Redefining the Supply Chain Model on the Milicz Carp Market

1

Faculty of Life Sciences and Technology, Institute of Economics Sciences, Wrocław University of Environmental and Life Sciences, 50-375 Wroclaw, Poland

2

Faculty of Law, Administration and Economics, Institute of Economics Sciences, University of Wrocław, 50-137 Wrocław, Poland

*

Author to whom correspondence should be addressed.

Sustainability 2020, 12(7), 2934; https://0-doi-org.brum.beds.ac.uk/10.3390/su12072934

Submission received: 9 February 2020

/

Revised: 28 March 2020

/

Accepted: 31 March 2020

/

Published: 7 April 2020

(This article belongs to the Special Issue Agricultural Value Chains: Innovations and Sustainability)

Abstract

:The growing demand for cheap food is a key factor in maintaining long supply chains. Increasing the distance between the producer and the consumer results not only in certain problems in maintaining profitability by small, local producers, but also in a threat to food safety. One way to counteract these adverse effects is to sell food through short supply chains. They shape the market in the direction of maintaining care for the sustainable development of all food production, but above all, maintaining and strengthening the production capacity ensuring the transparency of the high-quality food production process from an identifiable source of origin. The purpose of this article is to indicate the conditions on the side of both carp producers and consumers, conducive to building short supply chains, and determine whether they can be an effective alternative sales model in Polish conditions. The article focuses on the possibilities of developing short supply chains on the carp market in the Barycz Valley, concentrating the largest area of carp ponds in Europe. The research (surveys) included the five largest fishing farms and, on the recipient side, individual consumers and restaurants located in the Barycz Valley and Wrocław, and agritourism facilities in the researched area. The obtained results confirmed that short supply chains in the area of Polish aquaculture are characterized by high implementation potential. However, it is necessary to modify the current sales model so that the producers’ expectations regarding the sales volume and the obtained price are balanced with the expectations of consumers articulating the will to buy fish at a given time, place, and price. This, in turn, will ensure the high economic efficiency of fishing farms, and consumers will have access to a high-quality product.

1. Introduction

As a result of the increasing processes of land and capital concentration, strong competition, and the demand for cheap food, the dominant form of food distribution is based on long supply chains. However, there are alternative development paths for the agri-food sector that can lead to sustainable local development which does not disturb the balance between the social-environmental and economic spheres. One of the systems is short food supply chains. Its development is becoming extremely important, not only because of the care for sustainable development of the sector, but first and foremost to maintain local production capacity ensuring a transparent high-quality food production process with a known source of origin.

In recent years, not only in the European Union but also around the world, we have been dealing with many different initiatives based on short food supply chains, such as direct sales on farms, ‘agricultural markets,’ online shopping carts, partnerships of producers and consumers. By organizing and supporting the activities of producers and consumers they visibly change the local food market shape. The impact of short supply chains on the increase in profitability of small farms involved in food production and processing is undeniable.

The emergence of short supply chains has also triggered a wide polemic about the premises and potential effects of their implementation, both among the interested parties themselves—mainly producers—but also scientists and researchers. Despite the prevailing opinions indicating the advantage of short supply chains over long ones, this form of sales still has its opponents and is treated rather as a supportive solution. One of the arguments raised in discussions with producers is the fear of costs disproportionate to the scale of production, generated for example by transporting products to the final recipient. Therefore, there is a strong need to conduct multidimensional research on short supply chains, both on the supply and demand side, in all areas of food production.

A review of available studies indicates a certain limitation of research to short supply chains of unprocessed and processed agricultural products. There is, however, a significant gap in research enabling the determination of short supply chains in aquaculture potential, which continues to largely rely on sales with multi-links chains. There are particularly few studies on the implementation and development of short supply chains by fisheries farms in Poland. Hence, all analyses of this phenomenon in Poland are extremely important.

This article presents the results of research conducted on the reconstruction of the current model of carp sales in the Barycz Valley in Poland, which is the largest area of carp ponds in Europe. They were dictated by the main research question: Can sales forms based on short supply chains be an effective alternative distribution model on the carp market?

The article aims to indicate the conditions on the side of both carp producers and consumers that favor the development of local sales systems based on short supply chains. The goal formulated in this way defined the structure of the article. Section 2 presents the theoretical aspects of short supply chains. An analysis of various types of studies (articles, reports) and documents regulating the scope and directions of the European Union policy towards short food supply chains was used here. Section 3 introduces the nature of the carp market in the Barycz Valley. The complexity of the researched area, which is reflected, among others, in the concentration of sales in the six largest fishing farms was emphasized here. The main part of the article is Section 4 describing the results of surveys conducted among the selected fish farms representing the supply side of the supply chain and among those creating demand: Individual consumers, restaurants, and agritourism facilities from the Barycz Valley area. Section 5 and Section 6 summarize the considerations, sequentially presenting discussion and conclusions.

