The Impact of Internal, External and Enterprise Risk Management on the Performance of Micro, Small and Medium Enterprises

Abstract

:1. Introduction

2. Literature Review

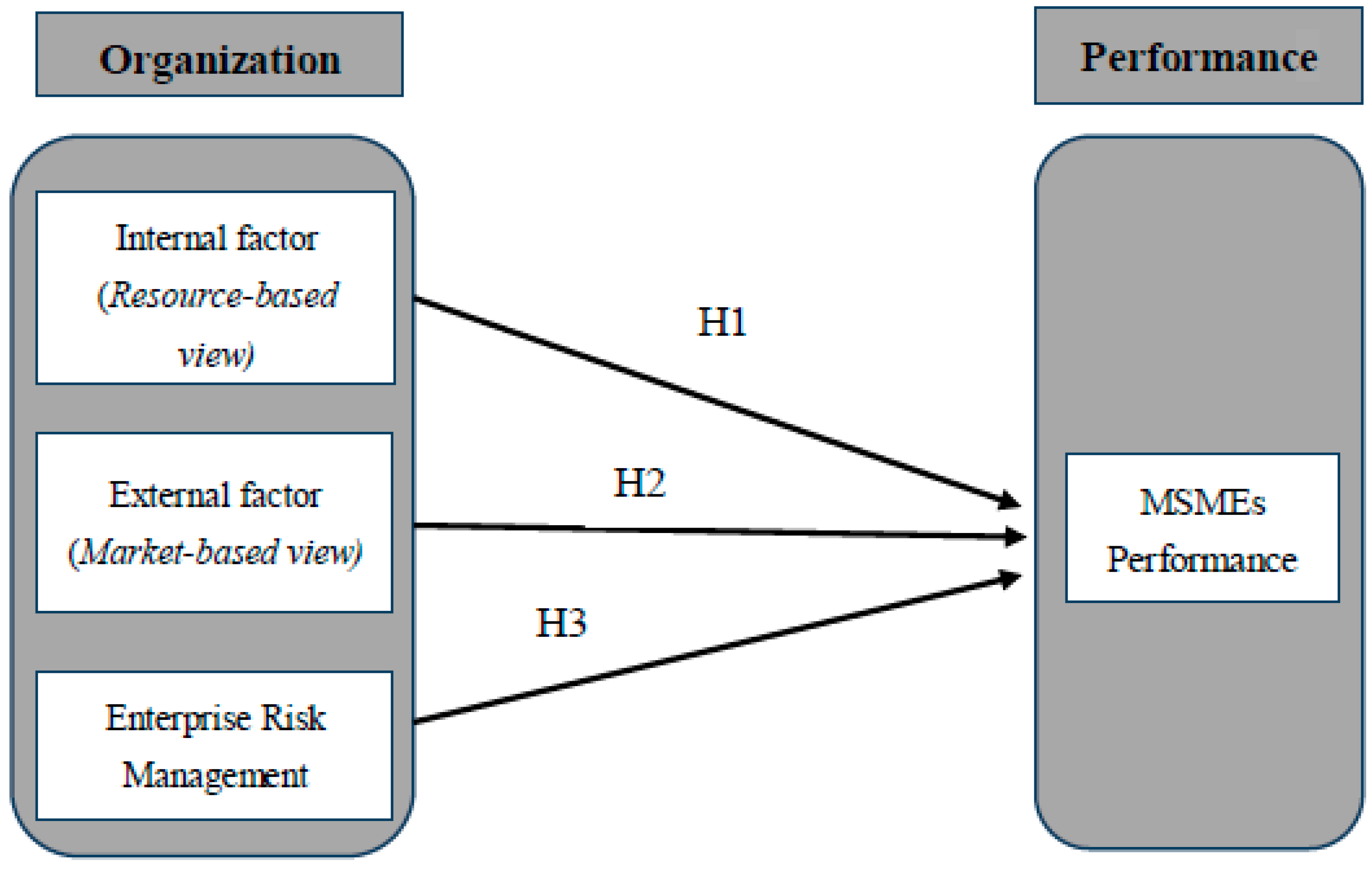

2.1. Resource-Based View

2.2. Market-Based View

2.3. Enterprise Risk Management (ERM)

2.3.1. The Relationship between Internal Factors and Performance

2.3.2. The Relationship between External Factors and Performance

2.3.3. The Relationship between Risk Management and Performance

3. Methodology

3.1. Participants

3.2. Measures

3.3. Procedures

4. Data Analysis

5. Results

5.1. Validity and Reliability Test

5.2. Correlation Test

6. Discussion

7. Conclusions

7.1. Summary, Implications and Contribution of This Study

- (1)

