Quantitative Estimation and Spatiotemporal Characteristic Analysis of Price Deviation in China's Housing Market

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

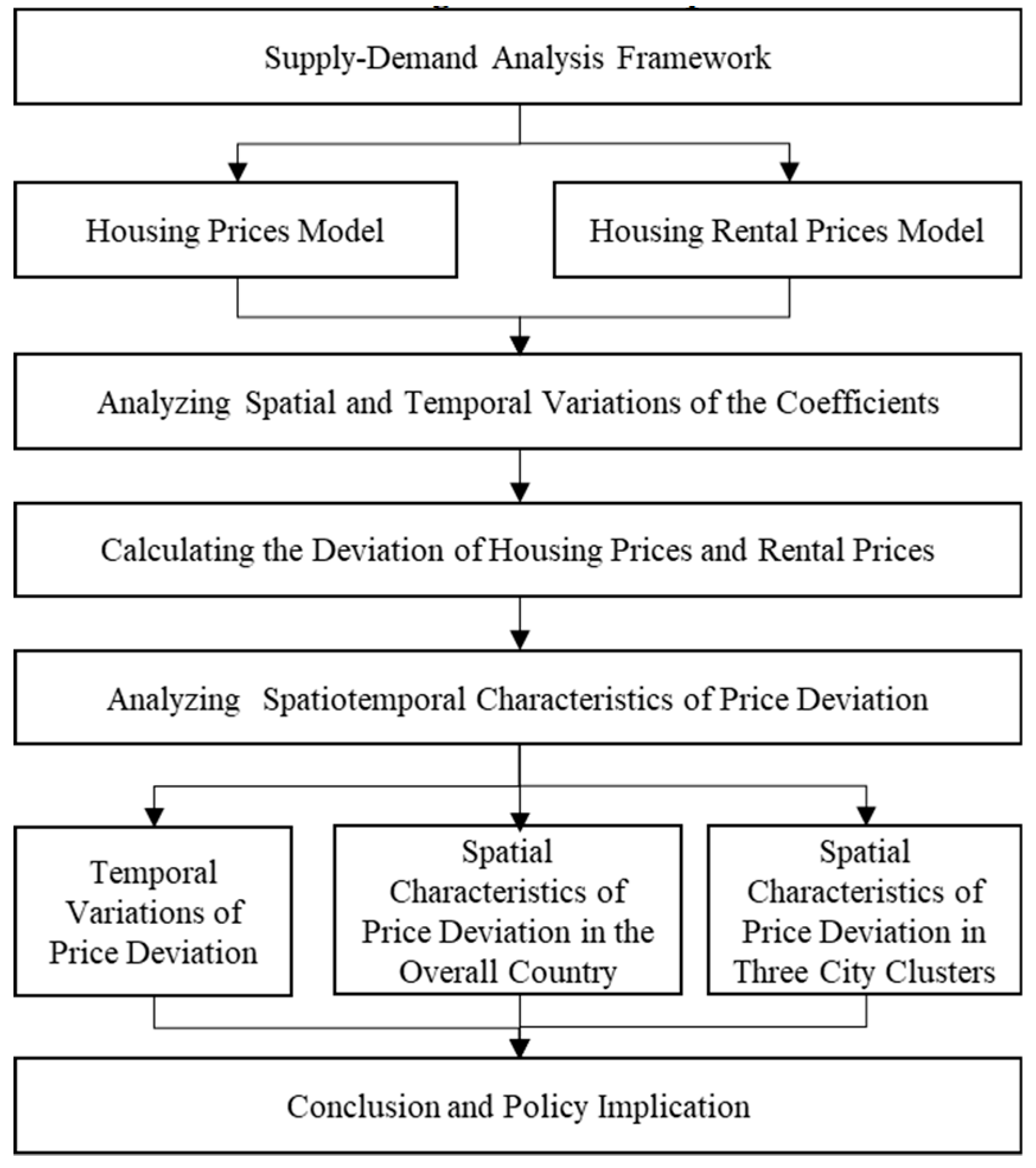

3.1. Research Process

3.2. Method of Price Deviation Estimation

3.3. Geographically and Temporally Weighted Regression Model

3.4. Empirical Analysis Framework and Model

3.5. Data

4. Results and Discussions

4.1. Model Comparison

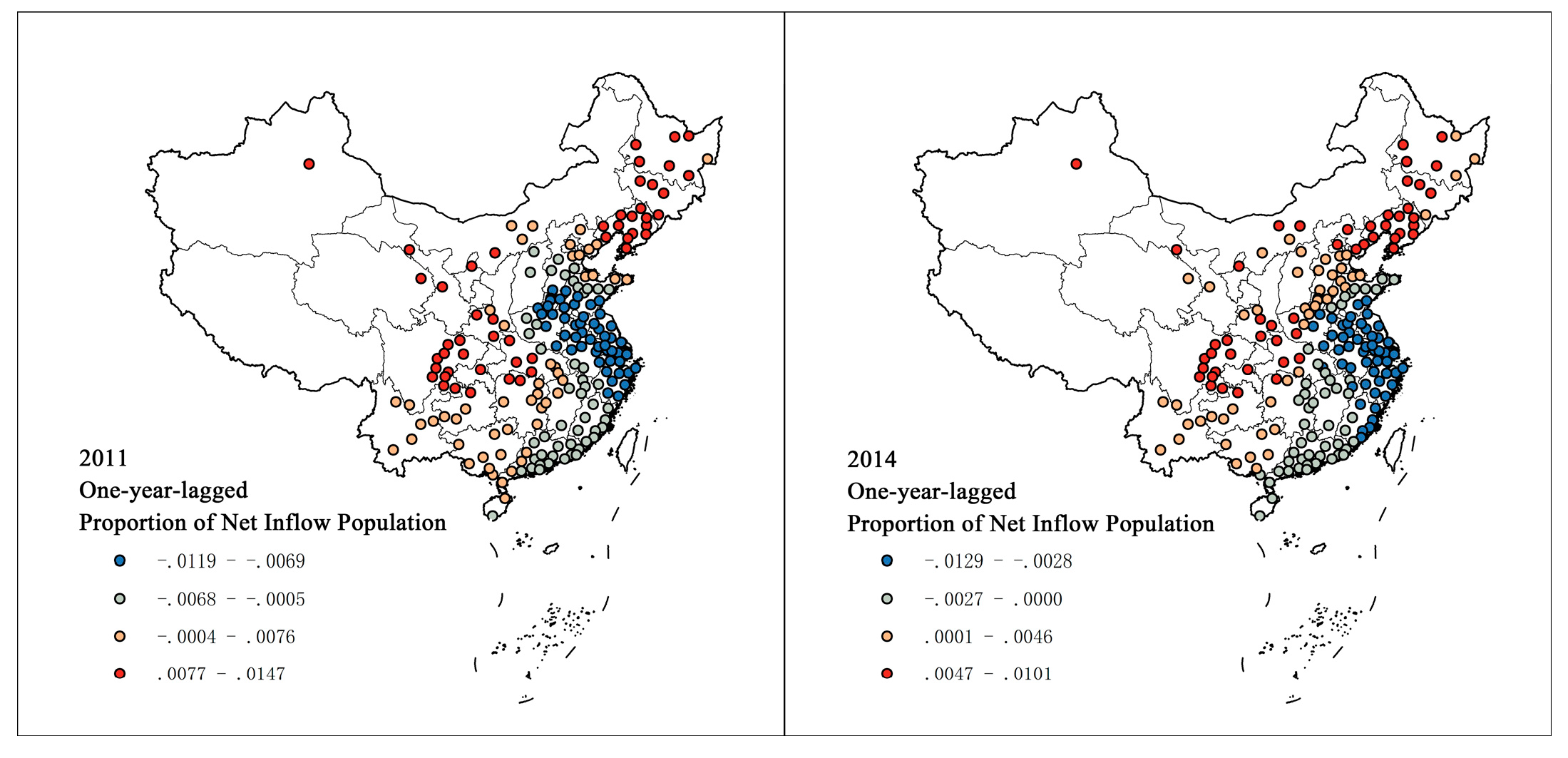

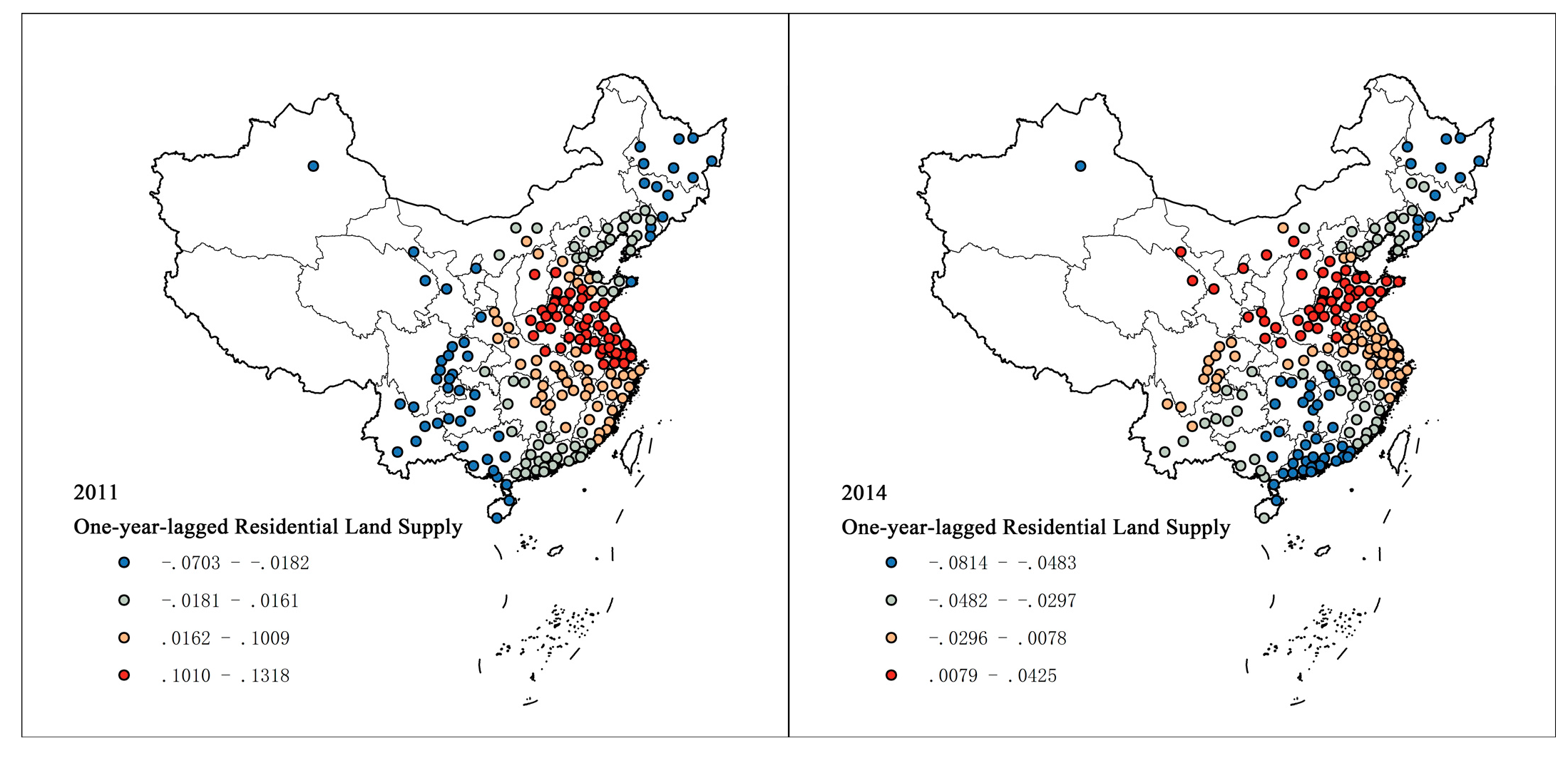

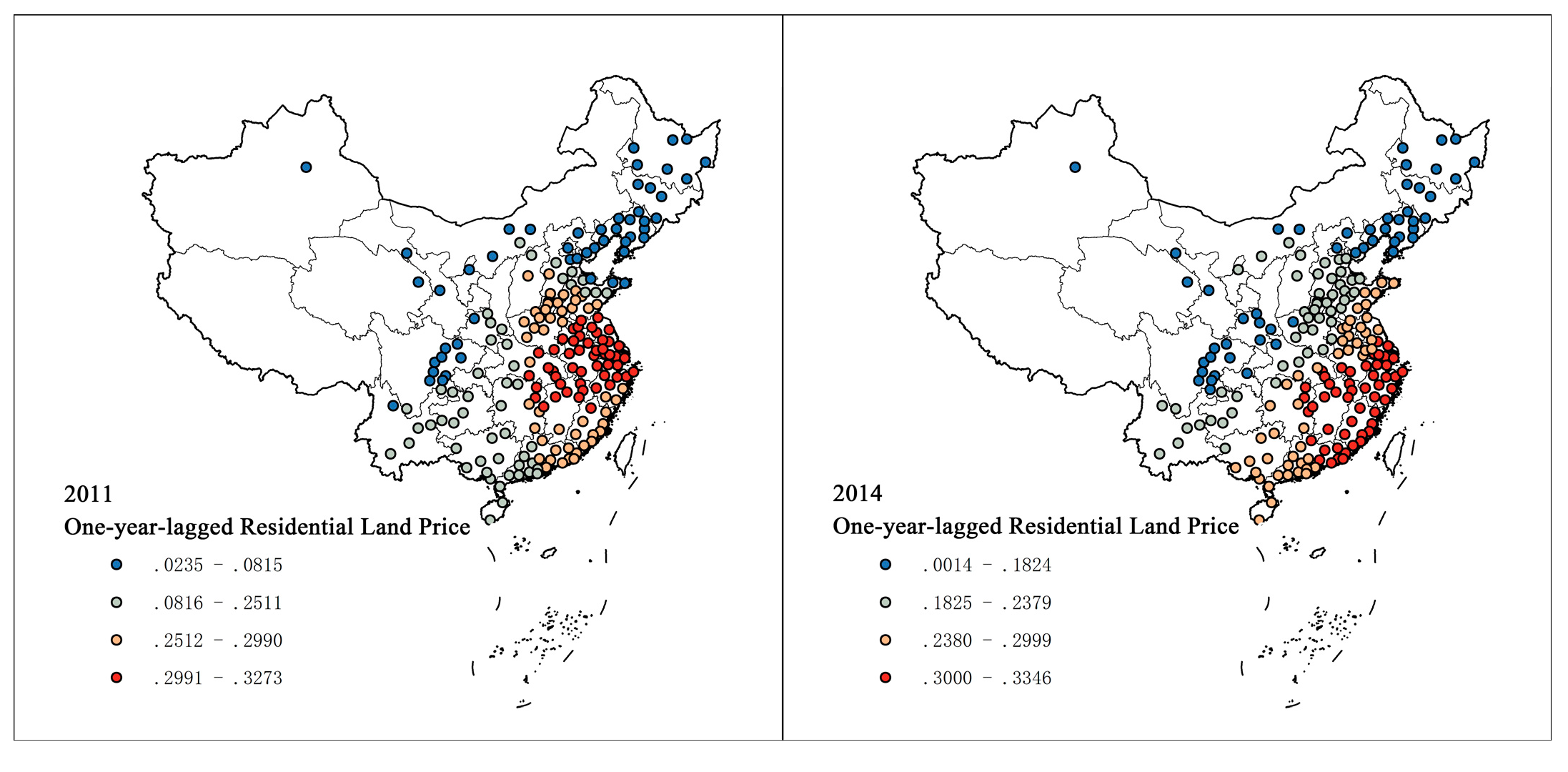

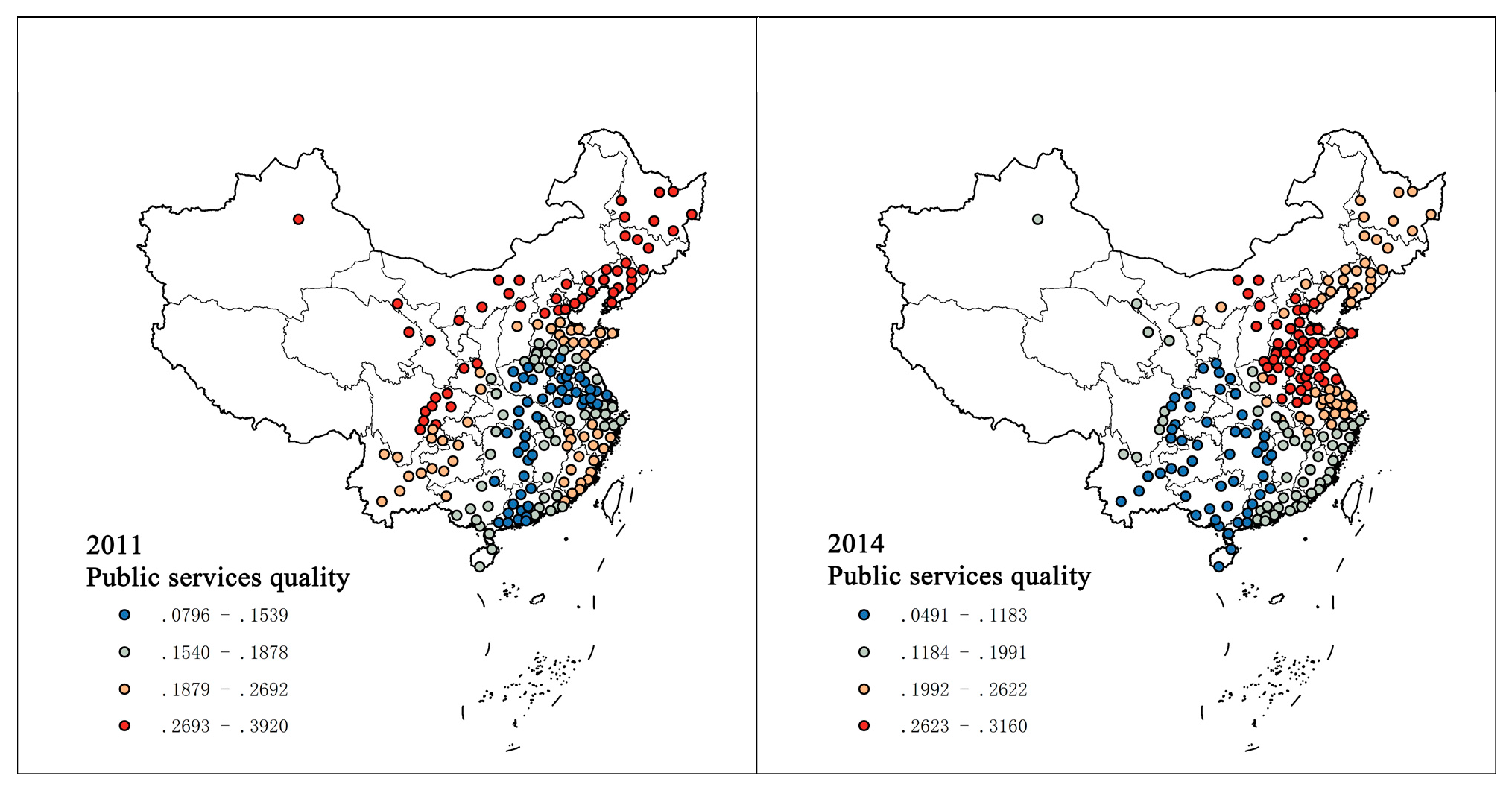

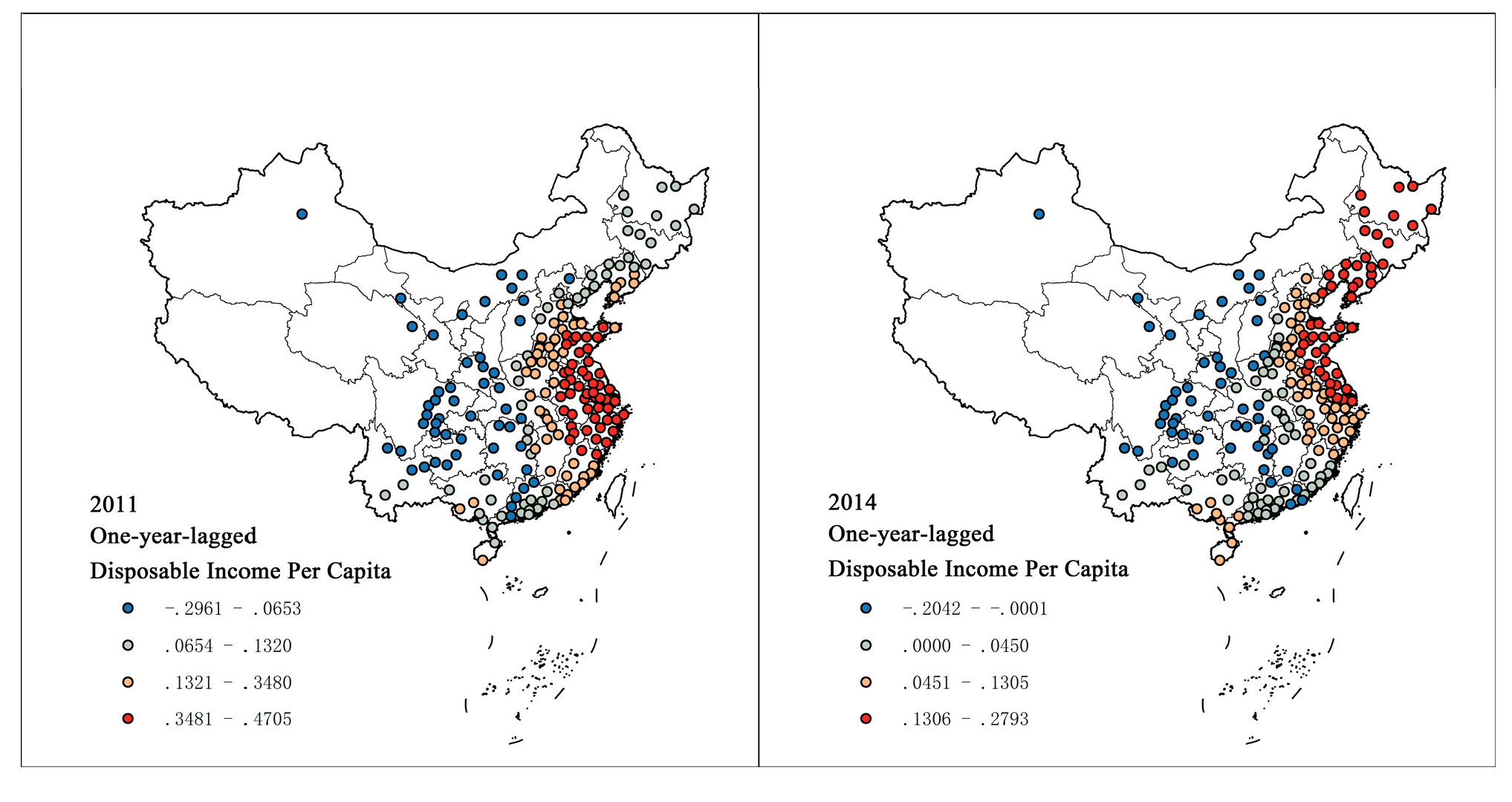

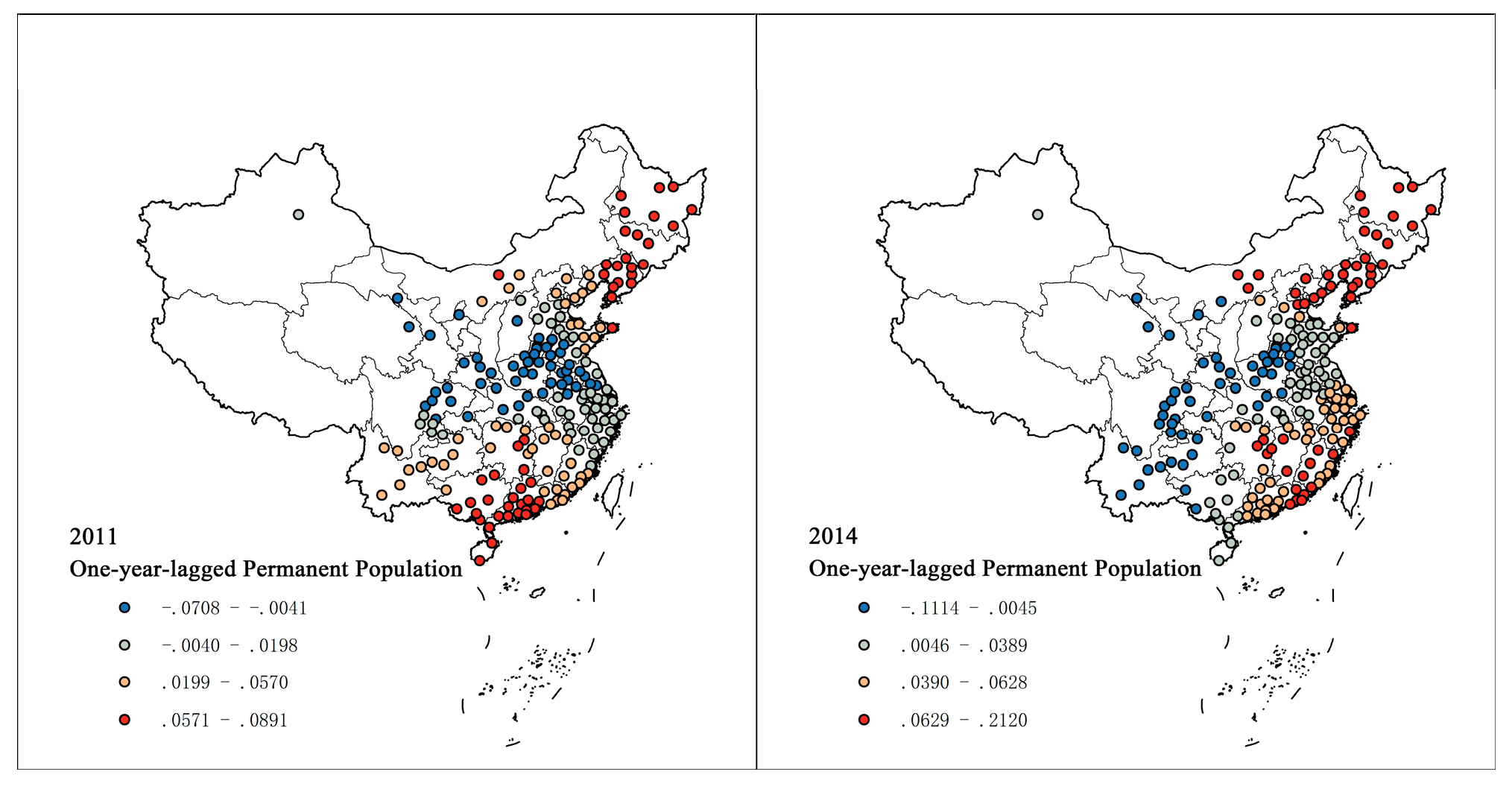

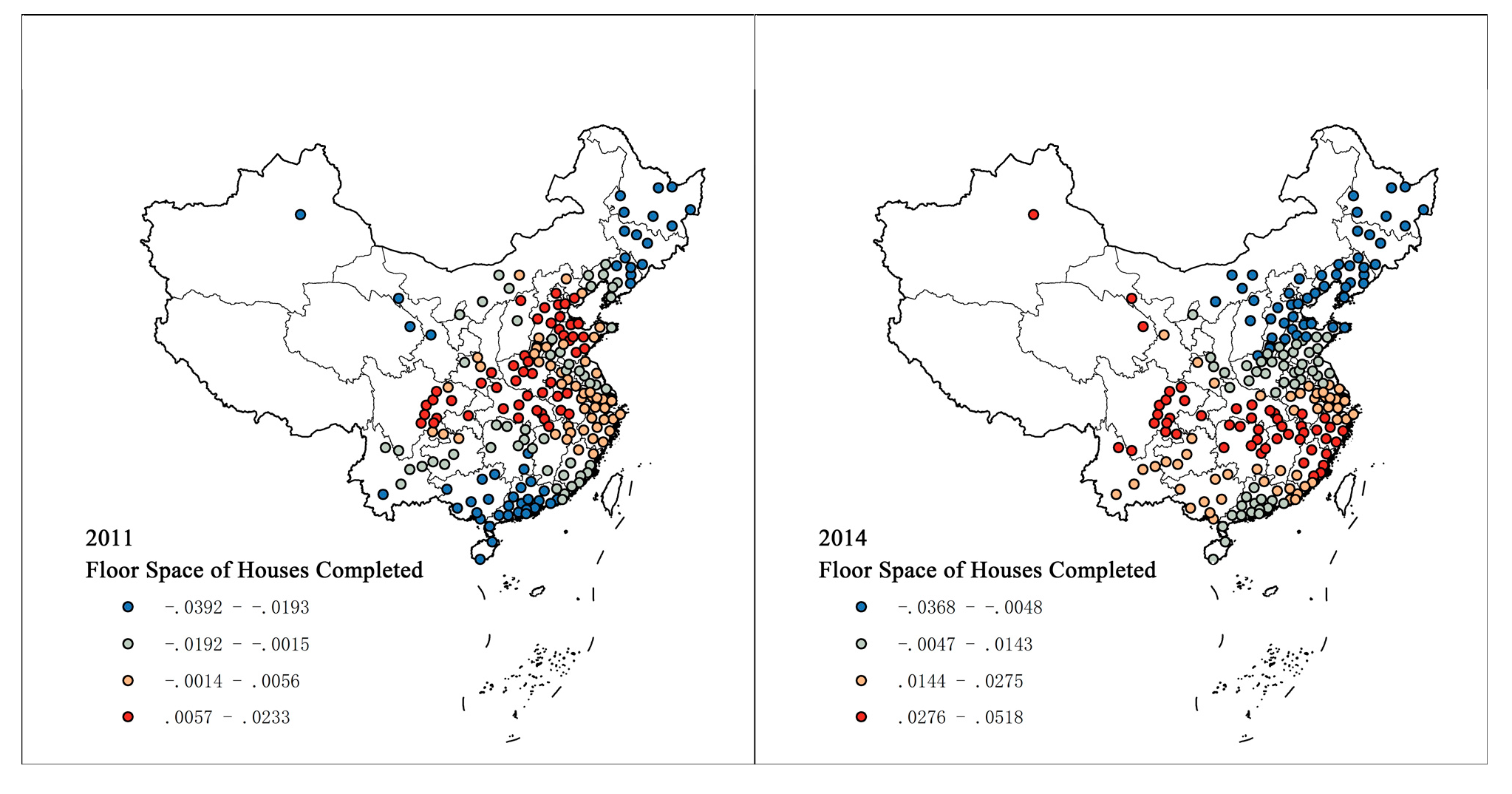

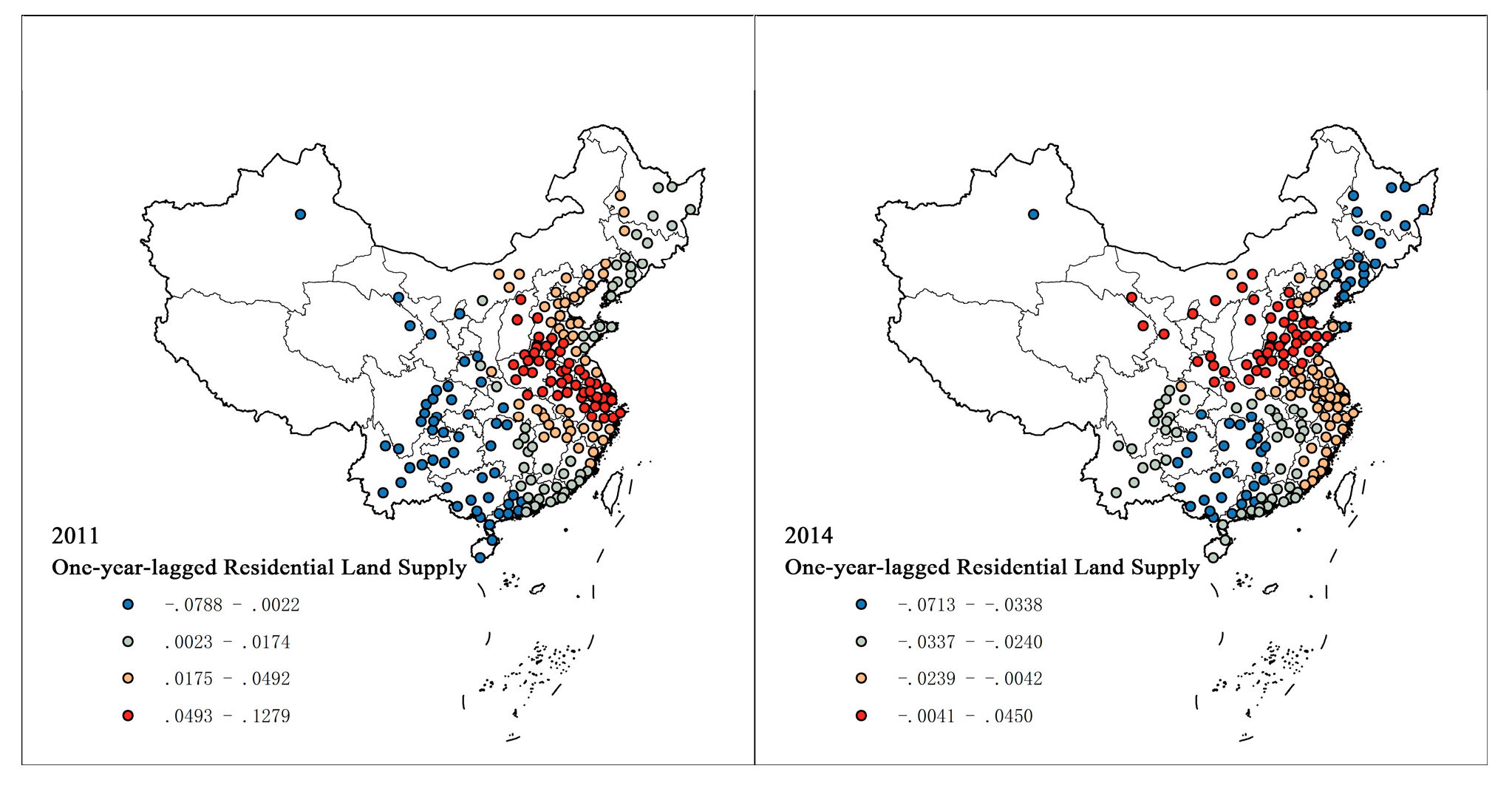

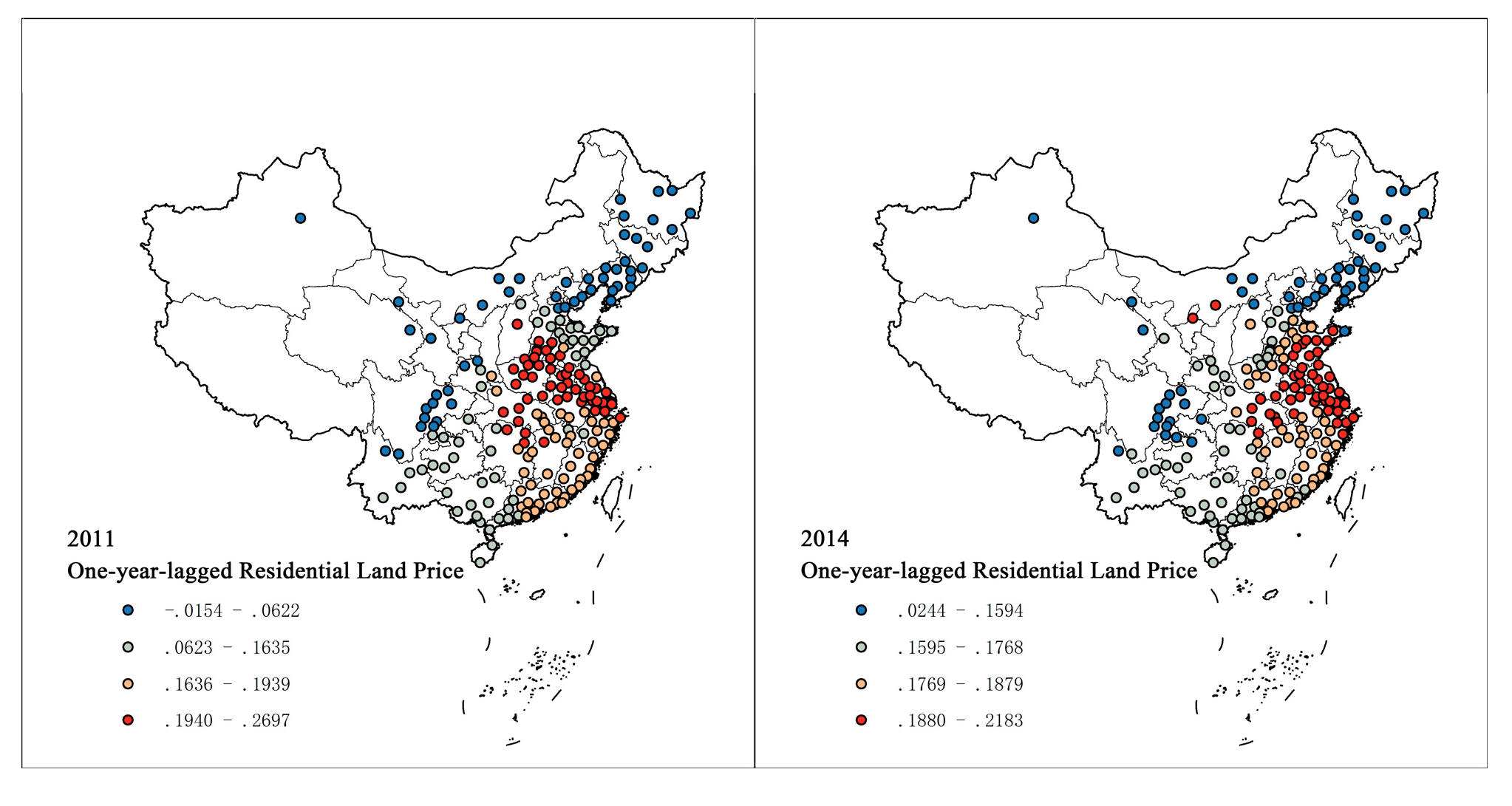

4.2. Spatial and Temporal Variations of the Coefficients

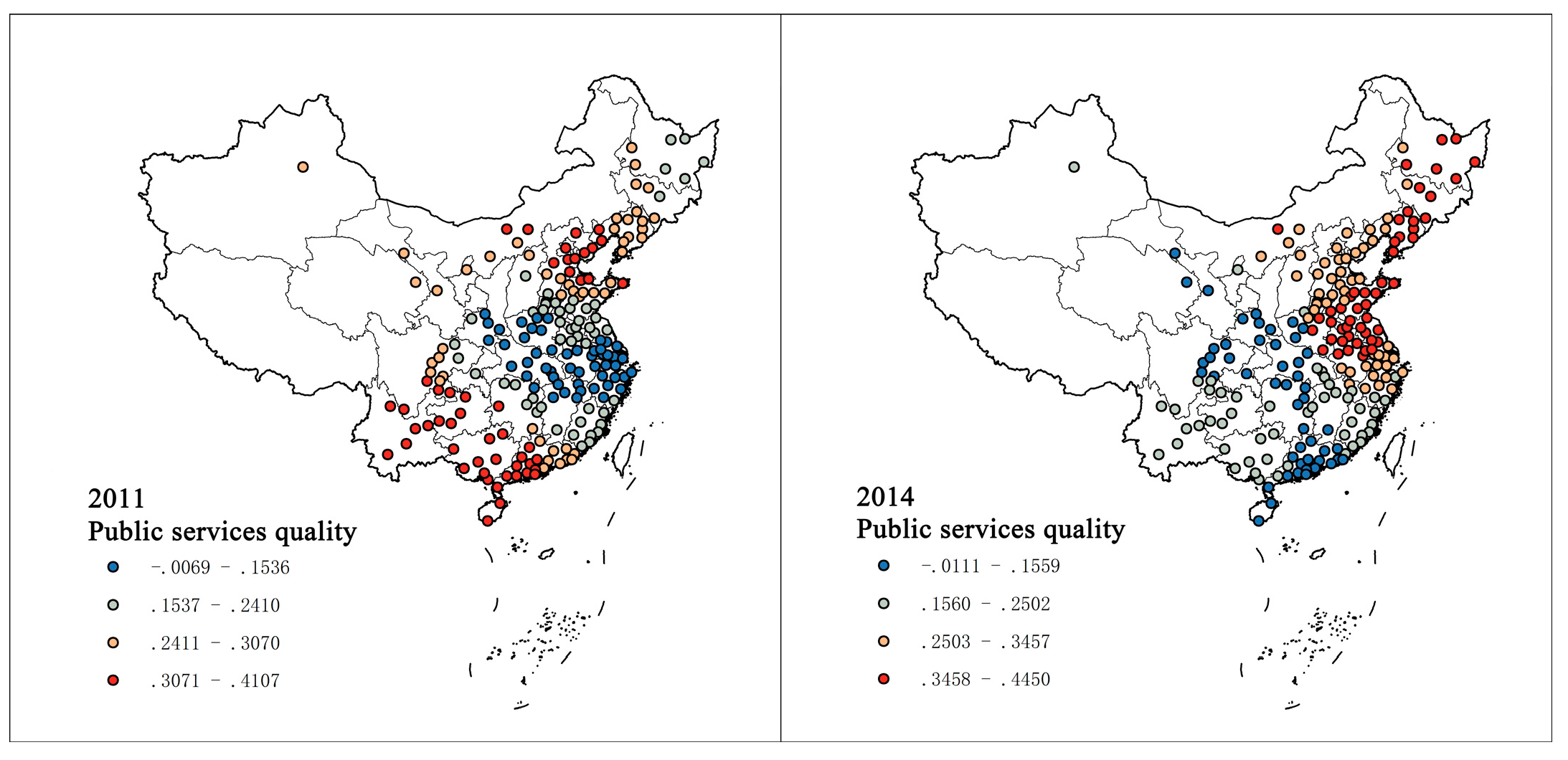

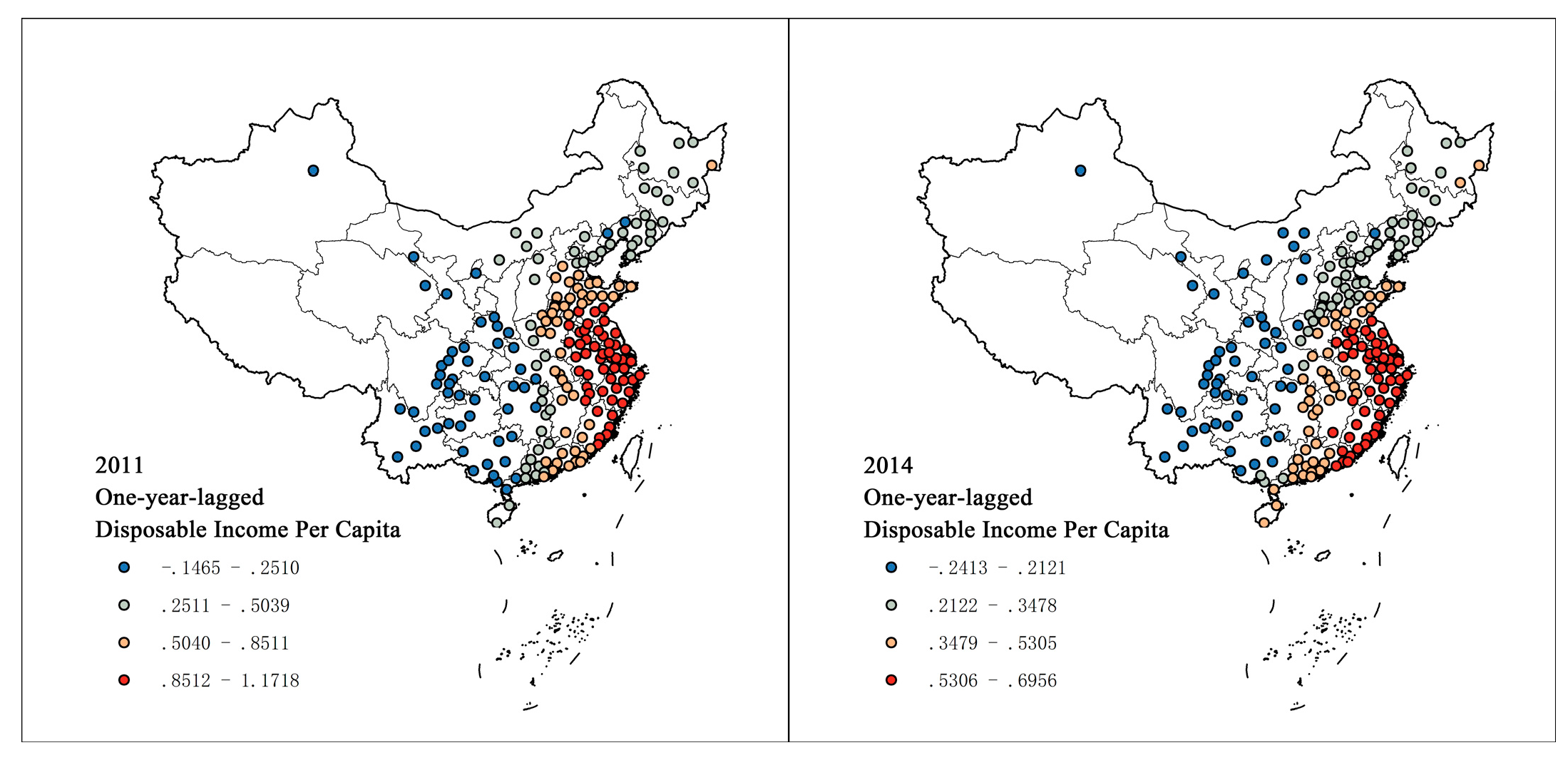

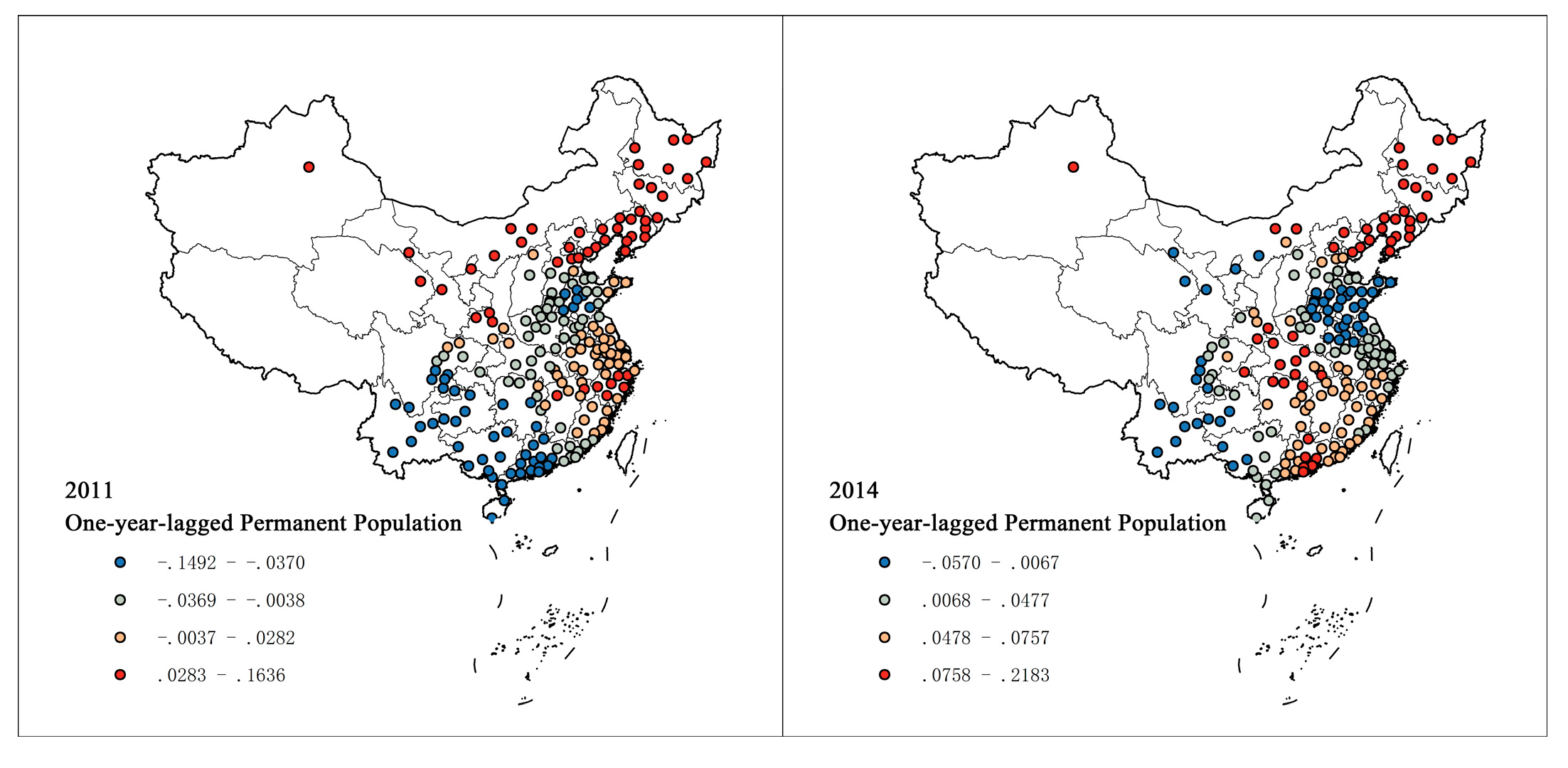

4.2.1. Variables Affecting Housing Prices

4.2.2. Variables Affecting Housing Rental prices

4.3. Analysis of the Spatiotemporal Characteristics of Price Deviations based on the Overall Country

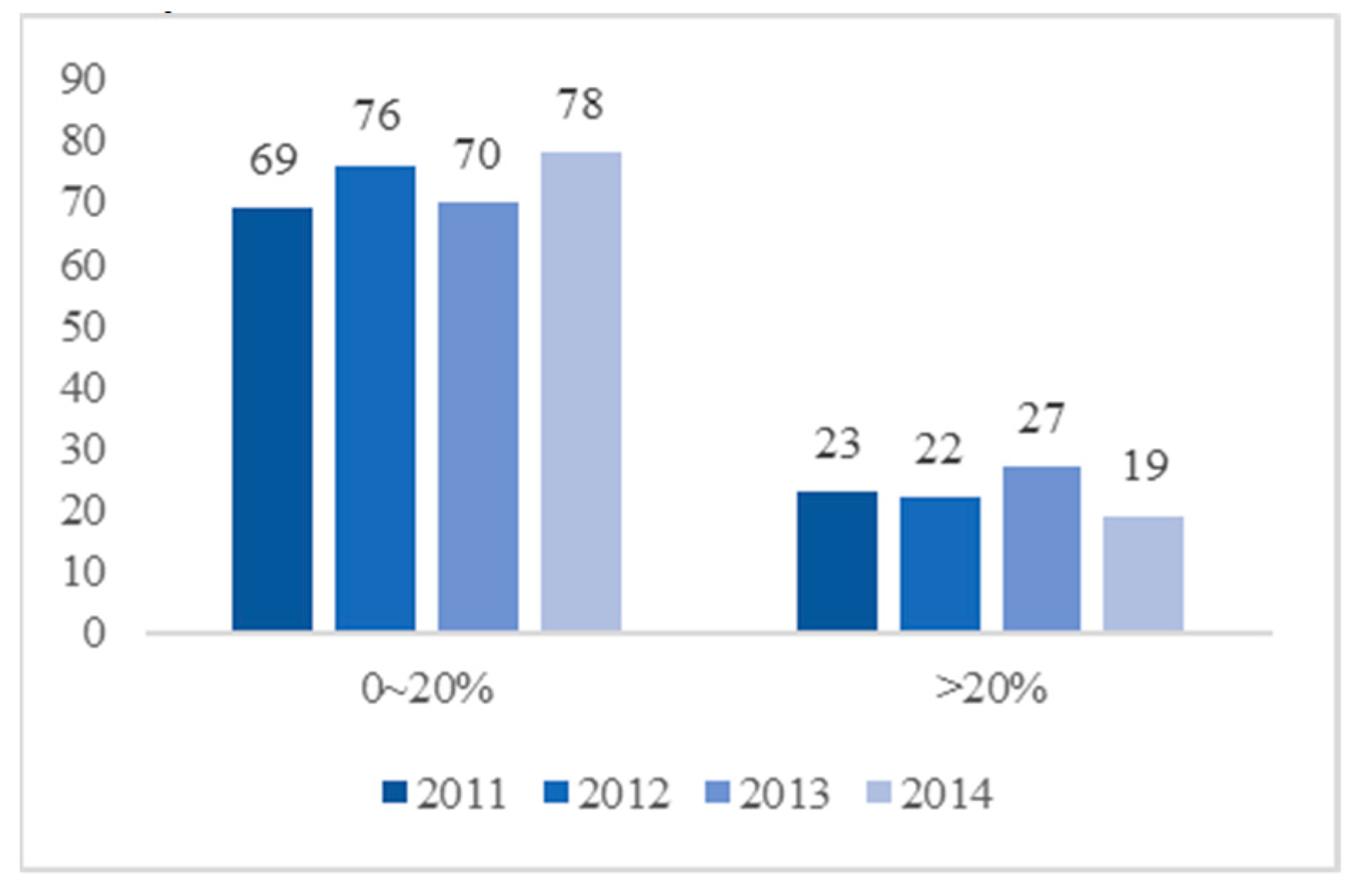

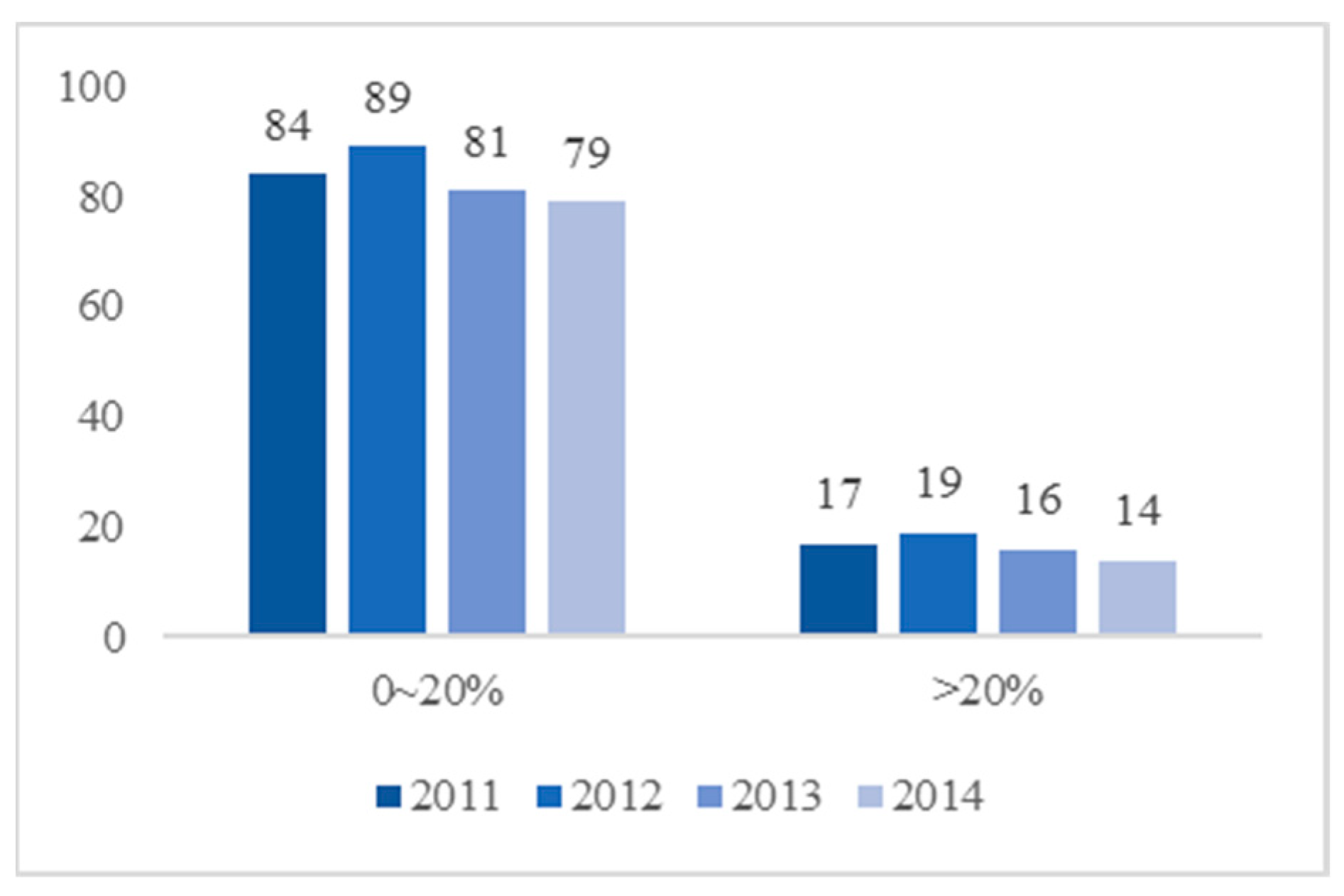

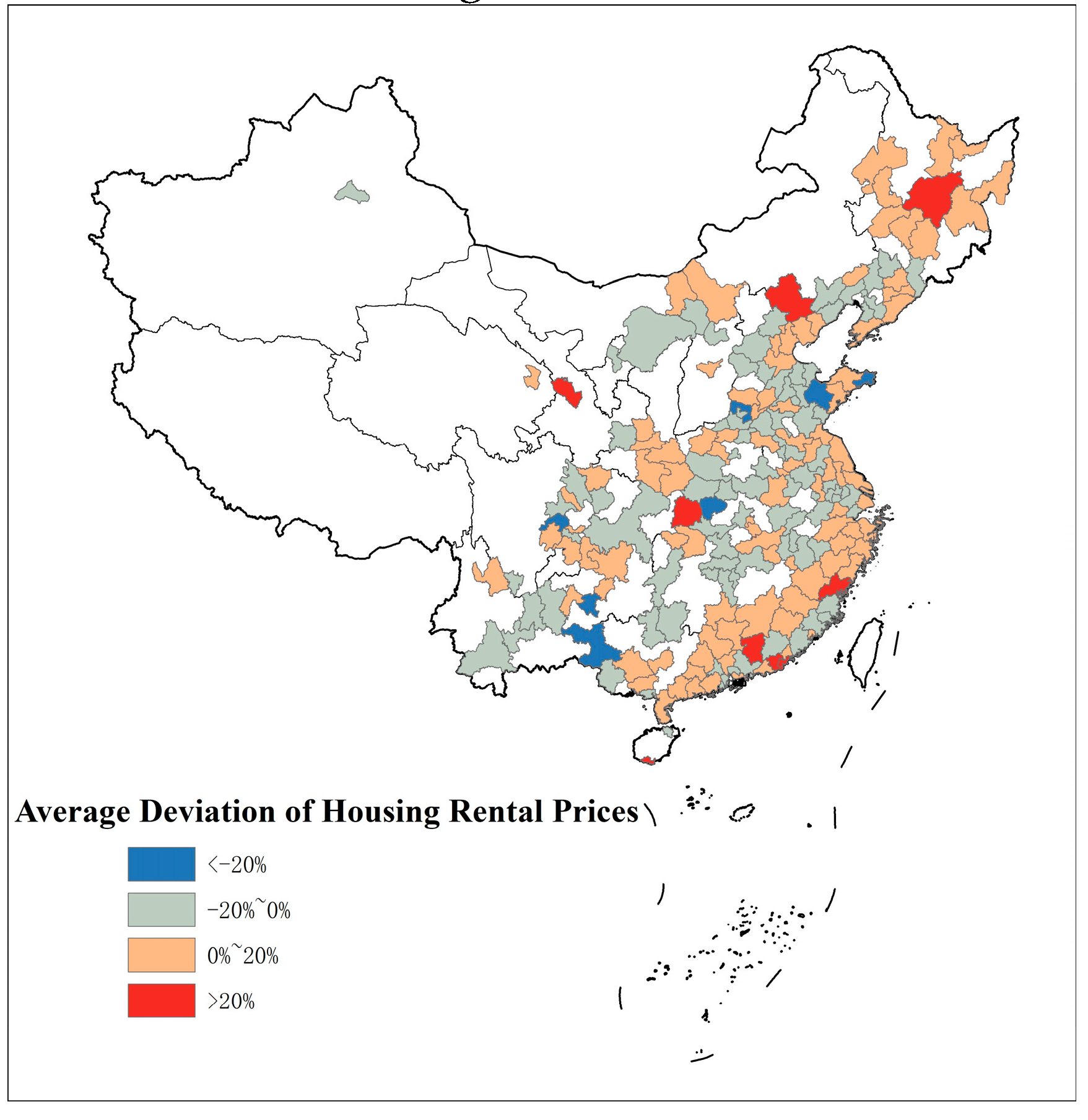

4.3.1. Temporal Variations of Price Deviations

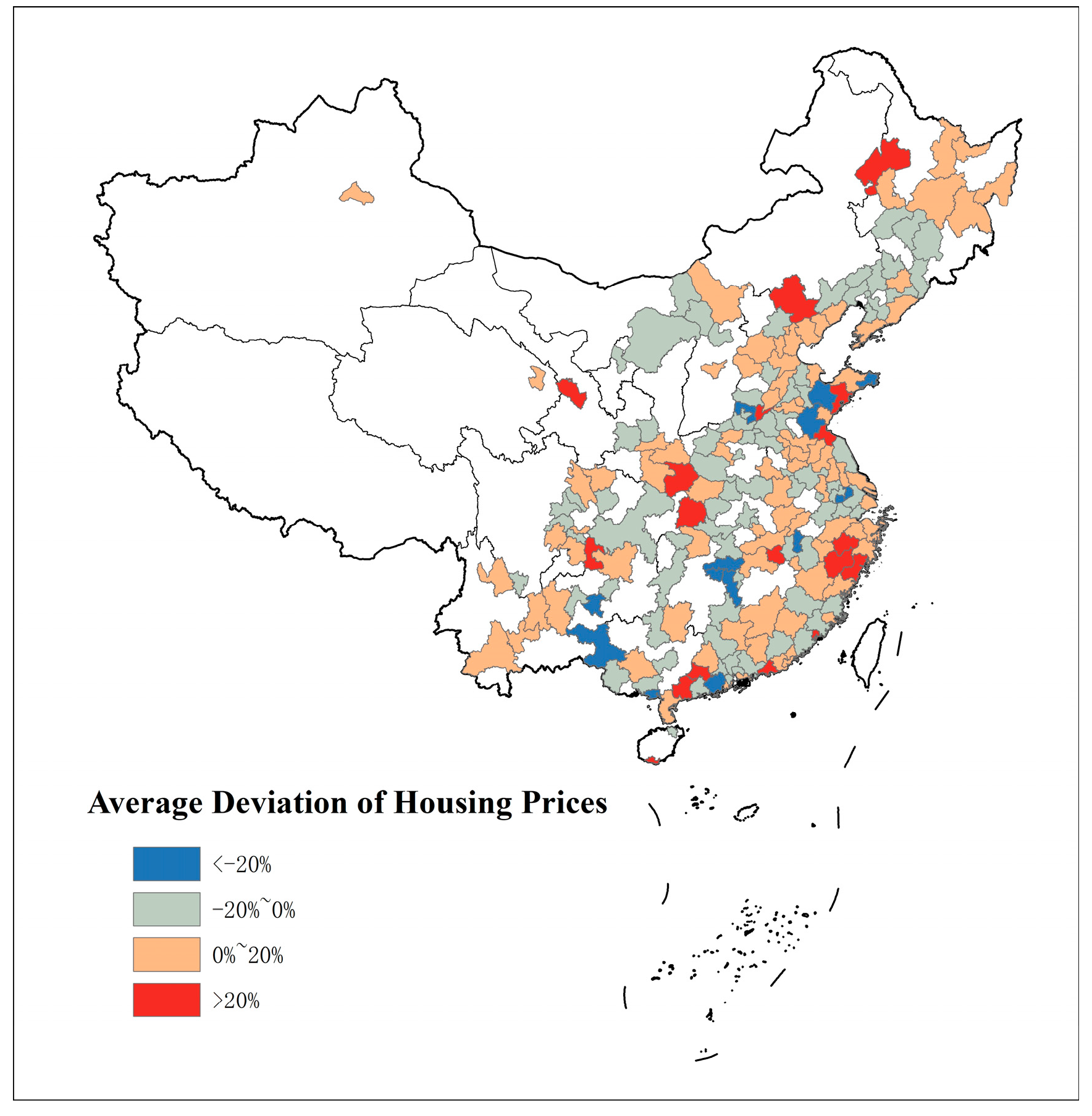

4.3.2. Spatial Characteristics of Price Deviations

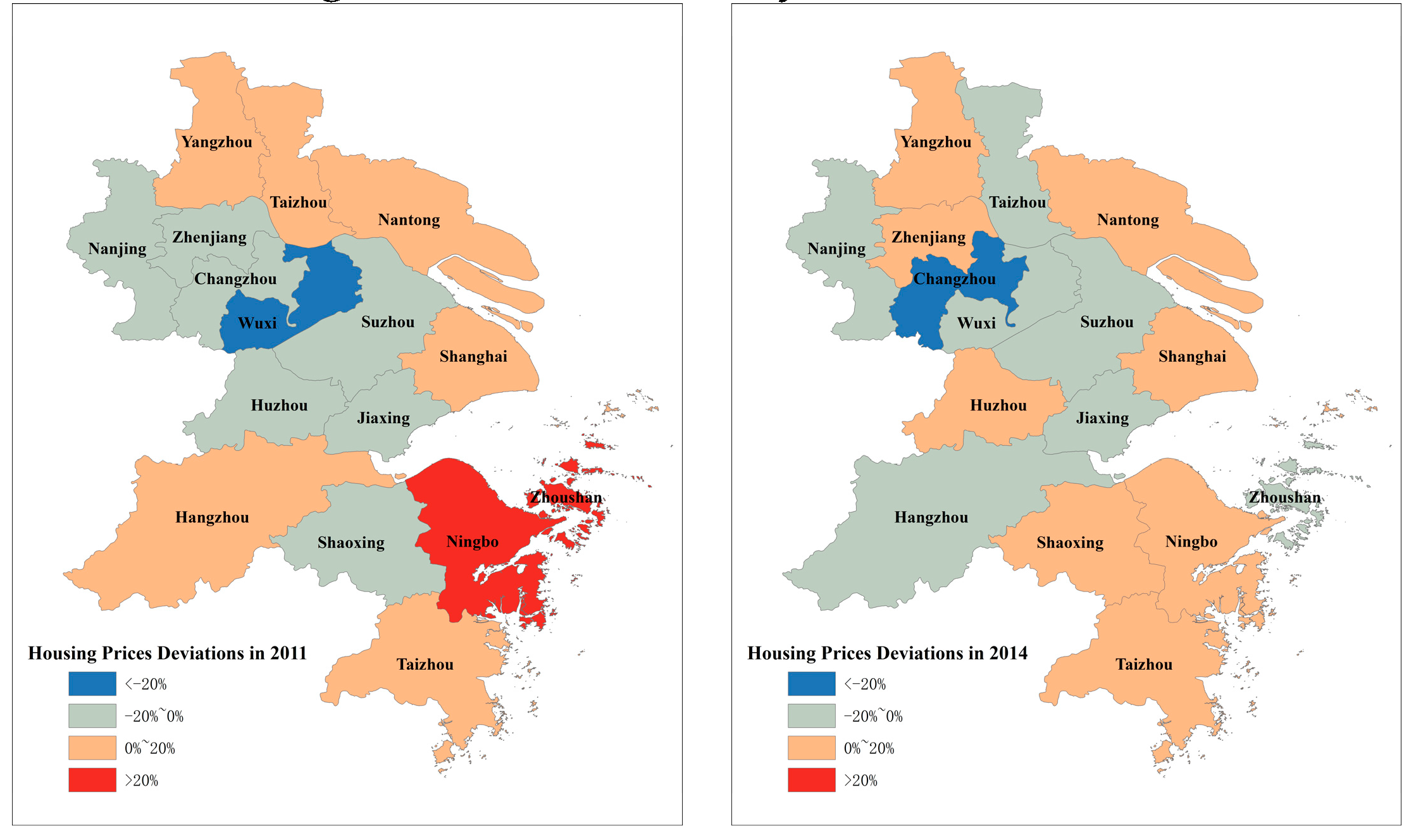

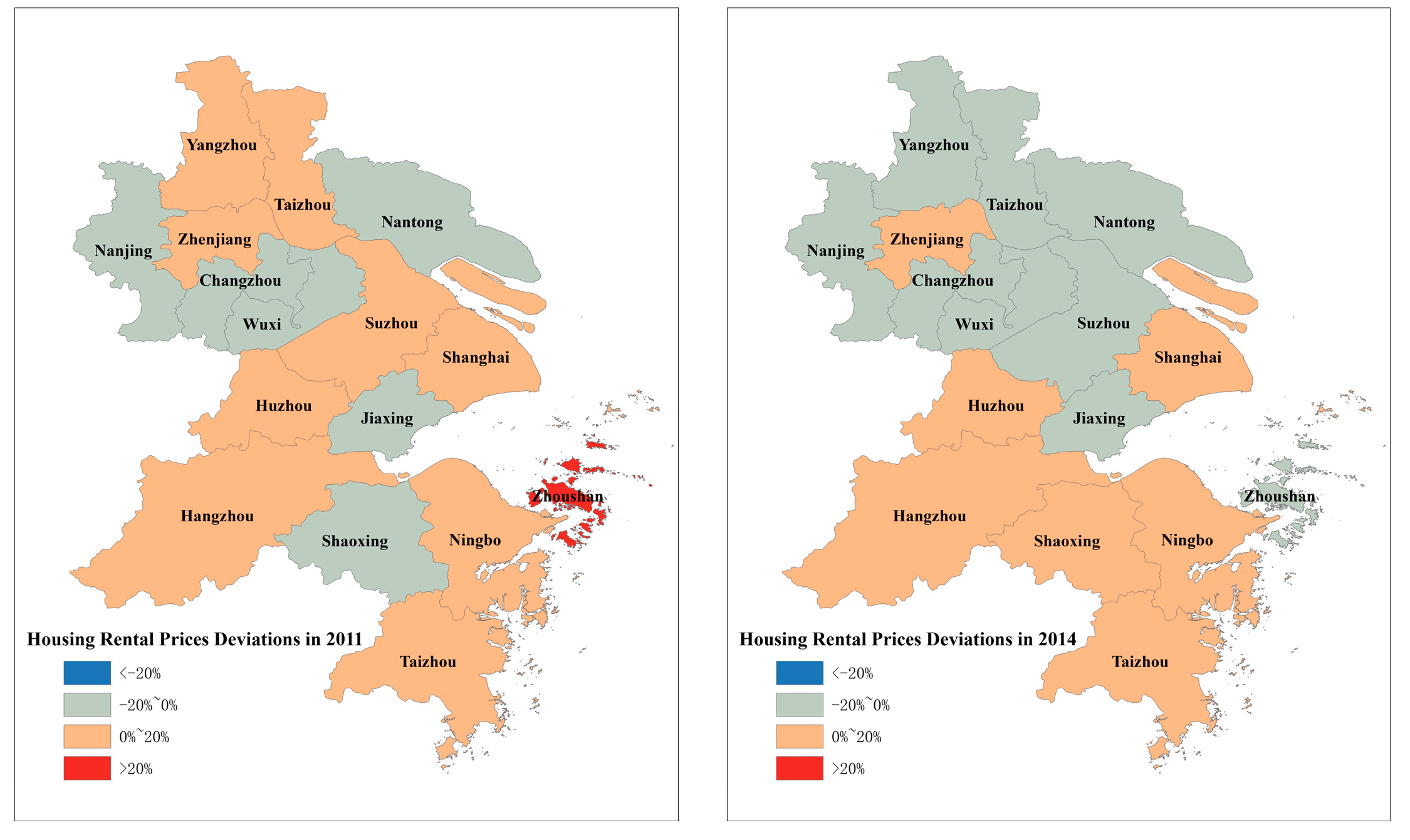

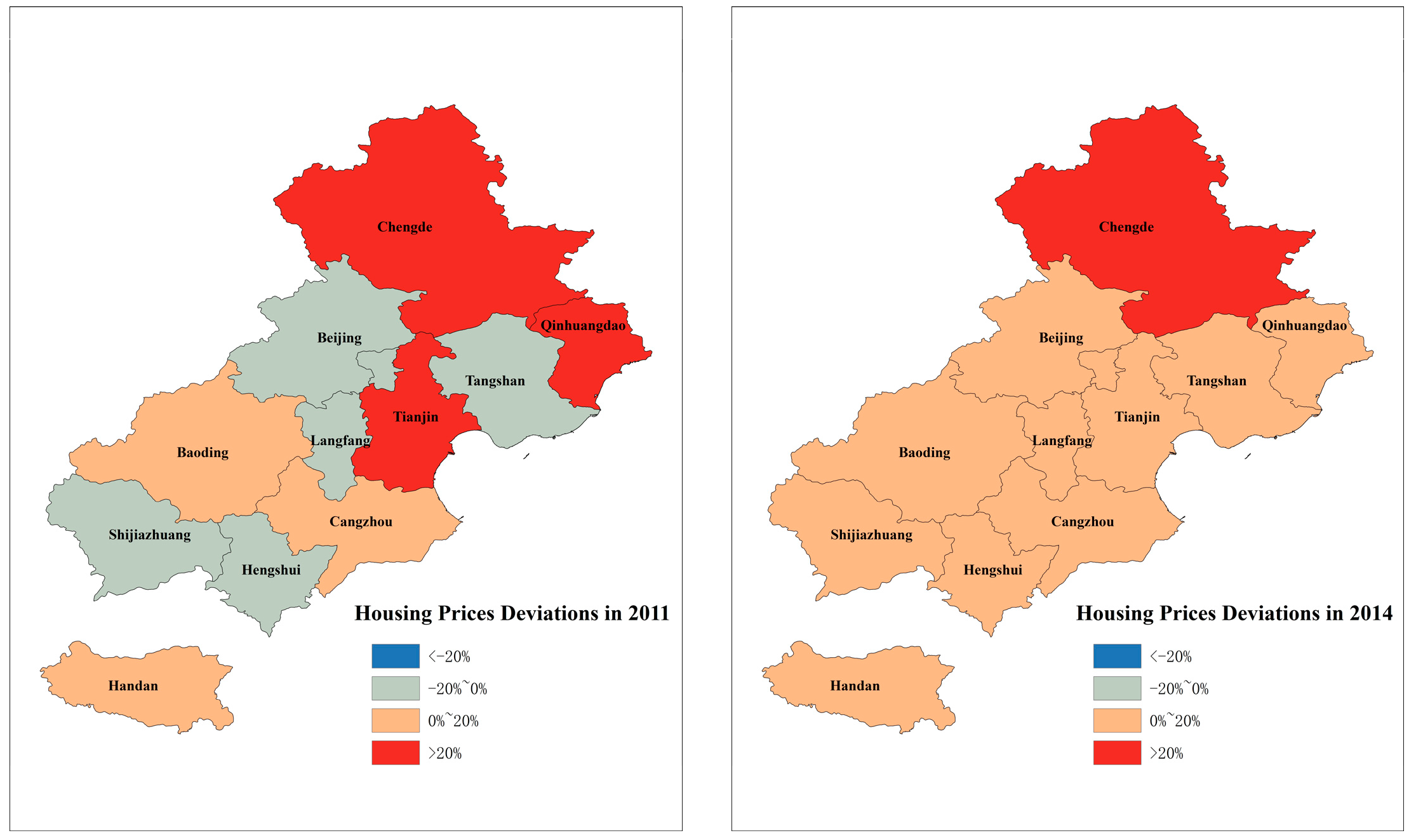

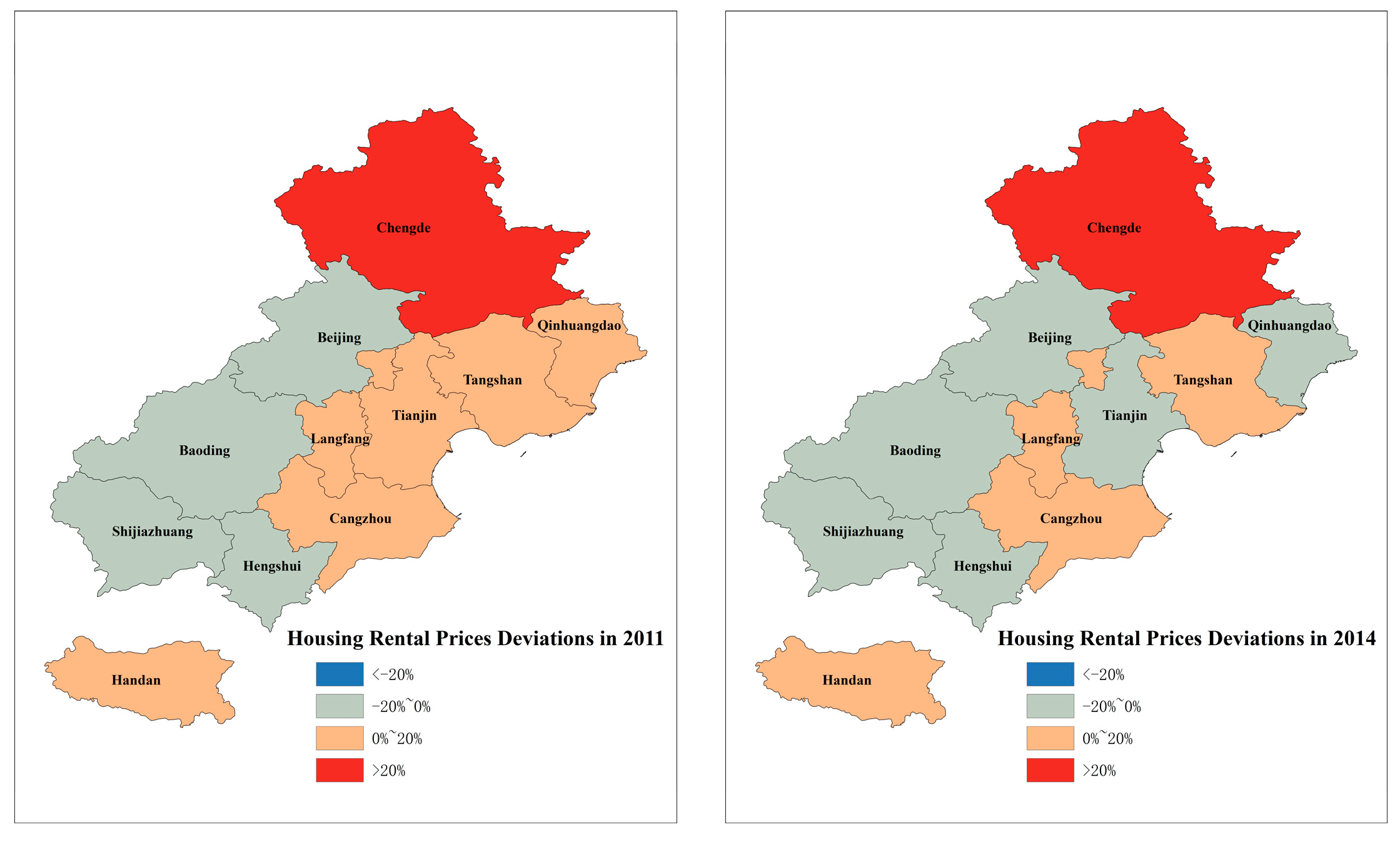

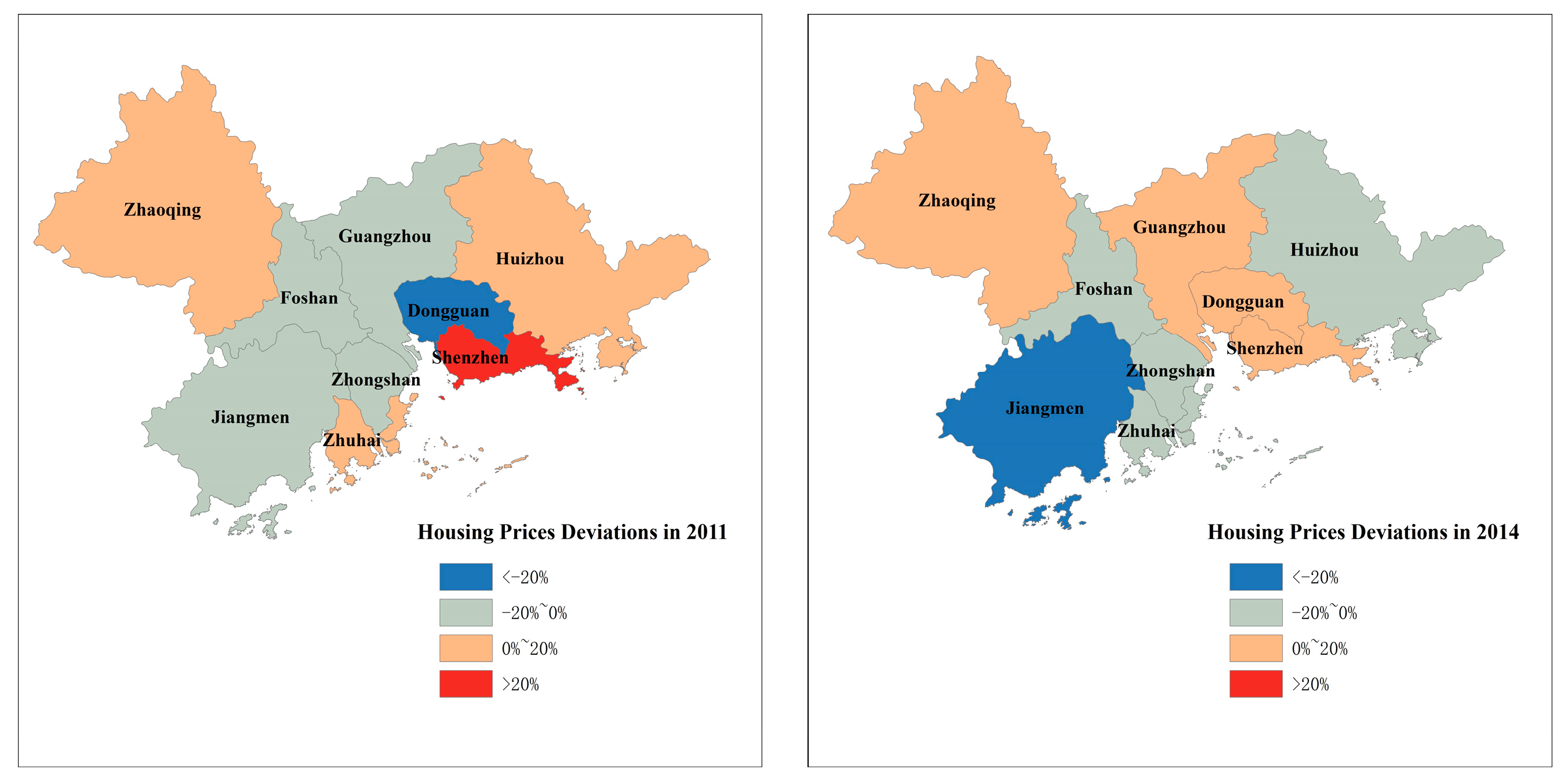

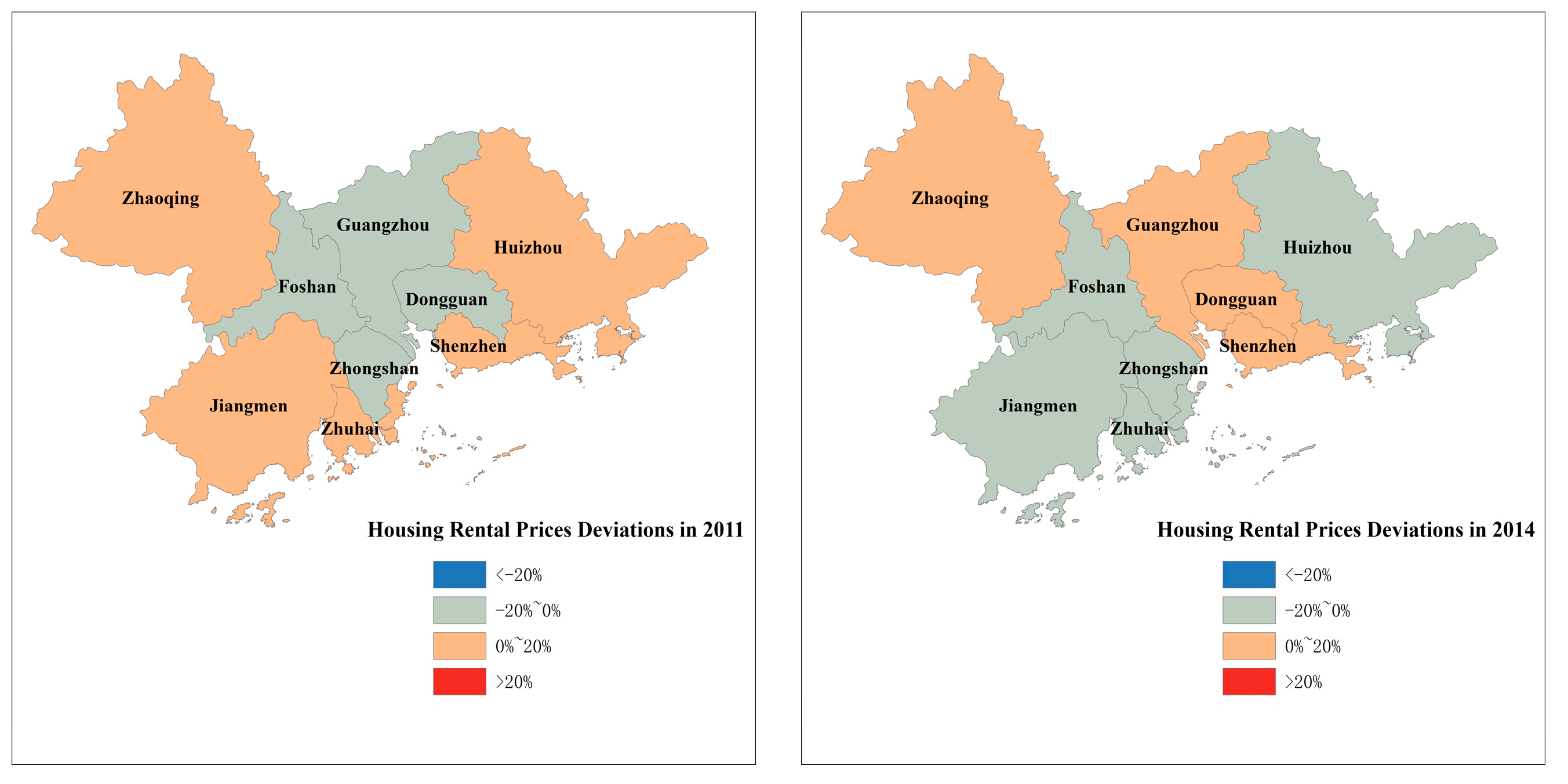

