] [CrossRef]

- Phan, Chung Thanh, Sizhong Sun, Zhang-Yue Zhou, and Rabiul Beg. 2019. Does microcredit increase household food consumption? A study of rural Vietnam. Journal of Asian Economics 62: 39–51. [Google Scholar] [CrossRef]

- Phan, Chung Thanh, Sizhong Sun, Zhang-Yue Zhou, and Rabiul Beg. 2020a. Does microcredit improve rural households’ social network? Evidence from Vietnam. The Journal of Development Studies 56: 1947–63. [Google Scholar] [CrossRef]

- Phan, Dinh Hoang Bach, Paresh Kumar Narayan, R. Eki Rahman, and Akhis R. Hutabarat. 2020b. Do financial technology firms influence bank performance? Pacific-Basin Finance Journal 62: 101210. [Google Scholar] [CrossRef]

- PL. 2020. Thu hút FDI 8 tháng: Vốn giải ngân và đăng ký đều “hụt hơi”. Available online: https://thoibaonganhang.vn/thu-hut-fdi-8-thang-von-giai-ngan-va-dang-ky-deu-hut-hoi-105783.html (accessed on 1 May 2021).

- Poon, Jessie P. H, and Diep T. Thai. 2010. Micro-credit and development in northern vietnam. Geografiska Annaler: Series B, Human Geography 92: 65–79. [Google Scholar] [CrossRef]

- Revell, Jack. 1982. The OECD report on costs and margins in banking. In Bank Management in a Changing Domestic and International Environment: The Challenges of the Eighties. Edited by Donald E. Fair and François Léonard de Juvigny. Dordrecht: Springer, pp. 287–99. [Google Scholar]

- Saghi-Zedek, Nadia. 2016. Product diversification and bank performance: Does ownership structure matter? Journal of Banking & Finance 71: 154–67. [Google Scholar] [CrossRef]

- Sanya, Sarah, and Simon Wolfe. 2010. Can banks in emerging economies benefit from revenue diversification? Journal of Financial Services Research 40: 79–101. [Google Scholar] [CrossRef] [Green Version]

- Sawada, Michiru. 2013. How does the stock market value bank diversification? Empirical evidence from Japanese banks. Pacific-Basin Finance Journal 25: 40–61. [Google Scholar] [CrossRef] [Green Version]

- Stiroh, Kevin J., and Adrienne Rumble. 2006. The dark side of diversification: The case of US financial holding companies. Journal of Banking & Finance 30: 2131–61. [Google Scholar] [CrossRef]

- Teixeira da Silva, Jaime A., and Quan-Hoang Vuong. 2021. The right to refuse unwanted citations: Rethinking the culture of science around the citation. Scientometrics. [Google Scholar] [CrossRef]

- Thu Phuong. 2019. Giải ngân vốn FDI năm 2019 đạt kỷ lục. Available online: https://congthuong.vn/giai-ngan-von-fdi-nam-2019-dat-ky-luc-130612.html (accessed on 1 May 2021).

- Tran, Thi Bich Ngoc. 2017. Speculative bubbles in emerging stock markets and macroeconomic factors: A new empirical evidence for Asia and Latin America. Research in International Business and Finance 42: 454–67. [Google Scholar] [CrossRef]

- Tran, Quoc Trung. 2020. Foreign ownership and investment efficiency: New evidence from an emerging market. International Journal of Emerging Markets 15: 1185–99. [Google Scholar] [CrossRef]

- Tran, Nam Hoai, and Chi Dat Le. 2017. Financial conditions and corporate investment: Evidence from Vietnam. Pacific Accounting Review 29: 183–203. [Google Scholar] [CrossRef]

- Tran, Nam Hoai, and Chi Dat Le. 2020. Ownership concentration, corporate risk-taking and performance: Evidence from Vietnamese listed firms. Cogent Economics & Finance 8: 1732640. [Google Scholar] [CrossRef]

- Tran, Thi Thanh Tu, and Thi Hoang Yen Tran. 2015. Green bank: International experiences and Vietnam perspectives. Asian Social Science. [Google Scholar] [CrossRef]

