City Branding, Sustainable Urban Development and the Rentier State. How Do Qatar, Abu Dhabi and Dubai Present Themselves in the Age of Post Oil and Global Warming?

Abstract

:1. Introduction

2. The Politics of Branding and Sustainable Urban Development in Qatar, Abu Dhabi and Dubai

2.1. The Concept of City Branding

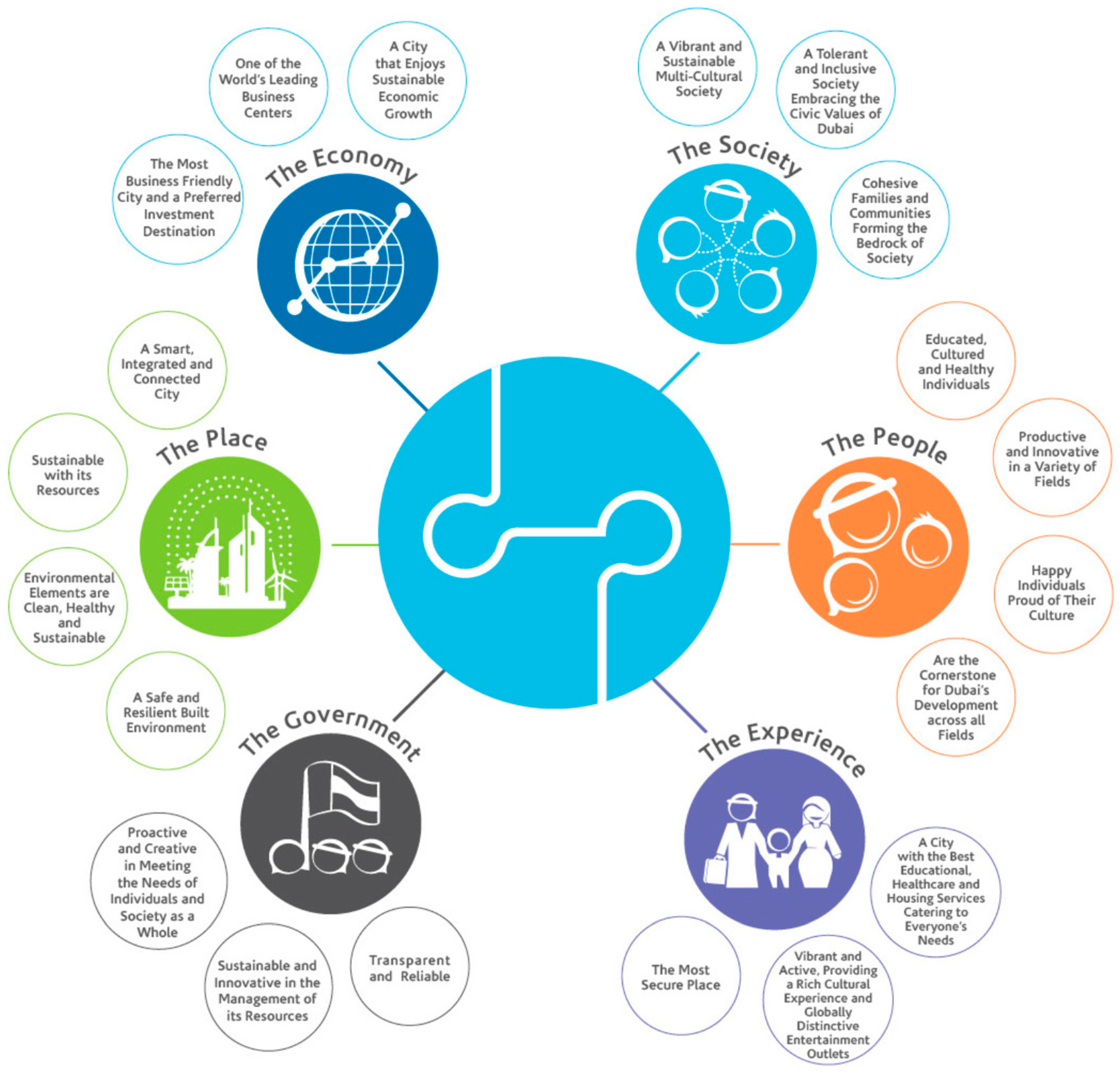

2.2. City Branding in Qatar, Abu Dhabi and Dubai

3. Research Design and Methodology

3.1. Research Design and Case Selection

3.2. Key Concepts and Operationalization

3.3. Data Collection and Analysis

4. Visions, Plans, Frameworks and Other Online Sources in Place Branding and Policy-Making

5. Branding and Implementing Sustainable Urban Development in Qatar, Abu Dhabi and Dubai

5.1. Branding and Implementing Economic Diversification

5.2. Branding and Implementing the Development of an Innovation System

5.3. Branding and Implementing the Smart and Sustainable Cities

6. Results of the Analysis

7. Conclusions and Discussion

- Which steps have been taken to substantiate Qatar, Abu Dhabi and Dubai’s claims to economic and ecological modernization?

