Corporate Governance and Corporate Social Responsibility: Evidence from the Role of the Largest Institutional Blockholders in the Korean Market

Abstract

:1. Introduction

2. Institutional Monitoring and CSR in the Korean Market

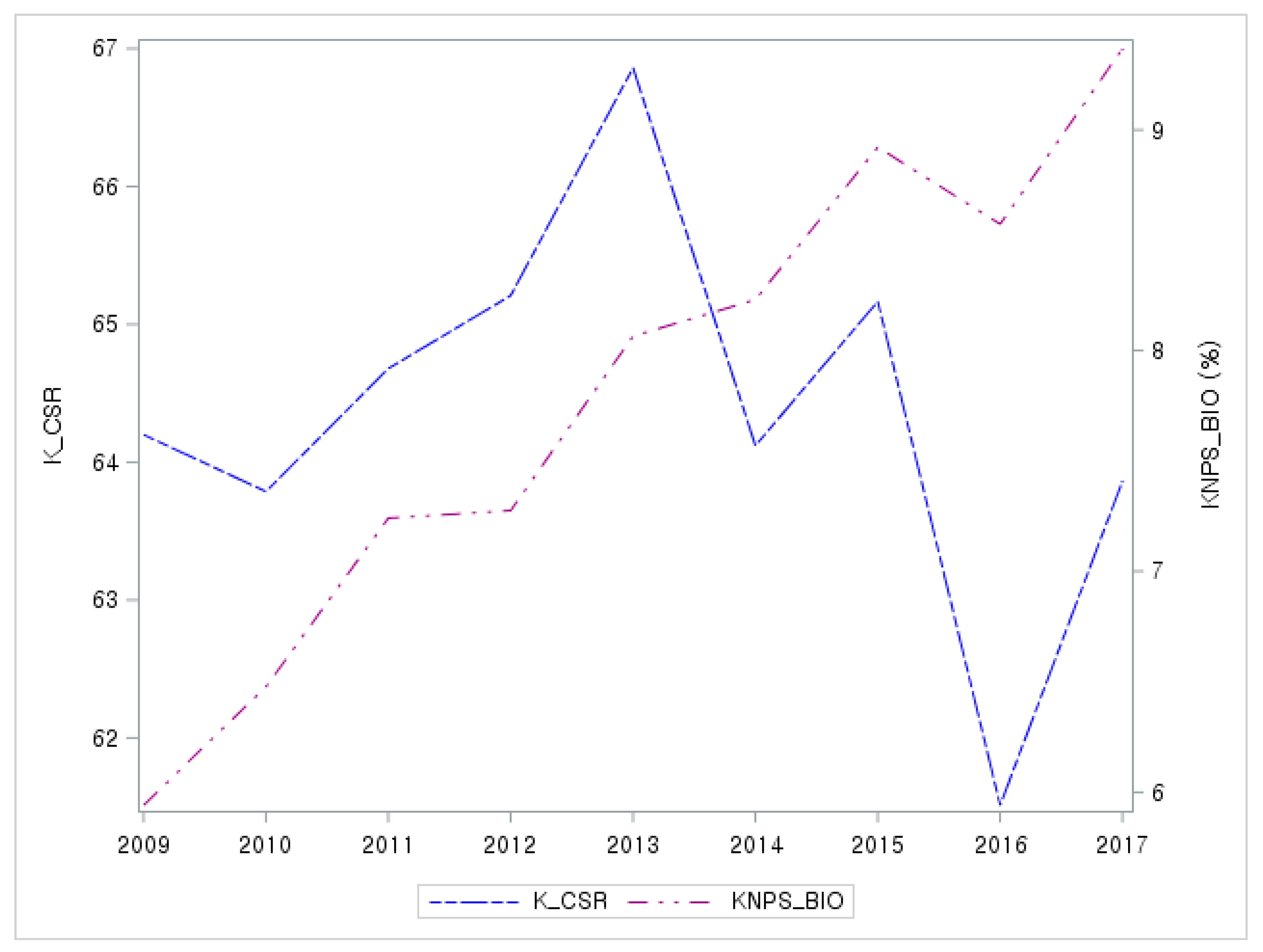

3. Sample Data

4. Empirical Analysis

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Smith, M.P. Shareholder activism by institutional investors: Evidence from CalPERS. J. Financ. 1996, 51, 227–252. [Google Scholar] [CrossRef]