- Tran, Ngo My, and Huy Huynh Truong. 2011. Herding behaviour in an emerging stock market: Empirical evidence from Vietnam. Research Journal of Business Management 5: 51–76. [Google Scholar] [CrossRef]

- Tran, Minh Tam, Minh Quang Le, Thi Khuyen Le, and Phu Thanh Ngo. 2019a. Earnings quality: Does state ownership matter? Evidence from Vietnam. In Paper presented at the Beyond Traditional Probabilistic Methods in Economics, 14–16 January, Ho Chi Minh City, Vietnam. Cham: Springer. [Google Scholar]

- Tran, Trung, Tien Trung Nguyen, Thi Phuong Thao Trinh, and Thi Thu Hien Le. 2019b. Impact of micro-credit on child education in Vietnam: Parametric and non-parametric approaches. Asian Journal of Scientific Research 12: 249–55. [Google Scholar] [CrossRef]

- Tuan, Luu. 2014. From corporate governance to balanced performance measurement. Knowledge Management Research & Practice 12. [Google Scholar] [CrossRef]

- Van, Loan Thi-Hong, Anh The Vo, Nhan Thien Nguyen, and Duc Hong Vo. 2019. Financial inclusion and economic growth: An international evidence. Emerging Markets Finance and Trade 57: 239–63. [Google Scholar] [CrossRef]

- Vietnam Government Portal. 2020. Về việc phê duyệt Chiến lược tài chính toàn diện quốc gia đến năm 2025, định hướng đến năm 2030. Available online: http://www2.chinhphu.vn/portal/page/portal/chinhphu/noidungchienluocphattrienkinhtexahoi?_piref33_14725_33_14721_14721.strutsAction=ViewDetailAction.do&_piref33_14725_33_14721_14721.docid=5014&_piref33_14725_33_14721_14721.substract= (accessed on 1 May 2021).

- Vo, Xuan Vinh. 2016. Foreign ownership and stock market liquidity—Evidence from Vietnam. Afro-Asian Journal of Finance and Accounting 6: 1. [Google Scholar] [CrossRef]

- Vo, Xuan Vinh. 2017a. Do foreign investors improve stock price informativeness in emerging equity markets? Evidence from Vietnam. Research in International Business and Finance 42: 986–91. [Google Scholar] [CrossRef]

- Vo, Xuan Vinh. 2017b. Trading of foreign investors and stock returns in an emerging market—Evidence from Vietnam. International Review of Financial Analysis 52: 88–93. [Google Scholar] [CrossRef]

- Vo, Dinh-Tri. 2020. Dependency on FDI inflows and stock market linkages. Finance Research Letters 38: 101463. [Google Scholar] [CrossRef]

- Vo, Xuan Vinh, and Hong Thu Bui. 2016. Liquidity, liquidity risk and stock returns: Evidence from Vietnam. International Journal of Monetary Economics and Finance 9: 67. [Google Scholar] [CrossRef]

- Vo, Xuan Vinh, and Craig Ellis. 2017. An empirical investigation of capital structure and firm value in Vietnam. Finance Research Letters 22: 90–94. [Google Scholar] [CrossRef]

- Vo, Xuan Vinh, and Phuc Canh Nguyen. 2014. Monetary policy and bank credit risk in Vietnam pre and post Global Financial Crisis. In Risk Management Post Financial Crisis: A Period of Monetary Easing. Bingley: Emerald Group Publishing Limited, pp. 277–90. [Google Scholar]

- Vo, Xuan Vinh, and Huu Huan Nguyen. 2018. Bank restructuring and bank efficiency—The case of Vietnam. Cogent Economics & Finance 6: 1520423. [Google Scholar] [CrossRef] [Green Version]

- Vo, Anh The, Loan Thi-Hong Van, Duc Hong Vo, and Michael McAleer. 2019. Financial inclusion and macroeconomic stability in emerging and frontier markets. Annals of Financial Economics 14: 1950008. [Google Scholar] [CrossRef] [Green Version]

- Vu, Thi-Hanh, Van-Duy Nguyen, Manh-Tung Ho, and Quan-Hoang Vuong. 2019. Determinants of Vietnamese listed firm performance: Competition, wage, CEO, firm size, age, and international trade. Journal of Risk and Financial Management 12: 62. [Google Scholar] [CrossRef] [Green Version]

