From Bitcoin to Central Bank Digital Currencies: Making Sense of the Digital Money Revolution

1

Department of Informatics Engineering, University of Coimbra, CISUC, 3004-531 Coimbra, Portugal

2

Faculty of Economics and INESC Coimbra, University of Coimbra, CeBER, 3004-531 Coimbra, Portugal

3

Faculty of Economics, University of Coimbra, CeBER, 3004-531 Coimbra, Portugal

*

Author to whom correspondence should be addressed.

Future Internet 2021, 13(7), 165; https://0-doi-org.brum.beds.ac.uk/10.3390/fi13070165

Submission received: 4 June 2021

/

Revised: 22 June 2021

/

Accepted: 24 June 2021

/

Published: 27 June 2021

(This article belongs to the Special Issue The Next Blockchain Wave Current Challenges and Future Prospects)

Abstract

:We analyze the path from cryptocurrencies to official Central Bank Digital Currencies (CBDCs), to shed some light on the ultimate dematerialization of money. To that end, we made an extensive search that resulted in a review of more than 100 academic and grey literature references, including official positions from central banks. We present and discuss the characteristics of the different CBDC variants being considered—namely, wholesale, retail, and, for the latter, the account-based, and token-based—as well as ongoing pilots, scenarios of interoperability, and open issues. Our contribution enables decision-makers and society at large to understand the potential advantages and risks of introducing CBDCs, and how these vary according to many technical and economic design choices. The practical implication is that a debate becomes possible about the trade-offs that the stakeholders are willing to accept.

1. Introduction

Money is a tangible or electronic item universally accepted as a medium of payment in immediate or deferred time for goods, assets, and services in a given economy or socio-cultural environment. Money is traditionally defined by its functions, as systematized by Jevons [1]: it serves as a medium of exchange, a unit of account, the standard of deferred payment, and a store of value (“A Medium, a Measure, a Standard, a Store”). As a medium of exchange, money intermediates trades, resolving the inefficiencies of barter systems, such as the need for complementary interests for the trade to take place. As a unit of account, money enables denomination of prices of all goods, assets, and services in the economy, making the price system more transparent and informative. As a standard of deferred payment, money serves to denominate and settle debts. Finally, as a store of value, money serves as a medium of future payment. Some authors argue that the medium of exchange and store of value functions conflict, as the former implies the predisposition for its immediate use, while the latter requires that money be retained for future use (see, for instance, [2]).

The story most recounted about the invention of money goes back to Adam Smith, who conjectured that it was created to facilitate trading because of the division of labor [3]. Previously, there was a barter economy, or mainly a gift economy, as argued by several anthropologists [4]. The evolution of money is not linear, as different types of money have coexisted in time and within economies. However, loosely speaking, we may classify money into four types, in chronological order: Commodity, representative, fiat, and scriptural or electronic money. Commodity money draws its value from the commodity it is made of. In ancient times, several items served as a medium of exchange; some were useful in daily life, such as livestock and grain, while others were merely appealing, such as shells and beads [5]. At some point in history, metals began to be used to produce money due to their durability, divisibility, and homogeneity [6]. Then, coinage enabled the standardization and certification of metal currency. However, it also allowed the sovereign powers (who retained the supply monopoly) to issue coins with an intrinsic value lower than its nominal (facial) value. Representative money, often printed on paper, is a tangible token representing a claim on a commodity (for commodity-backed money) and, as such, it is redeemable in species. The abandonment of the gold standard at the outbreak of World War I resulted in the disuse of representative money. Fiat money is not redeemable and has no intrinsic value. Its worth originates in a government decree, i.e., it has a legal tender. Metal coins and banknotes are fiat money, commonly called cash. Nowadays, most money circulates in electronic form (scriptural money), mainly consisting of electronic records representing current deposits in the banking system. Since fiat money backs those deposits, the public can exchange them for banknotes and metal coins. When providing credit to the economy, the banking system uses its reserves, formed by cash and deposits in the central bank, to support new deposits. In the fractional reserve banking, these new deposits surpass by far the amount of reserves needed to support them, creating a money multiplier effect. For instance, the minimum reserves required by the European Central Bank (ECB) are just 1% of the deposits and, in March 2020, the Federal Reserve Board announced a minimum reserve requirement ratio of 0%. On the one hand, the central bank controls the issuing of electronic money by controlling the monetary base (also called high-powered money), formed by coins and banknotes in the hands of the non-monetary sector and reserves of commercial banks. On the other hand, electronic money is in part endogenous to the economy as it also depends on the demand for credit. Nowadays, electronic money has an even broader definition that includes the activity of non-bank institutions, such as payment service providers. For instance, the European Central Bank [7] (p. 1) defines electronic money (e-money) as “an electronic store of monetary value on a technical device that may be widely used for making payments to entities other than the e-money issuer. The device acts as a prepaid bearer instrument which does not necessarily involve bank accounts in transactions”. For a comprehensive historical overview of the evolution from primitive forms of money to digital, please refer to [8].

The history of money reveals an indisputable pattern: over the centuries, there has been a process of money dematerialization, with the nominal (facial) value of currencies increasingly detached from their intrinsic value. Accordingly, one may say that all money that exists in developed economies is fiat money. In the last 15 years, we have accelerated towards the ultimate dematerialized money economy—a cashless economy. We can identify three technology-driven interacting forces that are disrupting the current global landscape.

First, users claim for faster, easier, more efficient, secure, and universally accessible payment services, which only digitalization can provide [9]. This desire led to an intensified use of debit and credit cards, namely in e-commerce transactions, and catalyzed the use of new technologies to circulate money, such as electronic wallets and contactless payments [10]. In turn, this has fostered the entry of new non-bank players (e.g., PayPal, Apple Pay, Revolut) with a recognized brand and enough scale to gain an advantage over traditional banking institutions and sustain oligopolistic positions in the retail payment system [11]. FinTech startups and mobile network operators are now competing with banks as payment service providers and are gaining remarkable market share.

Second, the digitalization of retail payment systems reinforces its role and creates a substitution effect on other forms of money, namely cash. The reduction in the demand for cash is visible in developed economies and has been particularly acute in some countries, like Sweden, where the amount of cash in circulation halved from 2007 to 2018 [12].

Third, the huge success of cryptocurrencies, and particularly Bitcoin, attracted extensive media coverage and the attention of individuals and, increasingly, institutional investors, sustaining the idea that there is an alternative to fiat money and creating the perception that Blockchain provides the ideal platform on which non-governmental currencies may be issued, managed, and traded. Since the publication of the paper that introduced Bitcoin [13], the cryptocurrency market has expanded at an impressive pace. On 5 May 2021 there were more than 9500 cryptocurrencies traded on more than 370 credible online exchanges, according to the CoinMarketCap site [14], reaching a daily trading volume of more than 213 billion USD. Also on 5 May 2021 cryptocurrencies had a market capitalization of more than 2.2 trillion USD, of which around 45% accounts for the Bitcoin segment, making it the largest unregulated market in the world [15]. However, as noticed by [16], while all cryptocurrencies can theoretically and practically serve as a medium of exchange, only Bitcoin has shown the potential to serve as a store of value, which has been feeding its use as a medium of exchange. With the announcement of Libra, by Facebook, in 2019 [17], concerns of global policy makers have escalated [18]. A currency that would be dominated by a company with a user base of around 2 billion raised several alarms, as reported in The Guardian newspaper (23 June 2019 edition) [18]: the co-chair of the Economic Security Project stated that: “If even modestly successful, Libra would hand over much of the control of monetary policy from central banks to these private companies”. Although the second version of Libra (a single-currency stablecoin arrangement) also poses several monetary, banking, and user risks, [19] defends that its issuance should be allowed in the Euro Area, provided that the regulatory framework of the European Union is duly reinforced and the ECB grants Facebook access to its balance sheet to establish a 100% Central Bank Digital Currency (CBDC)-backed reserve. This would imply “(…) the configuration of Facebook as a Narrow Bank” [19] (p. 11) and would foster the adoption of the digital euro by the ECB. Also according to The Guardian Newspaper (23 June 2019 edition) [18], the Bank for International Settlements (BIS) stated that “(…) while there were potential benefits to be made, the adoption of digital currencies outside the current financial system could reduce competition and create data privacy issues”. However, in January 2020, officials from several central banks and from BIS met to discuss the potential for a central bank digital currency [20].

The above-described forces led countries and monetary authorities to start experimenting with the idea of introducing a new form of digital money—the CBDCs. The broad aim is to leverage the advantages afforded by digital technologies while retaining sovereign control over the stock of money used daily by citizens.

This paper intends to give a broad picture of some core economic and technical aspects of CBDCs. The task at hand is quite demanding due to the novelty and interdisciplinarity of the topic and the prolific and dispersed (mainly “grey”) literature. Consequently, perspective comes at the expense of detail, and hence some issues are only briefly addressed, and further discussion is needed.

Our main claim is that the implementation of CBDCs will shortly spread worldwide, and, although there is no consensus on the model to be adopted, one thing is certain: there is a particular need for careful planning. The success of CBDCs depends on the degree to which they meet the expectations of potential users and minimize the inherent impacts of negative economic dynamics. Our exposition is formulated upon four main questions:

- How does the inception of Bitcoin and other cryptocurrencies contribute to the conceptualization of CBCDs?

- What are the common patterns underlying the central banks’ experiments, proofs-of-concept, and pilots?

- What are the main benefits and risks of introducing CBDCs?

- What issues related to CBCD are still at an early stage of formulation? For instance, how can smart contracts be used to create programmable money? What are the impacts of these features in terms of money usage and monetary policy? What can be done to improve interoperability between CBDCs, without conditioning the monetary policy tools, especially in small economies? What can be done in terms of offline payments? How does replacing a crucial part of the monetary infrastructure affect cybersecurity?

