Short-Term Capital Flows, Exchange Rate Expectation and Currency Internationalization: Evidence from China

Abstract

:1. Introduction

2. Literature Review

3. Models and Theoretical Analysis

3.1. Interaction of RMB Exchange Rate Expectation and RMB Internationalization

3.2. Interaction of RMB Internationalization and Short-Term Capital Flows

4. Data Description

5. Empirical Results

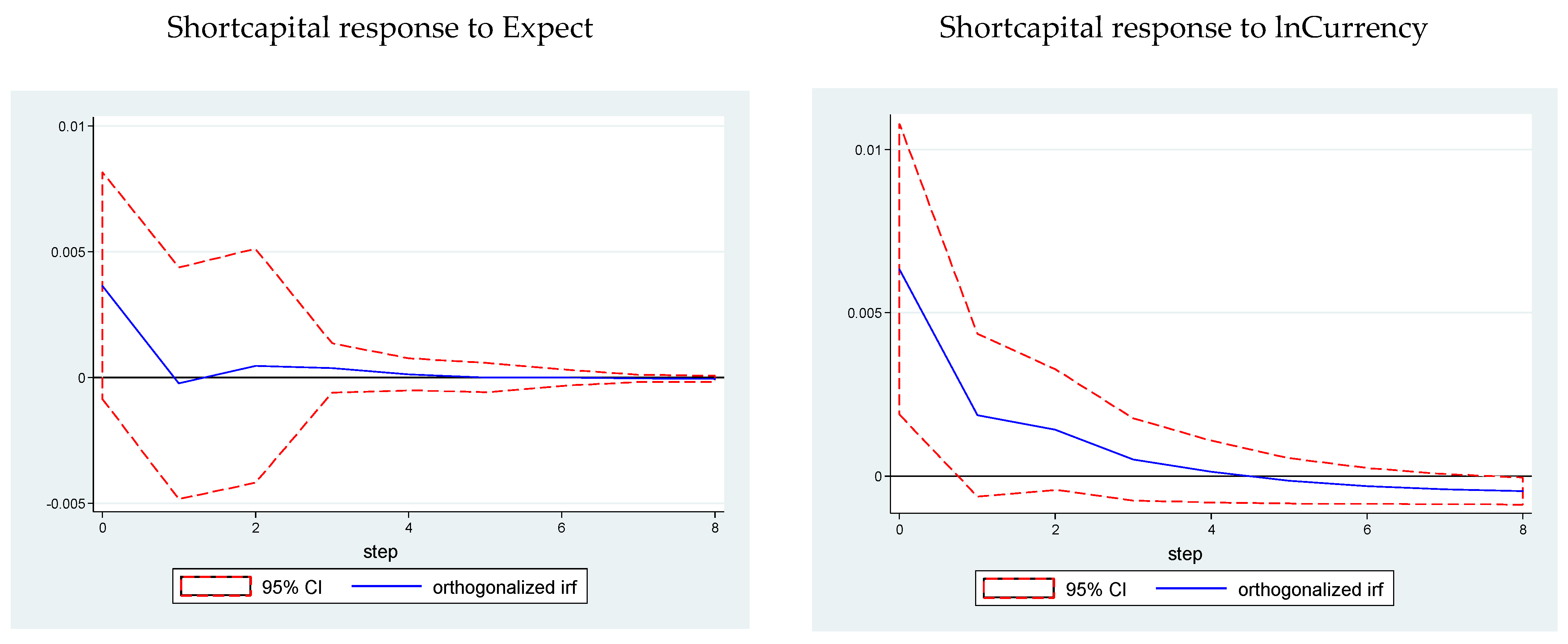

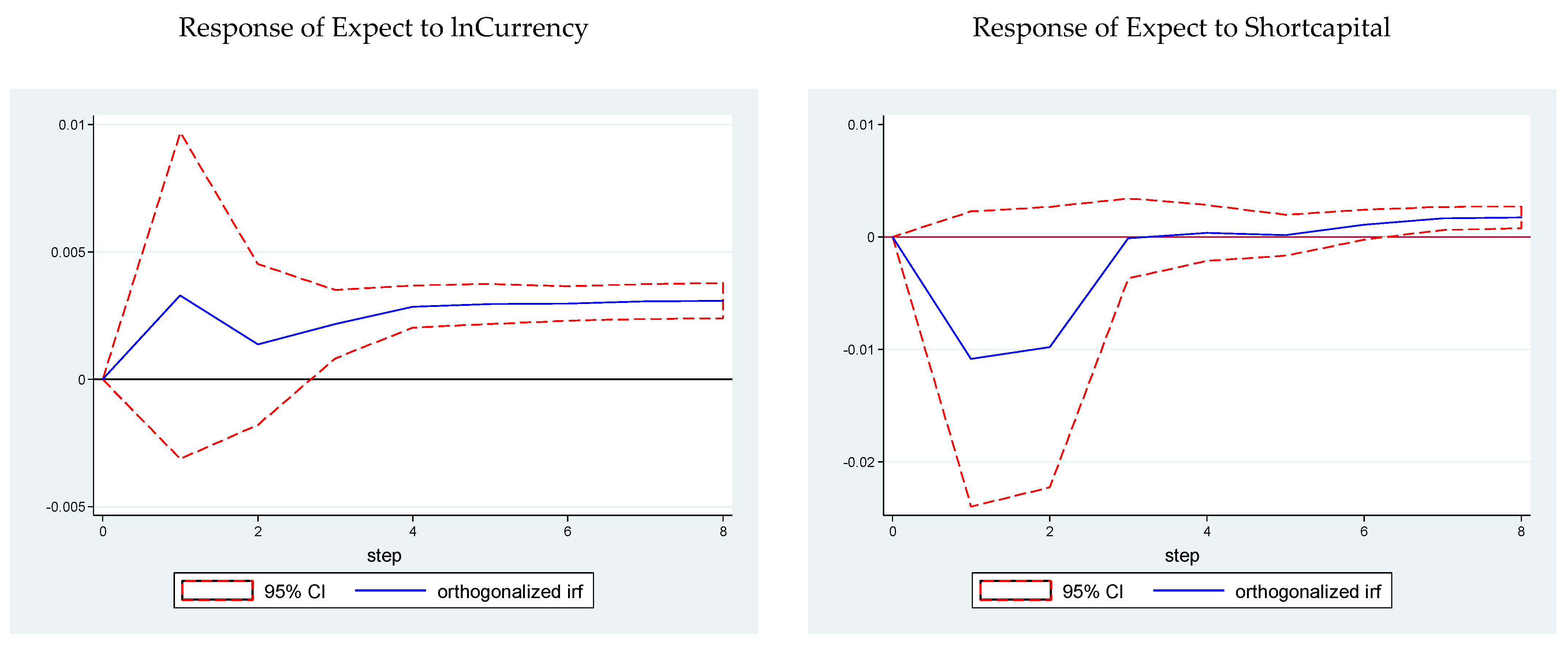

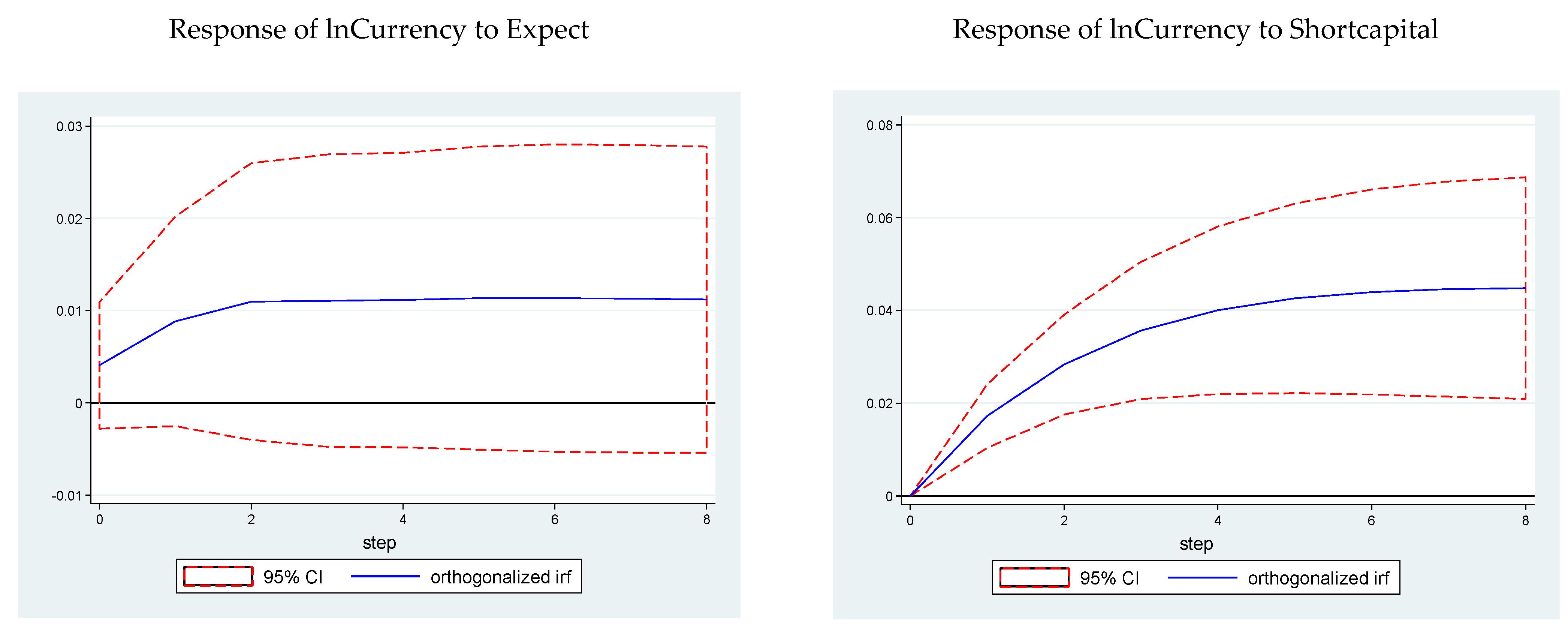

