The Relationship between Corporate Sustainability Disclosure and Firm Financial Performance in Johannesburg Stock Exchange (JSE) Listed Mining Companies

Abstract

:1. Introduction

- To examine the relationship between corporate environmental disclosure and return on investment in South Africa among selected JSE listed mining companies;

- To examine the relationship between corporate social disclosure and return on investment in South Africa among selected JSE listed mining companies.

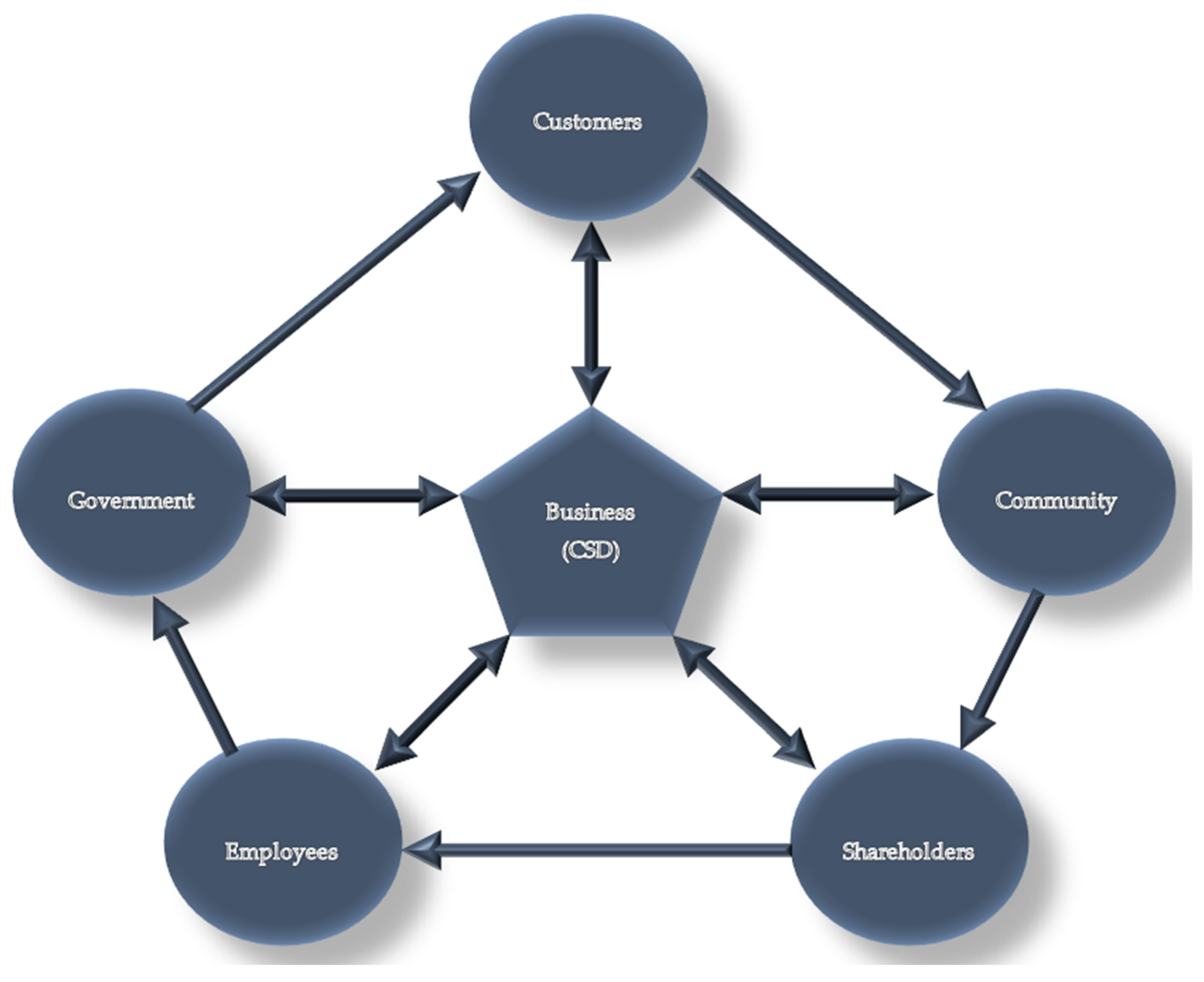

2. Theoretical Framework

2.1. Stakeholder Theory

2.2. Legitimacy Theory

2.3. Related Literature

2.3.1. Environmental Disclosure and Firm Financial Performance

2.3.2. Social Disclosure and Firm Financial Performance

3. Data, Variables and Empirical Models

3.1. Sampling and Method of Collection

3.2. Empirical Models and Variables

- y = the independent variable with i individuals and t periods;

- Xit = independent variable that varies with time;

- α = the unknown intercept for each;

- µit = the error associated with variables that occur between individuals;

- Ɛit = the error term associated with variables within each.

