Paving towards Strategic Investment Decision: A SWOT Analysis of Renewable Energy in Bangladesh

,

,

,

,  , and

, and

Abstract

:1. Introduction

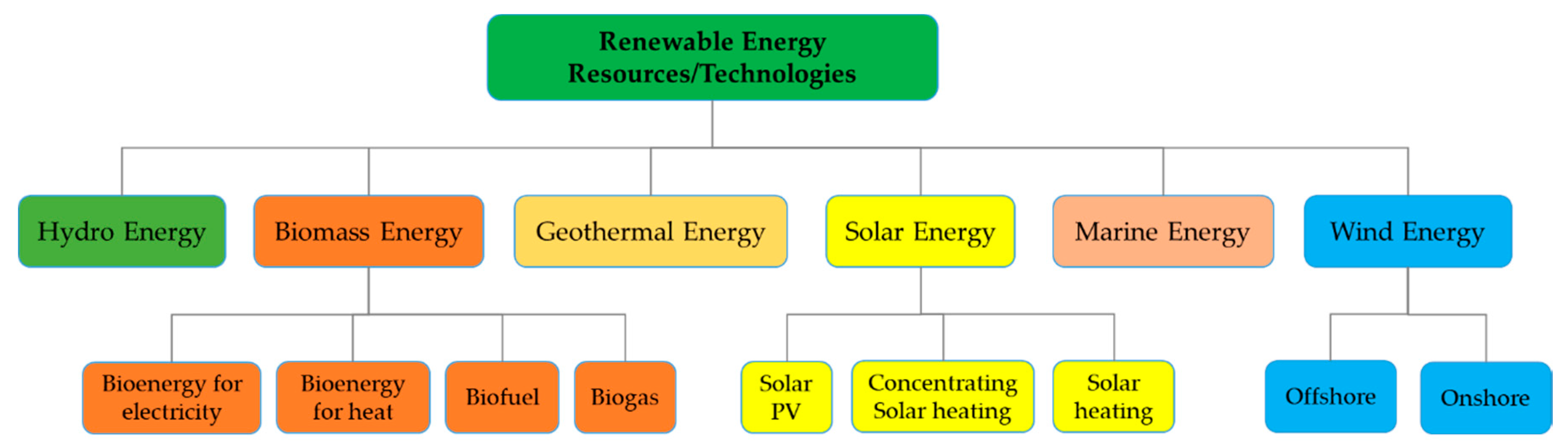

2. Outlook of the Renewable Energy Sector in Bangladesh

2.1. Biomass

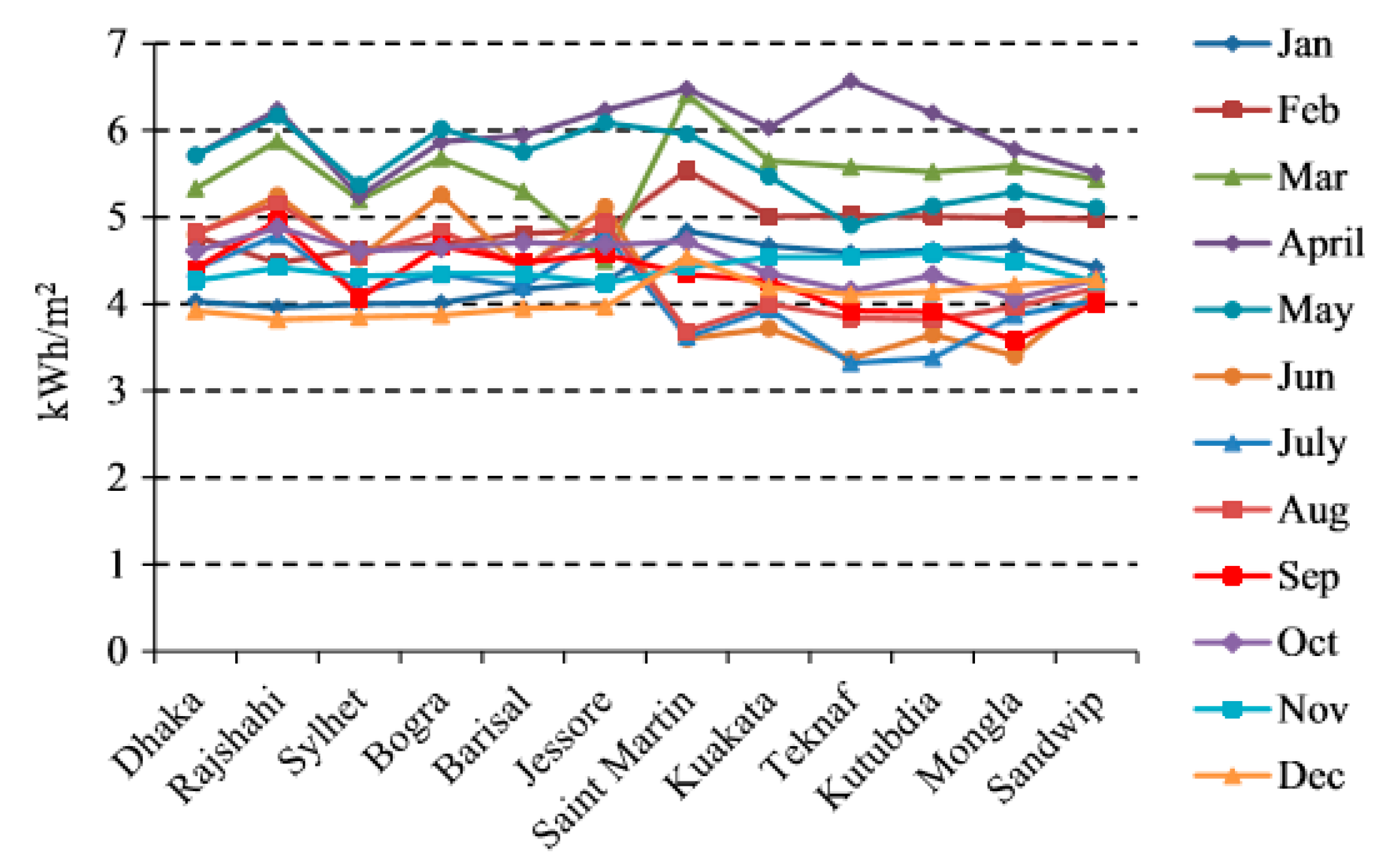

2.2. Solar

2.3. Hydro

2.4. Wind

2.5. Additional Renewable Resources

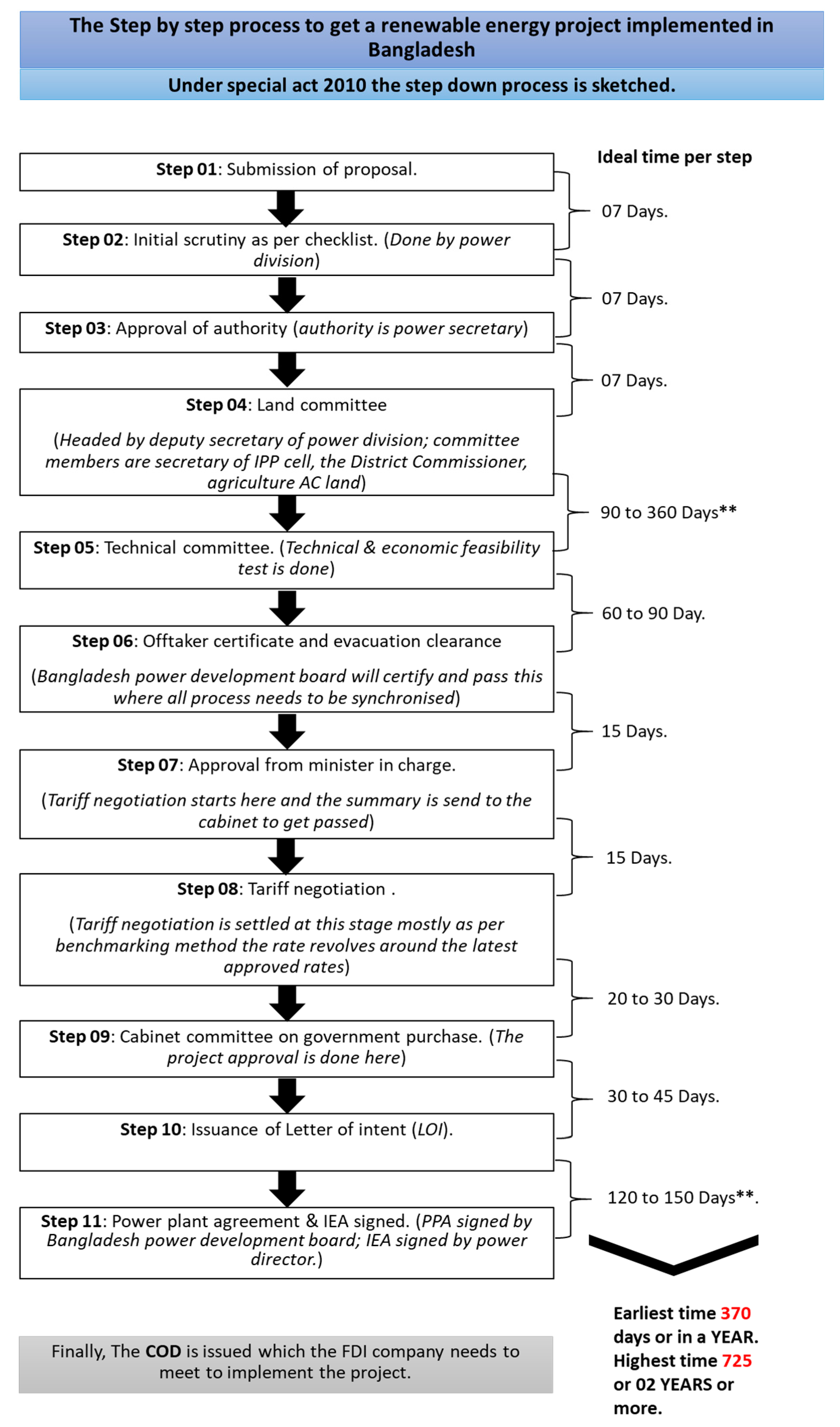

3. Methodology and Analytical Factor

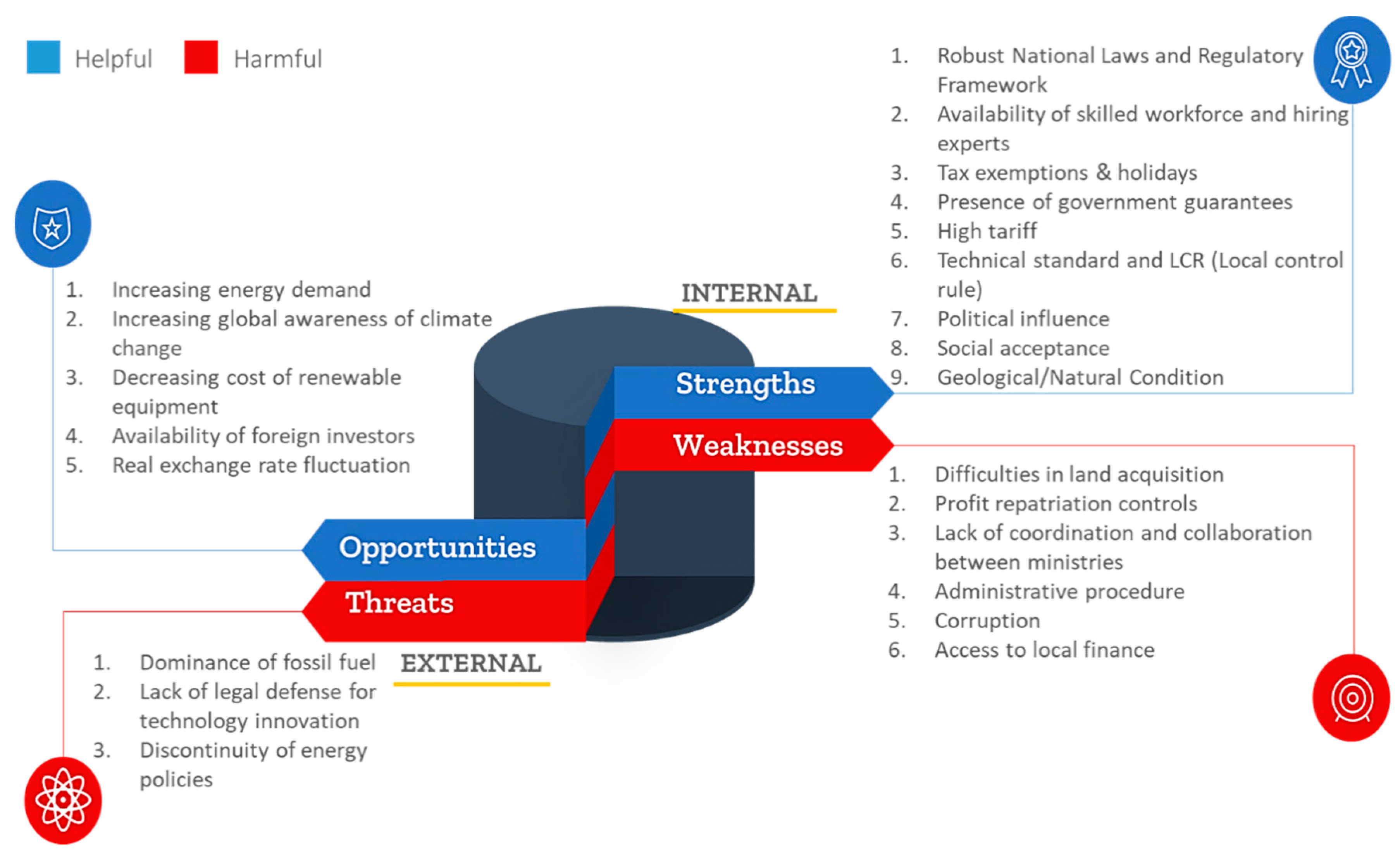

4. Results and Discussion

4.1. Strength Analysis

4.1.1. Robust National Laws and Regulatory Framework

4.1.2. Availability of Skilled Workforce and Hiring Experts

4.1.3. Tax Exemptions

4.1.4. Presence of Government Guarantees

4.1.5. High Tariff

4.1.6. Technical Standard and LCR (Local Control Rule)

4.1.7. Political Influence

4.1.8. Social Acceptance

4.1.9. Geological or Natural Condition

4.2. Analysis of Weaknesses

4.2.1. Difficulties in Land Acquisition/Rent/Lease

4.2.2. Profit Repatriation Controls

4.2.3. Lack of Coordination and Collaboration between Ministries

4.2.4. Administrative Procedure

4.2.5. Corruption

4.2.6. Access to Local Finance

4.3. Analysis of Opportunities

4.3.1. Increasing Energy Demand

4.3.2. Increasing Global Awareness of Climate Change

4.3.3. Decreasing Cost of Renewable Equipment

4.3.4. Availability of Foreign Investors

4.3.5. Real Exchange Rate Fluctuation

