1. Introduction

Electricity markets today are increasingly moving towards systems based on renewable energies. This results in the additional need for flexibility options. If renewable energies should provide most of the power, seasonal storages or similar flexibility options become more relevant. For example, the expansion of flexibility options in Germany is, among other things, reflected by the construction of transmission capacities to Norway, to utilize existing storage capacities. As renewable energies depend upon uncertain factors like water inflow, wind or solar irradiation, long-term uncertainty regarding these factors will become more important.

As electricity markets are changing, it is likely that electricity market price structures will also change. Predicting electricity market prices is important for estimating investment decisions and retail prices as well as supporting policy decision regarding, e.g., subsidies. Hence, it is important to be able to at least roughly model electricity market prices in markets with high shares of renewable energies and storages. To date, most countries had a thermally dominated power plant park and the focus of price modelling was not on markets with high shares of renewable energies and storages.

In contrast, Norway is a country which already has a high share of renewable energies and storages. In addition, 96.3% of Norway’s electricity production comes from hydro power plants and 1.4% from wind power (2017) [

1]. It has a storage capacity of 88 TWh, which means that

of the yearly Norwegian electricity demand can be stored (2017) [

1]. The Norwegian electricity market is therefore well suited for testing price modelling methods in markets with a high share of renewable energies and storages.

There are several types of models to model prices, e.g., statistical models, optimisation models, simulation models or hybrids. Every type of model has its strengths and weaknesses, but we believe that getting prices right in optimisation models is especially important for forecasting long-term electricity prices. This has two main reasons. First, optimisation models are used in energy economics to calculate cost-optimal pathways towards a decarbonized electricity system or to analyse the impact of certain policies (e.g., CO taxes, price zones, etc.). Subsequently, these pathways or policies are often analysed with regard to contribution margins of certain technologies and customer prices. Modelled electricity prices can be directly linked to a certain pathway or policy. Second, optimisation models are suited to investigate structural changes in the energy system, which is difficult for statistical models as they rely on historical data. Therefore, optimisation models can provide an insight on how electricity prices will develop under different conditions.

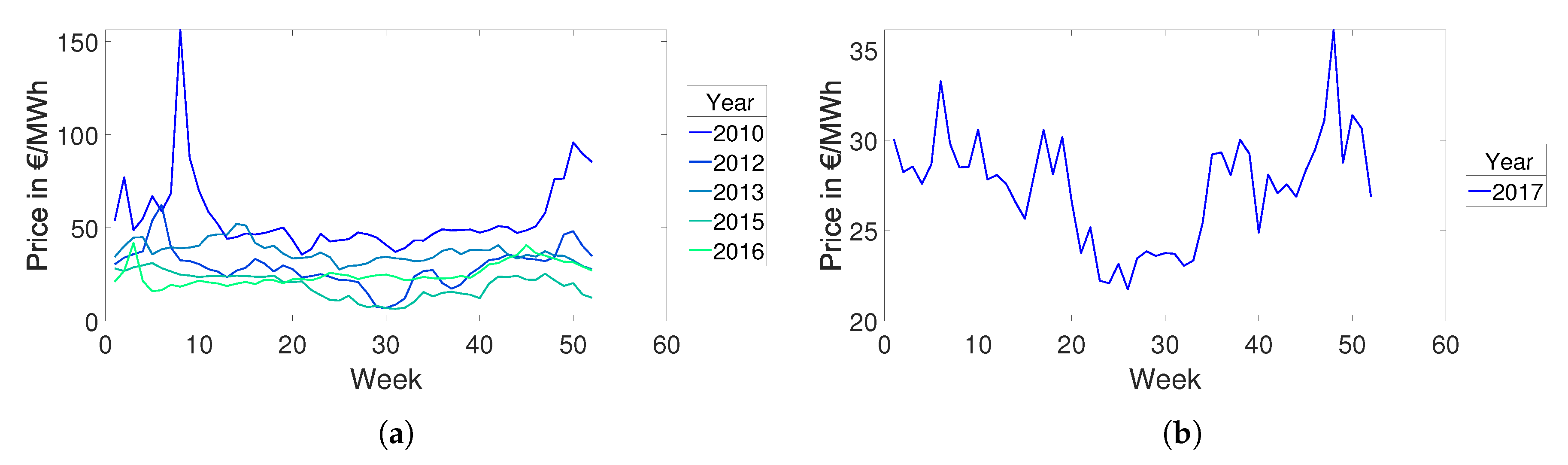

However, optimisation models should be able to capture the right trends and structure of electricity market prices. Under the assumption of an ideal market, in a thermally dominated power plant fleet, the marginal costs of production of the most expensive power plant are price-setting if the start-up and shut-down costs are neglected. With an increasing share of renewable energies, this would lead to a drop in prices for the majority of hours in the year. However, in markets with a high ratio of storage facilities, opportunity costs must also be taken into account and opportunity costs depend on expectations for the future. The average annual electricity market prices in Norway are about 36 €/MWh and clearly show seasonal structures (considered years: 2008–2017) [

1]. These seasonal structures are not adequately captured by deterministic models. We believe that long-term uncertainty has an impact on the modelled price structure in markets with high shares of renewable energies and storages. Therefore, it is also becoming more relevant for countries like Germany.

There is some literature on electricity spot price modelling with optimisation models, e.g., [

2,

3,

4,

5]. In [

2], both the day-ahead and the reserve market are modelled, while the other papers mentioned focus on the day ahead or intraday market. In [

3,

4,

5], an attempt is made to better meet price structures, as the price curves modelled with optimisation models are often too flat. In [

3], bidding mark-ups, e.g., start-up costs and risk premiums are added to the model. In [

5], the factors for price formation that cannot be explained by a fundamental optimisation model are explained with the help of a regression model, where the “main differences can be attributed to (avoided) start up-costs, market states and trading behavior” [

5]. The authors of [

4] analyse the impact of too narrow margins in modelled electricity prices on storages. In their model, the authors allow bids under and over the marginal production costs. For modelling purposes, however, historical storage production is subtracted from demand as a fixed hydrograph. However, these papers focus more on short-term modelling than on seasonal price variations. Therefore, they do not examine the influence of uncertainty on intra-year price structures. Additionally, the above-mentioned papers do not focus on markets with high shares of renewable energies and storages.

