An Intergenerational Issue: The Equity Issues Due to Public–Private Partnerships; The Critical Aspect of the Social Discount Rate Choice for Future Generations

Abstract

:1. Introduction

2. Intergenerational Equity Issues

2.1. Intergenerational Equity Issues

2.1.1. Social Discount Rate Approaches

2.1.2. Temporal Choice of High or Low SDR Value

3. Intergenerational Equity Issues Caused by PPPs

3.1. Introduction

- A.

- What is the risk of PPPs’ debts being off-balance sheet?

- B.

- How do the intergenerational equity issues position the society within the SWF?

3.2. Criticality of SDR in PPPs Decision-Making Process

3.3. Issues Caused by the SDR Choice

3.3.1. The Risk of PPP Debt on the (Long-Term) Fiscal Deficit

3.3.2. Justice of Resource Distribution between Generations

4. Parameters of Social Discount Rates (SDR)

4.1. Social Time Preference Rate (STPR)

- (a)

- The time preference (ρ)

- (b)

- The elasticity of marginal utility (μ)

- (c)

- The growth rate estimation (g)

4.2. Marginal Social Opportunity Cost (SOC) of Capital

4.3. STPR and SOC from an Ethical Perspective

5. Ethical Theories Related to Intergenerational Equity

5.1. Merits of Libertarianism

5.2. Merits of an Egalitarian Society

5.3. Merits of a Utilitarian Society

5.4. Merits of a Rawlsian Society

5.5. Trade-Off between STPR and SOC within the Ethical Theories

6. Sensitivity of Intergenerational Matters to the Level of SDR

6.1. Economic Growth

6.2. Technological Evolution

6.3. Event Uncertainty

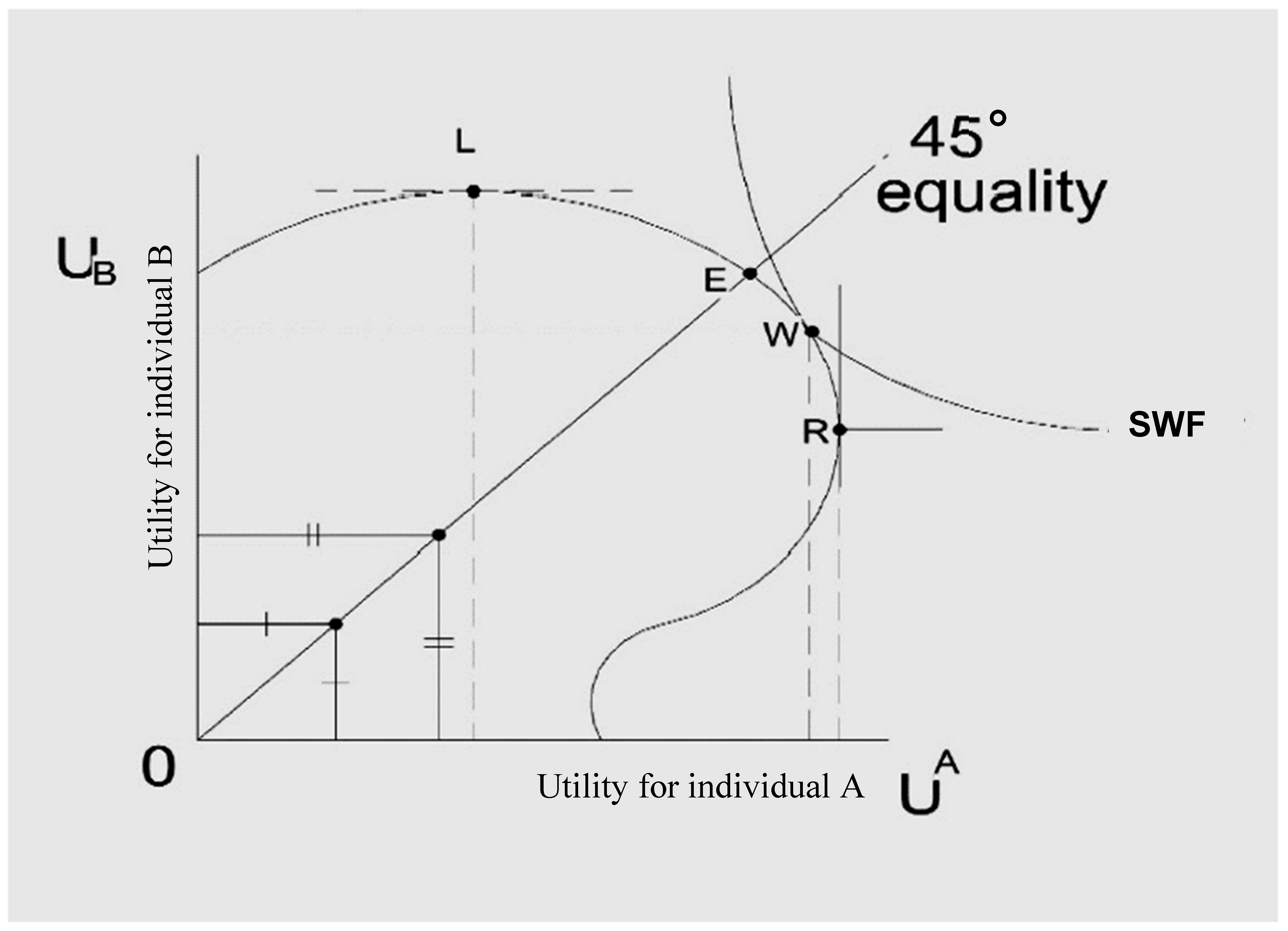

7. The Position of the State on the Social Welfare Function Based on the Used SDR

7.1. The Social Welfare Function (SWF)

7.2. UK Application

8. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Glossary

