Number of Financial Indicators as a Factor of Multi-Criteria Analysis via the TOPSIS Technique: A Municipal Case Study

Abstract

:1. Introduction

2. Theoretical Background

- Capable of fulfiling immediate or short-term (within one year) financial obligations;

- Capable of fulfiling one’s own financial obligations over the course of the budget year;

- Capable of fulfiling long-term financial obligations;

- Capable of financing programmes and services at a basic level as required by law.

Individual Financial Analysis at the Level of Local Governments

- The implementation of a set of regulatory rules issued by the Basel committee on banking supervision in 2004, known as “Basel II”, which set new terms for the value of capital and risk requirements for the banking sector;

- The eruption of the global financial crisis in 2008, which manifested in the bankruptcy of a number of enterprises and the destabilisation of individual economies.

- Statistical techniques (logit and probit models, discriminatory analysis methods, and factor analysis);

- Artificial intelligence and data-mining techniques (neural networks, decision-making trees, and supporting vector theory);

- Theoretical models (based on expert assessment).

- The selected financial indicators should have clear significance for Greek municipalities. In this case, the authors based their concept on specialist literature about the financial characteristics of subjects in the public sector,

- During the selection of financial indicators, the particularities of Greek local governments should be taken into consideration, particularly in relation to acquiring funds from the government;

- The number of evaluation criteria should not be too great and should be restricted to the minimum to ensure ease of use and the ability to update the resulting model.

3. Materials and Methods

- SG1: Identification of a homogenous group of municipalities from the perspective of the flow of funds from the state;

- SG2: Identification of a set of potential indicators for the requirements of assessing municipalities under Czech conditions;

- SG3: Quantification of differences arising from the use of various arrangements of the indicators.

3.1. Identification of Homogenous Groups of Municipalities from the Perspective of the Flow of Funds from the State

3.2. Identification of Homogenous Groups of Municipalities from the Perspective of the Flow of Funds from the State

- I1: Volume of total income per capita in CZK (MAX),

- I2: Volume of total assets (property) per capita in CZK (MAX),

- I3: Volume of total expenditure per capita in CZK (MIN),

- I4: Volume of liabilities per capita in CZK (MIN).

3.3. Identification of Homogenous Groups of Municipalities from the Perspective of the Flow of Funds from the State

- Methods of assessment based on a single criterion;

- Methods of assessment based on multiple criteria;

- Comparative methods;

- Managerial assessment methods;

- Other selected assessment methods.

