Data-Driven Services in Insurance: Potential Evolution and Impact in the Swiss Market

1

Institute for Risk and Insurance, Zurich University of Applied Sciences, 8401 Winterthur, Switzerland

2

Cognizant Technology Solutions, 8005 Zurich, Switzerland

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2021, 14(5), 227; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050227

Submission received: 2 May 2021

/

Revised: 13 May 2021

/

Accepted: 15 May 2021

/

Published: 19 May 2021

(This article belongs to the Special Issue Sustainability in the Service Industries)

Abstract

:Using real-time customer data holds great potential for the insurance industry. The frequency and relevance of interactions can be improved to provide assistance in real time. Better prevention and risk management can significantly improve pricing and reduce losses. These changes, however, hold the potential for structural changes in the industry. This research aims at understanding the potential path of the development of services in insurance and the challenges faced by insurers. A panel of industry experts provided the industry’s view, which was then compared with the responses of 1542 Swiss retail customers. We find that customers have high trust in insurance companies and are open to purchasing additional services, particularly for prevention and assistance. Insurance companies, however, are currently focusing on cost improvement measures. Customers are open to sourcing services from other providers, suggesting that insurance companies need to evolve their approach to take advantage of the current market window.

1. Introduction

The world’s most valuable resource is no longer oil, but data (The Economist 2017). Mining data for insights can enhance the productivity and competitiveness of companies and create substantial benefits for consumers (Manyika et al. 2011). This value creation is built upon the convergence of trends in digitalization and servitization, and is delivered to the customers through the introduction of new, customized products and services. The evolution of value creation, however, requires new organizational solutions and can trigger large-scale structural changes in the industry. This paper surveys insurance experts and customers in Switzerland to understand the likely path of evolution, generate insights for insurance companies and identify topics for future research.

Wamba et al. (2015) conduct a longitudinal study of the current literature to identify five dimensions in which big data can create value for companies: creating transparency, enabling experimentation, customizing actions, replacing human decisions and innovating business models. Achieving these results, however, is linked to a number of issues they identify: data policies—especially regarding privacy—are necessary, appropriate technology will need to be implemented, organizations will need to adapt their processes and expertise, access to relevant data will be critical, and industry structure will have an impact on the effectiveness of big data. The structural impact is significant: Bouwman et al. (2018) find that technology turbulence has a direct effect on business model experimentation and that this innovation has a positive effect on company performance. In their sample of 85 European SMEs, the impact was more extensive for big data than for social media, and they observe that big data affect a company’s core activities.

Vandermerwe and Rada (1988) introduce the concept of servitization, whereby companies bundle services in their core offerings to create new relationships with their customers and lock out competitors, lock in customers and increase the level of differentiation. They note that the cumulative effect of the introduction of new service offerings changes the dynamics of the industry in which the companies operate. Neely (2008) analyzes 10,634 manufacturing firms to identify 12 different forms of servitization and understand their financial impact. While servitization is widespread, especially for larger companies, its financial benefits are less clear and they appear to not cover the additional investment in skilled employees and working capital—the servitization paradox. He suggests this may be due to the challenges of shifting the mindsets of employees and customers, of managing multi-year timescales and of new business models/customer offering. Adrodegari and Saccani (2017) survey 222 published sources to conclude that service transformation requires fundamental changes in the firm’s structure, culture and competencies and in the way of delivering value and dealing with customers and stakeholders. Big data further accelerate this transformation by enabling enterprises to more quickly and more efficiently reconfigure their capabilities. Big data and servitization reinforce each other: the more an enterprise servitizes its products, the more users they have, the more data can be collected and information exploited through resell and/or reuse (Opresnik and Taisch 2015).

Zolnowski et al. (2016) investigate 20 cases from seven service industries, including one example from insurance, to understand how successful data-driven innovation has impacted their business models for value generation and value capture. These cases cover improvements in customer orientation, process optimization, better profitability and the optimization of resource planning, and the collection of information to complement and accelerate decision. They identify four innovation patterns linking cooperation between a company and its customers, and value vs. productivity improvements: cooperative value innovation, customer-centric value innovation, cooperative productivity improvements, and company-centric productivity improvements. Successful implementations of data-driven innovation combine improvements in both customer orientation and productivity, and they reinforce each other. The study concludes that data-driven innovations in service businesses will likely substantially transform the way corporations think and operate. Thus, the experience of servitization is accompanied by profound changes to the winning business models. Technology, especially big data, further impacts this change. The shift to services and their data-driven evolution is accompanied by significant challenges for the organization and can trigger fundamental changes in the industries where it occurs.

Big data require access to customer information. The privacy calculus theory indicates that individuals are willing to disclose personal information in exchange for some economic or social benefit. When the perceived benefits obtained by disclosing the information are higher than the risks assumed, the willingness to provide the information is given (Culnan and Armstrong 1999). However, the calculus can be situation-specific and rationally bounded (Kehr et al. 2013). Customers are more willing to share information when (a) information is collected in the context of an existing relationship; (b) they can control the future use of the information; (c) the information is relevant to the transaction; and (d) the information can be used to draw reliable and valid inferences (Stone and Stone 1990). Trust has been found to play a key role in information disclosure (Metzger 2004; Simpson 2012), and people tend to share with third parties more general information than sensitive data (Milne and Gordon 1993; Smith et al. 2011).

In insurance, in particular, customer relationships are of crucial importance, and the way of doing business is affected by insurers’ ability to better understand their customers (Beer et al. 2017; Garth and Westlake 2018). Changing customer expectations caused by the availability of new technologies but also generational shifts open up new challenges for the insurance industry. Policyholder expectations for individualized, more flexible, and real-time services are becoming more common and insurers need to be prepared and capable of handling these expectations (Beer et al. 2017; Buehler and Maas 2016). The majority of Swiss insurance customers prefer individual, more personalized, flexible services and consulting, thus putting pressure on insurers to develop new offerings and touchpoints (Deraëd and Henry 2012; Kotalakidis et al. 2016). In addition to satisfying customer expectations, data can also enable insurers to better tailor and individualize their products to the customers’ risk profile (Baecke and Bocca 2017), decrease information asymmetry (Cardon and Hendel 2001), and properly assess clients’ risks to calculate the premium adequately (Borna and Avila 1999; Rothschild and Stiglitz 1976).

Eling and Lehmann (2018) review the current literature of 84 academic papers to understand the impact of digitalization on the insurance value chain, and note that the academic discussion on the digitalization of insurance has been virtually non-existent. They predict that technology will bring significant change to the insurance industry in three broad categories: (1) new technologies change the way insurers and customers interact (e.g., social media, chatbots and robo-advisors); (2) new technologies can be used to automatize, standardize and improve the effectiveness and efficiency of business processes (e.g., online sales, digital claims settlement); and (3) new technologies create opportunities to modify existing products (e.g., telematics insurance) and to develop new ones (e.g., cyber insurance). Further, they categorize and detail the impact of digitalization on insurance along eight primary and six secondary insurance activities. The authors, however, are much more conservative in their assessment of the potential for disruption in the insurance industry. They consider unlikely that established non-insurance technology players would enter the insurance industry and capture parts of the value chain: insurance incumbents are not as keen to outsource parts of their value chain, established technology players should have better alternative investment opportunities, the regulatory environment and the expertise required necessitate a significant investment, and negative customer feedback in the case of a declined claim may spill over in their core business. Disruption from insurtechs is also considered unlikely: traditional insurers could just copy the insurtechs, or they could just buy them; insurtechs are more interested in collaborating than in competing with insurers; and regulatory constraints and lack of expertise challenge the expansion of insurtechs. However, data are not provided to support the qualitative analysis. Insurability of risk, on the other hand, may be affected by digitalization as new information may impact information asymmetry and risk pooling, new technologies may impact loss frequency and severity, connectivity increases dependencies among risks, and ethical and legal questions may arise. Thus, the authors view the impact of digitalization as a significant enhancement to but not a disruption of the existing business models of insurers, i.e., providing indemnification in case of loss and the connected activities related to pricing, distribution and customer interaction.

Cappiello (2020) follows a similar framework to investigate the impact of technology and insurtechs on insurance intermediation and customer loyalty. She also concludes that digitalization is destined to deeply modify insurance, impacting all activities in the value chain, from product development and underwriting to sales and distribution, policy and claims management, and asset and risk management. Further in agreement with Eling and Lehmann (2018), she also concludes that the potential for disruption in the industry due to insurtechs is low. The conclusions regarding the potential impact of established technology players, however, are less clear. In insurance, services coexist in the user’s and in the manufacturer’s spheres of availability, and continue to be influenced and activated by the latter (Normann 2001). A company can act to modify the service by varying premiums or conditions, while a customer’s behavior can impact the risk. This interrelation drives the potential for a more fundamental impact of technology on the insurance business model and leaves several research questions open regarding the opportunities provided by personalized services.

