Supply Chain Contracts under New Product Development Uncertainty

1

Korea University Business School, Korea University, Anam 145, Seongbuk, Seoul 02841, Korea

2

Department of Business Administration, Kyonggi University, Gwanggyosan, Yeongtong, Suwon 16227, Korea

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(23), 6858; https://0-doi-org.brum.beds.ac.uk/10.3390/su11236858

Submission received: 12 October 2019

/

Revised: 15 November 2019

/

Accepted: 28 November 2019

/

Published: 2 December 2019

(This article belongs to the Special Issue Collaborative Supply Chain Networks)

{kind=link}

{kind=link}

{kind=link}

Abstract

:New product development has been serving as a growth engine for companies; given this background, the innovation of suppliers that possess new technologies for new products has been a significant subject for manufacturers, particularly in high-tech industries. However, the technology uncertainty associated with the supplier’s development capability may become a considerable obstacle to new product development projects. In this paper, we further develop an analytical model that has been widely applied in the economics literature and examine two representative supply chain contracts, a revenue-sharing contract and a cost-sharing contract, for new product development through upstream innovation under technology uncertainty. We confirm that the supplier’s development capability has a significant impact on contract feasibility. The revenue-sharing contract helps to attain a higher new product quality level and profit for the supply chain. Furthermore, we explore the relationship between a manufacturer and a supplier concerning the performance of the new product development project. Adopting a Nash bargaining model, we analyze the two supply chain contracts under a cooperative relationship in which the manufacturer and supplier cooperatively determine the sharing portion of the revenue or cost. For both contracts, compared with the unilateral relationship, the cooperative relationship leads to a lower manufacturer profit, but a higher new product quality and a higher supply chain profit.

1. Introduction

Given that consumers’ desires and tastes continue to change, new product development is serving as a growth engine for companies and is an essential strategy for sustainable growth. Particularly, for companies in high-tech industries, where technology is rapidly evolving, it is imperative to gain a competitive advantage by developing new products. These new products can be classified into several categories, from those obtained through the improvement and modification of existing products to technically new-to-the-world products [1]. In this paper, we focus on completely new products, both technically and physically.

Traditionally, the performance of a newly developed products is considered to depend on the internal capabilities of the producing company. Recently, many companies have been developing new products in cooperation with suppliers that possess core components or new technologies for those products. For example, Apple receives Gorilla Glass, a type of scratch-resistant glass, from Corning to produce digital devices and sell them to consumers. This suggests that innovation from suppliers, such as Corning, is vital in the supply chain of manufacturers, such as Apple, to develop new products. Thus, it is important for manufacturers to encourage suppliers to invest in new technologies for new products. Using the same example, Apple invested USD 200 million in 2017 to support Corning’s latest glass processing facility, which allowed Corning to focus on developing bendable glass, leading to Apple’s expectation to launch its first foldable smartphone in 2020 [2]. Tesla Motors, the world’s largest manufacturer of electric vehicles (EV), procures lithium-ion battery cells, which are a core component of EV, from its sole supplier, Panasonic. In 2014, in preparation for Model 3, an affordable compact sedan, Tesla began the construction of Gigafactory 1 near Nevada, estimated to cost $5 billion, following Panasonic’s agreement to lead the mass production of battery cells at the factory. Recently, as Tesla and Panasonic’s relationship has been deteriorating, Tesla is attempting to establish a new relationship with CATL as a battery supplier in China and encourage innovations in battery technology [3,4].

Given the significance of suppliers’ innovation, how can a manufacturer encourage or motivate suppliers to invest in creating new technologies? How can a manufacturer obtain more profits from suppliers’ innovation activities? One method is that the manufacturer may consider several supply chain contracts that benefit the suppliers. Therefore, in this study, we address the impact of a revenue-sharing and a cost-sharing contract between manufacturers and suppliers for the development of new products. In addition to contracts, technology uncertainty is considered another important factor. Developing new products plays a decisive role in creating new growth engines for companies; however, at the same time, there are several risk factors involved, such as financial or operational risks [5]. When developing a completely new product, these risks may arise from technology uncertainty, particularly, development time uncertainty. The completion of the new product development project may be delayed due to unexpected events or a lack of capability of the supplier. Moreover, the value of a new product development may decline due to the earlier entry of competitors into the market. Therefore, this study evaluates the decision-making for a new product development under development time uncertainty.

In this paper, we further develop an analytical model that has been widely applied in the economics literature and analyze two types of contracts between a manufacturer and a supplier within a supply chain under the condition of technology uncertainty associated with the supplier’s development capability. Specifically, in a situation in which the manufacturer sets the price of the new product and the supplier determines the wholesale price and the quality level of the product, the type of contract and the relationship between two firms also affect the overall supply chain performance. Thus, our analysis proceeds as follows. First, an analysis is performed by comparing the revenue- and the cost-sharing contracts in the situation where the manufacturer unilaterally offers the contract terms, that is, the portion of revenue or cost that the manufacturer will share with the supplier. Second, we examine the two contracts under a cooperative relationship through a Nash bargaining game, in which the manufacturer and the supplier jointly determine the contract terms. Finally, we analyze how the decision-making for each contract changes under unilateral and cooperative relationships, respectively, in terms of which contract generates higher supply chain performance.

The results provide practical implications for manufacturers seeking for a new growth base through new product development. By understanding the impacts of the uncertainty stemming from the suppliers’ development capabilities and the relationship with them, we expect manufacturers to be able to implement supply chain contracts more effectively and achieve successful new product development.

The remainder of this paper is organized as follows. The literature related to this study is reviewed in Section 2. In Section 3, we analyze each contract-specific decision under a unilateral relationship under the underlying assumptions of the model. In Section 4, we analyze each contract-specific decision given a cooperative relationship and compare supply chain performances. Finally, Section 5 summarizes the main results and discusses managerial implications, limitations, and future research directions.