We have performed a snowballing review [21] of English language literature on this topic, encompassing both academic and grey sources (e.g., reports from central banks and regulators). Through extensive forward and backward searches, we have identified more than 100 relevant references that we use to support our work.

We organized the remainder of this paper as follows. In Section 2, we explain the main technological innovations introduced by Bitcoin, the cryptocurrency’s underlying philosophy, and its economic implications. We then introduce a taxonomy of CBDCs and provide a comparison between Bitcoin and traditional central bank money. Moving on to Section 3, we present various central banks’ experiments, proofs-of-concept, and pilots. Section 4 discusses the benefits and risks of introducing CBDCs, just before discussing the next steps in this journey, in Section 5. We close the paper with some conclusions.

2. From Bitcoin to Central Bank Digital Currencies (CBDCs)

When dealing with digital currencies, a key issue is to prevent double-spending, i.e., the risk of someone using the same cash tokens more than once. Unlike physical banknotes and traditional instruments to handle bank deposits, such as checks and debit and credit cards, which are difficult to duplicate, copies of digital artifacts are typically easy to make and indistinguishable from one another, which is a concern for digital cash. Before Bitcoin, the most well-known attempts to create a digital currency were proposed by David Chaum. However, DigiCash [22] and Ecash [23] employed a trusted third party to keep a record of all transactions, thus preventing users from spending more than their true balance. A key feature of Bitcoin is solving the double-spending problem using only technological mechanisms, thus dispensing with the need for trusted third parties and enabling a system where payments can be safely made peer-to-peer and currency issuance is decentralized [13]. To this end, Bitcoin relies on Blockchain, one of various distributed ledger technologies (DLT). Transactions are registered on an append-only database, replicated across a distributed network of peers, who only add new records to the existing ones after agreement using a consensus protocol. The use of timestamps and cryptographic mechanisms render recorded information virtually immutable. Additionally, more recent Blockchains can store and enforce smart contracts, which are pieces of machine-readable code that execute automatically once predetermined conditions are met [24].

The Bitcoin embodies a libertarian philosophy, namely ideas about individual privacy and limited government, as acknowledged by the European Central Bank: “The theoretical roots of Bitcoin can be found in the Austrian school of economics and its criticism of the current fiat money system and interventions undertaken by governments and other agencies (…)” [25] (p. 22). It is close to the concept of ideal money advocated by the right-libertarians, namely Friedrich von Hayek, who argued in favor of ending the monopoly of central banks in producing, distributing, and managing money [26]. The timing of the Bitcoin launch may have fostered its popularity, capitalizing on a widespread distrust of banks, monetary authorities, regulators, and politicians, due to the global financial crisis caused by subprime mortgages that spread to sovereign debt. Table 1 presents a broad comparison between Bitcoin and traditional fiat money.

The algorithm underlying Bitcoin constrains supply to 21 million units by design. It rewards miners who validate new blocks with a fixed number of newly minted units (the “block reward”) and transaction fees. The block reward started at 50 Bitcoin, and it is halved every 210,000 new blocks, which has happened roughly every four years. The most recent halving occurred in May 2020, cutting the block reward to 6.25 units. Transaction fees are a small portion of miners’ rewards, estimated to be on average just 6.5% of the total compensation [27]. However, the importance of transaction fees will increase and arguably constitute the mining activity’s overall reward. According to some, transaction fees will be enough incentive for the mining activity to continue, based on the assumptions that Bitcoin will continue to appreciate and energy costs will substantially decrease as renewable sources gain preponderance in the production mix [27]. Others claim that the reward mechanism for Bitcoin will change with a move from the proof-of-work to proof-of-stake consensus [27]. But many, especially in academia, argue that if the mining rewards come solely from transaction fees, then the Blockchain will become unstable, and the mining activity may cease altogether, precluding new in-chain transactions [28,29]. This scenario raises the question of how much the transaction fees should increase to maintain the profitability of the mining activity. If such costs are non-negligible, it will further reinforce the idea that Bitcoin is more of a market-based speculative asset than a new kind of money.

Not being the liability of anyone means that no one answers for Bitcoin if something goes wrong. Although Bitcoin is accepted as payment by some entities, it does not completely conform to the definition of money. For example, it is not universally accepted in a given economy and there is no absolute liquidity, meaning no guarantee that Bitcoin can be readily exchanged for cash or other goods, assets, and services in the economy. The Bitcoin price dynamics is characterized by short- and long-term hyper volatility, recurrent bubbles, and jumps. This erratic price behavior would force constant repricing of the items on sale (e.g., the labels of all products in supermarket shelves) rendering it impossible to use Bitcoin as a unit of account and an undesirable instrument to denominate and settle debts. Also, the extreme volatility of Bitcoin is inconsistent with a currency acting as a store of value, at least in the short-term [30,31,32]. According to [33] (p. 98) “at most, cryptocurrencies can be viewed as a new kind of tradable speculative asset, which can work as imperfect substitutes for traditional currencies”. Or, in the words of Hazlett and Luther [34] (p. 148), “there is a small corner of the internet where transactions are routinely conducted with Bitcoin serving as the medium of exchange. Over that domain, Bitcoin is money”. Tesla’s recent fumble with the possibility of purchasing a car using Bitcoin demonstrates well the difficulty in its acceptability as a widespread medium of payment. On 8 February 2021, in a filing with the Securities and Exchange Commission [35], Tesla disclosed that it had acquired $1.5 billion of Bitcoin to provide “more flexibility to diversify and maximize returns” and that it would begin accepting Bitcoin as a payment method for the vehicles soon. On 24 March 2021, Elon Musk, the CEO of Tesla, announced on Twitter that this was already in place for its cars in the USA. However, Tesla’s payment and eventual refund terms indicate that buyers would actually buy the cars at their USD value using Bitcoin and refunds would be made in Bitcoin or USD at Tesla’s sole and absolute discretion [36]. On 12 May, again using Twitter, Elon Musk announced that Tesla had “suspended vehicle purchases using Bitcoin” out of concern about “the rapidly increasing use of fossil fuels for Bitcoin mining” [37]. Twenty-four hours after Elon Musk’s message, Bitcoin was down more than 10%, wiping off 290 billion USD of its market capitalization [38].

Bitcoin’s pseudonymity (i.e., the identification of users by an address such as 1BvBMSEYstWetqTFn5Au4m4GFg7xJaNVN2 that bears no link to a natural identity) has been a source of concern for authorities, as it facilitates illegal activities, such as financing terrorism [39], the drug trade [40], or money laundering [41]. In fact, this might be a massive problem, as pointed out by, for instance, Foley and colleagues [42], who estimate that around one-quarter of Bitcoin users and one-half of Bitcoin transactions are associated with illegal activities, involving about 72 billion USD per year.

Nevertheless, the advantages and convenience of Bitcoin have not gone unnoticed, so authorities have been studying the phenomenon and possible adaptations for use in the context of the traditional activities of central banks. The Committee on Payments and Market Infrastructures (CPMI) of the BIS issued a report on digital currencies, with an emphasis on decentralized variants, discussing their impacts on various aspects of financial markets and the wider economy, and possible implications of interest to central banks of such innovations [43]. The main impediment to use Bitcoin as a medium of payment comes from its hyper volatility. Second-generation cryptocurrencies, generally called stablecoins, address this issue by pegging their price to fiat money, exchange-traded assets, or even other cryptocurrencies. The Libra project, announced on 18 June 2019, by a consortium led by Facebook, proposes such a stablecoin. Given the size of the Facebook user-base and the relevance of other founding members of the Libra Association, this new stablecoin promised to become a major player in the worldwide payment system, with a relative loss of importance of traditional national banking systems [44] and might undermine the effectiveness of central bank monetary policy [45,46]. In fact, the risks associated with the Libra project are systemic, surpass its monetary dimension, and may have global repercussions. Abraham and Guégan [47] show that these risks may be (a) financial (for instance, as argued by Groß and colleagues [44], a collective loss of confidence in the Libra might lead to negative dynamics, similar to a “too-big-to fail” bank run), (b) economic (for instance, the creation of a private oligopolistic payment system or taxation difficulties), (c) technological (for instance, cyberattacks, fraud, or even the failure of the Libra protocol), (d) political (Libra may have a large influence on the global financial system), and even (e) ethic and regulatory (for instance, the possibility of Libra having control over a large part of the world population, which raises concerns on privacy and data property issues). The fallout associated with these concerns has hindered the rollout of Libra, leading to delays and a rebrand, with the project and cryptocurrency now called Diem [48]. In fact, a public consultation by the European Central Bank about the digital euro [49] revealed that privacy was the highest-ranking concern among participants (about 43%), but with safeguards to prevent illegal activities. Security and usability also made the top list. Other authors point to security and control of monetary policy as concerns of governments when introducing CBDCs, together with “greater financial inclusion, reducing tax fraud, achieving greater control over money laundering” [50] (p. 1).

