The Relationship between Sustainable Development Practices and Financial Performance: A Case Study of Textile Firms in Vietnam

, and

, and

Abstract

:1. Introduction

2. Literature Review and Hypotheses Development

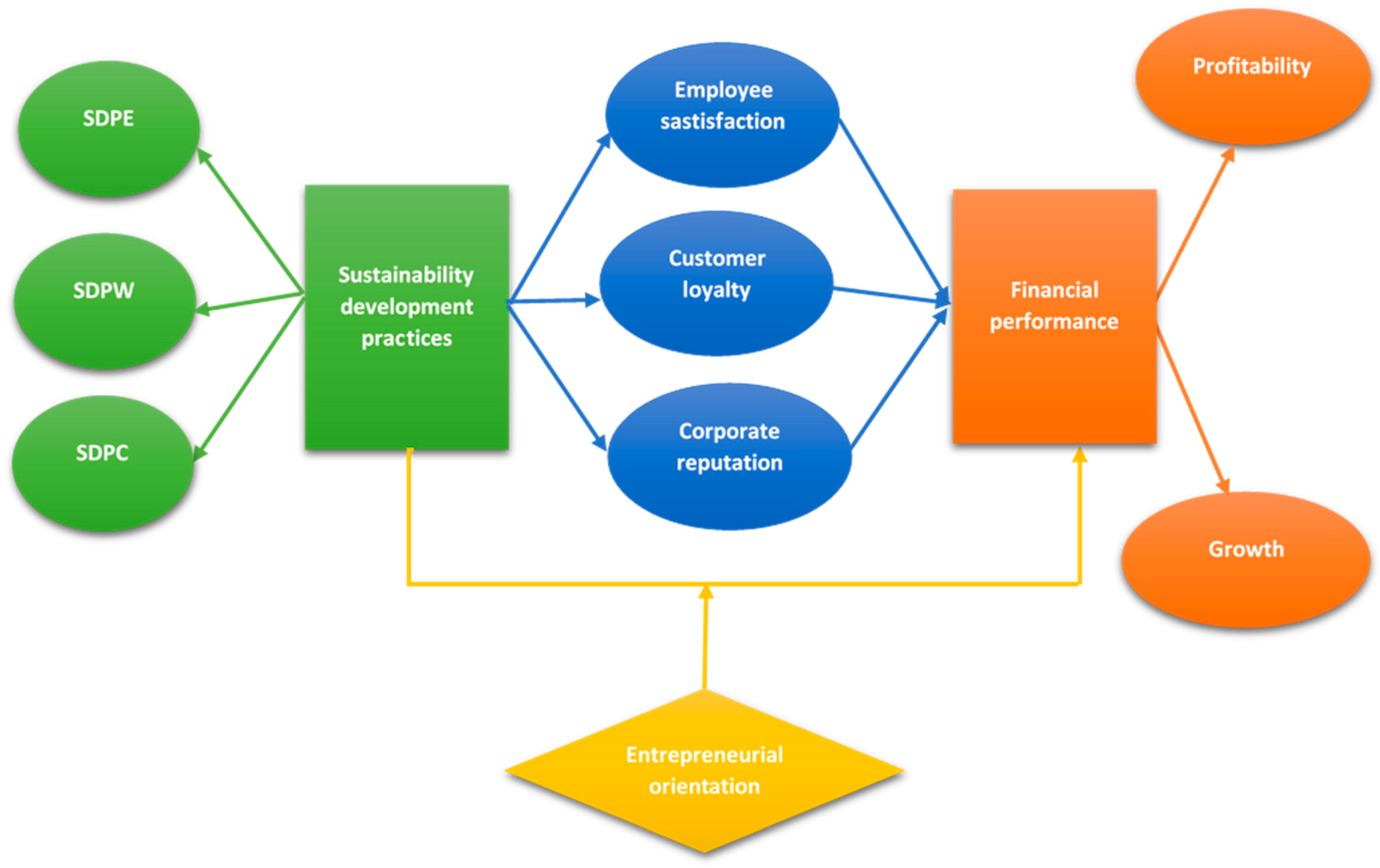

2.1. Sustainable Development Practices

2.2. Firm Financial Performance

2.3. Theoretical Background

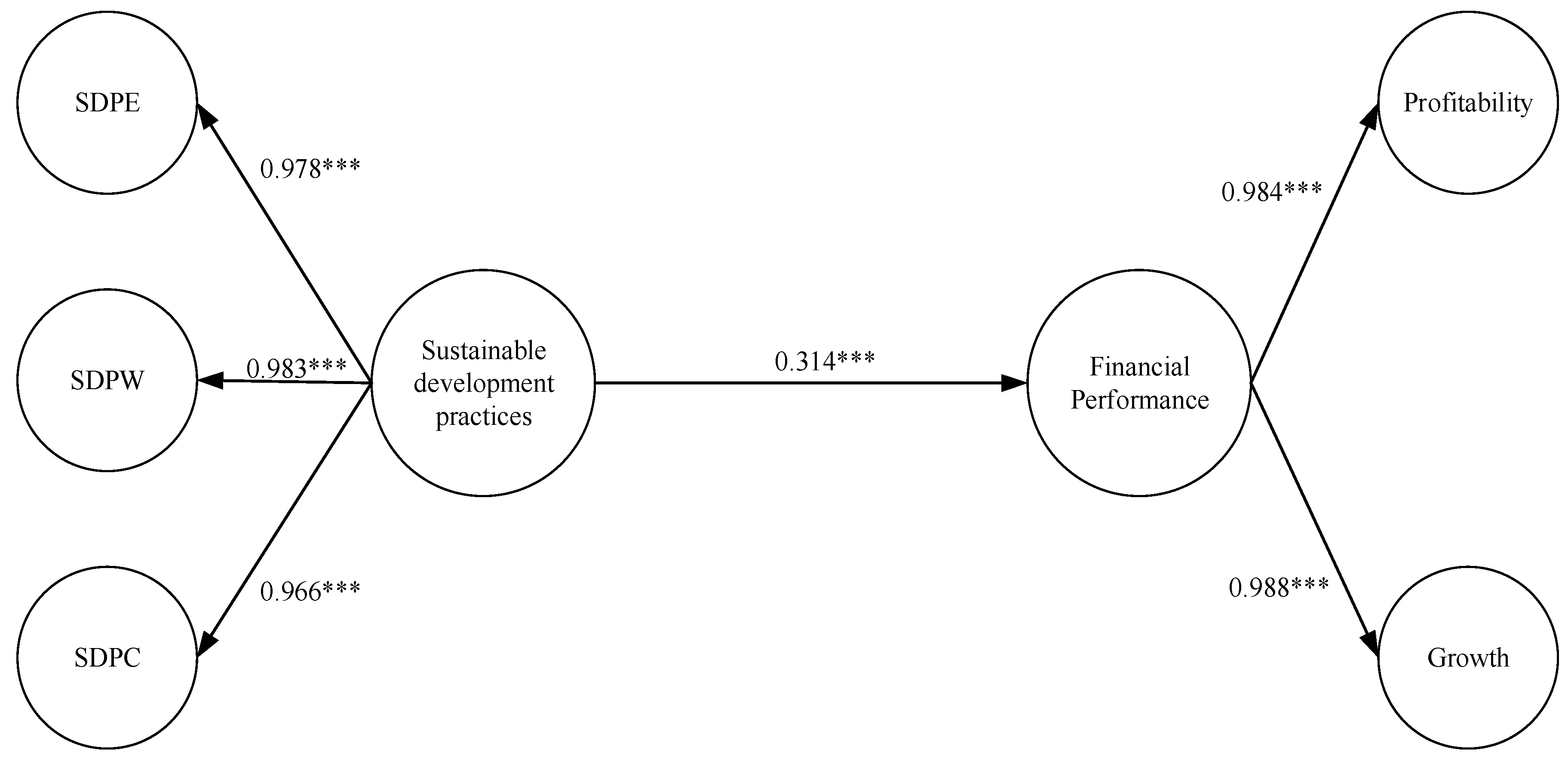

2.4. The Direct Relationship between SDPs and Financial Performance