4.4. Analysis of the Spatiotemporal Characteristics of Price Deviations based on Three City Clusters

5. Conclusions and Implication

5.1. Main Conclusions

5.2. Policy Implications

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Indexes | Obs. | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| The number of Primary Schools | 1,010 | 718.91 | 637.45 | 57.00 | 5544.00 |

| The number of Regular Secondary Schools | 1,010 | 227.10 | 141.29 | 42.00 | 1273.00 |

| The number of Regular Institutions of Higher Education | 1,010 | 10.79 | 16.62 | 0.00 | 91.00 |

| Teacher-student Ratio in Primary Schools | 1,010 | 0.06 | 0.02 | 0.03 | 0.49 |

| Teacher-student Ratio in Regular Secondary Schools | 1,010 | 0.08 | 0.02 | 0.04 | 0.19 |

| Expenditure for Education per capita | 1,010 | 1118.71 | 472.92 | 77.06 | 4377.01 |

| Number of Hospitals and Health Centres per 10000 Persons | 1,010 | 0.49 | 0.54 | 0.09 | 11.80 |

| Number of Beds of Hospitals and Health Centres per 10000 Persons | 1,010 | 40.41 | 11.16 | 12.35 | 83.49 |

| Number of Doctors per 10000 Persons | 1,010 | 20.10 | 7.09 | 1.74 | 72.38 |

| Number of Public Transportation Vehicles per 10000 persons | 1,010 | 8.94 | 8.28 | 0.79 | 110.52 |

| Length of Lines of Urban Rail Transit System (completed and under construction) | 1,010 | 21.26 | 80.17 | 0.00 | 748.05 |

| Number of Theatres, Music Halls and Cinemas per 10000 Persons | 1,010 | 0.05 | 0.12 | 0.00 | 1.00 |

| Collections of Public Libraries per 100 Persons | 1,010 | 64.87 | 106.31 | 1.74 | 1438.59 |

| Area of Parks and Green Land | 1,010 | 1893.80 | 3064.60 | 64.00 | 26910.00 |

| Green Covered Area as % of Completed Area | 1,010 | 40.05 | 7.39 | 0.36 | 95.25 |