- Is there a difference in this between rentier states (Abu Dhabi and Qatar) and former rentier states (Dubai)?

7.1. Discussion

7.2. Limitations of This Study and Suggestions for Further Research

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Davidson, C. (Ed.) Power and Politics in the Persian Gulf Monarchies; Hurst & Company: London, UK, 2011. [Google Scholar]

- Fromherz, A.J. Qatar: A Modern History; Georgetown University Press: Washington, DC, USA, 2017. [Google Scholar]

- Coates Ulrichsen, K. The United Arab Emirates: Power, Politics and Policymaking; Routledge: London, UK, 2017. [Google Scholar]

- Davidson, C. Dubai: The Vulnerability of Success; Hurst & Company: London, UK, 2008. [Google Scholar]

- Davidson, C. Abu Dhabi: Oil and Beyond; Hurst & Company: London, UK, 2009. [Google Scholar]

- Kamrava, M. Qatar: Small State, Big Politics; Cornell University Press: Ithaca, NY, USA, 2013. [Google Scholar]

- Roberts, D.B. Qatar: Securing the Global Ambitions of a City-State; Hurst & Company: London, UK, 2017. [Google Scholar]

- Commins, D. The Gulf States: A Modern History; I.B. Tauris: London, UK, 2012. [Google Scholar]

- Syed, A. Dubai: Guilded Cage; Yale University Press: New Haven, CT, USA, 2010. [Google Scholar]

- Luomi, M. The Gulf Monarchies and Climate Change: Abu Dhabi and Qatar in an Era of Natural Unsustainability; Hurst & Company: London, UK, 2012. [Google Scholar]

- Tok, E.; Al Mohammad, F.; Al Merekhi, M. Crafting smart cities in the gulf region: A comparison of Masdar and Lusail. Eur. Sci. J. 2014, 2, 1857–1881. [Google Scholar]

- Dinnie, K. (Ed.) City Branding: Theory and Cases; Palgrave Macmillan: Basingstoke, UK, 2011. [Google Scholar]

- Govers, R.; Go, F. Place Branding: Glocal, Virtual and Physical Identities, Constructed, Imagined and Experienced; Palgrave Macmillan: Basingstoke, UK, 2009. [Google Scholar]

- Westwood, S. Branding a ‘new’ destination: Abu Dhabi. In Destination Brands: Managing Place Reputation; Nigel, M., Pritchard, A., Pride, R., Eds.; Routledge: London, UK, 2011. [Google Scholar]

- Davidson, C. After the Sheikhs: The Coming Collapse of the Gulf Monarchies; Hurst & Company: London, UK, 2012. [Google Scholar]

- Coates Ulrichsen, K. Qatar and the Arab Spring; Hurst & Company: London, UK, 2014. [Google Scholar]

- World Bank. United Arab Emirates. 2019. Available online: https://data.worldbank.org (accessed on 15 March 2019).

- Coates Ulrichsen, K. Insecure Gulf: The End of Certainty and the Transition to the Post-Oil Era; Hurst & Company: London, UK, 2011. [Google Scholar]

- Krane, J. Dubaiu: The Story of the World’s Fastest City; Atlantic Books: London, UK, 2015. [Google Scholar]

- Kazerouni, A. Le Miroir des Cheikhs; Musee et Politique dans les Principautes du Golfe Persique; Presses Universitaires de France: Paris, France, 2017. [Google Scholar]

- Makadam, S.; Ramaswamy, R. Sustainable smart city: Masdar (UAE) (A City: Ecologically Balanced). Indian J. Sci. Technol. 2014, 9. [Google Scholar] [CrossRef]

- Al Naimi, A.; Karani, G.; Littlewood, J. Stakeholder Views on Land Reclamation and Marine Environment in Doha, Qatar. J. Agric. Environ. Sci. 2018, 7, 32–39. [Google Scholar]

- Angelidou, M. Smart city planning and development shortcomings. TeMA. J. Land Usemobil. Environ. 2017, 10, 77–94. [Google Scholar]

- Goess, S.; de Jong, M.; Meijers, E. City branding in polycentric urban regions: Identification, profiling and transformation in the Randstad and Rhine-Ruhr. Eur. Plan. Stud. 2016, 24, 2036–2056. [Google Scholar] [CrossRef]

- De Jong, M.; Chen, Y.; Joss, S.; Lu, H.; Zhao, M.; Yang, Q.; Zhang, C. Explaining city branding practices in China’s three mega-city regions: The role of ecological modernization. J. Clean. Prod. 2018, 179, 527–543. [Google Scholar] [CrossRef]