4.4. Analysis of Threats

4.4.1. Dominance of Fossil Fuel

4.4.2. Lack of Legal Defense for Technology Innovation

4.4.3. Discontinuity of Energy Policies

5. Conclusions and Policy Implications

6. Practical and Managerial Implications

7. Limitations and Direction for Future Research

Author Contributions

Funding

Conflicts of Interest

Appendix A. An Example of the Expert Interview Report

- What is the basic profile of your company? Included but not limited to firm’s size, firm’s ownership wholly owned subsidiary, equity joint venture, minimum equity participation, number of employees, business strategies and goal, competencies, type of investor, (namely, IPP developer, strategic investor or a combination), industry segment (in Bangladesh’s context specifically the generation segment for private investment).

- How important (economic benefit) do you think FDI in Bangladesh’s renewable energy sector?

- What are the strategic factors (as strength, weakness, opportunity, and threat) that are influential to make investment decision in Bangladesh’s renewable energy sector?

- At what extent you think the Institutional environment (smooth administration procedure/guidelines, political stability, rule abidance or law enforcement) factors influences the FDI decision? Which one among these is the most advantageous and the most disadvantageous in your opinion and why?

- At what extent you think the Macro-environment (Exchange rate fluctuation, access to local finance, cheap labor) factors impact the FDI decision? Which one among these is the most advantageous and the most disadvantageous in your opinion?

- At what extent you think the Natural resources/condition (Sunshine, duration of sun, proper wind, access to land) factors impact the FDI decision? Which one among these is the most advantageous and the most disadvantageous in your opinion?

- At what extent you think the Regulatory support (guarantee access to grid, absence of local requirement, Tech standards) factors impact the FDI decision? Which one among these is the most advantageous and the most disadvantageous in your opinion?

- At what extent you think the Political Support (renewable target, solid development plan, social acceptance) factors impact the FDI decision? Which one among these is the most advantageous and the most disadvantageous in your opinion?

- What are the potential barriers/threats and opportunities you think that are inhibiting sustainable FDI generation in Bangladesh’s renewable energy sector from both internal and external stakeholders?

- What are some of the renewable energy development policies (incentives, for example feed-in-tariffs, affordable land, i.e., solar parks, etc.) afforded by the government that are helping to strengthen and sustain new investment in the renewable energy sector?

