ESG (Environmental, Social and Governance) Performance and Board Gender Diversity: The Moderating Role of CEO Duality

Abstract

:1. Introduction

2. Literature Review and Research Hypothesis Development

3. Methods

3.1. Sample Selection

3.2. Empirical Specification

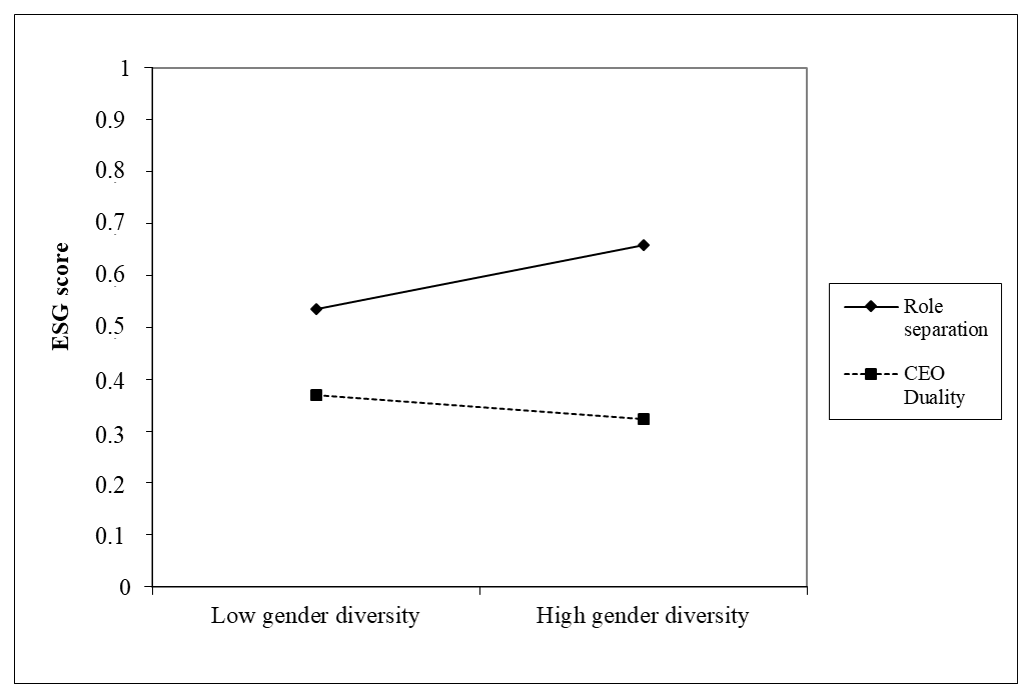

4. Results

Robustness Tests

5. Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Arena, C.; Cirillo, A.; Mussolino, D.; Pulcinelli, I.; Saggese, S.; Sarto, F. Women on board: Evidence from a masculine industry. Corp. Gov. Int. J. Bus. Soc. 2015, 15, 339–356. [Google Scholar] [CrossRef]

- Glass, C.; Cook, A.; Ingersoll, A.R. Do women leaders promote sustainability? Analyzing the effect of corporate governance composition on environmental performance. Bus. Strategy Environ. 2016, 25, 495–511. [Google Scholar] [CrossRef]

- Velte, P. Women on management board and ESG performance. J. Glob. Responsib. 2016, 7. [Google Scholar] [CrossRef]

- Vathunyoo Sila; Angelica Gonzalez, Jens Hagendorff, Women on board: Does boardroom gender diversity affect firm risk? J. Corp. Financ. 2016, 36, 26–53. [CrossRef] [Green Version]

- Manita, R.; Bruna, M.G.; Dang, R.; Houanti, L.H. Board gender diversity and ESG disclosure: Evidence from the USA. J. Appl. Account. Res. 2018, 19, 206–224. [Google Scholar] [CrossRef]

- Brown, L.D.; Caylor, M.L. Corporate Governance and Firm Performance. 2004. Available online: https://ssrn.com/abstract=586423 (accessed on 10 September 2020).