3.3.1. Introduction of the TOPSIS Technique as One of the MCDM Approaches to Assess Effectiveness

4. Assessment of the Financial Health of the Selected Group of Municipalities

4.1. Assessment Based on a Single Indicator (Variants A1, A2, A3, and A4)

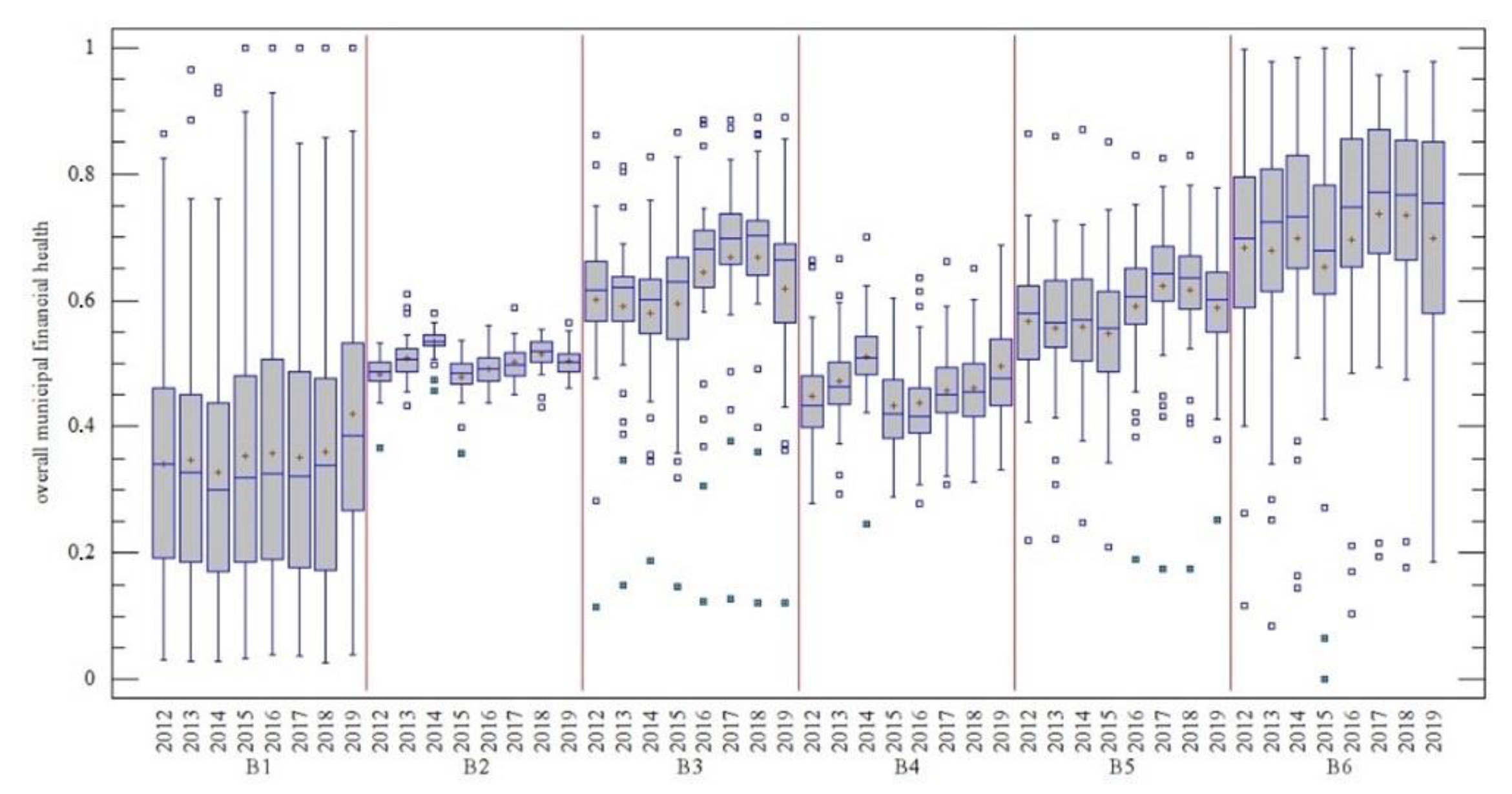

4.2. Assessment Based on Two Indicators (Variants B1, B2, B3, B4, B5, and B6)

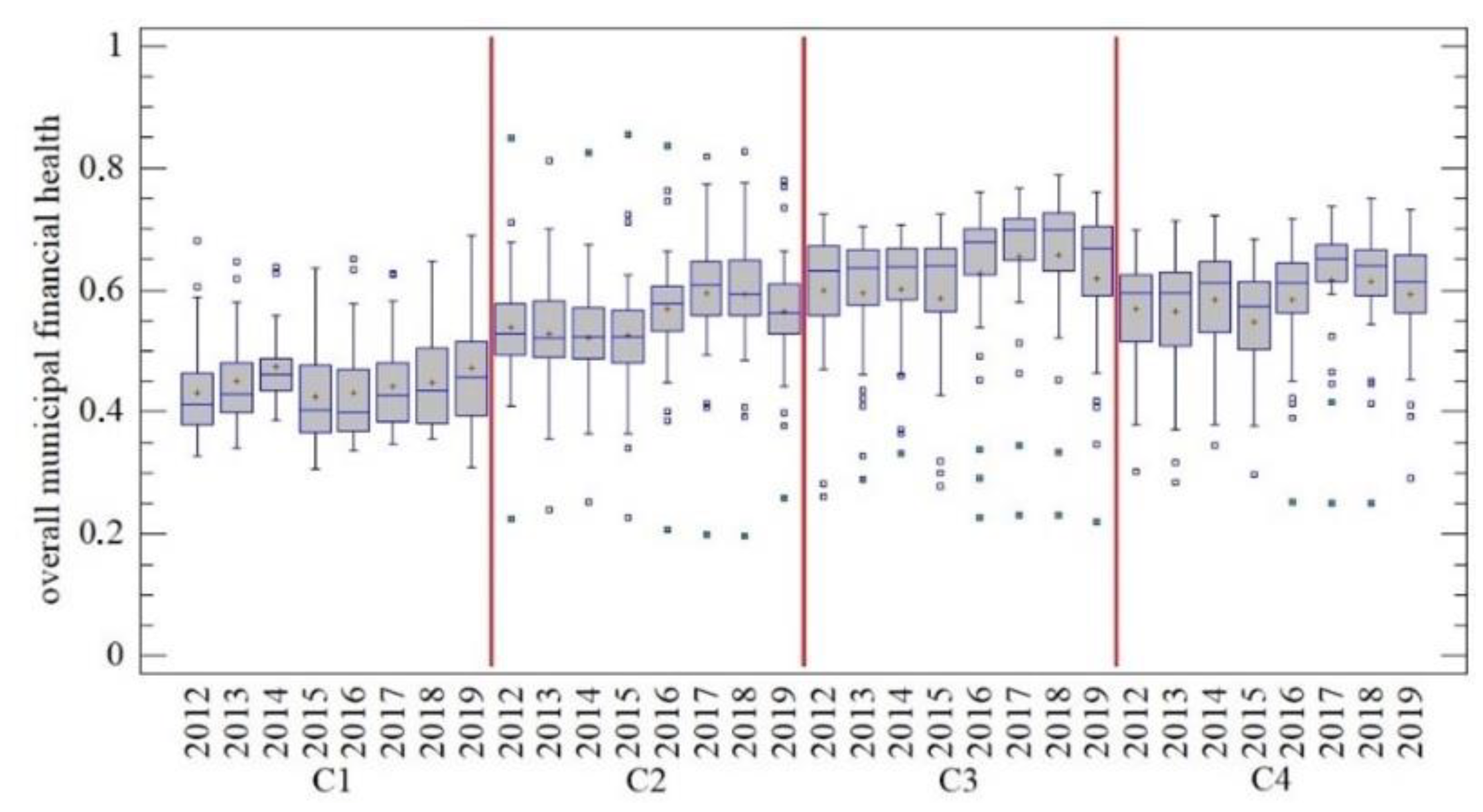

4.3. Assessment Based on Three Indicators (Variants C1, C2, C3, and C4)

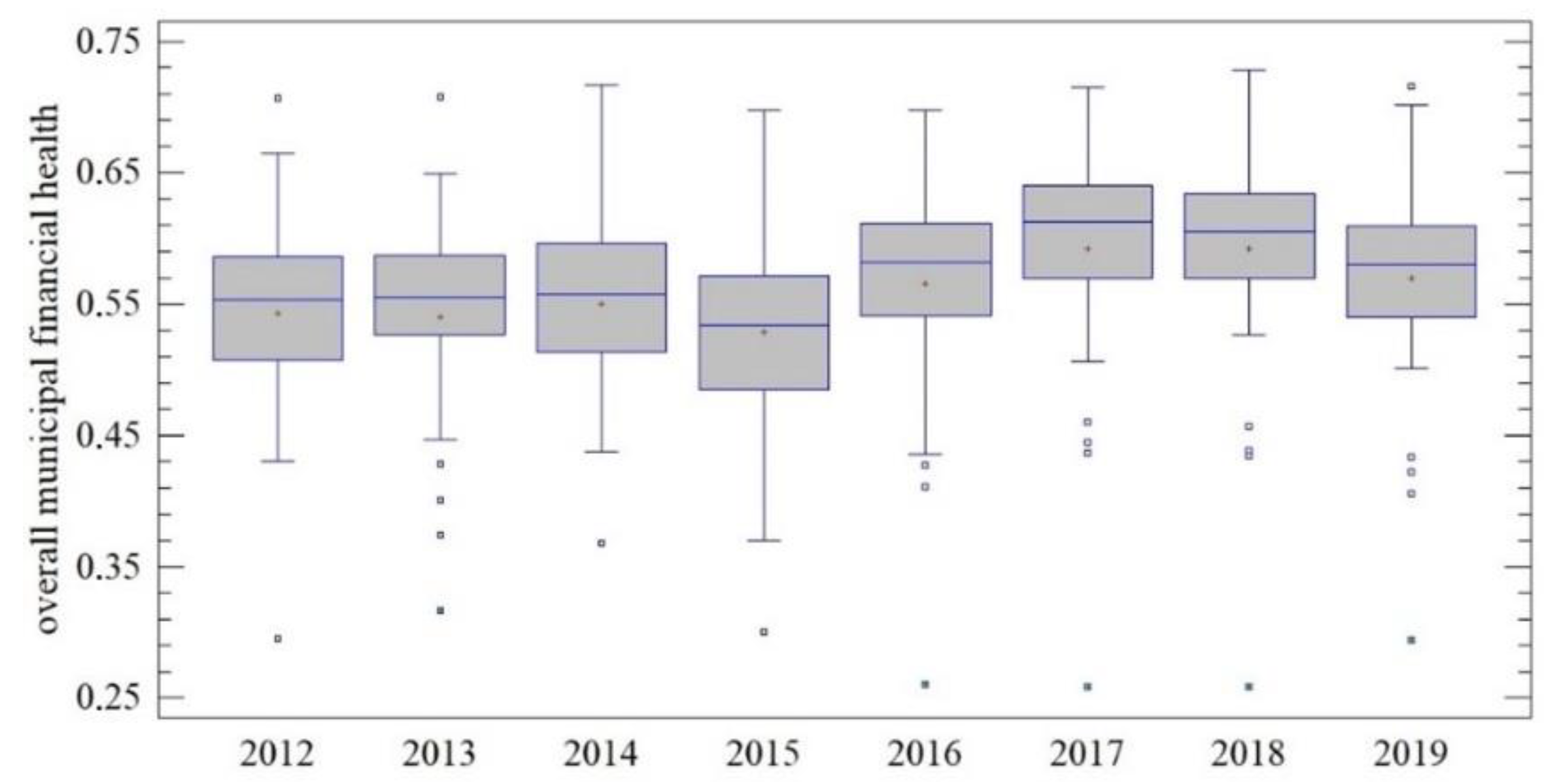

4.4. Assessment Based on Four Indicators (Variant D1)

4.5. Assessment of the Similarity of the Acquired Results

5. Discussion and Conclusions

- The basis of assessment is the identification of a relevant set of alternatives (a criteria matrix), which should have similar attributes across the assessed subjects to the greatest degree possible; thus, the (partial) homogeneity of the assessed set is an essential prerequisite for assessment;

- The selection of indicators that will subsequently be the subject of assessment should be subject to expert discussion or an extensive analysis of literary sources to demonstrate the justifiability of the specific criterion;