| KMO | Derived Principal Components | |||||

|---|---|---|---|---|---|---|

| F1 | F2 | F3 | F4 | F5 | ||

| 0.7752 | Eigenvalue | 3.40997 | 2.45115 | 1.94577 | 1.35036 | 1.08627 |

| % of variance | 0.2273 | 0.1634 | 0.1297 | 0.09 | 0.0724 | |

| Cumulative% | 0.2273 | 0.3907 | 0.5205 | 0.6105 | 0.6829 | |

References

- Antipa, P.; Lecat, R. The’Housing Bubble’and Financial Factors: Insights from a Structural Model of the French and Spanish Residential Markets. In Housing Markets in Europe; Springer: Berlin, Germany, 2010; pp. 161–186. [Google Scholar]

- Bucks, B.K.; Kennickell, A.B.; Moore, K.B.; Fries, G.; Neal, A.M. Recent Changes in U.S. Family Finances: Evidence from the 2001 and 2004 Survey of Consumer Finances. Fed. Reserve Bull. 2006, 90, 1–32. [Google Scholar]

- Manning, C.A. Intercity Differences in Home Price Appreciation. J. Real Estate Res. 1986, 1, 45–46. [Google Scholar]

- Manning, C.A. Explaining intercity home price differences. J. Real Estate Financ. Econ. 1989, 2, 131–149. [Google Scholar] [CrossRef]

- Ozanne, L.; Thibodeau, T. Explaining metropolitan housing price differences. J. Urban Econ. 1983, 13, 51–66. [Google Scholar] [CrossRef]

- Potepan, M.J. Explaining intermetropolitan variation in housing prices, rents and land prices. Real Estate Econ. 1996, 24, 219–245. [Google Scholar] [CrossRef]

- Fortura, P.; Kushner, J. Canadian InterCity House Price Differentials. Real Estate Econ. 1986, 14, 525–536. [Google Scholar] [CrossRef]

- Quigley, J.M. Real Estate Prices and Economic Cycles. Int. Real Estate Rev. 1999, 2, 1–20. [Google Scholar]

- Roback, J. Wages, rents, and the quality of life. J. Political Econ. 1982, 90, 1257–1278. [Google Scholar] [CrossRef]

