Is Environmental Sustainability Taking a Backseat in China after COVID-19? The Perspective of Business Managers

1

College of Information and Management Science, Henan Agricultural University, Zhengzhou 450046, China

2

Centre for Environment and Sustainability, University of Surrey, Surrey GU2 7XH, UK

*

Author to whom correspondence should be addressed.

Sustainability 2020, 12(24), 10369; https://0-doi-org.brum.beds.ac.uk/10.3390/su122410369

Submission received: 3 November 2020

/

Revised: 5 December 2020

/

Accepted: 10 December 2020

/

Published: 11 December 2020

(This article belongs to the Special Issue Assessment of Socio-Economic Sustainability and Resilience after COVID-19)

Abstract

:China’s quick economic recovery from COVID-19 has presented a narrow but vast opportunity to build an economy that is cleaner, fairer, and safer. Will China grab this opportunity? The answer rests with both business managers and the government. Based on a questionnaire survey of 1160 owners and managers of companies headquartered in 32 regions of China and covering 30 industries, this paper explores how COVID-19 has impacted Chinese business, especially with regard to the three dimensions of sustainability (economic, social, and environmental). The results suggest that Chinese companies’ sustainability priorities have been shifted towards the social dimension both during COVID-19 and into the post-pandemic phase, regardless of the type of ownership, company size, or market focus (domestic, overseas, or mixture of the two). However, all types of company prioritize the need for economic sustainability in the post-pandemic phase and in relative terms the importance of the environmental dimension has been diminished. Hence the potential for a post-pandemic environmental rebound effect in China is clear. But it does not have to be the case if Chinese businesses and the government take actions to change its recovery plans to embrace the environmental dimension of sustainability. The paper puts forward some suggestions and recommendations for businesses and the government.

1. Introduction

The new coronavirus (COVID-19) has posed an unprecedented challenge to global sustainable development (SD). As of December 2020, more than 65 million people have the disease and more than 1.5 million have died from it [1]. Strategies such as large-scale coronavirus screening tests, stringent hygiene protocols, isolation, and social distancing have been adopted by governments worldwide to fight the virus, and these have resulted in significant negative economic impacts in many countries. The whole world has almost been brought to a standstill as economic growth faltered and international transport greatly reduced, although on the positive side these have resulted in a significant reduction in global carbon emissions [2]. However, some argue that the drop in CO2 emissions is just temporary as it does not reflect any significant structural change in the economic, transport, or energy system [3], and unless there is such change, it will be hard to avoid the environmental rebound effect when COVID-19 is over [4,5]. At the same time, other environmental issues such as waste recycling and water contamination have been neglected during the pandemic [2] and new types of pollution have originated from the large-scale manufacture and distribution of COVID-19 protective gear such as face masks [6].

In fact, COVID-19′s unprecedented effect on most types of business operations may have already led to some sustainability initiatives being modified or cancelled [7]. A survey carried out in March 2020 by 101 UK-based energy and sustainability professionals found that 60% of the organizations had either confirmed their plans to pause investment in sustainability solutions or were considering doing so as a result of COVID-19 [8]. In an effort to avoid an environmental rebound effect, the Institute for Global Environmental Strategies [9] has been calling for a green/sustainable post-pandemic recovery.

In April 2020, Ursula von der Leyen—the president of the European Commission—pledged more than USD 800 billion to a European Green Deal which would turn the COVID-19 crisis into an opportunity to rebuild the EU economy in a different and more sustainable form [10]. EU leaders have agreed on an EU recovery plan which proposed to halve greenhouse gas emissions over the next 10 years by spending USD 28 billion to increase renewable energy capacity, USD 100 billion annually to improve home energy efficiency, and up to USD 67 billion to build zero-emission trains [11]. The International Energy Agency [12] has called for an annual one trillion USD investment in clean energy over the next three years. The South Korean government has promised a USD 10 billion Green New Deal to invest in renewable energy and an improvement in energy efficiency [13]. Costa Rica has become one of the few developing countries that has put in place a green recovery plan by introducing a new fee on gasoline as a way of funding social-welfare programs and is planning to issue new green bonds to fund the next stage of climate adaption programs [14]. The International Monetary Fund [15] has made climate resilience a key criterion for its lending and in June its 50 borrowing countries committed to include climate change in their COVID-19 recovery plans.

However, at the time of writing other major global players such as the US and China have no clear environmentally friendly recovery plans in place. Chinese leaders in May 2020 endorsed a proposal to spend USD 1.4 trillion on ‘new infrastructure’ including electric-vehicle charging stations, high-speed rail, and 5G technology which would stimulate economic growth with lower emissions, but there is no EU-type climate conditionality attached to its infrastructure projects. Despite the US’s decision to withdraw from the Paris Agreement, President Xi Jinping pledged that China will fulfil its obligation under the UN emission treaty. At the 19th Congress of the Chinese Communist Party in October 2017, Xi claimed that China was in the ‘driving seat’ when it comes to international cooperation on climate change. In fact, as an increasingly influential global player and amid COVID-19, China showed leadership by clearly stating its commitment to increasing its contribution to WHO while US decided to withdraw funding from the agency. In a virtual UN General Assembly in New York in September 2020, Xi Jinping promised that China would go carbon neutral before 2060 [16]. However, Xi’s pledge would need to be backed up with more detailed and concrete implementation plans which must reconcile carbon neutrality with China’s ongoing support for the fossil fuel industry [17].

Once the COVID-19 hot spot of the world, China was the first country to shut down while the rest of the world, most notably the USA, still underestimated the risk posed by the virus. Shutting down the Chinese economy may have helped address the spread of the virus, but it did have severe consequences. China’s economy suffered its first contraction in 28 years by shrinking 6.8% in the first quarter of 2020 compared to the same quarter in 2019. However, China has since then been on the path to recovery, and a year-on-year growth of 3.2% was achieved in the second quarter of 2020 [18]. As the first economy that is successfully (so far) recovering from COVID-19, China has presented itself a “narrow window, but vast opportunity” to build back its economy into something that is cleaner, fairer, and safer [19]. Based on a questionnaire survey of 1160 owners and managers of companies headquartered in mainland China as well as Hong Kong, Taiwan, and Macau and covering 30 industries, this paper explores how COVID-19 has impacted Chinese business, especially with regard to the three dimensions of sustainability (economic, social, and environmental) and provides an ‘ex-post’ assessment of the post-pandemic situation. It is assumed that China’s experience with green/sustainable recovery would make it a useful case study to explore given that the shape of the recovery elsewhere in the world is uncertain.

A number of theories helped inform the research, including the environmental rebound effect, slack resources theory, and the available funds hypothesis, and these are summarized in the following ‘Theoretical Background’ section. Previous literature on the impact of COVID-19 is also included in this section. This is followed by the hypotheses and the methodology employed in this study, including question design, data collection, and data analysis. Section four presents the results of the research, including the demographic information of the respondents, the impact that COVID-19 has had on the companies, coping strategies, and the current recovering situation, the changing sustainability priorities of the companies will also be explored in this section. Discussion of the results is also included in this section. The last section draws out some conclusions and suggests some implications for company mangers as well as theoretical implications and suggestions for future research.

2. Theoretical Background

2.1. Environmental Rebound Effect

The rebound effect is generally defined as the difference between the expected and actual environmental gains from an efficiency increase after the implementation of new technologies or other measures [4,20]. A good example of a rebound effect is found when a technological improvement in vehicle fuel efficiency makes driving cheaper but the saving is often offset by driving faster or further than before. Hence, resource efficiency may not reduce the use of resources and may even generate the contrary. Empirical rebound studies often try to capture the secondary effects of policies and behaviors. For example, although the use of information and communications technologies (ICT) was thought to be environmentally beneficial as it reduces road traffic and saves commuting time, Gossart [21] provided evidence of the rebound effect related to ICT and suggested ways of overcoming rebound. Of course, the magnitude of any rebound effect varies depending on cultural and structural context. For example, although the industrial Internet of things (IIoT) could potentially improve resource efficiency by establishing highly digitized, interconnected, self-regulating, and decentralized industrial value chains [22,23], it could rebound. By comparing China and Germany, Muller and Voigt [22] found the introduction of IIoT would cause more serious job loss problems in China than in Germany, and greater data security concerns in Germany than in China, while both countries would equally face a problem over skill shortages.

Various policies and measures taken by countries to contain the COVID-19 pandemic have caused abrupt changes in business operation, consumption, social interaction, and so on, and these changes have led to improvements in some environmental indicators such as air quality and greenhouse gas emissions. But will a rebound effect take place such that these changes are not permanent? Will the environmental improvement last in the future when the pandemic is over? A further question is whether the increased popularity of ICT and digitalization spurred by COVID-19 may backfire, as indicated by Muller and Voigt [22] and Gossart [21].

2.2. Sustainable Development in China

The principles of sustainable development have deep roots in China. The earliest ideas relating to sustainable development were recorded during the Xia dynasty (2070–1600 BC) in the Yellow River area in the form of religious beliefs. Back then, people respected the mountains and rivers in the same way they did their spiritual icons [24]. Chinese traditional philosophies such as Confucianism, Taoism, and Yin–Yang contain elements that are fundamental to sustainable development. For example, the basic foundation of Confucianism is the harmony between humans and nature while Taoism believes that all creatures are created by nature and advocates that following nature and taking no action is the best action to take [25]. Sustainable development also had an important place in Chairman Mao’s administration. He called for green policies because they would benefit agriculture, industry, and other aspects of society [24]. In September 2015, President Xi Jinping attended the UN Sustainable Development Summit and joined other world leaders in adopting the program entitled Transforming Our World: the 2030 Agenda for Sustainable Development, which opened a new era for the undertaking of global sustainable development and charted the course for national development and international development cooperation. At his various speeches to international audiences, Xi said “green mountains and clear water are as good as mountains of gold and silver.” Nonetheless, despite these historical roots and claims to be in the “driving seat” when it comes to tackling climate change, the question remains as to whether China will continue its leadership in sustainability during COVID-19; will climate change issues soon be forgotten after the pandemic as the emphasis shifts in favor of economic development?

2.3. Ownership, Size, Slack Resources, and Sustainability

Ownership has been widely discussed as a factor which could potentially influence a company’s pursuit of social and environmental responsibility [26]. Based on the Shanghai National Accounting Institute (SNAI) CSR Index, Li and Zhang [27] explored whether and how ownership structure affects corporate social responsibility (CSR) in emerging markets, and found that the stronger the state’s controlling of a firm is then the better the firm’s social and environmental performances. Zhang et al. [28] investigated corporate social responsibility of a group of Chinese state-owned enterprises (SOEs) and private-owned firms and found that Chinese SOEs are more environmentally responsible than private owned firms. Oh et al. [29] employed a sample of 118 large Korean firms and found a significant and positive relationship between CSR ratings and ownership of institutions (which are under strong influence of the Korean government). However, Oh et al. [29] also found foreign invested firms have relatively high CSR ratings and this result was confirmed by Lee et al. [30] who conducted a study using panel data of the Korea Economic Justice Institute (KEJI) Index and found a positive correlation between CSR performance and foreign ownership.

Size has also been discussed as a factor that may influence a firm’s social and environmental engagement. A positive relationship between firm size and social and environmental engagement has been found for firms in developed countries by Fry and Hock [31], Fombrun and Shanley [32], Pava and Krausz [33], McWilliams and Siegel [34], and Elsayed [35]. In recent years, this relationship has also been explored in emerging markets. For example, Zhang et al. [28] found that larger companies engage more in social and environmental responsibility in China than do smaller ones. The same conclusion was reached by Li and Zhang [27] in China and Muller and Kolk [36] in Mexico. Slack resources are the potentially utilizable resources that can be diverted or redeployed for the achievement of organizational goals. Slack resource theory suggests that because more profitable firms have more organizational slack (financial and other), they are likely to be more committed to CSR participation [37]. Based on slack resource theory, Preston and O’bannon [38] proposed an available funds hypothesis which suggests a positive relationship between a company’s profitability and its social performance, i.e., companies with better financial performance would contribute more to fund discretionary projects. The available funds hypothesis was also found to be the case for companies in China [28].