- Assessment based on a low number of indicators is insufficient, highly variable, and diverse.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Hiadlovský, V.; Rybovičová, I.; Vinczeová, M. Importance of Liquidity Analysis in the Process of Financial Management of Companies Operating in the Tourism Sector in Slovakia: An Empirical Study. Int. J. Qua. Res. 2016, 10, 799–812. [Google Scholar]

- Jegers, M. Financing constraints in nonprofit organisations: A ‘Tirolean’ approach. J. Corp. Financ. 2011, 17, 640–648. [Google Scholar] [CrossRef]

- Grizzle, C.; Sloan, M.F.; Kim, M. Financial factors that influence the size of nonprofit operating reserves. J. Public Budg. Acc. Financ. Manag. 2015, 27, 67–97. [Google Scholar] [CrossRef]

- Michalski, G. Risk pressure and inventories levels. Influence of risk sensitivity on working capital levels. Econ. Comp. Econ. Cyb. Stud. Res. 2016, 50, 189–196. [Google Scholar]

- Gavurova, B.; Korony, S. Efficiency of day surgery in Slovak regions during the years 2009–2014. Econ. Ann. XXI 2016, 159, 80–84. [Google Scholar] [CrossRef] [Green Version]

- Šofránková, B.; Kiseľáková, D.; Horváthová, J. Actual questions of risk management in models affecting enterprise perfor-mance. Ekon. Čas. 2017, 65, 644–667. [Google Scholar]

- Lesáková, Ľ.; Vinczeová, M.; Ondrušová, A. Factors Determining Profitability of Small and Medium Enterprises in Selected Industry of Mechanical Engineering in the Slovak Republic—The Empirical Study. Ekon. Manag. 2019, 22, 144–160. [Google Scholar]

- Ochrana, F.; Pavel, J.; Vítek, L. Veřejný Sektor a Veřejné Finance. Financování Nepodnikatelských a Podnikatelských Aktivit; Grada Publishing: Prague, Czech Republic, 2010; pp. 1–30. [Google Scholar]

- Vavrek, R. Disparity of Evaluation of Municipalities on Region and District Level in Slovakia. In Proceedings of the Hradec Economic Day, Hradec Králové, Czechia, 3–4 February 2015. [Google Scholar]

- Otrusinova, M.; Kulleová, A. Liquidity Values in Municipal Accounting in Czech Republic. J. Comp. 2019, 11, 84–98. [Google Scholar] [CrossRef] [Green Version]

- Sebestova, J.; Majerova, I.; Szarowska, I. Indicators for assessing the financial condition and municipality management. Adm. Man. Pub. 2018, 31, 97–110. [Google Scholar]

- Sytnyk, N.; Onyusheva, I.; Holynskyy, Y. The managerial issues of state budgets execution: The case of Ukraine and Kazakhstan. Pol. J. Man. Stud. 2019, 19, 445–463. [Google Scholar] [CrossRef]

- Tkáčová, A.; Konečný, P. Krajské mestá Slovenska a ich finančné zdravie. Sci. Pap. Univ. Pard. Ser. D 2017, 41, 193–205. [Google Scholar]

- Adrian, T.; Covitz, D.; Liang, N. Financial stability monitoring. An. Rev. Fin. Econ. 2015, 7, 357–395. [Google Scholar] [CrossRef] [Green Version]

- Turco, M. The management of the financial collapse of local bodies and its economic-territorial effects: The case of the mu-nicipality of Taranto. Int. J. Pub. Sec. Perf. Man. 2017, 3, 191–207. [Google Scholar]

- Padovani, E.; Rossi, F.M.; Orelli, R.L. The Use of Financial Indicators to Determine Financial Health of Italian Municipalities. SSRN Electron. J. 2010. [Google Scholar] [CrossRef]

- Berne, R.; Schramm, R. The Financial Analysis of Governments; Prentice Hall: Englewood Cliffs, NJ, USA, 1986; pp. 1–30. [Google Scholar]

- McDonald, B.D. Measuring the Fiscal Health of Municipalities; Cambridge Press: Cambridge, UK, 2017; pp. 1–30. [Google Scholar]

- Tyson, C.J. Exploring the Boundaries of Municipal Bankruptcy. Will. Law Rev. 2014, 50, 661–683. [Google Scholar]

- Cabaleiro, R.; Buch, E.; Vaamonde, A. Developing a Method to Assessing the Municipal Financial Health. Am. Rev. Public Adm. 2012, 43, 729–751. [Google Scholar] [CrossRef]

- Halim, E.H.; Mustika, G.; Sari, R.N.; Anugerah, R.; Mohd-Sanusi, Z. Corporate governance practices and financial performance: The mediating effect of risk management committee at manufacturing firms. J. Int. Stud. 2017, 10, 272–289. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Zhatkin, Y.; Gurvits, N.; Strouhal, J. Addressing Ethical Matters in Ukrainian Accounting Practice. Econ. Sociol. 2017, 10, 167–178. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Opluštilová, I. Finanční Zdraví Obcí a Jeho Regionální Diferenciace; Masaryk University: Brno, Czech Republic, 2012; pp. 1–50. [Google Scholar]