- Noori, N.; de Jong, M. Towards Credible City Branding Practices: How Do Iran’s Largest Cities Face Ecological Modernization? Sustainability 2018, 10, 1354. [Google Scholar] [CrossRef]

- Baker, B. Destination Branding for Small Cities, 2nd ed.; Creative Leap Books: Portland, OR, USA, 2012. [Google Scholar]

- Hankinson, G. Place branding research: A cross-disciplinary agenda and the views of practitioners. Place Branding Public Dipl. 2010, 6, 300–315. [Google Scholar] [CrossRef]

- Zenker, S.; Braun, E.; Petersen, S. Branding the destination versus the place: The effects of brand complexity and identification for residents and visitors. Tour. Manag. 2017, 58, 15–27. [Google Scholar] [CrossRef]

- Boisen, M.; Terlouw, K.; Groote, P.; Couwenberg, O. Reframing place promotion, place marketing, and place branding—Moving beyond conceptual confusion. Cities 2017, 80, 4–11. [Google Scholar] [CrossRef]

- Lu, H.; de Jong, M.; Chen, Y. Economic city branding in China: The multi-level governance of municipal self-promotion in the Greater Pearl River Delta. Sustainability 2017, 9, 496. [Google Scholar] [CrossRef]

- Kavaratzis, M. From city marketing to city branding: Towards a theoretical framework for developing city brands. Place Branding 2004, 1, 58–73. [Google Scholar] [CrossRef]

- Kavaratzis, M.; Ashworth, G. City branding: An effective assertion of identity or a transitory marketing trick? Ahmadreza Shirvani Dastgerdi Giuseppe De Luca Geographica Pannonica 2005, 96, 506–514. [Google Scholar] [CrossRef]

- Baker, B. Destination Branding for Small Cities: The Essentials for Successful Place Branding; Destination Branding Book: Portland, OR, USA, 2007. [Google Scholar]

- Anholt, S. Places: Identity, Image and Reputation; Springer: Basingstoke, UK, 2016. [Google Scholar]

- Shirvani-Dastgerdi, A.; De-Luca, G. Boosting city image for creation of a certain city brand. Geogr. Pannonica 2019, 23, 23–31. [Google Scholar] [CrossRef]

- Hudson, S.; Cárdenas, D.; Meng, F.; Thal, K. Building a place brand from the bottom up: A case study from the United States. J. Vacat. Mark. 2017, 23, 365–377. [Google Scholar] [CrossRef]

- Kavaratzis, M.; Kalandides, A. Rethinking the place brand: The interactive formation of place brands and the role of participatory place branding. Environ. Plan. A 2015, 47, 1368–1382. [Google Scholar] [CrossRef]

- Pedeliento, G.; Kavaratzis, M. Bridging the gap between culture, identity and image: A structurationist conceptualization of place brands and place branding. J. Prod. Brand Manag. 2019. [Google Scholar] [CrossRef]

- Al Madani, S. LinkedIn Profile. Available online: https://ae.linkedin.com/in/dr-sara-al-madani-b4b84722 (accessed on 30 April 2019).

- Cugurullo, F. Building a sand castle: An analysis of the genesis and development of Masdar City. J. Urban Technol. 2013, 20, 23–37. [Google Scholar] [CrossRef]

- Yin, R. Case Study Research: Design and Methods; Sage Publications: Los Angeles, CA, USA, 2003. [Google Scholar]

- Gerring, J. Qualitative Methods. Annu. Rev. Political Sci. 2017, 20, 15–36. [Google Scholar] [CrossRef]

- Mahdavy, H. The Pattern and Problems of Economic Development in Rentier States: The Case of Iran. In Studies in the Economic History of the Middle East; Oxford University Press: Oxford, UK, 1970. [Google Scholar]

- Government.ae. Plans and Initiatives for Sustainable Transportation. 1 July 2018. Available online: https://government.ae/en/information-and-services/education/importance-of-education-to-the-government (accessed on 30 February 2019).

- Qatar National Development Strategy 2011~2016; Qatar General Secretariat for Development Planning: Doha, Qatar, 2016.

- Qatar Higher Authorities. Qatar National Vision 2030. 2008, pp. 1–19. Available online: http://tinyurl.com/ha6fbgc (accessed on 30 February 2019).

- Arcadis. Dubai, Abu Dhabi and Doha Are the Region’s Most Sustainable Cities, Says New Index. 10 February 2015. Available online: https://www.arcadis.com/en/middle-east/news/latest-news/2015/2/dubaiabu-dhabi-and-doha-are-the-region-s-most-sustainable-citiessays-new-index (accessed on 15 April 2019).

- DEWA. Dubai Green Building Regulations & Specifications; Government of Dubai: Dubai, UAE, 2013. Available online: https://www.dewa.gov.ae/en/consultants-and-contractors/policies-and-regulations/circulars-and-forms/green-building (accessed on 25 May 2018).