2.4. The Impact of COVID-19

Understandably, recent publications on COVID-19 have focused mainly on medical and epidemiological dimensions of the pandemic, including treatments and vaccine development [39,40,41]. Some have noted the temporary improvement in environmental quality due to virus containment measures but have also expressed concerns about a possible rebound effect after the pandemic [2,3,4,5,42,43]. A few studies have looked at the economic and social impacts of COVID-19, especially on businesses. Barreiro-Gen et al. [7] surveyed 653 organizations internationally to analyze how the outbreak of COVID-19 had affected their sustainability priorities and they found that there had been a shift towards emphasizing the social dimension for most organizations while the environmental dimension had declined in importance. As a result, Barreiro-Gen et al. [7] suggested measures to avert the possible post-pandemic environmental rebound effect. Bartik et al. [44] explored the impact of COVID-19 on small businesses in the US and found that mass layoffs and closures occurred just a few weeks into the crisis and the risk of closure was negatively associated with the expected length of the crisis. Bartik et al. [44] also found that small businesses in the US are financially fragile and many of them anticipated problems such as bureaucratic hassles when seeking COVID-19 related funding.

Zabaniotou [45] considered COVID-19 as proof of an unsustainable human civilization and linked the pandemic to ecological sustainability and resilience. Zabaniotou [45] proposed a humanistic approach as a solution, based not only on virus containment strategies but also an ecological balance. A framework based on resilience was also proposed by D’Adamo and Rosa [46] as a post-pandemic recovery strategy.

However, few analyses to date have looked at the impacts of COVID-19 on sustainability in China especially from the point of view of businesses. This paper aims to explore the impacts COVID-19 may have had on sustainable development in China over both the short-term and long-term from the perspective of business. In particular, it sets out the results of research that sought to investigate whether and how priorities have changed among the three pillars of sustainable development during and post COVID-19 for companies with different ownerships, i.e.,:

- State-owned enterprise (SOE)

- Domestic private-owned company

- Foreign invested company (FIE)

- Domestic individual-owned company

3. Hypothesis and Research Design

3.1. Hypothesis

There are various types of businesses in China. Based on the ownership, they include mainly state-owned enterprises (SOEs), private-owned companies, foreign invested enterprise (FIE), and individual-owned companies. SOEs are companies that are owned and run by the Chinese government or stock companies having the state as the dominant stockholder. An FIE is a company that is invested solely by a foreign company (including companies based in Hong Kong, Macau, and Taiwan) or created through a partnership between foreign and Chinese investors. A Chinese domestic private-owned company is a Chinese company that is neither an SOE or an FIE and hires eight or more employees. An individual-owned company is a company that is neither an SOE nor an FIE and hires less than eight employees [47]. Both private-owned and individual-owned companies focus on domestic and overseas markets, with the larger companies being more orientated towards overseas. Because of the different stances of different types of companies in China, it is assumed that their sustainability priority changes would be different as a result of COVID-19. Based on the previous literature reviewed in Section 2.3, two hypotheses can be proposed:

Hypothesis 1 (H1).

SOEs and FIEs prioritize social sustainability and environmental sustainability more than domestic private and individual owned companies after COVID-19.

Hypothesis 2 (H2).

Bigger companies prioritize social and environmental sustainability more than small companies after COVID-19.

However, there could be a complication arising from the market focus of the company. Although the Chinese domestic market was hit hard at the beginning of the pandemic (February and March) when COVID-19 was mostly spreading within China, the overseas market was affected badly from March onward when the virus was spreading rapidly within Europe, US, and other parts of the world. Understandably, companies that have both domestic and overseas markets can avoid the negative economic impact better than companies that have a single market focus. Such companies with a diverse market focus could sell their products to overseas consumers in February and March while markets in China were subdued, but then switch to selling their produce/services in China after March once overseas markets had declined. Hence, based on slack resources theory and available funds hypothesis, a third hypothesis could be framed as:

Hypothesis 3 (H3).

Companies that enjoy both domestic and overseas markets prioritize social and environmental sustainability more than companies that focus solely on either domestic market or overseas market after COVID-19.

3.2. Data Collection

After a pilot study in June 2020, a questionnaire was finalized to explore if companies in China had changed their views of sustainable development. The questionnaire had a number of parts, including the demographic characterization of the surveyed companies, the general impact that COVID-19 had on them, how they coped with the impact, and the changing priority of the companies regarding the three-pillars of sustainable development. The targeted respondents were company owners and other managers across China, and the survey was designed to span all four types of company noted above as well as different sizes and market orientations. The survey was carried out online through a Chinese online survey platform Wenjuanxing in July 2020 with link to or QR code of the questionnaire being sent to potential respondents. A total of 1178 questionnaires were returned, of which 1160 (98%) were considered valid in the sense that they came from different IP addresses, had a clear indication of their company ownership and the questionnaire had been completed in no less than 207 s (the shortest time tested by the authors to complete the questionnaire). There was no reward for completing the questionnaire, so respondents had little incentive to attempt multiple returns. While it was possible for a single respondent to complete multiple returns from a number of IP addresses, it would seem unlikely in practice.

Respondents’ views of the importance of the three dimensions of SD (i.e., social, environmental, and economic) during three periods of COVID-19 (i.e., pre, during, and post) were assessed based on a five-point Likert scale with 1 being the least important, 5 being the most important, and the others are in the middle—the higher the score, the higher the perceived importance of the dimension. The average change (mean change) of the scores at later stages of COVID-19 compared to earlier stages (i.e., during vs. pre, post vs. during, and post vs. pre) were calculated using the following equation:

Mean change (environmental sustainability, post vs. pre) = Mean score (environmental sustainability, post) − Mean score (environmental sustainability, pre).

Similarly, for other changes in mean score:

Mean change (environmental sustainability, during vs. pre), Mean change (environmental sustainability, post vs. during), Mean change (social sustainability, post vs. pre), Mean change (social sustainability, during vs. pre), Mean change (social sustainability, post vs. during), Mean change (economic sustainability, post vs. pre), Mean change (economic sustainability, during vs. pre), and Mean change (economic sustainability, post vs. during).

If the mean change (environmental sustainability, during vs. pre) was bigger than zero, then environmental sustainability was assumed to have been prioritized more during COVID-19 [7]. If the mean change (environmental sustainability, post vs. during) was bigger than zero, then environmental sustainability was assumed to have been prioritized immediately after the pandemic. If the mean change (environmental sustainability, post vs. pre) was bigger than zero, then environmental sustainability was assumed to have been prioritized over the longer term after the COVID-19 impact had ended. The bigger the mean change, the higher the level of the prioritization. The same interpretations were applied to the other two dimensions of SD.

3.3. Data Analysis

SPSS 24 was employed to store and analyze the data. Crosstab and Chi-square tests were employed to test the correlation between company ownership, size, age, and market focus. Welch’s ANOVA was used to test changes in priority of sustainable development during and post COVID-19 for Chinese companies with different ownership, size, and market focus. As the data comprised scores, and these could not be assumed to be normally distributed, Welch’s ANOVA was deemed to be the best alternative and does have some advantages compared to non-parametric tests such as Kruskall–Wallis. Also, Chi-square and Welch’s ANOVA are relatively straightforward to implement and interpret compared to alternative approaches such as regression or factor analysis.

4. Results and Discussions

4.1. Company Profile

Table 1 shows the profiles of the surveyed companies based upon the answers provided by respondents. Table 1a presents the distribution of the sample of companies based on four main company categories:

- Ownership of the company (domestic private-owned company, SOE, FIE, and domestic individual-owned company)

- Number of employees (1000 and above, 300–999, 20–299, and 1–19)

- Age (less than 4 years, 4–10 years, 11–20 years, and older than 20 years)

- Market focus (overseas-focused, domestic-focused, mixed but mostly domestic-focused, and mixed but mostly export-focused)

Also shown in Table 1 are the geographical distribution of the companies in China (Table 1b) and their main area of activity (manufacturing, wholesale/retail, etc.; Table 1c).

Out of 1160 companies, 70.5% of them (818) were private-owned, 195 (16.8%) were SOEs, 76 (6.5%) were FIEs, and 71 (6.1%) were individually-owned. Half of the companies (588) had between 20 and 299 employees, a quarter (292) had between 300 and 999, 157 (13.5%) had 1000 employees and more, while only 123 (10.6%) had less than 20 employees. In terms of age, almost half of them (554) had existed for between 4 and 10 years, 262 (22.6%) had been around for between 11 and 20 years, and 119 (10.2%) was established within the past 4 years. Based on where the customers were mostly located, 65 (5.6%) of the companies saw themselves as overseas-focused, 201 (17.3%) were domestic-focused, one third of them (380) had both domestic and overseas customers with the domestic market being the main focus, while 514 (44.3%) also enjoyed both markets but were mostly overseas-focused.

The surveyed companies were headquartered in 32 regions in China; 241 (20.8%) were in Beijing, 155 (13.4%) were in Shanghai, 84 (7.2%) in Zhejiang, 79 (6.8%) in Jiangsu, 76 (6.5%) in Hebei, 70 (6.0%) in Guangdong, 68 (5.9%) in Henan, 55 (4.7%) in Sichuan, 53 (4.6%) in Hubei, 37 (3.2%) in Fujian, 240 (20.8%) were in other parts of China. The companies covered 30 industries, including IT/e-commerce/internet service (22.1%), manufacturing (13.7%), wholesale/retail (7.7%), fast moving consumer goods, i.e., snacks, drinks, cosmetics (6.9%), education/research/training (6.8%), clothing/textile/leather (4.9%), catering/entertainment/tourism (4.6%), real estate/construction (4.5%), communication/network equipment/value-added service (2.8%), finance (2.5%), and 23.6% other industries.

4.2. Ownership, Characterization, the General Impact of COVID-19, and Current Business Resumption

Table 2 indicates that company characterization (size, age, and market focus) and company ownership are significantly correlated (Pearson Chi-square tests all statistically significant at p < 0.01). As perhaps would be expected, it seems SOEs and FIEs are bigger in terms of number of employees, while private and individual owned companies, especially individual-owned, are smaller in size. SOEs and FIEs tend to have existed for longer than private and individual owned companies. In terms of the main market, SOEs tend to have mixed market, FIEs tend to have a more export focused market, private-owned companies tend to have a more domestic focused market, while individual-owned companies enjoy either overseas market or domestic market.

Generally speaking, companies with different ownerships have been impacted by COVID-19 to different extents. SOEs would seem to have been the least impacted with 28.7% of respondents in that category claiming that the company had been impacted in a ‘major’ way. The equivalent figure for FIEs was 31.6%. Individual-owned and private-owned companies appear to have been hit much harder by the pandemic with 54.9% and 43.5% (respectively) of respondents from those categories claiming that their companies had been majorly impacted by the pandemic. This is perhaps to be expected given that SOEs are state-backed and perhaps have better access to bank loans and state support. However, private-owned companies resumed their business almost as fast as SOEs with 34.4% of private-owned companies recovering more than 75% of their production capacity (35.9% for SOEs), followed by FIEs (30.3%). Individual-owned companies recovered the slowest with only 12.7% of them recovering more than 75% of their production capacity. Perhaps this is partly related to the speed at which China was able to bring the outbreak under control, but it may also be related to the smaller size of individually owned companies which means that they find it harder to lever support from banks and the state.