The importance of modelling uncertainty of intermittent renewable energies in hydro-thermal power plant parks for flexibility investments as well as (hydro) power plant scheduling is shown by several authors (e.g., [

6,

7]). Research on and use of stochastic modelling in markets with high shares of renewable energies and storages is widespread (e.g., [

8,

9,

10,

11,

12,

13,

14,

15,

16]). However, these papers do not deal with the influence of uncertainty on electricity market prices.

We found the following papers that examine the relationship between long-term uncertainty and electricity market prices. In [

17], the authors name the most important factors for modelling Norwegian electricity market prices. One of them is uncertainty regarding water inflow. They examine the effects of aggregated hydro power and temperature-dependent demand on electricity prices in case studies. Although the authors include uncertainty regarding water inflow into their model with a stochastic dual programming (SDP) approach, they do not analyse the impact of modelling uncertain water inflow on electricity prices. The authors of [

18] use a stochastic dual dynamic programming (SDDP) approach to address uncertainty. Their model is, among other things, used to model electricity market prices. However, they do not investigate the influence of modelling uncertainty on electricity prices. The authors of [

19] use a model similar to the one used in [

18]. Both models are based on the SDDP approach presented by [

20]. In [

19], the authors compare the SDP approach of [

17] with two SDDP approaches regarding electricity price modelling. The first one uses a statistical model to generate water inflow scenarios for the optimisation as well as the simulation. We denote this model with SDDP-1. The second approach uses the statistical model for the optimisation, but for the simulation historical inflow series are used (SDDP-2). When comparing the SDP approach to the SDDP-1 approach, they found out that the prices modelled with the SDP model are more volatile and higher than in the compared model. In contrast to that, the modelled prices of the SDDP-2 model are higher and more volatile than those of the SDP model. The authors of [

21] point out that those statistical models tend to underestimate the variance of the error term and thus underestimate extreme events. It is therefore likely that the SDDP-2 model has higher and more volatile prices than the SDDP-1 model for the following reason: The optimisation has not taken into account these more extreme water inflows, but the model still had to cope with them when the historic water inflow series realized in the simulation. The authors of [

21] propose a two stage SDDP model where both the water inflow series for the optimisation and the simulation are historical. The main objective of the paper was to develop a model that can deal with uncertainty as well as possible. As prices with this approach are less volatile and lower than those of the SDDP-2 model in [

19], the authors conclude that their model is better, as it can cope better with realistic water inflow series.

The literature review shows that modelling long-term uncertainty definitely has an impact on electricity prices in a market with a high share of renewable energies and storages. Different modelling approaches regarding uncertainty lead to different electricity prices. However, it is still open how uncertainty influences price structures within a year. Moreover, it is open which error occurs in not modelling uncertainty and thus it is not possible to deduce the importance of modelling uncertainty. Furthermore, if uncertainty affects electricity prices, there is a lack in understanding why it does affect electricity prices and which factors change the impact of uncertainty.

Our main findings are that uncertainty regarding water inflow combined with high shares of storages has a major influence on the structure of modelled electricity market prices. Water inflow, demand, and export profiles lead to a seasonal price structure when considering uncertainty of water inflow. Seasonal prices for primary energy sources and import intensify this effect. The higher the uncertainty of water inflow, the higher is the effect on the structure of electricity prices. Uncertainty has a significant influence in markets with a high share of renewable energies and storages because of two reasons. First, the inflow of water is afflicted with relatively high uncertainty. Second, the value of the energy in storages depends on the expected value of the future price scenarios. By modelling uncertainty, we recognise the seasonal price structures that exist in Norway. We conclude that the modelling of uncertainty concerning water inflow is an important factor for modelling prices with optimisation models in markets with high shares of storage. The principle price building mechanisms and effects shown in this paper also hold true for other uncertainties that have seasonal profiles like wind, sun or demand uncertainty. The impact of such other uncertainties depend on the height of uncertainty and in case of renewable energies on the shares in the system. As wind energy capacity is growing e.g., in Denmark and Germany, as well as transmission capacities to Norway, we think that the importance of modeling those uncertainties is also growing.

2. Applied Power Market Model, Data and General Approach

In this section, we explain the models and data used for analysing the effect of uncertainty on electricity prices. In addition, the basic approach of this paper on how to analyse and explain the effects of the inflow uncertainty is presented. We start with the linear optimisation model as it serves as a basis for the stochastic model. We proceed to describe the stochastic linear optimisation model and outline how we use this model to model electricity prices and to analyse the effects of inflow uncertainty.

To understand the effect of long-term uncertainty on electricity prices, we used a rather streamlined linear optimisation model. We present the simplifications made below and discuss them in

Section 4. The model minimizes operating costs, which include variable operation and maintenance costs, fuel costs, CO

costs and import costs. The model is restricted by

a demand restriction,

capacity restrictions for all power plants,

import restrictions,

run of river restrictions,

storage balance restrictions,

initial and end fill levels and

fill level restrictions.

For a mathematical formulation of the model, see

Appendix A. The basic structure of the model is similar to widely used electricity market models (e.g.,

,

,

).

