Time-Varying Nexus between Investor Sentiment and Cryptocurrency Market: New Insights from a Wavelet Coherence Framework

Abstract

:1. Introduction and Literature Background

2. Materials and Methods

2.1. The Wavelet Coherence Analysis

2.2. The Multivariate Wavelet

2.3. The Phase and Antiphase Relationship

2.4. Data Description

3. Findings and Discussions

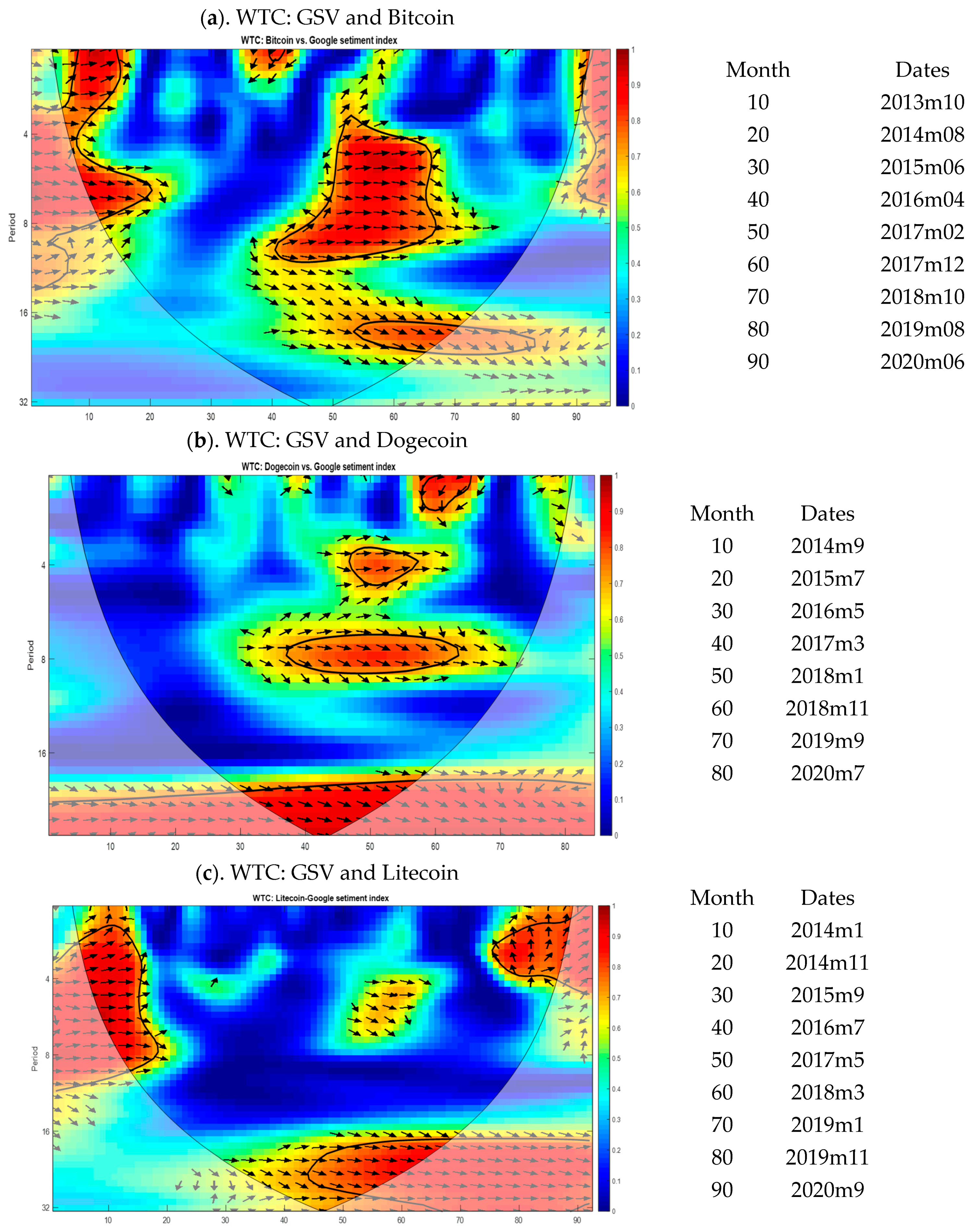

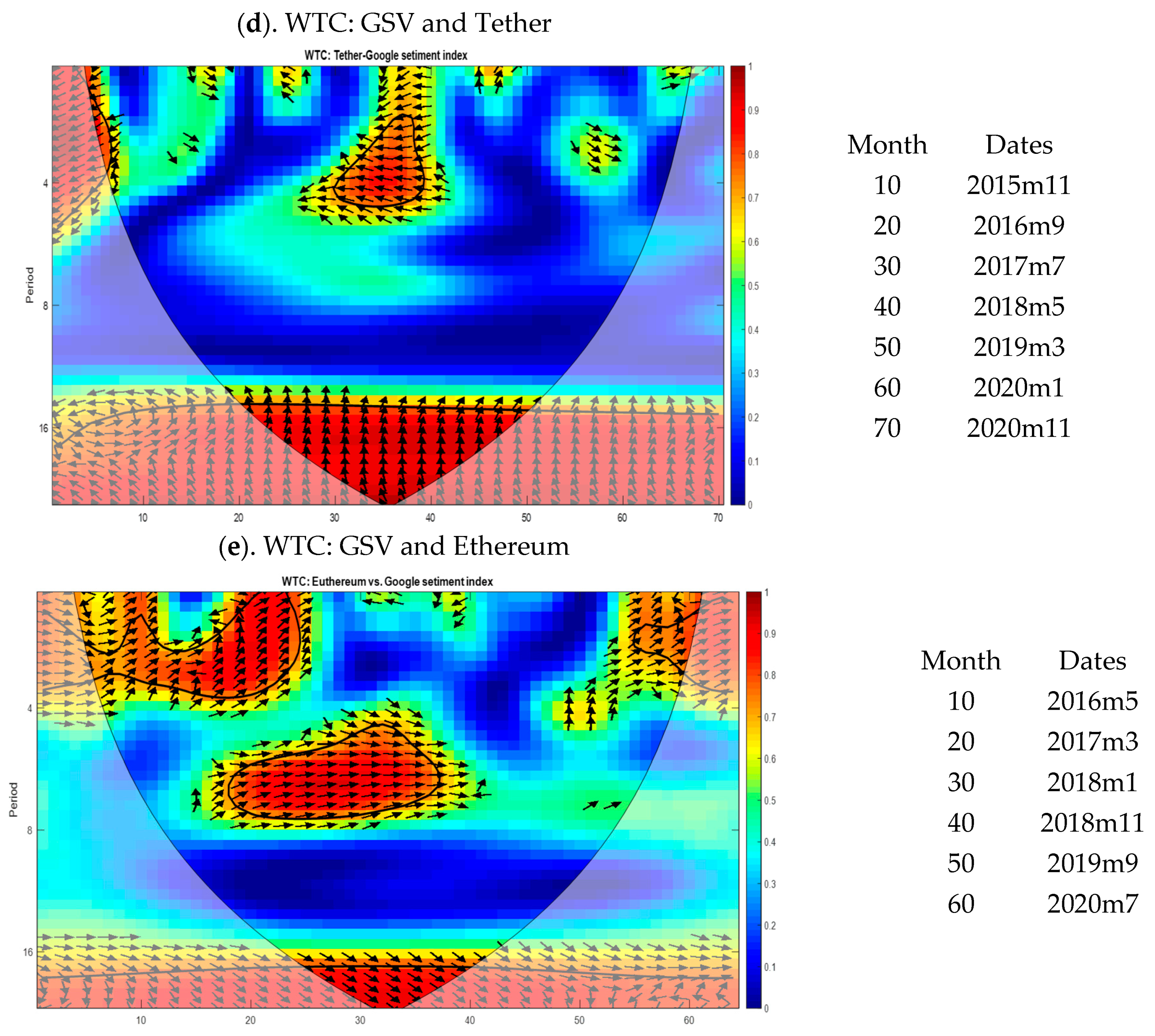

3.1. Wavelet Coherency Analysis of CC Prices

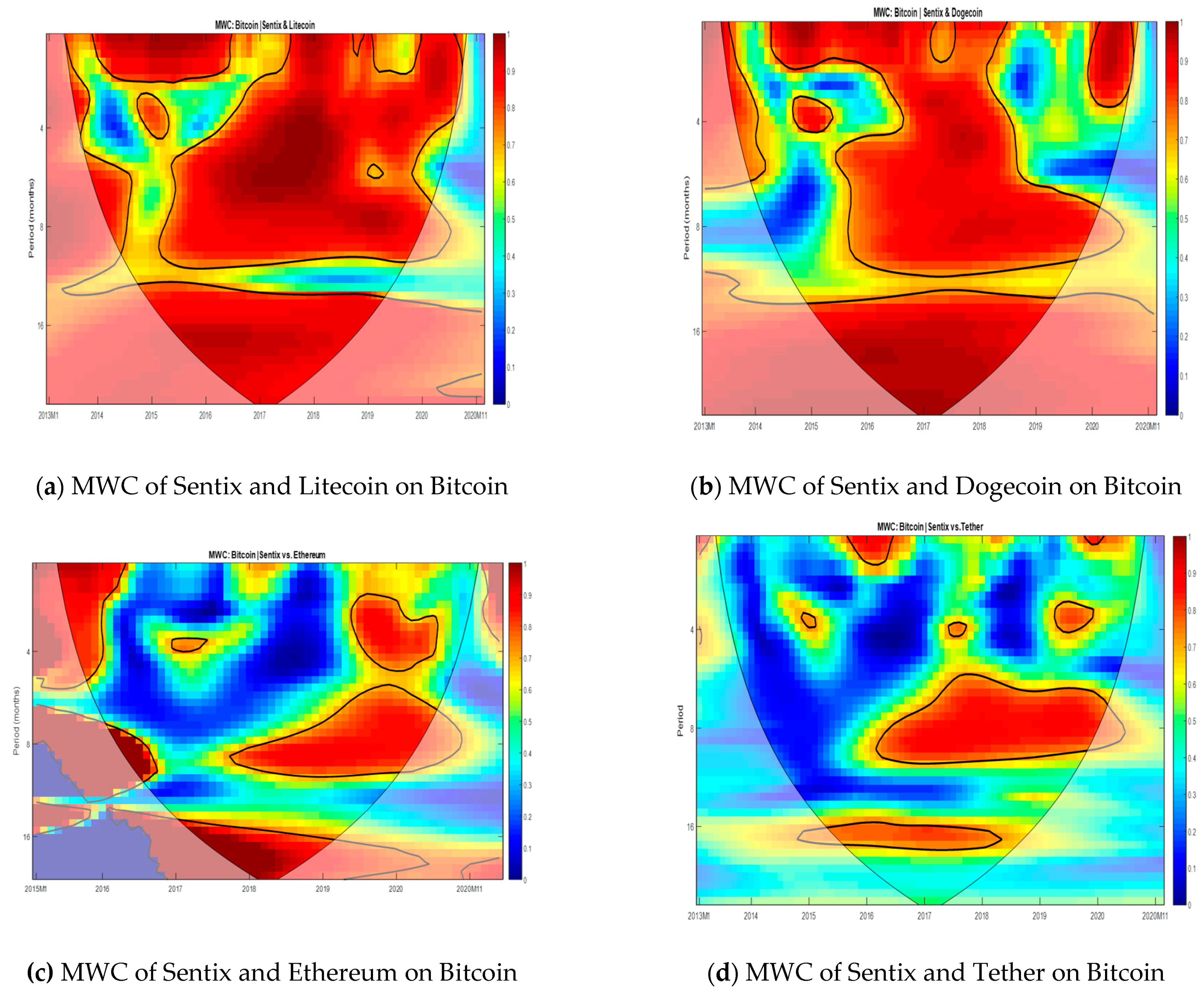

3.2. The Nexuses between Bitcoin, Altcoins, and Sentix Cryptocurrencies Index

3.2.1. Interaction between CC Prices and Sentix Cryptocurrencies Index

3.2.2. Multivariate Analysis: CC vs. Sentix Cryptocurrency Index

4. Robustness Check and Discussion

5. Concluding Remarks

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Aalborg, Halvor Aarhus, Molnár Peter, and Jon Erik de Vries. 2019. What can explain the price, volatility and trading volume of Bitcoin? Finance Research Letters 29: 255–65. [Google Scholar] [CrossRef]

