Integration of Photovoltaics in Buildings—Support Policies Addressing Technical and Formal Aspects

Abstract

:1. Introduction

2. Approach and Methods

3. BIPV—Market, Aspects of Building Integration and Characteristics of Political Support Policies

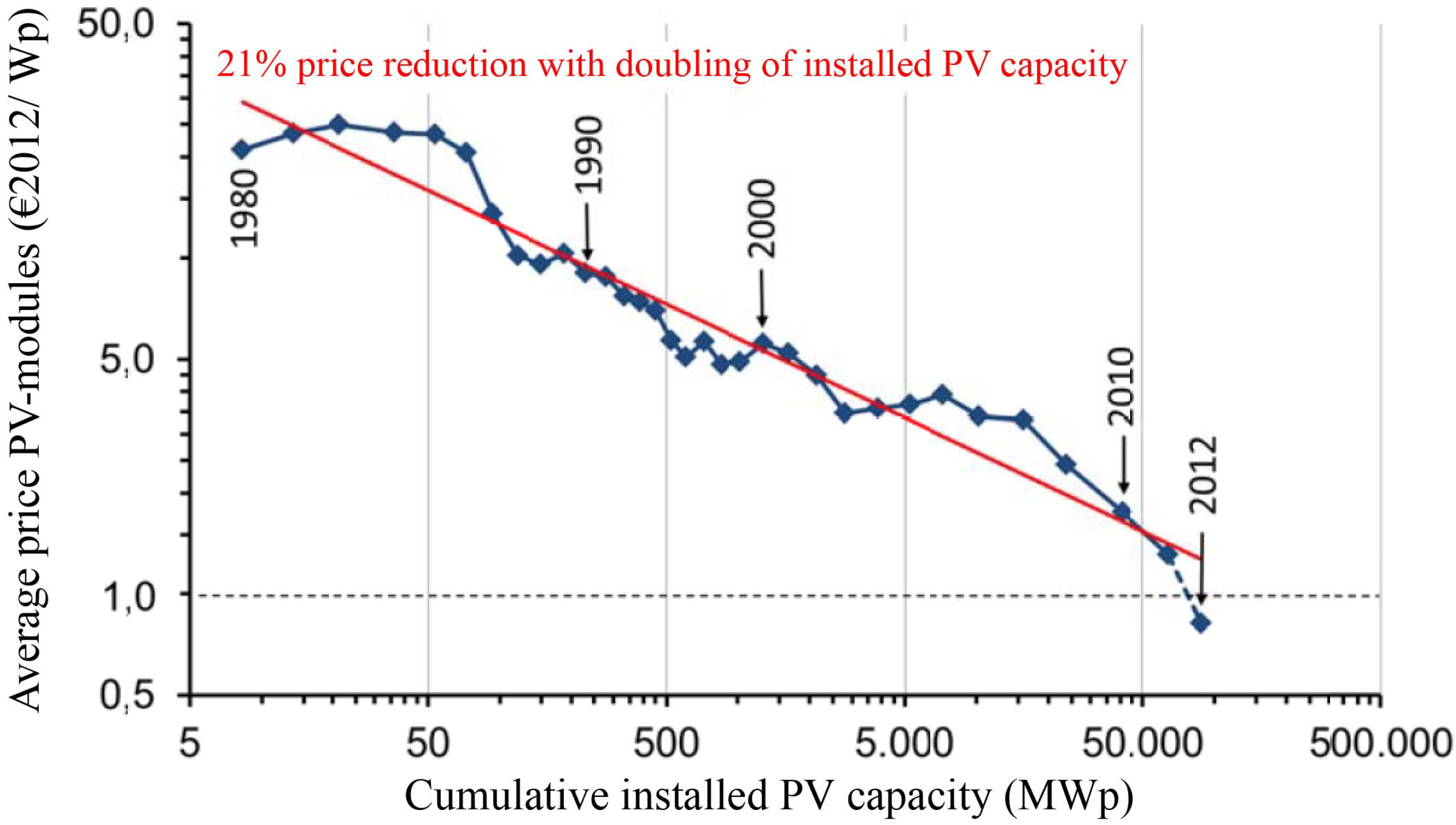

3.1. Future Market of Building Integrated Photovoltaics

3.2. Building Integrated Photovoltaics from a Technical and Formal Point of View

3.3. Characteristics of Financial Support Policies for PV and BIPV in Germany and in France

3.3.1. Characteristics of Financial Support Policies for PV and BIPV in Germany

{kind=link}

{kind=link}

{kind=link}

| Country/period | Location PV installation | Type of BIPV installation | Installed total capacity of PV installation | Feed-in tariff in euro cents/kWh | Proportion of electricity produced receiving feed-in tariff | Average feed-in tariff in euro cents/kWh for produced electricity |

|---|---|---|---|---|---|---|

| Germany 01.03.2013 – 31.03.2013 | Buildings & noise protection walls | All | 0 –10 kWp | 16.28 | 100% | 16.28 |

| All | 10 kWp–40 kWp | 15.44 | 90% | 13.90 | ||

| All | 40 kWp–1 MWp | 13.77 | 90% | 12.39 | ||

| All | 1 MWp–10 MWp | 11.27 | 100% | 11.27 | ||

| Outdoor area of non-residential buildings & sealed or converted land | No building integration | 0–1 MWp | 11.27 | 100% | 11.27 | |

| Germany 01.04.2013 – 30.04.2013 | Buildings & noise protection walls | All | 0 kWp–10 kWp | 15.92 | 100% | 15.92 |