While broadly in agreement with the insights from other markets, research on the willingness to share information (WSI) in insurance indicates that customer value involves not only the perception of product quality, but also company reputation and services. Further, this can be influenced by the level of satisfaction with the insurance agent (Steiner and Maas 2018). Insurance customers are open to sharing information with their insurers and are increasingly interested in accessing services provided by them (Bain & Company 2017). On the other hand, they are open to purchasing core insurance products, and presumably, ancillary services, from new entrants in the industry (Bain & Company 2018). Swiss insurance customers have been found to be generally in line with these findings: they are open to sharing information in general, and especially if they receive enhanced services or premium discounts in return. The type of information requested impacts this willingness to share: sharing traditional insurance-specific information, for example, regarding the vehicle or the location and dynamic of the accident, is not problematic. On the other hand, customers become more guarded when sharing information that is more behavioral in nature (Pugnetti and Elmer 2020). Several tests are already underway in the Swiss insurance market by incumbents, with a special focus on personalizing motor insurance (Arisov et al. 2019).

It is at this point unclear how to reconcile the experience outside of insurance with the current view within insurance. Digitization, big data and servitization have been shown to bring opportunities in several industries while requiring significant changes in the incumbents’ business models to harvest the full benefits and thus, potentially triggering shifts in the industry structure. Insurance customers have been shown to be open to purchasing additional services from insurers and to sharing personal information with them. At the same time, the available literature indicates that the transformation underway in insurance will improve the current operating and business models but should not alter value capture mechanisms and the structure of the industry. The data supporting this point of view, however, do not seem conclusive.

This research aims to understand the impact of data-driven services in insurance using primary data to address four fundamental questions for Swiss insurance businesses:

- How are Swiss insurance companies addressing the opportunities offered by data-driven services and do they see a long-term impact on the structure of the industry?

- Which insurance-related services are Swiss customers interested in, and how do they value the information needed to provide them? How do these results differ by gender, age cohort, and current insurance provider?

- How open are Swiss insurance customers to sourcing insurance-related services from non-insurers?

- How well does the view of insurance experts match customer priorities?

In addition to the literature reviewed above, we constituted a panel of insurance experts to verify the interest from practitioners in the topic and develop the research approach. These core experts were interviewed from April to June 2019 using qualitative semi-structured interviews, and their insights guided the structure of the survey as well as the selection of the broader set of experts surveyed.

2. Materials and Methods

We address the research questions above by conducting a survey of Swiss industry experts and of Swiss retail customers. In each survey, we investigate the likely evolution of services in insurance and their long-term impact on the industry, as shown in Table 1.

The experts were asked on a scale of one to six how likely it is that individual services will be standard in the industry in three to five years, and how likely it is that these services will be provided by new industry players in five to ten years. Customers were surveyed on their interest in using the services on a scale of one to six, with one meaning not interested at all and six meaning very interested. Separately, they were asked how much they value the different types of information required to provide the services, also on a scale of one to six, with one indicating not willing to share the information at all and six indicating no problem sharing the information. The type of information was matched to the services by the authors and the experts to determine the attractiveness of the service vs. the perceived “cost” of the information necessary to provide that service. In addition, customers were asked how open they are to sourcing the services from different types of providers.

Underlying the two surveys is a common set of services, summarized in Table 2. The list of services was developed together with the expert panel to capture the range of topics of interest to practitioners and is organized by line of business (LoB) and type of service. We surveyed services in three lines of business: auto/mobility, home/living, health/wellness, as well as cross-LoB services. In each LoB, we surveyed five types of services: protection/administration, prevention/risk management, assistance/emergency, cost control/claims management and life services not specific to insurance. An example of a service was provided for each combination to ensure consistent understanding of the topic for the respondents to the survey. This structure allowed us to summarize and compare the results by LoB and type of service as well as by individual service.

The survey was sent to 35 insurance experts identified by the expert panel in July 2019. In addition to the structure above, the experts were also asked about the business driver for introducing services in insurance. Twenty-three experts responded.

Retail customers were surveyed in January 2020 following an expert panel workshop to discuss the results of the expert survey. A total of 1542 German-speaking customers responded to the survey. Not all respondents answered all the questions, and all responses that had completed at least 95% were used. All respondents were current holders of P&C, Life and Health insurance policies in Switzerland. The responses were organized to be roughly equivalent in size by gender and across four age cohorts: 18–25, 26–35, 36–50 and above 50 years old. They were also asked to identify their key decision criteria when purchasing insurance, rate their trust in insurance and name their current insurance providers. A list of the five largest insurers in P&C, Life and Health in Switzerland was provided to collect insights in the portfolio of 13 insurance companies.

Different items of the survey were then used to address the research questions as summarized in Table 3.

3. Results

The responses to the survey and their analysis have been organized in this section to match the sequence and contents of the research questions above.