| DMU | Diminishing Marginal Utility |

| GDP | Gross Domestic Product |

| GFS | Government Finance Statistics |

| NPV | Net Present Value |

| MCF | Marginal Cost of Funds Criterion |

| PIF | Private Finance Initiative |

| PPP | Public–Private Partnership |

| PSC | Public Sector Comparator |

| SDR | Social Discount Rate |

| SNA | System of National Accounts |

| SOC | Social Opportunity Cost |

| SPC | Shadow Price of Capital |

| STPR | Social Time Preference Rate |

| SWF | Social Welfare Function |

| UK | United Kingdom |

| VfM | Value for Money |

References

- Arneson, Richard. 2013. Egalitarianism. The Stanford Encyclopedia of Philosophy (Summer 2013 Edition). Edited by Edward N. Zalta. Available online: https://plato.stanford.edu/archives/sum2013/entries/egalitarianism/ (accessed on 15 September 2019).

- Arrow, Kenneth. J. 1995. Discounting Climate Change Planning for an Uncertain Future. In Lecture Given at Institut d’Economie Industrielle. Toulouse: Université des Sciences Sociales, Available online: http://idei.fr/sites/default/files/medias/doc/conf/annual/paper_1995.pdf (accessed on 18 November 2021).

- Attfield, Robin. 1998. Environmental Ethics and Intergenerational Equity. Inquiry 41: 207–22. [Google Scholar] [CrossRef]

- Azfar, Omar. 1999. Rationalizing Hyperbolic Discounting. Journal of Economic Behavior and Organization 38: 245–52. [Google Scholar] [CrossRef]

- Baumol, William J. 1968. On the social rate of discount. The American Economic Review 58: 788–802. [Google Scholar]

- Blaiklock, T. Martin. 2011. Public Sector Comparators and Value for Money in PPP. Available online: https://publications.parliament.uk/pa/cm201012/cmselect/cmtreasy/1146/1146vw06.htm (accessed on 18 November 2021).