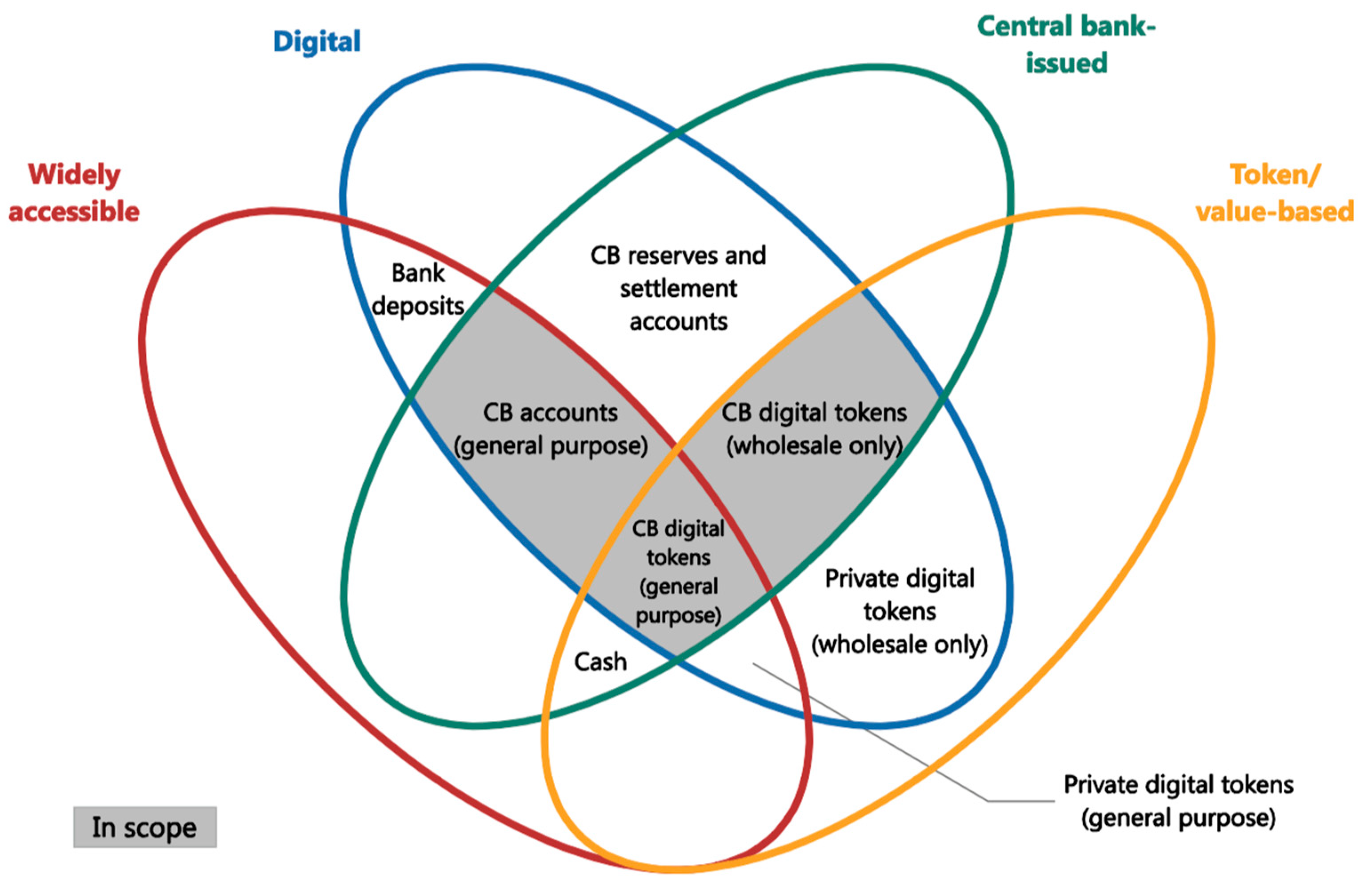

CBDCs are defined as “(…) new variants of central bank money different from physical cash or central bank reserve/settlement accounts” [9] (p. 1). The relationships between the various types of money are made clear by the money flower taxonomy, that is based on four key properties: issuer (central bank or not); form (digital or physical); accessibility (wide or restricted); and technology (token/value-based or account-based)—see Figure 1.

As depicted in the grey area of Figure 1, two main types of CBDC are generally acknowledged: general purpose (aka retail) and wholesale. Basically, the former is accessible to the general public and the latter is “(…) a restricted-access digital token for wholesale settlements (e.g., interbank payments, or securities settlement)” [9] (p. 2). Retail CBDCs can be account-based or token-based. The former is an account held by the public directly at the central bank, akin to the accounts normally held at commercial banks. This is in line with the proposals of the Nobel laureate James Tobin that, as far back as 1980s, argued that people should be able to have deposits in the central bank as a vehicle to store value without being subject to the risk of bank failure [52,53]. The latter is digital cash, the equivalent of physical banknotes, sharing many of the same properties, including the privacy of transactions.

Creating a CBDC requires additional economic, architectural, and technological design considerations. For example, whether there will be limits on the amount one can hold or if it should bear interest [54]; who will be the stakeholders and their roles (e.g., commercial banks, payments processors, FinTechs); what are the acceptable trade-offs between privacy and control of illegal activities; how should interoperability between CBDCs be implemented; what digital technologies can enable the desired characteristics. These and other considerations are being extensively studied by central banks worldwide via discussions, experiments, proofs-of-concept, and pilots. We present, synthesize, and discuss this ongoing research and the results known so far in the next section.

3. Experiments, Proofs-of-Concept, and Pilots

Before 2016, most central banks had not yet proceeded to actual CBDC experiments. For example, the Bank of China, which is nowadays at the forefront of retail CBDC implementation, started seriously exploring the concepts only in 2014 [55]. According to the dataset of [56], updated to April 2021, over 55 countries conducted retail CBDC experiments and, of those, at least 20 created pilots (mainly in the last two years) and three central banks/monetary areas supposedly launched their CDBCs to general availability.

Earlier experiments focused primarily on wholesale CBDCs rather than the retail variant [57,58]. While most of the experiments had a national scope, a few also evolved to support cross-border cooperation, namely Project Stella [59] and Projects Jasper/Ubin (Bank of Canada and Monetary Authority of Singapore). However, retail CBDCs are the ones garnering more interest of late. Of the more advanced generally available CDBCs, the Bahamas Sand Dollar, launched in 2020 [60], is arguably the first generally available retail CDBC. This currency is pegged to the Bahamas Dollar, which in turn is pegged at a 1:1 ratio to the USD. This early interest can illustrate the need for smaller central bank currencies pegged to more significant ones to act proactively in the CBDC domain, otherwise risking replacement by electronic transactions using the stronger currency. According to several [61,62], the only large economy to launch a retail CBDC so far is China, with its e-CNY/DCEP (Digital Currency Electronic Payment). However, although it has been made available in certain areas in early 2021, it is still in pilot, and full adoption is expected only after 2023 [63], even though proofs of concept of increasing breadth have been proceeding, including the proposal of its availability for attendees of Beijing’s 2022 Winter Olympics. Finally, on 31 March 2021, the DCash was launched as a pilot open to the public by the East Caribbean Central Bank [64]. This currency is also indirectly pegged to the USD via the East Caribbean Dollar (although not at a 1:1 ratio). In the latest survey by the BIS, over 85% of banks admitted to exploring the advantages and drawbacks of CDBC [65]. CDBCs involve a very diversified set of actors and initiatives on different stages of maturity, graphically depicted in ([58], p. 3).

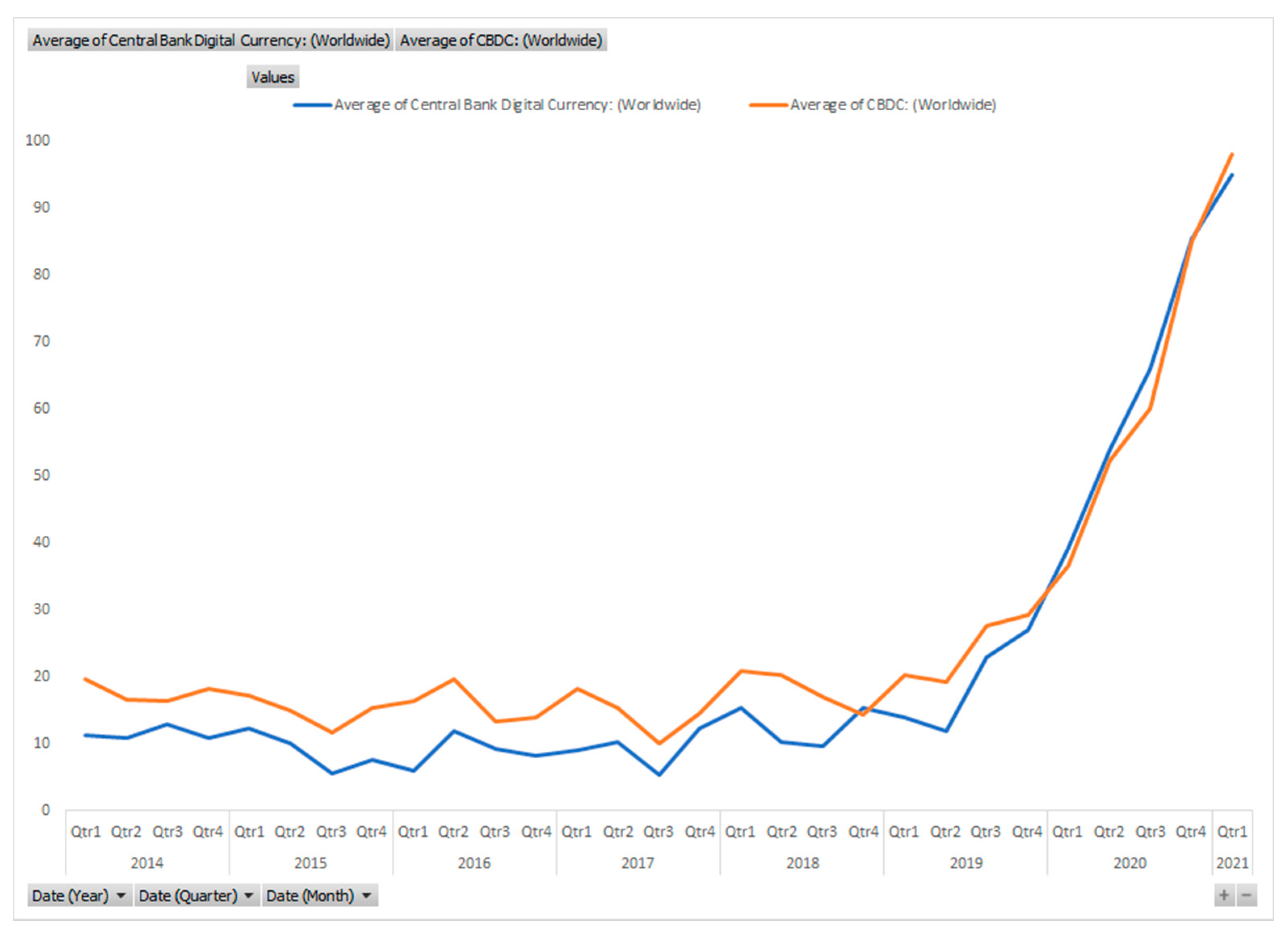

The worldwide interest in CBDCs is also visible in Google Trends search data results for the expression “Central Bank Digital Currency” [66]. A steep increase is noticeable in the most recent years. To reduce seasonality effects, we present the monthly data averaged by quarter in Figure 2.