- Rosen, S. Wage-based indexes of urban quality of life. Curr. Issues Urban Econ. 1979, 74–104. [Google Scholar]

- Antoniucci, V.; Marella, G. Housing price gradient and immigrant population: Data from the Italian real estate market. Data Brief 2018, 16, 794–798. [Google Scholar] [CrossRef]

- Egner, B.; Grabietz, K.J. In search of determinants for quoted housing rents: Empirical evidence from major German cities. Urban Res. Pract. 2018, 11, 460–477. [Google Scholar] [CrossRef] [Green Version]

- Soo, C.K. Quantifying sentiment with news media across local housing markets. Rev. Financ. Stud. 2018, 31, 3689–3719. [Google Scholar] [CrossRef] [Green Version]

- Howard, G.; Liebersohn, C. What Explains US House Prices? Regional Income Divergence. In Proceedings of the Regional Income Divergence, 2019 Annual Meeting, St. Louis, MI, USA, 27–29 June 2019; Society for Economic Dynamics: Minneapolis, MN, USA, 2019. [Google Scholar]

- Abraham, J.M.; Hendershott, P.H. Bubbles in Metropolitan Housing Markets. J. Hous. Res. 1996, 7, 191–207. [Google Scholar]

- Capozza, D.R.; Hendershott, P.H.; Mack, C. An anatomy of price dynamics in illiquid markets: Analysis and evidence from local housing markets. Real Estate Econ. 2004, 32, 1–32. [Google Scholar] [CrossRef] [Green Version]

- Goodman, A.C.; Thibodeau, T.G. Where are the speculative bubbles in US housing markets? J. Hous. Econ. 2008, 17, 117–137. [Google Scholar] [CrossRef]

- Nellis, J.G.; Longbottom, J.A. An empirical analysis of the determination of house prices in the United Kingdom. Urban Stud. 1981, 18, 9–21. [Google Scholar] [CrossRef]

- Case, K.E.; Shiller, R.J. Is there a bubble in the housing market? Brook. Pap. Econ. Act. 2003, 2003, 299–362. [Google Scholar] [CrossRef] [Green Version]