References

- Moniruzzaman, M.; Day, R. Gendered energy poverty and energy justice in rural Bangladesh. Energy Policy 2020, 144, 111554. [Google Scholar] [CrossRef]

- Khan, S.A.R. The nexus between carbon emissions, poverty, economic growth, and logistics operations-Empirical evidence from Southeast Asian countries. Environ. Sci. Pollut. Res. 2019, 26, 13210–13220. [Google Scholar] [CrossRef] [PubMed]

- Karim, M.E.; Karim, R.; Islam, M.T.; Muhammad-Sukki, F.; Bani, N.A.; Muhtazaruddin, M.N. Renewable energy for sustainable growth and development: An evaluation of law and policy of Bangladesh. Sustainability 2019, 11, 5774. [Google Scholar] [CrossRef] [Green Version]

- Masud, M.H.; Nuruzzaman, M.; Ahamed, R.; Ananno, A.A.; Tomal, A.N.M.A. Renewable energy in Bangladesh: Current situation and future prospect. Int. J. Sustain. Energy 2020, 39, 132–175. [Google Scholar] [CrossRef]

- Bangladesh Bank. Foreign Direct Investment (FDI) in Bangladesh: Survey Report January–June 2019; Bangladesh Bank: Dhaka, Bangladesh, 2019. [Google Scholar]

- Raihan, S.; Khan, S.S. Structural Transformation, Inequality Dynamics, and Inclusive Growth in Bangladesh; UNU-WIDER: Helsinki, Finland, 2020. [Google Scholar]

- Halder, P.K.; Paul, N.; Joardder, M.U.H.; Sarker, M. Energy scarcity and potential of renewable energy in Bangladesh. Renew. Sustain. Energy Rev. 2015, 51, 1636–1649. [Google Scholar] [CrossRef]

- KNOEMA. Bangladesh Primary Energy Consumption. Available online: https://knoema.com/atlas/Bangladesh/Primary-energy-consumption (accessed on 31 August 2019).

- Mollik, S.; Rashid, M.M.; Hasanuzzaman, M.; Karim, M.E.; Hosenuzzaman, M. Prospects, progress, policies, and effects of rural electrification in Bangladesh. Renew. Sustain. Energy Rev. 2016, 65, 553–567. [Google Scholar] [CrossRef]

- BP. BP Statistical Review of World Energy; BP: London, UK, 2014. [Google Scholar]

- IEEJ. Energy Scenario of of Bangladesh; IEEJ: Tokyo, Japan, 2012. [Google Scholar]

- YCHARTS. Bangladesh Coal Consumption. Available online: https://ycharts.com/indicators/bangladesh_coal_consumption (accessed on 31 August 2019).

- YCHARTS. Bangladesh Natural Gas Consumption. Available online: https://ycharts.com/indicators/bangladesh_natural_gas_consumption (accessed on 21 October 2020).

- Hou, Y.; Iqbal, W.; Muhammad Shaikh, G.; Iqbal, N.; Ahmad Solangi, Y.; Fatima, A. Measuring energy efficiency and environmental performance: A case of South Asia. Processes 2019, 7, 325. [Google Scholar] [CrossRef] [Green Version]

- Pan, X.; Uddin, M.K.; Han, C.; Pan, X. Dynamics of financial development, trade openness, technological innovation and energy intensity: Evidence from Bangladesh. Energy 2019, 171, 456–464. [Google Scholar] [CrossRef]

- Das, A.; Halder, A.; Mazumder, R.; Saini, V.K.; Parikh, J.; Parikh, K.S. Bangladesh power supply scenarios on renewables and electricity import. Energy 2018, 155, 651–667. [Google Scholar] [CrossRef]

- Dastagir, M.R. Modeling recent climate change induced extreme events in Bangladesh: A review. Weather Clim. Extrem. 2015, 7, 49–60. [Google Scholar] [CrossRef] [Green Version]

- Gielen, D.; Boshell, F.; Saygin, D.; Bazilian, M.D.; Wagner, N.; Gorini, R. The role of renewable energy in the global energy transformation. Energy Strateg. Rev. 2019, 24, 38–50. [Google Scholar] [CrossRef]

- Gulagi, A.; Ram, M.; Solomon, A.A.; Khan, M.; Breyer, C. Current energy policies and possible transition scenarios adopting renewable energy: A case study for Bangladesh. Renew. Energy 2020, 155, 899–920. [Google Scholar] [CrossRef]

- Amin, S.B.; Rahman, S. (Eds.) Importance of Energy Efficiency in Bangladesh. In Energy Resources in Bangladesh; Springer International Publishing: Cham, Switzerland, 2019; pp. 15–19. [Google Scholar]

- Chowdhury, T.; Chowdhury, H.; Thirugnanasambandam, M.; Hossain, S.; Barua, P.; Ahamed, J.U.; Saidur, R.; Sait, S.M. Is the commercial sector of Bangladesh sustainable?—Viewing via an exergetic approach. J. Clean. Prod. 2019, 228, 544–556. [Google Scholar] [CrossRef]

- Brown, A.; Müller, S.; Dobrotková, Z. Renewable Energy: Markets and Prospects by Technology; IEA: Paris, France, 2011. [Google Scholar]

- REN21. Renewables 2014 Global Status Report; REN21: Paris, France, 2014. [Google Scholar]

- MPEMR. Renewable Energy Policy of Bangladesh; MPEMR: Dhaka, India, 2008.