| All | 10 kWp–40 kWp | 15.10 | 90% | 13.59 | ||

| All | 40 kWp–1 MWp | 13.47 | 90% | 12.12 | ||

| All | 1 MWp–10 MWp | 11.02 | 100% | 11.02 | ||

| Outdoor area of non-residential buildings & sealed or converted land | No building integration | 0 MW–1 MWp | 11.02 | 100% | 11.02 | |

| France 01.10.2012 – 31.12.2012 | Residential buildings | Complete (IAB) | 0 kWp–9 kWp | 34.15 | 100% | 34.15 |

| Complete (IAB) | 9 kWp–36 kWp | 29.88 | 100% | 29.88 | ||

| Buildings for education and health care | Complete (IAB) | 0 kWp–9 kWp | 22.79 | 100% | 22.79 | |

| Complete (IAB) | 9 kWp–36 kWp | 22.79 | 100% | 22.79 | ||

| Other Buildings | Complete (IAB) | 0 kWp–9 kWp | 19.76 | 100% | 19.76 | |

| All building types | Simplified (ISB) | 0 kWp–36 kWp | 19.34 | 100% | 19.34 | |

| Simplified (ISB) | 36 kWp–100 kWp | 18.37 | 100% | 18.37 | ||

| All installation types | No building integration & all above maximum integration capacity | 0 MW–12 MW | 8.40 | 100% | 8.40 | |

| France 01.01.2013 – 31.01.2013 | Residential buildings | Complete (IAB) | 0 kWp–9 kWp | 31.59 | 100% | 31.59 |

| Complete (IAB) | 9 kWp–36 kWp | 27.64 | 100% | 27.64 | ||

| Buildings for education and health care | Complete (IAB) | 0 kWp–9 kWp | 21.43 | 100% | 21.43 | |

| Complete (IAB) | 9 kWp–36 kWp | 21.43 | 100% | 21.43 | ||

| Other Buildings | Complete (IAB) | 0 kWp–9 kWp | 18.58 | 100% | 18.58 | |

| All building types | Simplified (ISB) | 0 kWp–36 kWp | 18.17 | 100% | 18.17 | |