- Peková, J.; Jetmar, M.; Tóth, P. Veřejný Sektor, Teorie a Praxe v ČR; Wolters Kluwer ČR: Prague, Czech Republic, 2019; pp. 325–337. [Google Scholar]

- Horvat, T.; Vidmar, M.; Justinek, G.; Bobek, V. Legislative, Organisational, and Economic Factors of Debt Level of Munici-palities in Slovenia. Lex Loc. J. Loc. Self-Gov. 2020, 18, 1067–1093. [Google Scholar]

- Brezovnik, B.; Finžgar, M.; Padovnik, S.A.; Mlinarič, F.; Oplotnik, Ž.J. Financing Municipal Tasks in Slovenia. Hrvat. Komparat. Javna Uprava 2019, 19, 173–206. [Google Scholar] [CrossRef]

- Dzialo, J.; Guziejewska, B.; Majdzinska, A.; Zoltaszek, A. Determinants of Local Government Deficit and Debt: Evidence from Polish Municipalities. Lex Loc. J. Loc. Self-Gov. 2019, 17, 1033–1056. [Google Scholar]

- Mihalovič, M. Performance Comparison of Multiple Discriminant Analysis and Logit Models in Bankruptcy Prediction. Econ. Sociol. 2016, 9, 101–118. [Google Scholar] [CrossRef] [PubMed]

- Mihalovič, M. Využitie skóringových modelov pri predikcii úpadku ekonomických subjektov v Slovenskej republike. Politická Ekon. 2018, 66, 689–708. [Google Scholar]

- Cohen, S.; Kaimenakis, N.; Venieris, G. Reaping the Benefits of Two Worlds: An Exploratory Study of the Cash and the Accrual Accounting Information Roles in Local Governments. J. App. Acc. Res. 2009, 14, 165–179. [Google Scholar] [CrossRef]

- Bellovary, J.L.; Giacomino, D.E.; Akers, M.D. A Review of Bankruptcy Prediction Studies: 1930-Present A Review of Bankruptcy Prediction Studies: 1930 to Present. J. Fin. Educ. 2007, 33, 1–43. [Google Scholar]

- Pereira, J.M.; Basto, M.; Da Silva, A.F. The Logistic Lasso and Ridge Regression in Predicting Corporate Failure. Procedia Econ. Financ. 2016, 39, 634–641. [Google Scholar] [CrossRef] [Green Version]

- Sun, J.; Li, H.; Huang, Q.H.; He, K.Y. Predicting financial distress and corporate failure: A review from the state-of-the-art definitions, modeling, sampling, and featuring approaches. Know. Bas. Sys. 2014, 57, 41–56. [Google Scholar] [CrossRef]

- Klepáč, V.; Hampel, D. Predicting financial distress of agriculture companies in EU. Agr. Econ. 2017, 63, 347–355. [Google Scholar]

- Papcunova, V. Evaluation of financial performance of contributory organizations under the jurisdiction of municipalities. Acta Reg. Environ. 2013, 10, 13–18. [Google Scholar] [CrossRef]

- Halásek, D.; Pilný, J.; Tománek, P. Určování Bonity Obcí; VŠB-TUO: Ostrava, Czech Republic, 2002; pp. 1–33. [Google Scholar]

- Provazníková, R. Financování Měst, Obcí a Regionů: Teorie a Praxe; Grada Publishing: Prague, Czech Republic, 2009; pp. 20–40. [Google Scholar]

- Malý, I.; Nemec, J. Možnosti Zvyšování Efektivnosti Veřejného Sektoru v Podmínkách Krize Veřejných Financí; Masaryk University: Brno, Czech Republic, 2011; pp. 1–40. [Google Scholar]