- Stiglitz, J.E. Symposium on bubbles. J. Econ. Perspect. 1990, 4, 13–18. [Google Scholar] [CrossRef] [Green Version]

- Stevenson, S. Modeling housing market fundamentals: Empirical evidence of extreme market conditions. Real Estate Econ. 2008, 36, 1–29. [Google Scholar] [CrossRef]

- Glaeser, E.L.; Gyourko, J.; Saiz, A. Housing supply and housing bubbles. J. Urban Econ. 2008, 64, 198–217. [Google Scholar] [CrossRef] [Green Version]

- Mikhed, V.; Zemčík, P. Do house prices reflect fundamentals? Aggregate and panel data evidence. J. Hous. Econ. 2009, 18, 140–149. [Google Scholar] [CrossRef] [Green Version]

- Malpezzi, S.; Wachter, S. The role of speculation in real estate cycles. J. Real Estate Lit. 2005, 13, 141–164. [Google Scholar] [CrossRef] [Green Version]

- Dreger, C.; Zhang, Y. Is there a bubble in the Chinese housing market? Urban Policy Res. 2013, 31, 27–39. [Google Scholar] [CrossRef] [Green Version]

- Li, Q.; Chand, S. House prices and market fundamentals in urban China. Habitat Int. 2013, 40, 148–153. [Google Scholar] [CrossRef]

- Peng, W.; Tam, D.C.; Yiu, M.S. Property market and the macroeconomy of mainland China: A cross region study. Pac. Econ. Rev. 2008, 13, 240–258. [Google Scholar] [CrossRef]

- Wang, Z.; Zhang, Q. Fundamental factors in the housing markets of China. J. Hous. Econ. 2014, 25, 53–61. [Google Scholar] [CrossRef]

- Wu, J.; Gyourko, J.; Deng, Y. Evaluating the risk of Chinese housing markets: What we know and what we need to know. China Econ. Rev. 2016, 39, 91–114. [Google Scholar] [CrossRef] [Green Version]

- Yu, H. China’s house price: Affected by economic fundamentals or real estate policy? Front. Econ. China 2010, 5, 25–51. [Google Scholar] [CrossRef]