- Carleton, W.T.; Nelson, J.A.; Weisbach, M.S. The influence of institutions on corporate governance through private negotiations: Evidence from TIAA-CREF. J. Financ. 1998, 53, 1335–1362. [Google Scholar] [CrossRef]

- Del Guercio, D.; Hawkins, J. The motivation and impact of pension fund activism. J. Financ. Econ. 1999, 52, 293–340. [Google Scholar] [CrossRef]

- Gillan, S.L.; Starks, L.T. Corporate governance proposals and shareholder activism: The role of institutional investors. J. Financ. Econ. 2000, 57, 275–305. [Google Scholar] [CrossRef]

- O’Barr, W.M.; Conley, J.M.; Brancato, C.K. Fortune and Folly: The Wealth and Power of Institutional Investing; Irwin Professional Pub: Chicago, IL, USA, 1992. [Google Scholar]

- Chung, R.; Firth, M.; Kim, J. Institutional monitoring and opportunistic earnings management. J. Corp. Financ. 2002, 8, 29–48. [Google Scholar] [CrossRef]

- Hartzell, J.C.; Starks, L.T. Institutional investors and executive compensation. J. Financ. 2003, 58, 2351–2374. [Google Scholar] [CrossRef] [Green Version]

- Janakiraman, S.; Radhakrishnan, S.; Tsang, A. Institutional investors, managerial ownership, and executive compensation. J. Account. Audit. Financ. 2010, 25, 673–707. [Google Scholar] [CrossRef]

- Grinstein, Y.; Michaely, R. Institutional holdings and payout policy. J. Financ. 2005, 60, 1389–1426. [Google Scholar] [CrossRef]

- Chen, X.; Harford, J.; Li, K. Monitoring: Which institutions matter? J. Financ. Econ. 2007, 86, 279–305. [Google Scholar] [CrossRef]

- Ferreira, M.A.; Massa, M.; Matos, P. Shareholders at the gate? Institutional investors and cross-border mergers and acquisitions. Rev. Financ. Stud. 2010, 23, 601–644. [Google Scholar] [CrossRef]

- Chung, C.Y.; Liu, C.; Wang, K.; Zykaj, B.B. Institutional monitoring: Evidence from the F-score. J. Bus. Financ. Account. 2015, 42, 885–914. [Google Scholar] [CrossRef]

- Coffee, J.C. Liquidity versus control: The institutional investor as corporate monitor. Columbia Law Rev. 1991, 91, 1277–1368. [Google Scholar] [CrossRef]

- Bhide, A. The hidden costs of stock market liquidity. J. Financ. Econ. 1993, 34, 31–51. [Google Scholar] [CrossRef]

- Parrino, R.; Sias, R.W.; Starks, L.T. Voting with their feet: Institutional ownership changes around forced CEO turnover. J. Financ. Econ. 2003, 68, 3–46. [Google Scholar] [CrossRef]

- Bushee, B.J. The influence of institutional investors on myopic R&D investment behavior. Account. Rev. 1998, 73, 305–333. [Google Scholar]

- Bushee, B.J.; Goodman, T.H. Which institutional investors trade based on private information about earnings and returns? J. Account. Res. 2007, 45, 289–321. [Google Scholar] [CrossRef] [Green Version]

- Bushee, B. Do institutional investors prefer near-term earnings over long-run value? Contemp. Account. Res. 2001, 18, 207–246. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Wu, S.I.; Lin, H.F. The correlation of CSR and consumer behavior: A study of convenience store. Int. J. Mark. Stud. 2014, 6, 66–80. [Google Scholar] [CrossRef] [Green Version]