- Internal and external strength factors of MSMEs has been proved to affect performance positively. These results can be important notes for MSMEs that the owner should pay more attention to manage their internal organizational issues in term of their human resources (HR), marketing, operation, and technology. For instance, in the HR area, the owner needs to put their concern on how the business can provide competitive benefit for retaining their employees’ than the competitors. Additionally, as 53.31% of MSMEs’ owners are aged more than 40 years old, they should think about the succession plan to sustain their business operation. Whereas in finance, the owner firstly should separate their personal and business asset as well as having a financial record of their business, to track their profit and loss as a basis of their future business strategy. In operational issues, they can undertake some efforts such as develop production efficiency to gain more profitable business. In the external factor, knowing how to compete with competitors also affects the performance of SMEs in seizing market share and a high level of profitability. If these factors are improved, this will enhance their performance, position in the market so as their ability to generate profits. In this manner, MSMEs is expected to maintain its long-term sustainability.

- (2)

- Based on the result of several underdeveloped areas in this research, it is known that the MSMEs are lack of awareness of their business development. Thus, the organizations related to this sector’ acquaintance need to give more attention of the MSMEs practice and give an evenly accompaniment or assistance that can also reach to the underdeveloped regions; and build the MSMEs awareness to apply the strategies that can help them grow their business. Then, providing appropriate treatment by clustering the MSMEs—e.g., based on their business size may create a better impact on the MSMEs growth.

7.2. Limitations and Future Research Direction

- (1)

- The results of this study are restricted to the MSMEs in Indonesia’s underdeveloped area with the one who has the offline store. As the advancement of technology, many MSMEs start their business with the use of an online basis. Thus, it may differ if the same research conducted in other respondents’ target groups and areas. Moreover, the selection of specific industry and the peculiar level of business such as micro or medium business—though it may only provide useful business acumen to specific MSME’s size and sectors.

- (2)

- The questionnaires that are used in this research delimitate the respondents to fill out the answer based on the available choices. Hence, conducting additional method as in-depth interview or Focus Group Discussion (FGD) will be beneficial for future research to draw a depth insight and valuable feedback from the potential respondents to give significant managerial impact and enhance their business’ performance.

- (3)

- This research used the variable of risk management by involving sub-variables of business’ operational, financial, and marketing. However, future research can include other risks sub-variables to make the research more comprehensive in analyzing the risk to influence business’ performance.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Dimension | Constructs | |

|---|---|---|

| Internal–Organization (IOM) | IOM1 | How is your employees’ level of business knowledge and expertise, compared to the competitors? |

| IOM2 | How efficient is the work schedules division in your business, compared to the competitors? | |

| IOM3 | How was your business’s production and marketing plan in the past year, compared to the competitors? | |

| IOM4 | How is your business ability (related to bonuses & incentives) in retaining employees, compared to the competitors? | |

| Internal–Marketing (IPE) | IPE2 | How is your effort in response to consumer complaints, compared to the competitors? |

| IPE3 | How is your effort to attract more buyers and loyal customers, compared to the competitors? | |

| IPE4 | How is your effort in performing promotion, compared to the competitors? | |

| IPE5 | How is your effort in the price-setting, compared to the competitors? | |

| Internal–Technical (ITS) | ITS1 | How was your production performance in achieving sales targets for the past year, compared to the competitors? |

| ITS2 | How is your business in employing the experienced workers who is expert in production process compared to the competitors? | |

| ITS3 | How is your business’ ability to produce large quantities of goods at a low cost compared to the competitors? | |

| ITS4 | How is your ability of distribution management compared to the competitors? | |

| Internal–Technology (ITG) | ITG2 | How is the use of technology – especially social media such as Facebook and Instagram, in your business’ marketing activities? |