4.3. Sustainability Priority Change for Companies Having Different Types of Ownership

Table 3 indicates that companies with different ownerships have statistically significant different social, economic, and environmental priorities before, during, and after COVID-19 (all F-values from Welch’s ANOVA were statistically significant at p < 0.01), and there is an increasing trend of means in each of the three dimensions of SD following the stages of COVID-19. For example, for private-owned companies, the mean score for the social dimension of SD increased from 3.30 prior to COVID-19 to 4.09 when this research was conducted in July 2020 (during the pandemic), and to 4.34 after the pandemic had ended in China. Clearly, COVID-19 has made companies with all types of ownership realize the importance of all three dimensions of SD. However, the highest mean scores in the table across all four types of company are for the economic dimension of SD in the post-COVID-19 stage (shaded cells in Table 3), indicating the importance of regaining economic strength over the longer term after the pandemic.

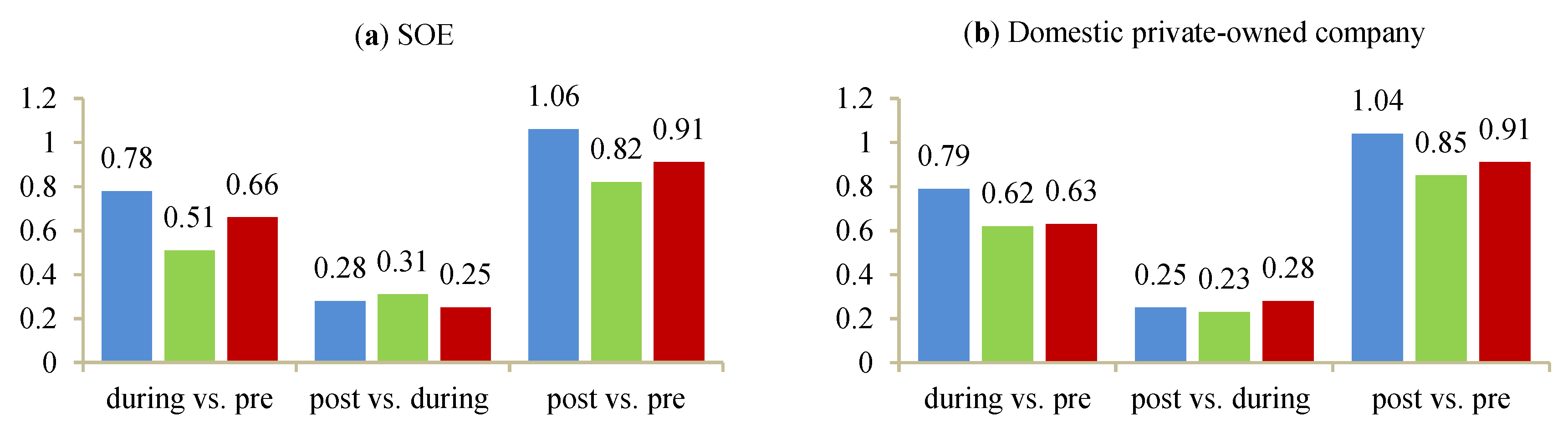

A Welch’s ANOVA test was performed on the scores for the dimensions of SD over the three periods of COVID-19 (pre, during, and post) and the results are shown in Table 4. In order to more clearly illustrate the trends in Table 4, Figure 1 presents the changes in the mean scores between the periods of COVID-19.

The results in Table 4 indicate that, for SOEs, there exists a significant difference among three dimensions of SD for pre- and post-COVID-19 periods, but there is no difference among dimensions of SD for the period during COVID-19, indicating the confusing state of Chinese SOEs during the pandemic. Figure 1a indicates that for Chinese SOEs, social sustainability was the most prioritized during the pandemic with a mean change (social responsibility, during vs. pre) in score of 0.78, but it was less prioritized than economic sustainability immediately after the pandemic (0.28 vs. 0.31); however, it was the most prioritized in a longer term after the pandemic comparing to economic and environmental sustainability (1.06 vs. 0.82 vs. 0.91). It would appear from Figure 1 that over the longer term SOEs prioritize social sustainability more than other companies (with a mean change of 1.06), followed by private-owned companies (1.04), individual-owned companies (0.98), and FIEs (0.88). It is not surprising given that Chinese SOEs have reportedly donated RMB 5.8 billion to help fight COVID-19, accounting for 47% of the total amount of corporate donations China received in response to COVID-19, while Chinese domestic private companies contributed 41% and FIEs only 12% [48]. Chinese SOEs’ generosity in philanthropy has been well documented and the reason for their generosity is that they are highly integrated with the state and thus have looser budget constraints [49]. However, the motive of Chinese domestic private companies’ donations, especially when facing a large-scale crisis, is mostly related to the protection of their property rights and nurturing of political connections, which in turn would lead to better profitability [50]. However, even with the long-term priority shift to the social dimension of SD after the pandemic, economic sustainability has remained absolutely essential post-COVID-19 for Chinese SOEs (4.47, Table 4), implying the falling importance of environmental sustainability at the post-COVID-19 era. Hence it would seem that Chinese SOEs are not prioritizing environmental sustainability as a result of COVID-19.

Table 4 also indicates that there exists a statistically significant difference among dimensions of SD for each stage of COVID-19 for Chinese domestic private-owned companies (p < 0.01), indicating a clear shift of priority of SD along with the development of COVID-19. In terms of the dynamics, Figure 1b indicates that for Chinese domestic private-owned companies, social sustainability was the most prioritized during the pandemic, with a mean change (social sustainability, during vs. pre) equal to 0.79, followed by environmental sustainability (0.63) and economic sustainability (0.62). But the priority shifted to environmental sustainability immediately after the pandemic (0.28 vs. 0.25 vs. 0.23). However, the long-term priority after the pandemic shifted back to social sustainability, followed by environmental sustainability, then economic sustainability (1.04 vs. 0.91 vs. 0.85). However, even with the priority shift to social sustainability after the pandemic, the absolute importance of the economic aspect of sustainability for this group of companies is clear with the highest mean score (4.48, Table 4). As with the SOEs, this indicates that environmental area of SD is also the least important dimension of sustainability for Chinese domestic private-owned companies.

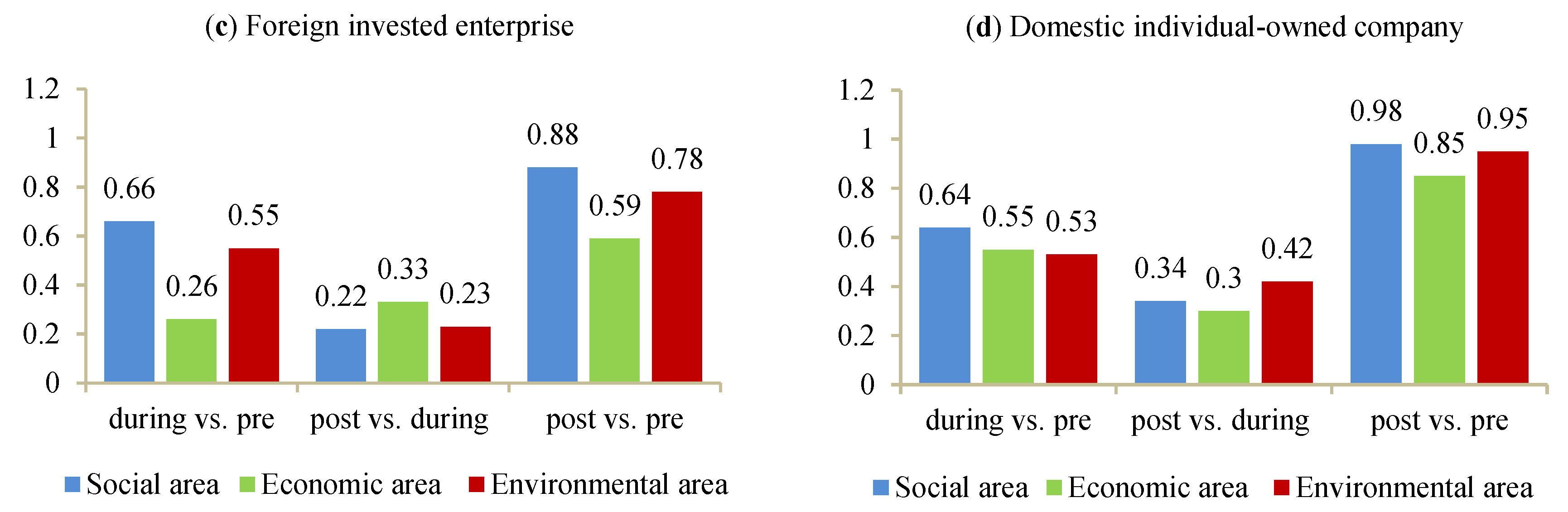

The results in Table 4 for FIEs indicate that there is a statistically significant difference among three dimensions of SD for the pre-COVID-19 period. But such difference does not exist for periods amid and post the pandemic. Figure 1c presents the mean changes in score for the FIEs. Clearly, during the pandemic, social sustainability has gained priority (0.66), more than environmental sustainability (0.55), while the least prioritized one is economic sustainability (0.26). But immediately after the pandemic, the priority shifted to economic aspect of SD with the mean change (economic sustainability, post vs. during) being 0.33, followed by environmental sustainability (0.23) and social sustainability (0.22). However, the long-term priority after the pandemic returned to the social area of sustainability with the mean change (social sustainability, post vs. pre) being 0.88, followed by environmental sustainability (0.78) and economic sustainability (0.59). Hence it would seem that FIEs in China were uncertain what to prioritize during and post the pandemic. However, with the highest mean scores pre-, during, and post-COVID-19, economic sustainability remains the all-time essential for FIEs operating in China.

For the Chinese domestic individual-owned companies, Table 4 suggests that there is no statistically significant difference among the dimensions of SD for each COVID-19 stage. However, just like other types of companies, Chinese domestic individual-owned companies see economic sustainability as essential throughout the pandemic stages (pre, during, and post, Table 4). However, in terms of the changes in score, Figure 1d indicates that Chinese domestic individual-owned companies prioritized social sustainability the most during COVID-19 with mean change (social sustainability, during vs. pre) being 0.64, followed by economic sustainability (0.55) and environmental sustainability (0.53). The most prioritized immediately after COVID-19 is environmental sustainability (0.42), followed by social sustainability (0.34) and economic sustainability (0.30). But over the longer term, the individual-owned companies prioritized social sustainability the most (0.98), followed by environmental sustainability (0.95) and economic sustainability (0.85).