- Janney, J.J.; Gove, S. Reputation and corporate social responsibility aberrations, trends, and hypocrisy: Reactions to firm choices in the stock option backdating scandal. J. Manag. Stud. 2011, 48, 1562–1585. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employees. Acad. Manag. J. 1997, 40, 658–672. [Google Scholar]

- Park, K.-H.; Byun, J.; Choi, P.M.S. Managerial overconfidence, corporate social responsibility, and financial constraints. Sustainability 2020, 12, 61. [Google Scholar] [CrossRef] [Green Version]

- Cheung, Y.L.; Tan, W.; Ahn, H.J.; Zhang, Z. Does corporate social responsibility matter in Asian emerging markets? J. Bus. Ethics. 2010, 92, 401–413. [Google Scholar] [CrossRef]

- Nam, Y.S.; Jun, H. The shaping of corporate social responsibility in Korea’s economic development. Glob. J. Bus. Manag. Account. 2011, 1, 10–20. [Google Scholar]

- Sharma, B. Contextualising CSR in Asia: Corporate Social Responsibility in Asian Economies; Lien Centre for Social Innovation: Singapore, 2013. [Google Scholar]

- Cho, E.; Chun, S.; Choi, D. International diversification, corporate social responsibility, and corporate governance: Evidence from Korea. J. Appl. Bus. Res. 2015, 31, 743. [Google Scholar] [CrossRef]

- Choi, S.; Aguilera, R.V. CSR dynamics in South Korea and Japan: A comparative analysis. In Corporate Social Responsibility: A Case Study Approach; Mallin, C., Ed.; Edward Elgar Publishing Ltd.: New York, NY, USA, 2009; pp. 123–147. [Google Scholar]

- Choi, B.B.; Lee, D.; Park, Y. Corporate social responsibility, corporate governance and earnings quality: Evidence from Korea. Corp. Gov. Int. Rev. 2013, 21, 447–467. [Google Scholar] [CrossRef]

- Kim, H.; Park, K.; Ryu, D. Corporate environmental responsibility: A legal origins perspective. J. Bus. Ethics 2017, 140, 381–402. [Google Scholar] [CrossRef]

- Gaspar, J.M.; Massa, M.; Matos, P. Shareholder investment horizons and the market for corporate control. J. Financ. Econ. 2005, 76, 135–165. [Google Scholar] [CrossRef]

- Yan, X.S.; Zhang, Z. Institutional investors and equity returns: Are short-term institutions better informed? Rev. Financ. Stud. 2009, 22, 893–924. [Google Scholar] [CrossRef]

- Burns, N.; Kedia, S.; Lipson, M. Institutional ownership and monitoring: Evidence from financial misreporting. J. Corp. Financ. 2010, 16, 443–455. [Google Scholar] [CrossRef]

- Johnson, R.A.; Greening, D.W. The effects of corporate governance and institutional ownership types on corporate social performance. Acad. Manag. J. 1999, 42, 564–576. [Google Scholar]

- Graves, S.B.; Waddock, S.A. Institutional owners and corporate social performance. Acad. Manag. J. 1994, 37, 1034–1046. [Google Scholar]

- Cox, P.; Brammer, S.; Millington, A. An empirical examination of institutional investor preferences for corporate social performance. J. Bus. Ethics 2004, 52, 27–43. [Google Scholar] [CrossRef]

- Neubaum, D.O.; Zahra, S.A. Institutional ownership and corporate social performance: The moderating effects of investment horizon, activism, and coordination. J. Manag. 2006, 32, 108–131. [Google Scholar] [CrossRef]

- Cox, P.; Wicks, P.G. Institutional interest in corporate responsibility: Portfolio evidence and ethical explanation. J. Bus. Ethics 2011, 103, 143–165. [Google Scholar] [CrossRef]

- Oh, W.Y.; Chang, Y.K.; Martynov, A. The effect of ownership structure on corporate social responsibility: Empirical evidence from Korea. J. Bus. Ethics 2011, 104, 283–297. [Google Scholar] [CrossRef]