Although the number of CDBC experiments and pilots may give an idea of homogeneity, this is far from true. Many variations are present in the different approaches, and we can find several independent attempts to create taxonomies [67,68,69] to characterize the approaches followed by the different central banks.

Table 2 shows a set of characteristics that CDBCs may possess. Notice that the experiments and pilots may include CDBCs pursuing just one (the most common case) or several alternative characteristics.

While no full data are available to perform a comprehensive matching of current central bank initiatives with the design goals of Table 2, using the dataset from [56,65], after removing duplicates and projects without information on three or more characteristics, some patterns emerge. From the remaining 20 CDBC projects, most are exploring either indirect (11) or hybrid (14) architectures, with direct claims in only four projects. The numbers do not add to 20 since three experiments do not declare architectures and others explore more than one. Regarding the infrastructure, we have an equal number of experiments exploring DLT and conventional databases (10 each), six looking into both and six without information. An equal number of experiments explore account-based and token-based (11 each) for access technology, with seven exploring both and five not providing information. Finally, the overall majority of experiments is limited to national interlinkages (14), with only five exploring international interoperation and one undefined on this characteristic. Some regularities are also apparent between characteristic choices: no project exploring a simple direct claims architecture has already selected the support infrastructure or a particular access model. This may reflect the lack of experience by the central banks regarding large-scale electronic “customer facing” operations. No particular linkage is found between access models and support infrastructure since all possible combinations exist on the experiment’s data. This is, as we speak (mid-2021), a field of rapid evolution, with several proposals regarding desirable CBDC characteristics having been presented in the past few months alone, including [71,72,73].

4. Benefits and Risks of CBDCs

Besides the customer-facing advantages of digital cash created up by the cryptocurrencies, a widespread adoption of CBDCs carries deeper benefits, but also significant risks. The literature discusses:

4.1. Benefits of CBDCs

More efficient and safer payments and settlement systems. Traditionally, in Europe and most of the Western world, banks have handled retail payment systems. However, recently, innovative FinTechs have challenged this dominance and changed consumer preferences and regulatory intervention [11]. The increasing non-bank competition in the financial domain, with a rising volume of payments undertaken by third-party entities not directly regulated by the central banks, may threaten control and introduce transaction safety risks, since financial oversight now occurs at a different level, if at all. Since consumer preferences for quicker and cheaper payment systems partly drive this change, the introduction of electronic currency by the central banks could provide the adequate infrastructure to support them within the current financial framework. However, while “the introduction of a general purpose or a wholesale only CBDC could bring a number of potential benefits to payment, clearing and settlement systems, (…) it could also pose several risks and challenges” [43] (p. 7) since it can undermine the position of current payment actors and provide perverse incentives. A potential upside is the increased resilience of the overall payment landscape that a complementary and distinct central bank-managed infrastructure supporting core payment services could offer [54].

Better visibility and transparency of monetary policy. The introduction of CDBCs may afford central banks better knowledge of the transactions occurring in real-time, allowing for more effective monitoring of critical financial data, additionally “it provides a landmark opportunity to enhance the transparency of the central bank’s monetary policy framework, including its nominal anchor, its tools and operations, and its policy strategy” [74] (p. 15). However, [43] (p. 9) cautions that current payment systems already ensure that “a CBDC may allow for better real-time data on economic activity but such gains are already largely achievable with existing payments data. A more persuasive argument is that a CBDC may help to maintain a direct link between central banks and citizens (especially where cash use is diminishing), which could help foster the public’s understanding of central banks’ roles and need for independence” [75].

Additional monetary policy tools. CBCDs may be designed to incorporate additional features, aiming at changing the short-term demand for the CBCD of individuals and firms, and, as such, can be used countercyclically to condition or promote consumption and investment. For example, time-limited money can have a due date for spending, after which it returns to the issuer. The Bank of China piloted this concept with DCEP “red envelopes” in 2021 [76]. Digital money can also have a built-in interest rate, which can be positive or negative [43] and equal or different from a current policy rate. Most notably, account-based interest-bearing CBDC relieves the zero lower bound constraint on monetary policy and increases the effectiveness of monetary policy in severe recessionary and deflationary periods [9,12,74,77].

Harder for black economy, money laundering, and tax evasion. According to the United Nations [78], “The estimated amount of money laundered globally in one year is 2–5% of global GDP, or $800 billion–$2 trillion in current US dollars”. Many illegal activities tend to rely on the anonymity of physical cash. According to the BIS [43] (p. 9), “given that a CBDC can allow for digital records and traces, it could improve the application of rules aimed at anti-money laundering and countering the financing of terrorism (AML/CFT), and possibly help reduce informal economic activities”. Even if token-based CBDCs are implemented together with the account-based variant to enable a degree of privacy to the public, the amounts transferable to the wallets may be restricted, effectively inhibiting the use for large-scale criminal activities. However, the BIS also cautions that the impact on fighting illegal activities may not be significant, since a traceable CBDC “would not necessarily be the main conduit for illicit transactions and informal economic activities” [43] (p. 9), and with the most likely CDBC architecture proposals, the “game of cats and mice” between regulatory agencies and money launderers is likely to continue with little change [79].

More inclusion of the unbanked or underbanked. Financial inclusion is one of the important motivations for the introduction of CBCDs mentioned by central banks [80]. According to the Bank of England [54] (p. 19), “the provision of basic accounts and an electronic payment system by the central bank could make a significant difference to financial inclusion”. The institution considers this relevant in “developing countries where the banking and payments system are underdeveloped”. However, the problem may be significant even in advanced economies, especially for the individuals most in need in times of crisis. In May 2020, 14 million American adults did not have a bank account and were waiting weeks or months to receive their coronavirus disease 2019 (COVD-19) stimulus checks. Additionally, they tend to lose between 1% and 10% of the check’s value to the cashers [81]. The use of CBDC digital wallets would enable higher efficiency and justice in the allocation of relief funds. However, the BIS also cautions that “for some segments of the population, barriers to the use of any digital currency may be large” [43] (p. 9). An example discussing CBDC acceptance in a region of Spain, exploring various sociodemographic variables, is presented in [82].

Positive overall macroeconomic impact. The wide adoption of a CBDC will reduce the costs of running the payment system (namely by reducing the frictions and costs associated with the storage, transport, and management of cash), increase its resilience to operational risks (cyberattacks, operational failures, and hardware faults), reduce tax evasion, corruption, and illicit activities, increase financial stability, reduce the costs of private monopolistic control, especially in the situation of a structural decrease in cash usage, and increase financial inclusion, especially in underbanked economies [83,84]. Additionally, it will reduce the regulatory costs of the banking sector by removing the need for a fractional reserve system [85], imposing a better discipline on commercial banks [86], reducing the vulnerability of banks, and reducing the political and economic incentives for governments to bail out the “too big to fail” institutions [87]. All in all, the benefits of the introduction of a CBDC in the payment system may spill over to the overall economy with a significant impact on the GDP, depending on the adoption rate of the CBDC by the general public.

4.2. Risks of CBDCs

Regarding risks stemming from the introduction of CBDCs, the literature mentions:

Risks to the business models of commercial banks. If central banks begin to compete with the private banking sector for deposits, offering to retail depositors a default risk-free venue alternative to bank deposits, then significant deposit balances could shift to the central banks from the commercial bank accounts, which would have implications for the balance sheets of the latter institutions and, thus, the amount of credit they could provide to the economy [54]. This disintermediation would also affect the ability of commercial banks to “perform essential economic functions, such as monitoring borrowers” [51] (p. 63). Furthermore, “commercial banks could lose a valuable interface with their consumers given that in some CBDC designs the “know-your-customer” function could fall to the central bank” [43] (p. 9). Some warn of far-reaching consequences: “divorcing payments from private bank deposits and even putting an end to banks’ ability to create money“ [88] (p. 1).

Increase of the systemic risk of the private banking sector. If central banks begin to compete directly with the private banking sector, then due to their superiority in terms of default risk, there will be an increase in the liquidity risk of commercial banks, which in turn may increase the probability of severe financial instability episodes. A negative confidence shock on a particular commercial bank may lead its clients to convert the bank deposits into a form of CBDC and potentiate a bank run. A bank run may undermine the overall confidence on the private banking sector and increase the rate of substitution of commercial bank deposits for CBDC, and the pace and intensity of the contagion effect [51,77,88]. Due to its grave impact, works such as [89] have studied the likelihood of bank runs as a function of the system characteristics and of the concrete features of the CBDC.