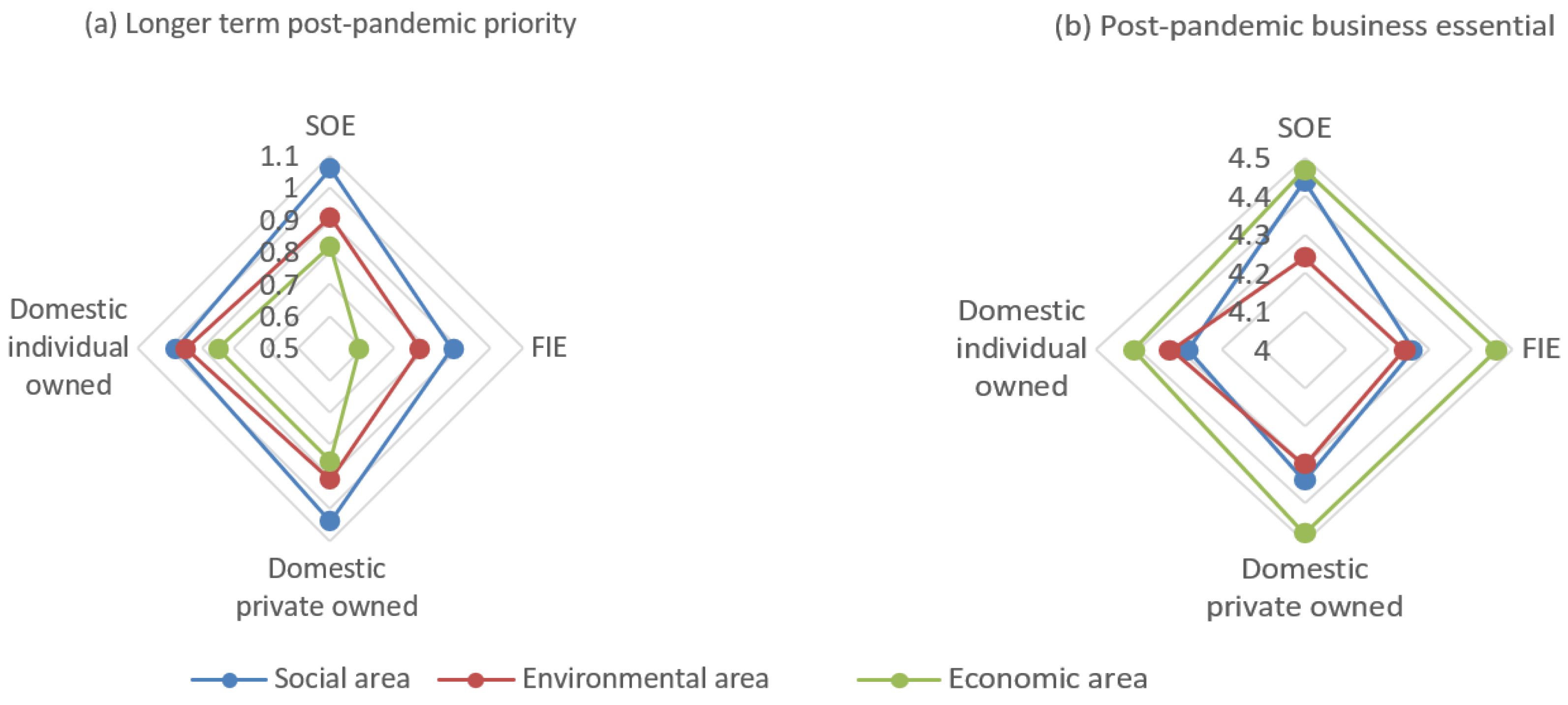

Based on these results, Figure 2 provides a picture of the longer-term post-pandemic priority and post-pandemic business essential for companies with different ownership. It is clear that hypothesis 1 has failed. Chinese SOEs and private companies have responded to COVID-19 by prioritizing social sustainability more during the pandemic and also in the longer term following the pandemic. By way of contrast, FIEs and individual-owned companies have prioritized social sustainability less since the outbreak of COVID-19 (Figure 2a). This result is consistent with the findings of Li and Zhang [27], Zhang et al. [28], and Oh et al. [29] that state ownership has a positive relationship with social performance. However, the result is contrary to those of Oh et al. [29] and Lee et al. [30] who found that foreign invested firms are good CSR performers. It is a disappointing finding considering the large number of FIEs in China (960,725 by the end of 2018 [51]), whose contribution to social and environmental development would make a difference to China’s long-term sustainability.

However, even with a priority for the social and environmental dimensions, economic sustainability is considered essential by all types of companies post-COVID-19, and this is more obvious for SOEs, domestic private-owned companies, and FIEs (Figure 2b), suggesting that environmental sustainability is the only one of the three dimensions that has been overlooked after the pandemic. This confirms the concerns of a post-pandemic environmental rebound effect as mentioned by Freire-Gonzalez and Vivanco [4], McCloskey and Heymann [5], Wang and Su [42], and Bao and Zhang [43]. It is even more worrying considering the bigger influence of SOEs, domestic private-owned companies, and FIEs in China’s long-term sustainability.

4.4. Company Size Analysis

As noted in Table 2, company size is related to company type, with SOEs and FIEs being larger in terms of number of employees compared to the domestic private companies. But in order to pick up on any effects of company size, Table 5 presents the results of a Welch’s ANOVA test using four categories based on company size. Large companies (mostly SOEs and FIEs) are defined as those having 1000 or more employees, medium companies are those having 300 to 999 employees, small companies are those having 20 to 299 employees, and micro-companies are those having 1–19 employees.

The results in Table 5 indicate that no matter what size the companies are, their social, economic, and environmental aspects of sustainability are statistically different before, during, and post COVID-19, with a clear increasing trend of the importance of all of them as the pandemic progressed. Again, the highest values go to the post-pandemic economic sustainability for companies of all sizes (shaded cells in Table 5). This is further evidence that although companies of all sizes are devoted to all areas of sustainable development, economic sustainability will still be essential in the post-pandemic era.

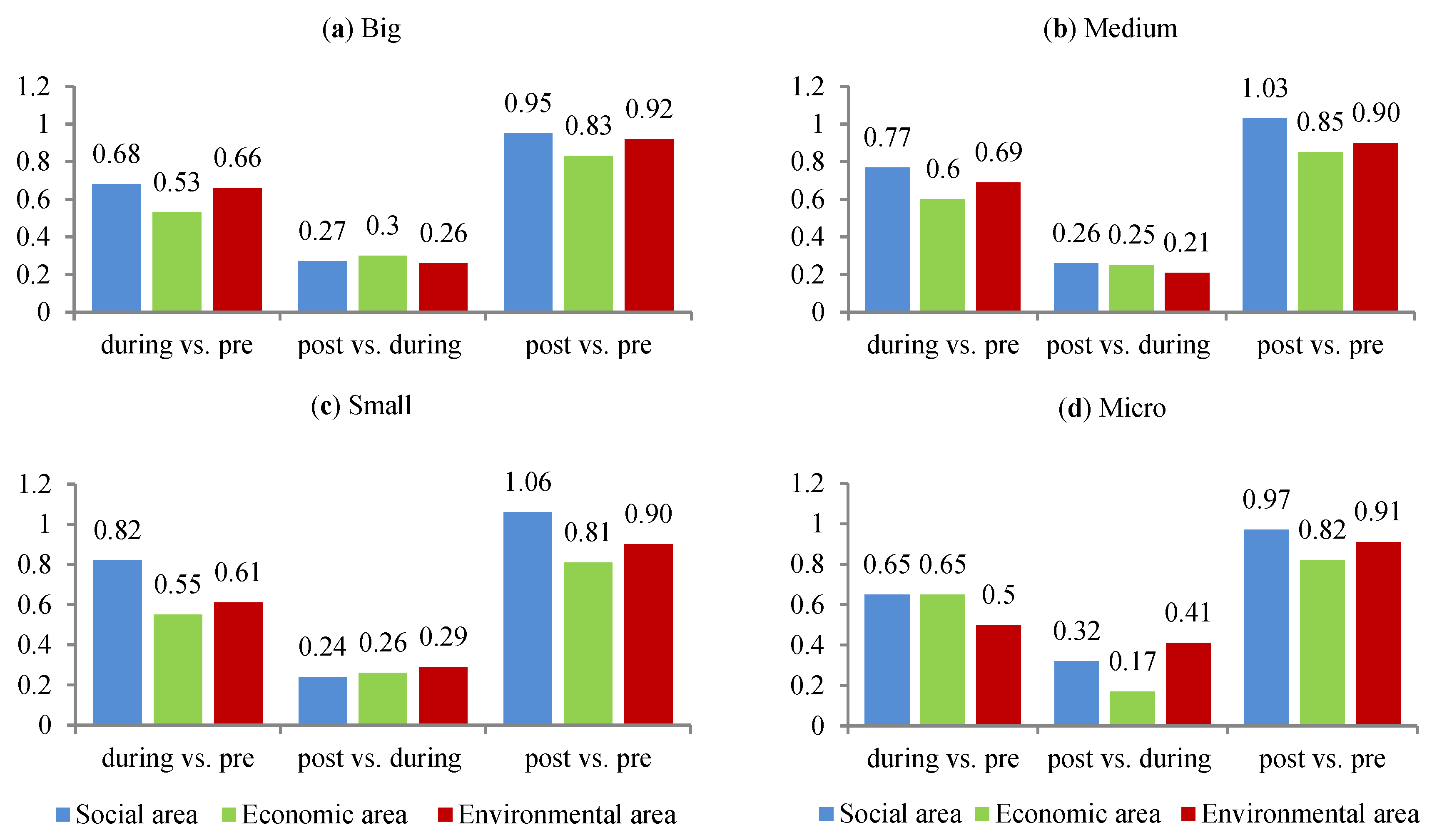

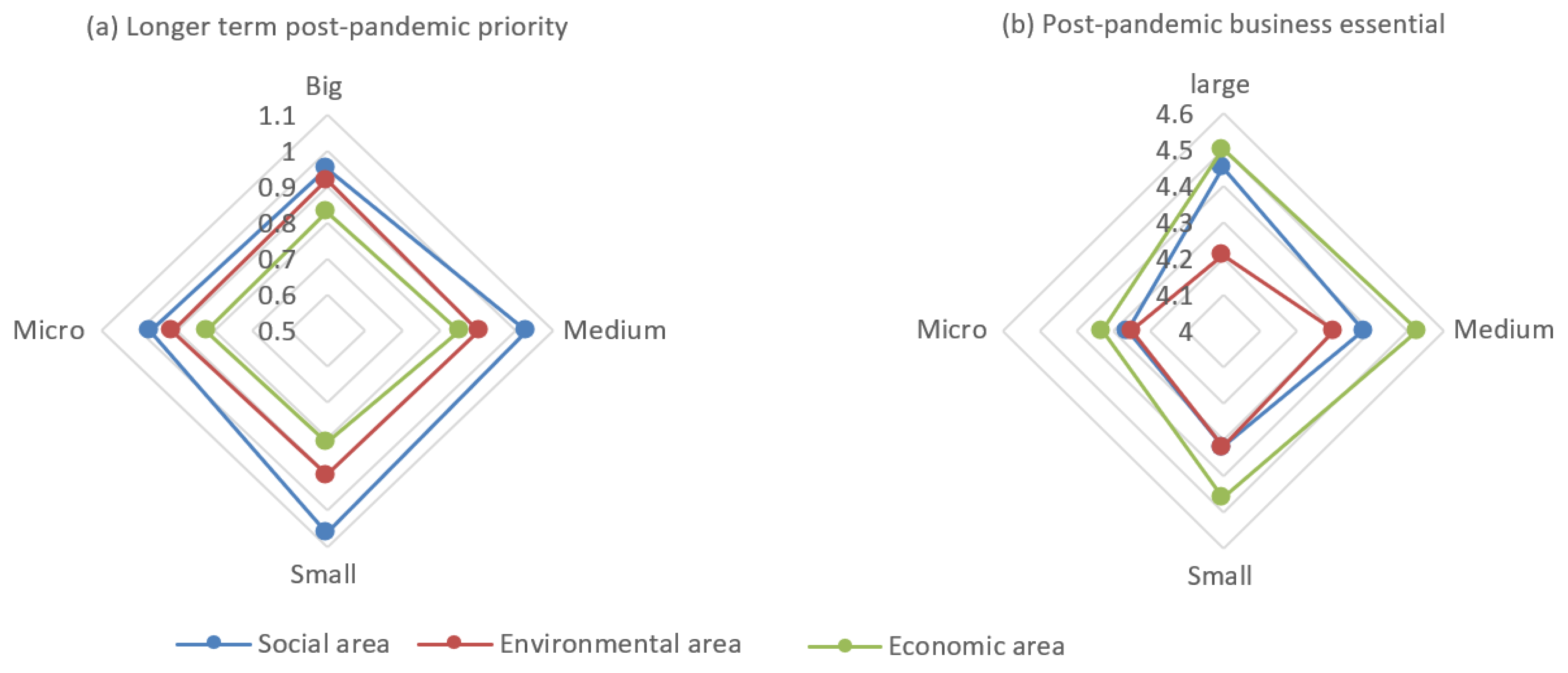

Figure 3 indicates that comparing to pre-COVID-19, big-, medium-, and small-sized companies prioritized social sustainability the most during the pandemic among three areas of SD with the mean changes (social sustainability, during vs. pre) being 0.68, 0.77, and 0.82, respectively (the left clusters of Figure 3), while micro-sized companies prioritized both social and economic sustainability during the same timeframe (both are 0.65). The priorities vary for the period between post and during COVID-19 (the middle clusters of Figure 3), while large companies prioritize economic area (with the mean change (economic sustainability, post vs. during) of 0.3), medium-sized companies prioritize social area (0.26), small and micro companies prioritize environmental area (0.29 and 0.41). However, comparing to pre-COVID-19 period, the post pandemic priorities are still social issues for companies of all sizes (the right clusters of Figure 3). But surprisingly, small companies (1.06) appeared to emphasize social sustainability the most, followed by medium-sized companies (1.03) and micro companies (0.97). Big companies appeared to place relatively less emphasis on social issues after the pandemic (0.95) as illustrated in Figure 4a. Hence, hypothesis 2 is proved to be false.