2. Literature Review

This study focuses on two research areas: new product development and supply chain contracts. First, new product development has long been an important research topic in operations management. Whereas most studies have focused on product development and innovation within a single firm [6], there is also a literature stream on the interactions between product development and supply chains [7,8,9]. For instance, Novak and Eppinger [10] studied the complexities of product development and the vertical integration of supply chains. Pero et al. [11] developed a framework for the alignment of new product development and supply chains using multiple case studies. Lin et al. [12] presented an empirical model which addressed the drivers of innovation in channel integration in supply chain management. Gilbert and Cvsa [13] examined the strategic mechanism of promoting downstream innovation in the supply chain, while Wang and Shin [14] focused on upstream innovation. This study considers innovation and new product development by upstream suppliers, such as in Wang and Shin [14].

While most studies on innovation or new product development within a supply chain focus on strategic decision making, such as price and quality, they ignore the effect of uncertainty in developing new products [15]. As Ragatz et al. [16] explained, companies are trying to integrate their suppliers earlier into the new product development process. This involvement may range from the simple consultation with the supplier on idea generation to making them fully responsible for the design of components or systems. Ragatz et al. [16] developed a model for investigating the effect of some elements of the supplier integration process on cost, quality, and new product development time, under conditions of technology uncertainty. Also, Loch and Terwiesch [17] addressed upstream and downstream operations in the presence of technical uncertainty. Baskaran and Krishnan [18] separated technical uncertainty into transnational and timing uncertainty, and analyzed the effect of both on decision making for new product development. Based on the literature, this paper studies decision making for new product development given development time uncertainty.

In terms of the supply chain contracting, Cachon [19] comprehensively reviewed various supply-chain contracts, identifying their advantages and drawbacks. More precisely, many studies tackle a revenue-sharing contract, which is widely used in reality. Cachon and Lariviere [20] identified the strengths and limitations of revenue-sharing contracts. Under consignment contracts with revenue-sharing, the overall supply-chain performance and individual firms’ performance depends on several factors, such as demand price elasticity or individual firms’ risk preferences [21,22]. Pan et al. [23] compared a revenue-sharing contract and a wholesale price contract under manufacturer-dominated and retailer-dominated situations in a supply chain. In addition to revenue-sharing contracts, a group of papers examines cost-sharing contracts in a supply chain. Leng and Parlar [24] found that properly designed lost-sales cost-sharing and buy-back contracts coordinated a supply chain through game-theoretic models. Chao et al. [25] introduced two contractual agreements for sharing the product recall costs and discussed their impact on quality improvement.

There is also a stream of work on the impact of supply chain contracts on product development and innovation. Baskaran and Krishnan [18] modeled the process of collaborative product development between two firms under revenue-sharing, cost-sharing, and effort-sharing mechanisms. Wang and Shin [14] studied the effect of a wholesale price, quality-dependent wholesale price, and revenue-sharing contracts on upstream innovation. In addition to product development, Ma et al. [26] designed the optimal contracts between a manufacturer and a retailer to enhance corporate social responsibility activities, which is sustainable business strategy.

Besides supply chain contract types, another factor affecting the performance of new product development projects is the contract mechanism used to determine the portion of revenue or cost shared by the supplier and the manufacturer. In supply chain management, many studies have already demonstrated the positive effects of a cooperative supply chain [27,28]. In terms of supply chain contracts, Zhao et al. [29] analyzed contracts between manufacturers and suppliers using a cooperative game theory approach, while Zhang et al. [30] analyzed the effects of cooperative investment and revenue-sharing contracts on supply chain coordination. Baskaran and Krishnan [18] studied cooperative contracts between two companies using a Nash bargaining game. Therefore, this study examines supply chain contracts considering both the unilateral relationship, in which the manufacturer leads the decision on the sharing ratio, and the cooperative relationship, in which the manufacturer and supplier determine together the ratio.

Finally, regarding modeling, while many models of supply chain contracts use stochastic market demand [31,32], others use different demand functions, such as the linear demand form widely used in marketing research [33,34]. Further, Wang and Shin [14] utilized Hotelling’s [35] product differentiation model. We extend the supply-chain literature by proposing a model with endogenous demand incorporating consumer heterogeneity, which has been little explored in this field.

3. Model Description

This paper considers a basic supply chain with an upstream supplier and a downstream manufacturer who carry out new product development. The supplier invests in the development of the new product’s main component, whose quality significantly influences the performance of the new product, while the manufacturer purchases the main component from the supplier and produces the new product. The manufacturer considers a revenue- or a cost-sharing contract to encourage the supplier to invest more in the development of the new product’s main component (hereafter, new product development).

The literature has shown that technology uncertainty has a considerable impact on new product development or technical innovation [36,37]. Among the different technology uncertainties, this paper explores the situation in which the time required for the new product development is uncertain, which we refer to as development time uncertainty. The development time uncertainty is critical when developing a new product, depending on the supplier’s capability, as well as the new product’s quality. Following the literature, we assume that the development time is exponentially distributed, with a probability density function [18]. The development rate represents the time required for the new product development, and we assume that , where is the supplier’s innate development capability and is the quality of the new product. The function indicates that a higher supplier capability reduces the time needed to develop a new product, while the higher quality of the new product requires longer development time. This paper thus examines how development time uncertainty affects decision making for a new product development.

New product development entails several costs. First, the supplier makes an upfront investment, such as building new facilities, which incurs a fixed cost of development. As fixed cost is a function of the new product’s quality level, it takes the form , where is a development cost parameter. Moreover, the new product development incurs variable costs. The supplier has unit production cost and the manufacturer has unit manufacturing cost , both increasing with the new product’s quality level.

Furthermore, new product development entails opportunity costs for both the supplier and manufacturer. As such, the value of the new product development in a supply chain can depend on the extent of competitors’ new product development efforts. However, since the state of competitors’ new product development is uncertain, a delay in new product development incurs an opportunity cost for the supply chain [38]. Commitment to developing one product or technology may also incur an opportunity cost in that other, better opportunities can be lost [5]. Higher quality for a new product implies longer development time, resulting in higher opportunity costs. Therefore, we model the costs as , where is an opportunity cost parameter.