- Dubai Government. Dubai Industrial Strategy 2030. 10 February 2015. Available online: https://www.dubaiplan2021.ae//wp-content/uploads/2016/06/Dubai-Industrial-Strategy-2030.pdf (accessed on 20 May 2018).

- Government of United Arab Emirates. Annual Economic Report. 27 January 2017. Available online: http://www.economy.gov.ae/EconomicalReportsEn/MOE Annual Report 2017_English.pdf (accessed on 15 April 2019).

- Government.ae. Dubai. 1 July 2018. Available online: https://government.ae/en/information-and-services/education/importance-of-education-to-the-government (accessed on 1 July 2018).

- Government.ae. Dubai Clean Energy Strategy. 1 July 2018. Available online: https://government.ae/en/information-and-services/education/importance-of-education-to-the-government (accessed on 1 July 2018).

- Qatar Education and Training. 4 May 2018; In www.export.gov. Available online: https://www.export.gov/article?id=Qatar-Education-and-Training (accessed on 04 May 2018).

- Hazem Shayah, M.; Qifeng, Y. Development of Free Zones in United Arab Emirates. Int. Rev. Res. Emerg. Mark. Glob. Econ. 2015, 2, 286–294. [Google Scholar]

- Qatar Green Building Council. QGBC & QNV 2030. 2018. Available online: https://qatargbc.org/aboutus/qgbc-qnv2030 (accessed on 15 May 2018).

- Castells, M.; Hall, P. Technopoles of the World: Making of 21st-Century Industrial Complexes; Routledge: London, UK, 1994. [Google Scholar]

- Yigitcanlar, T.; Lee, S.H. Korean ubiquitous eco-city: A smart-sustainable form or a branding hoax. Technol. Forecast. Soc. Chang. 2014, 89, 100–114. [Google Scholar] [CrossRef]

- Cugurullo, F. Urban eco-modernisation and the policy context of new eco-city projects: Where Masdar City fails and why. Urban Stud. 2016, 53, 2417–2433. [Google Scholar] [CrossRef]

- Yigitcanlar, T. Smart cities: An effective urban development and management model? Aust. Plan. 2015, 52, 27–34. [Google Scholar] [CrossRef]

{kind=link}

| Key Concept | Definition | Indicator |

|---|---|---|

| Rentier state | A state which derives all or a substantial portion of its national revenues from the rent of indigenous resources to external clients. Dependent upon it as a source of income, it may generate rents externally by manipulating the global political and economic environment. Such manipulation may include monopolies, trading restrictions, and the solicitation of subsidies or aid in exchange for political influence [44] | Presence of an autocratic regime with one or a small number of dominant families able to control and redistribute the revenues derived from natural resources. It can use them intelligently and flexibly to appease its citizens and (more selectively) immigrant groups to stay in place. Qatar and Abu Dhabi have high amounts of natural resources and therefore ample opportunity to appease, Dubai has limited amounts of them left. Qatar and Abu Dhabi are therefore full rentier states, Dubai is a semi-rentier state. It is now practically a rentier-service hub, as it is effectively the major port and business centre for most of the region’s oil and gas rentier states. |

| Place branding strategy | The practice of conveying a brand or symbolic essence of a nation, region or city to target audiences for enhancing one’s fame and reputation or otherwise obtaining strategic gain [31] while acknowledging that geographical and situational aspects are sufficiently addressed and setting the branding strategy and its objectives is not merely a top down endeavour, but also includes involvement of local stakeholders and citizenry, and a process be outlined that allows place elements and place based associations to combine and form a place brand [39,40] | Presence of a well-branded policy vision of economic diversification (1a) Presence of a well-branded policy vision of higher education (1b) Presence of a well-branded policy vision of sustainable urban expansion (1c) Presence of a large and conspicuous investment programme in green-labelled new industries (2a) Presence of a large and conspicuous investment programme in higher education (2b) Presence of a large and conspicuous investment programme in green-labelled residential expansion projects (2c) |

| Policy initiatives | Specific actions undertaken in response to generally formulated policy goals and ambitions and as such the physical embodiment of the actual implementation of the brand | Number and size of spaces displaying the emergence of non-oil and gas industries (3a) Number and size of spaces displaying the emergence of a strong research and higher education system (3b) Number and size of spaces displaying residential area development with green features (3c) Emerging variety and characteristics of the non-oil and gas industries (4a) Emerging quantity and quality of a thriving research and higher education system (4b) Emerging green and liveable features in sustainable residential areas (4c) |

| Emirates | Name | The Year of Establishment | Profile/Brand | Area/Location | Investment/Source of Funding | Type of Industries/Institutions Are in |

