Dynamic Development of the Global Organic Food Market and Opportunities for Ukraine

,

,

Abstract

:1. Introduction

2. Theoretical Basis of Formation and Structuring of the Global Organic Food Market

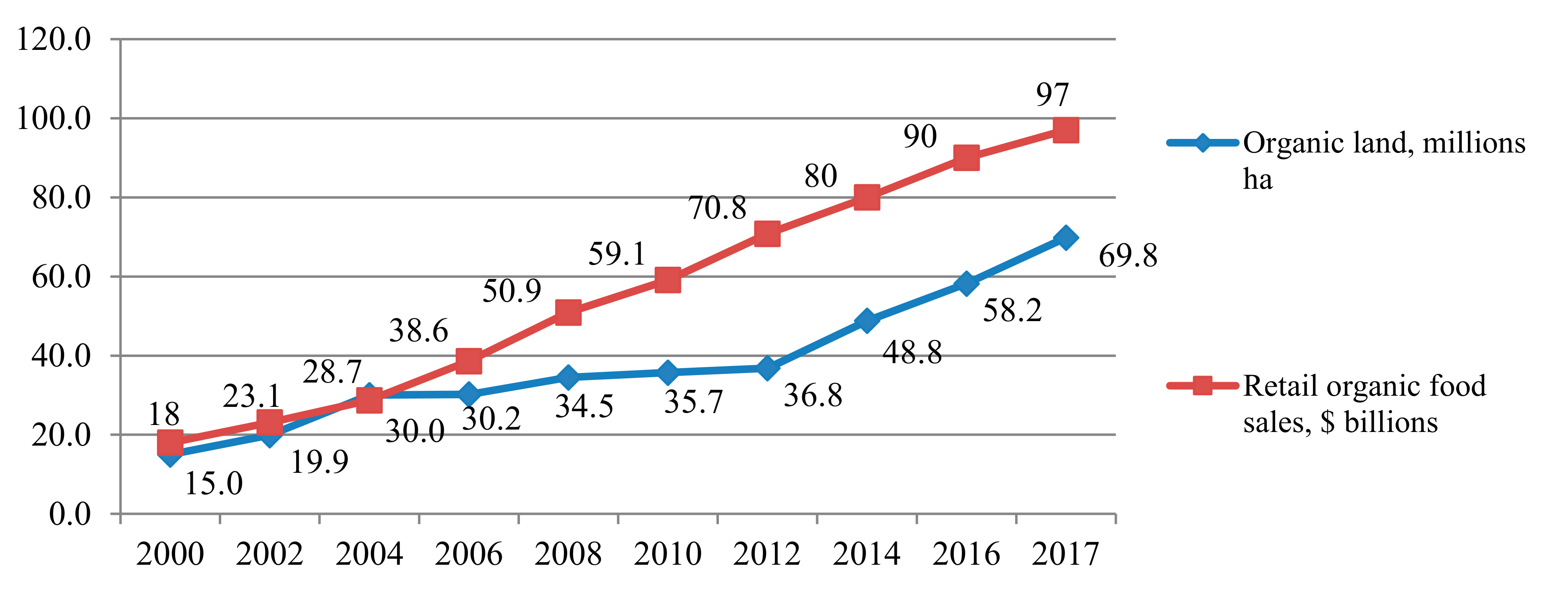

2.1. Formation of the Global Organic Food Market

2.2. Product Approach of the Global Organic Food Market

2.3. Ecoinnovation in the Organic Sector by Groups

3. Transformation of the Global Organic Food Market

3.1. Main Trends in the Development of Organic Food Markets in World Regions and Continents

3.2. Disproportions of the Global Organic Food Market

4. Overview of the Organic Sector in Ukraine

5. Data and Methods

6. Results and Discussion

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Osaulenko, O.; Yatsenko, O.; Reznikova, N.; Rusak, D.; Nitsenko, V. The productive capacity of countries through the prism of sustainable development goals: Challenges to international economic security and to competitiveness. Financ. Credit Act. Probl. Theory Pract. 2020, 2, 492–499. [Google Scholar] [CrossRef]

- The World of Organic Agriculture. Statistics and Emerging Trends 2019, FiBL & IFOAM. 2019. Available online: https://shop.fibl.org/chen/mwdownloads/download/link/id/1202/ (accessed on 10 June 2020).