The decision-making timeline, illustrated in Figure 1, includes three stages. First, the manufacturer and supplier sign the contract. There are two different contracts: (i) a revenue-sharing contract, in which the manufacturer first proposes to share an portion of its revenue with the supplier, and (ii) a cost-sharing contract, in which the manufacturer offers the supplier to share a portion of the development cost. Second, the supplier then determines the quality level of the new product and the wholesale price . Finally, the manufacturer decides on the new product price , and the revenues of the new product development project are realized.

This paper finds the optimal solutions through an analytical model that has been widely applied in the economics literature since the seminal paper by Mussa and Rosen [39]. A new product is defined by a single dimension called quality . The quality means a core component that determines the overall quality of the product or a combination of components indicating “the more, the better” [40,41]. Each consumer has a marginal valuation or willingness to pay for quality . Then, the utility function for a consumer from purchasing the new product becomes , and the consumer purchases the new product unless his/her utility is negative. Since consumers have heterogeneous valuations about quality, we assume that consumers’ willingness to pay for quality follows a uniform distribution on . The uniform distribution is not only commonly used in other analytical models, but it is also particularly suitable when it is difficult to predict the distribution of consumer preferences for quality [42,43,44,45]. From this assumption, we can derive the endogenous demand for the new product in this market setting as follows: .

4. Contracts under a Unilateral Relationship

4.1. Revenue-Sharing Contract

Here, we examine a revenue-sharing contract, in which the manufacturer shares a fraction of its revenue with the supplier. Considering the manufacturing and opportunity costs for the development time, the manufacturer’s profit is represented as:

The supplier’s profit, including the production, development, and opportunity costs for development time, is expressed as:

To obtain the optimal supply-chain decisions, we use backward induction. In Stage 3, the manufacturer determines the new product price that maximizes profit function (1) as:

In Stage 2, the supplier anticipates that the manufacturer will set the new product price as in Equation (3) and determines the quality level of the new product and the wholesale price to maximize profit function (2) as follows:

Finally, in Stage 1, considering Equation (4), the manufacturer determines the share of its revenue to maximize profit. The following proposition represents the optimal revenue share and profit under the revenue-sharing contract.

Proposition 1.

- (a)

- When, the optimal revenue share is 1. When, the optimal revenue share is:

- (b)

- When,is decreasing in the development cost and supplier’s development capability and increasing in the opportunity cost.

- (c)

- When, the optimal profits of the manufacturer and supplier are, respectively:

The proof of Proposition 1 is provided in Appendix A.

Proposition 1 indicates that the supplier’s development capability has a significant impact on the contract feasibility. When the supplier’s capability is low, it is optimal for the manufacturer not to share its revenue with the supplier, which implies that the manufacturer uses the wholesale price contract broadly used in many supply chains. When the revenue-sharing contract is feasible, that is, when the supplier’s capability is high, as the development cost increases, the manufacturer should retain a smaller share of its revenue. This is because the high development cost causes the supplier to be reluctant to invest in new product development. Therefore, when new product development is costly, the manufacturer can encourage the supplier to invest in the new product by offering a higher share of its revenue to the supplier.

Proposition 1 also shows how the development capability of the supplier affects the optimal revenue share. As the development capability of the supplier increases, it can obtain a larger share of the revenue from the manufacturer because the value of the new product development increases. Moreover, a high opportunity cost implies the competitors have a high capability for the new product development, which results in a high uncertainty about dominating the market, or that improving other abilities in the supply chain may bring significant benefits. Thus, for a higher opportunity cost, the manufacturer should retain a larger revenue share to protect its profit.

4.2. Cost-Sharing Contract

Under the cost-sharing contract, the manufacturer offers to share fraction of the development cost with the supplier. The profits of the manufacturer and supplier are, respectively:

As in the previous section, we identify the optimal decision by backward induction. At first, the manufacturer determines the new optimal product price to maximize profit function (5) as follows:

Next, anticipating that the manufacturer will set the product price as in Equation (7), the supplier determines the quality level and wholesale price of the new product to maximize profit function (6):

Finally, considering Equation (8), the manufacturer sets the sharing ratio of the development cost to maximize its profit. Proposition 2 shows the optimal cost share and profits of the manufacturer and supplier under a cost-sharing contract.

Proposition 2.

- (a)

- The optimal cost share is 0.

- (b)

- The optimal profits of the manufacturer and supplier are, respectively:

The proof of Proposition 2 is provided in Appendix A.

Proposition 2 shows that it is optimal for the manufacturer not to share the development cost with the supplier, regardless of the supplier’s capability. In other words, a cost-sharing contract is not performed between the manufacturer and supplier, which indicates that this becomes a wholesale price contract.

4.3. Comparison between the Revenue- and Cost-Sharing Contracts

Here, we compare the results of the revenue- and cost-sharing contracts and analyze which contract is more efficient under a certain condition when developing a new product. and in the superscript refer to the revenue- and cost-sharing contracts, respectively. As seen in Proposition 2, it is optimal not to perform the cost-sharing contract; we keep calling it cost-sharing contract for consistency, although the cost-sharing contract refers to the wholesale price contract in this section.

Proposition 3.

When , the quality level of the new product, manufacturer’s profit, and supplier’s profit are higher under the revenue-sharing contract than the cost-sharing contract. Moreover, as the supplier’s development capability increases, the profitability of the revenue-sharing contract also increases.

The proof of Proposition 3 is provided in Appendix A.

Proposition 3 shows that, when the supplier’s development capability is high, a revenue-sharing contract results in a higher new product quality level and higher profits for the manufacturer as well as the supplier, resulting in an overall higher profit for the supply chain. One might expect that the manufacturer would gain more profit from a no revenue-sharing approach. However, by sharing the revenue with the supplier, the supplier sets the wholesale price lower and improves the quality level, which in turn enables the manufacturer to set the new product’s price higher. This mechanism involves that the manufacturer prefers the revenue-sharing contract. Furthermore, as the supplier’s development capability increases, the profitability gap between the revenue- and cost-sharing contracts increases because the manufacturer can set the new product’s price higher and the supplier can obtain a larger revenue share.