- Boardman, Anthony E., David H. Greenberg, Aidan R. Vining, and David L. Weimer. 2017. Cost-Benefit Analysis: Concepts and Practice. Cambridge: Cambridge University Press. [Google Scholar]

- Börzel, Tanja A., and Thomas Risse. 2005. Public-private partnerships: Effective and Legitimate Tools of International Governance? In Complex Sovereignty: Reconstructing Political Authority in the Twenty First Century. Edited by Edgard Grande and Louis W. Pauly. Toronto: University of Toronto Press, pp. 195–216. [Google Scholar] [CrossRef]

- Braun, Virginia, and Victoria Clarke. 2006. Using thematic analysis in psychology. Qualitative Research in Psychology 3: 77–101. [Google Scholar] [CrossRef] [Green Version]

- Broome, John. 1992. Counting the Cost of Global Warming. Cambridge: The White Horse Press. [Google Scholar]

- Broome, John. 2008. The ethics of climate change. Scientific American 298: 96–102. [Google Scholar] [CrossRef]

- Broome, John. 2012. Climate Matters: Ethics in a Warming World, 1st ed. New York: WW Norton & Company. [Google Scholar]

- Broome, John, and Duncan K. Foley. 2016. A World Climate Bank’. In Institutions for Future Generations. Edited by Iñigo González-Ricoy and Axel Gosseries. Oxford: Oxford University Press, pp. 156–69. [Google Scholar]

- Burgess, David F. 1989. The social opportunity cost of capital in the presence of labour market distortions. Canadian Journal of Economics 22: 245–62. [Google Scholar] [CrossRef]

- Burgess, David F., and Richard O. Zerbe. 2011. Appropriate Discounting for Benefit-Cost Analysis. Journal of Benefit-Cost Analysis 2: 1–20. [Google Scholar] [CrossRef]

- Chakravarty, Sukhamoy. 1962. The Existence of an Optimum Savings Program. Econometrica 30: 178–87. [Google Scholar] [CrossRef] [Green Version]

- Contreras, Carlos. 2014. Value for Money: To what extent does discount rate matter? Revista de Economía Aplicada 22: 93–112. [Google Scholar]

- Coyle, Diane, and Marianne Sensier. 2019. The imperial treasury: Appraisal methodology and regional economic performance in the UK. Regional Studies 54: 283–95. [Google Scholar] [CrossRef] [Green Version]

- Dasgupta, Partha S., and Geoffrey M. Heal. 1979. Economic Theory and Exhaustible Resources. Welwyn: Nisbet. Cambridge: Cambridge University Press. [Google Scholar]

- Dasgupta, Ajit K., and David W. Pearce. 1972. Cost-Benefit Analysis: Theory and Practice. London: Macmillan International Higher Education. [Google Scholar]

- de Steiguer, J. Edward. 2016. A Student’s Guide to Cost-Benefit Analysis for Natural Resources. Available online: https://cals.arizona.edu/classes/rnr485/ch6.htm (accessed on 15 June 2018).

- Engel, Eduardo, Ronald Fischer, and Alexander Galetovic. 2013. The Basic Public Finance of Public-Private Partnerships. Journal of the European Economic Association 11: 83–111. [Google Scholar] [CrossRef] [Green Version]

- Feldstein, Martin S. 1964. The Social Time Preference Discount Rate in Cost Benefit. The Economic Journal 74: 360–79. [Google Scholar] [CrossRef]

- Fielding, Nigel. 2004. Getting the most from archived qualitative data: Epistemological, practical and professional obstacles. International Journal of Social Research Methodology 7: 97–104. [Google Scholar] [CrossRef]

- Fisher, Irving. 1930. The Theory of Interest, as Determined by Impatience to Spend Income and Opportunity to Invest It. New York: Macmillan. [Google Scholar]

- FRED. 2021. Total Credit to Private Non-Financial Sector, Adjusted for Breaks, for United Kingdom (QGBPAM770A). Basel: Bank for International Settlements, Available online: https://fred.stlouisfed.org/series/QGBPAM770A (accessed on 18 November 2021).

- Freeman, R. Edward, and Robert Phillips. 2002. Stakeholder Theory: A Libertarian Defense. Business Ethics Quarterly 12: 331–49. [Google Scholar] [CrossRef]

- Freeman, Mark, Ben Groom, and Michael Spackman. 2018. Social Discount Rates for Cost-Benefit Analysis: A Report for HM Treasury. London: HM Treasury. [Google Scholar]

- Gradinaru, Giani. 2013. Methods and techniques for quantifying the value of ecosystem services. Romanian Statistical Review 61: 29–44. Available online: https://econpapers.repec.org/article/rsrjournl/v_3a61_3ay_3a2013_3ai_3a5_3ap_3a29-44.htm (accessed on 18 November 2021).