This result is contrary to previous study results which suggest that bigger companies are more socially responsible than smaller companies either because big companies have more resources which can be used for social issues or because large companies face more public social scrutiny, and therefore must be more responsive to social issues [24,34,52,53,54]. Maybe large companies were impacted so much by COVID-19 (97.5% of the big companies in the survey were negatively affected by the pandemic and the number for the whole sample is 96.8%) that they decided to withdraw from social responsibility.

Again, the economic dimension of SD remains essential for companies of all sizes, especially the medium and large companies (Figure 4b). This leaves the environmental side of SD to be the most vulnerable, another indication of post-pandemic environmental rebound effect.

4.5. Market Focus Analysis

Table 6 presents the score data based on the market focus (domestic, overseas, or mixtures of both) of the company. As noted earlier, the different types of company have different market focuses and there is a linkage (Table 2) between the two. The results in Table 6 suggest that for all types of market focus the companies have increased their concentration on the three dimensions of sustainability as the COVID-19 pandemic progressed. In line with the previous analyses, economic sustainability emerges as having the greatest emphasis once the pandemic ends (shaded cells in Table 6).

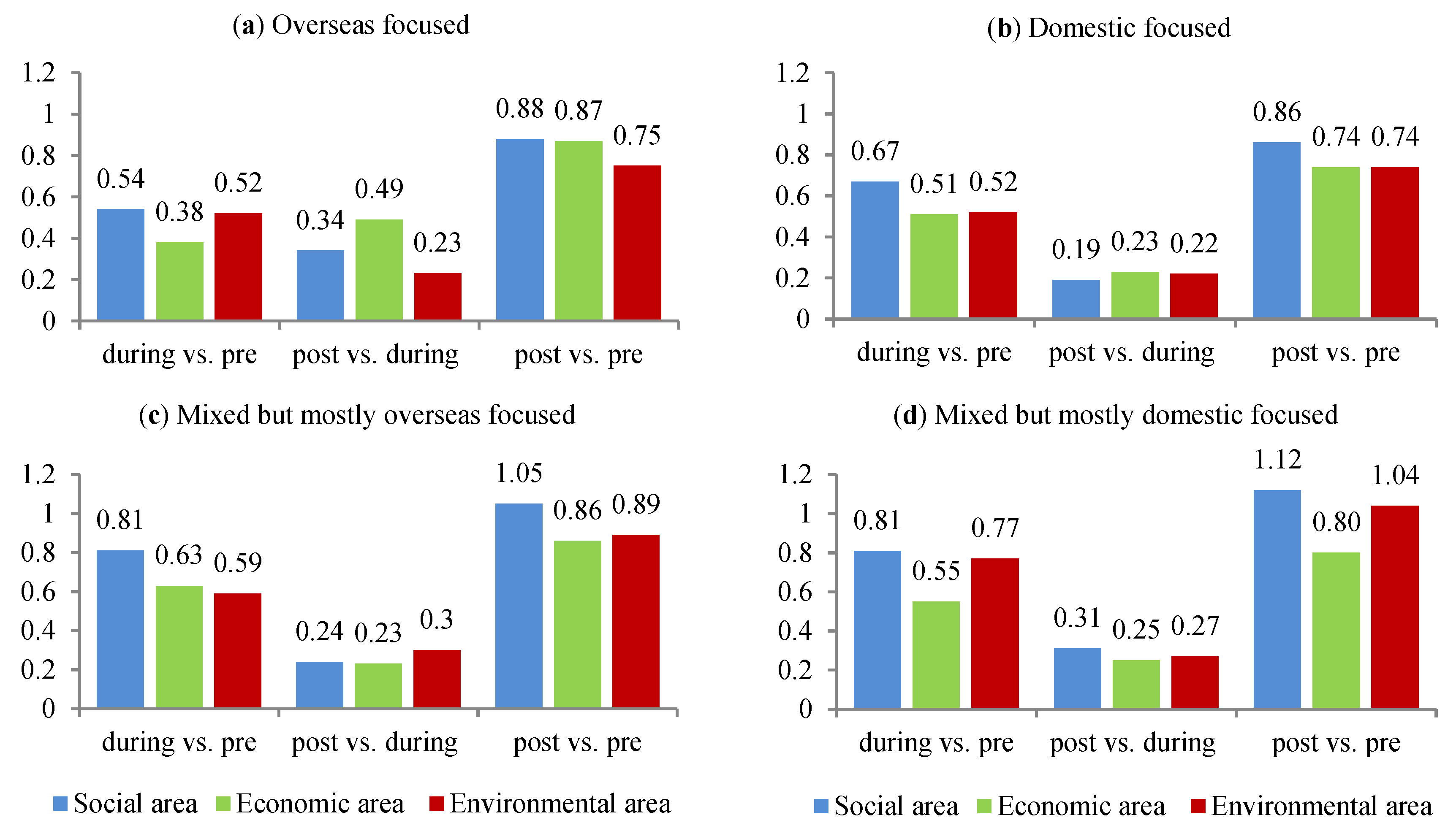

Figure 5 indicates that comparing to the pre-pandemic era, social sustainability has shown the largest change in priority during COVID-19 (the left clusters of Figure 5), especially for companies with mixed-market focuses (mean changes for both are 0.81), followed by domestic-focused companies (0.67) and overseas-focused companies (0.54). Comparing to the time during the pandemic, the post-pandemic priorities vary (the middle clusters of Figure 5), with economic sustainability being prioritized by overseas-focused (0.49) and domestic-focused (0.23) companies, and environmental sustainability being prioritized by companies with mixed but mostly overseas market-focused companies (0.30), and social sustainability being prioritized by overseas-focused companies (0.34). But the priority from pre- to post-pandemic is still social sustainability (the right clusters of Figure 5) with the lead being taken by the mixed but mostly domestic-focused companies (1.12), followed by mixed but mostly overseas-focused companies (1.05), solely overseas-focused companies (0.88), and then solely domestic-focused companies (0.86).

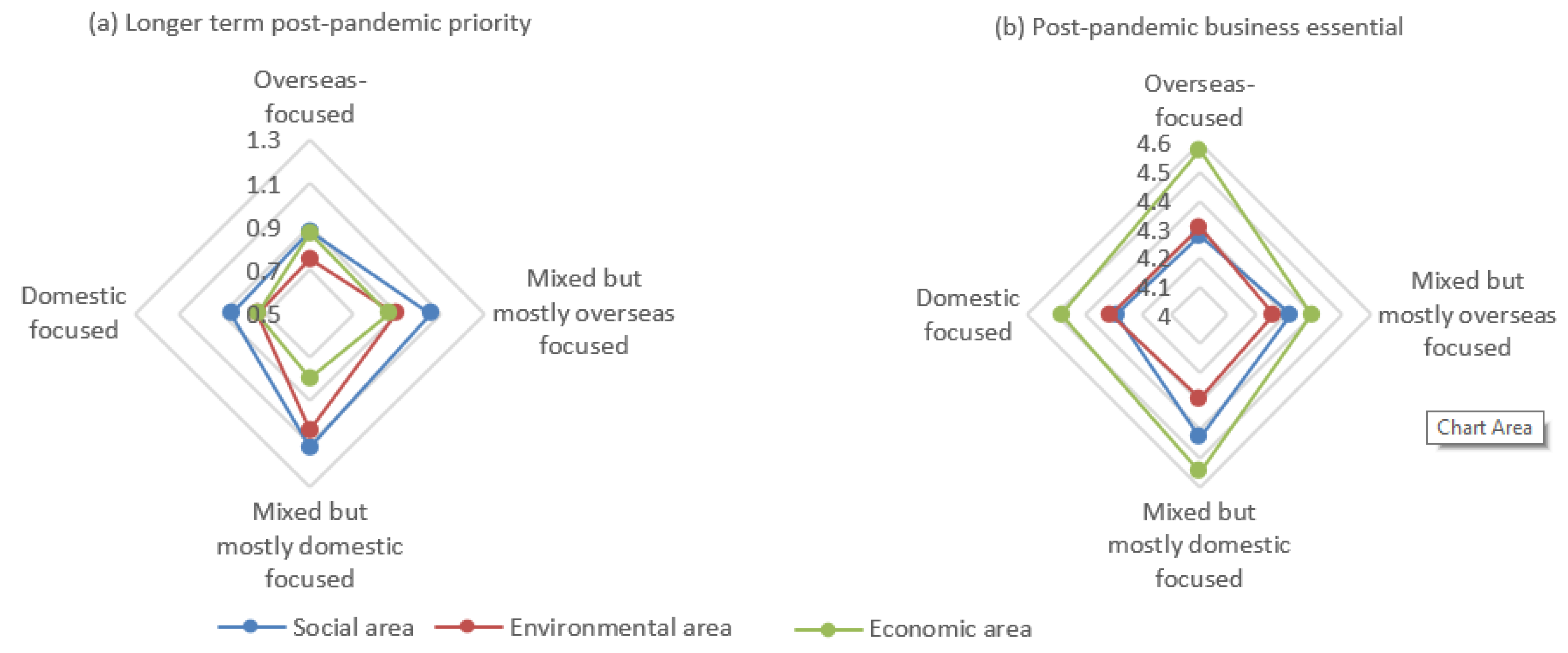

Therefore, the test of hypothesis 3 is passed. Indeed, possibly because of their better financial situation during the pandemic (38% of them were impacted badly while the number for the whole sample was 41%), companies with mixed markets prioritized social sustainability the most after the pandemic, followed by environmental sustainability. The levels of prioritization of mixed-market companies towards social and environmental sustainability are higher than companies that are solely overseas or domestic focused (Figure 6a). This finding may be explained by the slack resources theory [37] and available funds hypothesis [38]. However, all companies, regardless of their market focus, consider the economic dimension of sustainability as essential to their business. This is more obvious for overseas-focused companies and companies having a mixed market but more domestically-orientated (Figure 6b). Environmental sustainability is the least likely to receive attention during the pandemic and in the longer term following the pandemic.

5. Conclusions and Recommendations

In the research reported here the short and long-term impact of COVID-19 on sustainability are looked at from the perspective of 1160 business managers by investigating the changes of sustainability priorities during and post the pandemic, and three hypotheses have been tested. The results failed hypothesis 1 as social and environmental dimensions of sustainability are prioritized more by SOEs and private-owned companies and less by FIEs and individual-owned companies. The results also failed hypothesis 2 in that the larger the company, the more they appear to emphasize social and environmental sustainability. It was found that the social dimension of sustainability was prioritized the most by medium- and small-sized companies during COVID-19 and in the longer term after the pandemic, followed by the environmental dimension of sustainability. The largest companies, instead, appeared to show the least interest in social and environmental sustainability, and individually owned companies are in the middle of the range. However, hypothesis 3 is proved to be true as companies with mixed markets did prioritize social sustainability (the first) and environmental sustainability (the second) during the pandemic and in the longer term following the pandemic.