- Bauer, R.; Guenster, N.; Otten, R. Empirical evidence on corporate governance in Europe: The effect on stock returns, firm value and performance. J. Asset Manag. 2004, 5, 91–104. [Google Scholar] [CrossRef] [Green Version]

- Bhagat, S.; Bolton, B. Corporate governance and firm performance. J. Corp. Financ. 2008, 14, 257–273. [Google Scholar] [CrossRef]

- Arora, A.; Sharma, C. Corporate governance and firm performance in developing countries: Evidence from India. Corp. Gov. 2016, 16, 420–436. [Google Scholar] [CrossRef]

- Mio, C.; Venturelli, A.; Leopizzi, R. Management by objectives and corporate social responsibility disclosure. Account. Audit. Account. J. 2015, 28, 325–364. [Google Scholar] [CrossRef]

- Camilleri, M.A. Environmental, social and governance disclosures in Europe. Sustain. Account. Manag. Policy J. 2015, 6, 224–242. [Google Scholar] [CrossRef]

- Jizi, M.I.; Salama, A.; Dixon, R.; Stratling, R. Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. J. Bus. Ethics 2014, 125, 601–615. [Google Scholar] [CrossRef] [Green Version]

- Salama, A.; Anderson, K.; Toms, J.S. Does community and environmental responsibility affect firm risk? Evidence from UK panel data 1994–2006. Bus. Ethics: A Eur. Rev. 2011, 20, 192–204. [Google Scholar] [CrossRef]

- Taliento, M.; Favino, C.; Netti, A. Impact of environmental, social, and governance information on economic performance: Evidence of a corporate ‘sustainability advantage’ from Europe. Sustainability 2019, 11, 1738. [Google Scholar] [CrossRef] [Green Version]

- Jizi, M.; Nehme, R.; Salama, A. Do social responsibility disclosures show improvements on stock price? J. Dev. Areas 2016, 50, 77–95. [Google Scholar] [CrossRef] [Green Version]

- Sundarasen, S.D.D.; Je-Yen, T.; Rajangam, N. Board composition and corporate social responsibility in an emerging market. Corp. Gov. Int. J. Bus. Soc. 2016, 16, 35–53. [Google Scholar] [CrossRef]

- Husted, B.W.; de Sousa-Filho, J.M. Board structure and environmental, social, and governance disclosure in Latin America. J. Bus. Res. 2019, 102, 220–227. [Google Scholar] [CrossRef]

- Arya, B.; Zhang, G. Institutional reforms and investor reactions to CSR announcements: Evidence from an emerging economy. J. Manag. Stud. 2009, 46, 1089–1112. [Google Scholar] [CrossRef]

- Carter, D.A.; D’Souza, F.; Simkins, B.J.; Simpson, W.G. The gender and ethnic diversity of US boards and board committees and firm financial performance. Corp. Gov. Int. Rev. 2010, 18, 396–414. [Google Scholar] [CrossRef]

- O’Connell, V.; Cramer, N. The relationship between firm performance and board characteristics in Ireland. Eur. Manag. J. 2010, 28, 387–399. [Google Scholar] [CrossRef]

- Jermias, J.; Gani, L. The impact of board capital and board characteristics on firm performance. Br. Account. Rev. 2014, 46, 135–153. [Google Scholar] [CrossRef]

- Rao, K.; Tilt, C. Board composition and corporate social responsibility: The role of diversity, gender, strategy and decision making. J. Bus. Ethics 2016, 138, 327–347. [Google Scholar] [CrossRef]

- Joecks, J.; Pull, K.; Vetter, K. Gender diversity in the boardroom and firm performance: What exactly constitutes a “critical mass”? J. Bus. Ethics 2013, 118, 61–72. [Google Scholar] [CrossRef]

- Terjesen, S.; Sealy, R.; Singh, V. Women directors on corporate boards: A review and research agenda. Corp. Gov. Int. Rev. 2009, 17, 320–337. [Google Scholar] [CrossRef] [Green Version]

- Mahadeo, J.D.; Soobaroyen, T.; Hanuman, V.O. Board composition and financial performance: Uncovering the effects of diversity in an emerging economy. J. Bus. Ethics 2012, 105, 375–388. [Google Scholar] [CrossRef]