- Grimsey, Darrin, and Mervyn K. Lewis. 2002. Evaluating the Risks of Public Private Partnerships for Infrastructure Projects. International Journal of Project Management 20: 107–18. [Google Scholar] [CrossRef]

- Grimsey, Darrin, and Mervyn K. Lewis. 2005. Are Public Private Partnerships value for money? Accounting Forum 29: 345–78. [Google Scholar] [CrossRef]

- Groom, Ben, and David Maddison. 2018. New Estimates of the Elasticity of Marginal Utility for the UK. Environmental and Resource Economics 72: 1155–82. [Google Scholar] [CrossRef] [Green Version]

- Grout, Paul A. 1997. The economics of the private finance initiative. Oxford Review of Economic Policy 13: 53–66. [Google Scholar] [CrossRef]

- Grout, Paul A. 2003. Public and private sector discount rates in public–private partnerships. The Economic Journal 113: C62–C68. [Google Scholar] [CrossRef]

- Harberger, Arnold C. 1972. Project Evaluation: Collected Papers. London: Macmillan. [Google Scholar]

- Harrison, Mark. 2010. Valuing the Future: The Social Discount Rate in Cost-Benefit Analysis. Canberra: Productivity Commission. [Google Scholar]

- Heald, David. 2003. Value for money tests and accounting treatment in PFI schemes. Accounting, Auditing & Accountability Journal 16: 342–71. [Google Scholar] [CrossRef] [Green Version]

- HM Treasury. 2018. Central Government Guidance on Appraisal and Evaluation, The Green Book. London: HM Treasury. [Google Scholar]

- Hodge, Graeme, and Carsten Greve. 2007. Public-Private Partnerships: An International Performance Review. Public Administration Review 67: 545–58. [Google Scholar] [CrossRef]

- Hodge, Graeme A., Carsten Greve, and Anthony E. Boardman, eds. 2010. International Handbook on Public-Private Partnership. Cheltenham: Edward Elgar Publishing. [Google Scholar]

- Howarth, Richard B. 2005. Against high discount rates. In Perspectives on Climate Change: Science, Economics, Politics, Ethics (Advances in the Economics of Environmental Resources). Edited by Walter Sinnott-Armstrong and Richard B. Howarth. Bingley: Emerald Group Publishing Limited, vol. 5, pp. 99–120. [Google Scholar] [CrossRef]

- IMF. 2020. Government Finance Statistics. Available online: https://data.imf.org/?sk=a0867067-d23c-4ebc-ad23-d3b015045405 (accessed on 15 June 2020).

- Iossa, Elisabetta, and David Martimort. 2016. Corruption in PPPs, incentives and contract incompleteness. International Journal of Industrial Organization 44: 85–100. [Google Scholar] [CrossRef] [Green Version]

- Johansson, Åsa, Yvan Guillemette, Fabrice Murtin, David Turner, Giuseppe Nicoletti, Christine de la Maisonneuve, Guillaume Bousquet, and Francesca Spinelli. 2012. Looking to 2060: Long-Term Global Growth Prospects: A Going for Growth Report. OECD Economic Department Policy Note No. 3. Paris: The Organisation for Economic Co-Operation and Development. [Google Scholar] [CrossRef]

- Keen, Steve. 2017. Can We Avoid Another Financial Crisis? Hoboken: John Wiley & Sons. [Google Scholar]

- Kossova, Tatiana, and Maria Sheluntcova. 2016. Evaluating performance of public sector projects in Russia: The choice of a social discount rate. International Journal of Project Management 34: 403–11. [Google Scholar] [CrossRef]

- Kula, Erhun. 1985. An Empirical Investigation on the Social Time-Preference Rate for the United Kingdom. Environment and Planning A 17: 199–212. [Google Scholar] [CrossRef]

- Kula, Erhun. 1987. Social interest rate for public sector appraisal in the United Kingdom, the United States and Canada. Project Appraisal 2: 169–74. [Google Scholar] [CrossRef] [Green Version]