- Barnea, A.; Rubin, A. Corporate social responsibility as a conflict between shareholders. J. Bus. Ethics 2010, 97, 71–86. [Google Scholar] [CrossRef]

- Dam, L.; Scholtens, B. Does ownership type matter for corporate social responsibility? Corp. Gov. 2012, 20, 233–252. [Google Scholar] [CrossRef]

- Brickley, J.A.; Lease, R.C.; Smith, C.W. Ownership structure and voting on antitakeover amendments. J. Financ. Econ. 1988, 20, 267–291. [Google Scholar] [CrossRef]

- Chang, S.J. Ownership structure, expropriation, and performance of group-affiliated companies in Korea. Acad. Manag. J. 2003, 46, 238–253. [Google Scholar]

- Edmans, A. Does the stock market fully value intangibles? Employee satisfaction and equity prices. J. Financ. Econ. 2011, 101, 621–640. [Google Scholar] [CrossRef] [Green Version]

- Admati, A.R.; Pfleiderer, P. The “Wall Street Walk” and shareholder activism: Exit as a form of voice. Rev. Financ. Stud. 2009, 22, 2645–2685. [Google Scholar] [CrossRef] [Green Version]

- Waddock, S.A.; Graves, S.B. The corporate social performance–financial performance link. Strat. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Hong, H.; Kubik, J.D.; Scheinkman, J.A. Financial Constraints on Corporate Goodness; Working paper No. w18476; National Bureau of Economic Research: Boston, MA, USA, 2012. [Google Scholar]

- McWilliams, A.; Siegel, D. Profit maximizing corporate social responsibility. Acad. Manag. Rev. 2001, 26, 504–505. [Google Scholar] [CrossRef]

- Gompers, P.A.; Metrick, A. Institutional investors and equity prices. Q. J. Econ. 2001, 116, 229–259. [Google Scholar] [CrossRef]

- Surroca, J.; Tribó, J.A. Managerial entrenchment and corporate social performance. J. Bus. Financ. Account. 2008, 35, 748–789. [Google Scholar] [CrossRef] [Green Version]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Petersen, M.A. Estimating standard errors in finance panel data sets: Comparing approaches. Rev. Financ. Stud. 2009, 22, 435–480. [Google Scholar] [CrossRef] [Green Version]

- Del Guercio, D.; Tran, H. Institutional investor activism. In Socially Responsible Finance and Investing; Baker, H.K., Nofsinger, J.R., Eds.; John Wiley & Sons Inc.: Newark, NJ, USA, 2012; pp. 359–380. [Google Scholar]

- Dimson, E.; Karakaş, O.; Li, X. Active ownership. Rev. Financ. Stud. 2015, 28, 3225–3268. [Google Scholar] [CrossRef] [Green Version]

- Amihud, Y. Illiquidity and stock returns: Cross-section and time-series effects. J. Financ. Mark. 2002, 5, 31–56. [Google Scholar] [CrossRef] [Green Version]

- Ayers, B.C.; Ramalingegowda, S.; Yeung, P.E. Hometown advantage: The effects of monitoring institution location on financial reporting discretion. J. Account. Econ. 2011, 52, 41–61. [Google Scholar] [CrossRef]

- Tang, Y.; Qian, C.; Chen, G.; Shen, R. How CEO hubris affects corporate social (ir) responsibility. Strateg. Manag. J. 2015, 36, 1338–1357. [Google Scholar] [CrossRef]

- McCarthy, S.; Oliver, B.; Song, S. Corporate social responsibility and CEO confidence. J. Bank. Financ. 2017, 75, 280–291. [Google Scholar] [CrossRef] [Green Version]

- Loh, L.; Thomas, T.; Wang, Y. Sustainability reporting and firm value: Evidence from Singapore-listed companies. Sustainability 2017, 9, 2112. [Google Scholar] [CrossRef] [Green Version]

- Singh, P.J.; Sethuraman, K.; Lam, J.Y. Impact of corporate social responsibility dimensions on firm value: Some evidence from Hong Kong and China. Sustainability 2017, 9, 1532. [Google Scholar] [CrossRef] [Green Version]