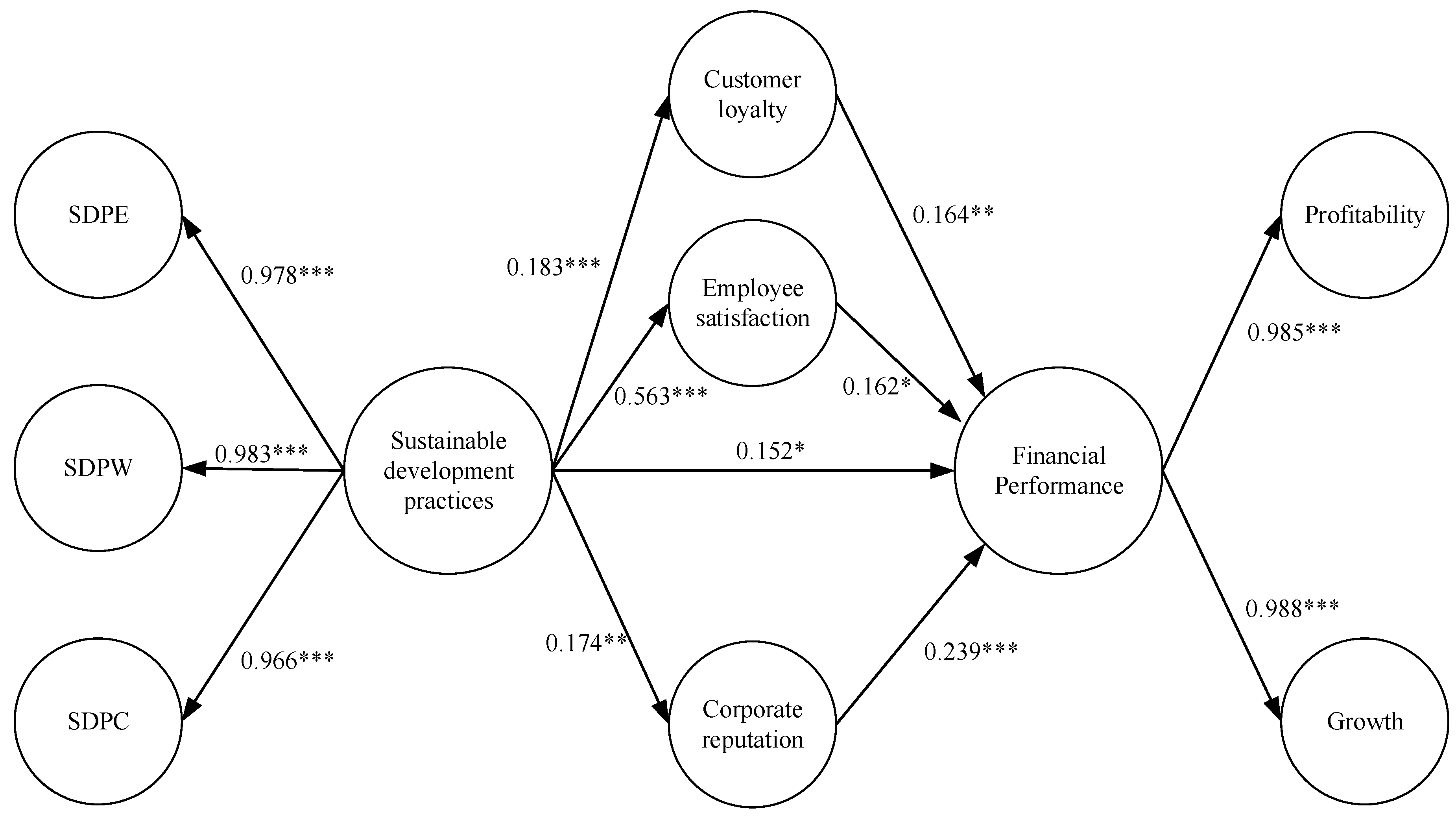

2.5. The Mediating Roles of Employee Satisfaction, Customer Loyalty, and Corporate Reputation

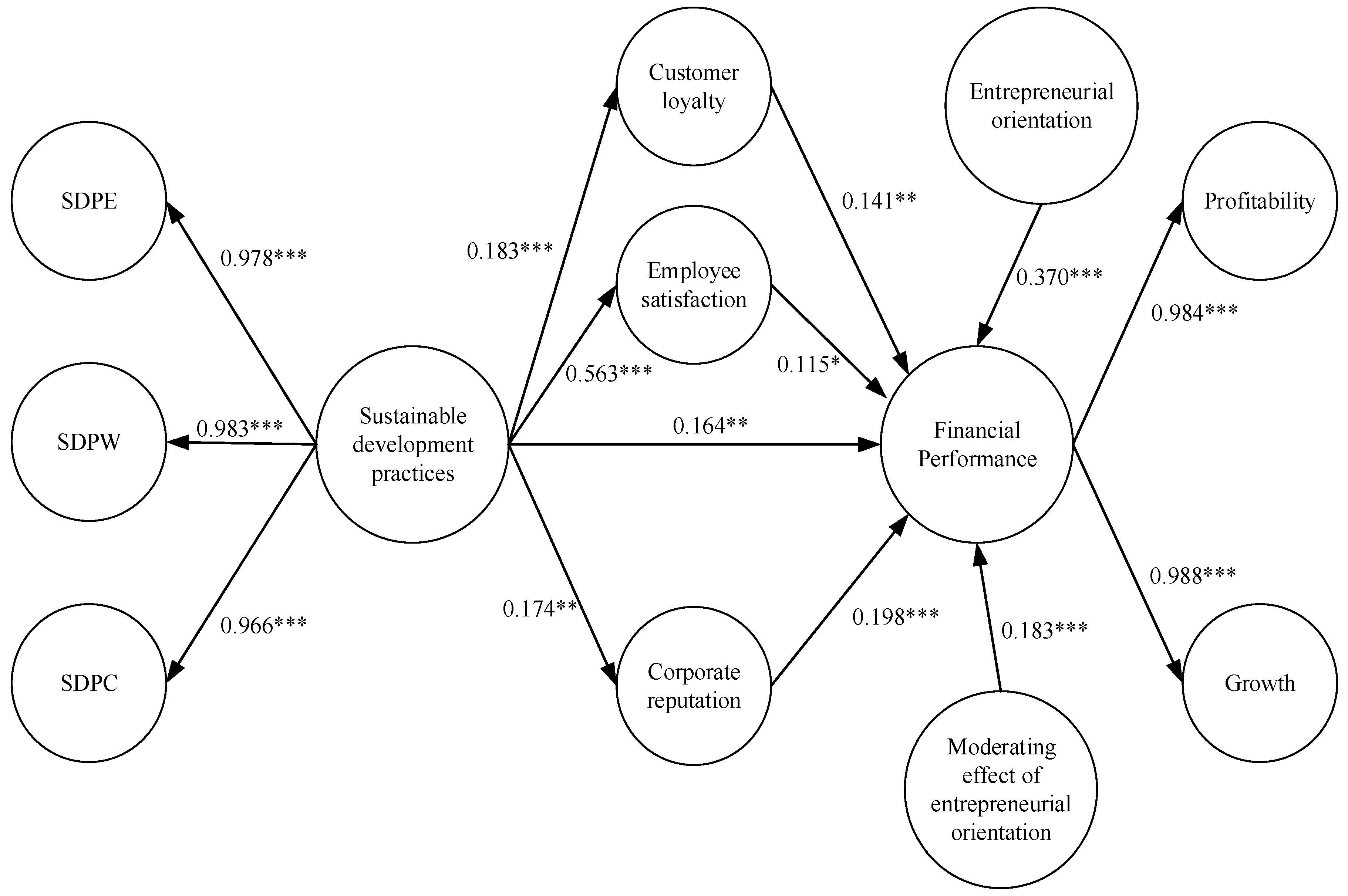

2.6. The Moderating Role of Entrepreneurial Orientation (EO)

3. Research Methodology

3.1. Research Sampling

3.2. Research Measures

3.3. Analysis Approach

4. Data Analysis

4.1. Measurement Model

4.2. Structural Models

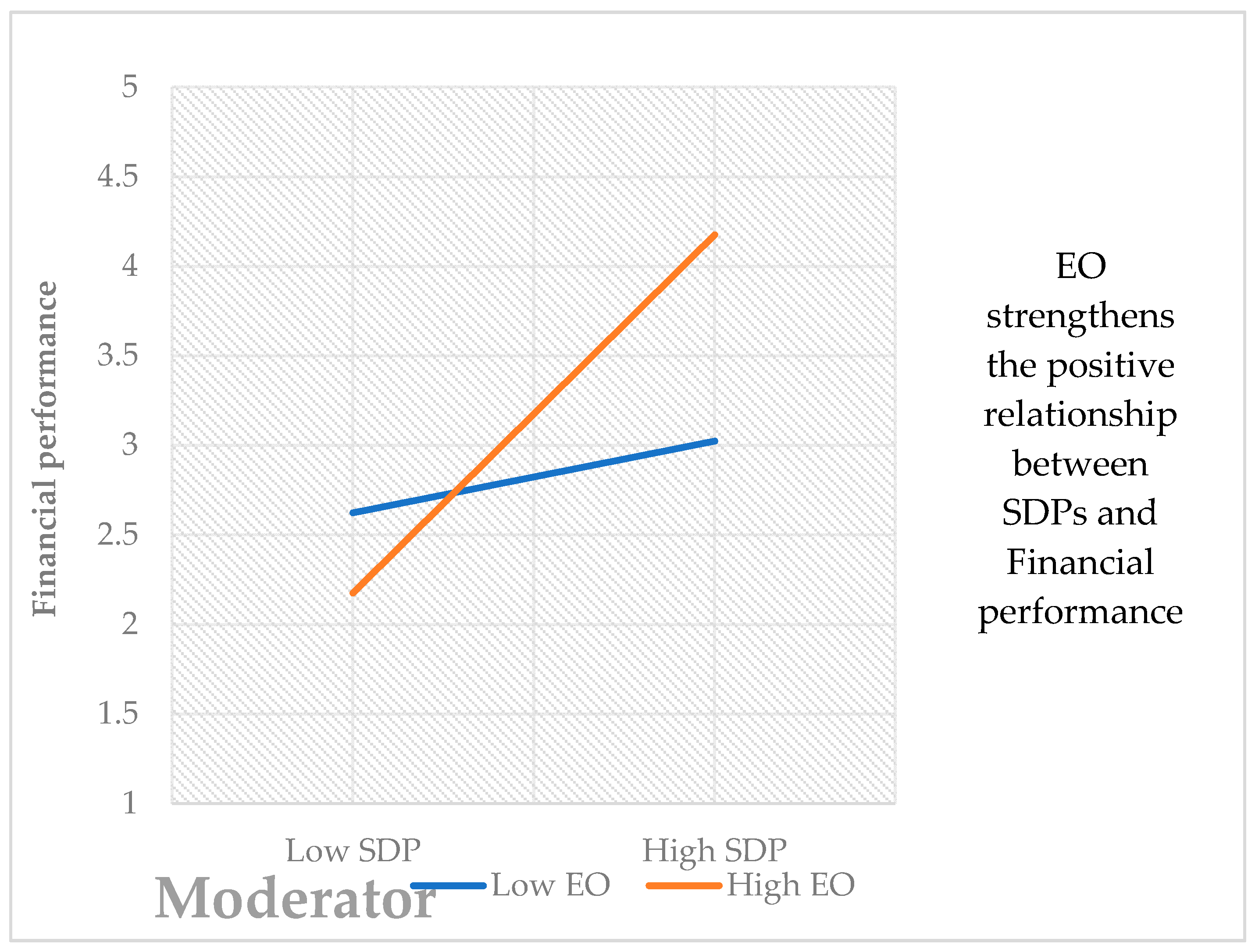

4.3. Testing for Moderating Effect of Entrepreneurial Orientation

5. Discussion and Implications

5.1. Theoretical Implications

5.2. Managerial Implications

6. Conclusions and Future Research

Author Contributions

Funding

Conflicts of Interest

Appendix A. Measurement of Variables in the Model

- SDPE1. Well-defined environment responsibilities

- SDPE2. Systems for measuring and assessing environmental performance

- SDPE3. Policies for substitution of polluting and materials and conservation of virgin materials