- Aysan, Ahmet Faruk, Ender Demir, Giray Gozgor, and Chi Kenug Marco Lau. 2019. Effects of the geopolitical risks on Bitcoin returns and volatility. Research in International Business Finance 47: 511–18. [Google Scholar] [CrossRef] [Green Version]

- Baig, Ahmed, Benjamin M. Blau, and Nasim Sabah. 2019. Price Clustering and Sentiment in Bitcoin. Finance Research Letters 29: 111–16. [Google Scholar] [CrossRef]

- Bariviera, Aurelio F. 2017. The inefficiency of Bitcoin revisited: A dynamic approach. Economics Letters 161: 1–4. [Google Scholar] [CrossRef] [Green Version]

- Bouoiyour, Jamal, Refk Selmi, Aviral K. Tiwari, and Muhammad Shahbaz. 2015. The nexus between oil price and Russia’s real exchange rate: Better paths via unconditional vs. conditional analysis. Energy Economics 51: 54–66. [Google Scholar] [CrossRef] [Green Version]

- Burggraf, Tobias, Toan Luu Duc Huynh, Markus Rudolf, and Mei Wang. 2020. Do FEARS drive Bitcoin? Review of Behavioral Finance. [Google Scholar] [CrossRef]

- Chen, Conghui, Lanlan Liu, and Ningru Zhao. 2020. Fear Sentiment, Uncertainty, and Bitcoin Price Dynamics: The Case of COVID-19. Emerging Markets Finance and Trade 56: 2298–309. [Google Scholar] [CrossRef]

- Chu, Jeffrey, Yuanyuan Zhang, and Stephen Chan. 2019. The adaptive market hypothesis in the high frequency cryptocurrency market. International Review of Financial Analysis 64: 221–31. [Google Scholar] [CrossRef]

- Ciaian, Pavel, Miroslava Rajcaniova, and DArtis Kancs. 2018. Virtual relationships: Short- and long-run evidence from BitCoin and altcoin markets. Journal of International Financial Markets, Institutions and Money 52: 173–95. [Google Scholar] [CrossRef]

- Conlon, Tomas, and Richard McGee. 2020. Safe haven or risky hazard? Bitcoin during the COVID-19 bear market. Finance Research Letters 35: 101607. [Google Scholar] [CrossRef]

- Corbet, Shaen, Andrew Meegan, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2018. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economic Letters 165: 28–34. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Brian Lucey, Andrew Urquhart, and Larisa Yarovaya. 2019. Cryptocurrencies as a financial asset: A systematic analysis. International Review of Financial Analysis 62: 182–99. [Google Scholar] [CrossRef] [Green Version]

- Corbet, Shaen, Charles Larkin, and Brian Lucey. 2020. The Contagion Effects of the COVID-19 Pandemic: Evidence from Gold and Cryptocurrencies. Finance Research Letters 35: 101554. [Google Scholar] [CrossRef]

- Da, Zhi, Joseph Engelberg, and Pengjie Gao. 2011. In Search of Attention. The Journal of Finance 66: 1461–99. [Google Scholar] [CrossRef]

- Demir, Ender, Giray Gozgor, Chi Keung Marco Lau, and Samuel A. Vigne. 2018. Does economic policy uncertainty predict the Bitcoin returns? An empirical investigation. Finance Research Letters 26: 145–49. [Google Scholar] [CrossRef] [Green Version]

- Demir, Ender, Mehmet Huseyin Bilgin, Gokhan Karabulut, and Asli Cansin Doker. 2020. The Relationship between Cryptocurrencies and COVID-19 Pandemic. Available online: https://www.ssrn.com/abstract=3585147 (accessed on 25 April 2020).