3.1. Expert Survey

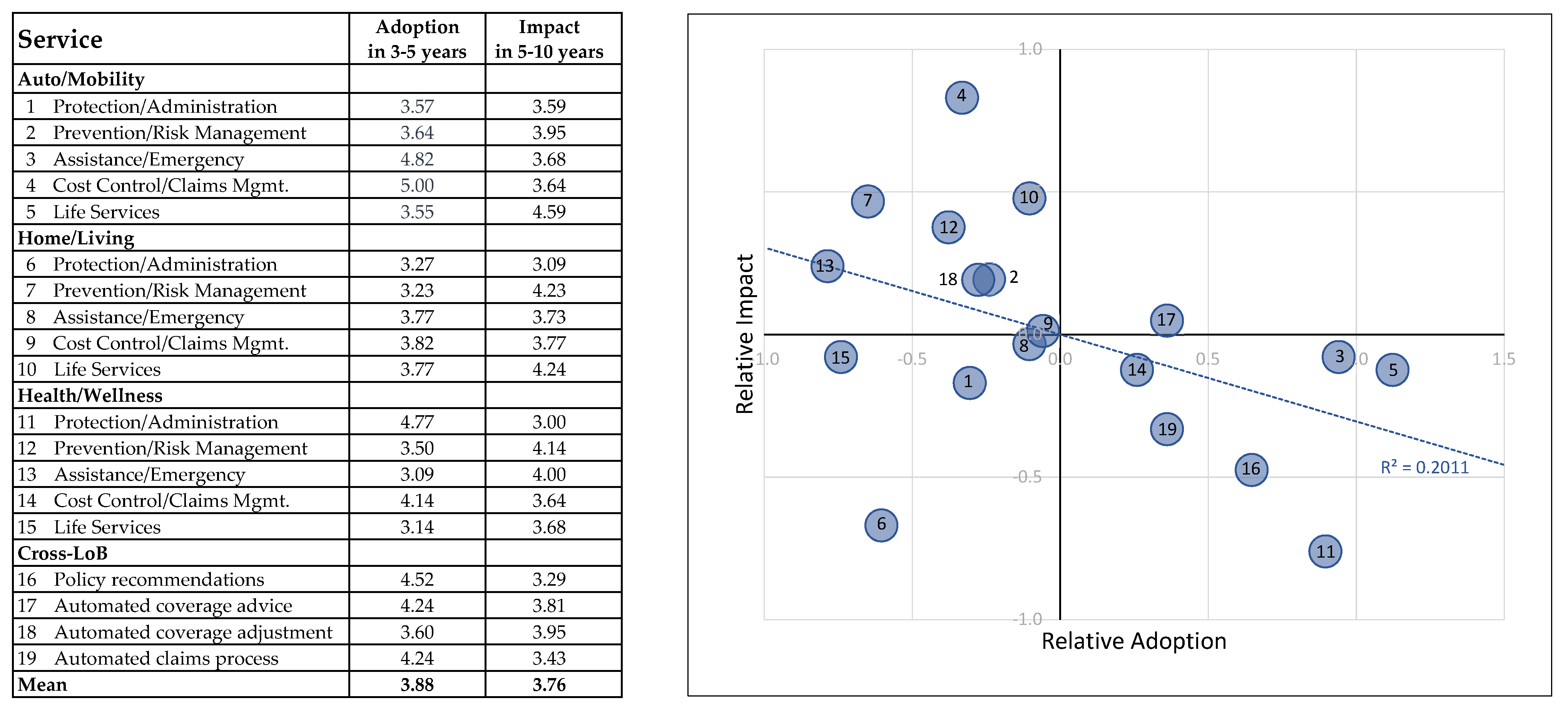

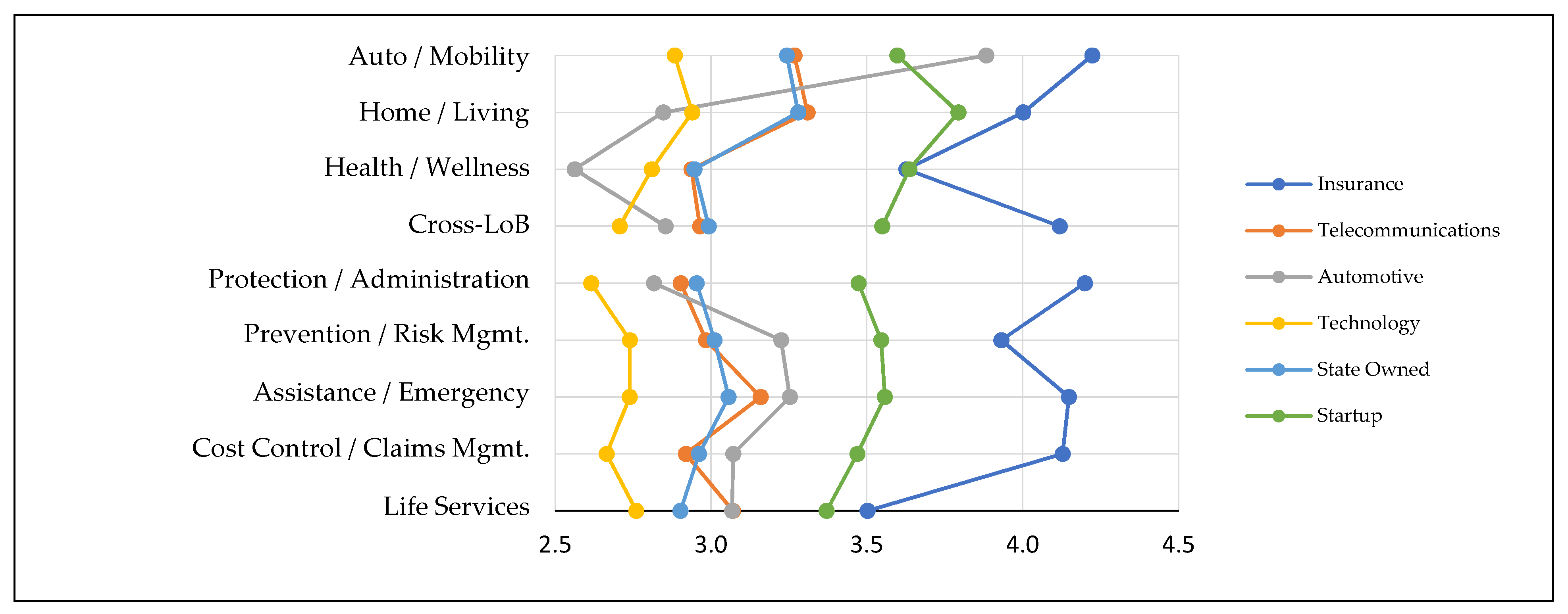

The results of the expert survey by individual service are shown in Figure 1. On the left side of the figure, we tabulate the responses. On average, both adoption in 3–5 years and impact in 5–10 years are slightly above the middle point of the 1 to 6 scale, indicating overall adoption, but not a widespread, standard offering of services, and an industry dynamic largely limited to the existing players. The view of the individual services for each line of business, however, is quite differentiated. In automotive and mobility services, the focus seems to lie in cost control and claims management with assistance and emergency services, whereas in health and wellness, the focus is on improving policy administration. Automated recommendations, advice and claims processing seem to be viewed as promising across the board, while services for the home seem to be lagging. The potential for impact in the structure of the industry seems to be driven by prevention and risk management services, enriched with services outside the insurance industry and automated adjustments to the insurance coverage. Thus, adoption seems to be focused on improving operations, while experts deem services adding value to customers as the most impactful in the long term. On the right side of Figure 1, we plot the values for both adoption in 3–5 years and impact in 5–10 years with respect to the average value for each dimension. Notable in this plot is the inverse relationship between the two dimensions: the experts polled indicated that the operational services that insurance companies are likely to introduce in the near future are, by and large, not the ones that are likely to have a longer-term impact on the dynamics of the industry. Conversely, a number of services deemed to be of significance in the long term are not being pursued as actively.

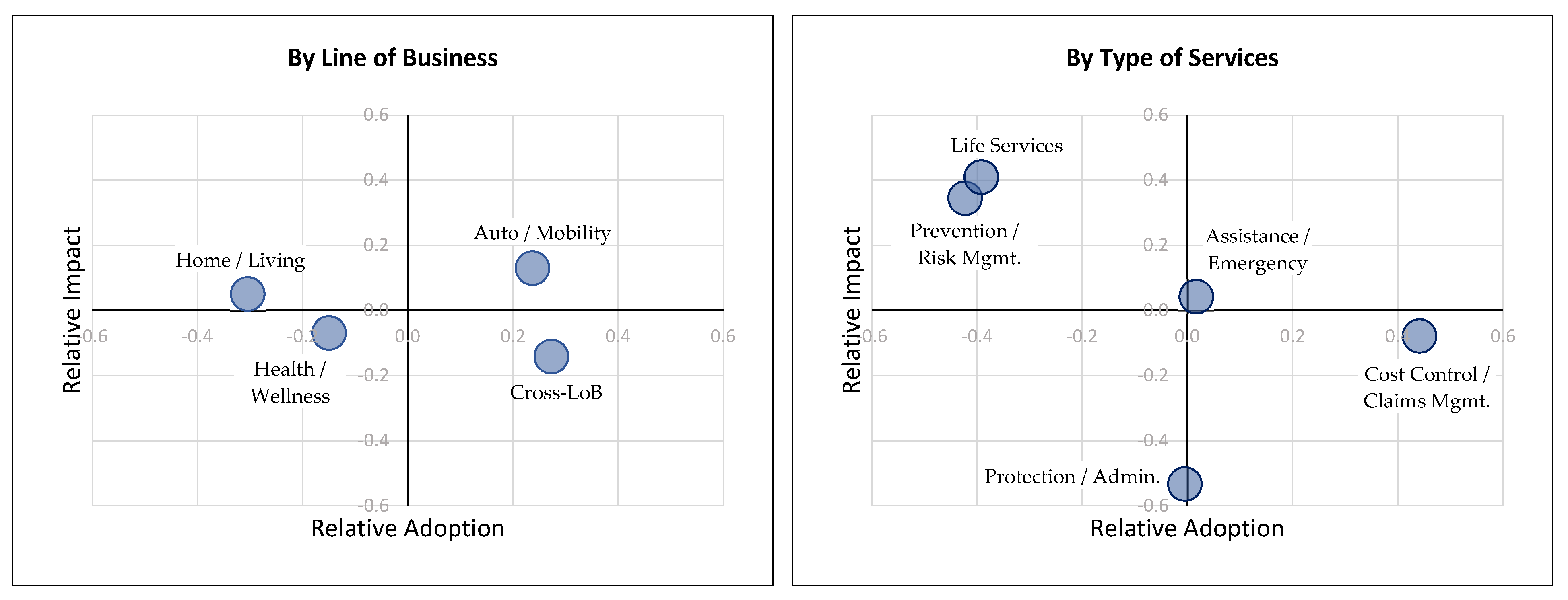

The same results can be summarized by line of business and by type of service to further highlight the core messages. These are shown in Figure 2. On the left side, we see that the adoption efforts are focused on automotive services and in automating cross-LoB processes. The impact of these efforts is expected to be comparable and somewhat limited across the lines of business. The differentiation across both dimensions, however, is much larger when analyzed by type of service. The industry seems to be focusing its efforts on cost control measures, and to a smaller extent on administration and assistance services. Risk management services for customers and adding non-insurance services is not in focus. Experts, however, view precisely these two types of services as the most likely to have an impact on the industry in the medium term, with assistance and claims management having an average impact and administration, unsurprisingly, the lowest impact.

The message from the experts can thus be interpreted as follows: data-driven services will be implemented in the Swiss insurance industry in the next few years and will likely have an impact in the industry dynamic among the existing players. The lines of business are likely to evolve at different rates, with automotive leading the development and home lagging. Cross-LoB capabilities to automate will emerge. The current implementation focus will lead to services deployed especially to control internal costs, with services for prevention and to satisfy non insurance-specific needs lagging. However, precisely these lagging services are the ones expert expect to have a longer-term impact on the structure of the industry.