- Tsyhankova, T.; Yatsenko, O.; Zavadska, Y. Global transformations of international organic agrofood markets. Manag. Theory Stud. Rural Bus. Infrastruct. Dev. 2014, 36, 425–434. [Google Scholar] [CrossRef] [Green Version]

- Antonets, S.S.; Antonets, A.S.; Pisarenko, V.M. Organic Farming: The Experience of PE Agroecology. Practical Advices; PBB PDAA: Poltava, Ukraine, 2010. [Google Scholar]

- Lupenko, Y.O. Formation of Supply and Demand in the Market for Organic Products. Organic Production and Food Security; Polessye: Zhytomyr, Ukraine, 2013. [Google Scholar]

- Podolynskyi, A. Introduction to Biodynamic Farming; Spiritual Cognition: Moscow, Russia, 1994. [Google Scholar]

- Rudnytska, O.V. Marketing Activities of Agricultural Enterprises in the Market of Organic Agri-Food Products. Ph.D. Thesis, National Agrarian University, Kiev, Ukraine, 2007. [Google Scholar]

- Dudar, O.T. Organization and Economic Bases of Formation of the Organic Agricultural Production. Ph.D. Thesis, Ternopil National Economic University, Ternopil, Ukraine, 2012. [Google Scholar]

- Padel, S. Conversion to Organic Farming: A Typical Example of the Diffusion of an Innovation? Sociol. Rural. 2001, 41, 40–61. [Google Scholar] [CrossRef]

- Fedorov, M.M.; Hodakivska, O.V.; Korchinska, S.G. The Development of Organic Production; NSC IAE: Kiev, Ukraine, 2011. [Google Scholar]

- Boyko, Y.O. The Development of the Organic Sector Agribusiness Enterprises in the Context of the Challenges of Globalization and European Integration. Ph.D. Thesis, The International University of Business and Law, Kherson, Ukraine, 2011. [Google Scholar]

- Kozlova, O.A. Theory and Methodology of Formation of Organic Market on the Basis of a Holistic Marketing. Ph.D. Thesis, Omsk State University F.M. Dostoevsky, Omsk, Russia, 2011. [Google Scholar]

- Yatsenko, O. Diversification of foreign economic activities of the agrarian sector of the economy in the global instability. Int. Sci. J. Prog. 2017, 1, 45–50. [Google Scholar]

- Yatsenko, O.; Ovcharenko, A. Global organic food market: Insights, challenges and opportunities. Ekon. Menadgment Savrem. Uslovima 2019, 2, 489–507. [Google Scholar]

- Yatsenko, O.M.; Zavadska, Y.S. Formation of demand for organic products in the agro-food market. Innov. Econ. 2010, 3, 204–208. [Google Scholar]

- Mazurova, A.Y. Geography of the World Market for Organic Food. Ph.D. Thesis, Lomonosov Moscow State University, Moscow, Russia, 2009. [Google Scholar]

- Zavadska, Y. Market of Organic Agrofood Products: Methodology of Formation and Development; Polessye: Zhytomyr, Ukraine, 2015. [Google Scholar]

- Bek, U. What Is Globalization? Mistakes of Globalism—Answers to Globalization; Grigoryev, A., Sedelkina, V., Eds.; Progress-Tradition: Moscow, Russia, 2001. [Google Scholar]

- Bilorus, O. Imperatives strategy of the development of Ukraine in the context of globalization. Econ. Ukr. 2001, 11, 17–21. [Google Scholar]

- Bilorus, O.G.; Lukyanenko, D.G. Globalization and Development Security; KNEU: Kiev, Ukraine, 2001. [Google Scholar]

- Vlasov, V.I. Globalization and global food problem. Econ. Aic. 2004, 1, 7–11. [Google Scholar]

- Maystro, S.V. State regulation of the agrarian market of Ukraine in conditions of globalization. Ph.D. Thesis, Classical Private University, Zaporizhzhia, Ukraine, 2009. [Google Scholar]

- Pakhomov, Y.; Lukyanenko, G.; Gubskii, B. The National Economy in the Global Competitive Environment; ICE: Kyiv, Ukraine, 1997. [Google Scholar]

- Sabluk, P.T.; Bilorus, O.G.; Vlasov, V.I. Globalization and Food; NSC IAE: Kiev, Ukraine, 2008. [Google Scholar]

- Sokolenko, S.I. Globalization of Production Systems: Network. Alliances. Partnership. Clusters: Ukrainian Context; Logos: Kiev, Ukraine, 2002. [Google Scholar]

- Sokolenko, S.I. Clusters in the Global Economy; Logos: Kiev, Ukraine, 2004. [Google Scholar]

- Held, D. Globalization/Anti-Globalization; Andruschenko, I., Ed.; KIC: Kiev, Ukraine, 2004. [Google Scholar]

- U.S. Department of Agriculture. National Agricultural Library. Standards and Certification. Available online: https://www.nal.usda.gov/afsic/standards-and-certification (accessed on 18 August 2019).