5. Contracts under a Cooperative Relationship

In Stage 1, when the manufacturer and supplier enter a contract, the manufacturer determines the level of or ratios to maximize its profit and offers it to the supplier. Here, we analyze the situation in which the manufacturer and supplier cooperatively determine the sharing portion of the revenue or cost building a strategic partnership. We assume that the two firms agree to adopt the bargaining model proposed by Nash [46,47].

5.1. Revenue-Sharing Contract

As in Section 4.1, using backward induction, after the manufacturer sets the new product’s price as to maximize its profit, the supplier determines the quality level of the new product and the wholesale price . Lastly, in Stage 1, the manufacturer and the supplier cooperatively determine how to split the revenue. The optimal revenue share is determined by:

The following proposition presents the optimal revenue share under the cooperative relationship and compares it with the results in Section 4.1. in the subscript means a contract under the cooperative relationship, and means the contract in Section 3, because it is a unilateral decision by the manufacturer.

Proposition 4.

- (a)

- When , the optimal revenue share is 1. When , the optimal revenue share is:

- (b)

- When , the optimal revenue share under the cooperative relationship is lower than that under the unilateral relationship.

- (c)

- When is less sensitive to the changes in and than .

The proof of Proposition 4 is provided in Appendix A.

Proposition 4 illustrates how the cooperative relationship affects a contract. First, the level of the supplier’s development capability that makes the revenue-sharing contract workable is lower under the cooperative relationship than the unilateral relationship, which implies that a revenue-sharing contract can be made easier under the cooperative relationship. When the revenue-sharing contract is feasible, the supplier can obtain a larger revenue share under a cooperative relationship because the supplier is involved in determining the revenue share to maximize its profit. Moreover, under the cooperative relationship, the optimal revenue share is also increasing in the supplier’s development capability and development cost, and is decreasing in the opportunity cost. Further, the changes are lower than under the unilateral relationship. In other words, a contract under the cooperative relationship is expected to be less affected by uncertainty in the supplier’s capability or costs.

The following proposition compares the revenue-sharing contract results between cooperative and unilateral relationships when the contract is feasible .

Proposition 5.

For a revenue-sharing contract, compared with the unilateral relationship, the cooperative relationship leads to (i) a higher new product quality level, (ii) a lower manufacturer profit, (iii) a higher supplier profit, and (iv) a higher supply chain profit.

The proof of Proposition 5 is provided in Appendix A.

Under a cooperative relationship, the quality level of the new product is higher than under a unilateral relationship because the quality level decreases as the revenue share increases , and the revenue share under a cooperative relationship is lower (see Proposition 4). In other words, as the supplier obtains a larger revenue share, it can be further motivated to develop a new product, leading to a higher quality of this new product. This finding implies that the cooperative relationship contributes to the performance improvement of the supplier. Furthermore, a smaller revenue share under the cooperative relationship reduces the manufacturer’s profit and increases the supplier’s profit. Consequently, the supply chain profit increases because the profit increase of the supplier is larger than the profit decrease of the manufacturer.

5.2. Cost-Sharing Contract

As in the previous section, we use backward induction. After going through Stage 3, in Stage 1, the manufacturer and the supplier cooperatively set the portion of the development cost they will share. The optimal cost share is determined by the following function:

Proposition 6.

- (a)

- When , the optimal cost share is 0. When , the optimal cost share is:

- (b)

- When is increasing in the development cost and supplier’s development capability and decreasing in the opportunity cost.

The proof of Proposition 6 is provided in Appendix A.

Unlike the unilateral relationship, under the cooperative relationship, a cost-sharing contract can be feasible. When the supplier’s development capability is sufficiently high, the supplier can enter the cost-sharing contract and determine the sharing cost fraction cooperatively with the manufacturer. As the development cost increases, the optimal cost share also increases. The high development cost makes the supplier reluctant to invest in new product development. Therefore, the manufacturer can encourage the supplier to embark on new product development by sharing a larger portion of the development cost. Additionally, the supplier can obtain a larger cost share as its development capability is higher, allowing the supplier to have more influence on decision-making in Stage 1. This result shows that, as the development cost and the supplier’s capability grow, the supplier benefits more from the cost-sharing contract, which is consistent with the results on the revenue-sharing contract. Finally, as the opportunity cost increases, the manufacturer wants to reduce the cost share because of the increased burden of sharing the development cost. Proposition 7 shows a comparison of the cost-sharing contract results under cooperative and unilateral relationships when the contract is feasible .

Proposition 7.

For a cost-sharing contract, compared with the unilateral relationship, the cooperative relationship leads to (i) a higher new product quality level, (ii) a lower manufacturer profit, (iii) a higher supplier profit, and (iv) a higher supply chain profit.

Under the cooperative relationship, the quality level of the new product is higher than under the unilateral relationship, the manufacturer’s profit decreases, and the supplier’s profit increases. The total profit of the supply chain also increases because the profit increase of the supplier is greater than the profit decrease of the manufacturer, which is the same as under the revenue-sharing contract.

5.3. Comparison of the Two Contracts under a Cooperative Relationship

Here, we compare the results of the revenue- and cost-sharing contracts under the cooperative relationship. According to the findings in the previous sections, the revenue- and cost-sharing contracts are not feasible when and , respectively. In other words, when is within range , both contracts are equivalent to the wholesale price contract; when is within the range , the cost-sharing contract is equivalent to the wholesale price contract; and when , both contracts are feasible. For consistency, we maintain the names of the revenue- and cost-sharing contracts, regardless of the feasible ranges.

Proposition 8.

The new product quality level and the supplier’s profit are higher under the revenue-sharing contract compared with the cost-sharing contract. Moreover, as the supplier’s development capability increases, the differences between the two contracts increase as well.