- Torchia, M.; Calabrò, A.; Huse, M.; Brogi, M. Critical Mass Theory and Women Directors’ Contribution to Board Strategic Tasks. Corp. Board Roleduties Compos. 2010, 6, 42–51. [Google Scholar] [CrossRef]

- Lückerath-Rovers, M. Women on boards and firm performance. J. Manag. Gov. 2013, 17, 491–509. [Google Scholar] [CrossRef] [Green Version]

- Campbell, K.; Mínguez-Vera, A. Gender diversity in the boardroom and firm financial performance. J. Bus. Ethics 2008, 83, 435–451. [Google Scholar] [CrossRef]

- Francoeur, C.; Labelle, R.; Sinclair-Desgagné, B. Gender diversity in corporate governance and top management. J. Bus. Ethics 2008, 81, 83–95. [Google Scholar] [CrossRef]

- Smith, N.; Smith, V.; Verner, M. Do women in top management affect firm performance? A panel study of 2,500 Danish firms. Int. J. Product. Perform. Manag. 2006, 55, 569–593. [Google Scholar] [CrossRef] [Green Version]

- Carter, D.A.; Simkins, B.J.; Simpson, W.G. Corporate governance, board diversity, and firm value. Financ. Rev. 2003, 38, 33–53. [Google Scholar] [CrossRef]

- Erhardt, N.L.; Werbel, J.D.; Schrader, C.B. Board of director diversity and firm financial performance. Corp. Gov. Int. Rev. 2003, 11, 102–111. [Google Scholar] [CrossRef] [Green Version]

- Giannarakis, G.; Konteos, G.; Sariannidis, N. Financial, governance and environmental determinants of corporate social responsible disclosure. Manag. Decis. 2014, 52, 1928–1951. [Google Scholar] [CrossRef]

- Bear, S.; Rahman, N.; Post, C. The impact of board diversity and gender composition on corporate social responsibility and firm reputation. J. Bus. Ethics 2010, 97, 207–221. [Google Scholar] [CrossRef]

- Ahern, K.R.; Dittmar, A.K. The changing of the boards: The impact on firm valuation of mandated female board representation. Q. J. Econ. 2012, 127, 137–197. [Google Scholar] [CrossRef]

- Bøhren, Ø.; Strøm, R. Governance and Politics: Regulating Independence and Diversity in the Board Room. J. Bus. Financ. Account. 2010, 37, 1281–1308. [Google Scholar] [CrossRef] [Green Version]

- Adams, R.B.; Ferreira, D. Women in the boardroom and their impact on governance and performance. J. Financ. Econ. 2009, 94, 291–309. [Google Scholar] [CrossRef] [Green Version]

- Shrader, C.B.; Blackburn, V.B.; Iles, P. Women in management and firm financial performance: An exploratory study. J. Manag. Issues 1997, 9, 355–372. [Google Scholar]

- Cucari, N.; Esposito De Falco, S.; Orlando, B. Diversity of board of directors and environmental social governance: Evidence from Italian listed companies. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 250–266. [Google Scholar] [CrossRef]

- Rose, C. Does female board representation influence firm performance? The Danish evidence. Corp. Gov. Int. Rev. 2007, 15, 404–413. [Google Scholar] [CrossRef]

- Randøy, T.; Thomsen, S.; Oxelheim, L. A Nordic perspective on corporate board diversity. Age 2006, 390, 1–26. [Google Scholar]

- Farrell, K.A.; Hersch, P.L. Additions to corporate boards: The effect of gender. J. Corp. Financ. 2005, 11, 85–106. [Google Scholar] [CrossRef] [Green Version]

- Adams, R.B.; Funk, P. Beyond the glass ceiling: Does gender matter? Manag. Sci. 2012, 58, 219–235. [Google Scholar] [CrossRef] [Green Version]

- De Cabo, R.M.; Gimeno, R.; Escot, L. Disentangling discrimination on Spanish boards of directors. Corp. Gov. Int. Rev. 2011, 19, 77–95. [Google Scholar] [CrossRef] [Green Version]