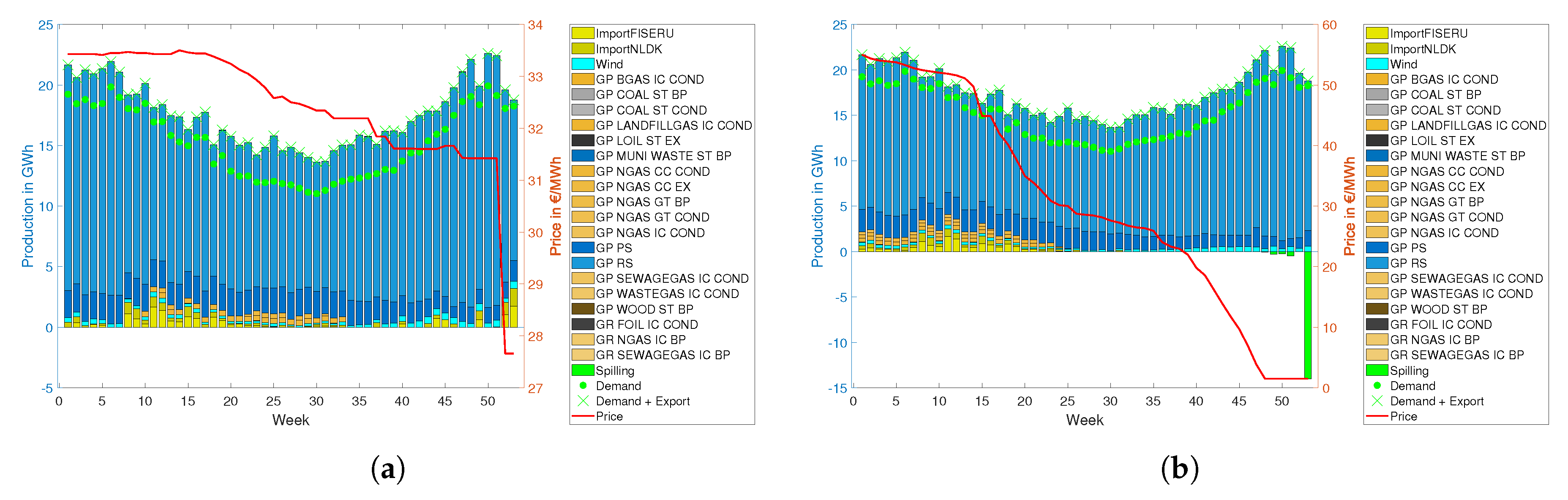

To keep the model comprehensible and fast, we took the following decisions. First of all, we aggregated all hours of the year into weekly representative time steps, as we want to analyse seasonal effects. All profiles (demand, wind, import, export, inflow) were averaged. The modelling horizon is one year. Furthermore, we aggregated the thermal power plants in terms of primary energy sources and power plant type. Moreover, all hydro power plants are aggregated into one reservoir power plant and one pumped storage power plant. We disregarded that Norway consists of five price zones and modelled Norway as one market area. Imports are modelled like power plants. Historical capacity limitations serve to restrict electricity imports and historical electricity prices in adjacent price zones represent the import costs. To obtain two representative import regions, we merged all price zones of Sweden, Finland and Russia into one representative import region as well as the Netherlands and the western price zone of Denmark into another one. For export, we decided to model it as a fixed curve added to the electricity demand curve instead. As there are only a few cogeneration of heat and power plants in Norway, we disregarded the heating market. In contrast, the reserve market in the Nordic countries is quite large, but we still neglect it here for simplicity reasons.