- y = the independent variable with i individuals and t periods;

- Xit = independent variable that varies with time;

- α = the unknown intercept for each;

- µit = the error associated with the fixed effects model.

4. Results

4.1. Fixed Effect Model for Environmental Disclosure and Return on Investment

4.2. Random Effect Model for Environmental Disclosure and Return on Investment

4.3. Fixed Effect Model for Social Disclosure and Return on Investment

4.4. Random Effect Model for Social Disclosure Return on Investment

5. Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Huang, J.; Xu, S.; Liu, D. Empirical study on the effects of corporate social responsibility disclosure in stock liquidity. Adv. Inf. Sci. Serv. Sci. 2014, 6, 62–69. [Google Scholar]

- Luning, S. Corporate Social Responsibility (CSR) for exploration. Consultants, companies and communities in process of engagements. Res. Policy 2012, 37, 205–211. [Google Scholar] [CrossRef]

- Guarnieri, R.; Kao, T. Leadership and CSR a perfect match: How top companies for leaders utilize CSR as a competitive advantage. People Strategy 2008, 31, 34–41. [Google Scholar]

- Kemp, L.J.; Vinke, J. CSR reporting: A review of the Pakistani aviation industry. South Asian J. Glob. Bus. Res. 2012, 1, 276–292. [Google Scholar] [CrossRef]

- Belal, A.R.; Cooper, S. The absence of corporate social responsibility reporting in Bangladesh. Crit. Respect. Account. 2011, 22, 654–667. [Google Scholar] [CrossRef] [Green Version]

- Garcia-Sanchez, I.; Frias-Aceitumo, J.; Rodriguez-Dominguez, L. Determinants of corporate social disclosure in Spanish local governments. J. Clean. Prod. 2013, 39, 60–72. [Google Scholar] [CrossRef]

- Mia, P.; Mamun, A. Corporate social disclosure during the global financial crisis. Int. J. Econ. Financ. 2011, 3, 174–187. [Google Scholar] [CrossRef]

- Elsakit, O.M.; Worthington, A.C. The attitudes of managers and stakeholders towards corporate social and environmental disclosure. Int. J. Econ. Financ. 2012, 4, 240–251. [Google Scholar] [CrossRef]

- Azim, M.; Ahmed, E.; D’netto, B. Corporate social disclosure of listed Bangladesh: A study of the financial sector. Int. Rev. Bus. Res. Pap. 2011, 7, 37–55. [Google Scholar]

- Ahamed, W.S.W.; Almsafir, M.K.; Al-Smadi, A.W. Does corporate social responsibility lead to improve in firm financial performance? Evidence from Malaysia. Int. J. Econ. Financ. 2014, 6, 1916–9728. [Google Scholar]

- Iqbal, N.; Ahmad, N.; Hamad, N.; Bashir, S.; Sattar, W. Corporate social responsibility and its possible impact on firm’s financial performance in banking sector of Pakistan. Arab. J. Bus. Manag. Rev. 2014, 3, 150–155. [Google Scholar]

- Hossain, M.; Reaz, M. The determinants and characteristics of voluntary disclosure by Indian banking companies. Corp. Soc. Res. Environ. Manag. 2007, 14, 274–288. [Google Scholar] [CrossRef]

- Wan Ahmad, W.N.K.; de Brito, M.P.; Tavasszy, L.A. Sustainable supply chain management in the oil and gas industry: A review of corporate sustainability reporting practices. Benchmarking Int. J. 2016, 23, 1423–1444. [Google Scholar] [CrossRef]

- Sobhani, F.A.; Zainuddin, Y.; Amran, A.; Baten, M.D.A. Corporate sustainability disclosure practices of selected banks: A trend analysis approach. Afr. J. Bus. 2011, 5, 2794–2804. [Google Scholar]

- Gunawan, J.; Djajadikerta, H.G.; Smith, M. An examination of corporate social disclosures in the annual reports of Indonesian listed companies. Asia Pac. Cent. Environ. Account. J. 2009, 15, 13–36. [Google Scholar]

- Patten, D.M. Intra-industry environmental disclosures in response to the Alaskan oil spill: A note on legitimacy theory. Account. Organ. Soc. 1992, 17, 471–475. [Google Scholar] [CrossRef]

- Zhang, T.; Gao, S.S.; Zhang, J.J. Corporate environmental reporting on the web—An exploratory study of Chinese listed companies. Issues Soc. Environ. Account. 2007, 1, 91–108. [Google Scholar] [CrossRef]

- Kalu, J.U.; Aliagha, G.U.; Buang, A. A Review of Economic Factors Influencing Voluntary Carbon Disclosure in the Property Sector of Developing Economies. Available online: https://0-iopscience-iop-org.brum.beds.ac.uk/article/10.1088/1755-1315/30/1/012010 (accessed on 20 May 2017).