3.2. Customer Survey—Services

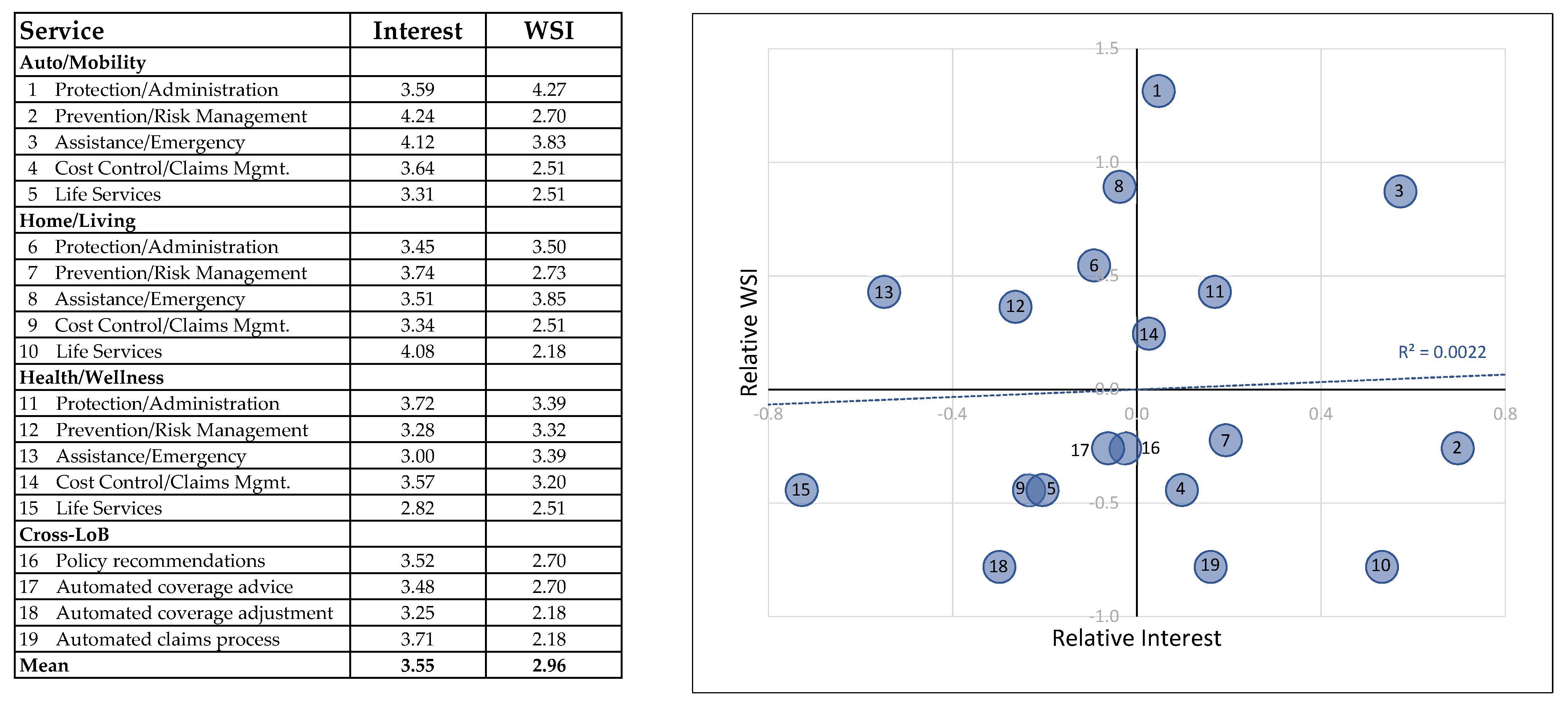

Insurance customers were surveyed regarding their interest in receiving a particular service and their degree of comfort sharing different types of information. The type of information was mapped by the experts onto the services to have an overall indicator of the willingness to share information (WSI) necessary to provide each service. The indicator matches the customer’s willingness to share the most critical piece of information, i.e., that with the lowest score. The detailed responses for the willingness to share each type of information are available in the Appendix A. These results are similar to others obtained in previous studies (e.g., Pugnetti and Elmer 2020, showing a greater willingness to share information related to insurance and more reticence regarding surveillance-type information. These results will therefore not be discussed in more detail in this paper.

The results of the customer survey are shown in Figure 3. Overall, customers are moderately interested in services but somewhat guarded in their sharing of information. Looking at the individual results there seems to be interest in prevention and assistance services in automotive, while in home the interest is more on non-insurance services. The interest in health services is muted overall, as is the interest in cross-LoB automated services. In automotive and in health, contrary to home, life services meet with noticeably less interest. Customers are relatively open to sharing administrative and emergency information, as well as health-related information. They are much less open to sharing real-time information necessary to provide additional services and to automate key process across LoBs. This is due to the type of information requested as discussed previously. Interest in the service and the willingness to share information (WSI) is plotted with respect to the average response on the right side of the figure. There we see that there is no correlation between the interest in a service and the perceived cost of the required information. A few services appear in the top right-hand quadrant, indicating a high interest from the customers and a larger than average willingness to share information. Automotive assistance and the administration for automotive and health stand out, indicating customer support for some types of emergency support but also the inadequacy of current administrative processes. In the lower left quadrant, on the other hand, we find services that are deemed not as interesting and where the necessary information is deemed costly. Here, we find several of the life services and automated cross-LoB services. This indicates potential barriers to automating core insurance processes and expanding insurance beyond traditional core offerings.

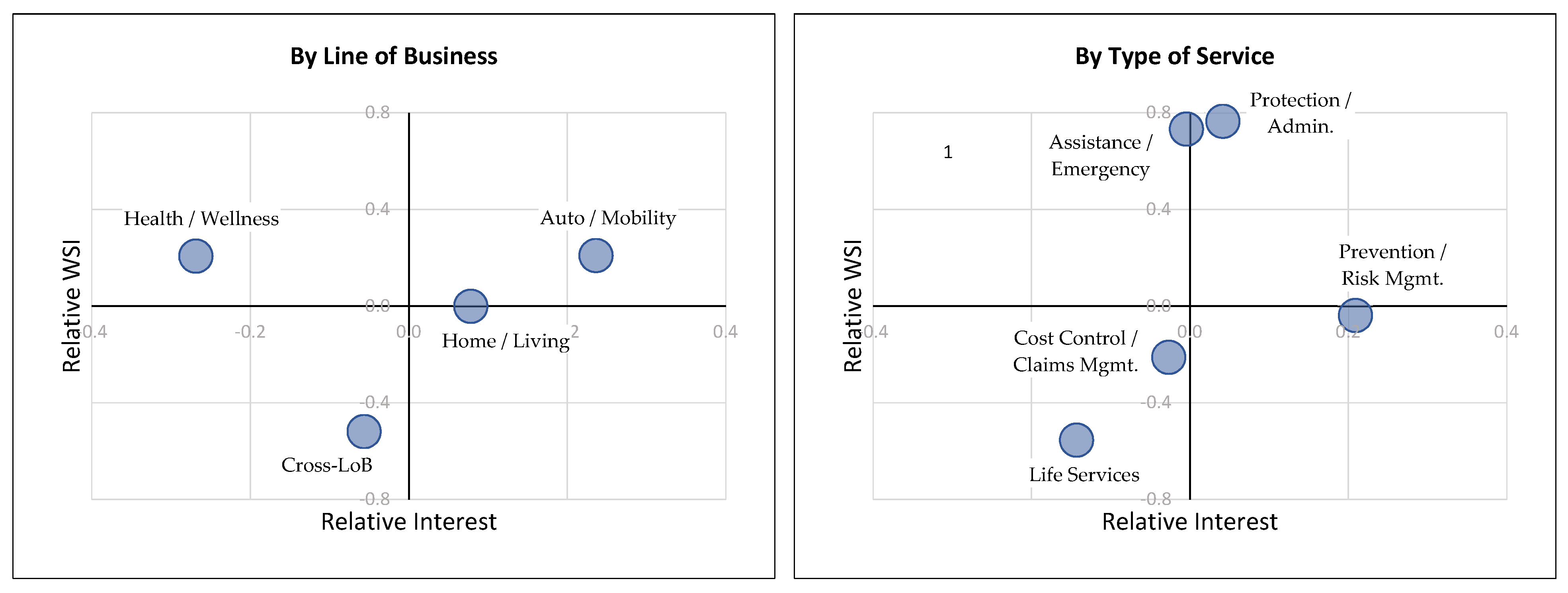

Similarly to the expert survey, we can summarize customer responses by line of business and by type of service. These results are shown in Figure 4. Overall, automotive services enjoy customer interest and a relative willingness to share the required information. Health services do not seem to enjoy the same interest. Most noticeable, however, is the overall reluctance from customers to share the information necessary to provide automated cross-LoB advice and coverage adjustment. The view by type of service provides a different set of insights: customers are open to sharing information related to administration and emergencies, but only moderately interested in these services. They are interested in prevention services but guarded with the necessary information. They are not as interested in cost control or life services, while also being reluctant to share the relative information.

Overall, customers provide a differentiated view of their interest in data-driven services. They are generally interested in prevention and assistance services, and more so for automotive and, to some extent, home. They are generally open to sharing administrative and emergency information but more guarded with more behavioral information. The differentiated nature of the result suggests that narrow, targeted service offerings are likely to be more successful than broader, company-wide or cross-LoB service offerings.

