The Conductive and Predictive Effect of Oil Price Fluctuations on China’s Industry Development Based on Mixed-Frequency Data

, ,

, ,

Abstract

:1. Introduction

2. Literature Review

3. Model Introduction

3.1. Introduction to the MIDAS Model

3.1.1. Basic MIDAS Regression Model

3.1.2. h-Step Forward-Prediction MIDAS (m,K,h) Model

3.1.3. h-Steps Forward-Prediction MIDAS(m,K,h)-AR(1) Model

3.2. Weight Function Selection and Setting

4. Modeling and Empirical Analysis of Mixed-Frequency Data Regression Model for Macroeconomic Impact Effect of Oil Price Fluctuation

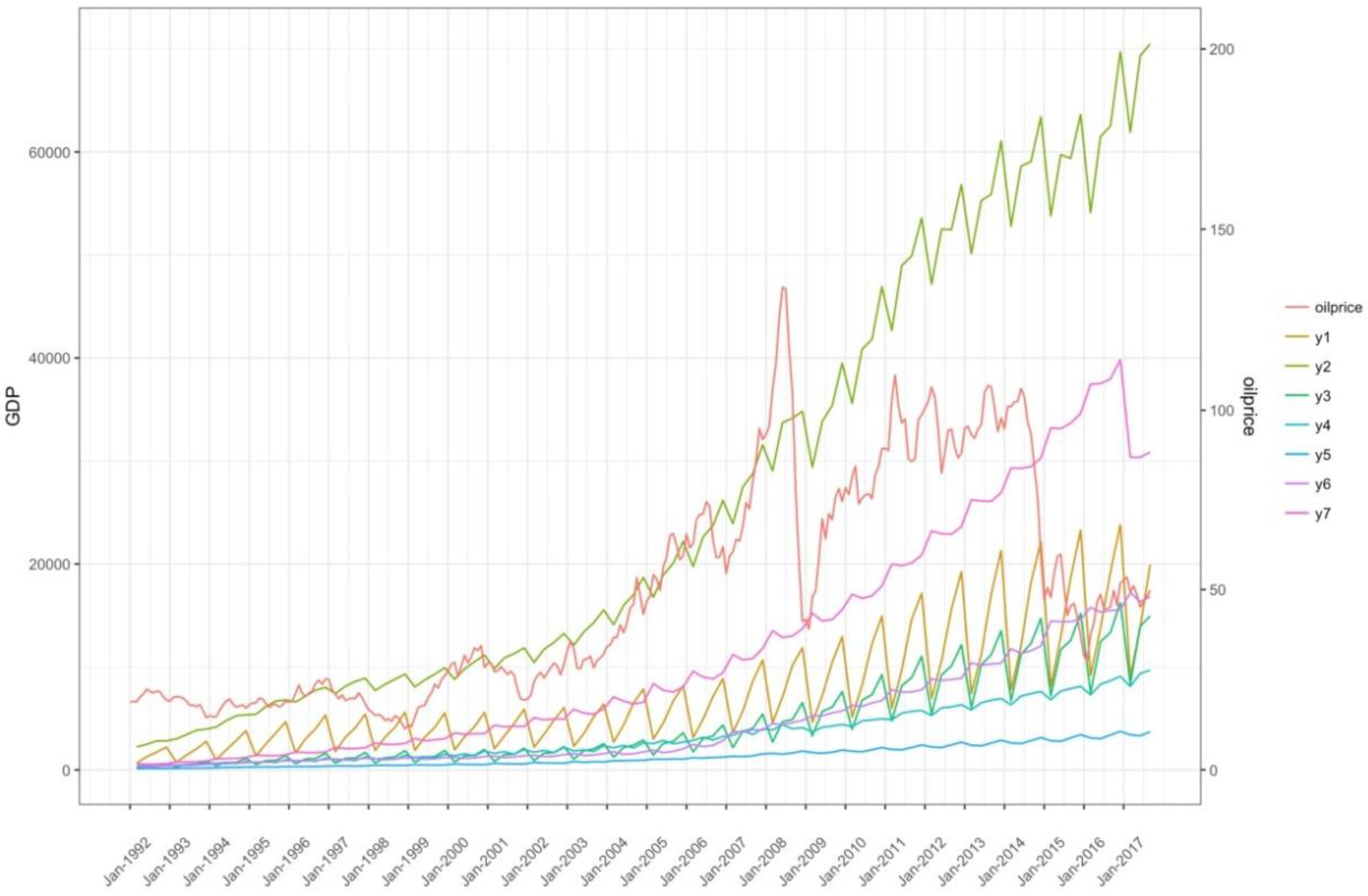

4.1. Indicator Selection and Data Description

4.2. Empirical Analysis Based on MIDAS(m,k,h)-AR(1) Model

4.3. Parameter Estimation Results and Fitting Accuracy Analysis

4.4. MIDAS(m,K,h)-AR(1) Model Forward 3-Step Prediction Analysis

4.5. Robustness Test of Empirical Results

5. Conclusions and Prospects

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Kilian, L. The Economic Effects of Energy Price Shock. Econ. Lit. 2008, 46, 871–909. [Google Scholar] [CrossRef]

- Ren, R.; Mao, M. The Impact of International Oil Price Fluctuation on China’s Macroeconomy: An Empirical Study Based on Chinese IGEM Model. World Econ. 2010, 12, 28–47. [Google Scholar]

- Barsoum, F.; Stankiewicz, F. Forecasting GDP growth using mixed-frequency models with switching regimes. Int. J. Forecast. 2015, 31, 33–50. [Google Scholar] [CrossRef]

- Pan, Z.; Wang, Q.; Wang, Y.; Yang, L. Forecasting U.S. real GDP using oil prices: A time-varying parameter MIDAS model. Energy Econ. 2018, 72, 177–187. [Google Scholar] [CrossRef]

- Zhang, B.; Xu, J. Impact of Oil Prices and China's Macroeconomics: Mechanisms, Impacts, and Countermeasures. Manag. World 2010, 11, 18–27. [Google Scholar]

- Silvestrini, A.; Veredas, J. Temporal aggregation of univariate and multivariate time series model: A survey. Econ. Surv. 2008, 22, 458–497. [Google Scholar] [CrossRef]

