Research on Risk Avoidance and Coordination of Supply Chain Subject Based on Blockchain Technology

1

School of Economics and Management, Tianjin Polytechnic University, Tianjin 300387, China

2

School of Management and Economics, Tianjin University, Tianjin 300072, China

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(7), 2182; https://0-doi-org.brum.beds.ac.uk/10.3390/su11072182

Submission received: 6 March 2019

/

Revised: 28 March 2019

/

Accepted: 8 April 2019

/

Published: 11 April 2019

Abstract

:Based on the influence of block chain technology on information sharing among supply chain participants, mean-CVaR (conditional value at risk) is used to characterize retailers’ risk aversion behavior, while a Stackelberg game is taken to study the optimal decision-making of manufacturers and retailers during decentralized and centralized decision-making processes. Finally, the mean-CVaR-based revenue-sharing contract is used to coordinate the supply chain and profit distribution. The research shows that, under the condition of decentralized decision-making, when the retailer’s optimal order quantity is low, it is an increasing function of the weighted proportion and the risk aversion degree, while, when the retailer’s optimal order quantity is high, it is an increasing function of the weighted proportion, and has nothing to do with the risk aversion degree. The manufacturer’s blockchain technology application degree is a reduction function of the weighted proportion. When the retailer’s order quantity is low, the manufacturer’s blockchain technology application degree is a decreasing function of risk aversion, while, when the retailer’s order quantity is high, the manufacturer’s blockchain technology application is independent of risk aversion. The profit of the supply chain system under centralized decision-making is higher than that of decentralized decision-making. The revenue sharing contract can achieve the coordination of the supply chain to the level of centralized decision-making. Through blockchain technology, transaction costs among members of the supply chain can be reduced, information sharing can be realized, and the benefits of the supply chain can be improved. Finally, the specific numerical simulation is adopted to analyze the weighted proportion, risk aversion and the impact of blockchain technology on the supply chain, and verify the relevant conclusions.

1. Introduction

With the continuous development of society, the advantages of blockchain technology itself have gradually become the focus of attention in the financial field. However, at present, blockchain technology and supply chain are less integrated. Only some supply chain financial enterprises apply blockchain technology. For example, IBM and many companies build blockchain technology alliances in the supply chain environment, and Wal-Mart builds pork supply chain to ensure food safety. The application of Block Chain 2.0 intelligent contract technology in supply chain realizes distributed accounting process, guarantees transaction security, resolves information asymmetry, reduces transaction risk, it does not need any intermediary agencies or intermediaries to intervene, and automatically completes transactions through intelligent contracts [1]. The information sharing characteristics of blockchain technology make the transactions of upstream and downstream members of the supply chain more transparent and can fully utilize the resources of upstream and downstream supply chains to reduce transaction costs and protect the environment [2,3]. This paper focuses on the application of blockchain technology in the supply chain for solving the problem of real-time information sharing among participants. Therefore, it is of great significance to apply blockchain technology to the supply chain to solve the problem of information asymmetry and high transaction cost currently faced by the supply chain.

At present, there are many studies on supply chain coordination under risk aversion, but no scholars have studied the risk aversion and coordination research of supply chain under the influence of blockchain technology. Research on the use of blockchain technology in the supply chain mainly focuses on traceability and credit issues. Chow [4] showed that blockchain technology can enhance supply chain transparency and management mechanisms. Kristoffer [5] started from the concept of technological innovation and used technical theory to construct a basic framework for realizing supply chain traceability. Kim [6] translated relevant agreements into smart contracts and used the traceability ontology to design the blockchain. N Kshetri [7] studied the role of blockchain technology in tracking insecure factors in the Internet of Things (IoT) supply chain, and further explored IoT security vulnerabilities through blockchain technology with the aim to prevent security vulnerability. Saveen A [8] analyzed the potential advantages of blockchain technology in manufacturing supply chains and proposed the future blockchain manufacturing supply chain. Xiwei Xu [9] used blockchain technology to solve the mistrust problem of supply chain participants and to build a sharing agreement for supply chain participants. Solving the trust problem of collaborative process execution through blockchain smart contracts does not require the involvement of any intermediary. Related research on supply chain risk aversion is mainly carried out by using mean-variance analysis [10], value at risk (VaR) [11,12], and conditional value at risk (CVaR) [13,14,15,16]. The risk measurement technology of CVaR, as proposed by Rockefeller et al. [17,18], can not only simplify the calculation method of CVaR, but also effectively measure the average return below a certain threshold. It can also overcome the shortcomings of VaR to some extent, and it is not easy to manipulate illegally. However, the shortcoming of CVaR is that it only measures the average value below the risk-based quantile, while ignoring the part above the quantile, which makes the decision-making target of the decision makers lower and the profit expectations decrease. To improve the defects of the CVaR criterion, Mu Yongguo et al. [19] used the mean-CVaR method to construct the wholesale price contract and the second-order contract optimal order quantity model and studied different price contract models under the uncertainty demand and risk aversion assumptions, the impact on supply chain revenues and the impact of extreme risk events on earnings. Xu M and Li J [20] adopted the mean-CVaR theory to study the optimal decision of the supply chain newsboy model when there is a stock-out cost. Gao Fei et al. [21] used the mean-CVaR model to study the inventory risk hedging problem of seasonal products. Then, they discussed that the hedging strategy can increase the order quantity and found that the method can increase the expected profit and the downside risk profit. Chen Yuke et al. [22] constructed a mathematical model based on mean-CVaR to measure the retailer’s risk characteristics, analyzed the optimal decision-making of closed-loop supply chain members in decentralized and joint decision-making, and proved that mean-CVaR can improve the retailer’s order quantity and return better than CVaR. The multi-level Stackelberg game model and the Nash equilibrium are used to solve the equilibrium decision of supply chain participants. In this paper, mean-CVaR is employed to describe the risk aversion behavior of supply chain members under Stackelberg, based on which the equilibrium decision of each participant in the supply chain is discussed.

The contributions of this paper are mainly embodied in three aspects:

- (1)

- This paper takes the influence of blockchain technology on the information sharing of the supply chain as the reference, solving the supply–demand matching problem in the supply chain with different information sharing degree.

- (2)

- The mean-CVaR model is adopted to describe the decision-making of each decision-maker in the supply chain under different risk aversion, which overcome the shortcomings of the CVaR model.

- (3)

- Based on the above, the mean-CVaR-based revenue sharing contract is designed to coordinate and distribute the revenue of the supply chain.