- Kurzweil, Ray. 2014. The singularity is near. In Ethics and Emerging Technologies. Edited by Ronald L. Sandler. London: Palgrave Macmillan, pp. 393–406. [Google Scholar] [CrossRef]

- Lind, Robert C., Kenneth J. Arrow, Gordon R. Corey, Partha Dasgupta, Amartya K. Sen, Thomas Stauffer, Joseph E. Stiglitz, Jacob A. Stockfisch, and Robert Wilson. 1982. Discounting for Time and Risk in Energy Policy. New York: Resources for the Future. [Google Scholar]

- Liu, Liqun. 2003. A marginal cost of funds approach to multi-period public project evaluation: Implications for the social discount rate. Journal of Public Economics 87: 1707–18. [Google Scholar] [CrossRef]

- Long-Sutehall Tracy, Magi Sque, and Julia Addington-Hall. 2010. Secondary Analysis of Qualitative Data: A Valuable Method for Exploring Sensitive Issues with an Elusive Population? Journal of Research in Nursing 16: 335–44. [Google Scholar] [CrossRef] [Green Version]

- Marini, Giancarlo, and Pasquale Scaramozzino. 2000. Social time preference. Journal of Population Economics 13: 639–45. [Google Scholar] [CrossRef]

- Marques, Domingos Ribeiro da Cunha, and Sanford Berg. 2011. Public-Private Partnership Contracts: A Tale of Two Cities with Different Contractual Arrangements. Public Administration 89: 1585–603. [Google Scholar] [CrossRef] [Green Version]

- McCulla, Stephanie H., Karin E. Moses, and Brent R. Moulton, eds. 2015. The National Income and Product Accounts and the System of National Accounts 2008; Comparison and Research Plans. (Statistical Data). Washington, DC: U.S. Government Printing Office. [Google Scholar]

- Milanovic, Branko. 2018. Why Inequality Matters? Available online: http://glineq.blogspot.com/2018/12/why-inequality-matters.html (accessed on 18 November 2021).

- Mirrlees, James A. 1967. Optimum growth when technology is changing. The Review of Economic Studies 34: 95–124. [Google Scholar] [CrossRef]

- Mitchell, Robert C., and Richard T. Carson. 1989. Using Surveys to Value Public Goods: The Contingent Valuation Method. New York: RFF Press, chp. 1. [Google Scholar] [CrossRef]

- Moore, Mark A., Anthony E. Boardman, Aidan R. Vining, David L. Weimer, and David H. Greenberg. 2004. “Just give me a number!” Practical values for the social discount rate. Journal of Policy Analysis and Management 23: 789–812. [Google Scholar] [CrossRef]

- Moore, Mark A., Anthony E. Boardman, and Aidan R. Vining. 2013. More appropriate discounting: The rate of social time preference and the value of the social discount rate. Journal of Benefit-Cost Analysis 4: 1–16. [Google Scholar] [CrossRef] [Green Version]

- Nordhaus, William D. 1994. Managing the Global Commons: The Economics of Climate Change. Cambridge: MIT Press. [Google Scholar]

- Nozick, Robert. 1974. Anarchy, State, and Utopia. Oxford: Blackwell. [Google Scholar]

- ONS, ed. 2019. Total Wealth in Great Britain: April 2016 to March 2018. Washington, DC: Office for National Statistics. [Google Scholar]

- Parfit, Derek. 1992. An Attack on the Social Discount Rate. Aalborg: Center for Philosophy and Public Policy. [Google Scholar]

- Pattberg, Philipp H., Frank Biermann, Sander Chan, and Ayşem Mert, eds. 2012. Public-Private Partnerships for Sustainable Development: Emergence, Influence and Legitimacy. Cheltenham: Edward Elgar Publishing. [Google Scholar]

- Pearce, David W., and R. Kerry Turner. 1990. Economics of Natural Resources and the Environment. Baltimore: Johns Hopkins University Press. [Google Scholar]

- Pearce, David, and David Ulph. 1995. A Social Discount Rate for the United Kingdom. Norwich: Centre for Social and Economic Research on the Global Environment, pp. 1–22. [Google Scholar]