- Hategan, C.-D.; Curea-Pitorac, R.-I. Testing the correlations between corporate giving, performance and company value. Sustainability 2017, 9, 1210. [Google Scholar] [CrossRef] [Green Version]

- Kim, W.S.; Park, K.; Lee, S.H. Corporate social responsibility, ownership structure, and firm value: Evidence from Korea. Sustainability 2018, 10, 2497. [Google Scholar] [CrossRef] [Green Version]

- Liu, C.; Chung, C.Y.; Sul, H.K.; Wang, K. Does hometown advantage matter? The case of institutional blockholder monitoring on earnings management in Korea. J. Int. Bus. Stud. 2018, 49, 196–221. [Google Scholar] [CrossRef]

- Choi, P.M.S.; Chung, C.Y.; Hwang, J.H.; Liu, C. Heads I Win, Tails You Lose: Institutional Monitoring Of Executive Pay Rigidity. J. Financ. Res. 2019, 42, 789–816. [Google Scholar] [CrossRef]

- Choi, P.M.S.; Chung, C.Y.; Liu, C. Self-attribution of overconfident CEOs and asymmetric investment-cash flow sensitivity. N. Am. J. Econ. Financ. 2018, 46, 1–14. [Google Scholar] [CrossRef]

- Chung, C.Y.; Hur, S.K.; Liu, C. Institutional investors and cost stickiness: Theory and evidence. N. Am. J. Econ. Financ. 2019, 47, 336–350. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Mean | Std. Dev. | Minimum | 25th Pct. | Median | 75th Pct. | Maximum |

|---|---|---|---|---|---|---|---|

| KNPS_BIO | 7.8924 | 2.3728 | 5.0000 | 5.9976 | 7.3100 | 9.2535 | 14.6600 |

| K_CSR | 64.1731 | 3.1617 | 52.7315 | 62.2419 | 64.3550 | 66.1978 | 75.1924 |

| SIZE | 21.1130 | 1.5586 | 17.9755 | 20.0718 | 20.8363 | 22.0333 | 26.0521 |

| LEV | 0.4581 | 0.1941 | 0.0621 | 0.2839 | 0.4561 | 0.5977 | 0.9328 |

| ROA | 0.0603 | 0.0746 | −0.2862 | 0.0257 | 0.0532 | 0.0851 | 1.5265 |

| Q | 1.2898 | 0.7684 | 0.3970 | 0.8888 | 1.0664 | 1.4427 | 7.5200 |

| RNDS | 0.0116 | 0.0233 | 0.0000 | 0.0000 | 0.0021 | 0.0101 | 0.1347 |

| BM | 1.0573 | 0.7839 | 0.0799 | 0.5580 | 0.8831 | 1.3241 | 9.3265 |

| CASHF | 0.0926 | 0.0800 | −0.1140 | 0.0556 | 0.0843 | 0.1184 | 1.5744 |

| SD | 0.3635 | 0.1594 | 0.0152 | 0.2863 | 0.3668 | 0.4573 | 0.8879 |

| HHI | 0.0751 | 0.0699 | 0.0461 | 0.0489 | 0.0494 | 0.0748 | 0.9177 |

| KNPS_BIO | K_CSR | SIZE | LEV | ROA | Q | RNDS | BM | CASHF | SD | HHI | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| KNPS_BIO | 1 | ||||||||||

| K_CSR | −0.0005 [0.9901] | 1 | |||||||||

| SIZE | −0.0191 [0.6399] | 0.1608 *** [<0.0001] | 1 | ||||||||

| LEV | 0.0460 [0.2606] | −0.1341 *** [0.0010] | 0.3991 *** [<0.0001] | 1 | |||||||

| ROA | −0.0200 [0.6238] | 0.0737 * [0.0709] | −0.0968 ** [0.0177] | −0.2681 *** [<0.0001] | 1 | ||||||

| Q | 0.0176 [0.6664] | 0.1665 *** [<0.0001] | −0.0126 [0.7567] | −0.1015 ** [0.0129] | 0.2531 *** [<0.0001] | 1 | |||||

| RNDS | 0.0446 [0.2750] | 0.2109 *** [<0.0001] | −0.0132 [0.7466] | −0.1599 *** [<0.0001] | 0.1090 *** [0.0075] | 0.3042 *** [<0.0001] | 1 | ||||