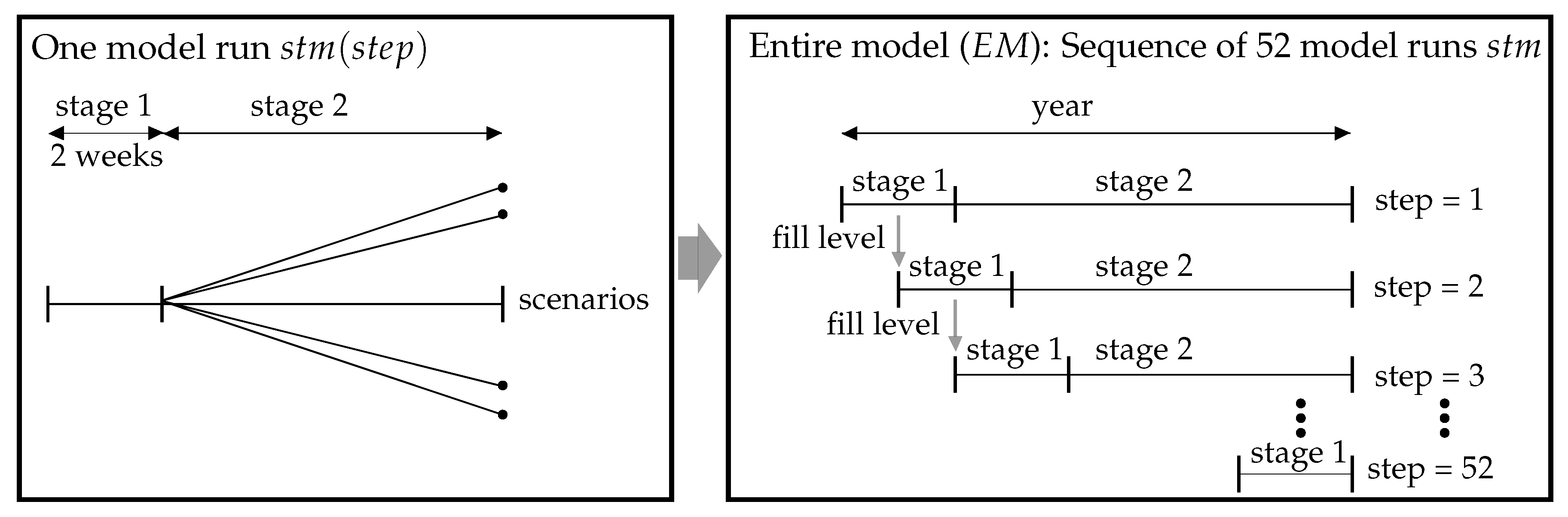

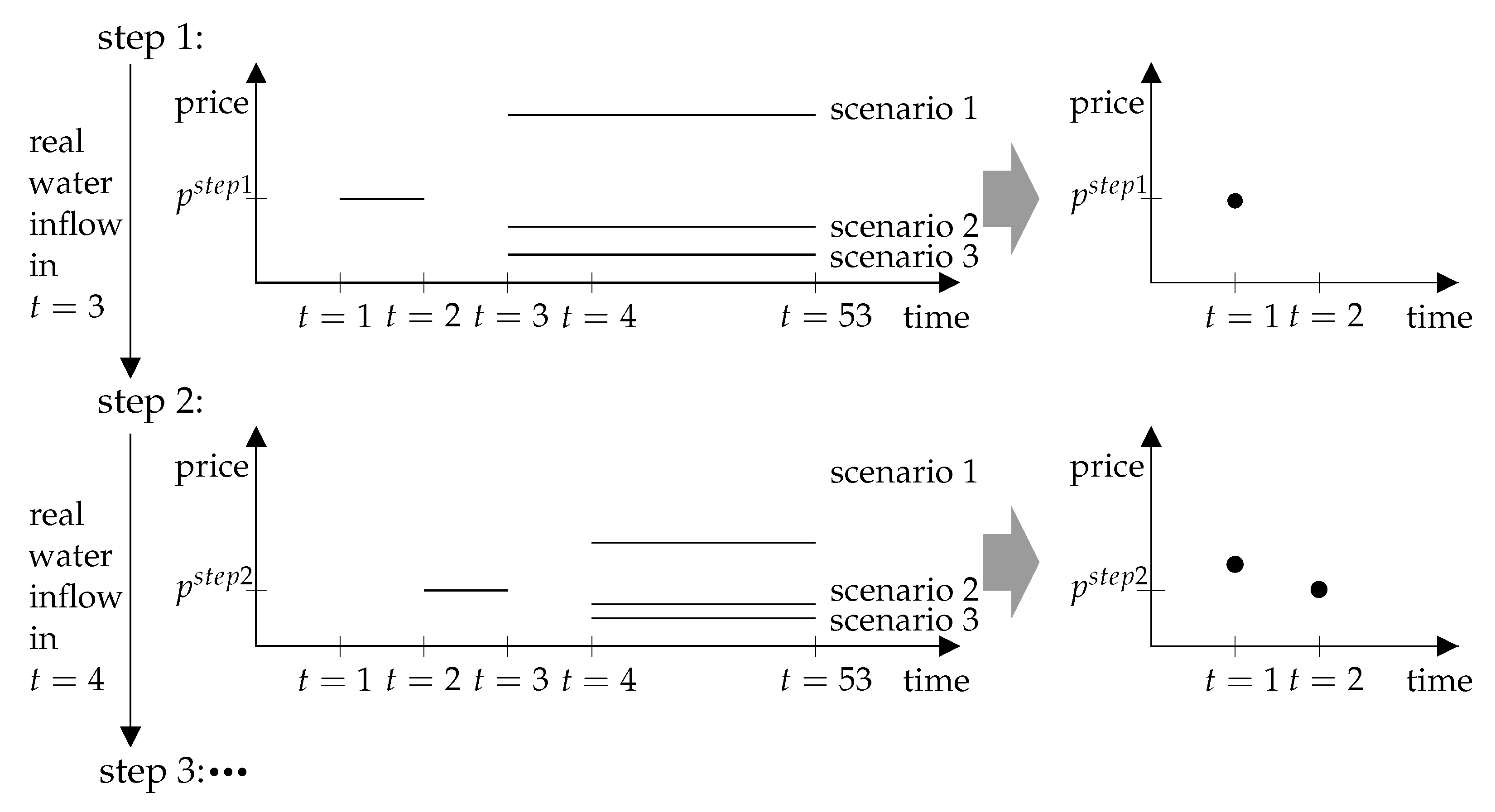

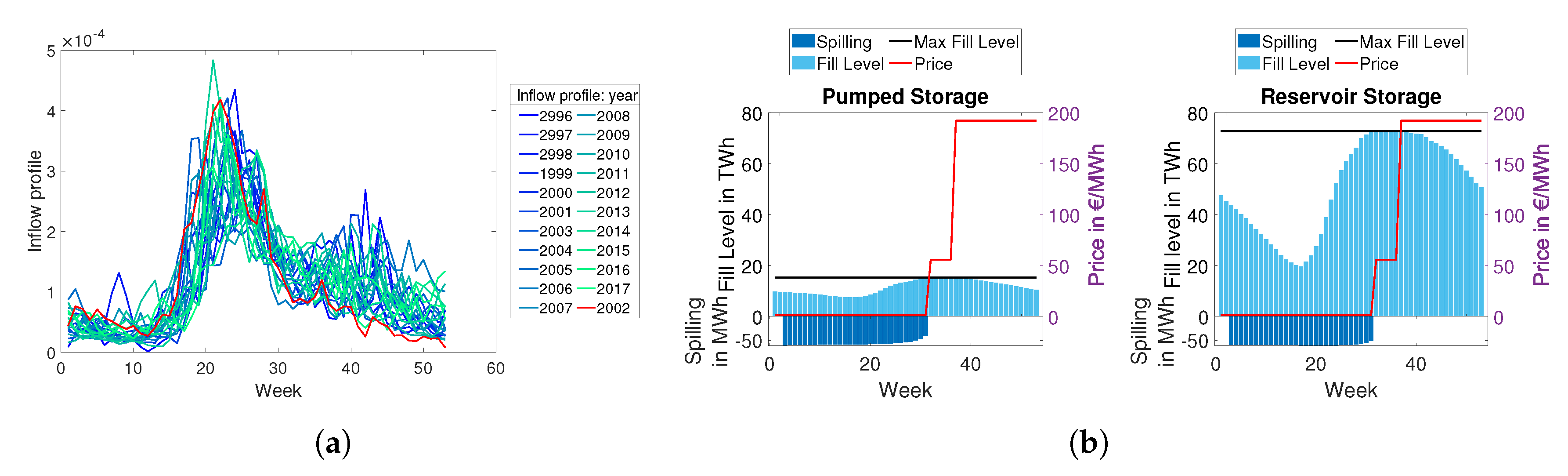

To include uncertainty regarding water inflow into the optimisation model, we used a second stage SDDP approach, with historic water inflow series for the optimisation scenarios and the simulation, based on the approach of [

21,

22]. The inflow can be predicted accurately for about one week [

7]. As our model is based on weekly time steps, we need two weeks of stage one to get a unique dual variable (see below). Therefore, the first two weeks of a stochastic model run

correspond to stage one, whereas the following weeks of uncertain water inflow correspond to stage two (see

Figure 1). With this approach, we underestimate at most the influence of uncertainty. Since we want to model a whole year and receive new information about the water inflow every week, we use a rolling horizon framework and therefore go successively through the year (see

Figure 1).