|---|---|---|---|---|---|---|

| Dubai | Jebel Ali Free Zone | 1985 | A unique trade ecosystem that reduces cost, while enabling new opportunities for growth. | 57 sq. km/Jebel Ali area at the far western end of Dubai | governmental funding | Logistics, Warehousing, Economic Trade Zone, Real Estate, Property |

| Dubai Airport Free Zone | 1996 | The fastest growing Zone in the world | 11 sq.km/Next to Dubai International Airport | governmental funding | Light manufacturing activities, Trading & General Trading, Services | |

| Dubai Internet City | 1999 | Innovation begins here | 139 sq. m/adjacent to Dubai Marina, Jumeirah Beach Residence | Dubai Holding subsidiary TECOM * Investments | Information and communications technology (ICT) companies | |

| Dubai Car & Automotive City Free Zone | 2000 | n/a | 743 sq. m/Ras Al Khor | Automotive industry | ||

| Dubai Media City | 2001 | The region’s leading media hub | Next to the Palm Jumeirah | TECOM Group | Media industry and services | |

| Dubai Multi Commodities Center | 2002 | The world’s #1 free zone | 2 sq.km/located in Jumeirah Lakes | DMCC is a government entity | Trading, Service, Industrial | |

| Dubai Healthcare City | 2002 | Your Health & Wellness Destination | 2.5 sq. km/Sheikh Zayed Road | governmental funding | Healthcare and clinical industry | |

| Dubai Techno Park | 2002 | n/a | 21.3 sq. km/Jebel Ali | governmental funding | High-profile companies specializing in technology, oil, gas and petrochemical industry and other industries | |

| Intl Media Production Zone | 2003 | n/a | 4 sq. km/Dubai International Financial Centre | TECOM Group | Media production Industry | |

| Dubai Silicon Oasis | 2004 | The integrated free zone technology park | 97740 sq. m/Middle of Dubai land | governmental funding | Services, Trading, Industrial: import raw material, manufacture, and process, assemble, package and export the finished product. | |

| Dubai Industrial City | 2004 | The leading manufacturing and logistics hub | 52 sq. km/Next to Jebel Ali International Airport | TECOM Group | Light and medium manufacturing | |

| Dubai Intl Financial Centre | 2004 | Gateway to Growth | 0.5 sq. km/Sheikh Zayed Road | governmental funding | Finance, Banking & Brokerage Services, Wealth Management, Reinsurance & Captive Insurance, | |

| Dubai Studio City | 2005 | Unleash your imagination | 2 sq. km/Sheikh Mohammad bin Zayed Road | TECOM Group | Film and broadcasting industry | |

| Dubai South | 2006 | The City of You—is an emerging master-planned city based on happiness of the individual. | 145 sq. km/around Al Maktoum International Airport | governmental and private funding | Light manufacturing activities, Logistics, Trading & General Trading, Educational and training, and educational consultancy services. | |

| Dubai Outsource Zone | 2007 | An outstanding business park dedicated to local and international outsourcing companies | Emirates Road | TECOM Group | Services: Business Process Outsourcing (BPO), HR Outsourcing, IT Outsourcing, back office and call center operations | |

| Gold and Diamond Park | 2011 | The Finest Creations, All Under One Roof | 47.5 sq. m/Sheikh Zayed Road | EMAAR group | Jewellery (gemstones, precious stones, gold, silver, platinum) trading, manufacturing, retails and services | |

| Dubai Design District(D3) | 2013 | A home for the region’s creative thinkers | 130 sq. m/Next to Business Bay, Dubai Mall, and Burj Khalifa | governmental funding | Digital media, arts, design, and fashion | |

| Abu Dhabi | Khalifa Industrial Zone (KIZAD) | 2010 | The Integrated Trade, Logistics and Industrial Hub of Abu Dhabi | 410 sq. km/located almost equidistant between Abu Dhabi and Dubai | governmental funding | Trade & logistics, Manufacturing; aluminum, food & beverage, pharmaceutical Packaging |

| Higher Corporation for Specialized Economic Zones | 2004 | A hub for a number of training | 14 sq. km/close to Musafah Sea Port, Abu Dhabi International Airport | governmental funding | Heavy to medium manufacturing, processing, and engineering activities | |

| Masdar City Free Zone | 2006 | An emerging global hub for clean technologies and renewable energy | 6 sq. km/6 kilometers away from the Abu Dhabi | Mubadala Development Company | Future green technology products | |

| Twofour54 | 2008 | One of the fastest growing media free zones in the region. | Proximity to Downtown Abu Dhabi | n/a | Media businesses | |

| Industrial City of Abu Dhabi (ICAD) | 2008 | n/a | 40 sq. m/located in the outskirts of Abu Dhabi city | n/a | Heavy-to-medium & Light-to-medium manufacturing, engineering and processing industries. | |