| ITG3 | How is the use of online marketplaces, such as Tokopedia, Bukalapak, Lazada, in marketing your products? | |

| ITG4 | How is you and your employees’ participation in joining trainings related to mastering technology related to your business? | |

| ITG5 | How is your participation in joining mentorship related to the application of technology held by the government institution and/or large companies, compared to the competitors? | |

| External–Industry (EIN) | EIN1 | How do you rate the superiority of your products compared to the competitors? |

| E1N2 | How do you assess the competitive advantages of your business’ promotion strategy (discount), compared to the competitors? | |

| EIN3 | How do you rate the superiority of your business’s competitiveness in terms of product distribution, compared to the competitors? | |

| Performance–Market Share (EPP) | EPP1 | Compared to the competitors, how was your sales performance in the past year? |

| EPP2 | Compared to the competitors, how was your sales growth performance? | |

| EPP3 | Compared to the competitors, how was your market share’s growth? | |

| Performance–Profitability (EPF) | EPF1 | Compared to the competitors, how was the performance of your business’ profit for the previous year? |

| EPF2 | Compared to the competitors, how was your business’ ability to achieve payback period/break-even-point? | |

| EPF3 | Compared to the competitors, how was your business’ net profit performance? | |

| ERM–Financial Risk (RKE) | RKE1 | Our business’ sales have declined in the past two years. |

| RKE2 | Our company often experiences losses. | |

| RKE3 | Our company has a very large amount of loan/debt. | |

| RKE4 | Our customers are often to not pay their debts. | |

| ERM–Marketing Risk (RP) | RP1 | Our company sales have declined in the past year. |

| RP2 | Our company only relies on a few customers. | |

| RP3 | Our company fails to promote our products continuously. | |

References

- Sarwono, H.A. Profil Bisnis Usaha Mikro, Kecil dan Menengah (UMKM); Bank Indonesia: Jakarta, Indonesia, 2015.

- Southiseng, N.; Walsh, J. Competition and Management Issues of SME Entrepreneurs in Laos: Evidence from Empirical Studies in Vientiane Municipality, Savannakhet and Luang Prabang. Asian J. Bus. Manag. 2010, 2, 57–72. [Google Scholar]

- Kot, S. Sustainable Supply Chain Management in Small and Medium Enterprises. Sustainability 2018, 10, 1143. [Google Scholar] [CrossRef]

- Androniceanu, A. The Three-Dimensional Approach of Total Quality Management, An Essential Strategic Option for Business Excellence. Amfiteatru Econ. 2017, 19, 61–67. [Google Scholar]

- Child, J. Organizational Structure, Environment and Performance: The Role of Strategic Choice. Sociology 1972, 6, 1–22. [Google Scholar] [CrossRef]

- Huang, S.K. The Impact of CEO Characteristics on Corporate Sustainable Development. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 234–244. [Google Scholar] [CrossRef]

- Lindsey, P.H.; Nourman, D.A. Human Information Processing: An Introduction to Psychology; American Press Inc.: New York, NY, USA, 1977. [Google Scholar]

- Smékalová, L. Evaluating The Cohesion Policy: Targeting of Disadvantaged Municipalities. Adm. Manag. Public 2018, 31, 143–154. [Google Scholar]

- Hou, X.; Wang, Q.; Zhang, Q. Market Structure, Risk Taking, and The Efficiency of Chinese Commercial Banks. Emerg. Mark. Rev. 2014, 20, 75–88. [Google Scholar] [CrossRef]

- Vithessonthi, C.; Tongurai, J. Financial Markets Development, Business Cycles, and Bank Risk in South America. Res. Int. Bus. Financ. 2016, 36, 472–484. [Google Scholar] [CrossRef]

- Lefebvre, L.A.; Mason, R.; Lefebvre, É. The Influence Prism in SMEs: The Power of CEOs’ Perceptions on Technology Policy and Its Organizational Impacts. Manage. Sci. 1997, 43, 856–878. [Google Scholar] [CrossRef]

- Tonello, M. Emerging Governance Practices in Enterprise Risk Management; Conference Board: New York, NY, USA, 2007. [Google Scholar]