| BM | −0.1576 *** [0.0001] | −0.1961 *** [<0.0001] | −0.0569 [0.1638] | 0.0572 [0.1615] | −0.2141 *** [<0.0001] | −0.5467 *** [<0.0001] | −0.1833 *** [<0.0001] | 1 | |||

| CASHF | −0.0342 [0.4025] | 0.1119 *** [0.0061] | −0.0183 [0.6532] | −0.2793 *** [<0.0001] | 0.9369 *** [<0.0001] | 0.2379 *** [<0.0001] | 0.1638 *** [<0.0001] | −0.2395 *** [<0.0001] | 1 | ||

| SD | −0.2727 *** [<0.0001] | −0.0207 [0.6127] | −0.0999 ** [0.0143] | 0.0896 ** [0.0281] | 0.0707 * [0.0832] | 0.0556 [0.1733] | −0.0079 [0.8453] | −0.0300 [0.4625] | 0.0817 ** [0.0453] | 1 | |

| HHI | −0.0029 [0.9419] | 0.0013 [0.9744] | 0.0192 [0.6380] | 0.0111 [0.7857] | 0.0165 [0.6863] | 0.0816 ** [0.0457] | −0.0391 [0.3379] | −0.0176 [0.6662] | 0.0160 [0.6957] | −0.0023 [0.9534] | 1 |