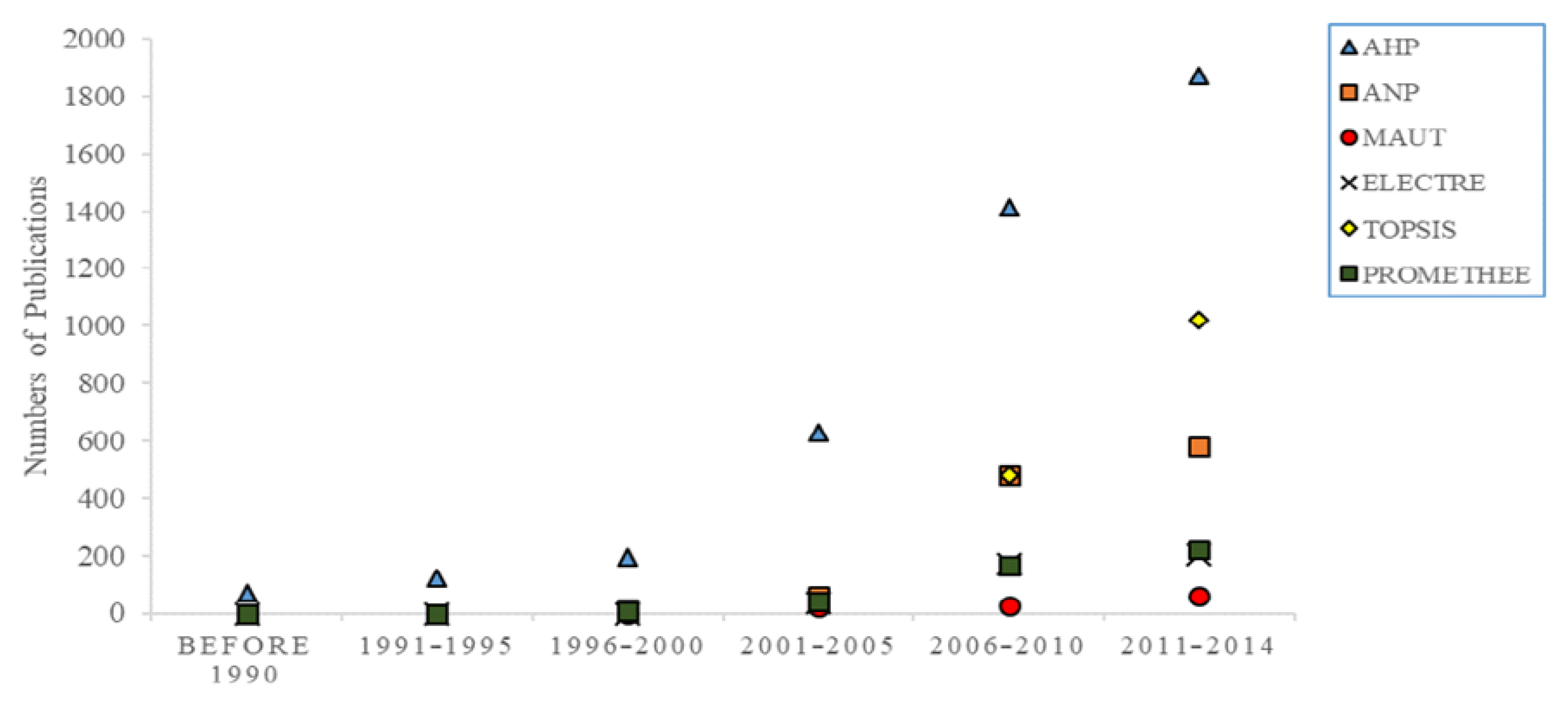

- Zavadskas, E.K.; Turskis, Z.; Kildienė, S. State of Art Surveys of Overviews on Mcdm/Madm Methods. Technol. Econ. Dev. Econ. 2014, 20, 165–179. [Google Scholar] [CrossRef] [Green Version]

- Hwang, C.L.; Yoon, K. Multiple Attributes Decision Making Methods and Applications; Springer: Berlin, Germany, 1981; pp. 1–15. [Google Scholar]

- Yoon, K. Systems Selection by Multiple Attribute Decision Making; Kansas State University: Manhattan, KS, USA, 1980; pp. 1–20. [Google Scholar]

- Tramarico, C.L.; Mizuno, V.; Antonio, V.; Salomon, P.; Augusto, F.; Marin, S. Analytic Hierarchy Process and Supply Chain Management: A Bibliometric Study. Proc. Comp. Scien. 2015, 55, 441–450. [Google Scholar] [CrossRef] [Green Version]

- Olson, D.L. Comparison of weights in TOPSIS models. Math. Comput. Model. 2004, 40, 721–727. [Google Scholar] [CrossRef]

- Streimikiene, D.; Balezentis, T.; Krisciukaitienė, I.; Balezentis, A. Prioritizing sustainable electricity production technologies: MCDM approach. Renew. Sustain. Energy Rev. 2012, 16, 3302–3311. [Google Scholar] [CrossRef]

- Zavadskas, E.K.; Mardani, A.; Turskis, Z.; Jusoh, A.; Nor, K. Development of TOPSIS Method to Solve Complicated Deci-sion-Making Problems: An Overview on Developments from 2000 to 2015. Int. J. Inf. Tech. Dec. Mak. 2016, 15, 1–38. [Google Scholar]

- Keršulienė, V.; Zavadskas, E.K.; Turskis, Z. SELECTION OF RATIONAL DISPUTE RESOLUTION METHOD BY APPLYING NEW STEP-WISE WEIGHT ASSESSMENT RATIO ANALYSIS (SWARA). J. Bus. Econ. Manag. 2010, 11, 243–258. [Google Scholar] [CrossRef]

- Zahedi, S.; Azarnivand, A.; Chitsaz, N. Groundwater quality classiffication derivation using multi-criteria-decision-making techniques. Ecol. Ind. 2017, 78, 243–252. [Google Scholar] [CrossRef]

- Yin, J.; Yang, X.Y.; Zheng, X.M.; Jiao, N.T. Analysis of the investment security of the accommodation industry for countries along the B&R: An empirical study based on panel data. Tour. Econ. 2017, 23, 1437–1450. [Google Scholar]