| Abu Dhabi Airport Free Zone | 2010 | A new global business address at the heart of Abu Dhabi Airports operations, will accelerate Abu Dhabi’s economic diversification | 12 sq. km/near Abu Dhabi International Airport | governmental funding/owned subsidiary of Abu Dhabi Airports | Aerospace and Aviation industry, Airport &, Airline Services, Marketing and Events, Knowledge and Development | |

| Abu Dhabi Ports Company (ADPC) Free Zone | 2012 | Abu Dhabi Port Company (ADPC) is a good spot for industries and trading companies. | 2.7 sq. km/between Dubai and Abu Dhabi, in Taweelah | governmental funding | Trade, industrial production of goods, services like banking, management consultancy or other professional services | |

| Abu Dhabi Global Market Free Zone | 2013 | An ideal location for investors to set up a company in the financial sector. | 1.14 sq. km/Al Maryah Island | governmental funding in collaborating with the bigwigs (International funding) | Financial service industry | |

| Qatar | Airport Free Zone—RAS BUFONTAS | 2018 | Technology, Trading and Logistics Hub | 3.96 sq. km/Adjacent to Hamad International Airport (HIA) | governmental funding/Qatar Free Zones Authority | Light Manufacturing, International Business Services, Aviation Sector, Emerging Technologies Logistics Hub |

| Port Free Zone—UM ALHOUL | 2018 | Hub with Industrial Focus | 30.3 sq. km/Adjacent to the Mesaieed Industrial Zone & Hamad Port | governmental funding/Qatar Free Zones Authority | Maritime Industries, Heavy Manufacturing, Industrial Sectors Focus, Emerging Technologies, Logistics Hub |

| Dubai | Abu Dhabi | Qatar | |||

|---|---|---|---|---|---|

| Economic Activity | GDP Share % (2017) | Economic Activity | GDP Share % (2016) | Economic Activity | GDP Share % (2016) |

| Wholesale and retail trade; repair of motor vehicles and motorcycles | 25.8 | Mining and quarrying (including crude oil and natural gas) | 35.9 | Mining and quarrying | 30.3 |

| Transportation and storage | 11.2 | Construction | 9.9 | Construction | 11.9 |

| Financial and insurance activities | 11 | Financial and insurance activities | 9.0 | Wholesale and retail trade; repair of motor vehicles and motorcycles | 10.0 |

| Manufacturing | 9 | Public administration and defence; compulsory social security | 7.3 | Financial and insurance activities | 9.6 |

| Real estate activities | 6.8 | Manufacturing | 6.5 | Manufacturing | 9.0 |

| Public administration and defense; compulsory social security | 6.8 | Wholesale and retail trade; repair of motor vehicles and motorcycles | 5.7 | Public administration and defense; compulsory social security | 8.7 |

| Construction | 6.5 | Real estate activities | 5.4 | Real estate activities | 7.7 |

| Professional, scientific and technical activities | 4 | Electricity, gas, and water supply; waste management activities | 4.1 | Financial intermediation services indirectly measured (FISIM) | 4.7 |

| Information and communication | 4 | Transportation and storage | 3.3 | Professional, scientific and technical activities; Administrative and support service activities | 3.7 |

| Accommodation and food service activities | 4 | Information and communication | 2.8 | Transportation and storage | 3.3 |

| Electricity, gas, steam and air conditioning supply | 3.4 | Professional, scientific and technical activities | 2.4 | Education | 2.1 |

| Administrative and support service activities | 3.3 | Administrative and support service activities | 1.6 | Human health and social work activities | 2.0 |

| Mining and quarrying | 1 | Education | 1.6 | Information and communication | 1.8 |

| Human health and social work activities | 1 | Human health and social work activities | 1.6 | Arts, entertainment and recreation; other service activities | 1.6 |

| Education | 0.7 | Accommodation and food service activities | 1.2 | Accommodation and food service activities | 1.2 |

| Other service activities | 0.5 | Agriculture, forestry and fishing | 0.7 | Electricity, gas, water supply, sewerage and waste management | 0.7 |

| Activities of households as employers; undifferentiated goods- and services-producing activities of households for own use | 0.5 | Activities of households as employers | 0.6 | Activities of households as employers; undifferentiated goods and services producing activities of households for own use | 0.7 |

| Arts, entertainment and recreation | 0.3 | Arts, recreation and other service activities | 0.3 | Import duties | 0.3 |

| Water supply; sewerage, waste management and remediation activities | 0.1 | Agriculture, forestry and fishing | 0.2 | ||

| Agriculture, forestry and fishing | 0.1 | ||||

| Gross Domestic Product | 100 | 100 | 100 | ||

| Emirates | Location | University | Level of Study | Established in Dubai | Number of Students |