Privacy risks. Current payment methods provide varying levels of privacy, from the almost complete anonymity of physical cash transactions to full traceability and documentary verification and monitoring in regulated bank accounts [68]. The design of a CBDC should provide/allow an adequate balance between public interests (usually best protected by unlimited access to information) and individual rights, which include privacy. To provide the required privacy characteristics, the design of the digital coins must concern itself with supporting the desired mix of functionalities, embracing “privacy by design” [90] since user privacy is seldom an emerging property of information handling systems. Furthermore, current regulations, particularly regarding anti-money laundering, prevent fully anonymous electronic payments [68] even though, in practice, the international reach of CBDCs implies interoperability between sovereign regulatory frameworks, raising challenges in ensuring transnational regulatory validity [58]. The required balance is achievable by segregating specific applications to specific kinds of account that impose limits on characteristics such as amounts, functionalities, or anticipated use. However, even for the most limited accounts, some minimal level of user identification may be required for account creation.

A few general approaches have been explored to allow for different levels of privacy in CBDC usage:

- The European Central Bank [91] made a proof-of-concept using time-limited “anonymity vouchers” that afford their owners the possibility of performing restricted value transactions with details not relayed to the monetary authorities. These vouchers are issued freely, but at a defined rate. Since a user is free to use or not each voucher, this limits the information regarding actual usage that the monetary authority can store.

- Project Stella [59] explored the concept of privacy-enhanced transactions (PETs) using three mechanisms, based on different technological support, to assure privacy: (a) segregating PETs, where information is segregated between participants and shared only on a “need to know” basis. Instead of a “common ledger,” there are separated “ledger subsets,” which means that parties will not have access to the full set of transactions, but only to those that include them; (b) hiding PETs, where, while there is a common ledger, various cryptographic techniques protect the stored information to prevent access from unauthorized parties; and (c) unlinking PETs, where the information present in the ledger is unlinked from the actual actors or actual transactions. Therefore, unauthorized third parties of a transaction can observe the transaction information and the amount but cannot determine the transacting relationships (i.e., that an Entity A transacted with an Entity B).

The various benefits and risks discussed above are not definitive. Their materialization depends on the design of CBDCs from both economic and technological perspectives and on its adoption rate by the economy.

5. The Road Ahead

Although cryptocurrencies supported by Blockchain heavily influenced the momentum for CBDCs, this technology will not necessarily underlie central bank-issued currencies. Decentralization and cryptographic mechanisms are used in Blockchain to remove the need for trusted third parties, but this is not a concern or desire of central banks. Even if they opt for decentralization for resilience, the central banks will always retain control of the CBDC network [54]. Additionally, Blockchains still suffer from scalability issues, which may be a problem for very high transaction rates. Some CBDC pilots have passed up DLTs in favor of other alternatives [9]. Others, such as the Bank of England, are keeping their options open [54]. It is worth noting that, even if central banks decide to use Blockchain technology, the negative externality of high energy consumption will not exist. The Bitcoin network uses a computationally heavy, and, thus, power-hungry, consensus algorithm to ensure the honesty of anonymous and potentially malicious peers. Conversely, in the case of CBDCs, the central banks will retain control of the network [54], hence enabling the use of much lighter and power-efficient consensus algorithms already in use in private Blockchains today. Auer and Boehme [92] extensively discuss why cryptocurrencies should not be the model for implementing CBDCs. They highlight the importance of intermediaries in the financial system, centralized control, and the usability of end-user devices, namely for those less technically adept, that may face difficulties in managing complex private encryption keys. Nevertheless, some characteristics of more modern Blockchains—such as smart contracts—may still be appealing in a CBDC scenario.

Smart contracts enable the creation of programmable money. Not to be confused with existing mechanisms to automate payments, such as open banking application programming interfaces (APIs), of which the European Union’s second Payment Services Directive (PSD2) is an example [93]. Programmable money is about embedding behavior in the money itself; for example, executing payments upon confirmation of the receipt of goods or routing tax payments directly to authorities at the point of sale [54]. Programmable money can be “designed to flow as easily as email without sacrificing regulatory controls, monetary policy or personal privacy” [94] (p. 7). It can automatically gain or lose value over time to implement interest [95], travel only to the intended destinations [96], or be valid only for specific acquisitions, such as food [95]. This ability could enforce rules, like those attached to the relief grants that some governments experimented with during COVID-19, meant to be spent in certain ways [96]. These embedded features reduce the fungibility of money but with a purpose, for example, to mitigate misuse. Programmable money may also “be effective monetary policy instruments to add liquidity quickly to the financial markets” [97] (p. 2), and several of its possible mechanisms are valuable to mitigate corruption.

The electronic nature of CDBC can also improve cross-border payments, which are frequently costly and inefficient. This goal can be achieved by interoperating central bank digital currencies (CBDCs), forming multi-CBDC (mCBDC) arrangements [98]. While no currently active CDBC pilots address interoperability explicitly, some banks have announced the intention to evolve towards mechanisms for cross-border payments [99]. Auer and colleagues [98] claim that compatible standards (e.g., similar regulatory frameworks, market practices, messaging formats, and data requirements) can help achieve these goals, as can interlinking systems via technical interfaces, common clearing mechanisms or related schemes, or even establishing a single multi-currency payment system. At this point, it is not yet clear which alternative will emerge as preferred. Nevertheless, while technical barriers are surmountable, the full convertibility enabled by interoperability must be balanced with Fleming–Mundell’s monetary policy trilemma [100], which states the practical impossibility to simultaneously stabilize the exchange rate, enjoy free international capital mobility, and engage in a monetary policy oriented toward domestic goals.

To ensure widespread adoption of CBDCs as a replacement for physical cash, offline payments must also be possible. Research on this topic is ongoing, namely by VISA, which proposes an approach for point-to-point payments between two devices [101]. It enables downloading money to a personal device (e.g., a smartphone) that stores it on secure hardware where a wallet provider manages it (e.g., a bank). Direct transactions between two devices can rely on Bluetooth or near field communication (NFC) [101,102]. At the moment, the creation of dedicated hardware devices to support CDBC usage also appears to be advancing quickly [103].

As the CBDC story unfolds, other relevant players, such as PayPal and VISA, press on with cryptocurrency-based offers. The former recently made Bitcoin payments available to its U.S. customers, rendering them as simple as using a credit or debit card associated with their wallet [104]. The latter processed its first transaction on Ethereum, using the USDC stablecoin rather than fiat money [105]. Both initiatives will further advance the mainstream adoption of cryptocurrencies by removing the spending barrier and instilling household names’ confidence. Time is ticking for central banks to provide a relevant alternative.

6. Conclusions

At the moment, Central Bank Digital Currencies are one of the hottest issues under debate, involving not only academics from different fields of knowledge, such as economics, finance, computer science, data analysts, and law but also regulators, monetary authorities and practitioners from all over the world. The recognized merits of Blockchain as a disruptive technology and the success of Bitcoin and other cryptocurrencies paved the way for central banks to rethink new venues for the issuance and management of fiat money. For many, Bitcoin and other cryptocurrencies do not, by themselves, threaten the pivotal role of central banks in existing payment systems, as they are conceptualized as more a market-based speculative asset than a new kind of money, or due to the narrowness of its influence. However, other structural changes are taking place, such as the significant reduction in the demand for cash happening in some countries and, most notably, the increasing importance of new players. FinTech startups and mobile network operators that compete with commercial banks as payment service providers have raised the “red flag” on the urgency of bringing into the system the technological innovations increasingly tagged as disruptive or revolutionary.

At first glance, the advent of CBDCs means the complete digitalization of money and, as such, the ultimate step in the secular dematerialization of money. As in most economic innovations, the movement towards a cashless economy is the response of authorities to the demands of society. Unquestionably, the demand for digitalization has been increasing at a steady pace, “not only in the many aspects of the daily life of families but also in the way firms conduct their businesses and states govern national affairs” and gained a more profound dimension in recent years due to the Covid-19 pandemic crisis [15]. Hence the launch of CBDC will directly fulfil the need for digitalization, while tightening the relationship between citizens and central banks.

However, one should note that a CBDC is not a Bitcoin-like or a stablecoin-like cryptocurrency governed by a central bank, nor the simple digitalization of cash. On the one hand, CBDCs may implement completely different currency concepts that share little more than their immateriality and the acronym; on the other hand, the implementation of CBDCs will have economic implications that surpass, by far, the changes in individual behavior produced by the digitalization of payment instruments. Bech and Garratt [51] proposed the most used and up-to-date systematization of the contemporaneous coexisting types of money, which became known as the “money flower”. Besides the restricted-access digital token for wholesale settlements, CBDC refers to general-purpose money, in the form of an account held by the public directly at the central bank, akin to the accounts commonly held at commercial banks (account-based) and digital cash, the equivalent of physical banknotes, sharing many of the same properties, including the privacy of transactions (token/value-based).

Although central bank experiments with CBDCs before 2016 were almost non-existent, with the remarkable exception of the Bank of China, and early experiments focused mainly on wholesale CBDCs, according to the latest survey by the BIS, dated January 2021, over 85% of banks admitted to exploring the advantages and drawbacks of CDBC [65]. Besides being at different development stages, these experiments are far from being homogeneous and present significant differences in terms of application area, architecture (operating and access models), access technology, central bank infrastructure, interlinkages, authority (which maps partially with infrastructure and access technology), availability and access limitations and restrictions.