- Drobetz, Wolfgang, Paul. P. Momtaz, and Henning Schroder. 2019. Investor Sentiment and Initial Coin Offerings. The Journal of Alternative Investments 21: 41–55. [Google Scholar] [CrossRef]

- Eom, Cheoljun, Taisei Kaizoji, Sang Hoon Kang, and Lukas Pichl. 2019. Bitcoin and investor sentiment: Statistical characteristics and predictability. Physica A: Statistical Mechanics Its Applications 514: 511–21. [Google Scholar] [CrossRef]

- Fang, Libing, Elie Bouri, Rangan Gupta, and David Roubaud. 2019. Does global economic uncertainty matter for the volatility and hedging effectiveness of Bitcoin? International Review of Financial Analysis 61: 29–36. [Google Scholar] [CrossRef]

- Gao, Zhenyu, Haohan Ren, and Bohui Zhang. 2020. Googling investor sentiment around the world. Journal of Financial and Quantitative Analysis 55: 549–80. [Google Scholar] [CrossRef] [Green Version]

- Griffin, John, and Amin Shams. 2020. Is Bitcoin Really Un-Tethered? The Journal of Finance 75: 1913–64. [Google Scholar] [CrossRef]

- Guègan, Dominique, and Thomas Renault. 2020. Does investor sentiment on social media provide robust information for Bitcoin returns predictability? Finance Research Letters 38: 101494. [Google Scholar] [CrossRef]

- Gurdgiev, Constantin, and Daniel OLoughlin. 2020. Herding and Anchoring in Cryptocurrency Markets: Investor Reaction to Fear and Uncertainty. Journal of Behavioral and Experimental Finance 25: 100271. [Google Scholar] [CrossRef]

- Härdle, Wolfgang Karl, Campbell R. Harvey, and Raphael C. G. Reule. 2020. Understanding cryptocurrencies. Journal of Financial Econometrics 18: 181–208. [Google Scholar] [CrossRef]

- Joseph, Kissan, Babajide M. Wintoki, and Zelin Zhang. 2011. Forecasting Abnormal Return and Trading Volume Using Investor Sentiment: Evidence from Online Search. International Journal of Forecasting 27: 1–21. [Google Scholar] [CrossRef]

- Karalevicius, Vytautas, Niels Degrande, and J. De Weerdt. 2018. Using sentiment analysis to predict interaday Bitcoin price movements. The Journal of Risk Finance 19: 56–75. [Google Scholar] [CrossRef]

- Asif Khan, Muhammad, Rubi Ahmad, Anna Azmi, and Muhammad Akbar. 2019. A new sentiment index for the Islamic stock market. Investment Analysts Journal 48: 146–72. [Google Scholar] [CrossRef]

- Kraajeveld, Olivier, and Johannes De Smed. 2020. The predictive power of public Twitter sentiment for forecasting cryptocurrency prices. Journal of International Financial Markets, Institutions and Money 65: 101188. [Google Scholar] [CrossRef]

- Kristoufek, Ladislav. 2013. BitCoin meets Google Trends and Wikipedia: Quantifying the relationship between phenomena of the Internet era. Scientific Reports 3: 3415. [Google Scholar] [CrossRef] [Green Version]

- Lansky, Jan. 2016. Analysis of Cryptocurrencies Price Development. Acta Informatica Pragensia 5: 118–37. [Google Scholar] [CrossRef]

- Li, Tianyu Ray, Anup S. Chamrajnagar, Xander R. Fong, Nickolas R. Rizik, and Feng Fu. 2019. Sentiment-Based Prediction of Alternative Cryptocurrency Price Fluctuations Using Gradient Boosting Tree Model. Frontiers in Physics 7: 98. [Google Scholar] [CrossRef]

- Lopez-Cabarcos, M. Angeles, Adam M. Perez-Pico, Juan Pineiro-Chousa, and Alekxandar Sevic. 2019. Bitcoin volatility, stock market and investor sentiment. Are they connected? Finance Research Letters 38: 101399. [Google Scholar] [CrossRef]

- Mihanović, Hrvoje, Mirko Orlić, and Zoran Pasarić. 2009. Diurnal thermocline oscillations driven by tidal flow around an island in the Middle Adriatic. Journal of Marine Systems 78. [Google Scholar] [CrossRef]

- Nakamoto, Satochi. 2009. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://www.bitcoinpaper.info/bitcoinpaper-html/ (accessed on 10 January 2020).