|---|---|---|---|---|---|

| Dubai | Dubai International Academic City | University of Dubai | Bachelor, Master, PhD | 1997 | 768 |

| Zayed university * | Bachelor, Master | 1998 | 2114 | ||

| Higher Colleges of Technology * | Applied Diploma, Bachelor, Master | 1988 | 733 | ||

| The National Institute for Vocational Education | Diploma, Certificate | 2006 | 210 | ||

| Amity University Dubai | Bachelor, Master, PhD | 2011 | 1882 | ||

| Birla Institute of Technology and Science Pilani | Bachelor, Master, PhD | 2000 | 1603 | ||

| British University in Dubai | Bachelor, Master, PhD | 2004 | 1139 | ||

| Cambridge College International | n/a | 2007 | 69 | ||

| Curtin University | Undergraduate, Postgraduate coursework | 2017 | 10 | ||

| ESMOD French Fashion Institute | Bachelor, Certificate | 2006 | 103 | ||

| Heriot-Watt University | Bachelor, Master, PhD | 2005 | 3644 | ||

| Institute of Management Technology Dubai | Bachelor, Master | 2006 | 499 | ||

| MENA College of Management | Bachelor | 2014 | 292 | ||

| Manipal Academy of Higher Education | Bachelor, Master, PhD | 2003 | 2343 | ||

| Murdoch University | Diploma, Bachelor, Master | 2008 | 718 | ||

| S P Jain School of Global Management | Bachelor, Master, PhD | 2004 | 1628 | ||

| Shaheed Zulfikar Ali Bhutto Institute of Science and Technology | Bachelor | 2003 | 706 | ||

| University of Birmingham | Bachelor, Master | n/a | n/a | ||

| University of St. Joseph | Bachelor | 2008 | 69 | ||

| Dubai Knowledge Village | Islamic Azad University | Bachelor, Master, PhD | 2004 | 423 | |

| Michigan State University | Master | 2008 | n/a | ||

| Middlesex University | Bachelor, Master | 2005 | 3141 | ||

| SAE Institute | Bachelor | 2005 | 403 | ||

| The University of Manchester | Master | 2005 | 529 | ||

| University of Bradford | Master | 2009 | 132 | ||

| University of Exeter | Bachelor, Master, PhD | 2006 | 49 | ||

| University of Wollongong | Bachelor, Master, PhD | 1993 | 3905 | ||

| Dubai Internet City | Emirates Aviation University | Diploma, Certificate, Bachelor, Master | 1991 | 1537 | |

| Hult International Business School | Bachelor, Master | 2008 | 395 | ||

| Dubai Media City | American University | Diploma, Certificate, Bachelor, Master | 1995 | 2297 | |

| Dubai Silicon Oasis | Rochester Institute of Technology | Bachelor, Master | 2008 | 891 | |

| Dubai South | University of South Wales | Bachelor, Master | 2017 | n/a | |

| Jumeirah Lake Towers | Moscow University for Industry and Finance | Bachelor, Master | 2013 | 95 | |

| MODUL University | Bachelor, Master | 2016 | 255 | ||

| Deira | London Business School | Master | 2006 | 208 | |

| Dubai International Financial Centre | CITY University of London | Bachelor, Master | 2007 | 240 | |

| Abu Dhabi | City of Abu Dhabi | Khalifa University * | Bachelor, Master, PhD | 1989 | 1336 |

| Petroleum Institute | n/a | 2006 | 1654 | ||

| Abu Dhabi Polytechnic | Diploma, Certificate, Bachelor | 2010 | 642 | ||

| Emirates College for Advanced Education | Bachelor, Master, PhD | 1993 | 369 | ||

| University of Strathclyde | Bachelor, Master | 1995 | 201 | ||

| New York Institute of Technology | Bachelor, Master | 2005 | 163 | ||

| Sorbonne University | Bachelor, Master | 2006 | 630 | ||

| Mohammed V University | Bachelor, Master, PhD | 2009 | n/a | ||

| Abu Dhabi School of Management | Master | 2013 | 250 | ||

| Khalifa city | Abu Dhabi University | Bachelor, Master, PhD | 2003 | 4374 | |

| Masdar City | Masdar Institute | n/a | 2007 | 417 | |

| Al Mafraq hospital | Fatma College of Health Sciences | Bachelor | 2006 | 612 | |

| Mohammed Bin Zayed City | Abu Dhabi Vocational Education and Training Institute | Diploma, Certificate | 2007 | 766 | |

| Saadiyat Island | New York University | Bachelor | 2010 | 618 | |

| Qatar | City of Doha | Qatar University * | Bachelor, Master, PhD | 1973 | 14000 |

| American Education Center | Certificate | 2005 | 400 | ||

| Doha Institute for Graduate studies * | Master | 2011 | 350 | ||

| College of North Atlantic | Diploma, Bachelor | 2002 | 2000 | ||

| Education City-Doha | Hamad Bin Khalifa University * | Master, PhD | 2010 | 6000 | |