- Yue, S.; Hongyu, L. Housing Prices and Economic Fundamentals: A Cross City Analysis of China for 1995—2002. Econ. Res. J. 2004, 6, 78–86. [Google Scholar]

- Yunfang, L.; Tiemei, G. Empirical Analysis on Real Estate Price Fluctuation in Different Provinces of China. Econ. Res. J. 2007, 8, 133–142. [Google Scholar]

- Huang, B.; Wu, B.; Barry, M. Geographically and temporally weighted regression for modeling spatio-temporal variation in house prices. Int. J. Geogr. Inf. Sci. 2010, 24, 383–401. [Google Scholar] [CrossRef]

- Oikarinen, E.; Engblom, J. Differences in housing price dynamics across cities: A comparison of different panel model specifications. Urban Stud. 2016, 53, 2312–2329. [Google Scholar] [CrossRef]

- Wang, S.; Wang, J.; Wang, Y. Effect of land prices on the spatial differentiation of housing prices: Evidence from cross-county analyses in China. J. Geogr. Sci. 2018, 28, 725–740. [Google Scholar] [CrossRef] [Green Version]

- Stewart Fotheringham, A.; Charlton, M.; Brunsdon, C. The geography of parameter space: An investigation of spatial non-stationarity. Int. J. Geogr. Inf. Syst. 1996, 10, 605–627. [Google Scholar] [CrossRef]

- Bitter, C.; Mulligan, G.F.; Dall’erba, S. Incorporating spatial variation in housing attribute prices: A comparison of geographically weighted regression and the spatial expansion method. J. Geogr. Syst. 2007, 9, 7–27. [Google Scholar] [CrossRef] [Green Version]

- Mou, Y.; He, Q.; Zhou, B. Detecting the spatially non-stationary relationships between housing price and its determinants in China: Guide for housing market sustainability. Sustainability 2017, 9, 1826. [Google Scholar] [CrossRef] [Green Version]