- Rokhmawati, A.; Sathye, M.; Sathye, S. The effect of GHG emission, environmental performance, and social performance on financial performance of listed manufacturing firms in Indonesia. Proc. Soc. Behav. Sci. 2015, 211, 461–470. [Google Scholar] [CrossRef]

- Ganda, F.; Ngwakwe, C.C. Water efficiency practices in South African banks. Environ. Econ. 2014, 5, 42–52. [Google Scholar]

- Busch, T.; Hoffmann, V.H. How hot is your bottom line? Linking carbon and financial performance. Bus. Soc. 2011, 50, 233–265. [Google Scholar] [CrossRef]

- Ntim, C.G. Corporate governance, corporate health accounting, and firm value: The case of HIV/AIDS disclosures in Sub-Saharan Africa. Int. J. Account. 2016, 51, 155–216. [Google Scholar] [CrossRef] [Green Version]

- Dawkins, C.; Ngunjiri, F.W. Corporate social responsibility reporting in South Africa: A descriptive and comparative analysis. J. Bus. Commun. 2008, 45, 286–307. [Google Scholar] [CrossRef]

- Rein, M.; Stott, L. Working together: Critical perspectives on six cross-sector partnerships in Southern Africa. J. Bus. Ethics 2009, 90, 79–89. [Google Scholar] [CrossRef]

- Udeh, C.; Smith, W.; Shava, H. HIV/AIDS Awareness and its Impact on the Profitability of Business Firms in Developing Nations. Mediterr. J. Soc. Sci. 2014, 5, 24–25. [Google Scholar] [CrossRef]

- GRI Reporting Guidance on HIV/AIDS: A Resource Document 10–16. 2003. Available online: https://slidex.tips/download/reporting-guidance-on-hiv-aids-a-gri-resource-document (accessed on 17 June 2019).

- De Bruyn, R. A Proposed Reporting Framework for HIV/Aids Disclosure by a Listed South African Companies. Meditari Acc. Res. 2008, 19, 59–78. [Google Scholar] [CrossRef]

- Grewatsch, S.; Kleindienst, l. When Does It Pay to be Good? Moderators and Mediators in the Corporate Sustainability–Corporate Financial Performance Relationship: A Critical Review. Bus. Ethics 2017, 145, 383–416. [Google Scholar] [CrossRef]

- Klassen, R.D.; McLaughlin, C.P. The impact of environmental management on firm performance. Manag. Sci. 1996, 42, 1199–1214. [Google Scholar] [CrossRef]

- Blanco; Guillamón-Saorín, E.; Guiral, A. Do nonsocially responsible companies achieve legitimacy through socially responsible actions? The mediating effect of innovation. J. Bus. Ethics 2013, 117, 67–83. [Google Scholar] [CrossRef]

- Slapper, T.F.; Hall, T.J. The Triple Bottom Line: What Is It and How Does It Work? Available online: https://www.ibrc.indiana.edu/ibr/2011/spring/pdfs/article2.pdf (accessed on 6 June 2016).

- Roux-Kemp, A. HIV/AIDS, to Disclose or Not to Disclose: That Is the Question. 2013. Available online: http://www.scielo.org.za/pdf/pelj/v16n1/08.pdf (accessed on 17 June 2019).

- Stats SA Mid-Year Population Estimates 2018. Available online: https://www.statssa.gov.za/publications/P0302/P03022018.pdf (accessed on 27 June 2019).

- Ganda, F.; Milondzo, K.S. The effect of carbon emissions on corporate financial performance. Sustainability 2018, 10, 2398. [Google Scholar] [CrossRef]

- Ganda, F.; Ngwakwe, C.C.; Ambe, C. The determinants of corporate green investment practices in the Johannesburg Stock Exchange (JSE) listed firms. Int. J. Sustain. Econ. 2017, 9, 250–279. [Google Scholar]

- Ganda, F. Green Research and Development (R&D) investments and its impact on Market Value of Firms: Evidence from South African mining firms. J. Environ. Plan. Manag. 2018, 61, 515–534. [Google Scholar]

- Wang, T.; Bansal, P. Social responsibility in new ventures: Profiting from a long-term orientation. Strateg. Manag. J. 2012, 33, 1135–1153. [Google Scholar] [CrossRef]

- PWC. Mining Tempting Times 2018. Available online: https://www.pwc.co.za/en/assets/pdf/mine-report-2018.pdf (accessed on 17 May 2019).

- The South African Business Coalition on HIV& AIDS (SABCOHA). Available online: https://www.sabcoha.org/wp-content/uploads/bsk-pdf-manager/10_Strategy-Document_source-doc.pdf (accessed on 19 June 2019).