The remainder of this paper is organized as follows. Section 2 describes the article and related assumptions. Section 3 shows the optimal order quantity of the retailer under the decision-making situation, the optimal production volume of the manufacturer and the optimal blockchain technology application degree of the upstream and downstream members of the supply chain. Section 4 studies the optimal decision of the concentrated situation. Section 5 elaborates the coordination design and profit distribution of the supply chain based on the mean-CVaR revenue sharing contract. Section 6 is a specific numerical analysis. Section 7 gives the relevant conclusions drawn from this paper and presents the shortcomings of this paper.

2. Problem Description and Related Assumptions

Based on the premise of the impact of blockchain technology on the supply chain, and, similar to existing research, to facilitate modeling, we only consider a two-level supply chain consisting of a risk-averse retailer and a risk-neutral manufacturer and use blockchain technology to quantitatively realize information sharing between manufacturers and retailers. Based on this, a Stackelberg game is used to explore the optimal decision-making problem of upstream and downstream members of the supply chain, and to solve the supply and demand matching problem between manufacturers and retailers. In the two-level supply chain system, we assume that the retailer is dominant, and manufacturers are responsible for producing multi-cycle products. In this paper, the multi-cycle is abstracted into the single-cycle problem. Both the manufacturer’s production and the retailer’s order are related to the degree () of the blockchain technology used by the upstream and downstream decision makers in the supply chain i.e. the sharing degree of inventory, sales, credit and other information among participants in the supply chain. During the sales period, the retailer sends order quantity to the manufacturer, and , where is the order quantity of the retailer in the last cycle after considering other factors affecting demand. In this paper, we only consider the impact of the application of blockchain technology on the supply and demand of upstream and downstream members of the supply chain. is the retailer’s sensitivity to the manufacturer’s blockchain application level, and , . Manufacturers predict organizational production based on demand , where is the sensitivity of the manufacturer to the extent of retailer blockchain application, and , . When information is shared, it will bring additional benefits to the participants of upstream and downstream supply chains, or in other words, the transaction cost is saved, which is related to the degree of information sharing. The transaction cost is the cost of finding a partner and is related to the transparency of the information of the partner. For example, the transaction cost saved by the manufacturer is , where is the transaction cost generated by a single search for the manufacturer’s partner. It is assumed that the market stochastic demand is , and the probability distribution function and the probability density function are and , respectively. Let and is assumed to satisfy the IFRD characteristics. This hypothesis is generally adopted in the research on supply chain finance and can guarantee the uniqueness and existence of the objective function in the solution process. Many distributions, such as normal distribution, exponential distribution and uniform distribution can satisfy the characteristics. is the production cost of the unit product; is the wholesale price of the unit product; is the sales price of the unit product; and is the residual value of the unsold product at the end of the period.

Based on the assumptions, the revenues of retailers and manufacturers are

CVaR is a method proposed by Rockafellar and Uryasev [18] to measure the degree of risk, mainly considering the average benefit below the quantile, and the CVaR model is also a consistent risk measurement model with sub-additive. To some extent, overcoming the shortcomings of VaR has become a common tool in supply chain risk decision-making. CVaR is usually defined as

However, the CVaR model only measures the average below the quantile yield, while ignoring the fraction above the quantile, which makes the decision maker’s decision-making goal too conservative because, when is small, the CVaR model only measures the risk aversion of the decision maker, while ignoring a large part of the income; and, when is large, the CVaR model measures most of the benefits, but fails to reflect the risk attitude of the decision makers. To overcome the shortcomings of the CVaR model, this paper uses mean-CVaR to measure the decision maker of risk aversion. It is a convex combination of the expected return and CVaR, thus maximizing the risk-avoiding decision maker’s expected return and minimizing the down-risk profit. The mean-CVaR model is as follows:

3. Decentralized Decision Model of Supply Chain Based on Mean-CVaR

Under the condition that the upstream and downstream members of the supply chain apply the blockchain technology, the manufacturer and retailer first determine the application degree of the blockchain before the start of the sales season. After the start of the sales season, the retailer purchases the product at the wholesale price according to his own ordering demand and sells it at the selling price . At the end of the period, if the market demand is less than the order quantity of the retailer, then the remaining products are treated with the residual value .

3.1. Optimal Decision of Retailers Based on Mean-CVaR

In the case of decentralized decision making, the retail problem is to seek the optimal order quantity and the application level of the blockchain to maximize its own revenue. First, we give the optimal quantile of CVaR when the risk aversion is under the CVaR criterion.

Theorem 1.

In the two-level Stackelberg game, under thecriterion, given the condition of the risk aversion, there is an optimalthat makes

Proof.

Substituting Equation (1) into Equation (3), we can obtain

where , , . ☐

Furthermore, it can be obtained by the first-order conditions

Notice that

Thus, we can conclude that is a strictly concave function with , therefore, and thus we can obtain .

Substituting into CVaR model yields

Theorem 2.

Under the mean-CVaR criterion, the optimal order quantity of the retailer and the optimal blockchain application level of the supplier are

Proof.

Substituting and into model yields

☐

According to the first-order conditions, we have

Furthermore, the second-order conditions yields

Thus, is a convex function with; then, from the first-order conditions, we have

Theorem 3.

(1) For any fixed, the optimal order quantity of retaileris a strict increasing function with the weighted proportion; The manufacturer’s optimal blockchain application degreeis a strict decreasing function with the weighted proportion. (2) For any fixed, when, the optimal order quantity of retailerand the manufacturer’s optimal blockchain application degreeare not affected by risk aversion degree; and when, the optimal order quantity of retaileris a strict increasing function with risk- aversion and the manufacturer’s optimal blockchain application degreeis a strict decreasing function with risk- aversion.

Proof.

According to Theorem 2, when , is an increasing function with and . is a monotonous non-reducing function. Thus, the optimal order quantity of retailer is an increasing function with and. The optimal blockchain application level of the manufacturer is a decreasing function with and ; when , we can easily obtain is an increasing function with , thus the optimal order quantity of retailer is an increasing function with and the manufacturer’s optimal blockchain application degree is a decreasing function with and . ☐

3.2. Optimal Decision of the Manufacturer

In the retailer-led Stackelberg game, the manufacturer’s problem is to determine the optimal wholesale price and the optimal blockchain application level to maximize its revenue. From Equation (2), the manufacturer’s decision function is as follows:

Furthermore, Equation (13) can be written as

Theorem 4.

In the two-level Stackelberg game, to maximize the profit of the manufacturer, the retailer’s optimal blockchain application level and the optimal wholesale price are determined by the following equation.

Proof.

(1) if , the Hessian matrix of with and is

☐

Thus, the hessian matrix of with and is non-negative definite. However, is an increasing function with , and the wholesale must satisfy , in order to maximize the profits of the manufacture, then we can obtain. If , we can easily obtain ; if , according to the first order , thus .