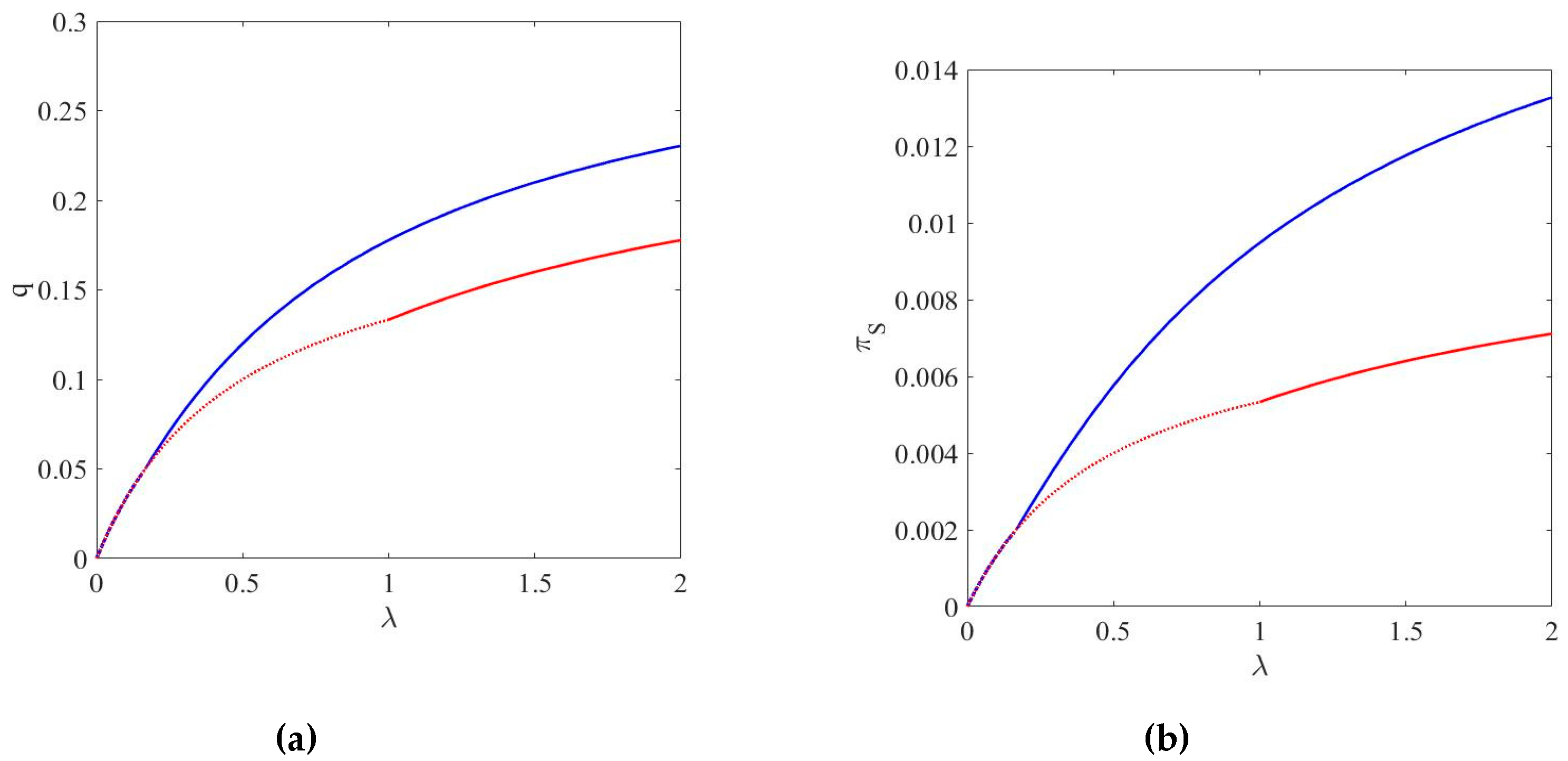

Proposition 8 shows that the revenue-sharing contract dominates the cost-sharing one in terms of the new product quality level and the supplier’s profit, which is consistent with the results for the unilateral relationship. Figure 2 illustrates Proposition 8 using a numerical example with and . The dotted lines indicate the ranges in which each contract is not feasible. When is within range , the two contracts are identical to the wholesale price contract. When is within range , the revenue-sharing contract can be performed but the cost-sharing contract is still not feasible. If is greater than , both contracts are workable. Figure 2 shows that the revenue-sharing contract leads to a higher quality level for the new product and a higher profit for the supplier, except when the supplier’s capability is sufficiently low.