We further analyze the responses by gender, age cohort and current insurer, as summarized in Appendix A. These results are in line with previous research, with men and women showing similar interest in additional services and younger customers significantly more interest than older customers. Men and younger people are also generally more open to sharing information with insurers. This indicates that data-driven services should increase in popularity over time as younger customers replace the existing core insurance customers and both the interest in services and the willingness to share information rise. The responses also show no significant differences among the customer portfolios of individual companies. The customer profile, the interest in services and the willingness to share information are essentially identical for all insurance companies. Customers of companies with different market approaches, such as Allianz with their operations focus and Mobiliar with their local delivery approach, are equally interested and open to sourcing services. Additionally, P&C companies do not have an advantage in automotive or health insurers in health services, and so on. This suggests that customers view the insurance industry as trustworthy overall and do not distinguish sharply between companies when asked about new services. This may also be indicative of an early stage of market development, and may change as services are introduced by individual companies and customers begin to experience them.

3.3. Customer Survey—Providers

In the survey, customers were asked to rate on a scale of one to six how open they were to purchasing the services listed from companies operating in different industries. The results are shown in Figure 5. Where the services were clearly identifiable with insurance, the insurance industry has a clear advantage with only a few exceptions. This result attests to the excellent perception of their insurance company among Swiss customers. A few exceptions can be explained with market affinity. Therefore, for example, automotive brands are a close second to insurers in services related to mobility, and existing specialized providers are narrowly in first place in health. In non-insurance services, the gap is narrower overall. Technology companies are not a provider of choice for any of the services, as consumers have low trust in them. These companies, however, should be able to leverage high volumes internationally and very cost-effective platforms if they decide to offer services, and should therefore be a strong competitor in spite of customer perception. Other industries are in-between these two extremes, with automotive companies particularly unwelcome to provide health services. The main challenge to insurers does not seem to come from established players but from specialized, potentially new providers. This indicates that while insurers enjoy an enviable position of trust on which to build their evolution and growth, they are also vulnerable to competition from specialized firms. Brand does not seem to play a particular role, but specialization for a particular purpose, as phrased in the survey question, may be important. The customer interest in these specialized competitors may indicate that the advantage enjoyed by insurers may be short-lived and raises the possibility of potential market entry by new competitors.

3.4. Expert and Customer View

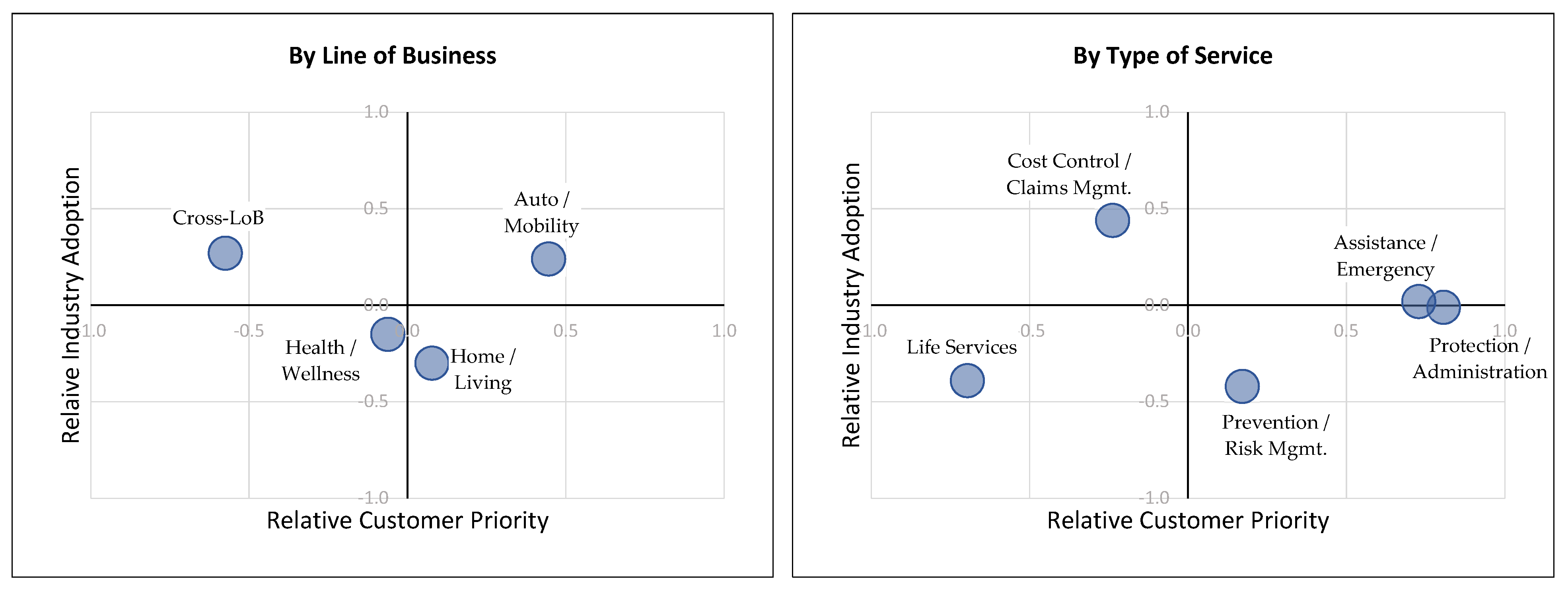

Utilizing the same survey structure for both customer and expert views allows direct comparison of the responses for both the relative speed of adoption and the impact on the industry by service. The results for the pace of adoption are shown in Figure 6. The y-axis is the likely adoption score provided by the experts; the x-axis is the algebraic sum of the customer score and their willingness to share the relevant information in order to derive an overall customer priority score. The results are plotted relative to their respective average values and summarized by line of business and type of service. The industry seems to be working according to customer priorities in automotive services, but concentrates on cross-LoB services not on the customers’ radar screens. The message is sharper when looking at the type of service. The industry is prioritizing cost controls, whereas customers are more open to prevention services. Process streamlining and emergency services could be further emphasized by the industry, and life services are seen as a problematic offering and not a focus. Thus, there seems to be only a tenuous link between industry adoption and customer priority.

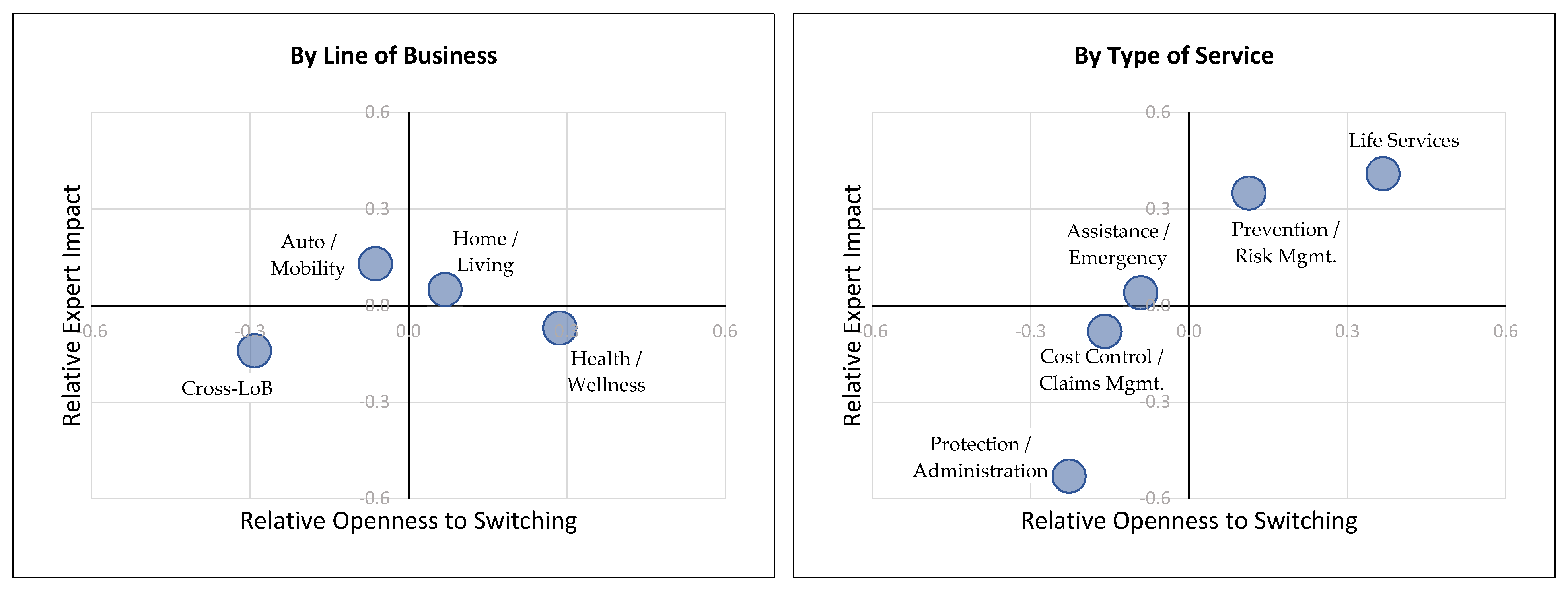

The expert view on impact is compared to the customers’ openness to switching providers in Figure 7. The y-axis is the expert view of impact, and the x-axis is the difference between the value provided for insurance and the next best value for customer provider preference, as discussed in Section 3.3. Again, the information is plotted relative to each dimension’s average value and summarized by line of business and type of service. There does not seem to be any agreement between experts and customers by line of business, with customers in general signaling a lower loyalty to health insurers and a higher loyalty to automotive providers than the expert view. The two views, however, are almost exactly aligned when summarized by type of service. Both experts and customers signal the importance of non-insurance services and prevention. Conversely, they recognize the lower strategic impact of cost control and administrative services.