Independent of the model used, the economic literature has highlighted several benefits and risks associated with the adoption of CBDCs. This new type of central bank money may render the payment and settlement systems more efficient and safer, provide better visibility and transparency over monetary policy, create additional monetary policy tools, discourage the black economy, money laundering, and tax evasion, and contribute to the inclusion of the unbanked or underbanked. All these benefits will ultimately have an overall positive macroeconomic impact. Conversely, CBDCs pose new risks to the business models of commercial banks, may increase the systemic risk of the private banking sector, and may jeopardize individual rights, most notably, privacy (on the concerns of privacy violations by the Bank of China, see [106]). Although most studies argue that the benefits outweigh the risks, they also suggest that the balance depends on how and at what pace CBDCs replace cash [107]. The view most subscribed to is that the central bank should issue a CBDC that meets the expectations (for instance, potential users of the digital euro seem to value privacy, security, and broad usability [108]), and exempt itself from pursuing further actions to accelerate cash replacement. As such, cash and CBDC should coexist to the extent desired by the effective and potential users [77].

We have presented the challenges and choices ahead in the coming worldwide diffusion of CBDCs and revised the currently proposed approaches to their introduction. We have shown that, while Bitcoin and current cryptocurrencies may have provided a driver to their adoption, the technology, goals, and challenges associated with CBDCs are quite diverse from that starting point, and further divergence is expected. We have also shown that, at this moment, no “one size fits all” approach is seen as acceptable for all CBDC applications, and quite a few options are being actively explored, sometimes in parallel, by the central banks.

Author Contributions

Introduction, H.S.; From Bitcoin to Central Bank Digital Currencies, P.R.C.; Experiments, proofs-of-concept, and pilots, P.M.; Benefits and risks of CBDCs, P.R.C., P.M., H.S.; The road ahead; P.R.C., P.M.; Conclusions: H.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research was partially funded by (a) national funds through the FCT—Foundation for Science and Technology, I.P., within the scope of the project CISUC—UID/CEC/00326/2020 and by European Social Fund, through the Regional Operational Program Centro 2020, Portugal; and (b) ERDF Funds through the Centre’s Regional Operational Program and by National Funds through the FCT—Fundação para a Ciência e a Tecnologia, I.P. under the project CENTRO-01-0145-FEDER-029312, and also by FCT Grants UIDB/00308/2020 (INESC Coimbra), and UIDB/05037/2020 (CeBER).

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Jevons, W.S. Money and the Mechanism of Exchange; D. Appleton: New York, NY, USA, 1876; Available online: https://books.google.pt/books?id=D3QqAAAAYAAJ&printsec=frontcover&source=gbs_ge_summary_r&cad=0#v=onepage&q&f=false (accessed on 25 June 2021).

- Sawyer, M. Money: Means of Payment or Store of Wealth? In Modern Theories of Money: The Nature and Role of Money in Capitalist Economies; Rochon, L.-P., Rossi, S., Eds.; Edward Elgar Publishing: Cheltenham, UK, 2003; pp. 3–17. [Google Scholar]

- Smith, A. Of the origin and use of money. In General Equilibrium Models of Monetary Economies; Starr, R.M., Ed.; Academic Press: Cambridge, MA, USA, 1989; pp. 47–53. [Google Scholar] [CrossRef]

- Humphrey, C. Barter and Economic Disintegration. Man 1985, 20, 48–72. [Google Scholar] [CrossRef]

- Hoang, P.; Ducie, M. Cambridge IGCSE and O Level Economics, 2nd ed.; Hachette: London, UK, 2018; Available online: https://books.google.pt/books?id=gRdSDwAAQBAJ (accessed on 25 June 2021).

- Menger, K. On the Origin of Money. Econ. J. 1892, 2, 239–255. [Google Scholar] [CrossRef]

- European Central Bank. Electronic Money. European Central Bank. 16 November 2016. Available online: https://www.ecb.europa.eu/stats/money_credit_banking/electronic_money/html/index.en.html (accessed on 15 May 2021).

- Ammous, S. The Bitcoin Standard: The Decentralized Alternative to Central Banking; John Wiley & Sons: Hoboken, NJ, USA, 2018. [Google Scholar]

- Barontini, C.; Holden, H. Proceeding with caution—A Survey on Central Bank Digital Currency. Bank of International Settlements, 101. January 2019. Available online: https://www.bis.org/publ/bppdf/bispap101.htm (accessed on 25 June 2021).

- Omarini, A.E. Fintech and the Future of the Payment Landscape: The Mobile Wallet Ecosystem—A Challenge for Retail Banks? Int. J. Financ. Res. 2018, 9, 97. [Google Scholar] [CrossRef]

- Ley, S.; Foottit, I.; Honig, H.; King, D.; Doyle, M.; Turan, C.; Sonnad, V. Payments Disrupted. The Emerging Challenge for European Retail Banks. Deloitte. 2015. Available online: https://www2.deloitte.com/content/dam/Deloitte/uk/Documents/financial-services/deloitte-uk-payments-disrupted-2015.pdf (accessed on 15 May 2021).

- Riksbank, S. Payments in Sweden 2019. Sveriges Riksbank. November 2019. Available online: https://www.riksbank.se/en-gb/payments--cash/payments-in-sweden/payments-in-sweden-2019/ (accessed on 25 June 2021).

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. 31 October 2008. Available online: https://nakamotoinstitute.org/bitcoin/ (accessed on 15 May 2021).

- CoinMarketCap: Cryptocurrency Prices, Charts and Market Capitalizations. CoinMarketCap. 5 May 2021. Available online: https://coinmarketcap.com/ (accessed on 15 May 2021).

- Sebastião, H.M.C.V.; da Cunha, P.J.O.R.; Godinho, P.M.C. Cryptocurrencies and blockchain. Overview and future perspectives. Int. J. Econ. Bus. Res 2021, 21, 305–342. [Google Scholar] [CrossRef]

- Ammous, S. Can cryptocurrencies fulfil the functions of money? Q. Rev. Econ. Financ. 2018, 70, 38–51. [Google Scholar] [CrossRef]

- Constine, J. Facebook Announces Libra Cryptocurrency: All You Need to Know. TechCrunch. 18 June 2019. Available online: https://social.techcrunch.com/2019/06/18/facebook-libra/ (accessed on 15 May 2021).

- Inman, P.; Monaghan, A. Facebook’s LIBRA Cryptocurrency Poses Risks to Global Banking. The Guardian. 23 June 2019. Available online: http://www.theguardian.com/technology/2019/jun/23/facebook-libra-cryptocurrency-poses-risks-to-global-banking (accessed on 15 May 2021).

- Tercero-Lucas, D. A Global Digital Currency to Rule Them All? A Monetary-Financial View of the Facebook’s LIBRA for the Euro Area; Univeristat Autònoma de Barcelona: Barcelona, Spain, June 2020; Available online: https://ddd.uab.cat/record/232413 (accessed on 15 June 2021).

- Inman, P. Bank of England to Consider Adopting Cryptocurrency. The Guardian. 21 January 2020. Available online: http://www.theguardian.com/technology/2020/jan/21/bank-of-england-to-consider-adopting-cryptocurrency (accessed on 15 May 2021).

- Wohlin, C. Guidelines for snowballing in systematic literature studies and a replication in software engineering. In Proceedings of the 18th International Conference on Evaluation and Assessment in Software Engineering, New York, NY, USA, 13 May 2014; pp. 1–10. [Google Scholar] [CrossRef]

- Chaum, D. Blind Signatures for Untraceable Payments. In Advances in Cryptology; Springer: Boston, MA, USA, 1983; pp. 199–203. [Google Scholar] [CrossRef]

- Schoenmakers, B. Basic security of the ecash payment system. In State of the Art in Applied Cryptography, Course on Computer Security and Industrial Cryptography; Preneel, B., Rijmen, V., Eds.; Springer: Leuven, Belgium, 1997; pp. 342–356. Available online: http://www.win.tue.nl/~berry/papers/cosic.pdf?q=ecash (accessed on 25 June 2021).

- Swan, M. Blockchain: Blueprint for a New Economy, 1st ed.; O’Reilly Media Inc.: Sebastopol, CA, USA, 2015. [Google Scholar]

- European Central Bank. Virtual Currency Schemes; European Central Bank: Frankfurt am Main, Germany, 2012. [Google Scholar]

- Hayek, F.A. Denationalisation of Money: The Argument Refined, 3rd ed.; Institute of Economic Affairs; 1990; Available online: https://mises.org/library/denationalisation-money-argument-refined (accessed on 10 May 2021).

- Phillips, D.; Chipolina, S. What Will Happen to Bitcoin After All 21 Million Are Mined? Decrypt. 20 April 2021. Available online: https://decrypt.co/33124/what-will-happen-to-bitcoin-after-all-21-million-are-mined (accessed on 15 May 2021).

- Carlsten, M.; Kalodner, H.; Weinberg, S.M.; Narayanan, A. On the Instability of Bitcoin Without the Block Reward. In Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security, Vienna, Austria, 24 October 2016; pp. 154–167. [Google Scholar] [CrossRef]

- Easley, D.; O’Hara, M.; Basu, S. From mining to markets: The evolution of bitcoin transaction fees. J. Financ. Econ. 2019, 134, 91–109. [Google Scholar] [CrossRef]

- Ali, R.; Barrdear, J.; Clews, R.; Southgate, J. The Economics of Digital Currencies. Bank of England. 2014 Q3. September 2014. Available online: https://papers.ssrn.com/abstract=2499418 (accessed on 15 May 2021).