- Cai, R.; Yu, D.; Oppenheimer, M. Estimating the Effects of Weather Variations on Corn Yields Using Geographically Weighted Panel Regression. In Proceedings of the 2012 Annual Meeting, Seattle, WA, USA, 12–14 August 2012; Agricultural and Applied Economics Association: Milwaukee, WI, USA, 2012. [Google Scholar]

- Yu, D. Exploring spatiotemporally varying regressed relationships: The geographically weighted panel regression analysis. Int. Arch. Photogramm. Remote Sens. Spat. Inf. Sci. 2010, 38, 134–139. [Google Scholar]

- Tabak, B.M.; Miranda, R.B.; Fazio, D.M. A geographically weighted approach to measuring efficiency in panel data: The case of US saving banks. J. Bank. Financ. 2013, 37, 3747–3756. [Google Scholar] [CrossRef]

- Páez, A.; Uchida, T.; Miyamoto, K. A general framework for estimation and inference of geographically weighted regression models: 1. Location-specific kernel bandwidths and a test for locational heterogeneity. Environ. Plan. A 2002, 34, 733–754. [Google Scholar] [CrossRef]

- Mussa, A.; Nwaogu, U.G.; Pozo, S. Immigration and housing: A spatial econometric analysis. J. Hous. Econ. 2017, 35, 13–25. [Google Scholar] [CrossRef]

- Saiz, A. Immigration and housing rents in American cities. J. Urban Econ. 2007, 61, 345–371. [Google Scholar] [CrossRef] [Green Version]

- Wang, Y.; Wang, S.; Li, G.; Zhang, H.; Jin, L.; Su, Y.; Wu, K. Identifying the determinants of housing prices in China using spatial regression and the geographical detector technique. Appl. Geogr. 2017, 79, 26–36. [Google Scholar] [CrossRef]

- Chau, K.W.; Chin, T. A critical review of literature on the hedonic price model. Int. J. Hous. Sci. Its Appl. 2003, 27, 145–165. [Google Scholar]

