We applied the MFCA model throughout the whole purification process of the DWTS in May and September 2018. The water purification processes described in

Table 1,

Table 2,

Table 3,

Table 4,

Table 5 and

Table 6 make use of material and energy flows at every stage of the process of water purification except for the sedimentation process of the conventional plant that is done by gravity. In the water purification process, lime, oxidized iron, manganese, “superflocs,” chlorine, and silicon-sand are the input materials used. Pipes then transport the purified water to municipalities for distribution to households and business entities. We used the Umberto Efficiency

+ software to execute the MFCA calculation to visibly expose areas of inefficiency in the DWTS to improve process efficiency. MFCA can calculate actual material losses and energy usage. The graphical flow chart created by the Umberto model made the water treatment process transparent, hence making the production system easier understood. This graphical representation is also known as the

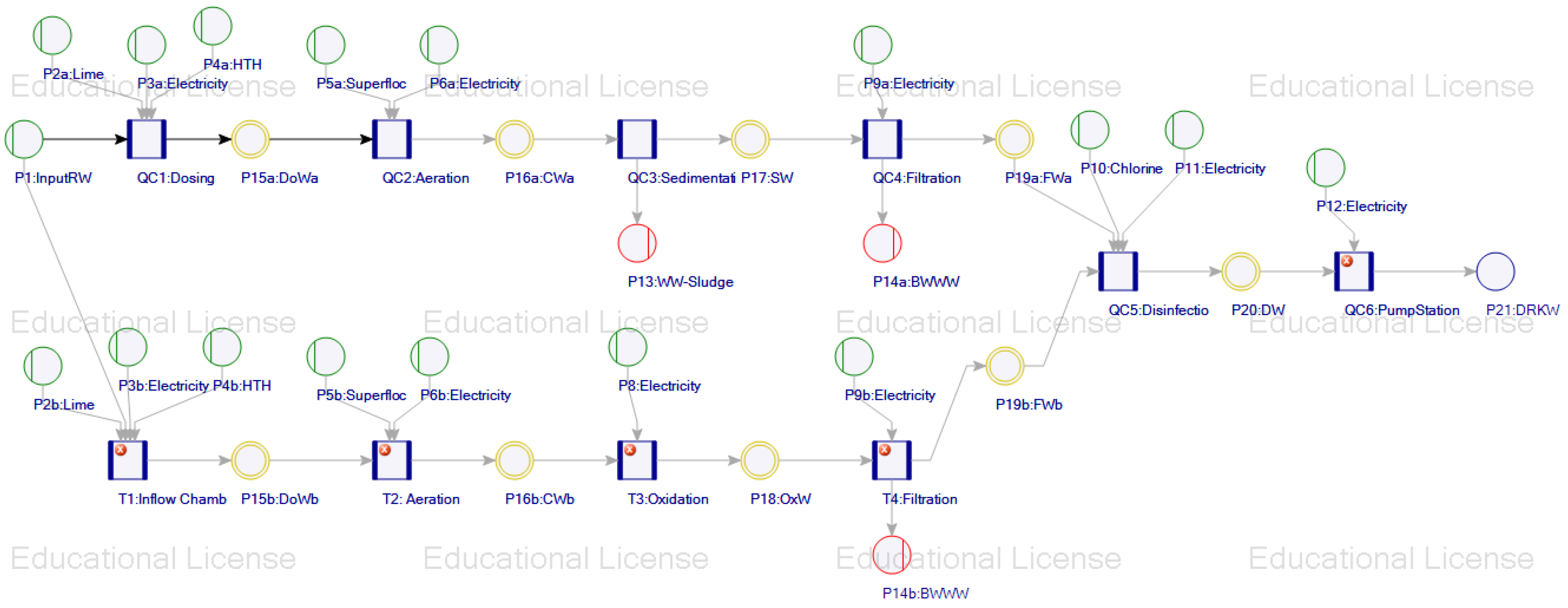

Sankey diagram that helps visualize the energy and material flows in the DWTS (see

Figure 1). It links process engineering knowledge with cost-saving during the water purification process to enable an efficient resource process and visualization. The

Sankey diagram visualizes all the hidden costs of the production cost. Also, it analyzes costs and water volume at every quantity center, to indicate phases that create material losses to be reduced or eliminated.