- Callahan, C.; Soileau, J. Does Enterprise Risk Management Enhance Operating Performance? Adv. Account. 2017, 37, 122–139. [Google Scholar] [CrossRef]

- Beasley, M.; Pagach, D.; Warr, R. Information Conveyed in Hiring Announcements of Senior Executives Overseeing Enterprise-Wide Risk Management Processes. J. Account. Audit. Financ. 2008, 23, 311–332. [Google Scholar] [CrossRef] [Green Version]

- Nocco, B.W.; Stulz, R.M. Enterprise Risk Management: Theory and Practice. J. Appl. Corp. Financ. 2006, 18, 8–20. [Google Scholar] [CrossRef]

- Boso, N.; Adeola, O.; Danso, A.; Assadinia, S. The Effect of Export Marketing Capabilities on Export Performance: Moderating Role of Dysfunctional Competition. Ind. Mark. Manag. 2017. [Google Scholar] [CrossRef]

- Peteraf, M.A. The Cornerstones of Competitive Advantage: A Resource-based View. Strateg. Manag. J. 1993, 14, 179–191. [Google Scholar] [CrossRef]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Porter, M.E. Towards a Dynamic Theory of Strategy. Strateg. Manag. J. 1991, 12, 95–117. [Google Scholar] [CrossRef]

- Pagach, D.; Warr, R. The Characteristics of Firms That Hire Chief Risk Officers. J. Risk Insur. 2011, 78, 185–211. [Google Scholar] [CrossRef]

- Paape, L.; Speklé, R.F. The Adoption and Design of Enterprise Risk Management Practices: An Empirical Study. Eur. Account. Rev. 2012, 21, 533–564. [Google Scholar] [CrossRef]

- Committee of Sponsoring Organizations of the Treadway Commissio (COSO). Enterprise Risk Management—Integrated Framework Executive Summary; American Institute of Certified Public Accountants (AICPA): New York, NY, USA, 2004. [Google Scholar]

- Kleffner, A.E.; Lee, R.B.; McGannon, B. The Effect of Corporate Governance on The Use of Enterprise Risk Management: Evidence From Canada. Risk Manag. Insur. Rev. 2003, 6, 53–73. [Google Scholar] [CrossRef]

- Faltejskova, O.; Dvorakova, L.; Hotovcova, B. Net Promoted Score Integration into The Enterprise Performance Measurement and Management System—A Way to Performance Methods Development. E M Ekon. Manag. 2016, 19, 93–107. [Google Scholar]

- Goncharuk, A.G. Enterprise Performance Management: Conception, Model and Mechanism. Pol. J. Manag. Stud. 2014, 4, 78–95. [Google Scholar]

- Spanos, Y.E.; Lioukas, S. An Examination Into The Causal Logic of Rent Generation: Contrasting Porter’s Competitive Strategy Framework and The Resource-based Perspective. Strateg. Manag. J. 2001, 22, 907–934. [Google Scholar] [CrossRef]

- Bendickson, J.S.; Chandler, T.D. Operational Performance—The Mediator Between Human Capital Development Program and Financial Performance. J. Bus. Res. 2019, 94, 162–171. [Google Scholar] [CrossRef]

- Cacciolatti, L.; Lee, S.H. Revisiting The Relationship between Marketing Capabilities and Firm Performance: The Moderating Role of Market Orientation, Marketing Strategy and Organisational Power. J. Bus. Res. 2016, 69, 5597–5610. [Google Scholar] [CrossRef]

- De Leeuw, S.; Van Den Berg, J.P. Improving Operational Performance by Influencing Shopfloor Behavior via Performance Management Practices. J. Oper. Manag. 2011, 29, 224–235. [Google Scholar] [CrossRef]

- Demirkesen, S.; Ozorhon, B. Impact of Integration Management on Construction Project Management Performance. Int. J. Proj. Manag. 2017, 35, 1639–1654. [Google Scholar] [CrossRef]

- Heckmann, N.; Steger, T.; Dowling, M. Organizational Capacity for Change, Change Experience, and Change Project Performance. J. Bus. Res. 2016, 69, 777–784. [Google Scholar] [CrossRef]