These results are an overall vote of confidence for the awareness of insurance experts of their customers’ view. At the same time, they sound an alarm bell for insurance companies. The current plans seem to focus on low impact, cost control and administrative services. Experts, however, have signaled that prevention services are much more important in the long run and that customers are open to sourcing these services elsewhere if necessary. Expanding beyond insurance services also holds long-term promise, but companies need to learn to navigate the acquisition of necessary information.

4. Discussion

The empirical results presented in Section 3 allow the research questions posed in Section 1 to be answered in detail.

- 1. How are Swiss insurance companies addressing the opportunities offered by data-driven services and do they see a long-term impact on the structure of the industry?

The experts surveyed indicate that data-driven services will be adopted in the next few years and that they have the potential to alter the dynamics of the industry to some extent. The industry seems to be focused on introducing services, especially those addressing mobility needs, and controlling costs in the near term. The potential impact, however, is viewed as coming from prevention/risk mitigation services as well as from non-insurance services. Real-time prevention can dramatically alter the risk profile of the insurance portfolio and any company that establishes effective practices will be able to more accurately price their risk. In addition, these services can further increase customer loyalty by increasing the frequency and relevance of interactions with their customers. Unfortunately, these are exactly the services that are not currently being developed and deployed. These results indicate a short-term focus on cost containment at the expense of long-term strategic advantage and open the industry up to the risks of complacency often displayed by successful incumbents.

- 2. Which insurance-related services are Swiss customers interested in, and how do they value the information needed to provide them? How do these results differ by gender, age cohort, and current insurance provider?

Swiss insurance customers are generally interested in the services but are somewhat guarded about sharing their personal information. They are generally more interested in automotive services and preventive services, and less in health services. They are generally open to providing information regarding assistance and administrative services and more guarded with information needed to automate coverage and claims processing, or to provide non-insurance services. This is driven by the more behavioral type of information required for these services, and these results are aligned with previous research. The results also indicate the opportunity to provide services in areas of higher customer acceptance—assistance and administration—and in areas of high customer interest—prevention.

Men and women do not differ substantially in their interest in services, but men are more open to sharing information. Younger customers are more interested in services and more willing to share information than older customers, suggesting that the opportunity to introduce services in insurance will accelerate over time as younger customers replace current core customers. The responses provided by customers of different insurance companies do not show any significant differences, regardless of the company’s market approach or its core lines of business. This suggests that customers may tend to view insurance as an overall market rather than different players and that services are in an early phase of development. The implication of this dynamic is that insurance companies have the opportunity to explore and develop new services without needing to specifically worry about their own customer expectations being different from those of the overall market.

- 3. How open are Swiss insurance customers to sourcing insurance-related services from non-insurers?

Insurers seem to enjoy a remarkably positive reputation among Swiss customers. They are by and large the preferred provider for the services investigated in this study. Only automotive companies are comparable for automotive services and specialized providers for health services. For non-insurance services, this comparative advantage is, not surprisingly, reduced. In general, Swiss customers are open to new, specialized providers, rather than established brands as a second choice to insurance companies. This dynamic potentially opens the door for a number of targeted offerings by start-ups or by special brands of established companies. In addition, potential competition from other non-insurance players should not be discounted: automotive companies are technologically and financially capable of entering the market and technology companies, while not well trusted, can deploy established data management capabilities and scaled operational platforms to provide services at an aggressive price point. Thus, insurance companies enjoy an advantage, but customers are open to other providers and the current advantage may expire over time if it is not exploited.

- 4. How well does the view of insurance experts match customer priorities?

The expert view of the adoption of services reflects their knowledge of the projects currently underway, and their responses do not match up all too well with the responses of the customer survey. Customers prioritize assistance and administration services: the first to provide help in case of an emergency, the second to alleviate the pain of interacting with insurance companies. They are also interested in services helping them prevent losses. Insurance companies, on the other hand, prioritize cost control measures and automating core processes, neither of which receive high scores from the customers. Containing operating costs is a rational economic choice for insurers, but should not come at the expense of other, more customer-focused measures. Customers do not consider non-insurance services a priority: they are interested in the services but are reluctant to share the necessary information. Insurance companies seem, therefore, to be justified in not prioritizing them.

Experts and customers, on the other hand, are very well aligned in their view of the potential for change triggered by the adoption of services. Life services, while challenging because of the information required, hold the highest potential for changes in the industry. Close to them, however, are prevention services. Unsurprisingly, the long-term strategic impact of administration and cost control measures is seen as less significant. The key insight from the study is the significance of data-driven prevention services. They can be significant drivers of portfolio risk and allow insurance companies to price more accurately and in particular, understand their risk in real time and dynamically adjust exposure. Experts view this area as particularly impactful to the insurance business model, and one on which insurance companies have not focused enough. Customers would like to access these services and are willing to share the necessary information. They are also relatively open to switching to providers outside the industry when these options become available. This dynamic poses an important strategic challenge for insurers. On the positive side, insurance companies can rely on their experts to accurately gauge market needs and guide this development.

5. Conclusions

The use of real-time information to provide services to customers holds the potential for significant improvements in customer interaction and the productivity of insurance companies. Labor-intensive processes can be automated to reduce costs and improve quality. The frequency and relevance of interaction can be vastly improved away from pure financial indemnification and once-yearly billing cycles, towards assistance in the moment of need. Better prevention and risk management can significantly improve the technical pricing process and reduce losses. The intersection and mutual reinforcement of digitization, big data and servitization have brought significant changes to successful business models and industry structure in many other sectors. These changes, therefore, may trigger similar changes in the insurance industry, as new players may be better able to leverage information to build strong customer interaction or better, behavioral pricing models. The evolution of services and data analysis is currently underway in insurance, but its effect is still unclear. Our research surveyed 23 experts and 1542 customers to understand the potential path of this evolution and its impact on the Swiss insurance market.

Swiss customers have a strong preference for their current insurance company to provide services, and insurers enjoy a large reservoir of goodwill in the market. However, there is real interest in additional services, and this is especially visible among younger customers. Insurers, therefore, may only have a limited time window to satisfy this demand. The competitors are more likely going to be specialized service providers, rather than established players in other industries. The exception may be technology companies which, in spite of not enjoying high consumer trust, can leverage data capabilities, capillary access and low-cost platforms. There are no significant differences in the current customer portfolios of the different insurance companies, suggesting an early stage of market development and the opportunity for incumbents to influence its evolution.

Our results indicate that customers are particularly interested in prevention and assistance services. These are also the types of services that hold the potential for long-term impact on the industry. Once concerns about information privacy have been satisfactorily addressed, integration with non-insurance services is likely to provide an impulse for further structural changes. Experts in the industry by and large recognize this dynamic. The industry, however, seems to be focused on optimizing internal costs rather than improving their value delivery to customers. This is especially significant for prevention and risk management services: customers show interest in them and are open to sourcing them outside the industry; insurance experts recognize this dynamic, but companies are not placing sufficient focus on developing them. These services can influence customer behavior or at the very least provide better information about this behavior, therefore influencing the risk profile and pricing of insurers’ portfolios. Prevention services offer the potential for significant improvements and the threat of disruption from new providers. They should, therefore, be prioritized by incumbents.

This research was focused on German-speaking Swiss customers and it would be interesting to understand how the perception of services in insurance and the willingness to share information changes in other countries. Similarly, it would be interesting to expand the set of experts to reflect a broader view from the industry. The survey was designed to provide one particular example by type of service, and this approach may have biased the responses. Future efforts could investigate how responses may differ for different services. The responses do not show differences among the customers of different insurance companies, and it would be interesting to understand when and how they start to diverge. The current literature links the impact of big data and digitalization to companies’ business models. As the offering of services in insurance evolves, it will be interesting to investigate and understand how successful business models are evolving. The market pull for services and the availability of technology solutions to provide them may significantly alter the dynamics of the insurance industry in the medium term.

Insurance companies should continue to trust their internal experts and expand service offerings, especially those focused on prevention, to add value to customers rather than concentrating on cost optimization. They have a window of opportunity to establish themselves with more comprehensive offerings. This window may close quickly, however, as other players may establish wider, deeper and more meaningful customer interactions through services. If this occurs, they may potentially find themselves relegated to the role of pure risk carrier and commoditized.