However, it does have to be noted that economic sustainability clearly stood out as having the highest status among three aspects of sustainability post-COVID-19 for all types, sizes, and market focus of business. This leaves environmental sustainability to be the relatively neglected dimension and confirms the possibility of a post pandemic environmental rebound effect that some suggest is already happening in China [55].

5.1. Managerial Implications

The above findings and discussion have implications for company managers. To avoid the post-pandemic environmental rebound effect, Chinese companies need to act now. It should be noted that while COVID-19 may not change the global picture with regard to sustainability, the results suggest that sustainability priorities of companies have changed. Additional measures are needed to counteract a possible rebound effect so as to ensure the environmental dimension of sustainable development is not neglected in favor of the social and economic dimensions. In addition, it is important to motivate and empower employees and other stakeholders to pursue sustainability goals and help them integrate these goals into their daily work routines, thus making sustainability everybody’s job rather than just the job of those who work in the sustainability department. This is especially important with the accelerating expansion of ICT and digitalization when company employees adapt to the ‘new normal’ way of working. Recent literature suggests that economic instruments like resources pricing or setting limits to resource use can be effective for this purpose [4]. Special attention should be paid to FIEs and Chinese individual-owned companies, companies larger in size and micro companies, and companies that sell products to only overseas markets or the domestic market.

Will China still be an important actor after COVID-19 in dealing with the issue of climate change? The answer is uncertain. Since government action and economic incentives post-pandemic would influence the global climate change path for decades [3], the opportunity to align long-term economic growth simultaneously with climate change objectives lies with the Chinese government and their decision-making in the coming months. The key is the balance of sustainability and resilience [45,46]. China’s quick economic recovery from COVID-19 has presented such an opportunity. To do this, China needs to further confirm its commitment to ‘new infrastructure’ building. Second, China should not let the pandemic delay the start of the carbon market and move forward with its national emissions trading system (ETS) which aims to limit and reduce CO2 emissions in a cost-effective manner. In addition, it is crucial for China to stop relying on coal and accelerate the growth of renewable power. Furthermore, although the planned EU-China summit this autumn is postponed, China should see it as a new opportunity for both parties to cooperate on building a greener global economy by aligning their recoveries with the principles of a green transition and bringing other countries along with them.

5.2. Theoretical Implications

This paper contributes to the scientific literature of the impact of COVID-19 by adding an empirical investigation of the sustainability priority change as the result of the pandemic in China. It also provides an empirical evidence of the possible rebound effect after the pandemic. Second, views of Chinese business owners and managers were considered in the research; this would help shed light on the business response to COVID-19. In addition, the predicted post-pandemic situation was assessed, which, given the high uncertainty of the possible impact of COVID-19 on the environment, provides an ‘ex-post’ perspective regarding the post-pandemic recovery worldwide.

5.3. Limitations and Future Research

The findings set out in the paper are subject to some limitations. First, only the views of business owners and managers were considered. Although it can be argued that these people are likely to have knowledge and be able to influence company sustainability policies to a greater extent than other employees, future research should garner the views of employee’s as no sustainability policy can be implemented without their engagement. Second, this research was conducted in China, where there has not been a second or third wave of the pandemic and where people’s lives have returned to being close to those they had before the pandemic. As all the respondents in the survey reside in China, they might not have experienced the consequences of the pandemic as much as people would have done in countries where the pandemic has lasted for much longer. This might influence the respondents’ prediction of the post-pandemic sustainability priority, and indeed may be reflected in the relatively small deviations between some of the pre- and post-COVID-19 SD figures. Hence the results of this research might not be readily generalizable to countries that have been hit harder and longer by COVID-19. Nonetheless, it does shed light on the post-pandemic situation for countries/regions with a similar COVID-19 experience. In addition, this research did not involve a detailed investigation regarding the mechanism of the impact (direct and/or indirect) of the changes noted by respondents and future research could look at this for specific areas such as an increased use of ICT due to COVID-19. However, it is important to note that differences in cultural background (as indicated by Muller and Voigt [22]) and the COVID-19 experience should be considered in this kind of study.

Author Contributions

Conceptualization, D.Z.; data curation, M.H.; formal analysis, D.Z.; funding acquisition, D.Z.; investigation, D.Z.; methodology, D.Z.; project administration, D.Z.; supervision, D.Z.; writing—original draft, D.Z.; writing—review and editing, D.Z. and S.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Department of Science and Technology of Henan Province, grant number: 202400410096.

Acknowledgments

The authors would like to thank everyone who offered help during the questionnaire survey.

Conflicts of Interest

The authors declare no conflict of interest.

References

- World Health Organization (WHO). WHO Coronavirus Disease (COVID-19) Dashboard. Available online: https://covid19.who.int/?gclid=EAIaIQobChMIzqaup7iF6wIVibPtCh0s7AzuEAAYASAAEgLJ2fD_BwE (accessed on 2 November 2020).

- Zambrano-Monserrate, M.A.; Ruano, M.A.; Sanchez-Alcalde, L. Indirect effects of COVID-19 on the environment. Sci. Total Environ. 2020, 728, 138813. [Google Scholar] [CrossRef] [PubMed]

- Le Quéré, C.; Jackson, R.B.; Jones, M.W.; Smith, A.J.P.; Abernethy, S.; Andrew, R.M.; De-Gol, A.J.; Willis, D.R.; Shan, Y.; Canadell, J.G.; et al. Temporary reduction in daily global CO2 emissions during the COVID-19 forced confinement. Nat. Clim. Chang. 2020, 10, 647–653. [Google Scholar] [CrossRef]

- Freire-González, J.; Vivanco, D.F. Pandemics and the Environmental Rebound Effect: Reflections from COVID-19. Environ. Resour. Econ. 2020, 76, 447–517. [Google Scholar] [CrossRef]

- McCloskey, B.; Heymann, D.L. SARS to novel coronavirus—Old lessons and new lessons. Epidemiol. Infect. 2020, 148, e22. [Google Scholar] [CrossRef] [Green Version]

- Huang, W.; Morawska, L. Face masks could raise pollution risks. Nature 2019, 574, 29–30. [Google Scholar] [CrossRef]

- Barreiro-Gen, M.; Lozano, R.; Zafar, A. Changes in Sustainability Priorities in Organisations due to the COVID-19 Outbreak: Averting Environmental Rebound Effects on Society. Sustainability 2020, 12, 5031. [Google Scholar] [CrossRef]

- McKinsey. COVID-19: Implications for Business. Available online: https://www.mckinsey.com/business-functions/risk/our-insights/covid-19-implications-for-business (accessed on 2 November 2020).

- Institute for Global Environmental Strategies (IGES). Implications of COVID-19 for the Environment and Sustainability. Available online: https://www.iges.or.jp/en/news/20200514 (accessed on 2 November 2020).

- European Commission. Europe’s Moment: Repair and Prepare for the Next Generation. Available online: https://ec.europa.eu/commission/presscorner/detail/en/ip_20_940 (accessed on 2 November 2020).

- European Council. A Recovery Plan for Europe. Available online: https://www.consilium.europa.eu/en/policies/eu-recovery-plan/ (accessed on 2 November 2020).

- International Energy Agency (IEA). Sustainable Recovery. Available online: https://www.iea.org/reports/sustainable-recovery (accessed on 2 November 2020).

- Bloomberg. South Korea’s $35 Billion Green Plan Skirts Zero-Carbon Target. Available online: https://www.bloomberg.com/news/articles/2020-07-14/green-new-deal-in-south-korea-stops-short-of-zero-carbon-target (accessed on 2 November 2020).

- World Bank (WB). Costa Rica Receives World Bank Support for Economic Recovery and Promoting Low-Carbon Development. Available online: https://www.worldbank.org/en/news/press-release/2020/06/25/apoyo-del-banco-mundial-a-costa-rica-para-promover-la-recuperacion-economica-y-un-desarrollo-bajo-en-carbono (accessed on 2 November 2020).

- International Monetary Fund (IMF). Greening the Recovery. Available online: https://www.imf.org/en/Topics/climate-change/green-recovery (accessed on 2 November 2020).

- Xinhua. Xi Focus: Xi Announces China Aims to Achieve Carbon Neutrality before 2060. Available online: http://www.xinhuanet.com/english/2020-09/23/c_139388764.htm (accessed on 2 November 2020).

- Financial Time (FT). China Pledges to Be ‘Carbon-Neutral’ by 2060. Available online: https://www.ft.com/content/730e4f7d-3df0-45e4-91a5-db4b3571f353 (accessed on 2 November 2020).

- National Bureau of Statistics of China (NBSC). Coordinative Efforts for Epidemic Control and Economic Development Delivered Notable Results with National Economic Recovered Gradually in the First Half of 2020. Available online: http://www.stats.gov.cn/english/PressRelease/202007/t20200716_1776211.html (accessed on 2 November 2020).

- United Nations (UN). No Excuse Not to Meet Net-Zero Emission Target by 2050, Secretary-General Says in Global Lecture on Climate Change, Stressing Time for Small Steps Has Passed. Available online: https://www.un.org/press/en/2020/sgsm20183.doc.htm (accessed on 2 November 2020).

- Vivanco, D.F.; McDowall, W.; Freire-González, J.; Kemp, R.; Van Der Voet, E. The foundations of the environmental rebound effect and its contribution towards a general framework. Ecol. Econ. 2016, 125, 60–69. [Google Scholar] [CrossRef]

- Gossart, C. Rebound effects and ICT: A review of the literature. In ICT Innovations for Sustainability; Hilty, L.M., Aebischer, B., Eds.; Advances in Intelligent Systems and Computing; Springer: Cham, Switzerland, 2015; Volume 310, pp. 435–448. [Google Scholar] [CrossRef] [Green Version]

- Müller, J.M.; Voigt, K.-I. Sustainable Industrial Value Creation in SMEs: A Comparison between Industry 4.0 and Made in China 2025. Int. J. Precis. Eng. Manuf. Green Technol. 2018, 5, 659–670. [Google Scholar] [CrossRef] [Green Version]

- Kuo, C.-C.; Shyu, J.Z.; Ding, K. Industrial revitalization via industry 4.0—A comparative policy analysis among China, Germany and the USA. Glob. Transit. 2019, 1, 3–14. [Google Scholar] [CrossRef]

- Zhang, D.; Morse, S.; Kambhampati, U. Sustainable Development and Corporate Social Responsibility, 1st ed.; Routledge: New York, NY, USA, 2018; p. 241. [Google Scholar]

- Li, Y.; Cheng, H.; Beeton, R.J.S.; Sigler, T.; Halog, A. Sustainability from a Chinese cultural perspective: The implications of harmonious development in environmental management. Environ. Dev. Sustain. 2016, 18, 679–696. [Google Scholar] [CrossRef]

- Peng, M.W. Institutional transitions and strategic choices. Acad. Manag. Rev. 2003, 28, 275–296. [Google Scholar] [CrossRef] [Green Version]

- Li, W.; Zhang, R. Corporate Social Responsibility, Ownership Structure, and Political Interference: Evidence from China. J. Bus. Ethics 2010, 96, 631–645. [Google Scholar] [CrossRef]

- Zhang, D.; Morse, S.; Kambhampati, U.; Li, B. Evolving Corporate Social Responsibility in China. Sustainability 2014, 6, 7646–7665. [Google Scholar] [CrossRef] [Green Version]