As a result, our entire model

consists of 52 stochastic model runs

. These model runs are determined by their starting week and are thus denoted with

where

. For the first model run

, the initial fill levels are exogenously given. In contrast, the initial fill levels of all other model runs

are determined by the fill levels of the previous model runs. In a first approach, only the annual water inflow quantity is uncertain and we assume the water inflow profile to be known. The water inflow of stage 2 for every scenario

in a model run

is calculated as the product of a historic water inflow profile and a yearly amount of water inflow depending on the scenario

:

for every time step

. We specify the water inflow scenarios

and their probabilities in

Section 3. The water inflow of stage 1 for time steps

is calculated in the same way, except that the annual water inflow does not depend on any scenario, but corresponds to the annual inflow of the realisation.

A more detailed and mathematical description of the stochastic model will be found in

Appendix B.

For a standard linear optimisation problem without degeneracy and an existing, finite solution, we can interpret the dual variables as shadow prices. We will briefly discuss this in the following. Following the typical nomenclature,

c denotes the cost vector,

x the variables that are optimised (e.g., production, fill level) and

represents the linear restrictions (e.g., demand restriction, capacity restrictions). For more details, see

Appendix A. The formulation of the primal problem of a linear optimisation model is:

with

and

. The associated dual problem looks as follows:

with

. We define the optimum value depending on

b as

According to [

23], the following equation holds in case of non-degeneracy:

with

signifying the optimal solution to the dual problem, and

denoting the

i-th component of the corresponding vector. For a more detailed proof, see [

23].

In the deterministic model, the dual variable of the demand restriction for each time step represents the electricity market price. The dual variable shows how the costs of the model change, when the electricity demand is marginally varied. Under the assumption of a market with perfect competition, the market participants will bid on the short-run marginal costs [

24], which includes marginal opportunity costs for storages. The most expensive bid of the market participants corresponds to the dual variable in each time step. For the stochastic model

, we always use the dual variable of week one of the demand equation of the model runs

. As we go in weekly steps through the year, we obtain an electricity price for each time step of the year.

All data are based on the Norwegian electricity market in 2017 (see

Appendix C).

The general approach to analyse the effects of inflow uncertainty in this paper is outlined in the following. First, pricing in a deterministic model in a market with high shares of renewable energies is discussed. This forms the basis for understanding the price formation in the stochastic model and for comparing the results of both approaches. Then, the principle of price formation in a stochastic model is explained.