Author Contributions

Research design, survey design, analysis, writing: C.P.; survey design, review: M.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

The authors would like to thank Ulrich Moser, Anne-Katrin Maser, Miriam Hürster, Tiziano Lenoci, Raphael Troitzsch, Kai Kunze, Angela Zeier Röschmann, Christoph Geering, Benno Keller, Sebastian Pfister, Julian Stylianou and Mathew Chittazhathu for their guidance and insightful feedback.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Customer interest in services. (1 = not interested at all; 6 = very interested).

| Service | Interest | Gender | M | F | p-Value | Age | 18–25 | 26–35 | 36–50 | >50 | p-Value |

|---|---|---|---|---|---|---|---|---|---|---|---|

| N= | 592 | 759 | N= | 331 | 369 | 342 | 312 | ||||

| Auto/Mobility | |||||||||||

| Protection/Administration | 3.59 | 3.71 | 3.51 | 0.02 | 3.66 | 3.54 | 3.73 | 3.45 | 0.11 | ||

| Prevention/Risk Management | 4.24 | 4.20 | 4.29 | 0.25 | 4.32 | 4.21 | 4.24 | 4.21 | 0.72 | ||

| Assistance/Emergency | 4.12 | 4.08 | 4.16 | 0.34 | 4.23 | 4.03 | 4.13 | 4.09 | 0.28 | ||

| Cost Control/Claims Management | 3.64 | 3.67 | 3.63 | 0.63 | 3.80 | 3.72 | 3.65 | 3.39 | <0.01 * | ||

| Life Services | 3.31 | 3.36 | 3.28 | 0.36 | 3.51 | 3.29 | 3.30 | 3.14 | 0.02 | ||

| Home/Living | |||||||||||

| Protection/Administration | 3.45 | 3.50 | 3.42 | 0.30 | 3.63 | 3.43 | 3.53 | 3.22 | <0.01 * | ||

| Prevention/Risk Management | 3.74 | 3.76 | 3.73 | 0.72 | 3.82 | 3.74 | 3.82 | 3.57 | 0.13 | ||

| Assistance/Emergency | 3.51 | 2.38 | 2.19 | 0.30 | 3.76 | 3.53 | 3.56 | 3.16 | <0.001 ** | ||

| Cost Control/Claims Management | 3.34 | 3.38 | 3.32 | 0.50 | 3.52 | 3.46 | 3.39 | 2.97 | <0.001 ** | ||

| Life Services | 4.08 | 3.98 | 4.16 | 0.02 | 4.19 | 4.02 | 4.09 | 4.02 | 0.34 | ||

| Health/Wellness | |||||||||||

| Protection/Administration | 3.72 | 3.72 | 3.72 | 0.98 | 3.90 | 3.85 | 3.67 | 3.40 | <0.001 ** | ||

| Prevention/Risk Management | 3.28 | 3.24 | 3.32 | 0.37 | 3.75 | 3.38 | 3.27 | 2.69 | <0.001 ** | ||

| Assistance/Emergency | 3.00 | 3.08 | 2.94 | 0.09 | 3.25 | 3.04 | 2.99 | 2.69 | <0.001 ** | ||

| Cost Control/Claims Management | 3.57 | 3.62 | 3.54 | 0.36 | 3.81 | 3.53 | 3.64 | 3.29 | <0.001 ** | ||

| Life Services | 2.82 | 2.92 | 2.74 | 0.04 | 3.27 | 2.91 | 2.82 | 2.23 | <0.001 ** | ||

| Cross-LoB | |||||||||||

| Policy recommendations | 3.52 | 3.56 | 3.49 | 0.44 | 3.62 | 3.55 | 3.64 | 3.25 | <0.01 * | ||

| Automated coverage advice | 3.48 | 3.52 | 3.46 | 0.49 | 3.74 | 3.43 | 3.55 | 3.21 | <0.001 ** | ||

| Automated coverage adjustment | 3.25 | 3.31 | 3.21 | 0.22 | 3.55 | 3.22 | 3.32 | 2.88 | <0.001 ** | ||

| Automated claims process | 3.71 | 3.72 | 3.70 | 0.80 | 3.87 | 3.79 | 3.77 | 3.37 | <0.001 ** |

** indicates α < 0.001; * indicates α < 0.01.

Table A2.

Customer willingness to share information (WSI). (1 = not willing to share at all; 6 = no problem to share the information).

Table A2.

Customer willingness to share information (WSI). (1 = not willing to share at all; 6 = no problem to share the information).

| Information | WSI | Gender | M | F | p-Value | Age | 18–25 | 26–35 | 36–50 | >50 | p-Value |

|---|---|---|---|---|---|---|---|---|---|---|---|

| N= | 592 | 759 | N= | 331 | 369 | 342 | 312 | ||||

| New car purchase | 4.27 | 4.40 | 4.18 | 0.01 | 4.30 | 4.44 | 4.30 | 4.01 | <0.01 * | ||

| Vehicle information | 4.08 | 4.13 | 4.04 | 0.33 | 4.15 | 4.08 | 4.09 | 3.97 | 0.59 | ||

| Crash sensor data | 3.83 | 3.95 | 3.74 | 0.02 | 3.80 | 3.96 | 3.85 | 3.68 | 0.21 | ||

| Daily schedule | 2.51 | 2.63 | 2.42 | 0.02 | 2.72 | 2.52 | 2.42 | 2.39 | 0.05 | ||

| Current location and history | 2.70 | 2.88 | 2.56 | <0.001 ** | 2.69 | 2.51 | 2.73 | 2.90 | 0.02 | ||

| Purchasing information | 3.50 | 3.48 | 3.53 | 0.57 | 3.63 | 3.57 | 3.42 | 3.36 | 0.16 | ||

| Emergency sensors in the house | 3.85 | 4.00 | 3.73 | <0.01 * | 3.87 | 3.97 | 3.82 | 3.72 | 0.28 | ||

| Smart home data w/o camera | 2.73 | 2.85 | 2.64 | 0.03 | 2.87 | 2.67 | 2.73 | 2.67 | 0.37 | ||

| Smart home data w/camera | 2.18 | 2.35 | 2.05 | <0.001 ** | 2.26 | 2.17 | 2.19 | 2.08 | 0.59 | ||

| Sports: training plan and activities | 3.32 | 3.39 | 3.27 | 0.21 | 3.77 | 3.42 | 3.13 | 2.93 | <0.001 ** | ||

| Health monitoring | 3.39 | 3.43 | 3.35 | 0.40 | 3.80 | 3.46 | 3.18 | 3.08 | <0.001 ** | ||

| Chronic conditions | 3.20 | 3.31 | 3.13 | 0.06 | 3.72 | 3.20 | 2.97 | 2.91 | <0.001 ** |

** indicates α < 0.001; * indicates α < 0.01.

References

- Adrodegari, Federico, and Nicola Saccani. 2017. Business models for the service transformation of industrial firms. The Service Industries Journal 37: 57–83. [Google Scholar] [CrossRef]

- Arisov, Elisabeth, Johannes Becker, Matthias Erny, and Angela Zeier Röschmann. 2019. Individualisierte Versicherungslösungen in einer Digitalen Welt. Winterthur: ZHAW School of Management and Law. [Google Scholar] [CrossRef]

- Baecke, Philippe, and Lorenzo Bocca. 2017. The Value of Vehicle Telematics Data in Insurance Risk Selection Processes. Decision Support Systems 98: 69–79. [Google Scholar] [CrossRef]

- Bain & Company. 2017. Building Connections—And Profits—With Ecosystem Services. In Customer Behavior and Loyalty in Insurance: Global Edition 2017. Boston: Bain & Company. [Google Scholar]

- Bain & Company. 2018. Customers Know What They Want. Are Insurers Listening? In Customer Behavior and Loyalty in Insurance: Global Edition 2018. Boston: Bain & Company. [Google Scholar]

- Beer, Simone, Alexander Braun, Pascal Bühler, Martin Eling, Peter Maas, Lukas Reichel, Matthias Rüfenacht, Philipp Schaper, Hato Schmeiser, Florian Schreiber, and et al. 2017. Assekuranz 2025: Quo Vadis? St. Gallen: Verlag Institut für Versicherungswirtschaft der Universität St. Gallen. [Google Scholar]

- Borna, Shaheen, and Stephen Avila. 1999. Genetic Information: Consumers’ Right to Privacy Versus Insurance Companies’ Right to Know a Public Opinion Survey. Journal of Business Ethics 19: 355–62. [Google Scholar] [CrossRef]

- Bouwman, Harry, Shahrokh Nikou, Francisco J. Molina-Castillo, and Mark de Reuver. 2018. The Impact of Digitalization on Business Models. Digital Policy, Regulation and Governance 20: 105–24. [Google Scholar] [CrossRef]

- Buehler, Pascal, and Peter Maas. 2016. Kunden Transformieren die Versicherungsmärkte|Digitale Transformation im Unternehmen Gestalten. Munich: Carl Hanser Verlag, pp. 99–113. [Google Scholar]

- Cappiello, Antonella. 2020. The Digital (R)evolution of Insurance Business Models. American Journal of Economics and Business Administration 1: 13. [Google Scholar] [CrossRef]

- Cardon, James H., and Igal Hendel. 2001. Asymmetric Information in Health Insurance: Evidence from the National Medical Expenditure Survey. The RAND Journal of Economics 32: 408–27. [Google Scholar] [CrossRef]

- Culnan, Mary J., and Pamela K. Armstrong. 1999. Information Privacy Concerns, Procedural Fairness, and Impersonal Trust: An Empirical Investigation. Organization Science 10: 104–15. [Google Scholar] [CrossRef]

- Deraëd, Pierre, and Julia Henry. 2012. Was Versicherungskunden Wirklich Wollen. Zurich: Bain & Company. [Google Scholar]

- Eling, Martin, and Martin Lehmann. 2018. The Impact of Digitalization on the Insurance Value Chain and the Insurability of Risks. The Geneva Papers 43: 359–96. [Google Scholar] [CrossRef]

- Garth, Denise, and Glenn Westlake. 2018. Digital Insurance 2.0: Playbooks for P&C Insurers to Win in the Digital Age. New York: Majesco, Available online: https://www.majesco.com/resources/digital-insurance-2-playbooks-for-pc-insurers/data (accessed on 23 June 2018).