- Vuong, Quan- Hoang. 2016. Global mindset as the integration of emerging socio-cultural values through mindsponge processes: A transition economy perspective. In Global Mindsets: Exploration and Perspectives. Edited by John Kuada. London: Routledge, pp. 109–26. [Google Scholar]

- Vuong, Quan-Hoang. 2018. The (ir)rational consideration of the cost of science in transition economies. Nature Human Behaviour 2: 5. [Google Scholar] [CrossRef]

- Vuong, Quan-Hoang. 2019a. The financial economy of Viet Nam in an age of reform, 1986–2016. In Routledge Handbook of Banking and Finance in Asia. Edited by Ulrich Volz, Peter Morgan and Naoyuki Yoshino. London: Routledge, pp. 201–22. [Google Scholar]

- Vuong, Quan-Hoang. 2019b. Breaking barriers in publishing demands a proactive attitude. Nature Human Behaviour 3: 1034–34. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Vuong, Quan-Hoang. 2020. Reform retractions to make them more transparent. Nature 582: 149. [Google Scholar] [CrossRef]

- Vuong, Quan-Hoang. 2021. The semiconducting principle of monetary and environmental values exchange. Economics and Business Letters 10: 1–9. [Google Scholar]

- Vuong, Quan Hoang, and Nancy K Napier. 2015. Acculturation and global mindsponge: An emerging market perspective. International Journal of Intercultural Relations 49: 354–67. [Google Scholar] [CrossRef]

- Vuong, Quan-Hoang, and Tri Dung Tran. 2009. The cultural dimensions of the Vietnamese private entrepreneurship. IUP Journal of Entrepreneurship Development 6: 54–78. [Google Scholar] [CrossRef] [Green Version]

- Vuong, Quan Hoang, Thu Hang Do, and Thu Trang Vuong. 2016. Resources, experience, and perseverance in entrepreneurs’ perceived likelihood of success in an emerging economy. Journal of Innovation and Entrepreneurship 5. [Google Scholar] [CrossRef] [Green Version]

- Vuong, Quan Hoang. 2016a. Survey data on entrepreneurs׳ subjective plan and perceptions of the likelihood of success. Data in Brief 6: 858–64. [Google Scholar] [CrossRef]

- Vuong, Quan Hoang. 2016b. Impacts of geographical locations and sociocultural traits on the Vietnamese entrepreneurship. SpringerPlus 5: 1189. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Vuong, Quan-Hoang, Quang-Khiem Bui, Viet-Phuong La, Thu-Trang Vuong, Viet-Ha T. Nguyen, Manh-Toan Ho, Hong-Kong T. Nguyen, and Manh-Tung Ho. 2018a. Cultural additivity: Behavioural insights from the interaction of Confucianism, Buddhism and Taoism in folktales. Palgrave Communications 4: 143. [Google Scholar] [CrossRef] [Green Version]

- Vuong, Quan-Hoang, Viet-Phuong La, Thu-Trang Vuong, Manh-Toan Ho, Hong-Kong T. Nguyen, Viet-Ha Nguyen, Hiep-Hung Pham, and Manh-Tung Ho. 2018b. An open database of productivity in Vietnam’s social sciences and humanities for public use. Scientific Data 5: 180188. [Google Scholar] [CrossRef]

- Vuong, Quan-Hoang, Quang-Khiem Bui, Viet-Phuong La, Thu-Trang Vuong, Manh-Toan Ho, Hong-Kong T. Nguyen, Hong-Ngoc Nguyen, Kien-Cuong P. Nghiem, and Manh-Tung Ho. 2019. Cultural evolution in Vietnam’s early 20th century: A Bayesian networks analysis of Hanoi Franco-Chinese house designs. Social Sciences & Humanities Open 1: 100001. [Google Scholar] [CrossRef]

- Vuong, Quan-Hoang, Manh-Tung Ho, Hong-Kong T. Nguyen, Thu-Trang Vuong, Trung Tran, Khanh-Linh Hoang, Thi-Hanh Vu, Phuong-Hanh Hoang, Minh-Hoang Nguyen, Manh-Toan Ho, and et al. 2020a. On how religions could accidentally incite lies and violence: Folktales as a cultural transmitter. Palgrave Communications 6: 82. [Google Scholar] [CrossRef]