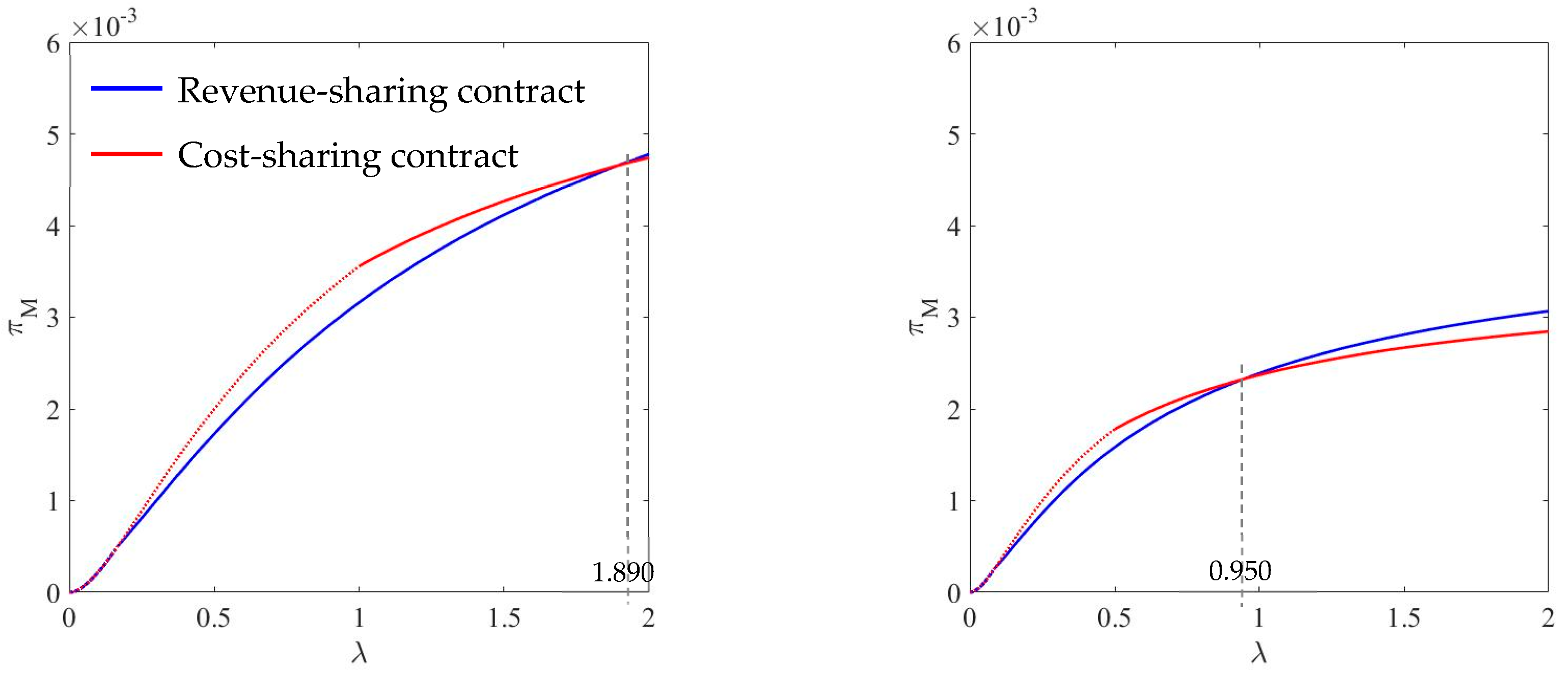

Given a unilateral relationship, the manufacturer’s profit is also higher in the revenue-sharing contract than the cost-sharing one. However, given the cooperative relationship, the cost-sharing contract is not always dominated by the revenue-sharing contract in terms of the manufacturer’s profit. Although there exists a threshold on the supplier’s development capability such that the cost-sharing contract is more profitable for the manufacturer, the threshold is not closed-form. Therefore, we analyze the manufacturer’s profit using the following numerical examples: (a) when the development cost is low, ; (b) when the development cost is high, , and the remaining parameters are identical in both cases, with and .

Figure 3 shows when and which contract yields a higher profit for the manufacturer; the dotted lines indicate the ranges in which the contract is not feasible. When the development capability is very low ( in (a) and in (b)), both contracts are not feasible and generate the same profits. When the development cost is intermediate ( in (a) and in (b)), the manufacturer’s profit is lower in the revenue-sharing contract. Under a unilateral relationship, the revenue-sharing contract always generates a higher manufacturer profit, while with the cooperative relationship, the revenue-sharing contract can be less profitable. This is because the revenue share that the manufacturer obtains in the cooperative relationship is lower than in the unilateral relationship. Moreover, as the development cost increases, the range under which the cost-sharing contract has more benefits than the revenue-sharing contract narrows (from to ).

Finally, the total profit of the supply chain is higher in the revenue-sharing contract than the cost-sharing one. The manufacturer’s profit is lower in the revenue-sharing contract when the development capability is intermediate, whereas the supplier’s profit is always higher in the revenue-sharing contract. However, the difference in the manufacturer’s profit between the two contracts is relatively small, while the difference in the supplier’s profit is relatively significant, which makes the revenue-sharing contract preferable in terms of the supply chain’s profit.

6. Discussion

This paper analyzed two broadly used contract types, the revenue- and cost-sharing contracts, in a supply chain consisting of a manufacturer and a supplier, considering development time uncertainty based on the supplier’s development capability. In a situation in which the manufacturer considers two contracts to encourage the supplier to invest in a new product development, we analyze the impact of the supplier’s development capability on supply chain decisions. Moreover, we compare the outcomes of the two contracts when the relationship between the manufacturer and supplier is either unilateral or cooperative.

The findings provide several managerial implications for manufacturers who plan to develop new products based on upstream innovation. First, the optimal contract depends on the supplier’s development capability, which is directly associated with the development time. In contrast to the existing literature, which focuses mainly on whether a contract coordinates the supply chain, our results suggest that before entering a contract and reviewing the coordination, the manufacturer should first thoroughly examine the supplier’s capability. We show that the revenue- or cost-sharing contracts are not always feasible; they can be feasible only if the supplier has enough development capability. Moreover, if the capability is high, the revenue-sharing contract helps attain a higher new product quality level and profit for the supply chain.

Second, we show that the contract mechanism to determine the ratio of the revenue or cost that the manufacturer shares with the supplier, based on the relationship between the two firms, affects the supply chain decisions and the performance of the new product development project. Thus, this study extends the findings of Baskaran and Krishnan [18], which considers only the cooperative relationship, and the findings of Wang and Shin [14], which considers only the unilateral relationship. When the manufacturer and the supplier collaboratively decide on the fraction of revenue or cost, the manufacturer’s profit is reduced, but the quality of the new product and the supply chain’s profit improve compared with the unilateral relationship. This finding demonstrates the positive effects of a cooperative relationship in a supply chain and suggests that it is worthwhile for manufacturers to consider a contract with suppliers that targets mutual growth for a successful new product development.

While we focus on a completely new product, technically or physically, some new products enter the market through the improvement and modification of existing products. In practice, electronic products, such as smartphones or laptops, are released as new products that have design modifications or quality improvements from previous versions. Therefore, a model that adopts a consumer utility function, including the surplus obtained from the use of existing products, will provide more comprehensive results; this will be tackled in future research. Furthermore, this paper restricted the analysis to two supply chain contracts in a supply chain consisting of two players. In reality, various contract types are used, such as a quality-dependent or a sharing contract considering revenue and cost simultaneously, and the supply chain can have multiple suppliers or manufacturers. Therefore, a model taking into account these issues would expand the practical implications of our research.