- Ursul, A.; Ursul, T. Environmental Education for Sustainable Development. Future Hum. Image 2018, 9, 115–125. [Google Scholar] [CrossRef]

- The Law of Ukraine. Basic Principles and Requirements for Organic Production, Circulation and Labeling of Organic Products. 6 June 2019. Available online: https://zakon.rada.gov.ua/laws/show/2496-19#Text (accessed on 8 July 2019).

- Pavlenko, I.; Kudryashova, E.; Belokopytova, L. Agro-food market of the region: Problems of formation and development. Fundam. Res. 2015, 8, 193–197. [Google Scholar]

- Churin, A. Agri-food market and its main elements of functioning. Econ. Prof. Bus. 2016, 3, 45–48. [Google Scholar]

- Kuepper, G.A. Brief Overview of the History and Philosophy of Organic Agriculture; Kerr Center for Sustainable Agriculture: Poteau, OK, USA, 2010. [Google Scholar]

- Behera, K.K.; Alam, A.; Vads, S.; Sharma, H.P.; Sharma, V. Organic farming history and technique. In Agroecology Strategies Climate Change; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2011; pp. 287–328. [Google Scholar]

- Ma, S.-M.; Joachim, S. Review of History and Recent Development of Organic Farming Worldwide. Agric. Sci. China 2006, 5, 169–178. [Google Scholar] [CrossRef]

- Svyrydenko, D.; Stovpets, O. Cultural and Economic Strategies of Modern China: In Search of the Cooperation Models across the Global World. Future Hum. Image 2020, 13, 102–112. [Google Scholar] [CrossRef]

- Ma, B. Value Shaping of Ecological Man: External Standard and Internal Idea. Future Hum. Image 2020, 13, 57–65. [Google Scholar] [CrossRef]

- Kucher, A.; Heldak, M.; Kucher, L.; Fedorchenko, O.; Yurchenko, Y. Consumer willingness to pay a price premium for ecological goods: A case study from Ukraine. Environ. Socio-Econ. Stud. 2019, 7, 38–49. [Google Scholar] [CrossRef] [Green Version]

- Wysmułek, J.; Hełdak, M.; Kucher, A. The Analysis of Green Areas’ Accessibility in Comparison with Statistical Data in Poland. Int. J. Environ. Res. Public Health 2020, 17, 4492. [Google Scholar] [CrossRef] [PubMed]

- Kotykova, O.; Babych, M. Economic Impact of Food Loss and Waste. Agris Line Pap. Econ. Inform. 2019, 11, 57–71. [Google Scholar] [CrossRef] [Green Version]

- Kotykova, O.; Babych, M. Limitations in availability of food in Ukraine as a result of loss and waste. Oeconomia Copernic. 2019, 10, 153–172. [Google Scholar] [CrossRef]

- OrganicBiz. It’s not Your Grandparents’ Farm. 2018. Available online: https://organicbiz.ca/advancements-being-made-to-support-modern-organic-farmers/ (accessed on 30 March 2020).

- AgriSecure. Ag Tech Not Only Makes Large-Scale Organics Possible, but More Profitable. 2019. Available online: https://www.agrisecure.com/ag-tech-not-only-makes-large-scale-organics-possible-but-more-profitable/ (accessed on 30 March 2020).

- Farm Berau. Technology, Innovation Drive Success in Organic Fields. 2017. Available online: https://www.fb.org/viewpoints/technology-innovation-drive-success-in-organic-fields (accessed on 30 March 2020).

- Bangkok Post. CAT Encourages Thai Farmers to Adopt Smart Farmer system. Available online: https://www.bangkokpost.com/business/1659632/cat-encourages-thai-farmers-to-adopt-smart-farmer-system (accessed on 30 March 2020).

- Agronomist and Arable Farmer. Organic Food Uses Blockchain Technology to Further Supply Chain Transparency this Organic September. Available online: http://www.aafarmer.co.uk/news/organic-food-uses-blockchain-technology-to-further-supply-chain-transparency-this-organic-september.html (accessed on 30 March 2020).

- Fortune. Walmart and 9 Food Giants Team Up on IBM Blockchain Plans. Available online: http://fortune.com/2017/08/22/walmart-blockchain-ibm-food-nestle-unilever-tyson-dole/ (accessed on 30 March 2020).

- Organic World. The World of Organic Agriculture 2019. Available online: https://www.organic-world.net/yearbook/yearbook-2019.html (accessed on 13 March 2019).

- U.S. Department of Agriculture. Organic. Available online: https://www.usda.gov/topics/organic (accessed on 18 August 2019).