- Baul, T.K.; Datta, D.; Alam, A. A comparative study on household level energy consumption and related emissions from renewable (biomass) and non-renewable energy sources in Bangladesh. Energy Policy 2018, 114, 598–608. [Google Scholar] [CrossRef]

- Berhanu, M.; Jabasingh, S.A.; Kifile, Z. Expanding sustenance in Ethiopia based on renewable energy resources—A comprehensive review. Renew. Sustain. Energy Rev. 2017, 75, 1035–1045. [Google Scholar] [CrossRef]

- Halder, P.K.; Paul, N.; Beg, M.R.A. Assessment of biomass energy resources and related technologies practice in Bangladesh. Renew. Sustain. Energy Rev. 2014, 39, 444–460. [Google Scholar] [CrossRef]

- Halder, P.K.; Paul, N.; Joardder, M.U.H.; Khan, M.Z.H.; Sarker, M. Feasibility analysis of implementing anaerobic digestion as a potential energy source in Bangladesh. Renew. Sustain. Energy Rev. 2016, 65, 124–134. [Google Scholar] [CrossRef]

- Nikolakakis, T.; Chattopadhyay, D.; Bazilian, M. A review of renewable investment and power system operational issues in Bangladesh. Renew. Sustain. Energy Rev. 2017, 68, 650–658. [Google Scholar] [CrossRef]

- Rahman, M.M.; Islam, A.K.M.S.; Salehin, S.; Al-Matin, M.A. Development of a model for techno-economic assessment of a stand-alone off-grid solar photovoltaic system in Bangladesh. Int. J. Renew. Energy Res. 2016, 6, 140–149. [Google Scholar]

- Chowdhury, P.; Jenkins, A.; Islam, Z.S.; Jenkins, A.; Islam, Z.S. Feasibility of solar-biomass hybrid cold storage for unelectrified rural areas of Bangladesh. In The Environmental Sustainable Development Goals in Bangladesh; Selim, S.A., Saha, S.K., Sultana, R., Roberts, C., Eds.; Routledge: London, UK, 2018; pp. 45–55. [Google Scholar]

- Khan, I. Power generation expansion plan and sustainability in a developing country: A multi-criteria decision analysis. J. Clean. Prod. 2019, 220, 707–720. [Google Scholar] [CrossRef]

- Faraz, T. Benefits of Concentrating Solar Power over Solar Photovoltaic for Power Generation in Bangladesh. In Proceedings of the 2nd International Conference on the Developments in Renewable Energy Technology (ICDRET 2012), Dhaka, Bangladesh, 5–7 January 2012; pp. 1–5. [Google Scholar]

- Nandi, S.K.; Ghosh, H.R. Prospect of wind–PV-battery hybrid power system as an alternative to grid extension in Bangladesh. Energy 2010, 35, 3040–3047. [Google Scholar] [CrossRef]

- Ullah, H.; Hoque, T.; Hasib, M. Current status of renewable energy sector in Bangladesh and a proposed grid connected hybrid renewable energy system. Int. J. Adv. Renew. Energy Res. 2012, 1, 618–627. [Google Scholar]

- Baten, M.Z.; Amin, E.M.; Sharin, A.; Islam, R.; Chowdhury, S.A. Renewable energy scenario of Bangladesh: Physical perspective. In Proceedings of the 2009 1st International Conference on the Developements in Renewable Energy Technology (ICDRET), Dhaka, Bangladesh, 17–19 December 2009; pp. 1–5. [Google Scholar]

- Guha, D.K.; Henkel, H.; Imam, B. Geothermal Potential in Bangladesh-Results from Investigations of Abandoned Deep Wells. In Proceedings of the World Geothermal Congress, Bali, Indonesia, 25–29 April 2010; pp. 25–29. [Google Scholar]

- Phadermrod, B.; Crowder, R.M.; Wills, G.B. Importance-Performance Analysis based SWOT analysis. Int. J. Inf. Manag. 2019, 44, 194–203. [Google Scholar] [CrossRef] [Green Version]

- Ishola, F.A.; Olatunji, O.O.; Ayo, O.O.; Akinlabi, S.A.; Adedeji, P.A.; Inegbenebor, A.O. Sustainable nuclear energy exploration in Nigeria—A SWOT analysis. Procedia Manuf. 2019, 35, 1165–1171. [Google Scholar] [CrossRef]

- Kamran, M.; Fazal, M.R.; Mudassar, M. Towards empowerment of the renewable energy sector in Pakistan for sustainable energy evolution: SWOT analysis. Renew. Energy 2020, 146, 543–558. [Google Scholar] [CrossRef]

- Chen, W.M.; Kim, H.; Yamaguchi, H. Renewable energy in eastern Asia: Renewable energy policy review and comparative SWOT analysis for promoting renewable energy in Japan, South Korea, and Taiwan. Energy Policy 2014, 74, 319–329. [Google Scholar] [CrossRef]

- Lei, Y.; Lu, X.; Shi, M.; Wang, L.; Lv, H.; Chen, S.; Hu, C.; Yu, Q.; da Silveira, S.D.H. SWOT analysis for the development of photovoltaic solar power in Africa in comparison with China. Environ. Impact Assess. Rev. 2019, 77, 122–127. [Google Scholar] [CrossRef]

- Markovska, N.; Taseska, V.; Pop-Jordanov, J. SWOT analyses of the national energy sector for sustainable energy development. Energy 2009, 34, 752–756. [Google Scholar] [CrossRef]

- Hamami, S.; Aloui, H.; Chaker, N.; Neji, R. SWOT Analysis: Tunisian Energy System. In Proceedings of the 2015 6th International Renewable Energy Congress (IREC 2015), Sousse, Tunisia, 24–26 March 2015; Volume 317, pp. 1–6. [Google Scholar]

- Agyekum, E.B.; Ansah, M.N.S.; Afornu, K.B. Nuclear energy for sustainable development: SWOT analysis on Ghana’s nuclear agenda. Energy Rep. 2020, 6, 107–115. [Google Scholar] [CrossRef]

- Queensland Government. Benefits and Limitations of SWOT Analysis. Available online: https://www.business.qld.gov.au/starting-business/planning/market-customer-research/swot-analysis/benefits-limitations (accessed on 22 October 2020).