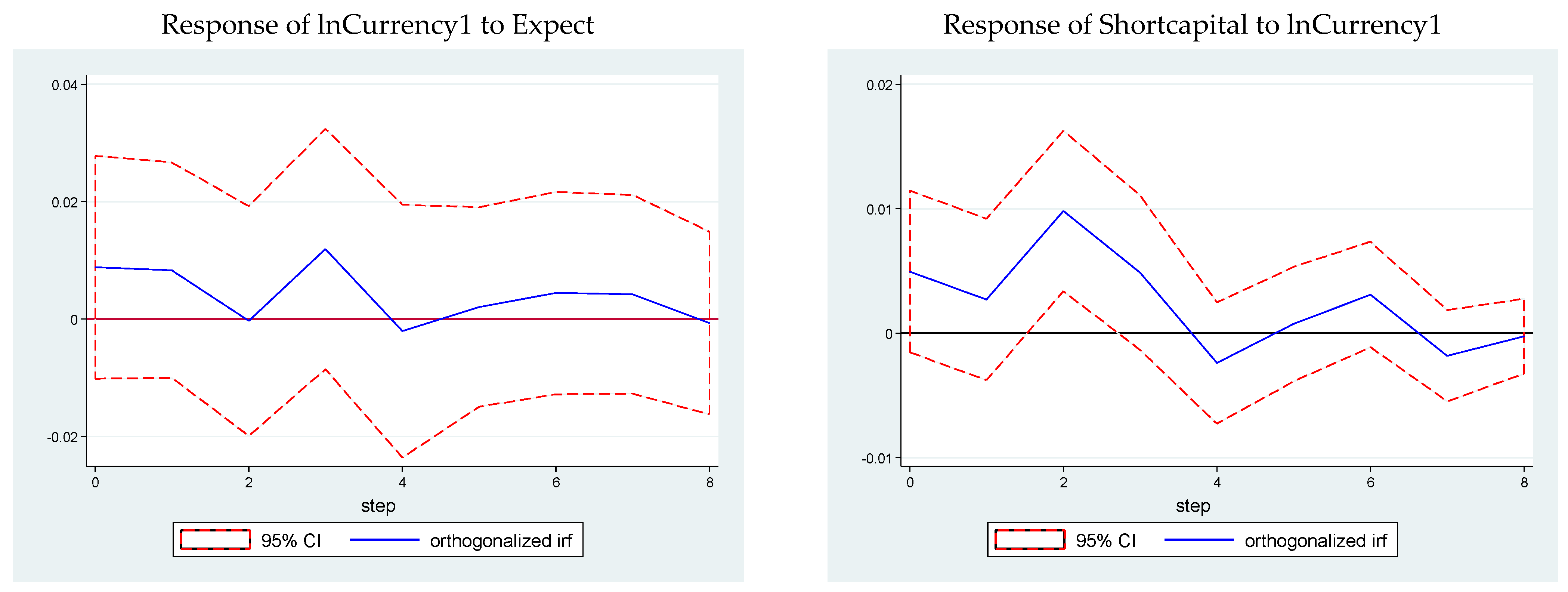

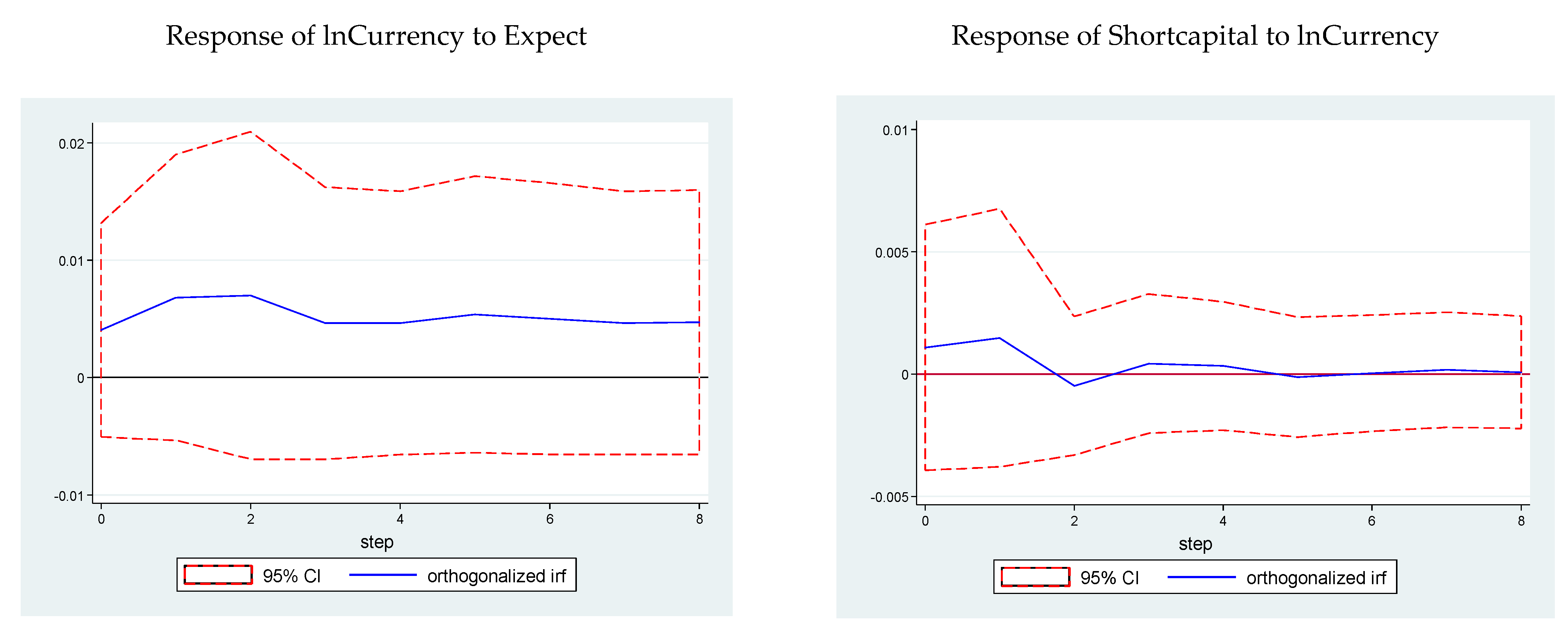

5.1. Impulse Response Effect Analysis

5.2. Variance Decomposition

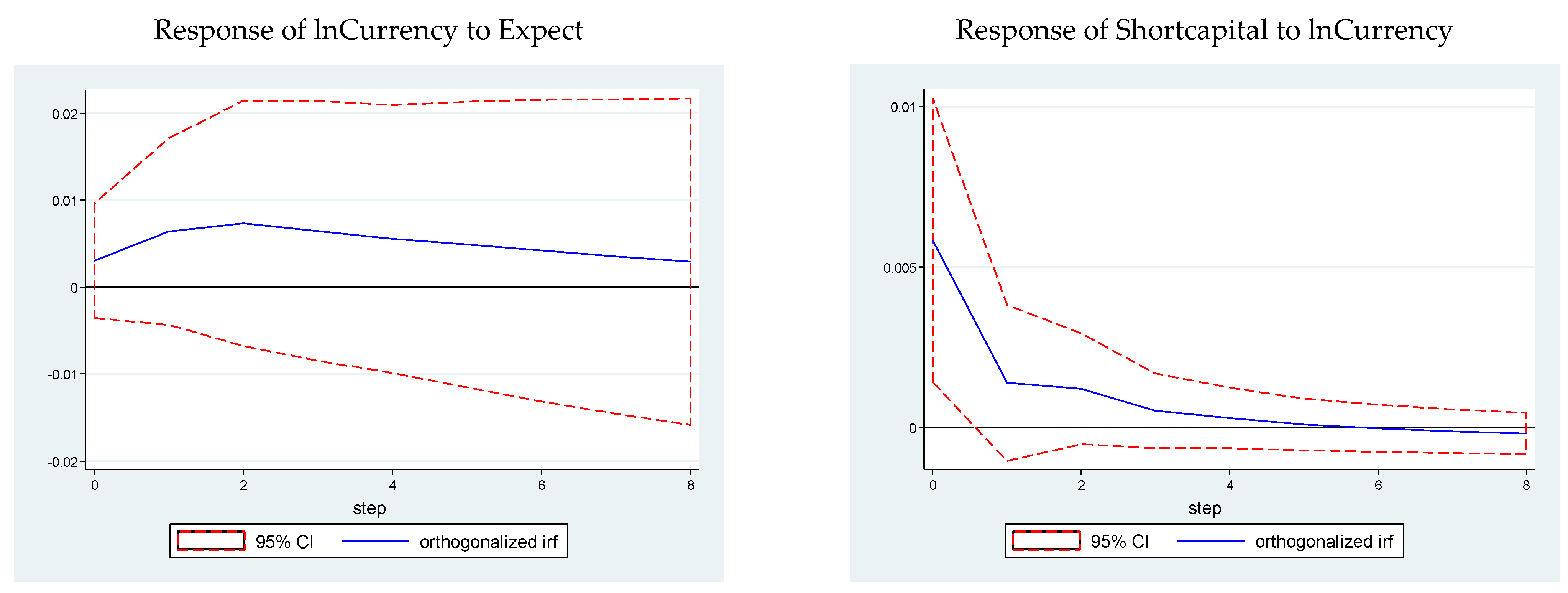

5.3. Robustness Checks

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Adebiyi, Adebayo Michael. 2005. Broad Money Demand, Financial Liberalization and Currency Substitution. Paper presented at 8th Capital Markets Conference, Indian Institute of Capital Markets Paper, Paris, France, July 8–13. [Google Scholar]