The conclusions presented in the article result, first of all, from the analysis of specific fishing farms located in the Barycz Valley. Secondly, in relation to the demand side, they are formulated concerning recipient groups characterized by specific features determined by local, cultural, economic, and social factors. Research and conclusions, however, are a significant contribution to solving several problems in Polish aquaculture arising, among others, as results of changes in tastes, eating habits of consumers, and the progressing globalization opening the Polish carp market, also for other producers, e.g., from China or the neighboring Czech Republic. They can also be a kind of Polish voice in the discussion on the future of the European Union policy in the field of food safety.

2. The Concept of Short Food Supply Chains (SFSCs)

The concept of the supply chain can be generally defined as all processes that seek to change the location of the product in time and space, along with information shaping and optimizing these processes. In other words, it is a product-related business relationship network through which products move from production site to consumption [1]. Many approaches emphasize the role of the end customer (consumer)—who is a key link in the chain towards whom the products and services, starting from the source, through all the intermediate forms, flow.

There are many types of supply chains depending on the product specifics or industry, including flexible, lean, agile, fragile and sensitive, resilient, green, balanced, e-chain, and FMCG (fast moving consumer goods) supply chains. Their large diversity means that enterprises (producers) do not limit themselves to choose only one, but more often decide to diversify them [2]. Properly organized and analyzed in real-time is one of the most effective ways to optimize costs and improve the key financial indicators.

In the case of aquaculture products, long (with multi-links) or short (up to a maximum of one intermediary) chains can usually be discussed.

The first short food supply chains (SFSCs) conceptualizations were created at the turn of the century [3] and refer to three elements in the producer-consumer relationship: Face-to-face, spatial proximity, and spatially extended.

The European Commission has adopted the general definition of short food supply chain as a chain that includes a limited number of business entities involved in cooperation, drives local economic development, and is characterized by close geographical and social links between producers, processors, and consumers. In this approach, SFSCs require: “Horizontal and vertical cooperation between supply chain entities for the creation and development of short supply chains and local markets.” [4]. The Commission has made clear that support for the short supply chain creation only covers the supply chains in which no more than one intermediary is involved between the farmer and the consumer [5].

The interest of the European Commission in the SFSCs issue was reflected in one of the six priorities of the European Agricultural Fund for Rural Development for 2014–2020: “Promoting food chain organization and risk management in agriculture.” This priority enables the member states, among others, to shape the short supply chains [6]. Unfortunately, in Poland, the SFSCs concept became a priority only in 2017 [7]. Previously, they were not included in the Rural Development Program (RDP).

In the literature on the subject, SFSCs are defined differently. According to the French Agency for Environment and Energy Management ADEME [8], we can talk about short supply chains in two cases:

- When we deal with direct sales, or

- When we deal with a maximum of one intermediary, provided that the sale takes place within a range of up to 150 km.

In Italy, however, the short supply chains are only defined as ‘direct sales’ [9]. According to Migliore et al. [10], all SFSCs definitions have only one thing in common: They reduce the number of intermediaries between the food producer and the consumer while ensuring food safety for the consumer.

It is currently assumed that the main motive for shortening food supply chains is the need to [7]:

- Increase transparency—the food consumer knows exactly where the food comes from, how it was produced;

- Reduce costs to ensure a competitive price to the consumer while ensuring quality and continuity of supply;

- Increase producers’ income.

However, the results of in-depth research on SFSCs leads to the conclusion that the motives related to the implementation of sustainable development principles are also important, which also takes into account the impact of SFSCs on the social and environmental aspects [11,12] as well as the revitalization of the rural economy [13].

It is also worth emphasizing that in the literature on the subject more and more often the authors emphasize the importance of local government for the development of SFSCs [14]. According to Babczuk et al. [15], activities of local authorities aimed at creating short supply chains favor the development of local agriculture and have a positive impact on the increase of residents’ living standards in rural areas.

Summing up, it can be stated that both literature studies and own observations lead to the conclusion that there is no single, universal definition of SFSCs [16]. This is due to the fact that SFSCs systems should be constructed individually and should take account of the country’s (or region’s) socio-economic-political situation and the expected goals. Therefore, for the needs of the study, a short supply chain was defined by specifying the necessary conditions it should meet. The definition includes both the specificity of the carp market and the level of socio-economic development in Poland. As a result, it was assumed that SFSCs should have the following parameters [17]:

- The distance between the place of production and the place of sale may not exceed 100 km;

- There can be a maximum of one sales link, excluding commercial networks operating in many geographically dispersed locations;

- It is necessary to ensure constant, current, and up to date communication between the producer and the consumer, including the one regarding the source of the product.