(2) If , the optimal order quantity of the retailer satisfies

In this case, we can get the hessian matrix of with and is negative definite. The first order yields

If , the retailer’s optimal blockchain application level and the optimal wholesale price are as follows

If , the retailer’s optimal blockchain application level and the optimal wholesale price are as follows

(3) If , the optimal order quantity of the retailer satisfies .

In this case, we can get the hessian matrix of with and is negative definite. The first order, yields

If , the retailer’s optimal blockchain application level and the optimal wholesale price are as follows

If , the retailer’s optimal blockchain application level and the optimal wholesale price are as follows

4. Centralized Decision Model of the Supply Chain

When manufacturers and retailers make decisions in a centralized manner, they can be assumed to be a risk-neutral decision-making body. we use the superscript “c” to represent the centralized decision model. Then, the profit of centralized decision-making is as follows

Furthermore, Equation (23) can be written as

Since , according to the first order, the optimal order quantity of retailers in centralized decision making is . Then, we can obtain the total profit of the supply chain in centralized decision making as .

5. Revenue Sharing Contract of Supply Chain Based on Blockchain Technology and Mean-CVaR Criteria

In the context of decentralized decision-making, Spengler [23] pointed out that both upstream and downstream sides of the supply chain engage in a Stackelberg game. Each side attempts to maximize their own interests, giving cause to the double marginalization effect across supply chain members. Consequently, the overall profit of the supply chain system will be lower than the return achieved by a centralized model for decision-making. Contract coordination is a condition necessary to improve supply chain performance. Using contract coordination can effectively eliminate the double marginalization effect across supply chain members. In addition, the gap between decentralized decision-making and centralized decision-making can be closed, which has the potential to generate profits. Furthermore, the use of contract coordination design can take full advantage of any resources inside and outside the supply chain.

If the retailer and the manufacturer reach an agreement, the manufacturer shall provide the retailer with a lower wholesale price at the beginning of the contract period. At the end of the contract, the members of both parties shall distribute the overall profit of the supply chain according to the proportion that was agreed. Assuming that the manufacturer’s share is , the retailer’s share is , and we use the superscript “rs” to represent the revenue-sharing contract. Then, the profits of supply chain members are as follows:

Using the inverse derivation method, we firstly solve the optimal order quantity of the retailer under the mean-CVaR criterion and the application degree of the optimal blockchain of the manufacturer. On this basis, we apply the revenue sharing contract to solve the optimal wholesale price of the manufacturer and the application of the retailer’s optimal blockchain, finally reaching the coordination of the supply chain.

Theorem 5.

Under the coordination of mean-CVaR criteria and revenue sharing contract, the optimal wholesale priceand the optimal blockchain application level of the manufacturer are as follows

Proof.

Under the coordination of the revenue-sharing contract, similar to the proof process of Theorem 2, it is easy to conclude that the optimal order quantity of the retailer is

☐

To make the profits of the supply chain system achieve the effect of centralized decision-making, we must satisfy . We can easily conclude that the optimal wholesale price is

According to , we can obtain .

Theorem 6.

Under the coordination of mean-CVaR criteria and revenue-sharing contract, the optimal blockchain application level of retaileris

Proof.

For the manufacturer, substituting into Equation (24) yields

☐

Furthermore, Equation (28) can be written as

(1) If , according to the first order , if , we can easily obtain, and, if , then combined with Theorem 5, the optimal blockchain application level of the retailer is as follows

(2) If , according to the first order , the optimal blockchain application level of the retailer is as follows

Under the condition of satisfying Theorems 5 and 6, to enable the upstream and downstrea-m members of the supply chain to accept the contract and achieve the perfect coordination of the supply chain, the revenue distribution ratio must also satisfy the following inequality group.

Therefore, under mean-CVaR criterion, the profits of supply chain system coordinated by revenue sharing contract are as follows:

Under the coordination of revenue sharing contract, when the wholesale price of the manufacturer satisfies Theorem 5, and satisfies Equations (31) and (32), the supply chain based on the blockchain technology and the mean-CVaR achieves a perfect coordination state.