| Simplified (ISB) | 36 kWp–100 kWp | 17.27 | 100% | 17.27 | ||

| All installation types | No building integration & all above maximum integration capacity | 0 MW–12 MW | 8.18 | 100% | 8.18 | |

| France 01.02.2013 – 31.03.2013 | All building types* | Complete (IAB) | 0 kWp–9 kWp | 31.59 | 100% | 31.59 |

| Simplified (ISB) | 0 kWp–36 kWp | 18.17 | 100% | 18.17 | ||

| Simplified (ISB) | 36 kWp–100 kWp | 17.27 | 100% | 17.27 | ||

| All installation types | No building integration & all above maximum integration capacity | 0 MW–12 MW | 8.18 | 100% | 8.18 | |

| *An additional feed-in tariff bonus of 10% or 5% is available for components made in Europe meeting IAB or ISB criteria in installations with a maximum capacitiy of less than 100 kWp | ||||||

3.3.2. Characteristics of Financial Support Policies for PV and BIPV in France

4. Conclusions and Outlook for BIPV

Acknowledgments

Conflict of Interest

References

- James, T.; Goodrich, A.; Woodhouse, M.; Margolis, R.; Ong, S. Building-Integrated Photovoltaics (BIPV) in the Residential Sector: An Analysis of Installed Rooftop System Prices; NREL/TP-6A20-53103; NREL National Renewable Energy Laboratory: Golden, CO, USA, 2011; p. 50. [Google Scholar]

- Hall, M. World Passes 100 GW Installed PV Capacity Mark. Available online: http://www.pv-magazine.com/news/details/beitrag/world-passes-100-gw-installed-pv-capacity-mark_100010145/#axzz2WGhwHqSz (accessed on 16 February 2013).

- Nicola, S. Germany Added Record Solar Panels in 2012 Even as Subsidies Cut. Available online: http://www.bloomberg.com/news/2013-01-07/germany-added-record-solar-panels-in-2012-even-as-subsidies-cut.html (accessed on 16 February 2013).

- Parkinson, G. The Top Solar Countries—Past, Present and Future. Available online: http://reneweconomy.com.au/2013/the-top-solar-countries-past-present-and-future-96405 (accessed on 16 February 2013).

- Burger, B. Photovoltaik ist mit 30 Gigawatt stärkste Stromerzeugungstechnik in Deutschland (Photovoltaics is with 30 Gigawatts most powerful Electricity Production Technology in Germany). Available online: http://www.ise.fraunhofer.de/de/aktuelles/meldungen-2012/photovoltaik-ist-mit-30-gigawatt-staerkste-stromerzeugungstechnik-in-deutschland (accessed on 16 February 2013).

- Wirth, H. Aktuelle Fakten zur Photovoltaik in Deutschland (Current Facts Regarding Photovoltaics in Germany); Fraunhofer-Institut für Solare Energiesysteme (Fraunhofer Institute for Solar Energy Systems) Fraunhofer ISE: Freiburg, Germany, 2013; p. 76. [Google Scholar]

- Kress, M.; Landwehr, I. Akzeptanz Erneuerbarer Energien in EE-Regionen; Institut für ökologische Wirtschaftsforschung (IÖW): Berlin, Germany, 2012; p. 40. [Google Scholar]

- Sensfuß, F.; Ragwitz, M.; Genoese, M. The Merit-Order Effect: A Detailed Analysis of the Price Effect of Renewable Electricity Generation on Spot Market Prices in Germany; Fraunhofer Institute Systems and Innovation Research (Fraunhofer ISI): Karlsruhe, Germany, 2007; p. 28. [Google Scholar]