Cost Tables

The results of the analyses are presented in

Table 1,

Table 2,

Table 3,

Table 4,

Table 5,

Table 6,

Table 7,

Table 8,

Table 9 and

Table 10. The following coloration depicts the different phases of the water purification processes. The green color represents input material, and other resources (good) used at each phase. The orange color depicts the intermediate output, while the red color represents inefficiency or waste (negative). The light blue color represents the final salable output.

Table 1 (QC1) is the dosing process of the traditional plant. QC1 receives 6000 m

3 (this is the total daily capacity of the traditional plant) of raw water from the dam as input. At this point, lime and a chemical called calcium hypochlorite (HTH) are added as input. The lime and calcium hypochlorite are meant to disrupt micro-organism cells through oxidation. The energy input in QC1 is used by the machine to blend the chemical combinations with the raw water.

Table 1 also shows the quantity and the monetary value of the different input at quantity center 1. It includes 6000 m

3 of natural water at R1.33/m

3, 1.60 kg of HTH at R37.60/kg, 44.88 kW of electricity at R4.75 kW/h, and 150 kg of lime at R5.50/kg.

Furthermore,

Table 1 shows the total output from this process, which is represented as DoWa, which is then transferred to the next purification process known as aeration. The total volume of water purified at quantity center 1 is 6000 m

3 of water at R1.5182/m

3. It is noteworthy that there is no water loss at this process in water purification.

Table 2 shows the second stage of the water purification process in a conventional plant known as aeration. The output of QC1 becomes the input of QC2 because it is a process. At this quantity center, the inputs are 6000 m

3 of DoWa at R1.5182/m

3, 0.58 kW of electricity at R4.75/kW, and 71.25 kg of “superflocs” at R12.58/kg. The “superflocs,” which contain iron (Fe) and manganese (Mn), are added at this quantity center to separate impurities from the water and make finer particles form. The electrical energy used during this process is not high when compared to the electricity used in QC1 because of the capacity of the machine. The total output from this quantity center is 6000 m

3 of the “good” product at R1.6630/m

3, represented as CWa in

Table 3. This is transferred as an input to the next process known as sedimentation.

The third process of water purification at the conventional plant is the settling tank or sedimentation. This process receives “good” product of 6000 m

3 of water from QC2 at R1.6630/m

3 from the other process of water purification known as aeration. The sedimentation process is where heavier flocs can settle down for good quality water flowing through the weirs (channel) to the next purification process. During this process in the conventional plant, no added cost is incurred for chemicals or electricity; hence, the price per cubic meter (m

3) remains the same. The movement of processed water to the next purification process is done by gravity. It is important to note that water loss occurs at this quantity center during the water purification process. Water loss (“negative” product) of 2.5 m

3 was captured at this process; hence, the output represented as SW in

Table 3 is 5997.50 m

3 at R1.6630/m

3. The water loss in this process results from sludge formation, whereby the heavier flocs settle down, allowing “sedimented” water to flow to the subsequent process of the water purification. The “negative” product in this process was not included in the table because, in a costing process, all inefficiencies (the “negative” product) are included in the calculation of the “good” product so as not to lose the critical aspect of the water purification cost.

Table 4 shows the fourth process in the water purification process of a conventional plant, the filtration. Water input of R5997.50 m

3 at R1.6630/m

3 was received from QC3, and 58.30 kW/h of electricity at R4.75/kWh was used at this quantity center. In QC4, water purification happens through sand filtration using filter nozzles to remove impurities trapped and backwashed. The high energy consumption in QC4 results from high usage of machine capacity for backwashing. It is done for about one and a half hours. QC4 recorded water loss amounting to 104 m

3. The water loss is occasioned by backwashing to flush trapped impurities from the water. The amount of “good” water transferred to QC5 is 5893.50 m

3 at R1.7401/m

3.

Table 4, which is the filtration phase of the conventional plant, is merged with the packaged plant (the two plants converge at the disinfectant phase in

Table 9, where the outputs of these plants are combined into one phase (see the

Sankey diagram)). Table T1 (Inflow Chamber) is the first phase of the packaged plant (consists of Tables T1–T4), which later combines with the output of the conventional plant at QC5 for disinfection before being transferred to the pumping station (QC6) for distribution to the municipal bulk water tank (to be distributed to users). The conventional plant consists of Tables QC1–QC4.