- Jaakkola, M.; Möller, K.; Parvinen, P.; Evanschitzky, H.; Mühlbacher, H. Strategic Marketing and Business Performance: A Study in Three European “Engineering Countries”. Ind. Mark. Manag. 2010, 39, 1300–1310. [Google Scholar] [CrossRef]

- Kianto, A.; Sáenz, J.; Aramburu, N. Knowledge-Based Human Resource Management Practices, Intellectual Capital and Innovation. J. Bus. Res. 2017, 81, 11–20. [Google Scholar] [CrossRef]

- Meutia; Ismail, T. The Influence of Competitive Pressure on Innovative Creativity. Acad. Strateg. Manag. J. 2015, 14, 117–128. [Google Scholar]

- Popaitoon, S.; Siengthai, S. The Moderating Effect of Human Resource Management Practices on The Relationship between Knowledge Absorptive Capacity and Project Performance in Project-oriented Companies. Int. J. Proj. Manag. 2014, 32, 908–920. [Google Scholar] [CrossRef]

- Tang, Y.; Wang, P.; Zhang, Y. Marketing and Business Performance of Construction SMEs in China. J. Bus. Ind. Mark. 2007, 22, 118–125. [Google Scholar] [CrossRef]

- Kaleka, A.; Morgan, N.A. How Marketing Capabilities and Current Performance Drive Strategic Intentions in International Markets. Ind. Mark. Manag. 2016. [Google Scholar] [CrossRef]

- Yu, W.; Ramanathan, R.; Nath, P. Environmental Pressures and Performance: An Analysis of The Roles of Environmental Innovation Strategy and Marketing Capability. Technol. Forecast. Soc. Chang. 2017, 117, 160–169. [Google Scholar] [CrossRef]

- Dvorsky, J.; Popp, J.; Virglerova, Z.; Kovács, S.; Oláh, J. Assessing the Importance of Market Risk and Its Sources in the SME of the Visegrad Group and Serbia. Adv. Decis. Sci. 2018, 22, 1–25. [Google Scholar]

- Li, Y.; Nie, D.; Zhao, X.; Li, Y. Market Structure and Performance: An Empirical Study of The Chinese Solar Cell Industry. Renew. Sustain. Energy Rev. 2017, 70, 78–82. [Google Scholar] [CrossRef]

- Purnama, C.; Subroto, W.T. Competition Intensity, Uncertainty Environmental on The Use of Information Technology and Its Impact on Business Performance Small and Medium Enterprises. Int. Rev. Manag. Mark. 2016, 6, 984–992. [Google Scholar]

- Brustbauer, J. Enterprise Risk Management in SMEs: Towards a Structural Model. Int. Small Bus. J. Res. Entrep. 2016, 34, 70–85. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance; Free Press: New York, NY, USA, 2008; ISBN 978-3-319-54539-4. [Google Scholar]

- Kiseláková, D.; Sofranková, B.; Cábinová, V.; Soltésová, J. Analysis of Enterprise Performance and Competitiveness to Streamline Managerial Decisions. Pol. J. Manag. Stud. 2018, 17, 101–111. [Google Scholar] [CrossRef]

- MacCrimmon, K.R.; Wehrung, D.A.; Stanbury, W.T. Taking Risks: The Management of Uncertainty; Free Press: New York, NY, USA, 1986; ISBN 0029195608. [Google Scholar]

- March, J.G.; Shapira, Z. Managerial Perspectives on Risk and Risk Taking. Manag. Sci. 1987, 33, 1401–1418. [Google Scholar] [CrossRef]

- Lam, J. The CRO is Here to Stay. Risk Manag. 2001, 48, 16–22. [Google Scholar]

- Dirjen PDT. Rencana Strategis (RENSTRA) Direktorat Jendral Pembangunan Daerah Tertinggal Tahun 2015–2019; Ditjen PDT: Jakarta, Indonesia, 2019. [Google Scholar]

- Bank Sentral RI Undang-Undang Republik Indonesia No.20 Tahun 2008 Tentang Usaha Mikro, Kecil, dan Menengah. Available online: https://www.bi.go.id/id/tentang-bi/uu-bi/Documents/UU20Tahun2008UMKM.pdf (accessed on 5 April 2019).