- Fama, E.F.; Jensen, M.C. Separation of ownership and control. J. Law Econ. 1983, 26, 301–325. [Google Scholar] [CrossRef]

- Ntim, C.G. Board diversity and organizational valuation: Unravelling the effects of ethnicity and gender. J. Manag. Gov. 2015, 19, 167–195. [Google Scholar] [CrossRef]

- Pfeffer, J. Size and Composition of Corporate Boards of Directors: The Organization and its Environment. Adm. Sci. Q. 1972, 17, 218–229. [Google Scholar] [CrossRef]

- Pfeffer, J.; Salancik, G.R. The External Control of Organisations: A Resource Dependence Perspective; Harper & Row: New York, NY, USA, 1978. [Google Scholar]

- Hillman, A.J.; Dalziel, T. Boards of directors and firm performance: Integrating agency and resource dependence perspectives. Acad. Manag. Rev. 2003, 28, 383–396. [Google Scholar] [CrossRef]

- Arnegger, M.; Hofmann, C.; Pull, K.; Vetter, K. Firm size and board diversity. J. Manag. Gov. 2014, 18, 1109–1135. [Google Scholar] [CrossRef]

- Shaukat, A.; Qiu, Y.; Trojanowski, G. Board attributes, corporate social responsibility strategy, and corporate environmental and social performance. J. Bus. Ethics 2016, 135, 569–585. [Google Scholar] [CrossRef] [Green Version]

- Wood, W.; Eagly, A.H. Gender Identity. In Handbook of Individual Differences in Social Behavior; Leary, M.R., Hoyle, R.H., Eds.; The Guilford Press: New York City, NY, USA, 2009; pp. 109–125. [Google Scholar]

- Adams, R.B.; Licht, A.N.; Sagiv, L. Shareholders and stakeholders: How do directors decide? Strateg. Manag. J. 2011, 32, 1331–1355. [Google Scholar] [CrossRef]

- Krüger, P. Corporate Social Responsibility and the Board of Directors. Job Market Paper. Toulouse Sch. Econ. Fr. 2009. [Google Scholar] [CrossRef]

- Singh, V.; Terjesen, S.; Vinnicombe, S. Newly appointed directors in the boardroom: How do women and men differ? Eur. Manag. J. 2008, 26, 48–58. [Google Scholar] [CrossRef] [Green Version]

- Zhang, J.Q.; Zhu, H.; Ding, H.B. Board composition and corporate social responsibility: An empirical investigation in the post Sarbanes-Oxley era. J. Bus. Ethics 2013, 114, 381–392. [Google Scholar] [CrossRef]

- Hillman, A.J.; Cannella, A.A., Jr.; Harris, I.C. Women and racial minorities in the boardroom: How do directors differ? J. Manag. 2002, 28, 747–763. [Google Scholar] [CrossRef]

- Hillman, A.J.; Shropshire, C.; Cannella Jr, A.A. Organizational predictors of women on corporate boards. Acad. Manag. J. 2007, 50, 941–952. [Google Scholar] [CrossRef] [Green Version]

- Nielsen, S.; Huse, M. The contribution of women on boards of directors: Going beyond the surface. Corp. Gov. Int. Rev. 2010, 18, 136–148. [Google Scholar] [CrossRef]

- Ciocirlan, C.; Pettersson, C. Does workforce diversity matter in the fight against climate change? An analysis of Fortune 500 companies. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 47–62. [Google Scholar] [CrossRef]

- Ben-Amar, W.; McIlkenny, P. Board effectiveness and the voluntary disclosure of climate change information. Bus. Strategy Environ. 2015, 24, 704–719. [Google Scholar] [CrossRef]

- Rodriguez-Dominguez, L.; Gallego-Alvarez, I.; Garcia-Sanchez, I.M. Corporate governance and codes of ethics. J. Bus. Ethics 2009, 90, 187. [Google Scholar] [CrossRef]

- Iyengar, R.J.; Zampelli, E.M. Self-selection, endogeneity, and the relationship between CEO duality and firm performance. Strateg. Manag. J. 2009, 30, 1092–1112. [Google Scholar] [CrossRef]