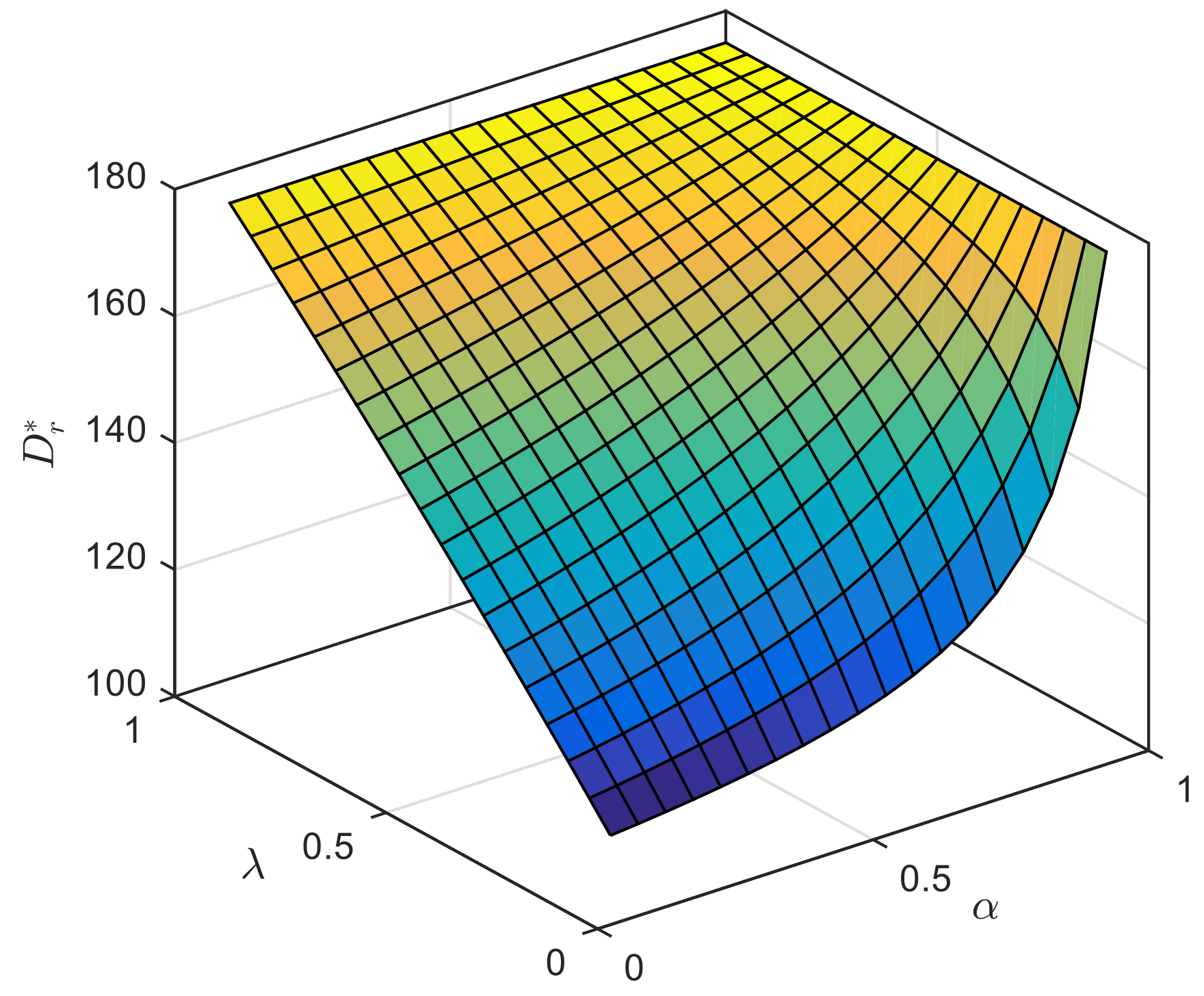

6. Numerical Examples

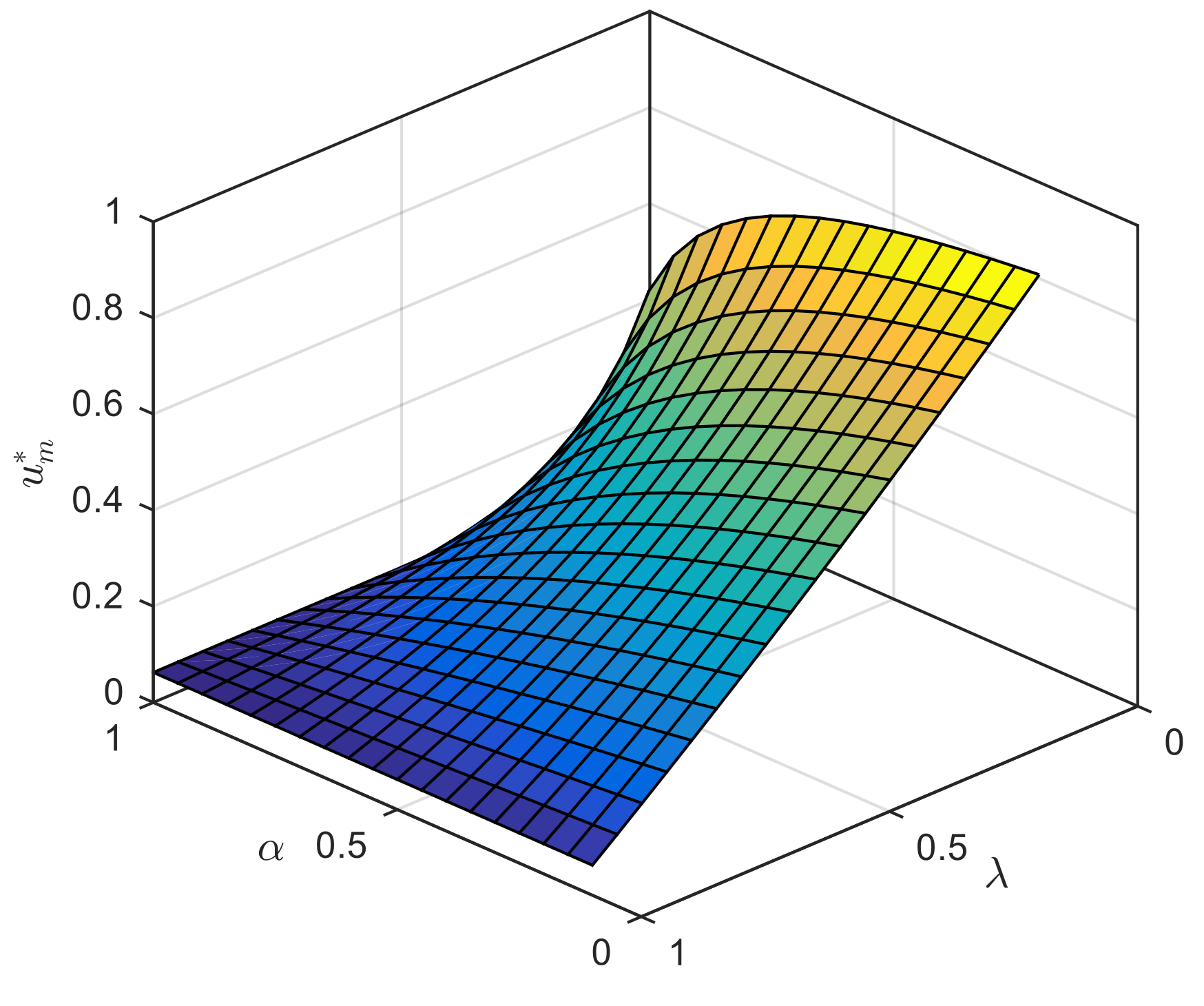

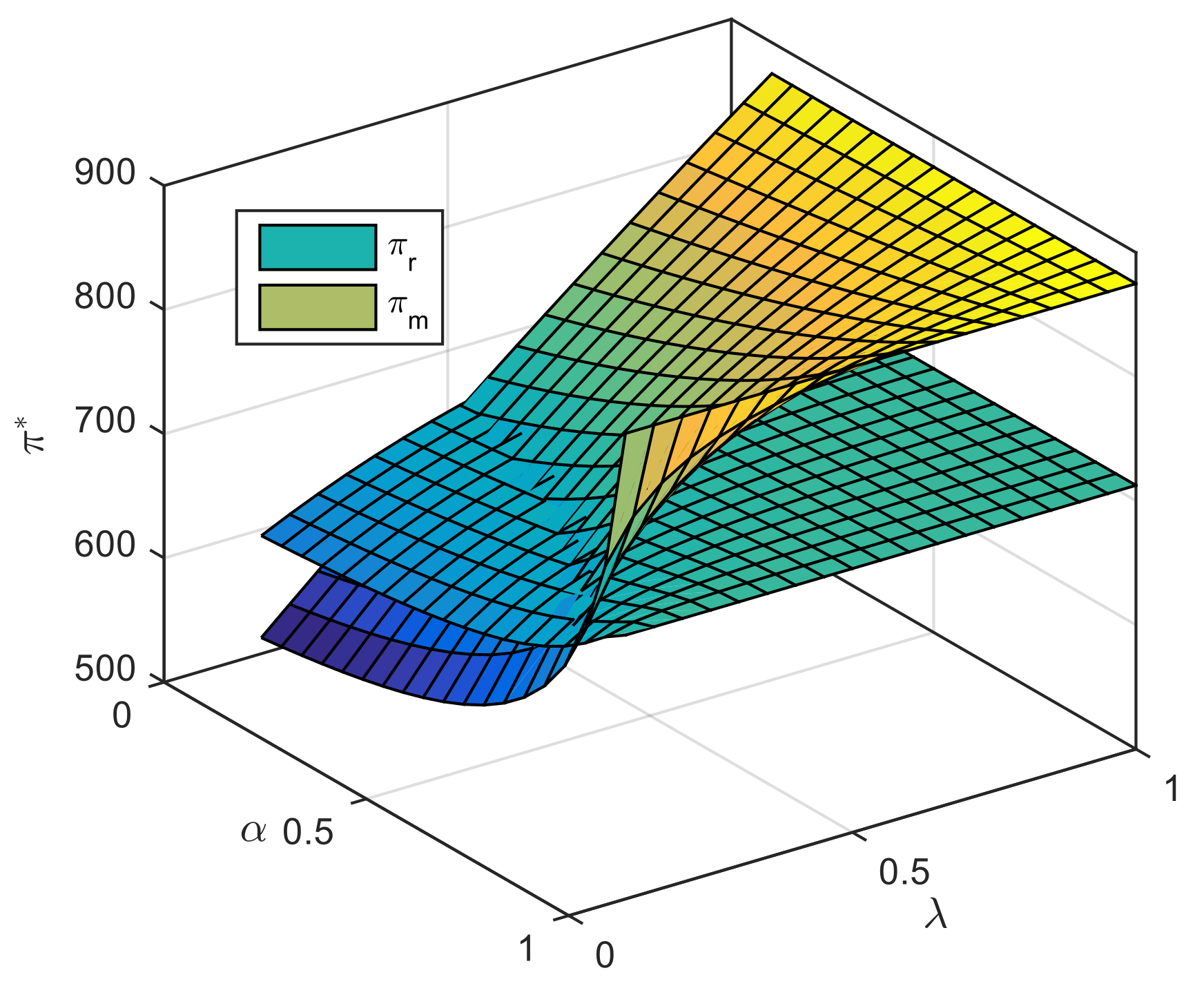

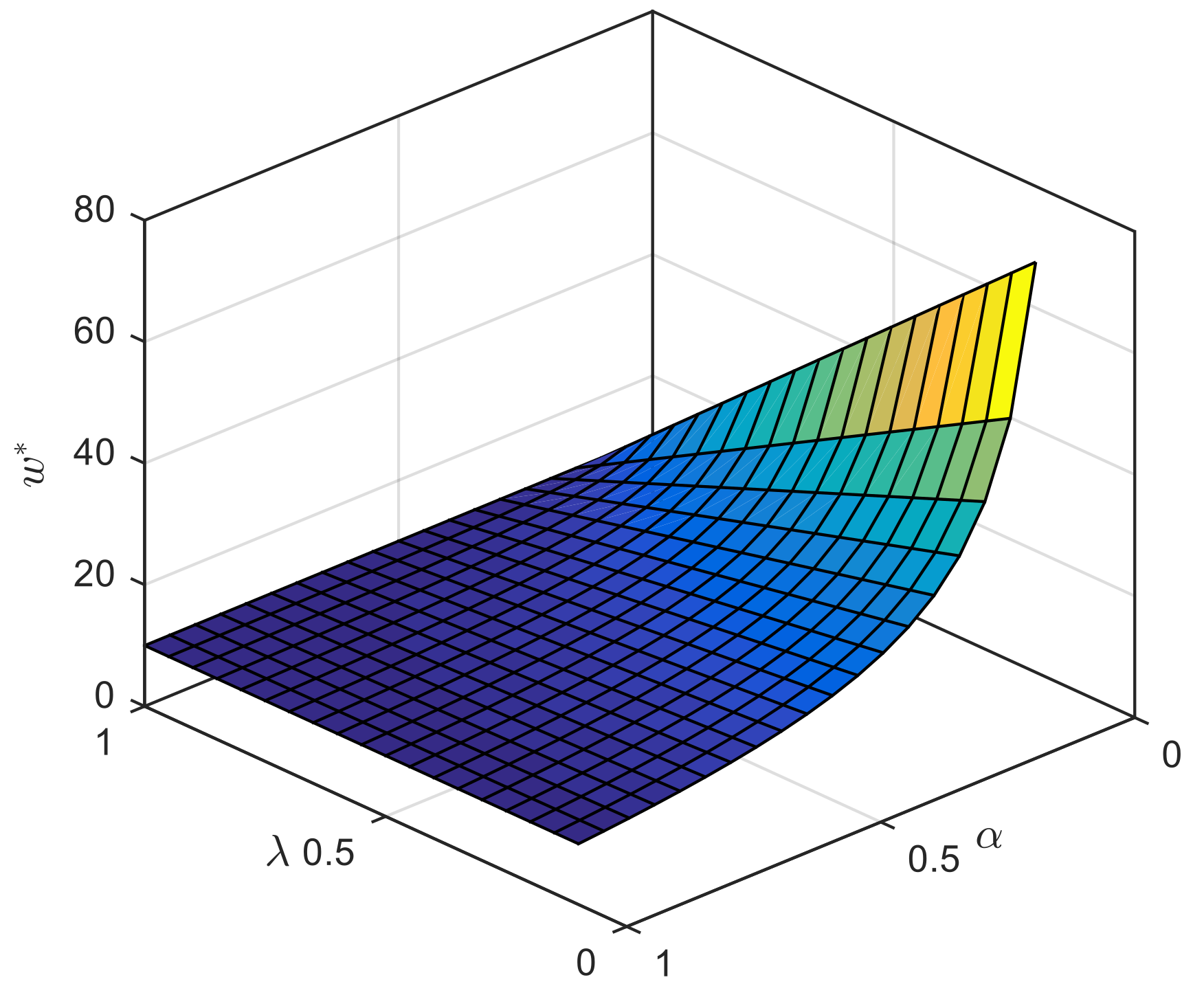

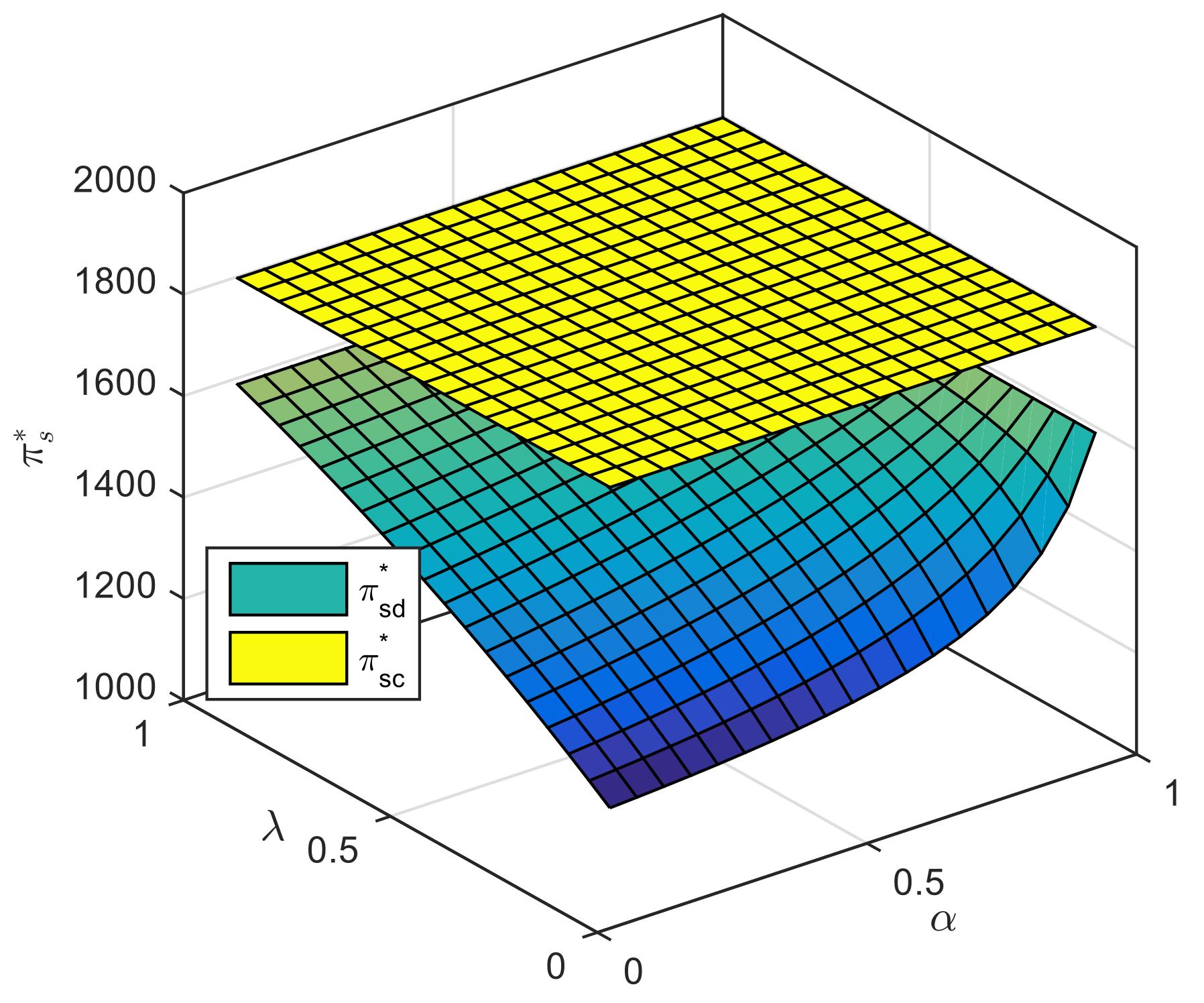

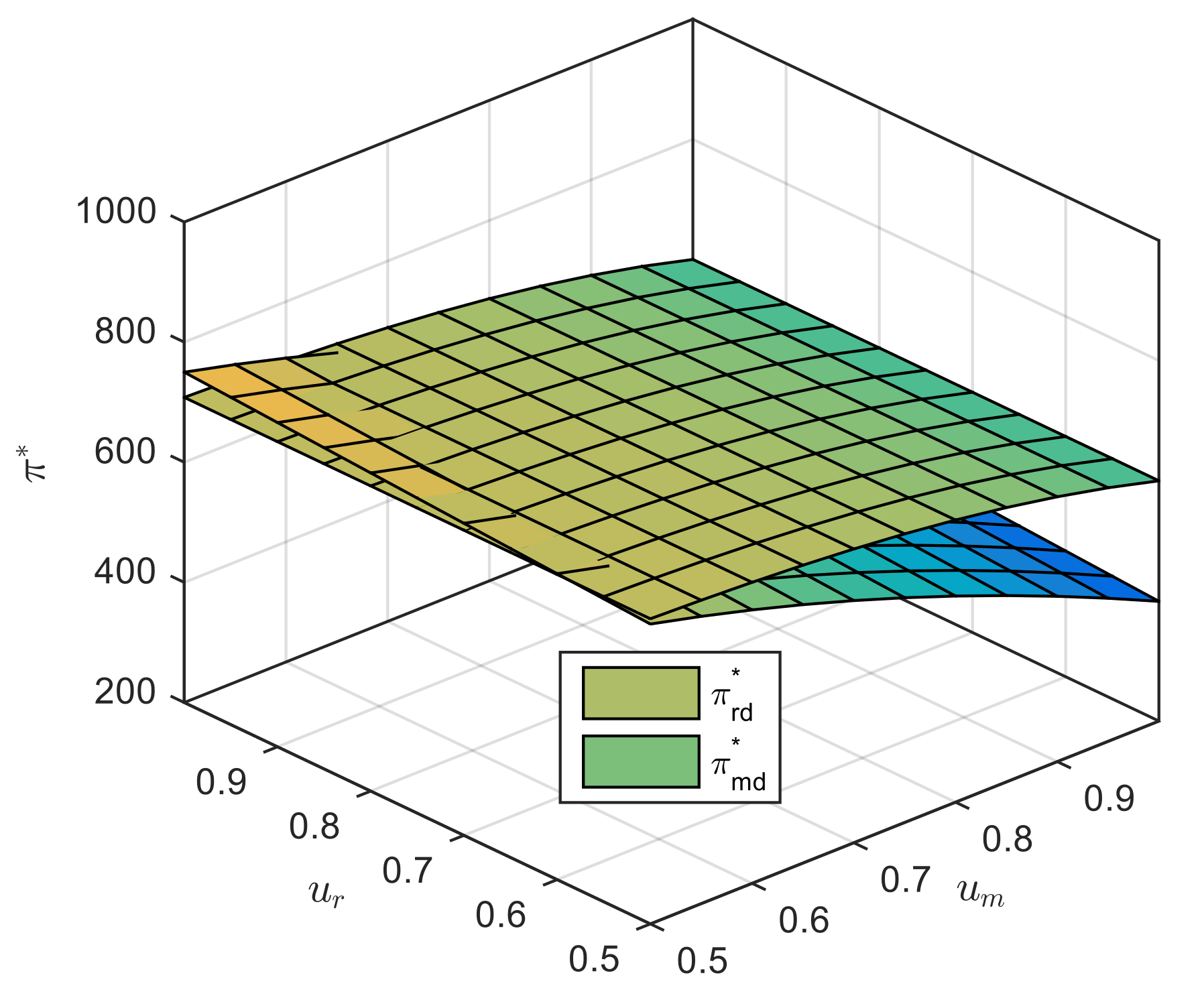

We explored the equilibrium solutions of supply chain systems under various decision-making conditions by using MATLAB to conduct numerical simulations and analyzed the impact of different parameters on the profits of supply chain members. It was assumed that market demand obeys the uniform distribution of and , , , , , , and . Figure 1 shows that, under the mean-CVaR criterion, the retailer’s optimal order quantity is an increasing function of weighted proportion and risk aversion . Especially when is fixed, if indicates that the retailer’s preference is close to risk neutrality, the optimal order quantity approximates the risk-neutral optimal order quantity; when is certain, if , then the retailer’s optimal order quantity approximates the risk-neutral optimal order quantity. According to Figure 2, the manufacturer’s blockchain application degree is a strict decreasing function with weighted proportion and risk aversion . Figure 3 shows that, under the decentralized decision, if weighted proportion is constant, the retailer’s target profit is an increasing function with risk aversion. If risk aversion degree is constant, the retailer’s target profit is also an increasing function of weighted proportion , and the retailer’s target profit is kept constant after the increase of the risk aversion and the weighted proportion. Figure 4 shows