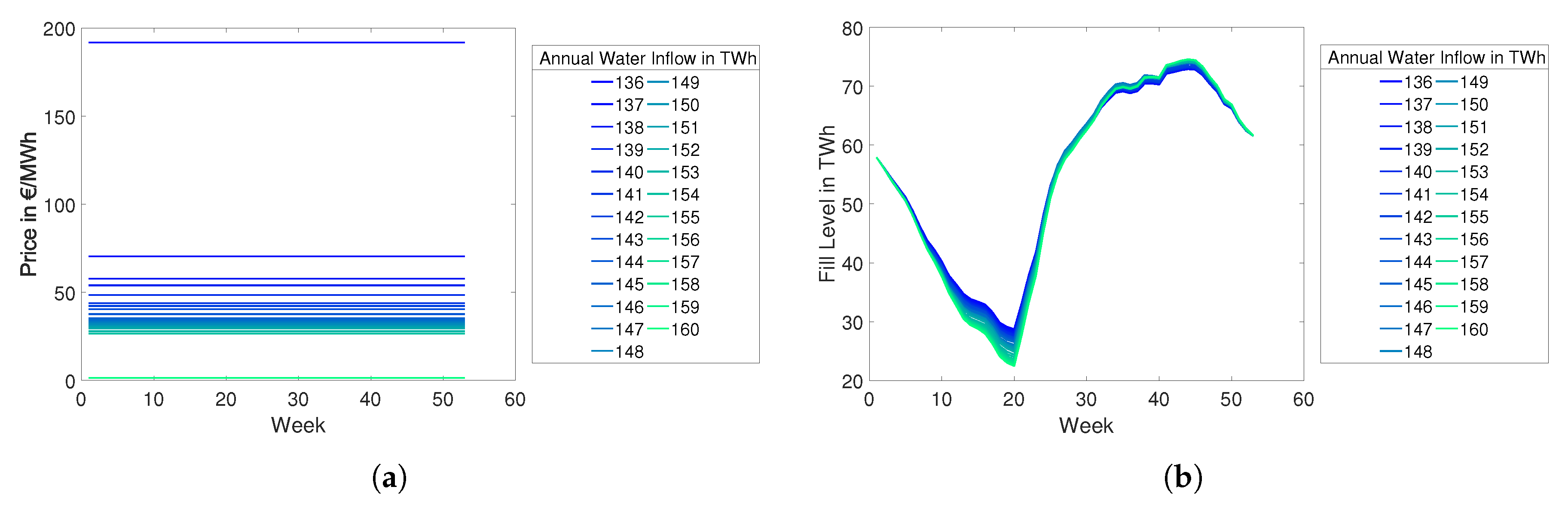

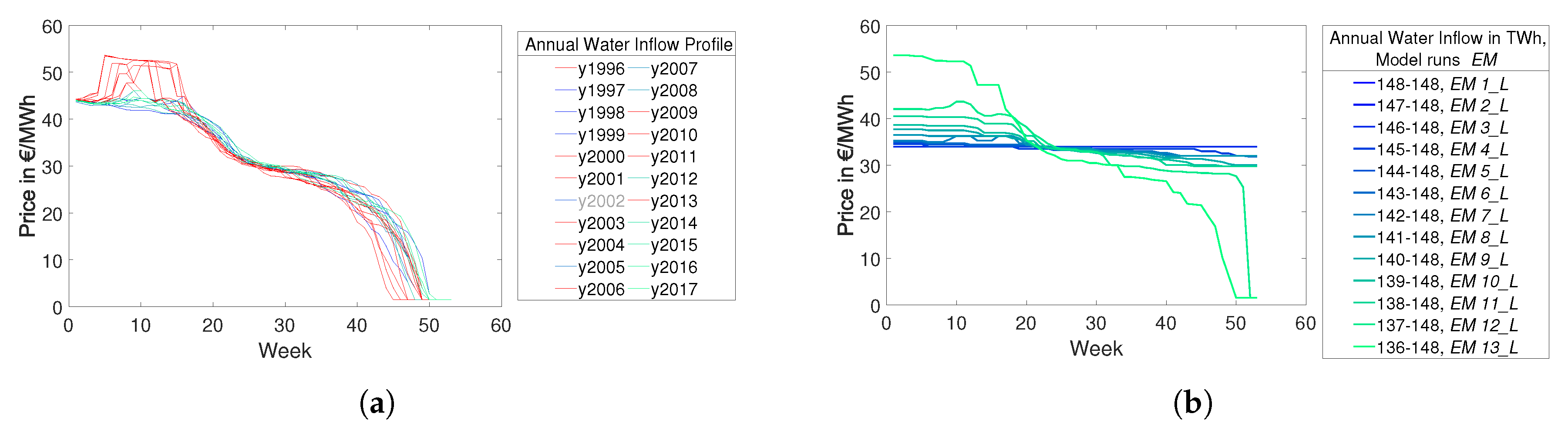

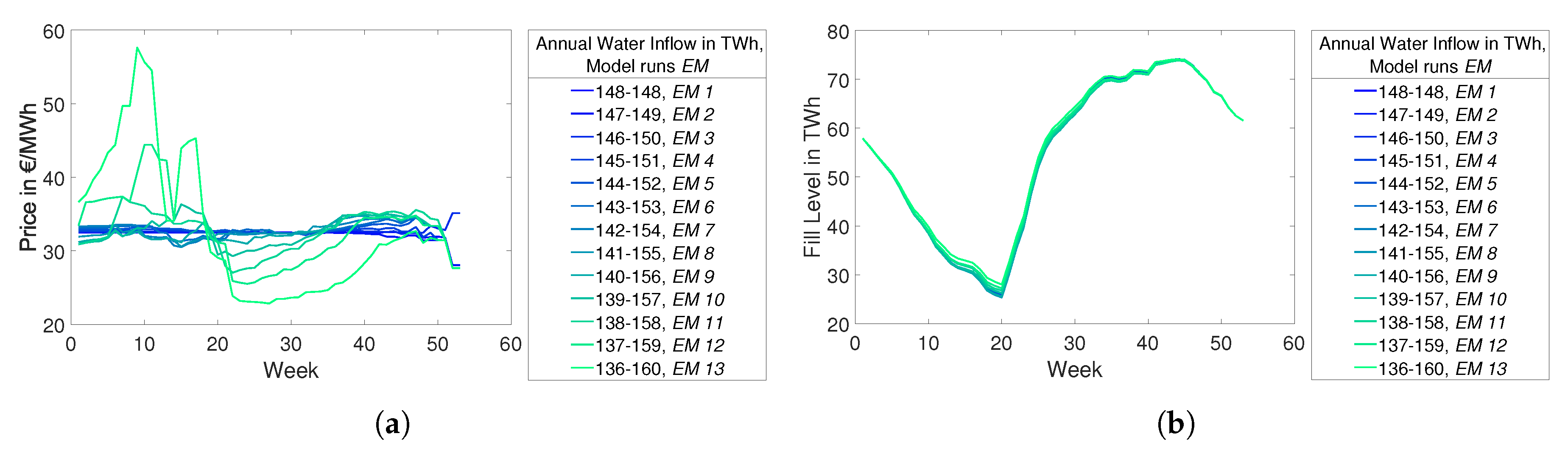

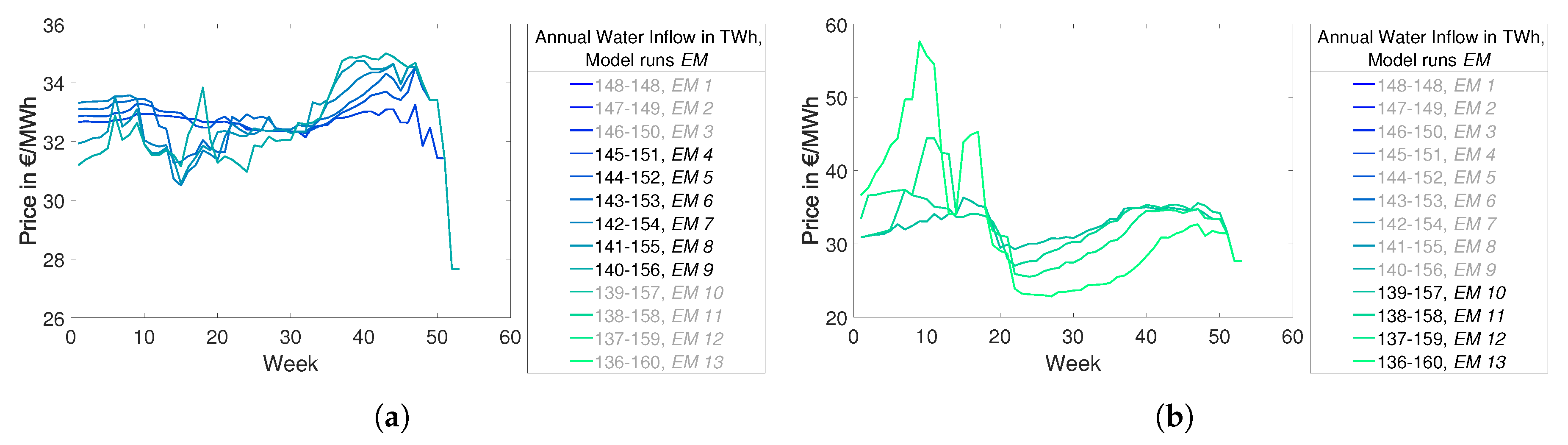

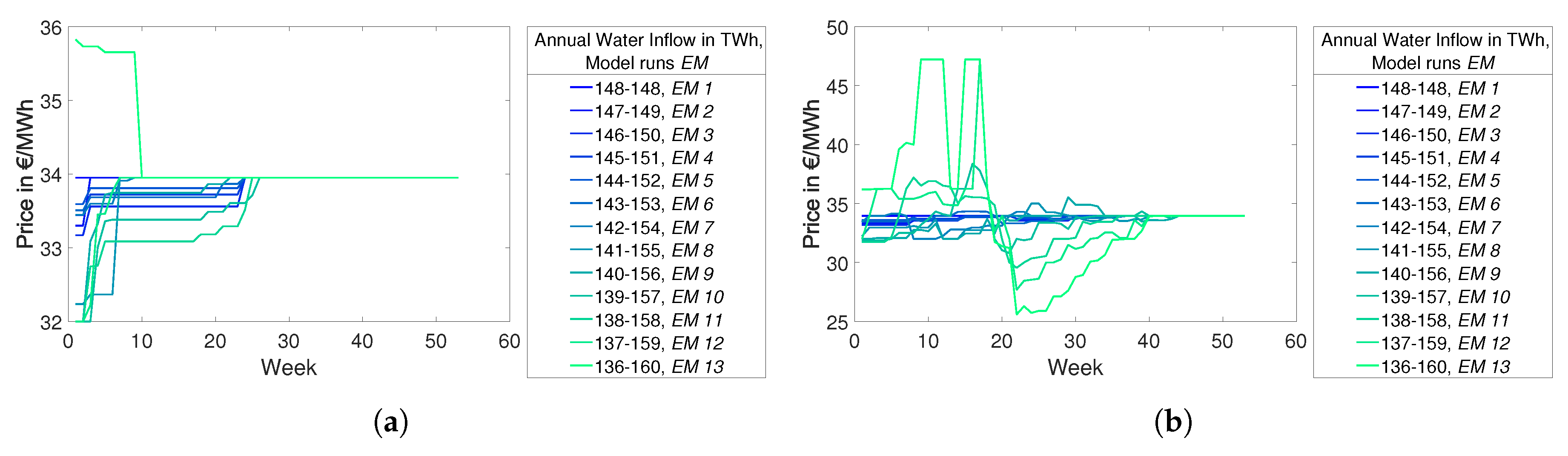

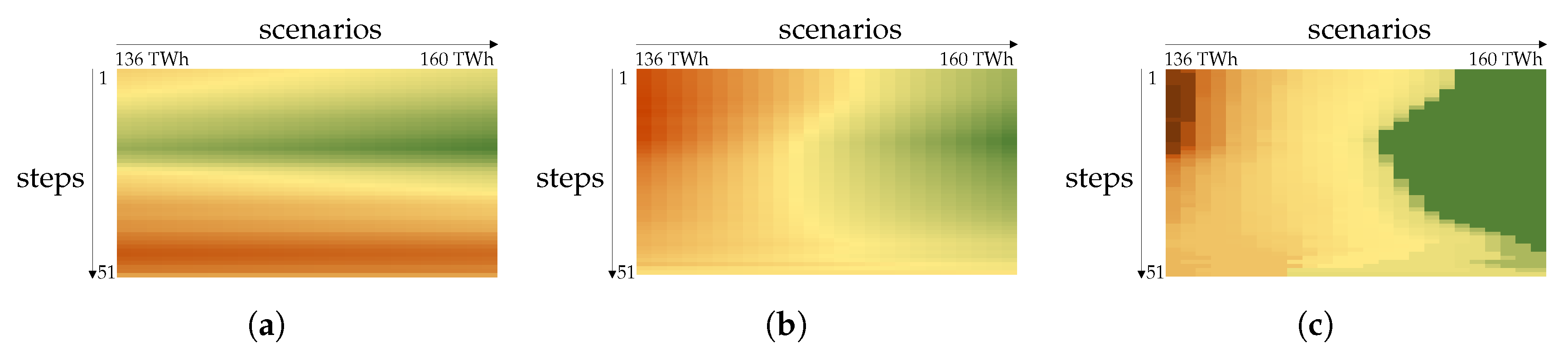

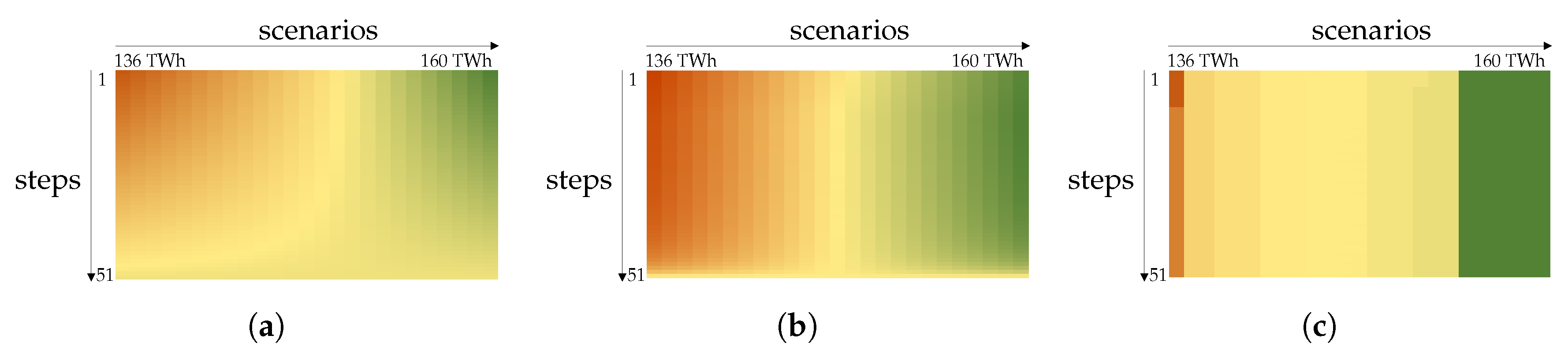

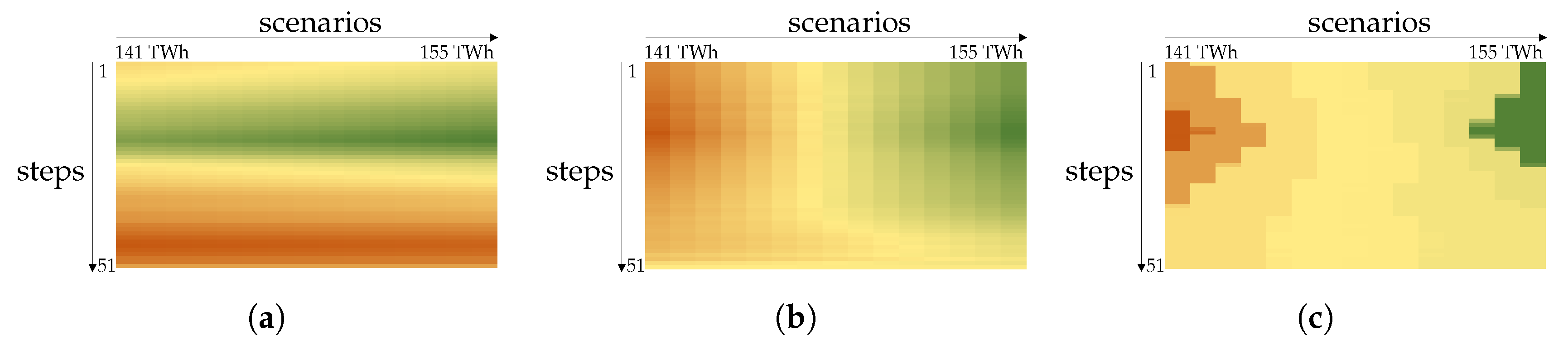

Subsequently, the influence of the inflow uncertainty is examined using the presented model. For this purpose, model runs with a different degree of uncertainty are compared. More precisely, this means that successively more scenarios are added to each model run , thus increasing the uncertainty. Hence, it can be determined what changes with increasing uncertainty and the reasons for this can be investigated. Three basic scenarios are defined for this purpose: (1) Less water is expected than inflows; (2) More water is expected than inflows; (3) The same amount of water is expected as inflow, i.e., the expected value of the water inflow of the scenarios corresponds to the real water inflow. In these three contrasting settings, the different modes of action and effects of uncertainty can be analysed well. In the first setting, we start with a model run that has only one inflow scenario and is therefore deterministic. Then, we add a second inflow scenario where the annual inflow is 1 TWh lower. In a third model run , a third scenario is added, where the annual water inflow is 1 TWh lower than the second scenario and so on. For the second setting, analogous inflow scenarios are added, which are each 1 TWh higher than the previous inflow scenario. In the third setting, two scenarios are successively added to each model run , each with 1 TWh less and 1 TWh more than the scenarios before. For all model runs, we assumed the probability of the inflow scenarios to be equally distributed.