| Mean | Q1 | Q2 | Q3 | Q4 | Q4–Q1 (t-stat) |

|---|---|---|---|---|---|

| Quantiles Are Formed Based on Average Lagged KNPS_BIO | |||||

| KNPS_BIO | 5.4087 | 6.5996 | 8.1673 | 10.4830 | 5.0743 *** (9.28) |

| K_CSR | 64.4293 | 65.1524 | 64.3562 | 64.5096 | 0.0803 (0.24) |

| Model (1), K_CSR | Model (2), K_CSR with Chaebol Dummy | |||

|---|---|---|---|---|

| Intercept | 55.366 *** | 25.886 *** | 59.519 *** | 30.481 *** |

| (16.09) | (5.70) | (16.25) | (6.01) | |

| KNPS_BIOt–1 | −0.034 | 0.020 | −0.078 | −0.015 |

| (−0.41) | (0.27) | (−0.95) | (−0.21) | |

| Chaebol_Dummy | −0.283 ** | −0.231 ** | ||

| (−2.23) | (−2.15) | |||

| KNPS_BIOt–1Χ Chaebol_Dummy | 0.560 | 1.031 | ||

| (0.21) | (0.41) | |||

| SIZEt–1 | 0.457 *** | 0.155 | 0.344 ** | 0.121 |

| (2.77) | (1.05) | (2.00) | (0.77) | |

| LEVt–1 | −3.877 *** | −2.125 ** | −3.673 *** | −2.328 ** |

| (−3.21) | (−1.98) | (−2.95) | (−2.08) | |

| ROAt–1 | 5.216 | 4.100 | 8.725 | 6.337 |

| (0.78) | (0.70) | (1.27) | (1.03) | |

| Qt–1 | −0.373 | −0.147 | −0.579* | −0.345 |

| (−1.33) | (−0.60) | (−1.94) | (−1.29) | |

| RNDSt–1 | 17.925 ** | 9.731 | 16.112 * | 7.492 |

| (2.05) | (1.27) | (1.84) | (0.95) | |

| BMt–1 | −0.313 | 0.036 | −0.860 ** | −0.417 |

| (−1.24) | (0.16) | (−2.25) | (−1.21) | |

| CASHFt–1 | −3.017 | −0.710 | −6.744 | −3.296 |

| (−0.47) | (−0.13) | (−1.01) | (−0.55) | |

| SDt–1 | 4.111 ** | 5.474 *** | 2.789 | 5.112 *** |

| (2.40) | (3.64) | (1.40) | (2.83) | |

| HHIt–1 | 2.106 | 1.826 | 0.621 | 1.231 |

| (0.75) | (0.74) | (0.22) | (0.49) | |

| MARKET_D | 0.824 | 0.853 * | 0.874 * | 0.955 ** |

| (1.58) | (1.88) | (1.67) | (2.05) | |

| K_CSRt–1 | 0.515 *** | 0.476 *** | ||

| (8.64) | (7.48) | |||

| Firm-fixed effects | Yes | Yes | Yes | Yes |

| Year dummies | Yes | Yes | Yes | Yes |

| Adj. R-Squared | 0.1360 | 0.3430 | 0.1297 | 0.3101 |

| Obs. | 554 | 554 | 554 | 554 |

| C1 | C2 | C3 | C4 | C5 | C6 | |

|---|---|---|---|---|---|---|

| Intercept | 6.548 *** | 13.157 *** | 2.130 | 8.968 *** | −0.031 | 6.695 *** |

| (3.17) | (4.44) | (1.24) | (4.05) | (−0.04) | (3.80) | |

| KNPS_BIOt–1 | −0.038 | 0.083 | 0.059 | 0.040 | −0.012 | 0.066 |

| (−0.83) | (1.18) | (1.42) | (0.72) | (−0.56) | (1.55) | |

| SIZEt–1 | 0.076 | −0.232 * | 0.124 | −0.140 | 0.072* | −0.106 |

| (0.84) | (−1.72) | (1.52) | (−1.35) | (1.67) | (−1.29) | |

| LEVt–1 | 0.438 | 1.160 | −0.255 | 1.323 * | −0.402 | 0.628 |

| (0.66) | (1.18) | (−0.43) | (1.73) | (−1.33) | (1.05) | |

| ROAt–1 | 5.833 | 11.317 ** | 9.196 *** | 9.004 ** | −3.389 ** | 0.711 |

| (1.58) | (2.08) | (2.79) | (2.14) | (−2.05) | (0.21) | |

| Qt–1 | 0.038 | 0.178 | 0.110 | −0.071 | −0.014 | 0.064 |

| (0.25) | (0.78) | (0.80) | (−0.40) | (−0.20) | (0.46) | |

| RNDSt–1 | 2.584 | 3.546 | 2.168 | 0.427 | −2.482 | 3.086 |

| (0.53) | (0.50) | (0.50) | (0.08) | (−1.15) | (0.71) | |

| BMt–1 | −0.137 | −0.282 | −0.129 | −0.312 * | −0.059 | −0.198 |

| (−0.98) | (−1.37) | (−1.03) | (−1.96) | (−0.95) | (−1.57) | |

| CASHFt–1 | −2.957 | −8.913 * | −7.230 ** | −7.680 * | 2.671 * | −0.903 |

| (−0.83) | (−1.70) | (−2.27) | (−1.88) | (1.67) | (−0.28) | |

| SDt–1 | −1.782 * | −5.899 *** | −2.217 ** | −5.930 *** | 1.179 *** | −3.598 *** |

| (−1.83) | (−4.11) | (−2.57) | (−5.29) | (2.76) | (−4.09) | |

| HHIt–1 | −0.237 | 0.846 | 1.134 | −0.886 | −0.190 | 1.022 |

| (−0.15) | (0.37) | (0.82) | (−0.50) | (−0.27) | (0.73) | |

| MARKET_D | 0.095 | 0.161 | −0.203 | 0.136 | 0.138 | 0.156 |

| (0.33) | (0.38) | (−0.79) | (0.41) | (1.07) | (0.60) | |

| K_CSRt–1 | 0.580 *** | 0.516 *** | 0.350 *** | 0.569 *** | 0.697 *** | 0.558 *** |