- Baur, D.G.; Dimpfl, T. The volatility of Bitcoin and its role as a medium of exchange and a store of value. Empir. Econ. 2021. [Google Scholar] [CrossRef] [PubMed]

- Yermack, D. Is Bitcoin a Real Currency? An Economic Appraisal. In Handbook of Digital Currency; Chuen, D.L.K., Ed.; Academic Press: San Diego, CA, USA, 2015; pp. 31–43. [Google Scholar] [CrossRef]

- Bação, P.; Duarte, A.P.; Sebastião, H.; Redzepagic, S. Information Transmission between Cryptocurrencies: Does Bitcoin Rule the Cryptocurrency World? Sci. Ann. Econ. Bus. 2018, 65, 97–117. [Google Scholar] [CrossRef]

- Hazlett, P.K.; Luther, W.J. Is bitcoin money? And what that means. Q. Rev. Econ. Financ. 2020, 77, 144–149. [Google Scholar] [CrossRef]

- Tesla, Inc. Annual Report on form 10-K for the Year Ended 31 December 2020. United States—Securities and Exchange Commission; 8 February 2021. Available online: https://www.sec.gov/ix?doc=/Archives/edgar/data/1318605/000156459021004599/tsla-10k_20201231.htm (accessed on 15 May 2021).

- Lambert, F. Tesla Explains How Dumb It Is to Buy a Car with Bitcoin in Its Own Disclosure. Electrek. 24 March 2021. Available online: https://electrek.co/2021/03/24/tesla-dumb-buy-car-with-bitcoin/ (accessed on 15 May 2021).

- Kolodny, L. Elon Musk Says Tesla Will Stop Accepting Bitcoin for Car Purchases, Citing Environmental Concerns. CNBC. 12 May 2021. Available online: https://www.cnbc.com/2021/05/12/elon-musk-says-tesla-will-stop-accepting-bitcoin-for-car-purchases.html (accessed on 15 May 2021).

- Kharpal, A. As Much as $365 Billion Wiped off Cryptocurrency Market after Tesla Stops Car Purchases with Bitcoin; NBC News: London, UK, 13 May 2021; Available online: https://www.nbcnews.com/tech/tech-news/365-billion-wiped-cryptocurrency-market-musks-tweet-rcna922 (accessed on 15 May 2021).

- Dion-Schwarz, C.; Manheim, D.; Johnston, P. Terrorist Use of Cryptocurrencies: Technical and Organizational Barriers and Future Threats; RAND Corporation: Santa Monica, CA, USA, 2019. [Google Scholar] [CrossRef]

- Hurlburt, G.F.; Bojanova, I. Bitcoin: Benefit or Curse? IT Prof. 2014, 16, 10–15. [Google Scholar] [CrossRef]

- Bryans, D. Bitcoin and Money Laundering: Mining for an Effective Solution. Indiana Law J. 2014, 89, 13. [Google Scholar]

- Foley, S.; Karlsen, J.R.; Putniņš, T.J. Sex, Drugs, and Bitcoin: How Much Illegal Activity Is Financed through Cryptocurrencies? Rev. Financ. Stud. 2019, 32, 1798–1853. [Google Scholar] [CrossRef]

- CPMI-MC. Central Bank Digital Currencies. Bank of International Settlements, 174. March 2018. Available online: https://www.bis.org/cpmi/publ/d174.htm (accessed on 10 May 2021).

- Groß, J.; Herz, B.; Schiller, J. Libra—Concept and Policy Implications. Wirtschaftswissenschaftliche Diskussionspapiere, Working Paper 02–19. 2019. Available online: https://www.econstor.eu/handle/10419/205241 (accessed on 15 May 2021).

- Brühl, V. Libra—A Differentiated View on Facebook’s Virtual Currency Project. Intereconomics 2020, 55, 54–61. [Google Scholar] [CrossRef] [Green Version]

- Schmeling, M. What is Libra? Understanding Facebook’s Currency. Goethe University Frankfurt, SAFE—Sustainable Architecture for Finance in Europe, Research Report 76. 2019. Available online: https://www.econstor.eu/handle/10419/204501 (accessed on 15 May 2021).

- Abraham, L.; Guégan, D. The other side of the Coin: Risks of the Libra Blockchain. arXiv 2020, arXiv:191007775. [Google Scholar] [CrossRef] [Green Version]

- Bursztynsky, J. Facebook-backed Libra Association Has Been Renamed DIEM. CNBC. 1 December 2020. Available online: https://www.cnbc.com/2020/12/01/facebook-backed-libra-digital-currency-has-been-renamed-diem.html (accessed on 15 May 2021).

- Panetta, F. 21st century cash: Central banking, technological innovation and digital currencies. In Do We Need Central Bank Digital Currency? Economics, Technology and Institutions; Milan, Italy, June 2018; pp. 28–31. Available online: https://www.suerf.org/studies/7025/do-we-need-central-bank-digital-currency-economics-technology-and-institutions (accessed on 17 June 2021).

- Alonso, S.L.N.; Fernández, M.Á.E.; Bas, D.S.; Kaczmarek, J. Reasons Fostering or Discouraging the Implementation of Central Bank-Backed Digital Currency: A Review. Economies 2020, 8, 41. [Google Scholar] [CrossRef]

- Bech, M.L.; Garratt, R. Central Bank Cryptocurrencies; Bank of International Settlements: Rochester, NY, USA, September 2017; Available online: https://papers.ssrn.com/abstract=3041906 (accessed on 15 May 2021).

- Tobin, J. Financial Innovation and Deregulation in Perspective. Bank Jpn. Monet. Econ. Stud. 1985, 3, 19–29. [Google Scholar]

- Tobin, J. A Case for Preserving Regulatory Distinctions. Challenge 1987, 30, 10–17. [Google Scholar] [CrossRef] [Green Version]

- Bank of England. Central Bank Digital Currency: Opportunities, Challenges and Design. Bank of England, Discussion Paper. March 2020. Available online: https://0-www-bankofengland-co-uk.brum.beds.ac.uk/-/media/boe/files/paper/2020/central-bank-digital-currency-opportunities-challenges-and-design.pdf?la=en&hash=DFAD18646A77C00772AF1C5B18E63E71F68E4593 (accessed on 25 June 2021).

- Alun, J. Explainer: How Does China’s Digital Yuan Work? Reuters. 19 October 2020. Available online: https://www.reuters.com/article/us-china-currency-digital-explainer-idUSKBN27411T (accessed on 28 April 2021).

- Auer, R.; Cornelli, G.; Frost, J. Rise of the Central Bank Digital Currencies: Drivers, Approaches and Technologies. Bank of International Settlements, 880. August 2020. Available online: https://www.bis.org/publ/work880.htm (accessed on 22 March 2021).

- Boar, C.; Holden, H.; Wadsworth, A. Impending Arrival—A Sequel to the Survey on Central Bank Digital Currency. Bank of International Settlements, 107. January 2020. Available online: https://www.bis.org/publ/bppdf/bispap107.htm (accessed on 25 June 2021).

- Pocher, N.; Veneris, A. Privacy and Transparency in CBDCs: A Regulation-by-Design AML/CFT Scheme. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Bank of Japan and European Central Bank. Balancing Confidentiality and Auditability in a Distributed Ledger Environment. BoJ & ECB, Project Stella Report Phase 4. February 2020. Available online: https://www.boj.or.jp/en/announcements/release_2020/data/rel200212a1.pdf (accessed on 1 May 2021).

- Da Cunha, P.J.O.R.; Soja, P.; Themistocleous, M. Blockchain for development: A guiding framework. Inf. Technol. Dev. 2021, 27. [Google Scholar] [CrossRef]

- Areddy, J.T. China Creates Its Own Digital Currency, a First for Major Economy. Wall Street Journal. 5 April 2021. Available online: https://www.wsj.com/articles/china-creates-its-own-digital-currency-a-first-for-major-economy-11617634118 (accessed on 28 April 2021).

- Popper, N.; Li, C. China Charges Ahead with a National Digital Currency. The New York Times. 1 March 2021. Available online: https://www.nytimes.com/2021/03/01/technology/china-national-digital-currency.html (accessed on 13 May 2021).

- McNally, C.A. The DCEP: Developing the Globe’s First Major Central Bank Digital Currency. China-US Focus. 28 December 2020. Available online: https://www.chinausfocus.com/finance-economy/the-dcep-developing-the-globes-first-major-central-bank-digital-currency (accessed on 28 April 2021).

- Eastern Caribbean Central Bank. Public Roll-Out of the Eastern Caribbean Central Bank’s Digital Currency—DCash! Eastern Caribbean Central Bank. 25 March 2021. Available online: https://www.eccb-centralbank.org/news/view/public-roll-out-of-the-eastern-caribbean-central-bankas-digital-currency-a-dcash (accessed on 1 May 2021).

- Boar, C.; Wehrli, A. Ready, Steady, Go?—Results of the Third BIS Survey on Central Bank Digital Currency. Bank of International Settlements, 114. January 2021. Available online: https://www.bis.org/publ/bppdf/bispap114.htm (accessed on 22 May 2021).

- Google Trends. 2021. Available online: https://trends.google.com/trends/explore?date=2014-01-01%202021-04-01&q=CBDC,%2Fg%2F11g9svs5sb (accessed on 2 May 2021).

- Auer, R.; Boehme, R. The Technology of Retail Central Bank Digital Currency. Bank of International Settlements. March 2020. Available online: https://www.bis.org/publ/qtrpdf/r_qt2003j.htm (accessed on 22 March 2021).

- HLTF-CBDC. Report on a Digital Euro. European Central Bank, High-Level Task Force on Central Bank Digital Currency. October 2020. Available online: https://www.ecb.europa.eu/pub/pdf/other/Report_on_a_digital_euro~4d7268b458.en.pdf (accessed on 25 June 2021).

- Kiff, J.; Alwazir, J.; Davidovic, S.; Farias, A.; Khan, A.; Khiaonarong, T.; Malaika, M.; Monroe, H.; Sugimoto, N.; Tourpe, H.; et al. A Survey of Research on Retail Central Bank Digital Currency; International Monetary Fund: Rochester, NY, USA, July 2020; SSRN Scholarly Paper ID 3639760. [Google Scholar] [CrossRef]

- Kahn, C.M.; Roberds, W. Why pay? An introduction to payments economics. J. Financ. Intermed. 2009, 18, 1–23. [Google Scholar] [CrossRef]

- Bank of England. New Forms of Digital Money. Bank of England, Discussion Paper. June 2021. Available online: http://0-www-bankofengland-co-uk.brum.beds.ac.uk/paper/2021/new-forms-of-digital-money (accessed on 17 June 2021).