- Statista. Worldwide Sales of Organic Food from 1999 to 2017 (in Billion U.S. Dollars). Available online: https://0-www-statista-com.brum.beds.ac.uk/statistics/273090/worldwide-sales-of-organic-foods-since-1999/ (accessed on 6 May 2020).

- Our Center has Signed a Cooperation Agreement with the Latin American Organization for the Certification of Organic Products IMOcert. Available online: http://www.ofcc.org.cn/index.php?optionid=675&auto_id=1308 (accessed on 4 June 2020).

- China and Denmark Signed a Memorandum of Understanding and Cooperation in the Field of Certification and Accreditation of Organic Products. Available online: http://www.cnca.gov.cn/xxgk/jgdt/201705/t20170504_54194.shtml (accessed on 4 June 2020).

- OTA. Millennials and Organic: A Winning Combination. Available online: https://ota.com/news/press-releases/19256 (accessed on 4 June 2020).

- Kyianytsia, L.L. The One Belt One Road Initiative as a New Silk Road: The (Potential) Place of Ukraine. Ukr. Policymaker 2019, 4, 21–26. [Google Scholar] [CrossRef]

- Biondo, A. Organic Food and the Double Adverse Selection: Ignorance and Social Welfare. Agroecol. Sustain. Food Syst. 2013, 38, 230–242. [Google Scholar] [CrossRef]

- Bartels, J.; Van den Berg, I. Fresh fruit and vegetables and the added value of antioxidants: Attitudes of non-light, and heavy organic food users. Br. Food J. 2011, 113, 1339–1352. [Google Scholar] [CrossRef]

- Żakowska Biemans, S. Polish consumer food choices and beliefs about organic food. Br. Food J. 2011, 113, 122–137. [Google Scholar] [CrossRef]

- Mesias Díaz, F.J.; Martinez-Carrasco Pleite, F.; Miguel Martinez Paz, J.; Gaspar García, P. Consumer knowledge, consumption, and willingness to pay for organic tomatoes. Br. Food J. 2012, 114, 318–334. [Google Scholar] [CrossRef]

- TechSci Research. Global Organic Food Market by Product 2012–2022. Available online: https://www.techsciresearch.com/report/global-organic-food-market-by-product-type-organic-meat-poultry-and-dairy-organic-fruits-and-vegetables-organic-processed-food-etc-by-region-europe-north-america-asia-pacific-etc-competition-forecast-and-opportunities/833.html (accessed on 23 October 2019).

- General Mills Home Page. Available online: https://www.generalmills.com/en (accessed on 5 February 2018).

- Whole Foods Market Home Page. Available online: https://www.wholefoodsmarket.com/ (accessed on 5 February 2018).

- WhiteWave Foods Home Page. Available online: https://www.whitewave.com/ (accessed on 5 February 2018).

- Hein Celestian Home Page. Available online: http://www.hain.com/company/ (accessed on 5 February 2018).

- United Natural Foods Home Page. Available online: https://www.unfi.com/products (accessed on 5 February 2018).

- ALDI Home Page. Available online: https://www.aldi.us/en/grocery-home/aldi-brands/simplynature/ (accessed on 5 February 2018).

- REWE Home Page. Available online: https://www.rewe-group.com/en/nachhaltigkeit/gruene-produkte/bio (accessed on 5 February 2018).

- Ecovia Intelligence. Plant-Based Foods Gaining Global Currency. Available online: http://www.ecoviaint.com/plant-based-foods-gaining-global-currency/ (accessed on 23 October 2019).

- Yatsenko, O.; Nitsenko, V.; Karasova, N.; William, H.M.; Parcell, J.L. Realization of the Potential of Ukraine—EU Free Trade Area in Agriculture. J. Int. Stud. 2017, 10, 258–277. [Google Scholar] [CrossRef] [PubMed]

- Ostapenko, R.; Herasymenko, Y.; Nitsenko, V.; Koliadenko, S.; Balezentis, T.; Streimikiene, D. Analysis of Production and Sales of Organic Products in Ukrainian Agricultural Enterprises. Sustainability 2020, 12, 3416. [Google Scholar] [CrossRef] [Green Version]

- Kucher, A. Estimation of Effectiveness of Usage of Liquid Organic Fertilizer in the Context of Rational Land Use: A Case Study of Ukraine. Prz. Wschod. 2017, 8, 95–105. [Google Scholar] [CrossRef] [Green Version]

- Paramparagat Krishi Vikas Yojana (PKVY). Manual for District-Level Functionaries. 2017. Available online: http://agricoop.nic.in/sites/default/files/model%20organic%20cluster%20demonstation%20and%20model%20organic%20f-arm%20guidlines%20dated%2003.04.2017.pdf (accessed on 20 November 2019).