Table 5 shows the first process of water purification in the packaged plant known as the inflow chamber for this study. This process is like that found at the conventional plant. Input for this quantity center was 6000 m

3 of raw water from the dam at R1.33/m

3, 50 kg of lime at R5.50/kg, the energy consumed was 25.22 kWh at R4.75/kWh, and calcium hypochlorite of 0.40 kg at R37.60/kg was added. The lime and calcium are reagents to disrupt micro-organism cellular processes by oxidation. Machines used energy consumption in T1 for dosing. The total output from T1 is 6000 m

3 at R1.4000/m

3, and this becomes an input for T2 in the water purification process for the packaged plant known as aeration.

Table 6 shows the second water purification process for a package plant known as aeration. The input for this quantity center is 6000 m

3 at R1.4000/m

3, 22.50 kg of “superflocs” at R12.58/kg, and 0.54 kW/h at R4.75/kWh of electricity. The “superflocs” are a chemical the removes impurities from the processed water at this stage of water purification in a package plant. T2 recorded no water loss. Hence, total production, represented by CWb in

Table 6 of 6000 m

3 at R1.45/m

3, was used as one of the inputs in the next purification process known as oxidation.

Table 7 shows the oxidation process of water purification in a package plant. This process is the second stage of aeration. The input at this process is 6000 m

3 of processed water at R1.4500/m

3 and electricity of 36 kWh at R4.75/kWh. The energy consumption in T3 resulted from the oxidation tank mixer used during water purification. No water loss was recorded in T3. Hence, the total output from this quantity center was 6000 m

3 at R1.4802/m

3, represented as OxW in

Table 7, and it was used as one of the inputs in the next water purification process known as filtration.

Table 8 shows the filtration process of the water purification for the

packaged plant at the DWTS. The input for this process is 6000 m

3 of processed water from the oxidation process at R1.4802/m

3 and 809.25 kWh at R4.75/kWh of electricity. T4 recorded a water loss of 253 m

3. The “good” product bears the cost of the “negative” product. Furthermore, water loss and high electricity consumption resulted from the backwashing done at this quantity center for a package plant. Therefore, the total output from this process is 5747 m

3 of water at R2.1210/m

3, represented as FW

B in

Table 8. This output became input at the next process called the disinfection process. In Table QC5, both the conventional and packaged plants outputs are combined at the disinfection phase (hence, we have the output of both the conventional plant (FW

A—5893.50 m

3) and the packaged plant (FW

B—5747 m

3) totaling drinkable water (DW) in P20: DW of 11,640.5 m

3.

Table 9 shows the disinfection process of water purification at the DWTS. This is the processing center where processed water from the filtration process of the conventional plant and the processed water of the “packaged” plant are combined for disinfection.

Table 9 shows the input from the two plants represented on the table as FWa for conventional plant and FWb for the packaged plant. The added input at this quantity center is chlorine of 28 kg at R28.55/kg and electricity of 52.80 kWh at R4.75 kWh. The addition of chlorine, known as chlorine gas at this quantity center, kills toxic micro-organisms in the water. The processed water is then allowed to settle in the contact reservoir to allow the chlorine to mix with the water and fit for human consumption properly. The energy used in QC5 resulted from the use of a machine to disinfect the water. It is imperative to note that no water loss was recorded in QC5. The total output for this quantity center was 11,640.50 m

3 of water at R2.1206/m

3, used as input at the last process of water purification known as the pump station.

Table 10 shows the last process of water purification at the DWTS, known as the pump station. The input of 11,640.50 m

3 of processed water from the disinfection process amount to R1.95/m

3 and consumes 12,384 kWh of electricity at R4.75/kWh, which resulted in the production of 11,640.50 m

3 of water at R7.00/m

3. The abnormal increase in the price per m

3 at this quantity center is because of the high capacity pumping machine used for this process of water purification. The processed water is pumped to the municipal reservoir for distribution to the public for consumption. Results from

Table 10 show the “true” cost of water purification at the DWTS as R7.00/m

3, which is higher than R6.75/m

3 presently charged by DWTS (it should be noted that the water tariff of R6.75/m

3 charged by the DTWS is the regulated tariff approved by the Department of Water and Sanitation, South Africa for bulk water sale to municipalities). Thus, we reiterate that one way of effectively managing water resources is to appropriately capture the volume of water loss and water-purification-related costs to improve its efficiency. The overhead costs of the DWTS are shown in

Table 11.