Furthermore, for each of the settings, it is examined which previously made assumptions about profiles and costs in the model change the influence of uncertainty. These are in particular water inflow profiles, other profiles (demand, export and wind), and cost assumptions of power plants and import.

Finally, we compare our results to the actual Norwegian electricity price structure to evaluate them.

4. Discussion

In

Section 3.3.4, we have shown that the model is suitable to explain general seasonal price structures in the Norwegian market, but not to forecast prices in a realistic way. This has several reasons. For a more detailed and realistic price forecast, a more complex model, including, e.g., a detailed hydro system, a temperature-dependent demand and more differentiated costs structures including costs for demand response (see [

17]) is necessary. Moreover, the assumption that the water inflow can be perfectly predicted for two weeks and is completely uncertain for the following weeks is probably not very realistic. However, the chosen simplifications help to better understand principle price building mechanisms and the impact of selected factors on the modelled prices under uncertainty. The analyses made here serve to identify principal effects and roughly quantify their magnitude.

Still, the question remains whether the basic results of this paper remain true when using a more complex model. Including a detailed hydro system as well as availabilities for hydro power plants and a reserve market into the modelling leads to a slightly different price building mechanism. However, this is not subject of this paper but would be interesting for future work. Nevertheless, we expect the effects shown in this paper to remain roughly the same even if the above factors are taken into account.

The fact that we only modelled one year with fixed end fill levels will probably strongly influence the last modelled weeks of the year. Therefore, we made some exemplary calculations on a longer modelling horizon. We used the same method as in