Author Contributions

Conceptualization, J.H. and P.L.; formal analysis, methodology, and validation, J.H.; writing–original draft preparation, J.H. and P.L.; writing–review and editing, P.L.; project administration, P.L.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Proof of Proposition 1.

(a) In Stage 1, by the first order condition, such that . By the second order condition, if , . Since , is the optimal solution to maximize . If is greater than 1, the sharing is not feasible. if and only if . Thus, when , the optimal revenue share is feasible.

(b) When , , , and . □

Proof of Proposition 2.

(a) In Stage 1, by the first order condition, such that . By the second order condition, . Because , the optimal cost sharing portion is 0. □

Proof of Proposition 3.

For such that , the supply chain profit difference between the revenue- and cost-sharing contracts, , is increasing in . . □

Proof of Proposition 4.

(a) We omit the solving process because it is similar to Proposition 1.

(b) When , , , and . □

Proof of Proposition 5.

For a revenue-sharing contract, if , , , , and is true. Thus, for such that , those are always true. □

Proof of Proposition 6.

(a) In Stage 1, by the first order condition, such that . By the second order condition, if , . Since , is the optimal solution to maximize . If , the sharing is not feasible. if and only if . Thus, when , the optimal cost share is feasible.

(b) When , , , and . □

References

- Marketing Insider. Categories of New Products—What Is a New Product? Available online: https://marketing-insider.eu/categories-of-new-products/ (accessed on 30 August 2019).

- The Verge. Apple Supplier Corning Is Working on Flexible Glass for Foldable Displays. Available online: https://www.theverge.com/2019/3/5/18251328/apple-corning-foldable-display-gorilla-glass-bendable-smartphone (accessed on 30 August 2019).

- Business Insider. 21 Incredible Facts about Elon Musk’s Gigafactory. Available online: https://www.businessinsider.com/tesla-gigafactory-facts-2016-9 (accessed on 13 November 2019).

- Caixin. Tesla Reaches Preliminary Battery-Supply Deal With CATL. Available online: https://www.caixinglobal.com/2019-11-06/tesla-reaches-preliminary-battery-supply-deal-with-catl-101479493.html (accessed on 13 November 2019).

- Cleverism. Managing Risks in Product Development. Available online: https://www.cleverism.com/managing-risks-in-product-development/ (accessed on 25 August 2019).

- Krishnan, V.; Ulrich, K.T. Product development decisions: A review of the literature. Manag. Sci. 2001, 47, 1–21. [Google Scholar] [CrossRef]

- Cvsa, V.; Gilbert, S.M. Strategic commitment versus postponement in a two-tier supply chain. Eur. J. Oper. Res. 2002, 141, 526–543. [Google Scholar] [CrossRef]

- Ulrich, K.T.; Ellison, D.J. Beyond make-buy: Internalization and integration of design and production. Prod. Oper. Manag. 2005, 14, 315–330. [Google Scholar] [CrossRef]

- Ülkü, S.; Toktay, L.B.; Yücesan, E. The impact of outsourced manufacturing on timing of entry in uncertain markets. Prod. Oper. Manag. 2005, 14, 301–314. [Google Scholar] [CrossRef]

- Novak, S.; Eppinger, S.D. Sourcing by design: Product complexity and the supply chain. Manag. Sci. 2001, 47, 189–204. [Google Scholar] [CrossRef]

- Pero, M.; Abdelkafi, N.; Sianesi, A.; Blecker, T. A framework for the alignment of new product development and supply chains. Supply Chain Manag. 2010, 15, 115–128. [Google Scholar] [CrossRef]

- Lin, Y.; Wang, Y.; Yu, C. Investigating the drivers of the innovation in channel integration and supply chain performance: A strategy orientated perspective. Int. J. Prod. Econ. 2010, 127, 320–332. [Google Scholar] [CrossRef]

- Gilbert, S.M.; Cvsa, V. Strategic commitment to price to stimulate downstream innovation in a supply chain. Eur. J. Oper. Res. 2003, 150, 617–639. [Google Scholar] [CrossRef]

- Wang, J.; Shin, H. The impact of contracts and competition on upstream innovation in a supply chain. Prod. Oper. Manag. 2015, 24, 134–146. [Google Scholar] [CrossRef]

- Dutta, S.; Weiss, A.M. The relationship between a firm’s level of technological innovativeness and its pattern of partnership agreements. Manag. Sci. 1997, 43, 343–356. [Google Scholar] [CrossRef]

- Ragatz, G.L.; Handfield, R.B.; Petersen, K.J. Benefits associated with supplier integration into new product development under conditions of technology uncertainty. J. Bus. Res. 2002, 55, 389–400. [Google Scholar] [CrossRef]

- Loch, C.H.; Terwiesch, C. Communication and uncertainty in concurrent engineering. Manag. Sci. 1998, 44, 1032–1048. [Google Scholar] [CrossRef]

- Bhaskaran, S.R.; Krishnan, V. Effort, revenue, and cost sharing mechanisms for collaborative new product development. Manag. Sci. 2009, 55, 1152–1169. [Google Scholar] [CrossRef]

- Cachon, G.P. Supply chain coordination with contracts. In Handbooks in Operations Research and Management Science; Elsevier: Amsterdam, The Netherlands, 2003; Volume 11, pp. 227–339. [Google Scholar]

- Cachon, G.P.; Lariviere, M.A. Supply chain coordination with revenue-sharing contracts: Strengths and limitations. Manag. Sci. 2005, 51, 30–44. [Google Scholar] [CrossRef]

- Wang, Y.; Jiang, L.; Shen, Z.J. Channel performance under consignment contract with revenue sharing. Manag. Sci. 2004, 50, 34–47. [Google Scholar] [CrossRef]

- Li, S.; Zhu, Z.; Huang, L. Supply chain coordination and decision making under consignment contract with revenue sharing. Int. J. Prod. Econ. 2009, 120, 88–99. [Google Scholar] [CrossRef]