- Kaur, A.; Lodhia, S.K. The state of disclosure on stakeholder engagement in sustainability reporting in Australian local councils. Pac. Account. Rev. 2014, 15, 54–74. [Google Scholar] [CrossRef]

- Sun, N.; Salam, A.; Hussainey, K.; Habbash, M. Corporate environmental disclosure, corporate governance and earnings management. Manag. Audit. J. 2010, 25, 679–700. [Google Scholar] [CrossRef] [Green Version]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Orij, R. Corporate social disclosures in the context of national cultures and stakeholder theory. Account. Audit. Account. J. 2010, 23, 868–889. [Google Scholar] [CrossRef] [Green Version]

- Clarkson, M.E. A shareholder framework for analysing and evaluating corporate social performance. Acad. Manag. Rev. 1995, 20, 92–117. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Towards a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar] [CrossRef]

- Islam, M.A.; Deegan, C. Motivations for an organisation within a developing country to report social responsibility information: Evidence from Bangladesh. Account. Audit. Account. J. 2008, 21, 850–874. [Google Scholar] [CrossRef]

- Gunawan, J. Perception of important information in corporate social disclosure: Evidence from Indonesia. Soc. Responsib. J. 2010, 6, 62–71. [Google Scholar] [CrossRef]

- Burgwal, D.V.D.; Vieira, R.J.O. Environmental disclosure determinants in Dutch listed companies. Rev. Contab. Financ. 2014, 25, 60–78. [Google Scholar] [CrossRef]

- Massoud, J.A.; Daily, B.F.; Bishop, J.W. Perceptions of environmental management systems: An examination of the Mexican manufacturing sector. Ind. Manag. Data Syst. 2011, 111, 5–18. [Google Scholar] [CrossRef]

- Bowrin, A.R. Corporate social and environmental reporting in the Caribbean. Soc. Responsib. J. 2013, 9, 259–280. [Google Scholar] [CrossRef]

- Cooper, S.M.; Owen, D.L. Corporate social reporting and stakeholder accountability: The missing link. Account. Organ. Soc. 2007, 32, 649–667. [Google Scholar] [CrossRef]

- Micah, L.C.; Ofurum, C.O.; Ihendinihu, J.U. Firms financial performance and human resource accounting disclosure in Nigeria. Int. J. Bus. Manag. 2012, 7, 67–75. [Google Scholar] [CrossRef]

- Callan, S.J.; Thomas, J.M. Corporate financial performance and corporate social performance: An update and reinvestigation. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 61–78. [Google Scholar] [CrossRef]

- Nwidobile, B.M. Corporate social responsibility costs and corporate financial performances in listed firms in Nigeria. J. Adv. Res. Manag. 2014, 1, 33–40. [Google Scholar]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Peters, R.; Mullen, M.R. Some evidence of the cumulative effects of corporate social responsibility on financial performance. J. Glob. Bus. Issues 2009, 3, 1–10. [Google Scholar]

- Cheng, W.L.; Ahmad, J. Incorporating stakeholder approach in corporate social responsibility (CSR): A case study at multinational corporations (MNCs) in Penang. Soc. Responsib. J. 2010, 6, 593–610. [Google Scholar] [CrossRef]

- Sharma, U.; Davey, H. Voluntary disclosure in the annual reports of Fijian companies. Int. J. Econ. Account. 2013, 4, 184–208. [Google Scholar] [CrossRef]

- Santoso, A.H.; Feliana, Y.K. The association between corporate social responsibility and corporate financial. Issues Soc. Environ. Acc. 2014, 8, 82–103. [Google Scholar] [CrossRef]

- Freedman, M.; Patten, D.M. Evidence on the pernicious effect of financial report environmental disclosure. Account. Forum 2004, 28, 27–41. [Google Scholar] [CrossRef]

- Aggarwal, P. Sustainability reporting and its impact on corporate financial performance: A literature review. Indian J. Commer. Manag. Stud. 2013, 4, 51–59. [Google Scholar]

- Oliveira, L.; Rodrigues, L.L.; Graig, R. Intellectual capital reporting in sustainability reports. J. Intellect. Cap. 2010, 11, 575–594. [Google Scholar] [CrossRef]

- Bae Choi, B.; Lee, D.; Psaros, J. An analysis of Australian company carbon emission disclosures. Pac. Account. Rev. 2013, 25, 58–79. [Google Scholar] [CrossRef]

- Chen, J.C.; Roberts, R.W. Toward a more coherent understanding of the organisation-society relationship: A theoretical consideration for social and environmental accounting research. J. Bus. Ethics 2010, 97, 651–665. [Google Scholar] [CrossRef]