- Zhao, J.; Xue, Y. Research on quarterly GDP estimation method in China. Stat. Res. 2009, 10, 25–32. [Google Scholar]

- Andreou, E. On the use of high frequency measures of volatility in MIDAS regression. J. Econ. 2016, 193, 367–389. [Google Scholar] [CrossRef]

- Ghysels, E.; Santa-Clara, P.; Valkanov, R. The MIDAS Touch: Mixed Data Sampling Regression Models. 2004. Available online: https://escholarship.org/uc/item/9mf223rs (accessed on 22 June 2004).

- Asgharian, A.; Hou, A.J.; Javed, F. The Importance of the Macroeconomic Variables in Forecasting Stock return Variance: A GARCH-MIDAS Approach. J. Forecast. 2013, 32, 600–612. [Google Scholar] [CrossRef] [Green Version]

- Pan, Z.; Wang, Y.; Wu, C.; Yin, L. Oil price volatility macroeconomic fundamentals: A regime switching GARCH-MIDAS model. J. Empir. Financ. 2017, 43, 130–142. [Google Scholar] [CrossRef]

- Clements, M.P.; Galvão, A.B. Macroeconomic forecasting with mixed-frequency data: Forecasting US output growth. J. Bus. Econ. Stat. 2008, 26, 546–554. [Google Scholar] [CrossRef]

- Clements, M.P.; Galvão, A.B. Forecasting US output growth using leading indicators: An appraisal using MIDAS models. Econometrics 2009, 24, 187–1206. [Google Scholar] [CrossRef]

- Frale, C.; Monteforte, L. FaMIDAS: A Mixed Frequency Factor Model with MIDAS Structure. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1829984 (accessed on 26 August 2010).

- Andreou, E.; Ghysels, E.; Kourtellos, A. Should macroeconomic forecasters use daily financial data and how? J. Bus. Econ. Stat. 2013, 31, 240–251. [Google Scholar] [CrossRef]

- Foroni, C.; Guérin, P.; Marcellino, M. Markov-switching mixed-frequency VAR models. Int. J. Forecast. 2015, 31, 692–711. [Google Scholar] [CrossRef]

- Baumeister, C.; Guérin, P.; Kilian, L. Do high-frequency financial data help forecast oil prices? The MIDAS touch at work. Int. J. Forecast. 2015, 31, 238–252. [Google Scholar] [CrossRef]

- Liu, H.; Liu, J. Real-time forecasting and short-term prediction of China’s macroeconomic aggregates. Econ. Res. 2011, 3, 4–17. [Google Scholar]