- European Network for Rural Development (ENRD). Guide to EU Support for Organic Farming. Available online: https://enrd.ec.europa.eu/news-events/news/guide-eu-support-organic-farming_en (accessed on 12 June 2018).

- Organic Agriculture Centre of Canada. Organic Science Cluster. Available online: https://www.dal.ca/faculty/agriculture/oacc/en-home/organic-science-cluster/OSCIII.html (accessed on 15 June 2020).

- Organic without Boundaries. Organic Public Procurement Is a Win-Win Scenario for Farmers, Consumers & Public Goods. Available online: https://www.organicwithoutboundaries.bio/2018/09/05/public-procurement/#.XU6jMugzbIU (accessed on 15 September 2019).

- Organic Federation Ukraine. Organic in Ukraine. Available online: http://www.organic.com.ua/uk/homepage/2010-01-26-13-42-29/ (accessed on 11 August 2018).

- Ukrainian Agrarian Confederation. Ukraine Exports almost 100% of Its Organic Produce to Europe. 2019. Available online: http://agroconf.org/content/mayzhe-100-organiki-ukrayina-eksportuie-do-ievropi (accessed on 19 May 2020).

- Kucher, A.; Anisimova, O.; Heldak, M. Efficiency of land reclamation projects: New approach to assessment for sustainable soil management. J. Environ. Manag. Tour. 2019, 10, 1568–1582. [Google Scholar] [CrossRef]

- Raišienė, A.G.; Yatsenko, O.; Nitsenko, V.; Karasova, N.; Vojtovicova, A. Global dominants of Chinese trade policy development: Opportunities and threats for cooperation with Ukraine. J. Int. Stud. 2019, 12, 193–207. [Google Scholar] [CrossRef]

- Research Institute of Organic Agriculture (FiBL). Latest Additions to the Organic Eprints Archive. Available online: http://www.fibl.org/en/themes/publications.html (accessed on 4 June 2020).

- Galeks-Agro Home Page. Available online: http://www.galeks-agro.com/ (accessed on 13 May 2020).

- EthnoProduct Home Page. Available online: http://www.ethnoproduct.com/ (accessed on 13 May 2020).

- Agrofirma Pole Home Page. Available online: http://agropole.com.ua/ua/ (accessed on 13 May 2020).

- Diamant Home Page. Available online: http://diamantltd.com.ua (accessed on 13 May 2020).

- Ovcharenko, A. The export-oriented development model of the organic food market of Ukraine. Black Sea Econ. Stud. 2018, 26, 21–26. [Google Scholar]

- Ovcharenko, A. Marketing technologies to promote organic agricultural production on global food market. Uzhorod Natl. Univ. Her. Int. Econ. Relat. World Econ. 2018, 18, 115–120. [Google Scholar]

- Agroecology Home Page. Available online: http://www.agroecology.in.ua (accessed on 13 May 2020).

- State Statistics Service of Ukraine. Available online: http://kiev.ukrstat.gov.ua (accessed on 24 May 2020).

{kind=link}

{kind=link}

| Group | Example | Description |

|---|---|---|

| Organizational form | Creating cooperatives and clusters | Since major producers of organic food are small and medium enterprises (farms), uniting into cooperatives and creating clusters let them freely exchange innovations and experience, increase their export power and establish close contact among all participants in the organic market. |

| Production | Collecting and analyzing data | This is a vital component for efficient and profitable production; thus, using specifically designed software promotes collecting and analyzing a great scope of data whose assessment lets organic food producers make more weighed decisions about production. |

| Technologies for organic weed reduction | Since the organic method of production requires bigger labor costs, which lead to an increase in organic food prices, there is a necessity to constantly search for new methods of growing process improvement and organic food production. Organic food producers regularly implement technologies such as cultivators for inter-row soil cultivation, mechanical weed reduction, etc. | |

| Technologies for accurate sowing | These are used in order to optimize harvests on the basis of received data and conditions. | |

| Internet of things (IoT) | The technology provides farmers with the data necessary for designing efficient planting schedules, which will further lead to crop capacity increases; improvements in produce quality; and decreases in exploitation costs, growing time and the use of energy. | |

| Sustainable packaging | Zero-waste packaging | Packaging is an important part of organic goods, especially provided that goods demand is growing in the market. Since organic production is linked to ecological issues, packaging (plastic) makes consumers concerned. Therefore, many organic food producers are constantly searching for innovation in packaging. A zero-waste direction (that is, the complete renunciation of using plastic as a packaging material) is becoming increasingly popular among organic producers. Additionally, product descriptions and labeling are essential parts of packaging since they provide accurate and actual information to consumers (peculiarities of labeling usage are provided in regulatory documents that directly suggest rules of production, transportation, etc. of organic food and vary depending on the chosen standard system). |