- SDPE4. Designs facilitating reduction of resource consumption and waste generation during production, distribution and product usage

- SDPE5. Preference for green products in purchasing

- SDPE6. Natural environment training for employees

- SDPE7. Regular voluntary information about environmental management to stakeholders

- SDPE8. Policies for preventing direct and indirect pollution of soil, water, and air

- SDPE9. Mechanism for supporting research and development of environmental technologies

- SDPW1. An equal opportunity action plan

- SDPW2. Anti-discrimination policies towards issues of gender, pregnancy, marital status

- SDPW3. Policies towards sexual harassment prohibition

- SDPW4. Policies for the training and development of employees

- SDPW5. The right to freedom of association, collective bargaining and complaint procedure

- SDPW6. Policies covering health and safety at work

- SDPW7. Provision for formal worker representation in decision making

- SDPW8. Compensation of workers as per legally mandated minimum wages

- SDPC1. Policy for contribution of skills and time of employees for community services

- SDPC2. Supports for third-party social and sustainable development-related initiatives

- SDPC3. Supports public policies and practices to promote human development and democracy

- SDPC4. Pursues partnerships with community organizations, government agencies and other industry groups dedicated to social causes

- SDPC5. Prohibits child labor, and violation of human rights

- SDPC6. Makes timely payment of taxes

- CL1. SDPs effectively affect the ability to repeat the purchase or order b

- CL2. The percentage of revenue from regular customers: c

![Sustainability 12 05930 i001]()

- CL3. The percentage of regular customers: c

![Sustainability 12 05930 i001]()

- ES1. The percentage of employee turnover of the firm: c

![Sustainability 12 05930 i001]()

- ES2. The percentage of staff employment via the recommendation of other employees: c

![Sustainability 12 05930 i001]()

- ES3. SDPs effectively affect employee attraction, motivation and commitment b

- ES4. SDPs create trust and commitment to long-term work of employees b

- CR1. Our firm is viewed by customers as one that is successful.

- CR2. We are seen by customers as being a very professional organization.

- CR3. Customers view our firm as one that is stable.

- CR4. Our firm’s reputation with customers is highly regarded.

- CR5. Our firm is viewed as well-established by customers

- EO1. has implemented important modifications in its products and services in the last 5 years

- EO2. has introduced several new lines of products and services in the last 5 years

- EO3. is often the first to introduce innovations (e.g., new products and services, new techniques and technologies, production methods)

- EO4. is generally the one to make the moves to which our competition replies

- EO5. favors high-risk projects that are supposed to bring in a lot of profit

- FP_P1. Return on assets (ROA)

- FP_P2. Return on Equity (ROE)

- FP_P3. Return on investment (ROI)

- FP_P4. Return on sales (ROS)

- FP_P5. Economic value added (EVA)

- FP_G1. Growth of assets

- FP_G2. Growth of net revenue

- FP_G3. Growth of profit after tax

- FP_G4. Growth of market share

- FP_G5. Growth of staff

- a item measured using 5-point scale, ranging from 1 for ‘it is not in the firm code’ to 5 for ‘it is in the firm code and fully implemented’;

- b item measured using 5-point scale, ranging from 1 for ‘strongly disagree’ to 5 for ‘strongly agree’;

- c responses were recoded into 5 groups of percentages;

- d item measured using 5-point scale, ranging from 1 for ‘below average much more’ to 5 for ‘above average much more’.

References

- Chabowski, B.; Mena, J.; Gonzalez-Padron, T. The structure of sustainability research in marketing, 1958–2008: A basis for future research opportunities. J. Acad. Mark. Sci. 2011, 39, 55–70. [Google Scholar] [CrossRef]

- Cruz, L.B.; Pedrozo, E.A.; Estivalete, V.F.B. Towards sustainable development strategies: A complex view following the contribution of edgar morin. Manag. Decis. 2006, 44, 871–891. [Google Scholar] [CrossRef]

- Labuschagne, C.; Brent, A.C.; van Erck, P.C.R. Assessing the sustainability performances of industries. J. Clean. Prod. 2005, 13, 373–385. [Google Scholar] [CrossRef] [Green Version]

- Sarkis, J.; Cordeiro, J.J. An empirical evaluation of environmental efficiencies and firm performance: Pollution prevention versus end-of-pipe practice. Eur. J. Oper. Res. 2001, 135, 102–113. [Google Scholar] [CrossRef]

- Brundtland Commission. Our Common Future; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- Elkington, J. Cannibals with forks. In The Triple Bottom Line of 21st Century Business; Capstone Publishing: Oxford, UK, 1997. [Google Scholar]

- Goldsmith, S.; Samson, D. Sustainable Development and Business Success: Reaching Beyond the Rhetoric to Superior Performance; Foundation for Sustainable Economic Development University of Melbourne: Melbourne, Australia, 2005. [Google Scholar]

- Grimaldi, F.; Caragnano, A.; Zito, M.; Mariani, M. Sustainability engagement and earnings management: The italian context. Sustainability 2020, 12, 4881. [Google Scholar] [CrossRef]

- Alshehhi, A.; Nobanee, H.; Khare, N. The impact of sustainability practices on corporate financial performance: Literature trends and future research potential. Sustainability 2018, 10, 494. [Google Scholar] [CrossRef] [Green Version]

- Hart, S.L.; Ahuja, G. Does it pay to be green? An empirical examination of the relationship between emission reduction and firm performance. Bus. Strategy Environ. 1996, 5, 30–37. [Google Scholar] [CrossRef]

- Surroca, J.; Tribo, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef]

- Aupperle, K.E.; Carroll, A.B.; Hatfield, J.D. An empirical examination of the relationship between corporate social responsibility and profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar]