- Hahn, R.; Lülfs, R. Legitimizing negative aspects in GRI-Oriented sustainability reporting: A qualitative analysis of corporate disclosure strategies. J. Bus. Ethics 2014, 123, 401–420. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Meyer, J.W.; Scott, W.R. Organizational Environments: Ritual and Rationality; Sage: Beverly Hills, CA, USA, 1983. [Google Scholar]

- Aerts, W.; Cormier, D. Media legitimacy and corporate environmental communication. Account. Organ. Soc. 2009, 34, 1–27. [Google Scholar] [CrossRef]

- Dowling, J.; Pfeffer, J. Organizational Legitimacy: Social values and organisational behaviour. Pac. Sociol. Rev. 1975, 18, 122–136. [Google Scholar] [CrossRef]

- Gray, R.; Owen, D.; Adams, C. Accounting and Accountability; Prentice Hall: London, UK, 1996. [Google Scholar]

- Jupe, R. Disclosure in Corporate Environmental Reports: A Test of Legitimacy Theory. 2005. Available online: http://www.kent.ac.uk (accessed on 11 May 2015).

- Deegan, C. Organizational Legitimacy as a Motive for Sustainability Reporting; Unerman, J., O’Dwyer, B., Bebbington, J., Eds.; Routledge: London, UK, 2007; pp. 127–149. [Google Scholar]

- Behram, N.K. A Cross-Sectoral Analysis of environmental disclosures in a legitimacy theory context. J. Manag. Sustain. 2015, 5, 20–37. [Google Scholar] [CrossRef]

- Collins, T. Gulf Oil Spill. 2010. Available online: https://www.ocean.si.edu (accessed on 11 May 2015).

- Pereira Eugénio, T.; Costa Lourenço, I.; Morais, A.I. Sustainability strategies of the company TimorL: Extending the applicability of legitimacy theory. Manag. Environ. Qual. Int. J. 2013, 24, 570–582. [Google Scholar] [CrossRef]

- Branco, C.M.; Rodrigues, L.L. Factors influencing social responsibility disclosure by Portuguese companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Magness, V. Strategic posture, financial performance and environmental disclosure. Account. Audit. Account. J. 2006, 19, 540–563. [Google Scholar] [CrossRef]

- Tower, G.; Rusmin, R. Legitimising corporate sustainability reporting throughout the world. Australas. Account. Bus. Financ. J. 2012, 6, 19–34. [Google Scholar]

- Lanis, R.; Richardson, G. Corporate social responsibility and tax aggressiveness: A test of legitimacy theory. Account. Audit. Account. J. 2013, 26, 75–85. [Google Scholar] [CrossRef]

- Archel, P.; Husillos, J.; Larrinaga, C.; Spence, C. Social disclosure, legitimacy theory and the role of the state. Account. Audit. Account. J. 2009, 22, 1284–1307. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Tilling, M.W.; Tilt, C.A. The edge of legitimacy: Voluntary social and environmental reporting in Rothmans’ 1956–1999 annual reports. Account. Audit. Account. J. 2010, 23, 55–81. [Google Scholar] [CrossRef]

- Chelli, M.; Richard, J.; Durocher, S. France’s new economic regulations: Insights from institutional legitimacy theory. Account. Audit. Account. J. 2014, 27, 283–316. [Google Scholar] [CrossRef]

- Haji, A.A. Corporate social responsibility disclosures over time: Evidence from Malaysia. Manag. Audit. J. 2013, 28, 647–676. [Google Scholar] [CrossRef]

- Cho, C.H. Legitimation strategies used in response to environmental disaster: A French case study of Total S.A.’s Erika and AZF incidents. Eur. Account. Rev. 2009, 18, 33–62. [Google Scholar] [CrossRef]

- Hooghiemstra, R. Corporate communication and impression management new perspectives. Why companies engage in corporate social reporting. J. Bus. Ethics 2000, 27, 55–68. [Google Scholar] [CrossRef]

- SAICA Student Handbook 2017/2018: King IV Report on Governance for South Africa. Available online: https://www.saica.co.za/Technical/Assurance/SAICAHandbookIFRSHandbook/tabid/535/language/en-ZA/Default.aspx (accessed on 24 June 2019).

- Calace, D. Non-financial reporting in Italian SMEs: An exploratory study on strategic and cultural motivations. Int. J. Bus. Adm. 2014, 5, 34–48. [Google Scholar]

- Spencer, C.; Gray, R. Social and Environmental Reporting and the Business Case Research Report no.98; ACCA: London, UK, 2007. [Google Scholar]

- Endrikat, J.; Guenther, E.; Hoppe, H. Making sense of conflicting empirical findings: A meta-analytic review of the relationship between corporate environmental and financial performance. Eur. Manag. J. 2014, 32, 735–751. [Google Scholar] [CrossRef]