| Blockchain | Using blockchain encourages the creation of a transparent system of goods itineraries that considerably increases consumers’ trust in products. Thus, the British Soil Association in cooperation with technology start-up Provenance developed a pilot technology that will enable consumers who possess Near-Field-Communication smartphones to receive the necessary information about organic food. In addition to food chain transparency assistance, the use of blockchain by food/industrial groups for facilitation of the direct sales process is a perspective; consumers can also save up to 30% on daily purchasing by buying directly from food producers. Food industry leaders, such as Walmart, Nestlé, Unilever and others in cooperation with IBM are actively implementing blockchain technology in order to support digital data protection and the promotion of food tracking (e.g., chicken, chocolate and bananas). | |

| Zero miles | The “zero miles” initiative and “100% produce” of local production have become widespread in Spain. The Casa Grande de Xanceda milk company, which produces organic yogurt, is a good example of their efficient implementation. The company has signed priority deals with local suppliers not only on produce delivery but also dealing with issues of farm maintenance and animals’ well-being. | |

| U-pick | Organic farms all over the world offer a service of organic food being collected by consumers. | |

| Marketing | Green marketing | Despite the fact that organic food production has positive effects on the environment, the system of food delivery from producers to consumers is still an issue. Thus, organic companies resort to using such tools of green marketing as creating local points of sale where local consumers buy foods, thus reducing CO2 emissions into the atmosphere when transporting food from point A to point B. American company Buddha Teas, which sells various organic tea blends, is a good example of implementing “green” marketing. The company uses materials that have minimal negative effects on the environment and either decompose naturally or can be recycled for packaging production. |

| Specifics | Region | |||||

|---|---|---|---|---|---|---|

| North America | Europe | Asia | Latin America | Oceania | Africa | |

| 1. Online trade development | + | + | + | - | - | - |

| 2. Promotion of organic food by large retailers using own brands | + | + | + | - | - | - |

| 3. Increase in alternative produce segment demand | + | + | - | - | + | - |

| 4. Organic movement development | + | + | + | + | - | + |

| 5. Vegetarian and vegan lifestyle popularization | + | + | + | - | + | - |

| 6. Extension of food niche | + | + | + | + | + | - |

| 7. State support of organic production development | + | + | + | + | + | - |

| 8. Availability of regulatory base for market regulating and product certification | + | + | + | - | + | + |

| 9. Implementation of organic production courses in educational institutions | + | + | - | - | - | - |

| 10. Production system transparency | + | + | - | - | - | - |

| 11. Local production development | + | + | + | + | + | - |

| Countries | Specifics |

|---|---|

| The USA | Tough competition in the market; developed institutional structure; generator of new tendencies in the global organic food market, which are promptly adopted by organic food consumers from other countries; 75% of organic food is exported to USMCA countries (Canada and Mexico); setting direct connections between large chain resellers and small and medium organic producers, creating collaborations that lead to exclusion of all resellers by creating own supply systems. |

| Germany | Favorable economic environment; imports of a large quantity of organic food from EU countries since demand considerably exceeds supply; developed European regional and national chain of supermarkets and organic shops, which have relatively big assortments of organic food. |

| France | Demand satisfaction of 70% due to own production, with the other 30% covered by imports from European countries; considerable price difference between organic and traditional goods, at 79%. |

| Italy | Fragmented and competitive market; about 5% of food exports of Italy are organic food; major trade partners of Italy are Germany, France, the Benelux countries, Scandinavian countries and the USA; active organic food consumers of Italy are educational establishments; Italian organic sector mainly produces plant-source products. |

| Spain | Organic sector of Spain is export-oriented, mainly towards Central European countries; 80% of Spanish products are imported by Germany, France and Great Britain; so-called “sustainable restaurants” are widespread in Spain; they prefer local organic food suppliers. |

| China | Export-oriented development direction of Chinese organic sector; countries that import organic food from China are the USA, European countries, Japan and others; over 80% of domestic market is controlled by hypermarkets and specialized shops; the growth of solvent population forms demand for ecologically safe food; the world e-commerce development driver. |

| India | Concentration of the largest number of organic producers; major countries importing organic food from India are the USA, Canada, Switzerland and Israel; annual growth of Indian organic food market is at 20%–30%; considerable development potential if domestic issues are solved: creating transparent certification process, strengthening national brands’ role in the international market and state support of national producers; has the first 100% organic city. |