- Geng, P.; Qi, H. Quarterly GDP real-time data forecast and evaluation in China. Stat. Res. 2012, 1, 8–14. [Google Scholar]

- Zheng, T.; Wang, X. Measuring and real-time analysis of mixture data in China’s economic cycle. Econ. Res. J. 2013, 6, 58–70. [Google Scholar]

- Li, Z.; Zheng, Y. Research on China’s economic cycle system based on mixture data model. Statistics 2015, 1, 33–40. [Google Scholar]

- Jiang, Y.; Guo, Y.; Zhang, Y. Forecasting China’s GDP growth using dynamic factors and mixed-frequency data. Econ. Model. 2017, 66, 132–138. [Google Scholar] [CrossRef]

- Stock, J.H.; Watson, M.W. How did leading indicator forecasts perform during the 2001 recession? Fed. Reserv. Bank Richmond Econ. Q. 2003, 89, 71–90. [Google Scholar]

- Xu, J.; Zhang, X.; Tang, G. Mixed data sampling volatility model. Quant. Econ. Tech. Econ. 2007, 11, 77–85. [Google Scholar]

- He, Y.; Lin, B. Forecasting China’s total energy demand and its structure using ADL-MIDAS model. Energy 2018, 151, 420–429. [Google Scholar] [CrossRef]

- Maximo, C. Mixed-frequency VAR models with Markov-switching dynamics. Econ. Lett. 2013, 121, 369–373. [Google Scholar]

- Ghysels, E.; Qian, H. Estimating MIDAS regressions via OLS with polynomial parameter profiling. Econ. Stat. 2018. [Google Scholar] [CrossRef]

- Schorfheide, F.; Song, D. Real-time forecasting with a mixed-frequency VAR. Bus. Econ. Stat. 2015, 33, 366–380. [Google Scholar] [CrossRef]