- Rechner, P.L.; Dalton, D.R. CEO duality and organizational performance: A longitudinal analysis. Strateg. Manag. J. 1991, 12, 155–160. [Google Scholar] [CrossRef]

- Naciti, V. Corporate governance and board of directors: The effect of a board composition on firm sustainability performance. J. Clean. Prod. 2019, 237, 117727. [Google Scholar] [CrossRef]

- Shahbaz, M.; Karaman, A.S.; Kilic, M.; Uyar, A. Board attributes, CSR engagement, and corporate performance: What is the nexus in the energy sector? Energy Policy 2020, 143, 111582. [Google Scholar] [CrossRef]

- Velte, P. Does CEO power moderate the link between ESG performance and financial performance? Manag. Res. Rev. 2019, 43, 497–520. [Google Scholar] [CrossRef]

- Javeed, S.A.; Lefen, L. An analysis of corporate social responsibility and firm performance with moderating effects of CEO power and ownership structure: A case study of the manufacturing sector of Pakistan. Sustainability 2019, 11, 248. [Google Scholar] [CrossRef] [Green Version]

- Li, Y.; Gong, M.; Zhang, X.Y.; Koh, L. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. Br. Account. Rev. 2018, 50, 60–75. [Google Scholar] [CrossRef] [Green Version]

- Walls, J.L.; Berrone, P. The power of one to make a difference: How informal and formal CEO power affect environmental sustainability. J. Bus. Ethics 2017, 145, 293–308. [Google Scholar] [CrossRef]

- Perrini, F.; Russo, A.; Tencati, A. CSR strategies of SMEs and large firms. Evidence from Italy. J. Bus. Ethics 2007, 74, 285–300. [Google Scholar] [CrossRef]

- Doni, F.; Martini, S.B.; Corvino, A.; Mazzoni, M. Voluntary versus mandatory non-financial disclosure. Meditari Account. Res. 2019, 28, 781–802. [Google Scholar] [CrossRef]

- Pizzi, S.; Venturelli, A.; Caputo, F. The “comply-or-explain” principle in directive 95/2014/EU. A rhetorical analysis of Italian PIEs. Sustain. Account. Manag. Policy J. 2020. [Google Scholar] [CrossRef]

- Hausman, J. Specification Tests in Econometrics. Econometrica 1978, 46, 1251–1271. [Google Scholar] [CrossRef] [Green Version]

- McBrayer, G.A. Does persistence explain ESG disclosure decisions? Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1074–1086. [Google Scholar] [CrossRef]

- Eccles, R.; Ioannou, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef] [Green Version]

- Blau, P.M. Inequality and Heterogeneity; The Free Press: New York, NY, USA, 1977. [Google Scholar]

- Aiken, L.S.; West, S.G.; Reno, R.R. Multiple Regression: Testing and Interpreting Interactions; SAGE: Thousand Oaks, CA, USA, 1991. [Google Scholar]

- CONSOB (The National Commission for Companies and the Stock Exchange). Report on Corporate Governance of Italian Listed Companies. 2019. Available online: http://www.consob.it/documents/46180/46181/rcg2019.pdf/941e4e4e-60db-4f89-afb3-32bddb8488e0 (accessed on 10 September 2020).

- Drempetic, S.; Klein, C.; Zwergel, B. The Influence of Firm Size on the ESG Score: Corporate Sustainability Ratings under Review. J. Bus. Ethics 2019, 167, 333–360. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L.L. Factors influencing social responsibility disclosure by Portuguese companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- O’Brien, R.M. A caution regarding rules of thumb for variance inflation factors. Qual. Quant. 2007, 41, 673–690. [Google Scholar] [CrossRef]

- Shannon, C.E. A mathematical theory of communication. Bell Syst. Tech. J. 1948, 27, 379–423. [Google Scholar] [CrossRef] [Green Version]

- Gordini, N.; Rancati, E. Gender diversity in the Italian boardroom and firm financial performance. Manag. Res. Rev. 2017, 40, 75–94. [Google Scholar] [CrossRef]

- Rushton, M. A note on the use and misuse of the racial diversity index. Policy Stud. J. 2008, 36, 445–459. [Google Scholar] [CrossRef]