| Latin American countries | Important regional organic food supplier; the biggest quantities of organic land are located in Argentina, Brazil and Uruguay; 80% to 90% of produce is exported to the EU, the USA (about 70% of organic food imported to the USA is from Latin America) and Japan; exports cover a wide range of food, including bananas and coffee beans from Central America, Paraguayan and Brazilian sugar as well as Argentinean meat. |

| African countries | The largest quantity of organic areas, favorable climate and a lot of water bodies; organic food is mainly exported. |

| Region | Index | 2016 | 2017 | 2016–2017, % | 2007–2017, % |

|---|---|---|---|---|---|

| Africa | The number of organic goods producers, millions | 1.11 | 1.14 | 3.3 | 182.4 |

| Consumption, $ | - | - | - | - | |

| Asia | The number of organic goods producers, millions | 0.74 | 0.82 | 9.9 | 70.6 |

| Consumption, $ | 1.92 | 2.34 | 21.87 | - | |

| Europe | The number of organic goods producers, millions | 0.46 | 0.45 | −1.4 | 73.7 |

| Consumption, $ | 46.11 | 56.84 | 23.27 | - | |

| Latin America | The number of organic goods producers, millions | 0.37 | 0.40 | 6.5 | 78.7 |

| Consumption, $ | 1.47 | 1.47 | - | - | |

| North America | The number of organic goods producers, millions | 0.027 | 0.026 | −2.3 | 236.1 |

| Consumption, $ | 132.21 | 134.59 | 1.78 | - | |

| Oceania | The number of organic goods producers, millions | 0.018 | 0.019 | 3.2 | 13.0 |

| Consumption, $ | 29.95 | 35.93 | 20.00 | ||

| The world | The number of organic goods producers, millions | 2.73 | 2.86 | 4.7 | 105.3 |

| Consumption, $ | 12.77 | 13.79 | 7.98 | - |

| Year/Indicator | Organic Land, % | Number of Producers | Domestic Market, Millions of $ |

|---|---|---|---|

| 2011 | 0.65 | 155 | 5.6 |

| 2012 | 0.66 | 164 | 8.2 |

| 2013 | 0.95 | 175 | 13.4 |

| 2014 | 1.0 | 182 | 16.1 |

| 2015 | 1.0 | 210 | 19.3 |

| 2016 | 1.0 | 360 | 23.4 |

| 2017 | 0.7 | 375 | 32.4 |

| Growth rate, % | - | 242 | 576 |

| Name of the Company | Organic Exports | Location and Organic Land | Organic Certificates and Certification Body |

|---|---|---|---|

| Haleks-Agro PE | Organic products: grains (oats, rye, barley, buckwheat, millet, corn, etc.). Exports: Switzerland, Germany, Hungary, the Netherlands, Italy, etc. | Zhytomyr region, 8 thousand ha | Certificate of the Institute of Market Ecology (IMO), Organic Standard |

| EthnoProduct TM | Organic products: milk, sour cream, yogurt, butter, honey, meat, vegetables, grains and legumes. Exports: Germany, Switzerland, Norway, the Netherlands and the Czech Republic. | Chernihiv region, 4 thousand ha | Organic Standard, BioSiusse |

| Agrofirma Pole LLC | Organic products: millet, organic cereals, legumes and oilseeds. Exports: the Netherlands, Germany, Austria, Italy, Belgium, Australia, Malaysia, Poland, the Czech Republic and France. | Cherkasy region, 9 thousand ha | Organic Standard, BioSuisse, QSCert |

| Diamant Ltd. LLC | Organic products: instant cereal flakes from all kinds of legumes. Exports: Romania, the Netherlands and the UAE (5%–10% of production). | Poltava region | Organic Standard |

| Agroecology PE | Organic products: winter and spring wheat, rye, barley, oats, buckwheat, corn and sunflowers. Exports: Switzerland (90%) and Germany. | Poltava region, 8 thousand ha | Organic Standard |

| Year | Volume of Consumer Organic Market, Hundreds of Euros (Y) | Number of Organic Enterprises (X1) | GDP (X2) | Average Salary, Euros (X3) | Population Fraction Aged 16–59, Hundreds of People (X4) |