- Choi, K.J.; Henry, R.; Lehar, A.; Reardon, J.; Safavi-Naini, R. A Proposal for a Canadian CBDC; Social Science Research Network: Rochester, NY, USA, February 2021; SSRN Scholarly Paper ID 3786426. [Google Scholar] [CrossRef]

- Alonso, S.L.N.; Jorge-Vazquez, J.; Forradellas, R.F.R. Central Banks Digital Currency: Detection of Optimal Countries for the Implementation of a CBDC and the Implication for Payment Industry Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 72. [Google Scholar] [CrossRef]

- Bordo, M.D.; Levin, A.T. Central Bank Digital Currency and the Future of Monetary Policy; National Bureau of Economic Research: Cambridge, MA, USA, August 2017; p. w23711. [Google Scholar] [CrossRef]

- Mersch, Y. Why Europe Still Needs Cash. Project Syndicate. 28 April 2017. Available online: https://www.ecb.europa.eu/press/key/date/2017/html/ecb.sp170428.en.html (accessed on 11 May 2021).

- Huang, X. China’s DCEP project launches biggest digital yuan test yet. Forkast. 3 March 2021. Available online: https://forkast.news/china-dcep-digital-yuan-pros-cons/ (accessed on 11 May 2021).

- Sveriges Riksbank. E-Krona Project, Report 1. Report 1. September 2017. Available online: https://www.riksbank.se/en-gb/payments--cash/e-krona/e-krona-reports/e-krona-project-report-1/ (accessed on 15 May 2021).

- Office on Drugs and Crime. Money Laundering. United Nations: Office on Drugs and Crime. 2021. Available online: http://www.unodc.org/unodc/en/money-laundering/overview.html (accessed on 21 April 2021).

- Dupuis, D.; Gleason, K.; Wang, Z. Money laundering in a CBDC World: A Game of Cats and Mice. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Bijlsma, M.; van der Cruijsen, C.; Jonker, N.; Reijerink, J. What Triggers Consumer Adoption of CBDC? De Nederlandsche Bank: Rochester, NY, USA, April 2021; Working Paper 709. [Google Scholar] [CrossRef]

- Scher, I. 14 Million American Adults Don’t Have a Bank Account. They’re Still Waiting for a Stimulus Payment. Business Insider. 5 May 2020. Available online: https://www.businessinsider.com/coronavirus-stimulus-check-payment-no-bank-account-waiting-2020-5 (accessed on 15 May 2021).

- Alonso, S.L.N.; Jorge-Vazquez, J.; Forradellas, R.F.R. Detection of Financial Inclusion Vulnerable Rural Areas through an Access to Cash Index: Solutions Based on the Pharmacy Network and a CBDC. Evidence Based on Ávila (Spain). Sustainability 2020, 12, 7480. [Google Scholar] [CrossRef]

- Barrdear, J.; Kumhof, M. The Macroeconomics of Central Bank Issued Digital Currencies. BoE Staff Work. Pap. 2016, 605. [Google Scholar] [CrossRef]

- Davoodalhosseini, M. Central Bank Digital Currency and Monetary Policy. Bank of Canada, 2018–36. July 2018. Available online: https://www.bankofcanada.ca/2018/07/staff-working-paper-2018-36/ (accessed on 18 May 2021).

- Raskin, M.; Yermack, D. Digital currencies, decentralized ledgers and the future of central banking. In Research Handbook on Central Banking; Conti-Brown, P., Lastra, R.M., Eds.; Edward Elgar Publishing: Amsterdam, The Netherlands, 2018; pp. 476–486. Available online: https://www.elgaronline.com/view/edcoll/9781784719210/9781784719210.00028.xml (accessed on 18 May 2021).

- Thakor, A.V. Fintech and banking: What do we know? J. Financ. Intermed. 2020, 41, 100833. [Google Scholar] [CrossRef]

- Niepelt, D. Reserves for All? Central Bank Digital Currency, Deposits, and Their (Non)-Equivalence. Int. J. Cent. Bank. 2020, 62. Available online: https://www.ijcb.org/journal/ijcb20q2a6.htm (accessed on 18 May 2021).

- Tolle, M. Central Bank Digital Currency: The End of Monetary Policy as We Know It? Bank Underground. 25 July 2016. Available online: https://bankunderground.co.uk/2016/07/25/central-bank-digital-currency-the-end-of-monetary-policy-as-we-know-it/ (accessed on 30 April 2021).

- Sanchez-Roger, M.; Puyol-Antón, E. Digital Bank Runs: A Deep Neural Network Approach. Sustainability 2021, 13, 1513. [Google Scholar] [CrossRef]

- Hustinx, P. Privacy by design: Delivering the Promises. Identity Inf. Soc. 2010, 3, 253–255. [Google Scholar] [CrossRef] [Green Version]

- European Central Bank. In Focus—Exploring Anonymity in Central Bank Digital Currencies. European Central Bank, 4/2019. December 2019. Available online: https://www.ecb.europa.eu/paym/intro/publications/pdf/ecb.mipinfocus191217.en.pdf (accessed on 30 April 2021).

- Auer, R.; Boehme, R. Central Bank Digital Currency: The Quest for Minimally Invasive Technology. Bank of International Settlements, BIS Working Papers 948. June 2021. Available online: https://www.bis.org/publ/work948.htm (accessed on 17 June 2021).

- Directive (EU) 2015/2366 of the European Parliament and of the Council of 25 November 2015 on Payment Services in the Internal Market, Amending Directives 2002/65/EC, 2009/110/EC and 2013/36/EU and Regulation (EU) No 1093/2010, and Repealing Directive 2007/64/EC (Text with EEA Relevance); Volume OJ L; 2015; Available online: http://data.europa.eu/eli/dir/2015/2366/oj/eng (accessed on 21 April 2021).

- McCaleb, J.; Lin, L.; Lund, J. Programmable money: Will central banks take the lead? IBM Institute for Business Value. February 2018. Available online: https://www.ibm.com/downloads/cas/WVJNWYO4 (accessed on 15 May 2021).

- Bechtel, A.; Gross, J.; Sandner, P.; von Wachter, V. Programmable Money and Programmable Payments. Medium. 29 September 2020. Available online: https://jonasgross.medium.com/programmable-money-and-programmable-payments-c0f06bbcd569 (accessed on 15 May 2021).

- Lewis, A. What Actually is Programmable Money? LinkedIn. 26 April 2020. Available online: https://www.linkedin.com/pulse/what-actually-programmable-money-antony-lewis/ (accessed on 15 May 2021).

- Lund, J.; McCaleb, J.; Kennedy, M.; Drury, N. Charting the evolution of programmable money. IBM Institute for Business Value. March 2019. Available online: https://www.ibm.com/thought-leadership/institute-business-value/report/programmoneyevo (accessed on 15 May 2021).

- Auer, R.; Haene, P.; Holden, H. Multi-CBDC Arrangements and the Future of Cross-Border Payments. Bank of International Settlements, 115. March 2021. Available online: https://www.bis.org/publ/bppdf/bispap115.htm (accessed on 25 June 2021).

- Lim, M. 4 Central Banks and BIS Exploring CBDC Bridge for Asia and Middle East. Forkast. 25 February 2021. Available online: https://forkast.news/central-banks-bis-cbdc-bridge-asia-middle-east/ (accessed on 11 May 2021).

- Obstfeld, M.; Shambaugh, J.C.; Taylor, A.M. The Trilemma in History: Tradeoffs Among Exchange Rates, Monetary Policies, and Capital Mobility. Rev. Econ. Stat. 2005, 87, 423–438. [Google Scholar] [CrossRef]

- Christodorescu, M.; Gu, W.C.; Kumaresan, R.; Minaei, M.; Ozdayi, M.; Price, B.; Raghuraman, S.; Saad, M.; Sheffield, C.; Xu, M.; et al. Towards a Two-Tier Hierarchical Infrastructure: An Offline Payment System for Central Bank Digital Currencies. arXiv 2020, arXiv:201208003. [Google Scholar]

- Sheffield, C. Central Bank Digital Currency and the Future: Visa Publishes New Research. VISA Blog. 17 December 2020. Available online: https://usa.visa.com/visa-everywhere/blog/bdp/2020/12/17/central-bank-digital-1608165518834.html (accessed on 15 May 2021).

- Phillips, T. Chinese Banks Unveil CBDC Hardware Prototypes for Multiple Use Cases. NFC World. 4 May 2021. Available online: https://www.nfcw.com/2021/05/04/371992/chinese-banks-unveil-cbdc-hardware-prototypes-for-multiple-use-cases/ (accessed on 6 May 2021).

- Irrera, A. PayPal Launches Crypto Checkout Service. Reuters. 30 March 2021. Available online: https://www.reuters.com/article/us-crypto-currency-paypal-exclusive-idUSKBN2BM10N (accessed on 15 May 2021).

- Harper, C. Visa Settles USDC Transaction on Ethereum, Plans Rollout to Partners. CoinDesk. 29 March 2021. Available online: https://www.coindesk.com/visa-uses-anchorage-to-settle-usdc-transaction-on-ethereum-in-further-crypto-push (accessed on 15 May 2021).

- Le, K. New China digital yuan wallet with fingerprint ID raises privacy worries. Forkast. 12 May 2021. Available online: https://forkast.news/chinas-new-digital-yuan-wallet-with-fingerprint-id-causes-privacy-worries/ (accessed on 18 May 2021).