Table 11 displays the total overhead expenses on water produced at the DWTS. Production overhead cost is integrated into material and energy or system costs to make up the production cost. The inclusion of overhead costs enables the calculation of the “true” water purification cost. Besides, it is necessary to include related personnel costs in determining accurate production cost. Consequently, the ZAR8.6508/kl includes all expenses related to daily water treatment at the DWTS.

Nonetheless, the exemption of the daily ZAR1.6508/kl overhead cost calculation resulted in erroneous water purification costs and, subsequently, inaccurate water pricing. Such erroneous cost calculation and subsequent incorrect pricing limits managers’ ability to implement cost-saving opportunities. The failure of the current costing system to gather all associated water processing costs may have failed to rectify continuous water loss incurred daily. Besides, water pricing by the DWTS is subject to the Department of Water and Sanitation’s (DWS) fixed water tariff policy as the supervising government department. Thus, we argue that the DWS should allow water utilities to function as a profit center by allowing them to determine the price of their product. Similarly, because the DWTS relies on the DWS to pay its personnel salary, the DWS has allowed the DWTS and LNW’s management to overlook apparent production-related losses.

The MFCA system can provide support for the managerial decision about water pricing, as it can make visible and transparent stages or phases in the water purification process that are inefficient, for instance, in this study, the problem of the pumping device with a low capacitor. The management of the DWTS has failed to pick out the inefficient capacitor of the pumping machine for years, thus incurring daily losses. Besides this, we found from the MFCA analysis that energy cost resulting from the inefficient pumping device was not included in the input-output approach of determining water purification costs. Likewise, by revealing inefficient stages in the water purification process, the MFCA analysis enables the management of DWTS to fulfill its environmental and economic responsibility sustainably.

Regarding the pricing of the output water, the MFCA analysis shows that the DWTS’s water pricing decisions were underestimated by about 21.97% (). The reason for the underestimation is because water utilities do not depend on water production cost to determine its water pricing, but rely on the water tariff regulation by the Department of Water and Sanitation (DWS) influenced by the Water Act, which regards water provisioning the constitutional right of its citizens. Besides this, in terms of the total cost of ZAR8.6508/kl, it is worth noting the high proportion of the direct costs of ZAR7.00/kl. Nonetheless, of more significance is the impact which the one task of the pumping station has on the high cost of water purification is ZAR5.05/kl or 72% of the direct water purification cost. Hence, we suggest that any efficiency saving in this phase of the water purification process will have a significant effect on the overall cost. Thus, we reiterate that one way of effectively managing water resources is to appropriately capture the volume of water loss and water-purification-related costs to improve its efficiency.

The DWTS is operating at a loss of ZAR1.9008/kl. The current cost accounting system of DWTS is inadequate to capture water loss and the related cost information. A more specific waste capturing system is needed to expose the actual water loss and related costs to support the manager’s decision-making and create opportunities to minimize losses and cost-saving. Material loss is the excess of raw material that does not become saleable output. Reducing material loss means better resource efficiency and more cost-saving opportunities for any organization. Estimating and attributing costs to material losses is an essential aspect of purification, which would help in improving material usages, and in turn, reduce direct costs. The water utilities in South Africa are responsible for capturing water loss and its related costs in order to know the “true” value of water purification and so maximize profit. Using a suitable management accounting system can capture accurate water loss and its related costs information. In so doing, it enables water scheme managers to make informed water loss reduction decisions. Findings from the DTWS revealed the absence of an accounting system for capturing water loss during the water purification process. This study has proven that the implementation of MFCA and the extension of its implementation is achievable in state-controlled agencies South African water utilities. The implementation of the MFCA to capture water loss-related costs data is lacking in DWTS. Evidence from the study’s analysis shows that the MFCA could help managers make effective water loss reduction decisions when the full cost of water purification is known.

{kind=link}