- Petters, Arlie O., and Xiaoying Dong. 2016. The Time Value of Money. In An Introduction to Mathematical Finance with Applications. Springer Undergraduate Texts in Mathematics and Technology. New York: Springer, pp. 13–82. [Google Scholar]

- Pigou, Arthur C. 1932. The effect of reparations on the ratio of international interchange. The Economic Journal 42: 532–43. [Google Scholar] [CrossRef]

- Plater, Zygmunt J. B., Robert H. Abrams, Robert L. Graham, Lisa Heinzerling, David A. Wirth, and Noah D. Hall. 1998. Environmental Law and Policy: Nature, Law, and Society, 2nd ed. Saint Paul: West Group. [Google Scholar]

- Postema, Gerald J. 2006. Interests, universal and particular: Bentham’s utilitarian theory of value. Utilitas 18: 109–33. [Google Scholar] [CrossRef]

- Price, Colin. 1988. Investment, reinvestment, and the social discount rate for forestry. Forest Ecology and Management 24: 293–310. [Google Scholar] [CrossRef]

- Ramsey, Frank P. 1928. A Mathematical Theory of Saving. The Economic Journal 38: 543–59. [Google Scholar] [CrossRef]

- Rawls, John. 1971. A Theory of Justice. Cambridge: Harvard University Press. [Google Scholar]

- Regan, Michael, Jim Smith, and Peter Love. 2011. Infrastructure Procurement: Learning from Private–Public Partnership Experiences ‘Down Under’. Environment and Planning C: Government and Policy 29: 363–78. [Google Scholar] [CrossRef]

- Roemer, John, and Kōtarō Suzumura, eds. 2007. Intergenerational Equity and Sustainability. New York: Palgrave MacMillan. [Google Scholar]

- Roumboutsos, Athena B. 2010. Sustainability, social discount rates and the selection of project procurement method. International Advances in Economic Research 16: 165–74. [Google Scholar] [CrossRef]

- Rowland, David, and Allyson Pollock, eds. 2002. Understanding the Private Finance Initiative: The School Governor’s Essential Guide to PFI. London: UNISON. [Google Scholar]

- Schomaker, Rahel M. 2020. Conceptualizing corruption in public private partnerships. Public Organization Review 20: 807–20. [Google Scholar] [CrossRef] [Green Version]

- Schwartz, Gerd, Ana Corbacho, and Katja Funke. 2008. Public Investment and Public-Private Partnership: Addressing Infrastructure Challenges and Managing Fiscal Risks. New York: Palgrave MacMillan. [Google Scholar]

- Sen, A. 1987. On Ethics and Economics. Oxford: Blackwell. [Google Scholar]

- Shmelev, Stanislav E., and Robert U. Ayres. 2021. On the Creation and Destruction of National Wealth: Are Financial Collapses Endogenous? Sustainability 13: 7352. [Google Scholar] [CrossRef]

- Simon, Herbert. 2000. Bounded rationality in social science: Today and tomorrow. Mind & Society 1: 25–39. [Google Scholar] [CrossRef]

- Smith, Warrick. 1997. Covering Political and Regulatory Risks: Issues and Options for Private Infrastructure Arrangements. In Dealing with Public Risk in Private Infrastructure. Edited by Timothy Irwin, Michael Klein, Guillermo E. Perry and Mateen Thobani. Washington, DC: World Bank Latin American and Caribbean Studies, pp. 45–85. [Google Scholar]

- Sozou, Peter D. 1998. On Hyperbolic Discounting and Uncertain Hazard Rates. Proceedings of the Royal Society of London. Series B: Biological Sciences 265: 2015–20. [Google Scholar] [CrossRef] [Green Version]

- Spackman, Michael, ed. 1991. Government Economic Service Working Paper No. 13 (Treasury Working Paper No. 58). London: HM Treasury. [Google Scholar]

- Spackman, Michael. 2004. Time Discounting and of the Cost of Capital in Government. Fiscal Studies 25: 467–518. [Google Scholar] [CrossRef]

- Spackman, Michael. 2017. Social Discounting: The SOC/STP Divide. Leeds: Centre for Climate Change Economics and Policy. [Google Scholar]

- Stern, Nicholas. 2007. Stern Review: The Economics of Climate Change. Cambridge: Cambridge University Press, Available online: www.hm-treasury.gov.uk (accessed on 18 November 2021).