3. The Carp Market in the Barycz Valley

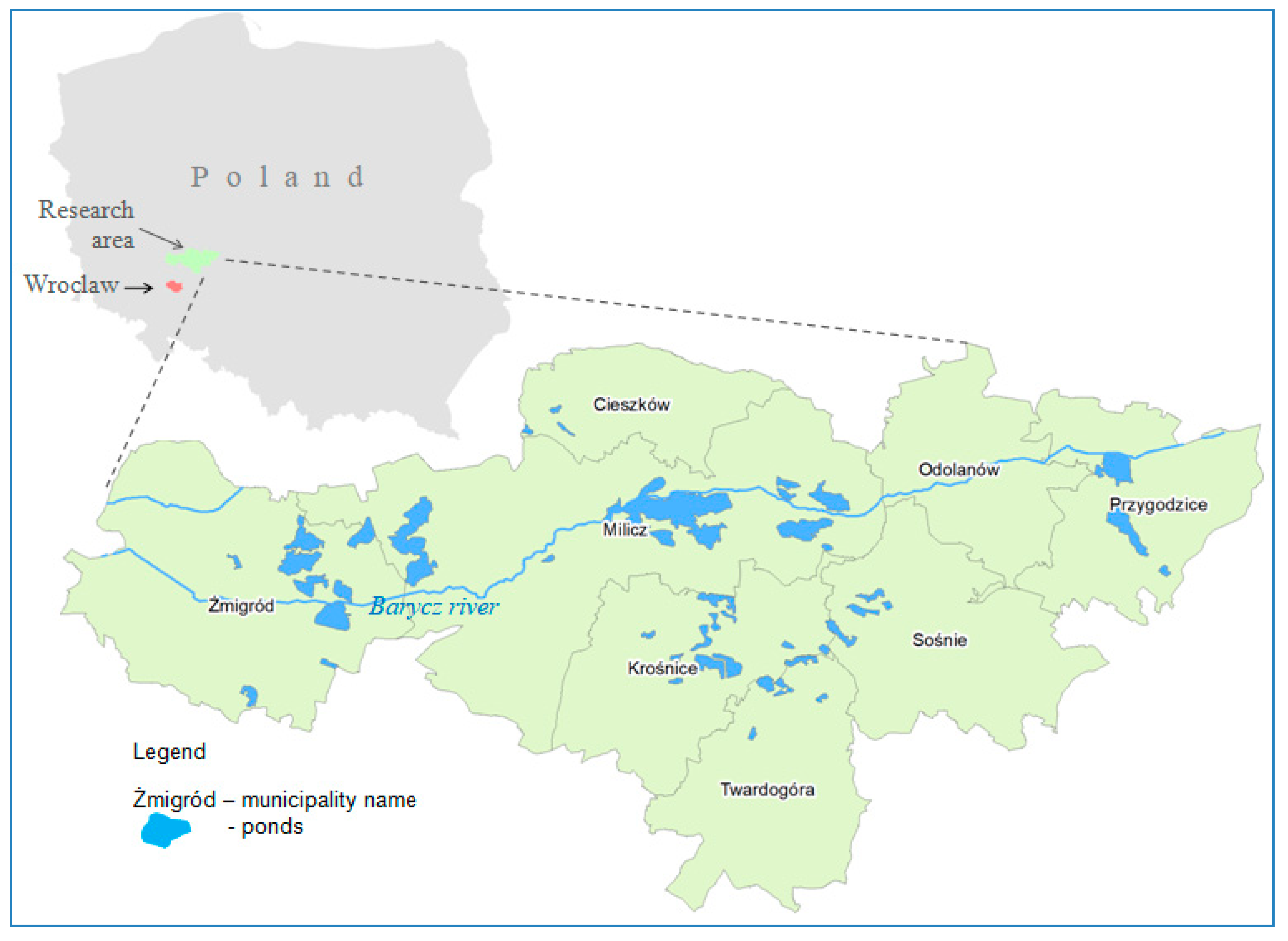

The Barycz Valley is located in the north-eastern part of the Lower Silesian Province and in the south-western part of the Greater Poland Province. It includes eight communes: Cieszków, Krośnice, Milicz, Twardogóra, and Żmigród in the territory of the Lower Silesian Province and Przygodzice, Odolanów, and Sośna in the territory of the Greater Poland Province, as shown in Figure 1.

Carp breeding (the flagship product of Polish aquaculture) has been conducted in these areas since the 11th century, which has influenced the region’s specificity. Currently, there are 26 fishing farms with a total area of 8253.45 ha, with permanent employment of 271 employees [18]. It is the largest carp breeding center in Europe.