- Nitsch, J.; Pregger, T.; Naegler, T.; Heide, D.; de Tena, D.L.; Trieb, F.; Scholz, Y.; Nienhaus, K.; Gerhardt, N.; Sterner, M.; et al. Langfristszenarien und Strategien für den Ausbau der Erneuerbaren Energien in Deutschland bei Berücksichtigung der Entwicklung in Europa und Global (Long-term scenarios and strategies for the development of renewable energies in Germany considering the development in Europe and global); Deutsches Zentrum für Luft- und Raumfahrt (DLR), Institut für Technische Thermodynamik Abt. Systemanalyse und Technikbewertung, Fraunhofer Institut für Windenergie und Energiesystemtechnik (IWES), Ingenieurbüro für neue Energien (IFNE): Stuttgart, Kassel, Teltow, Germany, 2012; p. 345. [Google Scholar]

- Klaus, T.; Vollmer, C.; Werner, K.; Lehmann, H.; Müschen, K. Energieziel 2050: 100% Strom aus Erneuerbaren Quellen (Energy Target 2050: 100% Electricity from Renewable Sources); Umweltbundesamt (German Federal Environmental Agency): Dessau-Roßlau, Germany, 2010; p. 196. [Google Scholar]

- Henning, H.-M.; Palzer, A. 100% Erneuerbare Energien für Strom und Wärme in Deutschland (100% Renewable Energies for Electricity and Heat in Germany); Fraunhofer-Instituts für Solare Energiesysteme (Fraunhofer Institute for Solar Energy Systems) Fraunhofer ISE: Freiburg, Germany, 2011; p. 37. [Google Scholar]

- Shell. New Lens Scenarios: A Shift in Perspective for a World in Transition; Royal Dutch Shell International: London, UK, 2013; p. 48. [Google Scholar]

- Statistische Zahlen der deutschen Solarstrombranche (Photovoltaik) [Statistical Figures of the German Solar Electricity Industry (Photovoltaics)]; Bundesverband Solarwirtschaft e.V. (German Solar Industry Association) BSW-Solar: Berlin, Germany, 2012; p. 4.

- Bofinger, S.; Glotzbach, T.; Saint-Drenan, Y.-M.; Braun, M.; Erge, T. Rolle der Solarstromerzeugung in Zukünftigen Energieversorgungsstrukturen—Welche Wertigkeit hat Solarstrom? (Role of Solar Electricity Production in Future Energy Supply Structures – What is the Siginificance of Solar Electricity?). 2008. [Google Scholar]

- Gebäudeintegrierte Photovoltaik-Systeme (Building-Integrated Photovoltaic Systems); Bundesverband Bausysteme e.V. (Federal Asscociation Construction Systems): Koblenz, Germany, 2012; pp. 1–4.

- AG Energiebilanzen e.V. Bruttostromerzeugung in Deutschland von 1990 bis 2012 nach Energieträgern (Gross Electricity Production in Germany from 1990 to 2012 by Energy Carriers). Available online: http://www.ag-energiebilanzen.de (accessed on 16 February 2013).

- Gebäudeintegrierte Photovoltaik-Systeme (Building-Integrated Photovoltaic Systems); Bundesverband Bausysteme e.V. (Federal Asscociation Construction Systems): Koblenz, Germany, 2010; pp. 1–4.

- Bernsen, O. Outlook on BIPV—Economische Kansen voor PV in Nederland. In NL Agency—Ministry of Economic Affairs; De Balie: Amsterdam, The Netherlands, 2012. [Google Scholar]

- Design-Build Solar Global BIPV Market Forecast to Hit US$7.5 Billion by 2015. Available online: http://www.designbuildsolar.com/news/global_bipv_market_forecast_to_hit_us7.5_billion_by_2015/ (accessed on 16 February 2013).

- Building-Integrated Photovoltaics Markets—2012; NanoMarkets: Glen Allen, VA, USA, 2012.