- Cooper, D.R.; Schindler, P.S. Business Research Methods, 12th ed.; McGraw-Hill/Irwin: New York, NY, USA, 2011; ISBN 9780073521503. [Google Scholar]

- Malhotra, N.K. Essentials of Marketing Research: A Hands-On Orientation; Pearson Education Limited: Essex, UK, 2015; ISBN 9780137066735. [Google Scholar]

- Chari, S.; Balabanis, G.; Robson, M.J.; Slater, S. Alignments and Misalignments of Realized Marketing Strategies with Administrative Systems: Performance Implications. Ind. Mark. Manag. 2017, 63, 129–144. [Google Scholar] [CrossRef]

- Linton, G.; Kask, J. Configurations of Entrepreneurial Orientation and Competitive Strategy for High Performance. J. Bus. Res. 2017, 70, 168–176. [Google Scholar] [CrossRef]

- Malhotra, N.K. Review of Marketing Research; M.E. Sharpe: New York, NY, USA, 2008; ISBN 9780765620927. [Google Scholar]

- Theriou, N.G.; Aggelidis, V.; Theriou, G.N. A Theoretical Framework Contrasting The Resource-based Perspective and The Knowledge-based View. Eur. Res. Stud. J. 2009, 12, 177–190. [Google Scholar]

- Grant, R.M. The Resource-Based Theory of Competitive Advantage: Implications for Strategy Formulation. Calif. Manag. Rev. 1991, 33, 114–135. [Google Scholar] [CrossRef]

- Asia Pacific Foundation of Canada. 2018 Survey of Entrepreneurs and MSMEs in Indonesia: Building the Capacity of MSMEs through Human Capital. Available online: https://apfcanada-msme.ca/research/2018-survey-entrepreneurs-and-msmes-indonesia-building-capacity-msmes-through-human (accessed on 1 April 2019).

- Rumelt, R.P. How Much Does Industry Matter? Strateg. Manag. J. 1991, 12, 167–185. [Google Scholar] [CrossRef]

- Khandwalla, P.N. The Design of Organizations; Harcourt Brace Jovanovich: New York, NY, USA, 1977; ISBN 0-15-517366-9. [Google Scholar]

- Wang, Z.; Kim, H.G. Can Social Media Marketing Improve Customer Relationship Capabilities and Firm Performance? Dynamic Capability Perspective. J. Interact. Mark. 2017, 39, 15–26. [Google Scholar] [CrossRef]

- Khalid, S.; Larimo, J. Affects of Alliance Entrepreneurship on Common Vision, Alliance Capability and Alliance Performance. Int. Bus. Rev. 2012, 21, 891–905. [Google Scholar] [CrossRef]