- Adhabi, E.A.R.; Anozie, C.B.L. Literature review for the type of interview in qualitative research. Int. J. Educ. 2017, 9, 86–97. [Google Scholar] [CrossRef] [Green Version]

- Painuly, J.P. Barriers to renewable energy penetration: A framework for analysis. Renew. Energy 2001, 24, 73–89. [Google Scholar] [CrossRef]

- Keeley, A.R.; Matsumoto, K. Investors’ perspective on determinants of foreign direct investment in wind and solar energy in developing economies–Review and expert opinions. J. Clean. Prod. 2018, 179, 132–142. [Google Scholar] [CrossRef]

- Maul, P.; Watkins, B.; Salter, P.; Mcleod, R. Quality Assurance in Performance Assessments; SKi: Oxfordshire, UK, 1999. [Google Scholar]

- Hidalgo, M.; Möllmann, C.; Hinz, H.; Coll, M.; Frelat, R.; López-López, S.H.L.; Mangano, M.C.; Otero, J.; Tzanatos, V.; Andonegui, P.V.E.; et al. Analyses Between European Atlantic and Mediterranean Marine Ecosystems To Move Towards an Ecosystem-Based Approach To Fisheries (Wgcomeda). ICES Sci. Rep. 2019, 1, 1–30. [Google Scholar]

- Kuhnert, P.M.; Martin, T.G.; Griffiths, S.P. A guide to eliciting and using expert knowledge in Bayesian ecological models. Ecol. Lett. 2010, 13, 900–914. [Google Scholar] [CrossRef] [PubMed]

- Morales-Ramirez, I.; Vergne, M.; Morandini, M.; Siena, A.; Perini, A.; Susi, A. Who is the expert? Combining intention and knowledge of online discussants in collaborative RE tasks. In Proceedings of the 36th International Conference on Software Engineering; ICSE Companion 2014-Proceedings; Association for Computing Machinery: New York, NY, USA, 2014; pp. 452–455. [Google Scholar]

- Krueger, T.; Page, T.; Hubacek, K.; Smith, L.; Hiscock, K. The role of expert opinion in environmental modelling. Environ. Model. Softw. 2012, 36, 4–18. [Google Scholar] [CrossRef]

- Hoff, T.; Straumsheim, P.; Bjørkli, C.A.; Bjørklund, R.A. An external validation of two psychosocial work environment surveys—A SWOT approach. Scand. J. Organ. Psychol. 2009, 1, 11–28. [Google Scholar]

- Hoof, T. Mapping the Organizational Climate for Innovation: Introducing SWOT as a Process Based Tool. In Confluence. Interdisciplinary Communications 2007/2008; Østreng, W., Ed.; Centre for Advanced Study, Norwegian Academy of Science and Letters: Oslo, Norway, 2009; pp. 75–79. ISBN 978-82-996367-6-6. [Google Scholar]

- Woodhouse, E. The obsolescing bargain redux: Foreign investment in the electric power sector in developing countries. NYU J. Int. Law Politics 2006, 38, 121–219. [Google Scholar]

- Lamech, R.; Saeed, K. What International Investors Look for when Investing in Developing Countries Results from a Survey of International Investors in the Power Sector; Energy and Mining Sector Board Discussion Paper; The World Bank: Washington, DC, USA, 2003. [Google Scholar]

- Besant-Jones, J.E. Reforming Power Markets in Developing Countries: What Have We Learned? Energy and Mining Sector Board; The World Bank: Washington, DC, USA, 2006. [Google Scholar]

- Thangavelu, S.M.; Wei Yong, Y.; Chongvilaivan, A. FDI, Growth and the Asian Financial Crisis: The Experience of Selected Asian Countries. World Econ. 2009, 32, 1461–1477. [Google Scholar] [CrossRef]

- Ang, J.B. Financial development and the FDI-growth nexus: The Malaysian experience. Appl. Econ. 2009, 41, 1595–1601. [Google Scholar] [CrossRef]

- Rahman, A. Foreign Direct Investment in Bangladesh, Prospects and Challenges, and Its Impact on Economy. Master’s Thesis, Asian Institute of Technology, Pathum Thani, Thailand, May 2012. [Google Scholar]

- UNCTAD. Investment Policy Review: Bangladesh; UNCTAD: Geneva, Switzearland, 2013. [Google Scholar]

- Raquiba, H.; Ishak, Z. Sustainability reporting practices in the energy sector of Bangladesh. Int. J. Energy Econ. Policy 2020, 10, 508–516. [Google Scholar] [CrossRef]

- Jones, N.; Warren, P. Innovation and distribution of solar home systems in Bangladesh. Clim. Dev. 2020, 13, 1–13. [Google Scholar] [CrossRef]

- Huang, F.; Liu, J.; Wang, Z.; Shuai, C.; Li, W. Of job, skills, and values: Exploring rural household energy use and solar photovoltaics in poverty alleviation areas in China. Energy Res. Soc. Sci. 2020, 67, 101517. [Google Scholar] [CrossRef]

- Rahman, A. Solar Home Systems Created 1.37 Lakh Jobs: Report. Available online: https://www.thedailystar.net/city/news/solar-home-systems-created-137-lakh-jobs-report-1969873 (accessed on 22 October 2020).