- Rozentale, L.; Blumberga, D. Methods to Evaluate Electricity Policy from Climate Perspective. Environ. Clim. Technol. 2019, 23, 131–147. [Google Scholar] [CrossRef] [Green Version]

- Zhang, L.; Zhang, L.; Xu, Y.; Zhou, P.; Yeh, C.-H. Evaluating urban land use efficiency with interacting criteria: An empirical study of cities in Jiangsu China. Land Use Policy 2020, 90, 104292. [Google Scholar] [CrossRef]

- Djodjević, B.; Krmac, E. Evaluation of energy-environment efficiency of European transport sectors: Non-radial DEA and TOPSIS approach. Energy 2019, 12, 2907. [Google Scholar]

- Brans, J.-P.; Mareschal, B. The PROMCALC & GAIA decision support system for multicriteria decision aid. Decis. Support Syst. 1994, 12, 297–310. [Google Scholar] [CrossRef]

- Yalcin, E.; Unlu, U. A multi-criteria performance analysis of initial public offering (IPO) firms using critic and vikor methods. Tech. Econ. Dev. Econ. 2018, 24, 534–560. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Municipalities with a Population Interval (from–to) | Coefficient of Gradual Transitions | Multiple of Gradual Transitions |

|---|---|---|

| 0–50 | 1.0000 | 1.0000 × the municipality’s population |

| 51–2000 | 1.0700 | 50 + 1.0700 × number of residents of the municipality’s population exceeding 50 |

| 2001–30,000 | 1.1523 | 2136.5 + 1.1523 × number of residents of the municipality’s population exceeding 2000 |

| 30,000 and more | 1.3663 | 34,400.9 + 1.3663 × number of residents of the municipality’s population exceeding 30,000 |

| Česká Lípa | Jablonec nad Nisou | Most | Tábor |

| České Budějovice | Jihlava | Olomouc | Teplice |

| Děčín | Karlovy Vary | Opava | Trutnov |

| Frýdek-Místek | Karviná | Pardubice | Třebíč |

| Havířov | Kladno | Písek | Třinec |

| Hradec Králové | Kolín | Prostějov | Ústí nad Labem |

| Cheb | Liberec | Přerov | Zlín |

| Chomutov | Mladá Boleslav | Příbram | Znojmo |

| Asset indicators: Value of assets per capita, Value of fixed tangible assets per capita, Value of land per capita, Value of structures per capita |

| Income indicators: Total income per capita, Own income per capita, Tax income per capita, Coefficient of the degree of self-sufficiency, Coefficient of the degree of dependence on non-recurring income, Regularly recurring income from assets, Regularly recurring income from fixed tangible assets, Regular income from structures |

| Expense indicators: Ordinary expenditures per capita, Capital expenses per capita, Total expenses per capita, Investment share coefficient |

| Combined indicators: Coefficient of the degree of coverage of ordinary expenditures, Gross savings, Coefficient of the degree of self-funding of investments, Coefficient of the degree of coverage of capital expenses, Coefficient of the degree of coverage of capital expenses from loans and obligations |

| Informative indicators: Population of the municipality, Total income, Interest, Paid instalments on bonds and positive leverage, Debt service, Debt service indicator, Assets, Liabilities, Balance in bank accounts, Loan and communal bonds, Accepted repayable financial aid and other debts, Indebtedness, Share of indebtedness in liabilities, 8 year balance, Current assets, Short-term liabilities |

| Monitoring indicators: Ratio of liabilities to total assets, Total (current) liquidity |

| Group Description | Combinations | |

|---|---|---|

| A | 1 criterion | A1(I1), A2(I2), A3(I3), A4(I4) |

| B | 2 criteria | B1(I1, I2), B2(I1, I3), B3(I1, I4), B4(I2, I3), B5(I2, I4), B6(I3, I4) |

| C | 3 criteria | C1(I1, I2, I3), C2(I1, I2, I4), C3(I1, I3, I4), C4(I2, I3, I4) |

| D | 4 criteria | D1(I1, I2, I3, I4) |

| Rank | MED (A1) | MED (A2) | MED (A3) | MED (A4) | ||||

|---|---|---|---|---|---|---|---|---|

| 1. | M30 | 28.069 | M30 | 200.795 | M15 | 7.219 | M15 | 1.537 |

| 2. | M26 | 27.036 | M26 | 181.783 | M21 | 8.350 | M28 | 1.792 |

| 3. | M27 | 26.764 | M32 | 169.485 | M20 | 8.632 | M21 | 2.101 |

| 4. | M29 | 25.095 | M18 | 134.463 | M22 | 9.567 | M14 | 2.401 |

| 5. | M32 | 24.892 | M29 | 122.644 | M16 | 9.777 | M25 | 2.552 |

| … | … | … | … | … | … | … | … | … |

| 28. | M22 | 10.884 | M20 | 51.318 | M29 | 22.498 | M4 | 12.851 |

| 29. | M12 | 10.325 | M21 | 48.230 | M32 | 22.823 | M2 | 14.483 |

| 30. | M20 | 8.858 | M15 | 42.303 | M27 | 23.111 | M26 | 14.563 |

| 31. | M21 | 8.722 | M22 | 41.283 | M30 | 25.579 | M30 | 22.761 |

| 32. | M15 | 8.468 | M12 | 34.967 | M26 | 26.131 | M1 | 24.930 |

| Rank | MED (B1) | MED (B2) | MED (B3) | MED (B4) | MED (B5) | MED (B6) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. | M30 | 1.000 | M13 | 0.562 | M28 | 0.850 | M18 | 0.657 | M32 | 0.841 | M15 | 0.975 |