- Kanter, R.M. Men and women of the corporation revisited. Manag. Rev. 1987, 76, 14. [Google Scholar]

- Torchia, M.; Calabrò, A.; Huse, M. Women directors on corporate boards: From tokenism to critical mass. J. Bus. Ethics 2011, 102, 299–317. [Google Scholar] [CrossRef]

- Post, C.; Rahman, N.; Rubow, E. Green Governance: Diversity in the Composition of Board of Directors and Environmental Corporate Social Responsibility (ECSR). Bus. Soc. 2011, 51. [Google Scholar] [CrossRef]

- Williamson, Ó. Transaction-Cost Economics: The Governance of Contractual Relations. J. Law Econ. 1979, 22, 233–261. [Google Scholar] [CrossRef]

- Hermalin, B.E.; Weisbach, M.S. Board of directors as an endogenously determined institution: A survey of the economic literature. Econ. Policy Rev. 2003, 9. [Google Scholar] [CrossRef]

- Johnson, S.G.; Schnatterly, K.; Hill, A.D. Board composition beyond independence: Social capital, human capital, and demographics. J. Manag. 2013, 39, 232–262. [Google Scholar] [CrossRef]

- Hambrick, D.C. Upper Echelons Theory: An Update. Acad. Manag. Rev. 2007, 32, 334–343. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Mean | S.D. | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) Blau_index | 0.446 | 0.149 | 1.000 | |||||||||

| (2) CEO_duality | 0.219 | 0.415 | −0.192 * | 1.000 | ||||||||

| (3) Leverage | 0.501 | 0.606 | 0.001 | 0.281 * | 1.000 | |||||||

| (4) Size (ln) | 12.143 | 2.455 | −0.141 | 0.046 | 0.041 | 1.000 | ||||||

| (5) Age | 35.719 | 31.234 | −0.075 | −0.125 | 0.012 | 0.054 | 1.000 | |||||

| (6) ROA (%) | 0.040 | 0.063 | −0.036 | 0.206 * | −0.057 | 0.259 * | −0.143 | 1.000 | ||||

| (7) Sector | 4.391 | 2.848 | −0.054 | 0.074 | 0.017 | 0.107 | 0.032 | 0.204 * | 1.000 | |||

| (8) Beta | 0.786 | 0.216 | −0.070 | −0.232 * | 0.067 | 0.160 | 0.096 | −0.357 * | −0.093 * | 1.000 | ||

| (9) Bod_indep (%) | 0.496 | 0.152 | 0.126 | −0.319 * | −0.153 | −0.100 | 0.112 | −0.283 * | −0.302 * | 0.257 * | 1.000 | |

| (10) Bod_size | 10.656 | 2.505 | −0.206* | −0.139 | −0.076 | 0.006 | 0.252 * | 0.005 | 0.015 | 0.015 | −0.021 | 1.000 |