- Bouvatier, Vincent. 2010. Hot Money Inflows and Monetary Stability in China: How the People’s Bank of China Took up the Challenge. Applied Economics 42: 1533–48. [Google Scholar] [CrossRef]

- Chen, Lang Nan, and Chen Yun. 2009. RMB Nominal Exchange Rate, Asset Price and Short-term International Capital Flows. Journal of Economic Management 1: 1–6. [Google Scholar]

- Cohen, Benjamin J. 1971. The Future of Sterling as an International Currency. London: Macmillan. [Google Scholar]

- Cohen, Benjamin J. 2012. The Yuan Tomorrow? Evaluating China’s Currency Internationalization Strategy. New Political Economy 17: 361–71. [Google Scholar] [CrossRef]

- Combes, Jean-Louis, Tidiane Kinda, and Patrick Plane. 2012. Capital Flows, Exchange Rate Flexibility, and the Real Exchange Rate. Journal of Macroeconomics 34: 1034–43. [Google Scholar] [CrossRef] [Green Version]

- Cuddington, John T. 1983. Currency Substitution, Capital Mobility and Money Demand. Journal of International Money and Finance 2: 111–33. [Google Scholar] [CrossRef] [Green Version]

- Eichengreen, Barry. 2011. The renminbi as an international currency. Journal of Policy Modeling 33: 723–30. [Google Scholar] [CrossRef]

- Fang, Xianming, Ping Pei, and Yihao Zhang. 2012. Motivation and Effects of International Speculative Capital Inflow: Empirical Tests Based on Sample Data from 1999 to 2011. Journal of Financial Research 1: 65–77. [Google Scholar]

- Frankel, Jeffrey. 2012. Internationalization of the RMB and Historical Precedents. Journal of Economic Integration 3: 329–65. [Google Scholar] [CrossRef] [Green Version]