- Khan, I. Impacts of energy decentralization viewed through the lens of the energy cultures framework: Solar home systems in the developing economies. Renew. Sustain. Energy Rev. 2020, 119, 109576. [Google Scholar] [CrossRef]

- Amin, S.B.; Rahman, S. Role of FDI in Energy Market in Bangladesh. In Energy Resources in Bangladesh; Springer International Publishing: Berlin/Heidelberg, Germany, 2019; pp. 81–84. [Google Scholar]

- Mahbub, T.; Jongwanich, J. Determinants of foreign direct investment (FDI) in the power sector: A case study of Bangladesh. Energy Strategy Rev. 2019, 24, 178–192. [Google Scholar] [CrossRef]

- Lopatkin, D.S.; Shushunova, T.N.; Shaldina, G.E.; Gibadullin, A.A.; Smirnova, I.L. Renewable and small energy development management. J. Physics Conf. Ser. 2019, 1399, 125993. [Google Scholar] [CrossRef] [Green Version]

- Proskuryakova, L. Energy technology foresight in emerging economies. Technol. Forecast. Soc. Chang. 2017, 119, 205–210. [Google Scholar] [CrossRef]

- Sequeira, T.N.; Santos, M.S. Renewable energy and politics: A systematic review and new evidence. J. Clean. Prod. 2018, 192, 553–568. [Google Scholar] [CrossRef]

- Karim, R.; Karim, M.E.; Munir, A.B.; Newaz, M.S. Social, Economic and Political Implications of Nuclear Power Plant in Bangladesh. In Proceedings of the Social Sciences Postgraduate International Seminar, Penang, Malaysia, 28 November 2017; pp. 11–17. [Google Scholar]

- Ajide, K.B.; Raheem, I.D. Institutions-FDI Nexus in ECOWAS Countries. J. African Bus. 2016, 17, 319–341. [Google Scholar] [CrossRef]

- Uddin, M.N.; Rahman, M.A.; Mofijur, M.; Taweekun, J.; Techato, K.; Rasul, M.G. Renewable energy in Bangladesh: Status and prospects. Energy Procedia 2019, 160, 655–661. [Google Scholar] [CrossRef]

- Khan, S.H.; Rahman, T.; Hossain, S. A brief study of the prospect of solar energy in generation of electricity in Bangladesh. Cyber J. Multidiscip. J. Sci. Technol. 2012, 1–8. [Google Scholar]

- Aryeetey, C.; Barthel, F.; Busse, M.; Loehr, C.; Osei, R. Empirical Study on the Determinants and Pro-Development Impacts of Foreign Direct Investment in Ghana; HWWI: Hamburg, Germany, 2008. [Google Scholar]

- te Velde, D.W. Policies Towards Foreign Direct Investment in Developing Countries: Emerging Best-PRACTICES and Outstanding Issues; Overseas Development Institute (ODI): London, UK, 2001. [Google Scholar]

- Khatun, F.; Ahamad, M. Foreign direct investment in the energy and power sector in Bangladesh: Implications for economic growth. Renew. Sustain. Energy Rev. 2015, 52, 1369–1377. [Google Scholar] [CrossRef]

- Majumder, R.; Khalil, M.; Rashi, M. Uranium Exploration Status in Bangladesh: Conceptual Study. In Proceedings of the IAEA: Technical Meeting on Uranium from Unconventional Resources, Vienna, Austria, November 2014; pp. 1–26. Available online: https://inis.iaea.org/collection/NCLCollectionStore/_Public/48/039/48039517.pdf (accessed on 19 December 2020).

- Islam, S.; Chu, C.; Smart, J.C.R. Challenges in integrating disaster risk reduction and climate change adaptation: Exploring the Bangladesh case. Int. J. Disaster Risk Reduct. 2020, 47, 101540. [Google Scholar] [CrossRef]

- Sarker, N.I.; Wu, M. Bureaucracy in Bangladesh: A Disaster Management Perspective. In Global Encyclopedia of Public Administration, Public Policy, and Governance; Farazmand, A., Ed.; Springer International Publishing: Cham, Switzerland, 2019; pp. 1–5. ISBN 978-3-319-31816-5. [Google Scholar]

- Rofiqul Islam, M.; Rabiul Islam, M.; Rafiqul Alam Beg, M. Renewable energy resources and technologies practice in Bangladesh. Renew. Sustain. Energy Rev. 2008, 12, 299–343. [Google Scholar] [CrossRef]

- Alam Hossain Mondal, M.; Kamp, L.M.; Pachova, N.I. Drivers, barriers, and strategies for implementation of renewable energy technologies in rural areas in Bangladesh—An innovation system analysis. Energy Policy 2010, 38, 4626–4634. [Google Scholar] [CrossRef]

- World Bank Group. Doing Business 2019: Training for Reform; The World Bank: Washington, DC, USA, 2019. [Google Scholar]

- Asadullah, M.N.; Chakravorty, N.N.T. Growth, governance and corruption in Bangladesh: A re-assessment. Third World Q. 2019, 40, 947–965. [Google Scholar] [CrossRef]

- Khan, I. Energy-saving behaviour as a demand-side management strategy in the developing world: The case of Bangladesh. Int. J. Energy Environ. Eng. 2019, 10, 493–510. [Google Scholar] [CrossRef] [Green Version]

- Hasan, M.K.; Mohammad, N. An Outlook over Electrical Energy Generation and Mixing Policies of Bangladesh to Achieve Sustainable Energy Targets-Vision 2041. In Proceedings of the 2nd International Conference on Electrical, Computer and Communication Engineering (ECCE 2019), Cox’s Bazar, Bangladesh, 7–9 February 2019; pp. 1–5. [Google Scholar]

- Alam, M.J.; Ahmed, M.; Begum, I.A. Nexus between non-renewable energy demand and economic growth in Bangladesh: Application of Maximum Entropy Bootstrap approach. Renew. Sustain. Energy Rev. 2017, 72, 399–406. [Google Scholar] [CrossRef]

- Erdiwansyah; Mamat, R.; Sani, M.S.M.; Sudhakar, K. Renewable energy in Southeast Asia: Policies and recommendations. Sci. Total Environ. 2019, 670, 1095–1102. [Google Scholar] [CrossRef]

- Woodhouse, M.; Smith, B.; Ramdas, A.; Robert, M. Crystalline Silicon Photovoltaic Module Manufacturing Costs and Sustainable Pricing: 1H 2018 Benchmark and Cost Reduction Roadmap; NREL: Golden, CO, USA, 2019.