| Respondent | Category | N | % |

|---|---|---|---|

| Gender | Male | 607 | 43.32 |

| Female | 794 | 56.68 | |

| Education | Primary School | 268 | 19.13 |

| Junior High School | 223 | 15.91 | |

| Senior High School | 636 | 45.39 | |

| Diploma | 36 | 2.57 | |

| Undergraduate | 133 | 9.49 | |

| Master/Doctoral | 8 | 0.58 | |

| No education | 97 | 6.93 | |

| Age (year) | <20 | 15 | 1.08 |

| 21–30 | 247 | 17.63 | |

| 31–39 | 392 | 27.98 | |

| >40 | 747 | 53.31 | |

| Business age (year) | 1–3 | 289 | 20.6 |

| 3–5 | 190 | 13.56 | |

| >5 | 922 | 65.81 |

| Dimension | Mean | Factor Loading | Validity | Reliability | |

|---|---|---|---|---|---|

| Internal–Organization (IOM) | IOM1 | 3.38 | 0.749 | 0.731 | 0.775 |

| IOM2 | 3.37 | 0.792 | |||

| IOM3 | 3.28 | 0.790 | |||

| IOM4 | 3.22 | 0.761 | |||

| Internal–Marketing (IPE) | IPE2 | 3.45 | 0.757 | 0.767 | 0.755 |

| IPE3 | 3.52 | 0.777 | |||

| IPE4 | 3.20 | 0.807 | |||

| IPE5 | 3.44 | 0.698 | |||

| Internal–Technical (ITS) | ITS1 | 3.28 | 0.806 | 0.785 | 0.816 |

| ITS2 | 3.23 | 0.772 | |||

| ITS3 | 3.17 | 0.842 | |||

| ITS4 | 3.15 | 0.794 | |||

| Internal–Technology (ITG) | ITG2 | 2.37 | 0.894 | 0.811 | 0.932 |

| ITG3 | 2.20 | 0.920 | |||

| ITG4 | 2.30 | 0.928 | |||

| ITG5 | 2.30 | 0.905 | |||

| External–Industry (EIN) | EIN1 | 3.48 | 0.794 | 0.690 | 0.776 |

| E1N2 | 3.24 | 0.857 | |||

| EIN3 | 3.27 | 0.842 | |||

| ERM–Financial Risk (RKE) | RKE1 | 3.34 | 0.732 | 0.633 | 0.662 |

| RKE2 | 3.74 | 0.819 | |||

| RKE3 | 3.91 | 0.710 | |||

| RKE4 | 3.89 | 0.555 | |||

| ERM–Marketing Risk (RP) | RP1 | 3.54 | 0.780 | 0.660 | 0.702 |

| RP2 | 3.82 | 0.833 | |||

| RP3 | 3.72 | 0.765 | |||

| Performance–Market Share (EPP) | EPP1 | 3.37 | 0.920 | 0.743 | 0.904 |

| EPP2 | 3.38 | 0.933 | |||

| EPP3 | 3.39 | 0.896 | |||

| Performance–Profitability (EPF) | EPF1 | 3.39 | 0.887 | 0.742 | 0.887 |

| EPF2 | 3.47 | 0.915 | |||

| EPF3 | 3.43 | 0.909 | |||

| No. | Variable | Validity | Reliability | Factor Loading |

|---|---|---|---|---|

| 1 | Internal | 0.768 | 0.782 | IOM = 0.853 |

| IP E = 0.820 | ||||

| ITS = 0.879 | ||||

| ITG = 0.609 | ||||

| 2 | External | 0.69 | 0.776 | EIN1 = 0.794 |

| EIN2 = 0.857 | ||||

| EIN3 = 0.842 | ||||

| 3 | Risk Management | 0.5 | 0.711 | RKE = 0.882 |

| RPE = 0.882 | ||||

| 4 | Performance | 0.5 | 0.891 | EPP = 0.950 |

| EP = 0.950 |

| Hypothesis | Correlation | Coefficient | Significance (1-Tailed) |

|---|---|---|---|

| 1 | Internal–Performance | 0.506 ** | 0.000 |

| 2 | External–Performance | 0.512 ** | 0.000 |

| 3 | Risk–Performance | 0.449 ** | 0.000 |

| Variable | R Square | Unstandardized Coefficient | Standardized Coefficient Beta | t | Sig | |

|---|---|---|---|---|---|---|

| Beta | Std. Error | |||||

| (Constant) | 0.112 | 0.000 | ||||

| Internal | 0.452 | 0.378 | 0.031 | 0.310 | 12.012 | 0.000 |

| External | 0.254 | 0.027 | 0.247 | 9.494 | 0.000 | |

| Risk | 0.450 | 0.024 | 0.374 | 18.586 | 0.000 | |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hanggraeni, D.; Ślusarczyk, B.; Sulung, L.A.K.; Subroto, A. The Impact of Internal, External and Enterprise Risk Management on the Performance of Micro, Small and Medium Enterprises. Sustainability 2019, 11, 2172. https://0-doi-org.brum.beds.ac.uk/10.3390/su11072172

Hanggraeni D, Ślusarczyk B, Sulung LAK, Subroto A. The Impact of Internal, External and Enterprise Risk Management on the Performance of Micro, Small and Medium Enterprises. Sustainability. 2019; 11(7):2172. https://0-doi-org.brum.beds.ac.uk/10.3390/su11072172

Chicago/Turabian StyleHanggraeni, Dewi, Beata Ślusarczyk, Liyu Adhi Kasari Sulung, and Athor Subroto. 2019. "The Impact of Internal, External and Enterprise Risk Management on the Performance of Micro, Small and Medium Enterprises" Sustainability 11, no. 7: 2172. https://0-doi-org.brum.beds.ac.uk/10.3390/su11072172