- Garber, Peter. 2011. What Drives CNH Market Equilibrium. Beijing: China Development Research Foundation. [Google Scholar]

- Genberg, Hans. 2009. Currency Internationalization: Analytical and Policy Issues. Hong Kong: Hong Kong Institute for Monetary Research Working Paper No. 31. [Google Scholar]

- Girton, Lance, and Dale W. Henderson. 1976. Central Bank Operations in Foreign and Domestic Assets under Fixed and Flexible Exchange Rates. Washington, DC: Board of Governors of the Federal Reserve System. [Google Scholar]

- Girton, Lance, and Don Roper. 1981. Theory and Implications of Currency Substitution. Journal of Money, Credit and Banking 13: 12–30. [Google Scholar] [CrossRef] [Green Version]

- Guo, Lianqiang, and Guoping Zhu. 2012. New Characteristics and Risk Aversion of Short-term Capital Flow in the Process of RMB Internationalization. Social Science Front 12: 47–50. [Google Scholar]

- Golley, Jane, and Rod Tyers. 2007. China’s Real Exchange Rate Puzzle. College of Business and Economics. Working Paper No. 479. Canberra: Austrilian National University. [Google Scholar]

- Hellmann, Thomas F., Kevin C. Murdock, and Joseph E. Stiglitz. 1994. Addressing Moral Hazard in Banking: Deposit Rate Controls vs. Capital Requirements. Working Paper No. 12. Unpublished manuscript. [Google Scholar]

- Ho, Kin-Yip, Yanlin Shi, and Zhaoyong Zhang. 2017. Does news matter in China’s foreign exchange market? Chinese RMB volatility and public information arrivals. International Review of Economics & Finance 52: 302–21. [Google Scholar]

- Ho, Kin-Yip, Yanlin Shi, and Zhaoyong Zhang. 2018. Public Information Arrival, Price Discovery and Dynamic Correlations in the Chinese Renminbi Markets. The North American Journal of Economics and Finance 46: 168–86. [Google Scholar] [CrossRef]

- Ito, Takatoshi, and Kiyotaka Sato. 2008. Exchange Rate Changes and Inflation in Post-Crisis Asian Economies: Vector Autoregression Analysis of the Exchange Rate Pass-Through. Journal of Money, Credit and Banking 40: 1407–38. [Google Scholar] [CrossRef]

- Jia, Xianjun. 2014. Cross-border Flows of Financial Capital and Reserve Currency Position: Based on Experience of Japanese Yuan. Study of International Finance 8: 35–43. [Google Scholar]

- Jiang, Xianling, Wei Liu, and Ye Bingnan. 2012. The Effect of Exchange Rate Expectation on Offshore Market RMB Demand. Study of International Finance 10: 68–75. [Google Scholar]

- Jiang, Xiandeng, Yanlin Shi, and Zhaoyong Zhang. 2021. Does US Partisan Conflict Affect China’s Foreign Exchange Reserves? International Review of Economics & Finance 75: 21–33. [Google Scholar] [CrossRef]

- Krugman, Paul Robin. 1984. The International Role of the Dollar: Theory and Prospect//Exchange Rate Theory and Practice. Chicago: University of Chicago Press, pp. 261–78. [Google Scholar]

- Lardy, Nicholas, and Patrick Douglass. 2011. Capital Account Liberalization and the Role of the Renminbi. Peterson Institute for International Economics, Working Paper. Washington, DC: Peterson Institute for International Economics. [Google Scholar]

- Lütkepohl, Helmut. 2006. New Introduction to Multiple Time Series Analysis. Berlin and Heidelberg: Springer. [Google Scholar]

- Lv, Guangming, and Man Xu. 2012. Short-term Capital Flow in China: Analysis of Three Motivations Base on Monthly VAR model. Study of International Finance 4: 61–68. [Google Scholar]

- Ma, Jun, and Jiangang Xu. 2012. Road of RMB Going Abroad. Beijing: China Economic Publishing Company, pp. 70–75. [Google Scholar]

- Maziad, Samar, Pascal Farahmand, Shengzu Wang, Stephanie Segal, and Faisal Ahmed. 2011. Internationalization of Emerging Market Currencies: A Balance between Risks and Rewards. IMF Staff Discussion Note. Washington, DC: International Monetary Fund. [Google Scholar]