{kind=link}

| Parameter | Estimator | Parameter | Estimator | Parameter | Estimator |

|---|---|---|---|---|---|

| 0.217359 [2.286437] | 0.113910 [1.281147] | 0.183333 [4.704382] | |||

| 0.967306 [59.43253] | 0.987512 [48.98643] | 0.969958 [117.2738] | |||

| 0.024132 [1.415262] | 0.004356 [0.166990] | 0.033026 [2.205154] | |||

| 0.205682 [4.156209] | 0.019268 [0.115753] | - | - | ||

| 0.973761 [114.1273] | 0.986925 [102.5549] | - | - | ||

| 0.022763 [1.868707] | 0.034992 [0.704258] | - | - | ||

| 0.116925 [2.202226] | 0.086810 [1.707934] | - | - | ||

| 0.974576 [75.23123] | 0.980559 [128.9928] | - | - | ||

| 0.032506 [1.630732] | 0.035997 [2.773510] | - | - |

| Parameter | Estimator | Parameter | Estimator | Parameter | Estimator |

|---|---|---|---|---|---|

| −11.25603 | 1.228978 | −1.849069 | |||

| −11.25269 | 19.99887 | −1.840730 | |||

| −0.233594 | −0.117343 | −0.167108 | |||

| 0.999655 | −4.328954 | - | - | ||

| 19.99851 | −4.324672 | - | - | ||

| −0.078274 | −0.161451 | - | - | ||

| 1.137604 | −0.923369 | - | - | ||

| 1.489250 | −1.760405 | - | - | ||

| −0.096772 | −0.089178 | - | - |

| Variable | |||||||

|---|---|---|---|---|---|---|---|

| 0.9922 | 0.9984 | 0.9963 | 0.9906 | 0.9919 | 0.9982 | 0.9982 | |

| 0.9921 | 0.9984 | 0.9963 | 0.9905 | 0.9918 | 0.9982 | 0.9982 | |

| AIC | −2.6979 | −3.6825 | −2.6589 | −2.0749 | −2.2297 | −3.1799 | −3.0816 |

| BC | −2.5415 | −3.5262 | −2.5016 | −1.9176 | −2.0694 | −3.0246 | −2.9253 |

| Index | RMSE | MAE | MAPE | SMAPE | Theil U1 | Thril U2 |

|---|---|---|---|---|---|---|

| MIDAS-AR() | 0.051005 | 0.043397 | 0.451102 | 0.451773 | 0.002656 | 1.366942 |

| NLS-AR() | 0.077419 | 0.064297 | 0.667335 | 0.670166 | 0.004039 | 2.079696 |

| MIDAS-AR() | 0.056311 | 0.052779 | 0.478657 | 0.478218 | 0.002552 | 1.720764 |

| NLS-AR() | 0.065965 | 0.060134 | 0.546285 | 0.544782 | 0.002986 | 2.033483 |

| MIDAS-AR() | 0.074842 | 0.055945 | 0.594264 | 0.596728 | 0.004002 | 1.188377 |

| NLS-AR() | 0.103864 | 0.081400 | 0.863433 | 0.869323 | 0.005565 | 1.667946 |

| MIDAS-AR() | 0.069855 | 0.053828 | 0.0595646 | 0.597509 | 0.003892 | 0.765898 |

| NLS-AR() | 0.099709 | 0.070062 | 0.771112 | 0.777125 | 0.005571 | 1.088555 |

| MIDAS-AR() | 0.068697 | 0.058577 | 0.732093 | 0.728919 | 0.004259 | 0.802420 |

| NLS-AR() | 0.073924 | 0.062179 | 0.777455 | 0.773489 | 0.004580 | 0.870296 |

| MIDAS-AR() | 0.086911 | 0.075465 | 0.782832 | 0.786843 | 0.004557 | 1.657324 |

| NLS-AR() | 0.110734 | 0.098661 | 1.023878 | 1.030471 | 0.005814 | 2.117174 |

| MIDAS-AR() | 0.110008 | 0.084351 | 0.805537 | 0.809210 | 0.005299 | 1.015265 |

| NLS-AR() | 0.109919 | 0.081284 | 0.775417 | 0.779712 | 0.005296 | 1.013958 |

| Industry | Variable | Prediction | Industry | Variable | Prediction |

|---|---|---|---|---|---|

| 9.555388 | 8.114250 | ||||

| 9.438882 | 7.995726 | ||||

| 9.325513 | 7.876813 | ||||

| 11.03643 | 9.626504 | ||||

| 10.93190 | 9.493557 | ||||

| 10.82886 | 9.361199 | ||||

| 9.384068 | 10.164602 | ||||

| 9.233696 | 10.013394 | ||||

| 9.086418 | 9.865988 | ||||

| 9.242429 | - | - | - | ||

| 9.237046 | - | - | - | ||

| 9.231608 | - | - | - |

| Parameter | Estimator | Parameter | Estimator | Parameter | Estimator |

|---|---|---|---|---|---|

| 0.216839 [2.244063] | 0.163099 [1.843402] | 0.186990 [4.605757] | |||

| 0.967456 [60.10916] | 0.972703 [50.97502] | 0.971708 [118.2614] | |||

| 0.023898 [1.541286] | 0.021977 [0.954592] | 0.027861 [2.037531] | |||

| 0.021976 [4.466114] | 0.148090 [2.516443] | - | - | ||

| 0.972868 [121.6097] | 0.967008 [61.73389] | - | - | ||

| 0.021976 [2.095907] | 0.029878 [1.465356] | - | - | ||

| 0.155621 [3.109614] | 0.087183 [2.375113] | - | - | ||

| 0.968537 [86.95664] | 0.974931 [114.5561] | - | - | ||

| 0.035254 [2.152473] | 0.040709 [3.129838] | - | - |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chai, J.; Cao, P.; Zhou, X.; Lai, K.K.; Chen, X.; Su, S. The Conductive and Predictive Effect of Oil Price Fluctuations on China’s Industry Development Based on Mixed-Frequency Data. Energies 2018, 11, 1372. https://0-doi-org.brum.beds.ac.uk/10.3390/en11061372

Chai J, Cao P, Zhou X, Lai KK, Chen X, Su S. The Conductive and Predictive Effect of Oil Price Fluctuations on China’s Industry Development Based on Mixed-Frequency Data. Energies. 2018; 11(6):1372. https://0-doi-org.brum.beds.ac.uk/10.3390/en11061372

Chicago/Turabian StyleChai, Jian, Puju Cao, Xiaoyang Zhou, Kin Keung Lai, Xiaofeng Chen, and Siping (Sue) Su. 2018. "The Conductive and Predictive Effect of Oil Price Fluctuations on China’s Industry Development Based on Mixed-Frequency Data" Energies 11, no. 6: 1372. https://0-doi-org.brum.beds.ac.uk/10.3390/en11061372