- European Commission. Energy Performance of Buildings; Directive 2010/31/EU; European Parliament and the Council of the European Union: Brussels, Belgium, 2010; p. 23. [Google Scholar]

- Chun, S. Korean Energy Management Cooperation, Building Energy Policies in Korea. In International Workshop EPC (Energy Performance Certificate) and Assessor System for Buildings; Korean Energy Management Cooperation: Seoul, Korea, 2012. [Google Scholar]

- Schuetze, T.; Hullmann, H. Wirtschaftliche Aspekte Beim Einsatz Multifunktionaler Photovoltaischer Bauteile (Economical Aspects of Mutifunctional Photovoltaic Building Component Applications). In Proceedings of the Symposium on Photovoltaische Solarenergie, Kloster Banz, Bad Staffelstein, Germany, 2–4 March 2011; pp. 546–551.

- Bendel, C. Multifunktionale Photovoltaikprodukte (Multifunctional Photovoltaic Products). In Proceedings of the Symposium on Photovoltaische Solarenergie, Kloster Banz, Bad Staffelstein, Germany, 5–7 March 2008; pp. 1–16.

- Vorschläge Zur Aktuellen EEG Debatte (Proposals to the Current EEG Debate); Bundesverband Bausysteme e.V. (Federal Asscociation Construction Systems): Koblenz, Germany, 2012.

- Hullmann, H.; Schuetze, T.; Bendel, C.; Funtan, P.; Kirchhof, J. Multifunktionale Photovoltaik—Photovoltaik in der Gebäudehülle (Multifunctional Photovoltaics—Photovoltaics in the Building Envelope); hwp—hullmann, willkomm & partner & Institut für Solare Energieversorgungstechnik (Institute for Solar Energy Supply Technology) ISET e.V.: Hamburg & Kassel, Germany, 2006; p. 92. [Google Scholar]

- Niederfuehr, M. BIPV—Technology Transfer from Bonded Construction Systems to PV. In Proceedings of the 27th European Photovoltaic Solar Energy Conference and Exhibition, Frankfurt, Germany, 25 September 2012; pp. 4224–4226.

- Lai, C.-M.; Lin, Y.-P. Energy saving evaluation of the ventilated BIPV walls. Energies 2011, 4, 948–959. [Google Scholar] [CrossRef]

- Dubey, S.; Tiwari, G.N. Analysis of PV/T flat plate water collectors connected in series. Sol. Energy 2009, 1485–1498. [Google Scholar] [CrossRef]

- Langniß, O.; Diekmann, J.; Lehr, U. Advanced mechanisms for the promotion of renewable energy—Models for the future evolution of the german renewable energy act. Energy Policy 2009, 1289–1297. [Google Scholar] [CrossRef]

- Frantzen, J.; Hauser, E. Kurzfristige Effekte der PV-Einspeisung auf den Großhandelsstrompreis (Short-term Effects of PV Feed-In on Wholesale Electricity Price); Institut für Zukunfts EnergieSysteme (Institute for Future Energy Systems) IZES: Berlin, Germany, 2012; p. 40. [Google Scholar]

- Hintergrund zur EEG-Umlage 2013 (Background Information on EEG Surcharge); Bundesverband Erneuerbare Energie e.V. (Federal Association Renewable Energy) BEE: Berlin, Germany, 2012; p. 14.

- Bundesministerium für Umwelt Naturschutz und Reaktorsicherheit (Federal Ministry for the Environment, Nature Conservation and Nuclear Safety). Photovoltaik: Einigung im Vermittlungsausschuss—Neuregelungen treten rückwirkend zum 1 April 2012 in Kraft (Photovoltaics: Agreement in the Conciliation Committee—New Regulation is Coming Into Effect with Retroactive Effect from 1 April 2012); Berlin, Germany, 28 June 2012. Available online: http://www.erneuerbare-energien.de/erneuerbare_energien/pressemitteilungen/pm/48562.php (accessed on 16 February 2013).

- Bundesnetzagentur (Federal Network Agency) EEG-Vergütungssätze für PV-Anlagen (EEG Feed-In Tariffs for PV Installations). Available online: http://www.bundesnetzagentur.de/DE/Sachgebiete/ElektrizitaetGas/ErneuerbareEnergienGesetz/VerguetungssaetzePVAnlagen/VerguetungssaetzePhotovoltaik_node.html (accessed on 16 February 2013).