- Friedman, M. The Social Responsibility of Business Is to Increase Its Profits; The New York Times Company: New York, NY, USA, 13 September 1970; pp. 122–126. [Google Scholar]

- Barnett, M.L.; Salomon, R.M. Does it pay to be really good? Addressing the shape of the relationship between social and financial performance. Strateg. Manag. J. 2012, 33, 1304–1320. [Google Scholar] [CrossRef]

- Lankoski, L. Corporate responsibility activities and economic performance: A theory of why and how they are connected. Bus. Strategy Environ. 2008, 17, 536–547. [Google Scholar] [CrossRef]

- Jayachandran, S.; Kalaignanam, K.; Eilert, M. Product and environmental social performance: Varying effect on firm performance. Strateg. Manag. J. 2013, 34, 1255–1264. [Google Scholar] [CrossRef]

- Grewatsch, S.; Kleindienst, I. When does it pay to be good? Moderators and mediators in the corporate sustainability-corporate financial performance relationship: A critical review. J. Bus. Ethics 2017, 145, 383–416. [Google Scholar] [CrossRef]

- Courrent, J.M.; Chasse, S.; Omri, W. Do entrepreneurial smes perform better because they are more responsible? J. Bus. Ethics 2018, 153, 317–336. [Google Scholar] [CrossRef]

- World Bank. Vietnam Data. Available online: https://data.worldbank.org/country/vietnam (accessed on 28 May 2020).

- CAFEF. Vinatex (vgt). Available online: http://cafef.vn/nam-2018-xuat-khau-det-may-viet-nam-thuoc-top-3-the-gioi-vinatex-vgt-thu-ve-1533-ty-loi-nhuan-20190107142007588.chn (accessed on 2 June 2020).

- SAC. Statement of Support for the Agreement on Sustainable Garment and Textile. Available online: https://apparelcoalition.org/public-policy-position-papers/ (accessed on 2 June 2020).

- Chan, R.Y.K. Does the natural-resource-based view of the firm apply in an emerging economy? A survey of foreign invested enterprises in china. J. Manag. Stud. 2005, 42, 625–672. [Google Scholar] [CrossRef]

- Brown, T.J.; Dacin, P.A. The company and the product: Corporate association and consumer product responses. J. Mark. 1997, 61, 68–84. [Google Scholar] [CrossRef] [Green Version]

- Chow, W.S.; Chen, Y. Corporate sustainable development: Testing a new scale based on the mainland chinese context. J. Bus. Ethics 2012, 105, 519–533. [Google Scholar] [CrossRef]

- Christmann, P. Effects of ‘best practices’ of environmental management on cost advantage: The role of complementary assets. Acad. Manag. J. 2000, 43, 663–680. [Google Scholar]

- Doering, D.; Cassara, A.; Layke, C.; Ranganathan, J.; Revenga, C.; Tunstall, D.; Vanasselt, W. Tomorrow’s Markets: Global Trends and Their Implications for Business; World Resources Institute: Baltimore, MD, USA, 2002. [Google Scholar]

- Baumann-Pauly, D.; Wickert, C.; Spence, L.J.; Scherer, A.G. Organizing corporate social responsibility in small and large firms: Size matters. J. Bus. Ethics 2013, 115, 693–705. [Google Scholar] [CrossRef] [Green Version]

- Ding, G.K.C. Sustainable construction: The role of environmental assessment tools. J. Environ. Manag. 2008, 86, 451–464. [Google Scholar] [CrossRef] [Green Version]

- Baumgartner, R.J.; Ebner, D. Corporate sustainability strategies: Sustainability profiles and maturity levels. Sustain. Dev. 2010, 18, 76–89. [Google Scholar] [CrossRef]

- Wiklund, J.; Shepherd, D. Entrepreneurial orientation and small business performance: A configurational approach. J. Bus. Ventur. 2005, 20, 71–91. [Google Scholar] [CrossRef]

- Blažková, I.; Dvouletý, O. Investigating the differences in entrepreneurial success through the firm-specific factors: Microeconomic evidence from the czech food industry. J. Entrep. Emerg. Econ. 2019, 11, 154–176. [Google Scholar] [CrossRef]

- Hult, G.T.M.; Ketchen, D.J.; Chabowski, R.B.; Hamman, M.K.; Dykes, B.J.; Pollitte, W.A.; Cavusgil, S.T. An assessment of the measurement of performance in international business research. J. Int. Bus. Stud. 2008, 39, 1064–1080. [Google Scholar] [CrossRef]

- Laroche, P. The Impact of Unions on Workplace Financial Performance: An Empirical Study in the French Context, Proceedings of the 56th Annual Meeting; Eaton, A., Ed.; IRRA: Champaign, IL, USA, 2004; pp. 154–172. [Google Scholar]

- Homburg, C.; Artz, M.; Wieseke, J. Marketing performance measurement systems: Does comprehensiveness really improve performance? J. Mark. 2012, 76, 56–77. [Google Scholar] [CrossRef]

- Harris, L.C. Market orientation and performance: Objective and subjective empirical evidence from UK companies. J. Manag. Stud. 2001, 38, 17–43. [Google Scholar] [CrossRef]

- Glick, W.H.; Washburn, N.T.; Miller, C.C. The Myth of Firm Performance, Proceedings of the Annual Meeting of American Academy of Management; American Academy of Management: Honolulu, HI, USA, 2005. [Google Scholar]

- Santos, J.; Brito, L. Toward a subjective measurement model for firm performance. Braz. Adm. Rev. 2012, 9, 95–117. [Google Scholar] [CrossRef] [Green Version]

- Whetten, D.A. Organizational growth and decline processes. Annu. Rev. Sociol. 1987, 13, 335–358. [Google Scholar] [CrossRef]

- López, M.V.; Garcia, A.; Rodriguez, L. Sustainable development and corporate performance: A study based on the dow jones sustainability index. J. Bus. Ethics 2007, 75, 285–300. [Google Scholar] [CrossRef]

- Wagner, M.; Blom, J. The reciprocal and non-linear relationship of sustainability and financial performance. Bus. Ethics A Eur. Rev. 2011, 20, 418–432. [Google Scholar] [CrossRef]

- Chernev, A.; Blair, S. Doing well by doing good: The benevolent halo of corporate social responsibility. J. Consum. Res. 2015, 41, 1412–1425. [Google Scholar] [CrossRef]

- Masud, M.A.K.; Nurunnabi, M.; Bae, S.M. The effects of corporate governance on environmental sustainability reporting: Empirical evidence from south asian countries. Asian J. Sustain. Soc. Responsib. 2018, 3, 3. [Google Scholar] [CrossRef]