- Froot, K.A.; Stein, J.C. Exchange rates and foreign direct investment: An imperfect capital markets approach. Q. J. Econ. 1991, 106, 1191–1217. [Google Scholar] [CrossRef]

- Kiyota, K.; Urata, S. Exchange Rate, Exchange Rate Volatility and Foreign Direct Investment. World Econ. 2004, 27, 1501–1536. [Google Scholar] [CrossRef]

- Khan, I. Drivers, enablers, and barriers to prosumerism in Bangladesh: A sustainable solution to energy poverty? Energy Res. Soc. Sci. 2019, 55, 82–92. [Google Scholar] [CrossRef]

- Gao, X.; Zhai, K. Performance evaluation on intellectual property rights policy system of the renewable energy in China. Sustainability 2018, 10, 2097. [Google Scholar] [CrossRef] [Green Version]

- Kim, Y.J.; Wilson, C. Analysing future change in the EU’s energy innovation system. Energy Strategy Rev. 2019, 24, 279–299. [Google Scholar] [CrossRef]

- Karim, R.; Karim, M.E.; Muhammad-Sukki, F.; Abu-Bakar, S.H.; Bani, N.A.; Munir, A.B.; Kabir, A.I.; Ardila-Rey, J.A.; Mas’ud, A.A. Nuclear energy development in Bangladesh: A study of opportunities and challenges. Energies 2018, 11, 1672. [Google Scholar] [CrossRef] [Green Version]

- Mahbub, T.; Jongwanich, J. Barriers to foreign direct investment in the power sector: Evidence from Bangladesh. Int. J. Dev. Issues 2019, 18, 310–333. [Google Scholar] [CrossRef]

- Alam, S. Intellectual property rights and other development challenges in Bangladesh. In Bangladesh Handbook of International Law; Shahabuddin, M., Ed.; Routledge, Taylor and Francis Group: London, UK, 2021; Accepted. [Google Scholar]

- Solangi, Y.A.; Tan, Q.; Mirjat, N.H.; Ali, S. Evaluating the strategies for sustainable energy planning in Pakistan: An integrated SWOT-AHP and Fuzzy-TOPSIS approach. J. Clean. Prod. 2019, 236, 117655. [Google Scholar] [CrossRef]

- Keeley, A.R.; Matsumoto, K. Relative significance of determinants of foreign direct investment in wind and solar energy in developing countries—AHP analysis. Energy Policy 2018, 123, 337–348. [Google Scholar] [CrossRef]

- Pušnik, M.; Sučić, B. Integrated and realistic approach to energy planning—A case study of Slovenia. Manag. Environ. Qual. Int. J. 2014, 25, 30–51. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Renewable Energy Sources | Potential Future | Entities Involved |

|---|---|---|

| Solar | Tremendous | Public and private sector |

| Biogas power plants based on Cattle waste | 350 MW given that 0.752 m3 of biogas consumption per kWh | Mostly by the private sector |

| Hydro | Latent prospect for micro or mini-hydro (max. 5 MW) are limited. Anticipated hydro potential approximately 500 MW | Predominantly by the public entities |

| Wind | Wind mapping is further required to gauge the potential | Mainly via PPP |

| Rice husk-based biomass gasification power plant | 300 MW given that 2 kg of husk consumption per kWh | Mostly by the private sector |

| Domestic biogas system | 8.6 million m3 of biogas | Both the public and private sector |

| Experts Field | List of Experts | Designation of the Expert | FDI Source or Headquarter | Sector or Experience | PROJECT SIZE | Interview Date |

|---|---|---|---|---|---|---|

| Industry | Expert A | Managing Director | United Kingdom | Solar | 28 MW | 4 August 2020 |

| Expert B | Chairman | Singapore | Solar | 50 MW | 20 July 2020 | |

| Expert C | Senior Engineer | China | Wind | 60 MW | 27 August 2020 | |

| Expert E | Deputy General Manager | China | Solar | 35 MW | 27 July 2020 | |

| Multilateral | Expert A | Director | USA | Solar and Wind—Multilateral Financial Organization | NA | 20 August 2020 |

| Expert C | Senior manger | Bangladesh | Solar and Wind—Local Non-Bank Financial Institution | NA | 12 August 2020 | |

| Government | Expert A | Chairman | Bangladesh | Solar and Wind—Regulatory and Policy Making Authority | NA | 29 July 2020 |

| Expert B | Deputy Director | Bangladesh | Solar and Wind—Green Financing and Policy Making Authority | NA | 29 August 2020 | |

| Academic | Expert A | Professor and Director | Bangladesh | Solar and Wind—Academic and Institutional Researcher | NA | 3 September 2020 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Karim, R.; Muhammad-Sukki, F.; Hemmati, M.; Newaz, M.S.; Farooq, H.; Muhtazaruddin, M.N.; Zulkipli, M.; Ardila-Rey, J.A. Paving towards Strategic Investment Decision: A SWOT Analysis of Renewable Energy in Bangladesh. Sustainability 2020, 12, 10674. https://0-doi-org.brum.beds.ac.uk/10.3390/su122410674

Karim R, Muhammad-Sukki F, Hemmati M, Newaz MS, Farooq H, Muhtazaruddin MN, Zulkipli M, Ardila-Rey JA. Paving towards Strategic Investment Decision: A SWOT Analysis of Renewable Energy in Bangladesh. Sustainability. 2020; 12(24):10674. https://0-doi-org.brum.beds.ac.uk/10.3390/su122410674

Chicago/Turabian StyleKarim, Ridoan, Firdaus Muhammad-Sukki, Mina Hemmati, Md Shah Newaz, Haroon Farooq, Mohd Nabil Muhtazaruddin, Muhammad Zulkipli, and Jorge Alfredo Ardila-Rey. 2020. "Paving towards Strategic Investment Decision: A SWOT Analysis of Renewable Energy in Bangladesh" Sustainability 12, no. 24: 10674. https://0-doi-org.brum.beds.ac.uk/10.3390/su122410674