|---|---|---|---|---|---|

| 2004 | 100 | 70 | 1504.08 | 89.34 | 29,514.60 |

| 2005 | 200 | 72 | 2011.59 | 126.15 | 29,656.30 |

| 2006 | 400 | 80 | 2533.22 | 164.57 | 29,812.10 |

| 2007 | 500 | 92 | 2771.31 | 195.54 | 29,799.80 |

| 2008 | 600 | 118 | 3524.39 | 234.68 | 29,738.50 |

| 2009 | 1200 | 121 | 2285.04 | 206.73 | 29,586.00 |

| 2010 | 2400 | 142 | 2567.34 | 213.30 | 29,328.60 |

| 2011 | 5100 | 155 | 3089.75 | 237.93 | 29,090.10 |

| 2012 | 7900 | 164 | 3333.32 | 295.20 | 28,842.20 |

| 2013 | 12,200 | 175 | 3415.94 | 308.49 | 28,622.90 |

| 2014 | 14,500 | 182 | 2663.73 | 221.09 | 28,372.50 |

| 2015 | 17,500 | 210 | 1837.50 | 173.65 | 26,613.30 |

| 2016 | 21,200 | 360 | 1892.58 | 183.35 | 26,317.40 |

| 2017 | 29,400 | 375 | 2366.80 | 236.81 | 25,982.00 |

| Indicator | Volume of Consumer Organic Market, Hundreds of Euros (Y) | Number of Organic Enterprises (X1) | GDP (X2) | Average Salary, Euros (X3) | Population Fraction Aged 16–59, Hundreds of People (X4) |

|---|---|---|---|---|---|

| Volume of consumer organic market, hundreds of euros (Y) | 1 | 0.9444 | −0.1459 | 0.2992 | −0.9644 |

| Number of organic enterprises (X1) | 0.9444 | 1 | −0.1207 | 0.31 | −0.9351 |

| GDP (X2) | −0.1459 | −0.1207 | 1 | 0.8387 | 0.3094 |

| Average salary, euros (X3) | 0.2992 | 0.31 | 0.8387 | 1 | −0.1386 |

| Population fraction aged 16–59, hundreds of people (X4) | −0.9644 | −0.9351 | 0.3094 | −0.1386 | 1 |

| Index | Scenario Type | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Pessimistic | Realistic | Optimistic | |||||||

| General description | Insignificant export increase, mainly of raw materials to European countries. | Export volume increase due to uniting into cooperatives and production of regional development. Creating Ukrainian organic brand in the existing markets. Use of aggressive popularizing marketing strategy. | Trade agreements will boost entering new markets. Appeal of online trade development in Asian countries must be used as a channel to enter Asian markets. Assortment development using production of goods with high added value; developing vegan and niche product ranges and creating ecopackaging. | ||||||

| Indicating changes | Renunciation of organic production by some producers; market seizure by foreign companies; absence of informing the population about organic production pros; decrease in domestic demand; absence of assortment diversification; preference of traditional products. | Export-oriented development of organic sector; increase in consumer market will take place at the expense of consumers with high income levels; introducing the variety of assortment mainly in specialized trade points, including shops specialized in imported goods, and a relatively insignificant assortment in supermarkets; weak/moderate marketing activity of organic companies; skeptical attitude of consumers to national organic trademark. | Extending organic assortment in trade points; holding marketing promotional campaigns and organic farm fairs; popularizing organic food value among the population; extension of food logistics routes; vertical producers’ integration; extension of state support tools for organic sector; entering foreign markets with ready products; developing online trade; establishing long-term partnering relations with importers; founding competent and professional marketing services; expanding organic land by 5%; receiving more than one organic certificate by organic producers. | ||||||

| Indicating index | Forecasted market volume | 2019 | $44.7 million | Forecasted market volume | 2019 | $47 million | Forecasted market volume | 2019 | $49.4 million |

| 2020 | $51.9 million | 2020 | $54.7 million | 2020 | $57.4 million | ||||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bazaluk, O.; Yatsenko, O.; Zakharchuk, O.; Ovcharenko, A.; Khrystenko, O.; Nitsenko, V. Dynamic Development of the Global Organic Food Market and Opportunities for Ukraine. Sustainability 2020, 12, 6963. https://0-doi-org.brum.beds.ac.uk/10.3390/su12176963

Bazaluk O, Yatsenko O, Zakharchuk O, Ovcharenko A, Khrystenko O, Nitsenko V. Dynamic Development of the Global Organic Food Market and Opportunities for Ukraine. Sustainability. 2020; 12(17):6963. https://0-doi-org.brum.beds.ac.uk/10.3390/su12176963

Chicago/Turabian StyleBazaluk, Oleg, Olha Yatsenko, Oleksandr Zakharchuk, Anna Ovcharenko, Olga Khrystenko, and Vitalii Nitsenko. 2020. "Dynamic Development of the Global Organic Food Market and Opportunities for Ukraine" Sustainability 12, no. 17: 6963. https://0-doi-org.brum.beds.ac.uk/10.3390/su12176963