- Beurden, P.; Gossling, T. The worth of values—A literature review on the relation between corporate social and financial performance. J. Bus. Ethics 2008, 82, 407–424. [Google Scholar] [CrossRef] [Green Version]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef] [Green Version]

- Borga, F.; Citterio, A.; Noci, G.; Pizzurno, E. Sustainability report in small enterprises: Case studies in italian furniture companies. Bus. Strategy Environ. 2009, 18, 162–176. [Google Scholar] [CrossRef]

- Reyes-Rodríguez, J.F.; Ulhøi, J.P.; Madsen, H. Corporate environmental sustainability in danish smes: A longitudinal study of motivators, initiatives, and strategic effects. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 193–212. [Google Scholar] [CrossRef]

- Spence, M.; Ben Boubaker Gherib, J.; Ondoua Biwolé, V. Sustainable entrepreneurship: Is entrepreneurial will enough? A north-south comparison. J. Bus. Ethics 2011, 99, 335–367. [Google Scholar] [CrossRef]

- Atkin, T.; Gilinsky, A.; Newton Sandra, K. Environmental strategy: Does it lead to competitive advantage in the us wine industry? Int. J. Wine Bus. Res. 2012, 24, 115–133. [Google Scholar] [CrossRef]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef] [Green Version]

- Torugsa, N.A.; O’Donohue, W.; Hecker, R. Proactive csr: An empirical analysis of the role of its economic, social and environmental dimensions on the association between capabilities and performance. J. Bus. Ethics 2013, 115, 383–402. [Google Scholar] [CrossRef] [Green Version]

- Davies, I.A.; Crane, A. Corporate social responsibility in small-and medium-size enterprises: Investigating employee engagement in fair trade companies. Bus. Ethics A Eur. Rev. 2010, 19, 126–139. [Google Scholar] [CrossRef]

- Ciliberti, F.; De Hahn, J.; De Groot, G.P.P. CSR codes and the principal-agent problem in supply chains: Four case studies. J. Clean. Prod. 2011, 19, 885–894. [Google Scholar] [CrossRef]

- Fuller, T.; Tian, Y. Social and symbolic capital and responsible entrepreneurship: An empirical investigation of sme narratives. J. Bus. Ethics 2006, 67, 287–304. [Google Scholar] [CrossRef]

- Tencati, A.; Perrini, F.; Pogutz, S. New tools to foster corporate socially responsible behavior. J. Bus. Ethics 2004, 53, 173–190. [Google Scholar] [CrossRef]

- Hammann, E.; Habisch, A.; Pechlaner, H. Values that create value: Socially responsible business practices in smes—Empirical evidence from german companies. Bus. Ethics A Eur. Rev. 2009, 18, 37–51. [Google Scholar] [CrossRef]

- Masud, M.A.K.; Harun, M.; Khan, T.; Bae, S.M.; Kim, J.D. Organizational strategy and corporate social responsibility: The mediating effect of triple bottom line. Int. J. Environ. Res. Public Health 2019, 16, 4559. [Google Scholar] [CrossRef] [Green Version]

- Saeidi, S.P.; Sofian, S.; Saeidi, P.; Saeidi, S.P.; Saaeidi, S.A. How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction. J. Bus. Res. 2015, 68, 341–350. [Google Scholar] [CrossRef]

- Fournier, S.; Yao, J.L. Reviving brand loyalty: A reconceptualization within the framework of consumer-brand relationships. Int. J. Res. Mark. 1997, 14, 451–472. [Google Scholar] [CrossRef]

- Hallowell, R. The relationships of customer satisfaction, customer loyalty, and profitability: An empirical study. Int. J. Serv. Ind. Manag. 1996, 7, 27–42. [Google Scholar] [CrossRef] [Green Version]

- Chi, C.G.; Gursoy, D. Employee satisfaction, customer satisfaction, and financial performance: An empirical examination. Int. J. Hosp. Manag. 2009, 28, 245–253. [Google Scholar] [CrossRef]

- Loveman, G.W. Employee satisfaction, customer loyalty, and financial performance: An empirical examination of the service profit chain in retail banking. J. Serv. Res. 1998, 1, 18–31. [Google Scholar] [CrossRef]

- Chang, C.C.; Chiu, C.M.; Chen, C.A. The effect of tqm practices on employee satisfaction and loyalty in government. Total. Qual. Manag. Bus. Excell. 2010, 21, 1299–1314. [Google Scholar] [CrossRef]

- Jenkins, H. A “business opportunity” model of corporate social responsibility for small-and medium-sized enterprises. Bus. Ethics A Eur. Rev. 2009, 18, 21–36. [Google Scholar] [CrossRef]

- Koys, D.J. How the achievement of human-resources goals drives restaurant performance. Cornell Hotel Restaur. Adm. Q. 2003, 44, 17–24. [Google Scholar] [CrossRef]

- Hasan, I.; Kobeissi, N.; Wang, H. Corporate social responsibility and firm financial performance: The mediating role of productivity. J. Bus. Ethics 2018, 149, 671–688. [Google Scholar] [CrossRef] [Green Version]

- Hess, R.L. The impact of firm reputation and failure severity on customers’ responses to service failures. J. Serv. Mark. 2008, 22, 385–398. [Google Scholar] [CrossRef]

- Murillo, D.; Lozano, J.M. Smes and csr: An approach to csr in their own words. J. Bus. Ethics 2006, 67, 227–240. [Google Scholar] [CrossRef]

- Kotha, S.; Rajgopal, S.; Rindova, V. Reputation building and performance: An empirical analysis of the top-50 pure internet firms. Eur. Manag. J. 2001, 19, 571–586. [Google Scholar] [CrossRef]

- Roberts, P.W.; Dowling, G.R. Corporate reputation and sustained superior financial performance. Strateg. Manag. J. 2002, 23, 1077–1093. [Google Scholar] [CrossRef]

- Lumpkin, G.T.; Dess, G.G. Clarifying the entrepreneurial orientation construct and linking it to performance. Acad. Manag. Rev. 1996, 21, 135–172. [Google Scholar] [CrossRef]

- Hull, C.E.; Rothenberg, S. Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strateg. Manag. J. 2008, 29, 781–789. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. Embedded versus peripheral corporate social responsibility: Psychological foundations. Ind. Organ. Psychol. 2013, 6, 314–332. [Google Scholar] [CrossRef]

- Kemp, R.; Parto, S.; Gibson, R.B. Governance for sustainable development: Moving from theory to practice. Int. J. Sustain. Dev. 2005, 8, 12–30. [Google Scholar] [CrossRef] [Green Version]