- Oh, W.Y.; Chang, Y.K.; Martynov, A. The Effect of Ownership Structure on Corporate Social Responsibility: Empirical Evidence from Korea. J. Bus. Ethics 2011, 104, 283–297. [Google Scholar] [CrossRef]

- Lee, J.; Kim, S.-J.; Kwon, I. Corporate Social Responsibility as a Strategic Means to Attract Foreign Investment: Evidence from Korea. Sustainability 2017, 9, 2121. [Google Scholar] [CrossRef] [Green Version]

- Fry, F.L.; Hock, R.J. Who claims corporate responsibility? The biggest and the worst. Bus. Soc. Rev. 1976, 18, 62–65. [Google Scholar]

- Fombrun, C.; Shanley, M. What’s in a name? Reputation, building and corporate strategy. Acad. Manag. J. 1990, 33, 233–258. [Google Scholar]

- Pava, M.L.; Krausz, J. The association between corporate social-responsibility and financial performance: The paradox of social cost. J. Bus. Ethics 1996, 15, 321–357. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate Social Responsibility: A Theory of the Firm Perspective. Acad. Manag. Rev. 2001, 26, 117. [Google Scholar] [CrossRef]

- Elsayed, K. Reexamining the Expected Effect of Available Resources and Firm Size on Firm Environmental Orientation: An Empirical Study of UK Firms. J. Bus. Ethics 2006, 65, 297–308. [Google Scholar] [CrossRef]

- Muller, A.; Kolk, A. Extrinsic and Intrinsic Drivers of Corporate Social Performance: Evidence from Foreign and Domestic Firms in Mexico. J. Manag. Stud. 2010, 47, 1–26. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance—Financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Preston, L.E.; O’Bannon, D.P. The corporate social-financial performance relationship: A typology and analysis. Bus. Soc. 1997, 36, 419–429. [Google Scholar] [CrossRef]

- Sun, J.; Zhuang, Z.; Zheng, J.; Li, K.; Wong, R.L.-Y.; Liu, D.; Huang, J.; He, J.; Zhu, A.; Zhao, J.; et al. Generation of a Broadly Useful Model for COVID-19 Pathogenesis, Vaccination, and Treatment. Cell 2020, 182, 734–743. [Google Scholar] [CrossRef]

- Wiersinga, W.J.; Rhodes, A.; Cheng, A.C.; Peacock, S.J.; Prescott, H.C. Pathophysiology, Transmission, Diagnosis, and Treatment of Coronavirus Disease 2019 (COVID-19): A Review. JAMA 2020, 324, 782–793. [Google Scholar] [CrossRef]

- Zhai, P.; Ding, Y.; Wu, X.; Long, J.; Zhong, Y.; Li, Y. The epidemiology, diagnosis and treatment of COVID-19. Int. J. Antimicrob. Agents 2020, 55, 105955. [Google Scholar] [CrossRef]

- Wang, Q.; Su, M. A preliminary assessment of the impact of COVID-19 on environment—A case study of China. Sci. Total Environ. 2020, 728, 138915. [Google Scholar] [CrossRef]

- Bao, R.; Zhang, A. Does lockdown reduce air pollution? Evidence from 44 cities in northern China. Sci. Total Environ. 2020, 731, 139052. [Google Scholar] [CrossRef]

- Bartik, A.W.; Bertrand, M.; Cullen, Z.; Glaeser, E.L.; Luca, M.; Stanton, C. The impact of COVID-19 on small business outcomes and expectations. Proc. Natl. Acad. Sci. USA 2020, 117, 17656–17666. [Google Scholar] [CrossRef]

- Zabaniotou, A. A systemic approach to resilience and ecological sustainability during the COVID-19 pandemic: Human, societal, and ecological health as a system-wide emergent property in the Anthropocene. Glob. Transit. 2020, 2, 116–126. [Google Scholar] [CrossRef]

- D’Adamo, I.; Rosa, P. How Do You See Infrastructure? Green Energy to Provide Economic Growth after COVID-19. Sustainability 2020, 12, 4738. [Google Scholar] [CrossRef]

- China State Council. The Labour Law of the People’s Republic of China (2016). Available online: https://www.chashebao.com/shebaotiaoli/16340.html (accessed on 2 November 2020).

- Center for Strategic and International Studies (CSIS). Chinese Philanthropists Rush to Respond to COVID-19. Available online: https://www.csis.org/blogs/trustee-china-hand/chinese-philanthropists-rush-respond-covid-19 (accessed on 2 November 2020).

- Lin, K.J.; Lu, X.; Zhang, J.; Zheng, Y. State-owned enterprises in China: A review of 40 years of research and practice. China J. Account. Res. 2020, 13, 31–55. [Google Scholar] [CrossRef]

- Su, J.; He, J. Does Giving Lead to Getting? Evidence from Chinese Private Enterprises. J. Bus. Ethics 2010, 93, 73–90. [Google Scholar] [CrossRef]

- Ministry of Commerce of the People’s Republic of China (MOC). Summary of the Direct Investment by Some Foreign Countries/Regions by the End of 2018. Available online: http://www.mofcom.gov.cn/article/tongjiziliao/v/ (accessed on 3 December 2020).

- Henriques, I.; Sadorsky, P. The Determinants of an Environmentally Responsive Firm: An Empirical Approach. J. Environ. Econ. Manag. 1996, 30, 381–395. [Google Scholar] [CrossRef]

- Russo, M.V.; Fouts, P.A. A resource-based perspective on corporate environmental performance and profitability. Acad. Manag. J. 1997, 40, 534–559. [Google Scholar]

- Lepoutre, J.; Heene, A. Investigating the Impact of Firm Size on Small Business Social Responsibility: A Critical Review. J. Bus. Ethics 2006, 67, 257–273. [Google Scholar] [CrossRef]

- Centre for Research on Energy and Clean Air (CREA). China’s Air Pollution Overshoots Pre-Crisis Levels for the First Time. Available online: https://energyandcleanair.org/wp/wp-content/uploads/2020/05/China-air-pollution-rebound-final.pdf (accessed on 2 November 2020).

Figure 1.

Mean change of the importance of each area of sustainable development at different stages of COVID-19 for companies with different ownership.

Figure 1.

Mean change of the importance of each area of sustainable development at different stages of COVID-19 for companies with different ownership.

Figure 2.

Longer term post-pandemic priority and post-pandemic business essential for companies with different ownership.

Figure 2.

Longer term post-pandemic priority and post-pandemic business essential for companies with different ownership.

Figure 3.

Mean change of each area of sustainable development for different sizes.

Figure 4.

Longer term post-pandemic priority and post-pandemic business essential for companies with different size

Figure 4.

Longer term post-pandemic priority and post-pandemic business essential for companies with different size

Figure 5.

Mean change of each area of sustainable development for companies with different product markets.

Figure 5.

Mean change of each area of sustainable development for companies with different product markets.

Figure 6.

Longer term post-pandemic priority and post-pandemic business essential for companies with different market focus.

Figure 6.

Longer term post-pandemic priority and post-pandemic business essential for companies with different market focus.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Profile of the companies who respondent to the online survey.

| (a) Ownership, size, age, and market focus | ||||||||||

| Ownership of the company | Domestic private-owned company | State-owned enterprise (SOE) | Foreign invested company (FIE) | Domestic individual-owned company | ||||||

| 818 (70.5%) | 195 (16.8%) | 76 (6.5%) | 71 (6.1%) | |||||||

| Company size a (number of employees or persons) | 1000 and above | 300–999 | 20–299 | 1–19 | ||||||

| 157 (13.5%) | 292 (25.2%) | 588 (50.7%) | 123 (10.6%) | |||||||

| Age of the company (year) | Less than 4 years | 4–10 (inc. 10) | 11–20 (inc. 20) | Longer than 20 years | ||||||

| 119 (10.3%) | 554 (47.8%) | 262 (22.6%) | 225 (19.4%) | |||||||

| Market focus of the company | Overseas-focused | Domestic-focused | Mixed but mostly domestic-focused | Mixed but mostly export-focused | ||||||

| 65 (5.6%) | 201 (17.3%) | 380 (32.8%) | 514 (44.3%) | |||||||

| (b) Regional distribution (32 regions) | ||||||||||

| Beijing | Shanghai | Zhejiang | Jiangsu | Hebei | Guangdong | Henan | Sichuan | Hubei | Fujian | others |

| 241 (20.8%) | 155 (13.4%) | 84 (7.2%) | 79 (6.8%) | 76 (6.5%) | 70 (6.0%) | 68 (5.9%) | 55 (4.7%) | 53 (4.6%) | 37 (3.2%) | 240 (20.8%) |

| (c) Industry distribution (30 industries) | ||||||||||

| IT/e-commerce/ internet service | Manufacturing | Wholesale/ retail | Fast moving consumer goods | Education/ training/ research | Clothing/ textile/ leather | Catering/ entertainment/ tourism | Real estate/ construction | Communication/ network equipment/value-added service | Others | |

| 256 (22.1%) | 159 (13.7%) | 89 (7.7%) | 80 (6.9%) | 79 (6.8%) | 57 (4.9%) | 53 (4.6%) | 52 (4.5%) | 32 (2.8%) | 304 (26.1%) | |

Note: The number of surveyed companies was 1160 and the figures are the number of companies that fall into that category (based upon answers provided by respondents) along with the percentage of the sample. a Company size is classified based on the official government document Notice of Issuing the Classification Criterion for SMEs (Ministry of Industry and Enterprises (2011) No. 300).

Table 2.

Crosstab and Chi-square test between company ownership and their characterization, general impact, and current business resumption.

Table 2.

Crosstab and Chi-square test between company ownership and their characterization, general impact, and current business resumption.

| Characterization /Impact/Resumption | Categories | Ownership Top Figures: Observed (Expected) Counts Bottom Figures: % within Column | Total | Chi-Square Tests | |||

|---|---|---|---|---|---|---|---|

| SOE | Private-Owned | FIE | Individual-Owned | ||||

| Size (No. of employees) | 1–19 | 3 (20.7) 1.5 | 70 (86.7) 8.6 | 2 (8.1) 2.6 | 48 (7.5) 67.6 | 123 10.6 | Pearson Chi-Square: 414.779 df: 9 Sig. (2-sided): 0.000 *** Note: 0 cells have expected count less than 5. The minimum expected count is 7.53 |

| 20–299 | 53 (98.8) 27.2 | 494 (414.6) 60.4 | 23 (38.5) 30.3 | 18 (36.0) 25.4 | 588 50.7 | ||

| 300–999 | 79 (49.1) 40.5 | 184 (205.9) 22.5 | 25 (19.1) 32.9 | 4 (17.9) 5.6 | 292 25.2 | ||

| 1000 and above | 60 (26.4) 30.8 | 70 (110.7) 8.6 | 26 (10.3) 34.2 | 1 (9.6) 1.4 | 157 13.5 | ||

| Age (No. of years established) | Less than 4 | 5 (20.0) 2.6 | 88 (83.9) 10.8 | 2 (7.8) 2.6 | 24 (7.3) 33.8 | 119 10.3 | Pearson Chi-Square: 239.951 df: 9 Sig. (2-sided): 0.000 *** Note: 0 cells have expected count less than 5. The minimum expected count is 7.28. |

| 4–10 | 40 (93.1) 20.5 | 448 (390.7) 54.8 | 25 (36.3) 32.9 | 41 (33.9) 57.7 | 554 47.8 | ||

| 11–20 | 53 (44.0) 27.2 | 178 (184.8) 21.8 | 26 (17.2) 34.2 | 5 (16) 7.0 | 262 22.6 | ||

| Above 20 | 97 (37.8) 49.7 | 104 (158.7) 12.7 | 23 (14.7) 30.3 | 1 (13.8) 1.4 | 225 19.4 | ||