| (1) | (2) | (3) | (4) | VIF | |

|---|---|---|---|---|---|

| DV: ESG Score | Model 1 | Model 2 | Model 3 | Model 4 | |

| Blau_index | 0.276 ** | 0.294 ** | 0.295 ** | 0.408 *** | 1.18 |

| (0.132) | (0.138) | (0.137) | (0.160) | ||

| CEO_duality (moderator) | 0.00389 | 0.0000911 | 1.42 | ||

| (0.0387) | (0.0381) | ||||

| Interaction | −0.562 *** | 1.25 | |||

| (0.208) | |||||

| Leverage | 0.00233 | 0.00223 | 0.00155 | 1.83 | |

| (0.0156) | (0.0161) | (0.0147) | |||

| Size | 0.00791 * | 0.00784 * | 0.00772 * | 1.20 | |

| (0.00425) | (0.00426) | (0.00414) | |||

| Age | −0.000236 | −0.000233 | −0.000170 | 2.56 | |

| (0.000365) | (0.000369) | (0.000374) | |||

| ROA | 0.243 | 0.241 | 0.263 | 1.86 | |

| (0.197) | (0.197) | (0.187) | |||

| Sector | −0.00581 | −0.00579 | −0.00624 | 2.95 | |

| (0.00624) | (0.00625) | (0.00621) | |||

| Beta | 0.127 ** | 0.127 ** | 0.130 *** | 1.34 | |

| (0.0515) | (0.0516) | (0.0482) | |||

| Bod_indep | 0.369 *** | 0.371 *** | 0.373 *** | 3.89 | |

| (0.0975) | (0.0987) | (0.0985) | |||

| Bod_size | 0.148 *** | 0.150 *** | 0.136 ** | 1.18 | |

| (0.0518) | (0.0548) | (0.0557) | |||

| Constant | 0.579 *** | 0.420 *** | 0.418 *** | 0.415 *** | |

| (0.0186) | (0.0610) | (0.0615) | (0.0601) | ||

| Observations | 128 | 128 | 128 | 128 | |

| Number of firms | 64 | 64 | 64 | 64 | |

| R-sq | 0.07 | 0.08 | 0.08 | 0.13 |

| (1) | (2) | (3) | (4) | VIF | |

|---|---|---|---|---|---|

| VARIABLES | Model 1 | Model 2 | Model 3 | Model 4 | |

| Shannon_index | 0.242 ** | 0.252 ** | 0.253 ** | 0.351 *** | 1.18 |

| (0.109) | (0.113) | (0.112) | (0.134) | ||

| CEO_duality (moderator) | 0.00285 | −0.000949 | 1.41 | ||

| (0.0388) | (0.0382) | ||||

| Interaction | −0.480 *** | 1.25 | |||

| (0.176) | |||||

| Leverage | 0.00199 | 0.00194 | 0.00138 | 1.85 | |

| (0.0157) | (0.0163) | (0.0151) | |||

| Size | 0.00798 * | 0.00791 * | 0.00789 * | 1.34 | |

| (0.00425) | (0.00426) | (0.00414) | |||

| Age | −0.000236 | −0.000233 | −0.000180 | 2.55 | |

| (0.000362) | (0.000367) | (0.000370) | |||

| ROA | 0.241 | 0.239 | 0.256 | 1.86 | |

| (0.198) | (0.197) | (0.188) | |||

| Sector | −0.00582 | −0.00581 | −0.00615 | 2.94 | |

| (0.00622) | (0.00623) | (0.00617) | |||

| Beta | 0.125 ** | 0.125 ** | 0.126 *** | 1.19 | |

| (0.0519) | (0.0521) | (0.0489) | |||

| Bod_indep | 0.366 *** | 0.368 *** | 0.367 *** | 3.92 | |

| (0.0972) | (0.0983) | (0.0979) | |||

| Bod_size | 0.148 *** | 0.149 *** | 0.137 ** | 1.17 | |

| (0.0515) | (0.0545) | (0.0553) | |||

| Constant | 0.579 *** | 0.421 *** | 0.421 *** | 0.418 *** | |

| (0.0185) | (0.0610) | (0.0615) | (0.0600) | ||

| Observations | 128 | 128 | 128 | 128 | |

| Number of id | 64 | 64 | 64 | 64 | |

| R-sq | 0.06 | 0.07 | 0.07 | 0.12 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Romano, M.; Cirillo, A.; Favino, C.; Netti, A. ESG (Environmental, Social and Governance) Performance and Board Gender Diversity: The Moderating Role of CEO Duality. Sustainability 2020, 12, 9298. https://0-doi-org.brum.beds.ac.uk/10.3390/su12219298

Romano M, Cirillo A, Favino C, Netti A. ESG (Environmental, Social and Governance) Performance and Board Gender Diversity: The Moderating Role of CEO Duality. Sustainability. 2020; 12(21):9298. https://0-doi-org.brum.beds.ac.uk/10.3390/su12219298

Chicago/Turabian StyleRomano, Mauro, Alessandro Cirillo, Christian Favino, and Antonio Netti. 2020. "ESG (Environmental, Social and Governance) Performance and Board Gender Diversity: The Moderating Role of CEO Duality" Sustainability 12, no. 21: 9298. https://0-doi-org.brum.beds.ac.uk/10.3390/su12219298