- Vuong, Quan-Hoang, Viet-Phuong La, Hong Kong Nguyen, Tung Ho, Thu-Trang Vuong, and Toan Ho. 2020b. Identifying the moral-practical gaps in corporate social responsibility missions of Vietnamese firms: An event-based analysis of sustainability feasibility. Corporate Social Responsibility and Environmental Management 28: 30–41. [Google Scholar] [CrossRef]

- Vuong, Quan-Hoang, Anh-Vinh Le, Viet-Phuong La, Phuong-Hanh Hoang, and Manh-Toan Ho. 2020c. Making social sciences more scientific: Literature review by structured data. MethodsX 7: 100818. [Google Scholar] [CrossRef]

- Vuong, Quan Hoang, Viet Phuong La, Thu Trang Vuong, Phuong Hanh Hoang, Manh Toan Ho, Manh Tung Ho, and Hong Kong To Nguyen. 2020d. Multi-faceted insights of entrepreneurship facing a fast-growing economy: A literature review. Open Economics 3: 25–41. [Google Scholar] [CrossRef] [Green Version]

- Vuong, Quan Hoang, Nguyen Minh Hoang, Pham Thanh Hang, Ho Manh Toan, and Nguyen Thanh Thanhh Huyen. 2021. Assessing the ideological homogeneity in entrepreneurial finance research by highly cited publications. Humanities and Social Sciences Communications 8. [Google Scholar] [CrossRef]

- Wonglimpiyarat, Jarunee. 2017. FinTech crowdfunding of Thailand 4.0 plicy. The Journal of Private Equity 21: 55. [Google Scholar] [CrossRef]

- World Bank. 2020. The Global Economic Outlook During the COVID-19 Pandemic: A Changed World. Available online: https://www.worldbank.org/en/news/feature/2020/06/08/the-global-economic-outlook-during-the-covid-19-pandemic-a-changed-world (accessed on 1 May 2021).

- World Bank. 2021. GDP (Current US$)—Vietnam. Available online: https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=VN&fbclid=IwAR0RFCQwdCE3Zm1P17H-SZ5l20NJ6UhqE_N1OVSLeMOwEPPPwE5g4UUfTfE (accessed on 1 May 2021).

- Zaim, Osman. 1995. The effect of financial liberalization on the efficiency of Turkish commercial banks. Applied Financial Economics 5: 257–64. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

| 1 | Economics |

| 2 | Business |

| 3 | Management |

| 4 | Education |

| 5 | Law |

| 6 | Agriculture |

| 7 | Environment/Sustainability Science |

| 8 | Sociology |

| 9 | Political Science |

| 10 | Logistics |

| 11 | Law |

| 12 | Healthcare |

| 13 | Geography |

| 14 | Urban Studies |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ho, M.-T.; Le, N.-T.B.; Tran, H.-L.D.; Nguyen, Q.-H.; Pham, M.-H.; Ly, M.-H.; Ho, M.-T.; Nguyen, M.-H.; Vuong, Q.-H. A Systematic and Critical Review on the Research Landscape of Finance in Vietnam from 2008 to 2020. J. Risk Financial Manag. 2021, 14, 219. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050219

Ho M-T, Le N-TB, Tran H-LD, Nguyen Q-H, Pham M-H, Ly M-H, Ho M-T, Nguyen M-H, Vuong Q-H. A Systematic and Critical Review on the Research Landscape of Finance in Vietnam from 2008 to 2020. Journal of Risk and Financial Management. 2021; 14(5):219. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050219

Chicago/Turabian StyleHo, Manh-Tung, Ngoc-Thang B. Le, Hung-Long D. Tran, Quoc-Hung Nguyen, Manh-Ha Pham, Minh-Hoang Ly, Manh-Toan Ho, Minh-Hoang Nguyen, and Quan-Hoang Vuong. 2021. "A Systematic and Critical Review on the Research Landscape of Finance in Vietnam from 2008 to 2020" Journal of Risk and Financial Management 14, no. 5: 219. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050219