that, under the decentralized decision-making conditions, the manufacturer’s wholesale price is a decreasing function with weighted proportion , but an increasing function with risk aversion , which indicates that the retailer’s order quantity decreases if the retailer’s risk aversion increases, and, to guarantee their own profits, manufacturers will increase the wholesale price appropriately. It can be seen in Figure 5 that, under the condition of decentralized decision-making, the system revenue of the supply chain is an increasing function of weighted proportion and risk aversion . However, no matter how it changes, the system benefit of decentralized decision-making is less than that of centralized decision-making. Figure 6 shows that the retailer’s revenue and the manufacturer’s revenue are related to the degree of application blockchain technology.

Next, we analyzed the impact of , and blockchain technology on the revenue of the supply chain system, as shown in Table 1. Table 1 shows that the higher the application of blockchain technology is, the higher the profit of the supply chain system is. Blockchain technology can reduce the transaction cost among the members of the supply chain and realize information sharing, thereby improving the overall revenue of the supply chain. Table 1 also shows that, under the coordination of revenue sharing contracts, the revenue of the supply chain system reaches the level of centralized decision-making.

Furthermore, we present the impact of the revenue sharing parameter on the manufacturer’s wholesale price, the manufacturer’s revenue, the retailer’s revenue, and the overall supply chain’s revenue under the revenue sharing contract in Table 2. Table 2 shows that, under the coordination of the revenue sharing contract, the wholesale price decreases with the increase of shared parameter , while the retailer’s income increases with the increase of shared parameter , and the manufacturer’s income increases with sharing parameter , but the retailer and the manufacturer gain and set the value to reach the level of centralized decision making.

7. Conclusions

In this paper, a two-level supply chain composed of manufacturers and retailers is constructed. Based on the influence of blockchain technology on the information sharing of the supply chain, mean-CVaR is used to describe the risk aversion behavior of retailers. The Stackelberg game is also taken to study the optimal decision-making and expected revenue of participants in a two-level supply chain composed of manufacturers and retailers in decentralized and centralized decision-making. On this basis, a revenue-sharing contract based on mean-CVaR is designed to coordinate the supply chain. The research shows that, under the condition of decentralized decision-making, when the retailer’s optimal order quantity is low, the retailer’s optimal order quantity is an increasing function of the weighted proportion and the risk aversion degree; and, when the retailer’s optimal order quantity is high, the optimal order quantity is an increasing function of the weighted proportion, and has nothing to do with the retailer’s risk aversion. The manufacturer’s blockchain technology application degree is a strict decreasing function of the weighted proportion. When the retailer’s order quantity is low, the manufacturer’s blockchain technology application degree is a decreasing function of the risk aversion degree, while, when the retailer’s order quantity is high, the manufacturer’s blockchain technology application degree is independent of the risk aversion. The benefits of the supply chain system under centralized decision-making are higher than those of decentralized decision-making, and the mean-CVaR revenue-sharing contract can achieve the coordination of the supply chain for reaching the level of centralized decision-making. Blockchain technology can reduce transaction costs among supply chain members, realize information sharing, and improve the profits of the supply chain.

Although the model proposed in this paper has some practical significance for the integration design of blockchain technology and the risk aversion supply chain, it still has some limitations. Firstly, to simplify the analysis, the manufacturer’s production and the retailer’s order quantity are simplified as a function of the block chain applicability and the previous order quantity. Secondly, we fail to consider the cost of goods out of stock. Therefore, in the next step, we will incorporate more factors into the model and conduct more in-depth research.

Author Contributions

The paper was written by F.L., and revised and checked by L.L. and E.Q. All authors read and approved the final manuscript.

Funding

This research was funded by National Social Science Foundation of China, grant number 15ZDB151 and the National Natural Science Foundation of China, grant number 7187020424.