- Nasir, Muhammad Ali, Toan Luu Duc Huynh, Sang Phu Nguyen, and Duy Duong. 2019. Forecasting cryptocurrency returns and volume using search engines. Finance Innovation 5: 2. [Google Scholar] [CrossRef]

- Ng, Eric K. W., and Johnny C. L. Chan. 2012. Geophysical applications of partial wavelet coherence and multiple wavelet coherence. Journal of Atmospheric and Oceanic Technology 29: 1845–53. [Google Scholar] [CrossRef]

- Nguyen, Thai Vu Hong, Binh Thanh Nguyen, Kien Son Nguyen, and Huy Pham. 2019. Asymmetric Monetary Policy Effects on Cryptocurrency Markets. Research in International Business and Finance 48: 335–39. [Google Scholar] [CrossRef]

- Philips, Ross C., and Denise Gorse. 2018. Cryptocurrency price drivers: Wavelet coherence analysis revisited. PLoS ONE 13. [Google Scholar] [CrossRef]

- Rognone, Lavinia, Stuart Hyde, and S. Sarah Zhang. 2020. News Sentiment in the Cryptocurrency Market: An Empirical Comparison with Forex. International Review of Financial Analysis 69: 101462. [Google Scholar] [CrossRef]

- Stavroyiannis, Stavros, Vassilios Babalos, Stelios Bekiros, Salim Lahmiri, and Gazi Salah Uddin. 2019. The high frequency multifractal properties of Bitcoin. Physica A: Statistical Mechanics Its Applications 520: 62–71. [Google Scholar] [CrossRef]

- Torrence, Christopher, and Gilbert P. Compo. 1998. A practical guide to wavelet analysis. Bulletin of the American Meteorological Society 79: 61–78. [Google Scholar] [CrossRef] [Green Version]

- Valencia, Franco, Alfonso Gómez-Espinosa, and Benjamin Valdés-Aguirre. 2019. Price Movement Prediction of Cryptocurrencies Using Sentiment Analysis and Machine Learning. Entropy 21: 589. [Google Scholar] [CrossRef] [Green Version]

- Yermack, David. 2013. Is Bitcoin a real currency? An economic appraisal. National Bureau of Economic Research 36: 843–50. [Google Scholar]

- Yuneline, Mirza Hedismarlina. 2019. Analysis of cryptocurrency’s characteristics in four perspectives. Journal of Asian Business and Economic Studies 26: 206–19. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Bitcoin | Dogecoin | Ethereum | Litecoin | SENTIX CC | Tether | |

|---|---|---|---|---|---|---|

| Mean | 2601.647 | 0.001381 | 217.8344 | 33.36953 | −42.88281 | 0.173776 |

| Median | 684.35 | 0.000316 | 180.015 | 7.105 | −46.25 | 0.009113 |

| Maximum | 13,850.4 | 0.008972 | 1118.31 | 232.1 | −21.5 | 1.877742 |

| Minimum | 218.5 | 0.000103 | 0.738644 | 1.44 | −61.5 | 0.004111 |

| Std. Dev. | 3298.403 | 0.001873 | 225.1042 | 49.98785 | 11.38285 | 0.322237 |

| Skewness | 1.480963 | 1.953783 | 1.640499 | 2.205586 | 0.497164 | 2.948231 |

| Kurtosis | 4.313236 | 6.748212 | 6.399608 | 7.739697 | 2.107605 | 13.98628 |

| Jarque–Bera | 27.9936 | 78.1818 | 59.52608 | 111.7951 | 4.760148 | 414.5779 |

| Probability | 0.000001 *** | 0.000 *** | 0.000 *** | 0.000 *** | 0.092544 *** | 0.000 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

AlNemer, H.A.; Hkiri, B.; Khan, M.A. Time-Varying Nexus between Investor Sentiment and Cryptocurrency Market: New Insights from a Wavelet Coherence Framework. J. Risk Financial Manag. 2021, 14, 275. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14060275

AlNemer HA, Hkiri B, Khan MA. Time-Varying Nexus between Investor Sentiment and Cryptocurrency Market: New Insights from a Wavelet Coherence Framework. Journal of Risk and Financial Management. 2021; 14(6):275. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14060275

Chicago/Turabian StyleAlNemer, Hashem A., Besma Hkiri, and Muhammed Asif Khan. 2021. "Time-Varying Nexus between Investor Sentiment and Cryptocurrency Market: New Insights from a Wavelet Coherence Framework" Journal of Risk and Financial Management 14, no. 6: 275. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14060275