- Gibbons, S.; Machin, S. Valuing school quality, better transport, and lower crime: Evidence from house prices. Oxf. Rev. Econ. Policy 2008, 24, 99–119. [Google Scholar] [CrossRef]

- Jim, C.Y.; Chen, W.Y. External effects of neighbourhood parks and landscape elements on high-rise residential value. Land Use Policy 2010, 27, 662–670. [Google Scholar] [CrossRef]

- Nguyen-Hoang, P.; Yinger, J. The capitalization of school quality into house values: A review. J. Hous. Econ. 2011, 20, 30–48. [Google Scholar] [CrossRef]

- Zheng, S.; Hu, W.; Wang, R. How much is a good school worth in Beijing? Identifying price premium with paired resale and rental data. J. Real Estate Financ. Econ. 2016, 53, 184–199. [Google Scholar] [CrossRef]

- Feng, H.; Lu, M. School quality and housing prices: Empirical evidence from a natural experiment in Shanghai, China. J. Hous. Econ. 2013, 22, 291–307. [Google Scholar] [CrossRef]

- Wen, H.; Xiao, Y.; Hui, E.C.; Zhang, L. Education quality, accessibility, and housing price: Does spatial heterogeneity exist in education capitalization? Habitat Int. 2018, 78, 68–82. [Google Scholar] [CrossRef]

- Wen, H.; Xiao, Y.; Zhang, L. School district, education quality, and housing price: Evidence from a natural experiment in Hangzhou, China. Cities 2017, 66, 72–80. [Google Scholar] [CrossRef]

- Hwang, M.; Quigley, J.M. Economic fundamentals in local housing markets: Evidence from US metropolitan regions. J. Reg. Sci. 2006, 46, 425–453. [Google Scholar] [CrossRef] [Green Version]

- Glaeser, E.L.; Gyourko, J.; Saks, R.E. Urban growth and housing supply. J. Econ. Geogr. 2005, 6, 71–89. [Google Scholar] [CrossRef] [Green Version]

- Mayer, C.J.; Somerville, C.T. Land use regulation and new construction. Reg. Sci. Urban Econ. 2000, 30, 639–662. [Google Scholar] [CrossRef]

- Pollakowski, H.O.; Wachter, S.M. The effects of land-use constraints on housing prices. Land Econ. 1990, 66, 315–324. [Google Scholar] [CrossRef]

- Zhang, D.; Liu, Z.; Fan, G.-Z.; Horsewood, N. Price bubbles and policy interventions in the Chinese housing market. J. Hous. Built Environ. 2017, 32, 133–155. [Google Scholar] [CrossRef]

- Oikarinen, E.; Bourassa, S.C.; Hoesli, M.; Engblom, J. US metropolitan house price dynamics. J. Urban Econ. 2018, 105, 54–69. [Google Scholar] [CrossRef]

| Variable | Dimensions | Indexes |

|---|---|---|

| Public Service Quality | Education [49,50,51,52,53] | Number of Primary Schools |

| Number of Regular Secondary Schools | ||

| Number of Regular Institutions of Higher Education | ||

| Teacher–student Ratio in Primary Schools | ||

| Teacher–student Ratio in Regular Secondary Schools | ||

| Expenditure for Education per capita | ||

| Health Care | Number of Hospitals and Health Centres per 10,000 Persons | |

| Number of Beds of Hospitals and Health Centres per 10,000 Persons | ||

| Number of Doctors per 10,000 Persons | ||

| Public Transportation | Number of Public Transportation Vehicles per 10,000 persons | |

| Length of the Lines of the Urban Rail Transit System (completed and under construction) | ||

| Culture and Entertainment | Number of Theatres, Music Halls, and Cinemas per 10,000 Persons | |

| Collections of Public Libraries per 100 Persons | ||

| Landscape | Area of Parks and Green Land | |

| Green Covered Area as % of Completed Area |

| Variables | Definition | Mean | Std. Dev. | Min. | Max. | Obs. | Source |

|---|---|---|---|---|---|---|---|

| LnPrice | Logarithm of residential house prices | 8.64 | 0.44 | 7.90 | 10.54 | 808 | http://www.creprice.cn/ |

| LnRentalPrices | Logarithm of residential house rental prices | 2.77 | 0.38 | 1.86 | 4.14 | 808 | http://www.creprice.cn/ |

| TDiff | Annual temperature difference | 43.48 | 9.04 | 8.00 | 76.00 | 808 | China Meteorological Data Service Center |

| PSQ | Public service quality | 0.03 | 0.49 | −0.90 | 3.45 | 808 | “China City Statistical Yearbook” “China Urban Construction Statistical Yearbook” |

| LnIncome t-1 | Logarithm of one-year-lagged per capita disposable income of urban households | 9.97 | 0.27 | 9.24 | 10.75 | 808 | “China City Statistical Yearbook” |

| Employment | Proportion of employed persons in a tertiary industry | 49.37 | 12.65 | 15.39 | 87.57 | 808 | “China City Statistical Yearbook” |

| LnPop t-1 | Logarithm of one-year-lagged permanent population | 6.01 | 0.62 | 4.23 | 8.00 | 808 | “China Statistical Yearbook For Regional Economy” |

| Inflowt-1 | One-year-lagged proportion of net inflow population in permanent population | 6.11 | 12.28 | 0.00 | 77.90 | 808 | “China City Statistical Yearbook” “China Statistical Yearbook For Regional Economy” |

| LnStock | Logarithm of floor space of commercial residential houses completed | 5.59 | 1.22 | 0.73 | 9.50 | 808 | “China City Statistical Yearbook” |

| LnCost | Logarithm of investment in real estate development per capita | 8.39 | 0.83 | 5.10 | 10.84 | 808 | “China City Statistical Yearbook” |

| Construction Area | Land used for urban construction as a percentage of the urban area | 10.36 | 9.94 | 0.44 | 86.15 | 808 | “China City Statistical Yearbook” |

| LnLand t-1 | Logarithm of one-year-lagged transaction volume of residential land | 4.65 | 1.29 | −1.71 | 7.79 | 808 | CREIS Databank |

| LnLandprice t-1 | Logarithm of one-year-lagged residential land price | 7.73 | 0.92 | 0.00 | 10.75 | 808 | CREIS Databank |

| Yieldt-1 | One-year-lagged rent-to-price ratio | 3.36 | 0.79 | 1.45 | 6.88 | 808 | http://www.creprice.cn/ |

| East | Eastern city = 1, Others = 0 | National Bureau of Statistics of China | |||||

| West | Western city = 1, Others = 0 | National Bureau of Statistics of China | |||||

| Municipality | Municipalities = 1, Others = 0 | National Bureau of Statistics of China | |||||

| Pro_capital | provincial capitals or municipalities with independent planning status = 1, Others = 0 | National Bureau of Statistics of China |

| Variables | Coefficient | t-Statistic | VIF |

|---|---|---|---|

| Constant | 1.8933 *** | 3.50 | - |

| TDiff | −0.0024 *** | −2.61 | 1.39 |

| PSQ | 0.1664 *** | 5.08 | 5.00 |

| Employment | 0.0018 *** | 2.65 | 1.41 |

| Inflowt-1 | 0.0009 | 0.98 | 2.32 |

| LnIncome t-1 | 0.5151 *** | 8.85 | 4.69 |

| LnPop t-1 | 0.0328 * | 1.74 | 2.66 |

| Construction Area | −0.0024 *** | −2.94 | 1.27 |

| LnStock | −0.0158 * | −1.72 | 2.42 |

| LnCost | 0.1130 *** | 7.17 | 3.30 |

| LnLand t-1 | −0.0439 *** | −5.53 | 2.03 |

| LnLandprice t-1 | 0.1026 *** | 10.14 | 1.70 |

| Pro_capital | 0.2132 *** | 6.96 | 2.37 |

| Municipality | 0.3879 *** | 4.61 | 2.67 |

| East | 0.1605 *** | 8.12 | 1.89 |

| West | −0.0754 *** | −3.37 | 1.63 |

| Year fixed effect | controlled | ||

| Diagnostic information | |||

| Observations | 808 | ||

| RSS | 32.8067 | ||

| Adjusted R-squared | 0.7806 | ||

| Variables | MIN | AVG | MAX | LQ | MED | UQ |

|---|---|---|---|---|---|---|

| Constant | −5.4636 | 1.6012 | 9.0184 | −1.1679 | 1.9853 | 4.5410 |

| TDiff | −0.0246 | −0.0048 | 0.0117 | −0.0089 | −0.0050 | −0.0002 |

| PSQ | −0.1075 | 0.2350 | 0.4462 | 0.1586 | 0.2338 | 0.3331 |

| Employment | −0.0041 | 0.0021 | 0.0065 | 0.0009 | 0.0021 | 0.0035 |

| Inflowt-1 | −0.0134 | 0.0004 | 0.0189 | −0.0044 | 0.0005 | 0.0059 |

| LnIncome t-1 | −0.3442 | 0.4615 | 1.2211 | 0.2282 | 0.4022 | 0.6881 |

| LnPop t-1 | −0.1492 | 0.0421 | 0.2411 | −0.0057 | 0.0361 | 0.0794 |

| Construction Area | −0.0133 | −0.0014 | 0.0161 | −0.0045 | −0.0021 | 0.0007 |

| LnStock | −0.1900 | −0.0157 | 0.0813 | −0.0274 | −0.0089 | 0.0084 |

| LnCost | −0.0669 | 0.0967 | 0.3106 | 0.0405 | 0.0987 | 0.1340 |

| LnLand t-1 | −0.1025 | −0.0021 | 0.1318 | −0.0400 | −0.0062 | 0.0206 |

| LnLandprice t-1 | 0.0014 | 0.1997 | 0.3524 | 0.1085 | 0.2223 | 0.2803 |

| Diagnostic information | ||||||

| Observations | 808 | |||||

| RSS | 20.4464 | |||||

| Adjusted R-squared | 0.8646 | |||||

| Spatiotemporal Distance Ratio [33] | 3.2493 | |||||

| Variables | Coefficient | t-Statistic | VIF |

|---|---|---|---|

| Constant | −0.3784 | −0.72 | - |

| TDiff | −0.0063 *** | −7.26 | 1.45 |

| PSQ | 0.1592 *** | 5.37 | 5.01 |

| Employment | 0.0006 | 0.99 | 1.41 |

| Inflowt-1 | 0.0037 *** | 4.56 | 2.39 |

| LnIncome t-1 | 0.1152 ** | 2.12 | 5.00 |

| LnPop t-1 | 0.0477 *** | 2.79 | 2.66 |

| Construction Area | −0.0024 *** | −3.23 | 1.27 |

| LnStock | −0.0246 *** | −2.97 | 2.42 |

| LnCost | 0.1622 *** | 11.34 | 3.32 |

| LnLand t-1 | −0.0290 *** | −4.04 | 2.03 |

| LnLandprice t-1 | 0.0666 *** | 7.04 | 1.81 |

| Yieldt-1 | 0.0727 *** | 7.58 | 1.35 |

| Pro_capital | 0.1976 *** | 7.13 | 2.37 |

| Municipality | 0.2569 *** | 3.36 | 2.68 |

| East | 0.1031 *** | 5.75 | 1.90 |

| West | −0.0272 | −1.33 | 1.65 |

| Year fixed effect | controlled | ||

| Diagnostic information | |||

| Observations | 808 | ||

| RSS | 26.8552 | ||

| Adjusted R-squared | 0.7628 | ||

| Variables | MIN | AVG | MAX | LQ | MED | UQ | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Constant | −7.5995 | −1.3963 | 3.7946 | −2.4657 | −1.3871 | −0.2160 | |||||

| TDiff | −0.0325 | −0.0103 | 0.0092 | −0.0182 | −0.0090 | −0.0017 | |||||

| PSQ | 0.0353 | 0.1917 | 0.3920 | 0.1204 | 0.1950 | 0.2590 | |||||

| Employment | −0.0037 | 0.0007 | 0.0044 | −0.0004 | 0.0008 | 0.0018 | |||||

| Inflowt-1 | −0.0056 | 0.0022 | 0.0147 | −0.0008 | 0.0019 | 0.0047 | |||||

| LnIncome t-1 | −0.3620 | 0.1766 | 0.6854 | 0.0496 | 0.1564 | 0.3112 | |||||

| LnPop t-1 | −0.1114 | 0.0569 | 0.2120 | 0.0177 | 0.0603 | 0.0889 | |||||

| Construction Area | −0.0070 | −0.0004 | 0.0100 | −0.0021 | −0.0010 | 0.0010 | |||||

| LnStock | −0.1259 | −0.0099 | 0.0518 | −0.0256 | −0.0052 | 0.0098 | |||||

| LnCost | 0.0356 | 0.1467 | 0.2661 | 0.1187 | 0.1434 | 0.1743 | |||||

| LnLand t-1 | −0.0788 | 0.0008 | 0.1279 | −0.0216 | −0.0043 | 0.0169 | |||||

| LnLandprice t-1 | −0.0154 | 0.1347 | 0.2697 | 0.0731 | 0.1496 | 0.1836 | |||||

| Yieldt-1 | −0.0261 | 0.05 53 | 0.1346 | 0.0227 | 0.0547 | 0.0916 | |||||

| Diagnostic information | |||||||||||

| Observations | 808 | ||||||||||

| RSS | 16.3625 | ||||||||||

| Adjusted R-squared | 0.8569 | ||||||||||

| Spatiotemporal Distance Ratio [33] | 3.12837 | ||||||||||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhou, X.; Qin, Z.; Zhang, Y.; Zhao, L.; Song, Y. Quantitative Estimation and Spatiotemporal Characteristic Analysis of Price Deviation in China's Housing Market. Sustainability 2019, 11, 7232. https://0-doi-org.brum.beds.ac.uk/10.3390/su11247232

Zhou X, Qin Z, Zhang Y, Zhao L, Song Y. Quantitative Estimation and Spatiotemporal Characteristic Analysis of Price Deviation in China's Housing Market. Sustainability. 2019; 11(24):7232. https://0-doi-org.brum.beds.ac.uk/10.3390/su11247232

Chicago/Turabian StyleZhou, Xiaoping, Zhenyang Qin, Yingjie Zhang, Linyi Zhao, and Yan Song. 2019. "Quantitative Estimation and Spatiotemporal Characteristic Analysis of Price Deviation in China's Housing Market" Sustainability 11, no. 24: 7232. https://0-doi-org.brum.beds.ac.uk/10.3390/su11247232