- Osburg, T. Social innovation to drive corporate sustainability. In Social Innovation: Solutions for a Sustainable Future; Osburg, T., Schmidpeter, R., Eds.; Springer: Berlin/Heidelberg, Germany, 2013; pp. 13–22. [Google Scholar]

- Do, B.; Nguyen, U.; Nguyen, N.; Johnson, L.W. Exploring the proactivity levels and drivers of environmental strategies adopted by vietnamese seafood export processing firms: A qualitative approach. Sustainability 2019, 11, 3964. [Google Scholar] [CrossRef] [Green Version]

- Saunders, M.; Lewis, P.; Thornhill, A. Research Methods for Business Students; Pearson: Harlow, England, 2012. [Google Scholar]

- Mishra, S.; Suar, D. Does corporate social responsibility influence firm performance of indian companies? J. Bus. Ethics 2010, 95, 571–601. [Google Scholar] [CrossRef]

- Leonidou, L.C.; Fotiadis, T.A.; Christodoulides, P.; Spyropoulou, S.; Katsikeas, C.S. Environmentally friendly export business strategy: Its determinants and effects on competitive advantage and performance. Int. Bus. Rev. 2015, 24, 798–811. [Google Scholar] [CrossRef]

- Leonidou, L.C.; Christodoulides, P.; Kyrgidou, L.P.; Palihawadana, D. Internal drivers and performance consequences of small firm green business strategy: The moderating role of external forces. J. Bus. Ethics 2017, 140, 585–606. [Google Scholar] [CrossRef] [Green Version]

- Sweeney, L. A Study of Current Practice of Corporate Social Responsibility (Csr) and an Examination of the Relationship between Csr and Financial Performance Using Structural Equation Modeling (Sem); Dublin Institute of Technology: Dublin, Ireland, 2009. [Google Scholar]

- Guthrie, J.P. High-involvement work practices, turnover, and productivity: Evidence from new zealand. Acad. Manag. J. 2001, 44, 180–190. [Google Scholar]

- Galbreath, J. How does corporate social responsibility benefit firms? Evidence from australia. Eur. Bus. Rev. 2010, 22, 411–431. [Google Scholar] [CrossRef]

- Mahon, J.F. Corporate reputation: Research agenda using strategy and stakeholder literature. Bus. Soc. 2002, 41, 415–445. [Google Scholar] [CrossRef]

- Hair, J.F.; Matthews, L.M.; Matthews, R.L.; Sarstedt, M. Pls-sem or cb-sem: Updated guidelines on which method to use. Int. J. Multivar. Data Anal. 2017, 1, 107–123. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (Pls-Sem); SAGE: Thousand Oaks, CA, USA, 2014. [Google Scholar]

- Chin, W.W.; Peterson, R.A.; Brown, S.P. Structural equation modeling in marketing: Some practical reminders. J. Mark. Theory Pract. 2008, 16, 287–298. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Prentice Hall: Upper Saddle River, NJ, USA, 2010. [Google Scholar]

- Wetzels, M.; Odekerken-Schröder, G.V.O.C. Using pls path modeling for assessing hierarchical construct models: Guidelines and empirical illustration. MIS Q. 2009, 33, 177–195. [Google Scholar] [CrossRef]

- Weber, O. Corporate sustainability and financial performance of chinese banks. Sustain. Account. Manag. Policy J. 2017, 8, 358–385. [Google Scholar] [CrossRef] [Green Version]

- ElAlfy, A.; Palaschuk, N.; El-Bassiouny, D.; Wilson, J.; Weber, O. Scoping the Evolution of Corporate Social Responsibility (CSR) Research in the Sustainable Development Goals (SDGs) Era. Sustainability 2020, 12, 5544. [Google Scholar] [CrossRef]

- The ASEAN Post. Making Vietnam’s Textile Industry Sustainable. Available online: https://theaseanpost.com/article/making-vietnams-textile-industry-sustainable (accessed on 2 June 2020).

- Perrini, F.; Russo, A.; Tencati, F.; Vurro, C. Deconstructing the relationship between corporate social and financial performance. J. Bus. Ethics 2011, 102, 59–76. [Google Scholar] [CrossRef]

- Dobre, E.; Stanila, G.O.; Brad, L. The influence of environmental and social performance on financial performance: Evidence from romania’s listed entities. Sustainability 2015, 7, 2513–2553. [Google Scholar] [CrossRef] [Green Version]

- Phan, T.T.H.; Nguyen, T.T.L. Nghiên cứu về nhận thức và thực trạng trách nhiệm xã hội doanh nghiệp trong các doanh nghiệp dệt may việt nam. J. Econ. Dev. 2018, 254, 106–112. [Google Scholar]

- Nguyen, Q.A.; Hens, L.; MacAlister, C.; Johnson, L.; Lebel, B.; Bach Tan, S.; Manh Nguyen, H.; Nguyen, T.N.; Lebel, L. Theory of reasoned action as a framework for communicating climate risk: A case study of schoolchildren in the mekong delta in vietnam. Sustainability 2018, 10, 2019. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, T.N.; Lobo, A.; Greenland, S. Pro-environmental purchase behaviour: The role of consumers’ biospheric values. J. Retail. Consum. Serv. 2016, 33, 98–108. [Google Scholar] [CrossRef]

- Nguyen, M.; Bensemann, J.; Kelly, S. Corporate social responsibility (CSR) in Vietnam: A conceptual framework. Int. J. Corp. Soc. Responsib. 2018, 3, 9. [Google Scholar] [CrossRef] [Green Version]

- Pham, T.H.; Nguyen, T.N.; Phan, T.T.H.; Nguyen, N.T. Evaluating the purchase behaviour of organic food by young consumers in an emerging market economy. J. Strateg. Mark. 2019, 27, 540–556. [Google Scholar] [CrossRef]