- Dixon-Fowler, H.R.; Slater, D.J.; Johnson, J.I.; Ellstrand, A.E.; Romi, A.M. Beyond “Does it pay to be green?” A meta-analysis of moderators of the CEP-CFP relationship. J. Bus. Ethics 2013, 112, 353–366. [Google Scholar] [CrossRef]

- Iwata, H.; Okada, K. How does environmental performance affect financial performance? Evidence from Japanese manufacturing firms. Ecol. Econ. 2011, 70, 1691–1700. [Google Scholar] [CrossRef] [Green Version]

- Albertini, E. Does environmental management improve financial performance? A meta-analytical review. Organ. Environ. 2013, 26, 431–457. [Google Scholar] [CrossRef]

- Misani, N.; Pogutz, S. Unravelling the effects of environmental outcomes and processes on financial performance: A non-linear approach. Ecol. Econ. 2015, 109, 150–160. [Google Scholar] [CrossRef]

- Horvathova, E. The impact of environmental performance on firm performance: Short-term costs and long-term benefits? Ecol. Econ. 2012, 84, 91–97. [Google Scholar] [CrossRef]

- Wu, J.; Liu, L.; Sulkowski, A. Environmental disclosure, firm performance, and firm characteristics: An analysis of S&P 100 firms. J. Acad. Bus. Econ. 2010, 10, 73–83. [Google Scholar]

- Smith, M.; Yahya, K.Y.; Amiruddin, M. Environmental disclosure and performance reporting in Malaysia. Asian Rev. Account. 2007, 15, 185–199. [Google Scholar] [CrossRef]

- Guidry, R.P.; Pattern, D.M. Voluntary disclosure theory and financial control variables: An assessment of recent environmental disclosure research. Account. Forum 2012, 36, 81–90. [Google Scholar] [CrossRef]

- Meng, X.H.; Zeng, S.X.; Tam, C.M. From voluntarism to regulation: A study on ownership, economic performance and corporate environmental information disclosure in China. J. Bus. Ethics 2014, 116, 217–232. [Google Scholar] [CrossRef]

- Ho, L.J.; Taylor, M.E. An empirical analysis of triple-bottom-line reporting and its determinants: Evidence from the United States and Japan. J. Int. Financ. Manag. Account. 2007, 18, 123–150. [Google Scholar]

- Fijałkowska, J.; Zyznarska-Dworczak, B.; Garsztka, P. Corporate Social-Environmental Performance versus Financial Performance of Banks in Central and Eastern European Countries. Sustainability 2018, 10, 772. [Google Scholar] [CrossRef]

- Nawaiseh, M.E. Do firm size and financial performance affect corporate social responsibility disclosure: Employees’ and environmental dimensions? Am. J. Appl. Sci. 2015, 12, 967–981. [Google Scholar] [CrossRef]

- Van der Laan Smith, J.; Adikhari, A.; Tondkar, R.H. Exploring differences in social disclosures internationally: A stakeholder perspective. J. Account. Public Policy 2005, 24, 123–151. [Google Scholar] [CrossRef]

- Garcia-Castro, R.; Arino, M.A.; Canela, M.A. Does social performance really lead to financial performance? J. Bus. Ethics 2009, 92, 107–126. [Google Scholar] [CrossRef]

- Skudiene, V.; McClatchey, C.; Kanclerytė, A. Strategic versus ad-hoc corporate social performance: An analysis of CSP maturity and its relationship to corporate financial performance. J. Manag. Sustain. 2013, 3, 16–32. [Google Scholar] [CrossRef]

- Lopez, M.V.; Garcia, A.; Rodriguez, L. Sustainable development and corporate performance: A study based on the Dow Jones Sustainability Index. J. Bus. Ethics 2007, 75, 285–300. [Google Scholar] [CrossRef]

- Crisostomo, V.L.; de Souza Felipe, F.; de Vasconcellos, F.C. Corporate social responsibility, firm value and financial performance in Brazil. Soc. Responsib. J. 2011, 7, 295–309. [Google Scholar] [CrossRef]

- Nollet, J.; Filis, G.; Mitrokostas, E. Corporate social responsibility and financial performance: A non-linear and disaggregated approach. Econ. Model. 2016, 52, 400–407. [Google Scholar] [CrossRef] [Green Version]

- Matuszak, Ł.; Ró˙za´ nska, E. A Non-Linear and Disaggregated Approach to Studying the Impact of CSR on Accounting Profitability: Evidence from the Polish Banking Industry. Sustainability 2019, 11, 183. [Google Scholar] [CrossRef]

- Aras, G.; Aybars, A.; Kutlu, O. Investigating the relationship between corporate social responsibility and financial performance in emerging markets. Int. J. Prod. 2010, 59, 229–254. [Google Scholar]

- Ngwakwe, C.C. Environmental responsibility and firm performance: Evidence from Nigeria. Int. J. Hum. Soc. Sci. 2009, 4, 1055–1062. [Google Scholar]