| (11.83) | (10.82) | (6.60) | (14.33) | (16.28) | (13.03) | |

| Firm-fixed effects | Yes | Yes | Yes | Yes | Yes | Yes |

| Year dummies | Yes | Yes | Yes | Yes | Yes | Yes |

| Adj. R-Squared | 0.4323 | 0.5018 | 0.2885 | 0.6213 | 0.6667 | 0.5687 |

| Obs. | 554 | 554 | 554 | 554 | 554 | 554 |

| Low Liquidity | High Liquidity | Low RNDS | High RNDS | |

|---|---|---|---|---|

| Intercept | 34.569 *** | 21.961 *** | 21.272 *** | 34.546 *** |

| (3.14) | (3.39) | (3.12) | (5.10) | |

| KNPS_BIOt–1 | 0.111 | −0.043 | 0.067 | 0.007 |

| (1.09) | (−0.40) | (0.58) | (0.07) | |

| SIZEt–1 | 0.222 | 0.154 | 0.130 | 0.260 |

| (0.51) | (0.68) | (0.60) | (1.14) | |

| LEVt–1 | −1.816 | −1.568 | −1.216 | −4.158 ** |

| (−1.22) | (−0.84) | (−0.72) | (−2.36) | |

| ROAt–1 | 5.086 | 8.646 | 7.162 | 2.266 |

| (0.46) | (0.85) | (0.58) | (0.32) | |

| Qt–1 | −1.299 *** | 0.068 | −0.490 | −0.116 |

| (−2.81) | (0.19) | (−1.38) | (−0.25) | |

| RNDSt–1 | 29.403 *** | −0.125 | 653.186 ** | 6.458 |

| (2.78) | (−0.01) | (2.21) | (0.63) | |

| BMt–1 | −0.791 * | 0.426 | −0.158 | 0.020 |

| (−1.81) | (1.39) | (−0.37) | (0.07) | |

| CASHFt–1 | −2.843 | 5.103 | −1.366 | 0.424 |

| (−0.26) | (0.69) | (−0.13) | (0.06) | |

| SDt–1 | 2.099 | 5.978 *** | 5.048 ** | 5.675 ** |

| (0.88) | (2.80) | (2.35) | (2.40) | |

| HHIt–1 | 0.958 | 5.887 | 2.228 | 7.440 |

| (0.36) | (0.75) | (0.81) | (0.99) | |

| MARKET_D | 0.691 | 2.179 ** | 1.131* | 0.284 |

| (1.04) | (2.43) | (1.85) | (0.37) | |

| K_CSRt–1 | 0.405 *** | 0.530 *** | 0.585 *** | 0.365 *** |

| (4.39) | (6.32) | (7.43) | (3.59) | |

| Firm-fixed effects | Yes | Yes | Yes | Yes |

| Year dummies | Yes | Yes | Yes | Yes |

| Adj. R-Squared | 0.2822 | 0.4270 | 0.4137 | 0.2209 |

| Obs. | 275 | 279 | 280 | 274 |

| F-stat: Low (KNPS_BIOt–1) = High (KNPS_BIOt–1) | ||||

| 0.23 | 0.52 | |||

| [0.78] | [0.56] | |||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Choi, D.; Choi, P.M.S.; Choi, J.H.; Chung, C.Y. Corporate Governance and Corporate Social Responsibility: Evidence from the Role of the Largest Institutional Blockholders in the Korean Market. Sustainability 2020, 12, 1680. https://0-doi-org.brum.beds.ac.uk/10.3390/su12041680

Choi D, Choi PMS, Choi JH, Chung CY. Corporate Governance and Corporate Social Responsibility: Evidence from the Role of the Largest Institutional Blockholders in the Korean Market. Sustainability. 2020; 12(4):1680. https://0-doi-org.brum.beds.ac.uk/10.3390/su12041680

Chicago/Turabian StyleChoi, Daeheon, Paul Moon Sub Choi, Joung Hwa Choi, and Chune Young Chung. 2020. "Corporate Governance and Corporate Social Responsibility: Evidence from the Role of the Largest Institutional Blockholders in the Korean Market" Sustainability 12, no. 4: 1680. https://0-doi-org.brum.beds.ac.uk/10.3390/su12041680