| Carnegie Mellon University | Bachelor | 2004 | 384 | ||

| Weill Cornell Medical College | Bachelor | 2001 | n/a | ||

| Northwestern University | Bachelor | 2008 | n/a | ||

| HEC Paris | Master, Certificate | 2010 | 4000 | ||

| Academic Bridge | Diploma, Certificate | 2001 | n/a | ||

| Georgetown university school of foreign service | Bachelor | 2005 | n/a | ||

| Texas A&M University | Bachelor, Master | 2003 | 635 | ||

| Virginia Commonwealth University | Bachelor, Master | 2010 | 339 | ||

| Cultural Village | Doha Film Institute | Certificate | 2010 | n/a | |

| * These are public universities; all others are private | |||||

| Name | Profile/Brand | Area/Location | Investment/Source of Funding | key Features | |

|---|---|---|---|---|---|

| Dubai | Dubai Smart City | The first happiest smart city in the world | Dubai land | Governmental | Renewable Energy Electric vehicles (EVs) Paperless government Smart Health Sustainability Green building regulation |

| Dubai Sustainable City | A sustainable lifestyle | 460000 sq. m/next to Dubai Studio City | Private funding (Diamond Developers) | Sustainable life style Eco system services (eco system for birds, productive land with date palms, farms) walkability Innovation center Green building regulation | |

| ‘Desert Rose’ Smart Sustainable City | A flower shaped environment-friendly city | 40 sq. km/a desert land at Dubai urban fringe | Dubai Municipality | Eco walk Indicative accessibility (pedestrian and cyclists, light-rail, roads) District Cooling Vacuum Solid Waste Network Multi-Utilities Tunnels Network Electrical Network Solar roofs & turbines | |

| Dubai South | The city of you- A city that defines itself by happiness of the individuals | 145 sq. km/next to Jebel Ali free zone | Governmental | The lieu of Expo 2020 Renewable energy Self-sustained urban destination to empower businesses, families and individuals to grow and prosper | |

| Abu Dhabi | Masdar City | A sustainable destination for residents and visitors to live, work, play and learn | 6 sq. km/beside Abu Dhabi International Airport | Mubadala Development Company | Clean Energy (Photovoltaic Power, Concentrated Solar Power, Wind, Waste-to-Energy, Energy Storage) Sustainability Eco-Villa prototype Mobility (driverless Personal Rapid Transit) Green building regulation |

| Qatar | Lusail | A city with a vision | 38 sq. km/located on the coast, about 23 km north of the city center of Doha | Qatari Diar Real Estate Investment Company | Eco Friendly Alternatives Mobility (light rail transportation, Water transport system, Cycle and Pedestrian Ways System, Road hierarchy System) Sustainable Infrastructures (District Cooling, Pneumatic Waste Collection, Sewage Treatment Plant) Building rating (Gulf Sustainability Assessment System) |

| MSHEIREB | Envisioning the city of the future | 764000 sq. m/Downtown Doha | Msheireb Properties (a subsidiary of Qatar Foundation) | Place Making and green building Walkability, Mixed Uses Authenticity Sustainability Mobility |

| Emirate | Rentier State | Active Place Branding | Free Economic Zones | Education/Academic Cities | Smart/Sustainable Residential Areas |

|---|---|---|---|---|---|

| Qatar | Yes (gas) | Yes | Small number of large ones | Small number of leading universities | One large project |

| Abu Dhabi | Yes (oil) | Yes | Small number of large ones | Small number of leading universities | One large project |

| Dubai | Not any more | Yes | Large number of small ones | Large number of middle-of-the-road universities | Several smaller projects |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

De Jong, M.; Hoppe, T.; Noori, N. City Branding, Sustainable Urban Development and the Rentier State. How Do Qatar, Abu Dhabi and Dubai Present Themselves in the Age of Post Oil and Global Warming? Energies 2019, 12, 1657. https://0-doi-org.brum.beds.ac.uk/10.3390/en12091657

De Jong M, Hoppe T, Noori N. City Branding, Sustainable Urban Development and the Rentier State. How Do Qatar, Abu Dhabi and Dubai Present Themselves in the Age of Post Oil and Global Warming? Energies. 2019; 12(9):1657. https://0-doi-org.brum.beds.ac.uk/10.3390/en12091657

Chicago/Turabian StyleDe Jong, Martin, Thomas Hoppe, and Negar Noori. 2019. "City Branding, Sustainable Urban Development and the Rentier State. How Do Qatar, Abu Dhabi and Dubai Present Themselves in the Age of Post Oil and Global Warming?" Energies 12, no. 9: 1657. https://0-doi-org.brum.beds.ac.uk/10.3390/en12091657