- Pan, K.; Lai, K.K.; Leung, S.C.; Xiao, D. Revenue-sharing versus wholesale price mechanisms under different channel power structures. Eur. J. Oper. Res. 2010, 203, 532–538. [Google Scholar] [CrossRef]

- Leng, M.; Parlar, M. Game-theoretic analyses of decentralized assembly supply chains: Non-cooperative equilibria vs. coordination with cost-sharing contracts. Eur. J. Oper. Res. 2010, 204, 96–104. [Google Scholar] [CrossRef]

- Chao, G.H.; Iravani, S.M.; Savaskan, R.C. Quality improvement incentives and product recall cost sharing contracts. Manag. Sci. 2009, 55, 1122–1138. [Google Scholar] [CrossRef]

- Ma, P.; Shang, J.; Wang, H. Enhancing corporate social responsibility: Contract design under information asymmetry. Omega 2017, 67, 19–30. [Google Scholar] [CrossRef]

- Shin, H.; Collier, D.A.; Wilson, D.D. Supply management orientation and supplier/buyer performance. J. Oper. Manag. 2000, 18, 317–333. [Google Scholar] [CrossRef]

- Liker, J.K.; Choi, T.Y. Building deep supplier relationships. Harv. Bus. Rev. 2004, 82, 104–113. [Google Scholar]

- Zhao, Y.; Wang, S.; Cheng, T.E.; Yang, X.; Huang, Z. Coordination of supply chains by option contracts: A cooperative game theory approach. Eur. J. Oper. Res. 2010, 207, 668–675. [Google Scholar] [CrossRef]

- Zhang, J.; Liu, G.; Zhang, Q.; Bai, Z. Coordinating a supply chain for deteriorating items with a revenue sharing and cooperative investment contract. Omega 2015, 56, 37–49. [Google Scholar] [CrossRef]

- Petruzzi, N.C.; Dada, M. Pricing and the newsvendor problem: A review with extensions. Oper. Res. 1999, 47, 183–194. [Google Scholar] [CrossRef]

- Lariviere, M.A. Supply chain contracting and coordination with stochastic demand. In Quantitative Models for Supply Chain Management; Springer: Boston, MA, USA, 1999; pp. 233–268. [Google Scholar]

- Yao, Z.; Leung, S.C.; Lai, K.K. Manufacturer’s revenue-sharing contract and retail competition. Eur. J. Oper. Res. 2008, 186, 637–651. [Google Scholar] [CrossRef]

- Chen, L.; Peng, J.; Liu, Z.; Zhao, R. Pricing and effort decisions for a supply chain with uncertain information. Int. J. Prod. Res. 2017, 55, 264–284. [Google Scholar] [CrossRef]

- Hotelling, H. Stability in competition. Econ. J. 1929, 39, 41–57. [Google Scholar] [CrossRef]

- Iansiti, M. Shooting the rapids: Managing product development in turbulent environments. Calif. Manag. Rev. 1995, 38, 37–58. [Google Scholar] [CrossRef]

- Krishnan, V.; Bhattacharya, S. Technology selection and commitment in new product development: The role of uncertainty and design flexibility. Manag. Sci. 2002, 48, 313–327. [Google Scholar] [CrossRef]

- Li, G.; Rajagopalan, S. Process improvement, learning, and real options. Prod. Oper. Manag. 2008, 17, 61–74. [Google Scholar] [CrossRef]

- Mussa, M.; Rosen, S. Monopoly and product quality. J. Econ. Theory 1978, 18, 301–317. [Google Scholar] [CrossRef]

- Moorthy, K.S.; Png, I.P. Market segmentation, cannibalization, and the timing of product introductions. Manag. Sci. 1992, 38, 345–359. [Google Scholar] [CrossRef] [Green Version]

- Desai, P.S. Quality segmentation in spatial markets: When does cannibalization affect product line design? Mark. Sci. 2001, 20, 265–283. [Google Scholar] [CrossRef] [Green Version]

- Besanko, D.; Winston, W.L. Optimal price skimming by a monopolist facing rational consumers. Manag. Sci. 1990, 36, 555–567. [Google Scholar] [CrossRef]

- Dhebar, A. Durable-goods monopolists, rational consumers, and improving products. Mark. Sci. 1994, 13, 100–120. [Google Scholar] [CrossRef]

- Bhattacharya, S.; Krishnan, V.; Mahajan, V. Operationalizing technology improvements in product development decision-making. Eur. J. Oper. Res. 2003, 149, 102–130. [Google Scholar] [CrossRef]

- Biyalogorsky, E.; Koenigsberg, O. The design and introduction of product lines when consumer valuations are uncertain. Prod. Oper. Manag. 2014, 23, 1539–1548. [Google Scholar] [CrossRef]

- Nash, J., Jr. The bargaining problem. Econometrica 1950, 18, 155–162. [Google Scholar] [CrossRef]

- Nash, J., Jr. Two-person cooperative games. Econometrica 1953, 21, 128–140. [Google Scholar] [CrossRef]

Figure 1.

Decision-making sequence.

Figure 2.

(a) Quality level of the new product and (b) supplier’s profit under a cooperative relationship.

Figure 2.

(a) Quality level of the new product and (b) supplier’s profit under a cooperative relationship.

Figure 3.

Manufacturer’s profit under a cooperative relationship.

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hong, J.; Lee, P. Supply Chain Contracts under New Product Development Uncertainty. Sustainability 2019, 11, 6858. https://0-doi-org.brum.beds.ac.uk/10.3390/su11236858

AMA Style

Hong J, Lee P. Supply Chain Contracts under New Product Development Uncertainty. Sustainability. 2019; 11(23):6858. https://0-doi-org.brum.beds.ac.uk/10.3390/su11236858

Chicago/Turabian StyleHong, Jihyun, and Pyoungsoo Lee. 2019. "Supply Chain Contracts under New Product Development Uncertainty" Sustainability 11, no. 23: 6858. https://0-doi-org.brum.beds.ac.uk/10.3390/su11236858

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.