- Kuo, L.; Yeh, C.; Yu, H. Disclosure of corporate social responsibility and environmental management: Evidence from China. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 273–287. [Google Scholar] [CrossRef]

- Piatti, D. Corporate social performance and social disclosure: Evidence from Italian mutual banks. Acad. Account. Financ. Stud. J. 2014, 18, 11–35. [Google Scholar]

- Patton, M.Q. Qualitative Research and Evaluation Methods; Sage: Thousand Oaks, CA, USA, 2002. [Google Scholar]

- Hsiao, C. Analysis of Panel Data, 3rd ed.; Cambridge University Press: Cambridge, UK, 2014. [Google Scholar]

- Iyoha, M.A. Applied Econometrics; Mindex Publishing: Benin City, Nigeria, 2004. [Google Scholar]

- Borenstein, M.; Hedges, L.V.; Higgins, J.P.T.; Rothstein, H.R. A basic introduction to fixed effect and random effects models for meta-analysis. Res. Synth. Methods 2010, 1, 97–111. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Does it pay to be different? An analysis of the relationship between corporate social and financial performance. Strateg. Manag. J. 2008, 29, 1325–1343. [Google Scholar] [CrossRef]

- Gatsi, J.G.; Anipa, C.A.A.; Gadzo, S.G.; Ameyibor, J. Corporate Social Responsibility, Risk Factor and Financial Performance of Listed Firms in Ghana. J. Appl. Financ. Bank. 2016, 6, 21–38. [Google Scholar]

- Baird, P.L.; Geylani, P.C.; Roberts, J.A. Corporate social and financial performance re-examined: Industry effects in a linear mixed model analysis. J. Bus. Ethics 2011, 109, 367–388. [Google Scholar] [CrossRef]

- Ameer, R.; Othman, R. Sustainability practices and corporate financial performance: A study based on the top global corporations. J. Bus. Ethics 2012, 108, 61–79. [Google Scholar] [CrossRef]

- Cho, C.; Robets, R.; Patten, D. The Language of US Corporate Environmental Disclosure. Account. Organ. Soc. 2010, 35, 431–443. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Overell, M.B.; Chapple, L. Environmental reporting and its relation to corporate environmental performance. Abacus 2011, 47, 27–60. [Google Scholar] [CrossRef]

- Dragomir, V.D. Environmentally sensitive disclosures and financial performance in a European setting. J. Account. Organ. Chang. 2010, 6, 359–388. [Google Scholar] [CrossRef]

- Lan, Y.; Wang, L.; Zhang, X. Determinants and features of voluntary disclosure in the Chinese stock market. China J. Account. Res. 2013, 6, 265–285. [Google Scholar] [CrossRef] [Green Version]

- Mathuva, D.M.; Kiweu, J.M. Cooperative social and environmental disclosure and financial performance of savings and credit cooperatives in Kenya. Adv. Account. 2016, 35, 197–206. [Google Scholar] [CrossRef]

- DEAT. Environmental Auditing, Integrated Environmental Management, Information Series 14; Department of Environmental Affairs and Tourism (DEAT): Pretoria, South Africa, 2004. Available online: https://www.environment.gov.za/sites/default/files/docs/series14_environmental_auditing.pdf (accessed on 20 March 2017).

- Sueyoshi, T.; Goto, M. Can environmental investment and expenditure enhance financial performance of US electric utility firms under the clean air act amendment of 1990? Energy Policy 2009, 37, 4819–4826. [Google Scholar] [CrossRef]

- Luo, X.; Bhattacharya, C.B. Corporate social responsibility, customer satisfaction, and market value. J. Mark. 2006, 70, 1–18. [Google Scholar] [CrossRef]

- Kleynhans, E.P.J.; Kruger, M.C. Effect of Black Economic Empowerment on profit and competitiveness of firms in South Africa. Acta Commer. 2014, 14, 1–10. [Google Scholar] [CrossRef]

- Lin, C.H.; Yang, H.L.; Liou, D.Y. The impact of corporate social responsibility on financial performance: Evidence from business in Taiwan. Technol. Soc. 2009, 31, 56–63. [Google Scholar] [CrossRef]

- Hansson, B. Company-based determinants of training and the impact of training on company performance: Results from an international HRM survey. Person. Rev. 2007, 36, 311–331. [Google Scholar] [CrossRef]