- McKinnon, Ronald I., and Wallace Oates. 1966. The Implications of International Economic Integration for Monetary, Fiscal and Exchange Rate Policies. Princeton Studies in International Finance No. 16. Princeton: Princeton University. [Google Scholar]

- Prasad, Eswar, and Shang-Jin Wei. 2005. The Chinese Approach to Capital Inflows: Patterns and Possible Explanations. NBER Working Paper No.11306. Cambridge: NBER. [Google Scholar]

- PBoC. 2020. 2020 RMB Internationalization Report. Beijing: The People’s Bank of China. [Google Scholar]

- Qin, Fengming, Junru Zhang, and Zhaoyong Zhang. 2018. RMB Exchange Rates and Volatility Spillover across Financial Markets in China and Japan. Risks 6: 120. [Google Scholar] [CrossRef] [Green Version]

- Reinhart, Carmen, and Guillermo Calvo. 2000. When Capital Inflows come to a Sudden Stop: Consequences and Policy Options. Germany: University Library of Munich. [Google Scholar]

- Sha, Wenbing, and Hongzhong Liu. 2014. RMB Internationalization, Exchange Rate Volatility and Exchange Rate Expectation. Study of International Finance 8: 10–18. [Google Scholar]

- Sun, Tao, and Xiaojing Zhang. 2006. Empirical Analysis of Cross-border Capital Flow: A Case Study of Hongkong Route. Journal of Financial Research 8: 111–21. [Google Scholar]

- SWIFT. 2012. RMB Internationalisation: Perspectives on the Future of RMB Clearing. La Hulpe City: SWIFT. [Google Scholar]

- The People’s Bank of China. 2015. 2015 Annual Report of Renminbi Internationalization. Beijing: The People’s Bank of China. [Google Scholar]

- Wang, Shihua, and Fan He. 2007. Short-term Capital Flow in China: Current Situation, Path and Factors. Journal of World Economy, 12–19. [Google Scholar]

- Wang, Xiaoyan, Qinli Lei, and Meizhou Li. 2012. The Effect of Currency Internationalization on Macro-economy in China. Statistical Research 5: 23–33. [Google Scholar]

- Wang, Xin. 2011. Study of Costs and Benefits in the Process of RMB internationalization. International Trade 8: 51–55. [Google Scholar]

- Wang, Yong. 2011. Cross-border Capital Flow Management Dilemma and Policy Proposal in the Process of RMB Internationalization. International Trade 9: 53–59. [Google Scholar]

- Xiang, Yu, and Haibo Zhu. 2013. Effect of Hongkong RMB Offshore Market on Short-term Capital Flow Volatility: Based on Analysis of Cross-border RMB Trade Settlement. Inner Mongolia Social Sciences 6: 90–94. [Google Scholar]

- Yu, Yongding. 2011. Some Thoughts on Renminbi Internationalization. International Economic Review 5: 7–13. [Google Scholar]

- Yu, Yongding. 2012. The Current RMB Exchange Rate Volatility and RMB Internationalization. International Economic Review 1: 18–26. [Google Scholar]

- Zhang, Bin, and Qiyuan Xu. 2012. RMB’s Internationalization under the System of Limited Exchange Rate and Capital Account Control. International Economic Review 4: 63–74. [Google Scholar]

- Zhang, Ming. 2012. Capital Account Liberalization should Progress Gradually in China. International Finance 7: 3–6. [Google Scholar]

- Zhang, Ming, and Xiaofen Tan. 2013. Main Motivation Factors of Short-term Capital Flow in China: Data of 2000 to 2012. Journal of World Economy 11: 93–116. [Google Scholar]

- Zervoyianni, Athina. 1993. International Macroeconomic Interdependence, Currency Substitution, and Price Stickiness. Journal of Macroeconomics 14: 59–86. [Google Scholar] [CrossRef]

- Zhang, Zhaoyong, and Kiyotaka Sato. 2012. Should Chinese Renminbi Be Blamed for Its Trade Surplus: An VAR Approach. The World Economy 35: 632–50. [Google Scholar] [CrossRef]

- Zhou, Xinmiao, Junru Zhang, and Zhaoyong Zhang. 2021. How does news flow affect cross-market volatility spillovers? Evidence from China’s stock index futures and spot markets. International Review of Economics & Finance 73: 196–213. [Google Scholar]