- Nguyen, T.T.H.; Yang, Z.; Nguyen, N.; Johnson, L.W.; Cao, T.K. Greenwash and green purchase intention: The mediating role of green skepticism. Sustainability 2019, 11, 2653. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, N.; Greenland, S.; Lobo, A.; Nguyen Hoang, V. Demographics of sustainable technology consumption in an emerging market: The significance of education to energy efficient appliance adoption. Soc. Responsib. J. 2019, 15, 803–818. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Number of Employees | n | % |

|---|---|---|

| <100 | 38 | 9.8 |

| 100–200 | 69 | 17.7 |

| 201–500 | 127 | 32.7 |

| 501–1000 | 83 | 21.3 |

| >1000 | 72 | 18.5 |

| Firm age | ||

| <5 | 58 | 14.9 |

| 5–10 | 101 | 25.9 |

| 11–15 | 152 | 39.1 |

| 16–20 | 47 | 12.1 |

| >20 | 31 | 8.0 |

| Firm type | ||

| Firms with 100% private ownership | 332 | 85.3 |

| Firms with government ownership | 57 | 14.7 |

| Headquarter location | ||

| Northern region | 180 | 46.3 |

| Central region | 91 | 23.4 |

| Southern region | 118 | 30.3 |

| Constructs | Items | Loadings | Mean | SD | α | CR | AVE |

|---|---|---|---|---|---|---|---|

| Environmental practices (SDPE) | SDPE1 | 0.792 *** | 3.94 | 0.653 | 0.798 | 0.841 | 0.655 |

| SDPE3 | 0.709 *** | 3.92 | 0.708 | ||||

| SDPE5 | 0.840 *** | 3.94 | 0.684 | ||||

| SDPE6 | 0.758 *** | 3.95 | 0.673 | ||||

| SDPE8 | 0.830 *** | 3.89 | 0.700 | ||||

| SDPE9 | 0.800 *** | 3.90 | 0.705 | ||||

| Social practice in the workplace (SDPW) | SDPW 1 | 0.851 *** | 3.98 | 0.660 | 0.812 | 0.849 | 0.572 |

| SDPW 2 | 0.781 *** | 3.84 | 0.704 | ||||

| SDPW 4 | 0.838 *** | 3.90 | 0.731 | ||||

| SDPW 5 | 0.915 *** | 3.95 | 0.673 | ||||

| SDPW 7 | 0.866 *** | 3.92 | 0.699 | ||||

| SDPW 8 | 0.900 *** | 3.92 | 0.668 | ||||

| Social practice in the community (SDPC) | SDPC 1 | 0.837 *** | 3.88 | 0.720 | 0.839 | 0.869 | 0.560 |

| SDPC 2 | 0.776 *** | 3.94 | 0.667 | ||||

| SDPC 4 | 0.801 *** | 3.92 | 0.728 | ||||

| SDPC 5 | 0.745 *** | 3.88 | 0.718 | ||||

| SDPC 6 | 0.836 *** | 3.90 | 0.749 | ||||

| Customer loyalty (CL) | CL1 | 0.834 *** | 2.53 | 0.993 | 0.838 | 0.838 | 0.634 |

| CL2 | 0.786 *** | 2.76 | 1.034 | ||||

| CL3 | 0.855 *** | 2.78 | 1.026 | ||||

| Employee satisfaction (ES) | ES1 | 0.739 *** | 3.82 | 0.803 | 0.932 | 0.932 | 0.775 |

| ES2 | 0.805 *** | 3.83 | 0.803 | ||||

| ES3 | 0.794 *** | 3.73 | 0.790 | ||||

| ES4 | 0.822 *** | 3.94 | 0.653 | ||||

| Corporate reputation (CR) | CR 1 | 0.856 *** | 3.92 | 0.708 | 0.880 | 0.890 | 0.697 |

| CR 2 | 0.821 *** | 3.94 | 0.684 | ||||

| CR 3 | 0.847 *** | 3.95 | 0.673 | ||||

| CR 4 | 0.819 *** | 3.89 | 0.700 | ||||

| CR 5 | 0.809 *** | 3.90 | 0.705 | ||||

| Financial performance: Growth (FP_G) | FP_G1 | 0.807 *** | 3.98 | 0.660 | 0.917 | 0.917 | 0.689 |

| FP_G2 | 0.829 *** | 3.84 | 0.704 | ||||

| FP_G3 | 0.836 *** | 3.90 | 0.731 | ||||

| FP_G4 | 0.844 *** | 3.95 | 0.673 | ||||

| FP_G5 | 0.784 *** | 3.92 | 0.699 | ||||

| Financial performance: Profitability (FP_G) | FP_P1 | 0.861 *** | 3.92 | 0.668 | 0.871 | 0.872 | 0.579 |

| FP_P2 | 0.795 *** | 3.88 | 0.720 | ||||

| FP_P3 | 0.830 *** | 3.94 | 0.667 | ||||

| FP_P4 | 0.847 *** | 3.92 | 0.728 | ||||

| FP_P5 | 0.732 *** | 3.88 | 0.718 | ||||

| Entrepreneurial orientation (EO) | EO 1 | 0.786 *** | 3.90 | 0.749 | 0.892 | 0.891 | 0.890 |

| EO 2 | 0.801 *** | 2.53 | 0.993 | ||||

| EO 3 | 0.797 *** | 2.76 | 1.034 | ||||

| EO 4 | 0.789 *** | 2.78 | 1.026 | ||||

| EO 5 | 0.811 *** | 3.82 | 0.803 |

| Constructs | SDP | CL | ES | CR | FP | EO |

|---|---|---|---|---|---|---|

| 1. Sustainable development practice (SDP) | 0.771 | |||||

| 2. Customer loyalty (CL) | 0.231 | 0.796 | ||||

| 3. Employee satisfaction (ES) | 0.256 | 0.363 | 0.880 | |||

| 4. Corporate reputation (CR) | 0.381 | 0.328 | 0.169 | 0.35 | ||

| 5. Financial performance (FP) | 0.571 | 0.239 | 0.416 | 0.525 | 0.795 | |

| 6. Entrepreneurial orientation (EO) | 0.252 | 0.568 | 0.319 | 0.396 | 0.598 | 0.41 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Phan, T.T.H.; Tran, H.X.; Le, T.T.; Nguyen, N.; Pervan, S.; Tran, M.D. The Relationship between Sustainable Development Practices and Financial Performance: A Case Study of Textile Firms in Vietnam. Sustainability 2020, 12, 5930. https://0-doi-org.brum.beds.ac.uk/10.3390/su12155930

Phan TTH, Tran HX, Le TT, Nguyen N, Pervan S, Tran MD. The Relationship between Sustainable Development Practices and Financial Performance: A Case Study of Textile Firms in Vietnam. Sustainability. 2020; 12(15):5930. https://0-doi-org.brum.beds.ac.uk/10.3390/su12155930

Chicago/Turabian StylePhan, Thi Thu Hien, Hiep Xuan Tran, Trung Thanh Le, Ninh Nguyen, Simon Pervan, and Manh Dung Tran. 2020. "The Relationship between Sustainable Development Practices and Financial Performance: A Case Study of Textile Firms in Vietnam" Sustainability 12, no. 15: 5930. https://0-doi-org.brum.beds.ac.uk/10.3390/su12155930