{kind=link}

| Research Variable | Measurement |

|---|---|

| Environmental Disclosure | Quantitative Content Analysis (Word count) |

| Social Disclosure | Quantitative Content Analysis (Word count) |

| Return On Investment | Profit before tax ÷ Total Assets |

| Sales Growth | (Current Year Sales -Previous Year Sales) ÷ Previous Year Sales |

| Leverage | Total long-term debt ÷ Total Assets |

| Variables | Observations | Mean | Std. Dev | Min | Max |

|---|---|---|---|---|---|

| Environmental Disclosure (EDY) | 50 | 8.46 | 6.145215 | 1 | 30 |

| Social Disclosure (SDY) | 50 | 29.84 | 29.16901 | 1 | 117 |

| Return On Investment (ROI) | 50 | 0.1890148 | 0.280528 | −0.208 | 0.92889 |

| Sales Growth | 50 | 0.0895764 | 0.193898 | −0.496 | 0.65345 |

| Leverage | 50 | 0.237122 | 0.104103 | 0.0669 | 0.5115 |

| Variables | EDY | SDY | ROI | Sales Growth | Leverage |

|---|---|---|---|---|---|

| EDY | 1 | ||||

| SDY | −0.1221 | 1 | |||

| ROI | −0.3126 | 0.3179 | 1 | ||

| Sales Growth | −0.0433 | −0.0599 | 0.2158 | 1 | |

| Leverage | −1.1447 | −0.0644 | −0.118 | 0.1147 | 1 |

| Variables | Random Effect Model | Fixed Effect Model | ||

|---|---|---|---|---|

| Coefficient | Standard Error | Coefficient | Standard Error | |

| EDY | −0.0019603 | 0.0043171 | −0.0004349 ** | 0.0044799 |

| Sales Growth | 0.2079847 ** | 0.0821838 | 0.1997456 ** | 0.0826443 |

| Leverage | −0.9086022 *** | 0.3401453 | −1.0109839 *** | 0.3677037 |

| Constant | 0.4024183 | 0.1236268 | 0.4166281 | 0.945937 |

| Sigma_u | 0.2714606 | 0.27508873 | ||

| Sigma_e | 0.10778816 | 0.10778816 | ||

| Rho | 0.86440187 | 0.86690334 | ||

| R2: Within | 0.2752 | 0.2789 | ||

| Between | 0.0268 | 0.0131 | ||

| Overall | 0.0584 | 0.0401 | ||

| Corr(u_i, Xb) | 0 (assumed) | −0.1982 | ||

| F(3, 37) | 4.77 | |||

| Prob > F | 0.0066 | |||

| Wald (X2) | 14.25 | |||

| Prob > chi2 | 0.0026 | |||

| Hausman Test (X2) | 0.5804 | |||

| Breuch-Pagan Test (X2) | 0.0000 | |||

| Number. of Obs. | 50 | 50 | 50 | 50 |

| Variables | Random Effect Model | Fixed Effect Model | ||

|---|---|---|---|---|

| Coefficient | Standard Error | Coefficient | Standard Error | |

| Sdy | 0.0017045 | 0.001128 | 0.0014069 | 0.001195 |

| Sales | 0.2031574 ** | 0.826091 | 0.1947259 ** | 0.810814 |

| Leverage | −0.8515363 *** | 0.3360223 | −0.9922509 *** | 0.3612355 |

| Constant | 0.3218711 | 0.1175239 | 0.3648733 | 0.0966802 |

| Sigma_U | 0.23270571 | 0.26553138 | ||

| Sigma_E | 0.10583757 | 0.1053757 | ||

| Rho | 0.8286008 | 0.86290789 | ||

| R2: Within | 0.3009 | 0.3048 | ||

| Between | 0.0723 | 0.0505 | ||

| Overall | 0.1059 | 0.0842 | ||

| Corr(u_i, Xb) | 0 | −0.1325 | ||

| F(3, 37) | 5.41 | |||

| Prob > F | 0.035 | |||

| Wald (X2) | 16.08 | |||

| Prob > chi2 | 0.0011 | |||

| Hausman Test (X2) | 0.6961 | |||

| Breuch-Pagan Test (X2) | 0.0000 | |||

| Number. of Obs. | 50 | 50 | 50 | 50 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wasara, T.M.; Ganda, F. The Relationship between Corporate Sustainability Disclosure and Firm Financial Performance in Johannesburg Stock Exchange (JSE) Listed Mining Companies. Sustainability 2019, 11, 4496. https://0-doi-org.brum.beds.ac.uk/10.3390/su11164496

Wasara TM, Ganda F. The Relationship between Corporate Sustainability Disclosure and Firm Financial Performance in Johannesburg Stock Exchange (JSE) Listed Mining Companies. Sustainability. 2019; 11(16):4496. https://0-doi-org.brum.beds.ac.uk/10.3390/su11164496

Chicago/Turabian StyleWasara, Tafadzwa Mark, and Fortune Ganda. 2019. "The Relationship between Corporate Sustainability Disclosure and Firm Financial Performance in Johannesburg Stock Exchange (JSE) Listed Mining Companies" Sustainability 11, no. 16: 4496. https://0-doi-org.brum.beds.ac.uk/10.3390/su11164496