- Sunstein, Cass R. 2009. Worst-Case Scenarios. Cambridge: Harvard University Press. [Google Scholar]

- Towe, Christopher M. 1991. The budgetary control and fiscal impact of government contingent liabilities. Staff Papers 38: 109–34. [Google Scholar] [CrossRef]

- Tullock, Gordon. 1964. The social rate of discount and the optimal rate of investment: Comment. The Quarterly Journal of Economics 78: 331–36. [Google Scholar] [CrossRef]

- Utting, Peter, and Ann Zammit. 2009. United Nations-business partnerships: Good intentions and contradictory agendas. Journal of Business Ethics 90: 39–56. [Google Scholar] [CrossRef]

- Van Ham, H., and Joop Koppenjan. 2001. Building Public-Private Partnerships: Assessing and managing risks in port development. Public Management Review 3: 593–616. [Google Scholar] [CrossRef]

- Weitzman, Martin L. 1998. Why the Far-Distant Future Should Be Discounted at Its Lowest Possible Rate. Journal of Environmental Economics and Management 36: 201–8. [Google Scholar] [CrossRef] [Green Version]

- Wenar, Lei. 2017. John Rawls, The Stanford Encyclopedia of Philosophy. Edited by Edward N. Zalta. Available online: https://plato.stanford.edu/archives/sum2021/entries/rawls/ (accessed on 3 December 2019).

- World Bank. 2020. International Comparison Program, World Bank, World Development Indicators database, World Bank, Eurostat-OECD PPP Programme. Available online: https://data.worldbank.org/indicator/PA.NUS.PPPC.RF?locations=GB (accessed on 18 November 2021).

- Young, Louise. 2002. Determining the Discount Rate for Government Projects. New Zealand Treasury Working Paper, No. 02/21. Wellington: New Zealand Treasury. [Google Scholar]

- Zhuang, Juzhong, Zhihong Liang, Tun Lin, and Franklin De Guzman. 2007. Theory and Practice in the Choice of Social Discount Rate for Cost-Benefit Analysis: A Survey. ERD Working Paper Series, No. 94. Manila: Asian Development Bank (ADB), Available online: http://hdl.handle.net/11540/1853 (accessed on 18 November 2021).

{kind=link}

| Discount Rate (%) | PFI | PSC | Difference in Favour of PFI |

|---|---|---|---|

| 6 | GBP 173.1 m | GBP 174.3 m | GBP 1.2 m |

| 5.5 | GBP 186.7 m | GBP 185.8 m | −GBP 0.9 m |

| 5 | GBP 202.0 m | GBP 198.8 m | −GBP 3.2 m |

| 4.5 | GBP 219.5 m | GBP 213.9 m | −GBP 5.6 m |

| 4 | GBP 239.3 m | GBP 231.2 m | −GBP 8.1 m |

| 3 | GBP 288.6 m | GBP 275.0 m | −GBP 13.6 m |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Al Yaqoobi, A.; Ausloos, M. An Intergenerational Issue: The Equity Issues Due to Public–Private Partnerships; The Critical Aspect of the Social Discount Rate Choice for Future Generations. J. Risk Financial Manag. 2022, 15, 49. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15020049

Al Yaqoobi A, Ausloos M. An Intergenerational Issue: The Equity Issues Due to Public–Private Partnerships; The Critical Aspect of the Social Discount Rate Choice for Future Generations. Journal of Risk and Financial Management. 2022; 15(2):49. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15020049

Chicago/Turabian StyleAl Yaqoobi, Abeer, and Marcel Ausloos. 2022. "An Intergenerational Issue: The Equity Issues Due to Public–Private Partnerships; The Critical Aspect of the Social Discount Rate Choice for Future Generations" Journal of Risk and Financial Management 15, no. 2: 49. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15020049