- Solarenergie-Förderverein Deutschland e.V. (German Solar Energy Development Association) Solarstrom-Vergütungen im Überblick (Overview Solar Electricity Feed-In Tariffs). Available online: http://www.sfv.de/lokal/mails/sj/verguetu.htm (accessed on 16 February 2013).

- Ernst, W. PV-Fassaden im Trend. Marktübersicht fassadenintegrierte Solarmodule (Trendy PV Facades. Market Overview Façade-Integrated Solar Modules). Metallbau 2012, 23, 52–63. [Google Scholar]

- Morlot, R. La reglementation pour L'integration des Produits Photovoltaiques au Bati (Regulation for the Integration of Photovoltaic Products in Buildings); PHOTON Réseau: Mise en oeuvre des systèmes photovoltaïques raccordés au réseau électrique (PHOTON Network: Implementation of Grid-Connected Photovoltaic Systems). Ademe: Centre d’Accueil de Valpré, Écully, France, 2005; pp. 69–83. [Google Scholar]

- Ministry of Territorial Equality and Housing & Ministry of Ecology Sustainable Development and Energy Solar Decathlon 2014 in France. Available online: http://www.solardecathlon2014.fr (accessed on 26 August 2012).

- Durand, Y. Photovoltaic Power Applications in France. National Survey Report 2011; French Agency for Environment and Energy Management (ADEME): Paris, France, 2012; p. 25. [Google Scholar]

- Pouthier, A. Photovoltaïque: le tarif d’achat de l’électricité produite par les installations intégrées en toiture entre 36 et 100 kWc augmenté de 5% (Photovoltaics: The Purchase Price of Electricity Genenerated by Integrated Rooftop Installations between 36 and 100 kWp Increased by 5%). Available online: http://www.lemoniteur.fr/137-energie/article/actualite/19151001-photovoltaique-le-tarif-d-achat-de-l-electricite-produite-par-les-installations-integrees-en-toiture (accessed on 16 February 2013).

- Actu-Evironnement (News-Environment) Photovoltaïque: les nouveaux tarifs d'achat intègrent les mesures d'urgence (Photovoltaics: New Purchase Prices include Emergency Measures). Available online: http://www.actu-environnement.com/ae/news/tarifs-achat-photovoltaique-baisse-bonification-simplification-17716.php4 (accessed on 16 February 2013).

- CEIAB Comité d'Evaluation des produits photovoltaïques Intégrés au Bâti (Committee for the Assessment of Building-Integrated Photovoltaic Products) Liste des procédés d'intégration photovoltaïques éligibles (List of eligible Photovoltaics Integration Processes). Available online: http://www.ceiab-pv.fr/ (accessed on 26 August 2012).

- HWP—Hullmann, Willkomm & Partner. Available online: http://www.hwp-hullmann-willkomm.de (accessed on 17 June 2013).

- KORANET Joint Call on Green Technologies. Available online: www.koranet.eu (accessed on 17 June 2013).

© 2013 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Schuetze, T. Integration of Photovoltaics in Buildings—Support Policies Addressing Technical and Formal Aspects. Energies 2013, 6, 2982-3001. https://0-doi-org.brum.beds.ac.uk/10.3390/en6062982

Schuetze T. Integration of Photovoltaics in Buildings—Support Policies Addressing Technical and Formal Aspects. Energies. 2013; 6(6):2982-3001. https://0-doi-org.brum.beds.ac.uk/10.3390/en6062982

Chicago/Turabian StyleSchuetze, Thorsten. 2013. "Integration of Photovoltaics in Buildings—Support Policies Addressing Technical and Formal Aspects" Energies 6, no. 6: 2982-3001. https://0-doi-org.brum.beds.ac.uk/10.3390/en6062982