| Market focus | Overseas-focused | 10 (10.9) 5.1 | 44 (45.8) 5.4 | 5 (4.3) 6.6 | 6 (4.0) 8.5 | 65 5.6 | Pearson Chi-Square: 58.235 df: 9 Sig. (2-sided): 0.000 *** Note: 2 cells (12.5%) have expected count less than 5. The minimum expected count is 3.98. |

| Mixed but mostly overseas focused | 91 (86.4) 46.7 | 352 (362.5) 43.0 | 50 (33.7) 65.8 | 21 (31.5) 29.6 | 514 44.3 | ||

| Mixed but mostly domestic focused | 74 (63.9) 37.9 | 276 (268.0) 33.7 | 16 (24.9) 21.1 | 14 (23.3) 19.7 | 380 32.8 | ||

| Domestic focused | 20 (33.8) 10.3 | 146 (141.7) 17.8 | 5 (13.2) 6.6 | 30 (12.3) 42.3 | 201 17.3 | ||

| General impact from COVID-19 | No | 12 (6.2) 6.2 | 19 (26.1) 2.3 | 2 (2.4) 2.6 | 4 (2.3) 5.6 | 37 3.2 | Pearson Chi-Square: 30.360 df: 6 Sig. (2-sided): 0.000 *** Note: 2 cells (16.7%) have expected count less than 5. The minimum expected count is 2.26. |

| Yes, minor | 127 (108.9) 65.1 | 443 (457.0) 54.2 | 50 (42.5) 65.8 | 28 (39.7) 39.4 | 648 55.9 | ||

| Yes, major | 56 (79.8) 28.7 | 356 (335.0) 43.5 | 24 (31.1) 31.6 | 39 (29.1) 54.9 | 475 40.9 | ||

| Business resumption (% of full production capacity) after COVID-19 | 25% and less | 4 (7.6) 2.1 | 33 (31.7) 4.0 | 1 (2.9) 1.3 | 7 (2.8) 9.9 | 45 3.9 | Pearson Chi-Square: 27.024 df: 9 Sig. (2-sided): 0.001 *** Note: 2 cells (12.5%) have expected count less than 5. The minimum expected count is 2.75. |

| 26–50% | 30 (31.9) 15.4 | 125 (134.0) 15.3 | 15 (12.4) 19.7 | 20 (11.6) 28.2 | 190 16.4 | ||

| 51–75% | 91 (91.1) 46.7 | 379 (382.2) 46.3 | 37 (35.5) 48.7 | 35 (33.2) 49.3 | 542 46.7 | ||

| Above 75% | 70 (64.4) 35.9 | 281 (270.1) 34.4 | 23 (25.1) 30.3 | 9 (23.4) 12.7 | 383 33.0 | ||

Note: N = 1160, ***: statistically significant at p < 0.01.

Table 3.

Welch’s ANOVA test of sustainability priority change for Chinese companies.

| Ownership | Dimension of Sustainability | Stage of COVID-19 | N | Mean Score | Sig. |

|---|---|---|---|---|---|

| SOE | Social sustainability | Before | 195 | 3.38 | 0.000 *** |

| During | 195 | 4.16 | |||

| Post | 195 | 4.44 | |||

| Economic sustainability | Before | 195 | 3.65 | 0.000 *** | |

| During | 195 | 4.16 | |||

| Post | 195 | 4.47 | |||

| Environmental sustainability | Before | 195 | 3.33 | 0.000 *** | |

| During | 195 | 3.99 | |||

| Post | 195 | 4.24 | |||

| Domestic private-owned company | Social sustainability | Before | 818 | 3.30 | 0.000 *** |

| During | 818 | 4.09 | |||

| Post | 818 | 4.34 | |||

| Economic sustainability | Before | 818 | 3.63 | 0.000 *** | |

| During | 818 | 4.25 | |||

| Post | 818 | 4.48 | |||

| Environmental sustainability | Before | 818 | 3.39 | 0.000 *** | |

| During | 818 | 4.02 | |||

| Post | 818 | 4.30 | |||

| FIE | Social sustainability | Before | 76 | 3.38 | 0.000 *** |

| During | 76 | 4.04 | |||

| Post | 76 | 4.26 | |||

| Economic sustainability | Before | 76 | 3.87 | 0.001 *** | |

| During | 76 | 4.13 | |||

| Post | 76 | 4.46 | |||

| Environmental sustainability | Before | 76 | 3.46 | 0.000 *** | |

| During | 76 | 4.01 | |||

| Post | 76 | 4.24 | |||

| Domestic individual-owned company | Social sustainability | Before | 71 | 3.30 | 0.000 *** |

| During | 71 | 3.94 | |||

| Post | 71 | 4.28 | |||

| Economic sustainability | Before | 71 | 3.56 | 0.000 *** | |

| During | 71 | 4.11 | |||

| Post | 71 | 4.41 | |||

| Environmental sustainability | Before | 71 | 3.37 | 0.000 *** | |

| During | 71 | 3.90 | |||

| Post | 71 | 4.32 |

Note: ***: statistically significant at p < 0.01, the shaded cells are the highest mean scores in the post-COVID-19 stage.

Table 4.

Welch’s ANOVA test of differences among dimensions of sustainability for each COVID-19 stage.

Table 4.

Welch’s ANOVA test of differences among dimensions of sustainability for each COVID-19 stage.

| Ownership | Stage of COVID-19 | Dimension of Sustainability | N | Mean Score | Sig. |

|---|---|---|---|---|---|

| SOE | Before | Social | 195 | 3.38 | 0.000 *** |

| Economic | 195 | 3.65 | |||

| Environmental | 195 | 3.33 | |||

| During | Social | 195 | 4.16 | 0.642 | |

| Economic | 195 | 4.16 | |||

| Environmental | 195 | 3.99 | |||

| Post | Social | 195 | 4.44 | 0.000 *** | |

| Economic | 195 | 4.47 | |||

| Environmental | 195 | 4.24 | |||

| Domestic private owned company | Before | Social | 818 | 3.30 | 0.000 *** |

| Economic | 818 | 3.63 | |||

| Environmental | 818 | 3.39 | |||

| During | Social | 818 | 4.09 | 0.000 *** | |

| Economic | 818 | 4.25 | |||

| Environmental | 818 | 4.02 | |||

| Post | Social | 818 | 4.34 | 0.000 *** | |

| Economic | 818 | 4.48 | |||

| Environmental | 818 | 4.30 | |||

| Foreign invested enterprise | Before | Social | 76 | 3.38 | 0.016 ** |

| Economic | 76 | 3.87 | |||

| Environmental | 76 | 3.46 | |||

| During | Social | 76 | 4.04 | 0.734 | |

| Economic | 76 | 4.13 | |||

| Environmental | 76 | 4.01 | |||

| Post | Social | 76 | 4.26 | 0.236 | |

| Economic | 76 | 4.46 | |||

| Environmental | 76 | 4.24 | |||

| Domestic individual owned company | Before | Social | 71 | 3.30 | 0.344 |

| Economic | 71 | 3.56 | |||

| Environmental | 71 | 3.37 | |||

| During | Social | 71 | 3.94 | 0.459 | |

| Economic | 71 | 4.11 | |||

| Environmental | 71 | 3.90 | |||

| Post | Social | 71 | 4.28 | 0.709 | |

| Economic | 71 | 4.41 | |||

| Environmental | 71 | 4.32 |

Note: ***: statistically significant at p < 0.01, **: statistically significant at p < 0.05, the shaded cells are the highest mean scores in the post-COVID-19 stage.

Table 5.

Welch’s ANOVA test of priority change for companies with different sizes.

| Size of Company | Sustainability | COVID-19 Stage | N | Mean | Sig. |

|---|---|---|---|---|---|

| Large | Social sustainability | Before | 157 | 3.50 | 0.000 *** |

| During | 157 | 4.18 | |||

| Post | 157 | 4.45 | |||

| Economic sustainability | Before | 157 | 3.67 | 0.000 *** | |

| During | 157 | 4.20 | |||

| Post | 157 | 4.50 | |||

| Environmental sustainability | Before | 157 | 3.29 | 0.000 *** | |

| During | 157 | 3.95 | |||

| Post | 157 | 4.21 | |||

| medium | Social sustainability | Before | 292 | 3.35 | 0.000 *** |

| During | 292 | 4.12 | |||

| Post | 292 | 4.38 | |||

| Economic sustainability | Before | 292 | 3.68 | 0.000 *** | |

| During | 292 | 4.28 | |||

| Post | 292 | 4.53 | |||

| Environmental sustainability | Before | 292 | 3.40 | 0.000 *** | |

| During | 292 | 4.09 | |||

| Post | 292 | 4.30 | |||

| Small | Social sustainability | Before | 589 | 3.26 | 0.000 *** |

| During | 589 | 4.08 | |||

| Post | 589 | 4.32 | |||

| Economic sustainability | Before | 589 | 3.65 | 0.000 *** | |

| During | 589 | 4.20 | |||

| Post | 589 | 4.46 | |||

| Environmental sustainability | Before | 589 | 3.40 | 0.000 *** | |

| During | 589 | 4.01 | |||

| Post | 589 | 4.30 | |||

| Micro | Social sustainability | Before | 123 | 3.29 | 0.000 *** |

| During | 123 | 3.94 | |||

| Post | 123 | 4.26 | |||

| Economic sustainability | Before | 123 | 3.51 | 0.000 *** | |

| During | 123 | 4.16 | |||

| Post | 123 | 4.33 | |||

| Environmental sustainability | Before | 123 | 3.34 | 0.000 *** | |

| During | 123 | 3.84 | |||

| Post | 123 | 4.25 |

Note: ***: statistically significant at p < 0.01, shade cells are the highest mean scores of companies of all sizes in the post-COVID-19 stage.

Table 6.

Welch’s ANOVA test of priority change for companies with different market focus.

| Market Orientation | Dimensions of Sustainability | COVID-19 Stages | N | Mean | Sig. |

|---|---|---|---|---|---|

| Overseas focused | Social sustainability | Before | 65 | 3.40 | 0.000 *** |

| During | 65 | 3.94 | |||

| Post | 65 | 4.28 | |||

| Economic sustainability | Before | 65 | 3.71 | 0.000 *** | |

| During | 65 | 4.09 | |||

| Post | 65 | 4.58 | |||

| Environmental sustainability | Before | 65 | 3.57 | 0.000 *** | |

| During | 65 | 4.09 | |||

| Post | 65 | 4.32 | |||

| Domestic orientated | Social sustainability | Before | 201 | 3.43 | 0.000 *** |

| During | 201 | 4.10 | |||

| Post | 201 | 4.29 | |||

| Economic sustainability | Before | 201 | 3.74 | 0.000 *** | |

| During | 201 | 4.25 | |||

| Post | 201 | 4.48 | |||

| Environmental sustainability | Before | 201 | 3.57 | 0.000 *** | |

| During | 201 | 4.09 | |||

| Post | 201 | 4.31 | |||

| Mixed but mostly overseas focused | Social sustainability | Before | 514 | 3.27 | 0.000 *** |

| During | 514 | 4.08 | |||

| Post | 514 | 4.32 | |||

| Economic sustainability | Before | 514 | 3.53 | 0.000 *** | |

| During | 514 | 4.16 | |||

| Post | 514 | 4.39 | |||

| Environmental sustainability | Before | 514 | 3.37 | 0.000 *** | |

| During | 514 | 3.96 | |||

| Post | 514 | 4.26 | |||

| Mixed but mostly domestic orientated | Social sustainability | Before | 381 | 3.31 | 0.000 *** |

| During | 381 | 4.12 | |||

| Post | 381 | 4.43 | |||

| Economic sustainability | Before | 381 | 3.75 | 0.000 *** | |