- Kehr, Flavius, Daniel Wentzel, and Peter Mayer. 2013. Rethinking the Privacy Calculus: On the Role of Dispositional Factors and Affect. Presented at the Thirty Fourth International Conference on Information Systems, Milan, Italy, December 15–18. [Google Scholar]

- Kotalakidis, Nikos, Henrik Naujoks, and Florian Mueller. 2016. Digitalisierung der Versicherungswirtschaft: Die 18-Milliarden-Chance. Munich and Zurich: Bain & Company. [Google Scholar]

- Manyika, James, Michael Chui, Brad Brown, Jacques Bughin, Richard Dobbs, Charles Roxburgh, and Angela Hung Byers. 2011. Big Data, the New Frontier for Innovation, Competition and Productivity. McKinsey Global Institute. [Google Scholar]

- Metzger, Miriam J. 2004. Privacy, Trust, and Disclosure: Exploring Barriers to Electronic Commerce. Journal of Computer-Mediated Communication 9: JCMC942. [Google Scholar] [CrossRef]

- Milne, George R., and Mary Ellen Gordon. 1993. Direct Mail Privacy-Efficiency Trade-offs within an Implied Social Contract Framework. Journal of Public Policy & Marketing 12: 206–15. [Google Scholar]

- Neely, Andy. 2008. Exploring the financial consequences of the servitization in manufacturing. Operations Management Research 1: 103–18. [Google Scholar] [CrossRef] [Green Version]

- Normann, Richard. 2001. Service Management: Strategy and Leadership in Service Business, 3rd ed. New York: Wiley & Sons, p. 256. ISBN 10: 0471494399. [Google Scholar]

- Opresnik, David, and Marco Taisch. 2015. The value of Big Data in servitization. International Journal of Production Economics 165: 174–84. [Google Scholar] [CrossRef]

- Pugnetti, Carlo, and Sandra Elmer. 2020. Self-Assessment of Driving Style and the Willingness to Share Personal Information. Journal of Risk and Financial Management 13: 53. [Google Scholar] [CrossRef] [Green Version]

- Rothschild, Michael, and Joseph Stiglitz. 1976. Equilibrium in Competitive Insurance Markets: An Essay on the Economics of Imperfect Information. Quarterly Journal of Economics 90: 629–49. [Google Scholar] [CrossRef] [Green Version]

- Simpson, Thomas W. 2012. What Is Trust? Pacific Philosophical Quarterly 93: 550–69. [Google Scholar] [CrossRef]

- Smith, H. Jeff, Tamara Dinev, and Heng Xu. 2011. Information Privacy Research: An Interdisciplinary Review. MIS Quarterly 35: 989–1015. [Google Scholar] [CrossRef] [Green Version]

- Steiner, Philipp Hendrik, and Peter Maas. 2018. When customers are willing to disclose information in the insurance industry: A multi-group analysis comparing ten countries. International Journal of Bank Marketing 36: 1015–33. [Google Scholar] [CrossRef]

- Stone, Eugene F., and Dianna L. Stone. 1990. Privacy in Organizations: Theoretical Issues, Research Findings, and Protection Mechanisms. Research in Personnel and Human Resources Management 8: 349–411. [Google Scholar]

- The Economist. 2017. The World’s Most Valuable Resource Is No Longer Oil, But Data. Available online: https://www.economist.com/leaders/2017/05/06/the-worlds-most-valuable-resource-is-no-longer-oil-but-data (accessed on 14 June 2020).

- Vandermerwe, Sandra, and Juan Rada. 1988. Servitization of business: Adding value by adding services. European Management Journal 6: 314–24. [Google Scholar] [CrossRef]

- Wamba, Samuel Fosso, Shahriar Akter, Andrew James Edwards, Geoffrey Chopin, and Denis Gnanzou. 2015. How ‘big data’ can make big impact: Findings from a systematic review and a longitudinal case study. International Journal of Production Economics 165: 234–46. [Google Scholar] [CrossRef]

- Zolnowski, Andreas, Towe Christiansen, and Jan Gudat. 2016. Business Model Transformation Patterns of Data-Driven Innovations. Research Papers, 146. Available online: https://aisel.aisnet.org/ecis2016_rp/146 (accessed on 14 June 2020).

Figure 1.

Experts’ view on adoption and impact of services.

Figure 2.

Experts’ view by line of business and type of service.

Figure 3.

Customer interest and WSI by service.

Figure 4.

Customer interest and WSI by line of business and type of service.

Figure 5.

Preference for service provider by industry.

Figure 6.

Expert vs. customer view of adoption.

Figure 7.

Expert vs. customer view of impact.

Table 1.

Research structure.

| Industry Perspective Expert Survey | Market Perspective Customer Survey | |

|---|---|---|

| Evolution of services | Adoption in 3–5 years | Interest vs. perceived “cost” of information needed |

| Impact of services | Impact in 5–10 years | Provider preference |

Table 2.

Services surveyed, detailed by line of business and type of service.

| Protection/ Administration | Prevention/ Risk Mgmt. | Assistance/ Emergency | Cost Control/ Claims Mgmt. | Life Services 1 | |

|---|---|---|---|---|---|

| Auto/Mobility | Automated policy changes based on new car purchase | Real-time warnings/recommendations while driving | Automated emergency call triggered in case of accident | Coordination of repair garage, replacement car, etc. | Location-based enabled services such as wash service, pickup, etc. |

| Home/Living | Policy updates after new construction/repairs | Automatic shutoff of water, gas, etc., in case of emergency | Dispatch contractor if flooding detected | Automated scheduling of inspections, repairs, etc. | Elder care—notification if bed not used/fridge not opened for 12 h |

| Health/Wellness | Automated processing of medical bills | Automated nutrition recommendations based on health monitoring | Automated scheduling of doctor visit based on critical health stats | Access to specialized provider network for chronic health conditions | Scheduling gym time when on travel in a new location based on calendar |

| Other/Cross-LoB | Policy analysis and recommendation for changes | Individualized, automated coverage advice | Automated coverage adjustment/dynamic insurance adjustments | Automated coverage adjustment/dynamic insurance adjustments | |

1 non-insurance-specific services.

Table 3.

Approach for addressing each research question.

| Research Question | Approach | |

|---|---|---|

| 1. | How are Swiss insurance companies addressing the opportunities offered by data-driven services and do they see a long-term impact on the structure of the industry? | Expert survey: adoption in 3–5 years and impact in 5–10 years of each service. |

| 2. | Which insurance-related services are Swiss customers interested in, and how do they value the information needed to provide them? How do these results differ by gender, age cohort, and current insurance provider? | Customer survey: interest in purchasing service and perceived value of the information required to provide the service. Analysis by gender, age cohort and named insurance provider. |

| 3. | How open are Swiss insurance customers to sourcing insurance-related services from non-insurers? | Customer survey: preference for provider by industry for each service. |

| 4. | How well does the view of insurance experts match customer priorities? | Evolution of services: comparison of customer interest in purchasing and the perceived cost of information by service vs. expert view of adoption in 3–5 years. Impact of services: comparison of customer preference in sourcing from non-insurance player vs. expert view of impact in 5–10 years. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Pugnetti, C.; Seitz, M. Data-Driven Services in Insurance: Potential Evolution and Impact in the Swiss Market. J. Risk Financial Manag. 2021, 14, 227. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050227

AMA Style

Pugnetti C, Seitz M. Data-Driven Services in Insurance: Potential Evolution and Impact in the Swiss Market. Journal of Risk and Financial Management. 2021; 14(5):227. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050227

Chicago/Turabian StylePugnetti, Carlo, and Mischa Seitz. 2021. "Data-Driven Services in Insurance: Potential Evolution and Impact in the Swiss Market" Journal of Risk and Financial Management 14, no. 5: 227. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050227