Acknowledgments

The authors thank two anonymous referees for their valuable suggestions and comments that led to significant improvement in the exposition of the paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Yan, Y.; Zhang, J. A study on supply chain subject with a risk-aversion retailer based on block chain technology. Ind. Eng. Manag. 2018, 6, 33–42. [Google Scholar]

- Zhang, P.; Qin, G.; Wang, Y. Optimal Maintenance Decision Method for Urban Gas Pipelines Based on as Low as Reasonably Practicable Principle. Sustainability 2019, 11, 153. [Google Scholar] [CrossRef]

- Gou, Z.H. Promoting and implementing urban sustainability in China: An integration of sustainable initiatives at different urban scales. Habitat Int. 2018, 82, 83–93. [Google Scholar]

- Christine, C. Blockchain for good? Improving supply chain transparency and human rights management. Gover. Direct. 2018, 70, 39–40. [Google Scholar]

- Francisco, K.; Swanson, D. The supply chain has no clothes: Technology adoption of blockchain for supply chain transparency. Gover. Direct. 2018, 2, 2. [Google Scholar] [CrossRef]

- Kim, H.M.; Laskowski, M. Towards an ontology-driven blockchain design for supply chain provenance. Comput. Soc. 2016. [Google Scholar] [CrossRef]

- Kshetri, N. Can blockchain strengthen the internet of things? IT Prof. 2017, 19, 68–72. [Google Scholar] [CrossRef]

- Abeyratne, S.A.; Monfared, R.P. Blockchain ready manufacturing supply chain using distributed ledger. Int. J. Res. Eng. Technol. 2016, 5, 1–10. [Google Scholar]

- Xu, X.Q.; Riveret, R.; Governatori, G.; Ponomarev, A.; Mendling, J. Untrusted business process monitoring and execution using blockchain. In Proceedings of the International Conference on Business Process Management, Rio de Janeiro, Brazil, 18–22 September 2016; pp. 329–347. [Google Scholar]

- Xu, G.Y.; Zhang, X.M. Coordinating the dual-channel risk-averse supply chain based on price discount. J. Syst. Manag. 2016, 25, 1114–1120. [Google Scholar]

- Zhu, C.B.; Ji, J.H.; Bao, X. Optimal order policy based on VaR with a supply-risk-averse retailer. J. Syst. Manag. 2014, 23, 861–866. [Google Scholar]

- Wang, D.P.; Gu, C.L.; Chun, X. Research on coordinating a dual-channel supply chain base on risk-aversion. In Proceedings of the 2016 Chinese Control and Decision Conference (CCDC), Yinchuan, China, 28–30 May 2016; pp. 4519–4525. [Google Scholar]

- Dai, J.S. Supply chain coordination with sales effort based on CVaR. J. Syst. Eng. 2017, 32, 252–264. [Google Scholar]

- Huang, J.; Yang, W.S. Supply chain decision model based on supplier CVaR and buy-back commitments. Chin. J. Manag. 2016, 13, 1250–1256. [Google Scholar]

- Liu, L.; Li, F.T. Optimal decision of deferred payment supply chain considering bilateral risk-aversion degree. Math. Prob. Eng. 2018, 2018, 11. [Google Scholar] [CrossRef]

- Chen, Q. A deferred payment strategy for risk-averse supply chain based on CVaR. Int. J. Simul. Syst. Sci. Technol. 2016, 17, 17.1–17.7. [Google Scholar]

- Rockafellar, R.T.; Uryasev, S. Conditional value-at-risk for general loss distributions. J. Bank. Financ. 2002, 26, 1443–1471. [Google Scholar] [CrossRef]

- Rockafellar, R.T.; Uryasev, S. Optimization of conditional value-at-risk. J. Risk 2000, 2, 21–41. [Google Scholar] [CrossRef]

- Mu, Y.G.; Mai, Q.; Feng, Y.J. Mean-CVaR models of price-only contracts of supply chain. J. Harbin Inst. Technol. 2009, 41, 298–300. [Google Scholar]

- Xu, M.; Li, J. Optimal decisions when balancing expected profit and conditional value-at-risk in newsvendor models. J. Syst. Sci. Complex. 2010, 23, 1054–1070. [Google Scholar] [CrossRef]

- Gao, F.; Chen, F.Y.; Chao, X.L. Joint optimal ordering and weather hedging decisions: Mean-CVaR model. Flex. Serv. Manuf. J. 2011, 23, 1–25. [Google Scholar] [CrossRef]

- Chen, Y.K.; Xiong, L.; Dong, J.R. Closed-loop supply chain coordination mechanism based on mean-CVaR. Chin. J. Manag. Sci. 2017, 25, 68–77. [Google Scholar]

- Spengler, J.J. Vertical integration and antitrust policy. J. Polit. Econ. 1950, 58, 347–352. [Google Scholar] [CrossRef]

Figure 1.

Impact of and on the optimal order quantity of the retailer.

Figure 2.

Impact of and on the optimal blockchain application level.

Figure 3.

Impact of and on the profits of supply chain members in decentralized decision-making.

Figure 4.

Impact of and on wholesale price in decentralized decision-making.

Figure 5.

Impact of and on the system profit of supply chain.

Figure 6.

Impact of α and λ on the system profit of supply chain.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

The relationships among , and block chain technology.

| System Revenue | Blockchain Application | ||||

|---|---|---|---|---|---|

| Condition | |||||

| unused blockchain | 1000.0 | 1796.88 | 1796.88 | ||

| blockchain application of the supply chain members | 1587.5 | 1796.88 | 1796.88 | ||

| 1569.39 | 1796.88 | 1796.88 | |||

| 1503.57 | 1796.88 | 1796.88 | |||

| 1384.63 | 1796.88 | 1796.88 | |||

| 1236.48 | 1796.88 | 1796.88 | |||

| 1100.0 | 1796.88 | 1796.88 |

Table 2.

Impact of on revenue sharing contract.

| 0 | 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2.813 | 2.406 | 2.000 | 1.594 | 1.188 | 0.781 | 0.375 | −0.031 | −0.438 | −0.844 | −1.250 | |

| −582.8 | −241.4 | 100.0 | 441.41 | 782.81 | 1124.2 | 1465.6 | 1807.0 | 2148.4 | 2489.8 | 2831.3 | |

| 2379.7 | 2038.3 | 1696.9 | 1355.5 | 1014.1 | 672.7 | 331.3 | −10.15 | −351.6 | −692.9 | −1034.4 | |

| 1796.9 | 1796.9 | 1796.9 | 1796.9 | 1796.9 | 1796.9 | 1796.9 | 1796.9 | 1796.9 | 1796.9 | 1796.9 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Liu, L.; Li, F.; Qi, E. Research on Risk Avoidance and Coordination of Supply Chain Subject Based on Blockchain Technology. Sustainability 2019, 11, 2182. https://0-doi-org.brum.beds.ac.uk/10.3390/su11072182

AMA Style

Liu L, Li F, Qi E. Research on Risk Avoidance and Coordination of Supply Chain Subject Based on Blockchain Technology. Sustainability. 2019; 11(7):2182. https://0-doi-org.brum.beds.ac.uk/10.3390/su11072182

Chicago/Turabian StyleLiu, Liang, Futou Li, and Ershi Qi. 2019. "Research on Risk Avoidance and Coordination of Supply Chain Subject Based on Blockchain Technology" Sustainability 11, no. 7: 2182. https://0-doi-org.brum.beds.ac.uk/10.3390/su11072182

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.