Section 2 but extended the time horizon. For the longer time horizon, we used the data of the same year in succession. This results in a subdued seasonal pattern for the first modelled years. This outcome is caused by the fact that the change in inflow is smaller in relation to the total energy quantities and therefore has a smaller impact. We also made an approach for a longer time horizon for model runs

where in each model run

the modelling horizon is one year. In this setting, the seasonal structures were not subdued, but were different from the ones shown here. This is due to the fact that in each model run

there is not only new information about the water inflow, but also about the last modeled time step (e.g., demand, end fill level) which change the ratio of energy quantities. Further research should be done on this subject.

The modelling approach with fixed start and end fill levels also leads to the problem that not all historical water inflows that have occurred can be modelled. We therefore chose a more generic approach and considered all annual water inflows that are feasible.

We assumed the amount of annual water inflow to be linearly distributed, which is approximately true except for the lower limit. Hence, we rather underestimate the effect of uncertainty in this point.

The influence of different underlying water inflow profiles is, in reality, probably less pronounced, as they can be balanced by the export profile, which is fixed in our modelling approach.

On the other hand, including uncertainty regarding water inflow profiles into the modelling would affect our results. It is reasonable to assume that this increases the influence of uncertainty, but further research should be done to understand in which way.

Although some research questions remain open, we believe that the basic mechanisms and effects remain correct and provide a good basis for further investigations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}