- Zhu, Mengnan, and Lin Liu. 2010. Short-run International Capital Flows, Exchange Rate and Asset Prices-An Empirical Study Based on Data after Exchange Rate Reform Since 2005. Finance & Trade Economics 5: 5–13. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Indicators Name | Sample Period | Time Frequency |

|---|---|---|

| RMB settlement of cross-border trade | 2012.1–2020.12 | Monthly |

| Standard Chartered RMB global indicator RGI | 2012.9–2017.6 | Monthly |

| Hong Kong offshore market RMB deposits | 2004.2–2020.12 | Monthly |

| China Bank offshore market index ORI | 2011.4–2020.4 | Quarterly |

| China Bank cross-border RMB index CRI | 2011.4–2020.3 | Quarterly |

| RMB settlement accumulation of cross-border trade | 2009.4–2020.4 | Quarterly |

| Variable | Test Type (c, t, n) | ADF Statistic | Critical Value | Significance Level | Conclusion |

|---|---|---|---|---|---|

| Shortcapital | (c, t, 0) | −14.369 | −4.006 | 1% | Stationary |

| lnCurrency | (c, t, 0) | −3.975 | −4.006 | 1% | Stationary |

| Expect | (c, t, 0) | −9.582 | −4.006 | 1% | Stationary |

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Expect | 203 | 0.041 | 0.124 | −0.227 | 0.465 |

| lnCurrency | 203 | 12.169 | 1.622 | 6.797 | 13.819 |

| Shortcapital | 203 | 0.014 | 0.038 | −0.108 | 0.113 |

| lnCurrency | Shortcapital | Expcet | ||||

|---|---|---|---|---|---|---|

| Period | Expect | Shortcapital | Expect | lnCurrency | lnCurrency | Shortcapital |

| 1 | 0.668 | 0 | 1.249 | 3.750 | 0 | 0 |

| 2 | 1.362 | 4.272 | 1.145 | 3.720 | 0.108 | 1.181 |

| 3 | 1.719 | 8.777 | 1.092 | 3.652 | 0.121 | 2.047 |

| 4 | 1.799 | 12.627 | 1.085 | 3.614 | 0.165 | 2.038 |

| 5 | 1.817 | 15.621 | 1.080 | 3.593 | 0.243 | 2.035 |

| 6 | 1.829 | 17.922 | 1.078 | 3.588 | 0.325 | 2.033 |

| 7 | 1.835 | 19.685 | 1.077 | 3.593 | 0.409 | 2.043 |

| 8 | 1.836 | 21.049 | 1.077 | 3.605 | 0.497 | 2.067 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Expect | lnCurrency | Shortcapital | |

| L.Expect | −0.136 ** | 0.0193 | −0.0139 |

| (0.0689) | (0.0349) | (0.0230) | |

| L2.Expect | −0.215 *** | 0.0131 | −0.00269 |

| (0.0681) | (0.0345) | (0.0227) | |

| L.lnCurrency | 0.110 * | 1.220 *** | −0.00219 |

| (0.0594) | (0.0301) | (0.0198) | |

| L2.lnCurrency | −0.0529 | −0.225 *** | −0.00113 |

| (0.0575) | (0.0292) | (0.0192) | |

| L.Shortcapital | −0.340 | 0.540 *** | 0.311 *** |

| (0.209) | (0.106) | (0.0698) | |

| L2.Shortcapital | −0.307 | 0.0690 | 0.171 ** |

| (0.212) | (0.108) | (0.0707) | |

| Constant | −0.629 *** | 0.0749 * | 0.0484 * |

| (0.0788) | (0.0399) | (0.0263) | |

| Observations | 201 | 201 | 201 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, M.; Qin, F.; Zhang, Z. Short-Term Capital Flows, Exchange Rate Expectation and Currency Internationalization: Evidence from China. J. Risk Financial Manag. 2021, 14, 223. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050223

Li M, Qin F, Zhang Z. Short-Term Capital Flows, Exchange Rate Expectation and Currency Internationalization: Evidence from China. Journal of Risk and Financial Management. 2021; 14(5):223. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050223

Chicago/Turabian StyleLi, Mingming, Fengming Qin, and Zhaoyong Zhang. 2021. "Short-Term Capital Flows, Exchange Rate Expectation and Currency Internationalization: Evidence from China" Journal of Risk and Financial Management 14, no. 5: 223. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050223