| 2. | M26 | 0.871 | M10 | 0.519 | M29 | 0.838 | M30 | 0.594 | M28 | 0.747 | M21 | 0.953 |

| 3. | M32 | 0.806 | M23 | 0.517 | M32 | 0.831 | M26 | 0.594 | M29 | 0.725 | M16 | 0.896 |

| 4. | M29 | 0.610 | M22 | 0.516 | M25 | 0.704 | M10 | 0.573 | M18 | 0.715 | M14 | 0.896 |

| 5. | M28 | 0.544 | M4 | 0.516 | M6 | 0.699 | M32 | 0.564 | M10 | 0.674 | M12 | 0.894 |

| … | … | … | … | … | … | … | … | … | … | … | … | … |

| 28. | M20 | 0.080 | M7 | 0.491 | M8 | 0.550 | M12 | 0.398 | M27 | 0.456 | M2 | 0.480 |

| 29. | M22 | 0.075 | M2 | 0.488 | M4 | 0.489 | M8 | 0.392 | M30 | 0.434 | M27 | 0.448 |

| 30. | M21 | 0.072 | M32 | 0.487 | M2 | 0.394 | M4 | 0.363 | M2 | 0.415 | M26 | 0.406 |

| 31. | M12 | 0.047 | M31 | 0.487 | M30 | 0.353 | M31 | 0.359 | M4 | 0.414 | M1 | 0.240 |

| 32. | M15 | 0.037 | M6 | 0.475 | M1 | 0.125 | M27 | 0.299 | M1 | 0.214 | M30 | 0.157 |

| Rank | MED (C1) | MED (C2) | MED (C3) | MED (C4) | ||||

|---|---|---|---|---|---|---|---|---|

| 1. | M30 | 0.642 | M32 | 0.826 | M28 | 0.743 | M18 | 0.716 |

| 2. | M26 | 0.630 | M29 | 0.737 | M25 | 0.714 | M28 | 0.691 |

| 3. | M32 | 0.610 | M28 | 0.734 | M14 | 0.710 | M32 | 0.683 |

| 4. | M18 | 0.547 | M26 | 0.640 | M15 | 0.695 | M14 | 0.673 |

| 5. | M10 | 0.533 | M18 | 0.639 | M21 | 0.690 | M10 | 0.667 |

| … | … | … | … | … | … | … | … | … |

| 28. | M8 | 0.378 | M30 | 0.481 | M27 | 0.514 | M2 | 0.455 |

| 29. | M15 | 0.374 | M8 | 0.465 | M26 | 0.503 | M4 | 0.446 |

| 30. | M22 | 0.370 | M4 | 0.408 | M2 | 0.452 | M27 | 0.421 |

| 31. | M4 | 0.358 | M2 | 0.396 | M30 | 0.333 | M30 | 0.407 |

| 32. | M12 | 0.356 | M1 | 0.225 | M1 | 0.247 | M1 | 0.294 |

| Rank | MED (D1) | |

|---|---|---|

| 1. | M32 | 0.695 |

| 2. | M28 | 0.686 |

| 3. | M18 | 0.653 |

| 4. | M29 | 0.652 |

| 5. | M10 | 0.635 |

| … | … | … |

| 28. | M27 | 0.477 |

| 29. | M30 | 0.452 |

| 30. | M4 | 0.438 |

| 31. | M2 | 0.435 |

| 32. | M1 | 0.295 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vavrek, R.; Bečica, J.; Papcunová, V.; Gundová, P.; Mitríková, J. Number of Financial Indicators as a Factor of Multi-Criteria Analysis via the TOPSIS Technique: A Municipal Case Study. Algorithms 2021, 14, 64. https://0-doi-org.brum.beds.ac.uk/10.3390/a14020064

Vavrek R, Bečica J, Papcunová V, Gundová P, Mitríková J. Number of Financial Indicators as a Factor of Multi-Criteria Analysis via the TOPSIS Technique: A Municipal Case Study. Algorithms. 2021; 14(2):64. https://0-doi-org.brum.beds.ac.uk/10.3390/a14020064

Chicago/Turabian StyleVavrek, Roman, Jiří Bečica, Viera Papcunová, Petra Gundová, and Jana Mitríková. 2021. "Number of Financial Indicators as a Factor of Multi-Criteria Analysis via the TOPSIS Technique: A Municipal Case Study" Algorithms 14, no. 2: 64. https://0-doi-org.brum.beds.ac.uk/10.3390/a14020064