Due to the intensification of globalization processes, long supply chains have become the dominant form of distribution in the Barycz Valley. However, recently several phenomena can be observed that have radically changed the carp market in Poland, and thus its supply chains. These are, among others [17]:

- Constantly spreading Koi herpes virus (KHV)—deadly to fish, but not dangerous to humans, which can lead to up to 70% of losses in carp breeding;

- Development of the population of legally protected fish-eating animals (mainly cormorants, but also white-tailed eagles, gray herons, white herons, minks, American minks, otters, raccoons, silver gulls, terns). Fishermen receive no financial compensation for the losses caused by these animals. Losses on this account are estimated from 10% to 50% of production depending on the region;

- Decreasing access to water, caused by global warming, lower average annual rainfall, decrease in groundwater level, with simultaneous irrational increase in the number of issued water and legal permits for establishing breeding districts;

- Restrictive environmental regulations—especially regarding fishing farms located within the Natura 2000 network;

- Institutional regulations—downtime in the payment of EU water and environmental subsidies in previous years and the introduced water tax;

- Increasing problems with the sale of live carp in Poland observed for years;

- Social campaigns such as ‘don’t buy live carp,’ which causes superrmarkets to gradually withdraw from the sale of live carp;

- Negative opinions that carp are oily, bony fish and ‘smell of silt’;

- Seasonality of consumption—80%–90% of total production is sold around the Christmas period, which is strongly associated with Polish tradition, in which carp is the basic dish on the Christmas table;

- The fact that only 8% of consumers buy carp directly from the producer [19].

These changes have become an inspiration for the diagnosis of existing supply chains on the Milicz carp market, along with an indication of how to rebuild them. Attention was primarily focused on the possibility to create a specific value based on cooperation between producers and final recipients.

4. Materials and Methods

The subject of the study, which constituted the basis for consideration, was the supply chains on the carp market in the Barycz Valley, where the largest area of carp ponds in Europe is located (the total area of breeding ponds there is 8253.45 ha) [18]. The research was conducted in the period between June and October 2019 in the form of surveys with representatives of fishing farms from the Barycz Valley area specializing in carp farming. Five fish farms were selected for the study, from the six largest in terms of production volume and the largest share in the regional carp market (Table 1). However, micro-fishing farms (i.e., those with less than 10 ha) were not included because the profile of fishing activities was not their main area of activity and most of the production was intended for self-supply.

The survey addressed to fisheries farms contained 30 open-ended and closed-ended questions. The questions concerned, among others: Availability of carp in the year-round offer, own carp processing, production volume, production costs, potential changes in production costs in connection with the introduction of the year-round carp offer, carp sales structure, barriers to the implementation of SFSCs. The research was conducted directly with the owners of fishing farms.

At the same time, the demand research was conducted, represented by open catering establishments, facilities providing agritourism services, and consumers as end-users. The survey covered:

- Sixteen restaurants offering fish, including five from the Barycz Valley and 11 from Wrocław (in both locations there are restaurants operating on the market from 1–5 years and over 5 years (four restaurants from the Barycz Valley, 10 from Wrocław). Virtually all offer dishes up to PLN 50 (10 from Wrocław, three from Barycz Valley), although in the case of the Barycz Valley two of the surveyed restaurants indicated a higher price point—up to PLN 100. The profile of the restaurant was defined: In the case of the Barycz Valley as regional cuisine (4), Wrocław—national, including Polish (7), and regional (3)).

- Ten agritourism facilities located in the Barycz Valley.

- A total of 139 consumers, including 108 residents of Wrocław (the largest city in the region).

The demand side studies were conducted using a survey. It was addressed to the restaurants and contained 16 questions, among which the closed-ended questions dominated. They concerned mainly the current offer of carp dishes and the possibility of extending the offer, as well as barriers related thereto. The survey addressed to agritourism farms contained 27 mostly closed-ended questions regarding, as in the case of the restaurants, the current and potential gastronomic offer of carp dishes. The consumer survey consisted of 23 questions. The results of the study were to determine the role of fish, especially carp, in the nutritional structure of consumers.

The research in restaurants and agritourism farms was performed in two stages. In the first stage, the survey was sent electronically, thus giving the respondents time to read the questions and gather the necessary data. Then a proper survey was conducted. In the case of consumers, the survey was taken using a questionnaire posted on the website.

As a supplement of the above research, in-depth interviews were conducted with people representing:

- Association Partnership for the Barycz Valley (Local Fisheries Group), promoting the consumption of carp all year round,

- Union of Fish Producers, lobbying for mutual contracts,

- Local government at the municipal level from the Barycz Valley area.

Based on the source material collected, the profitability of carp sales to various types of recipients was also assessed, namely: retail customers, supermarkets, and intermediaries. Due to the limited availability of financial data, a full simulation was performed only in the case of three farms.

To sum up, the research was primary and covered both the supply and demand side. The obtained results were used, firstly, to identify the existing supply chain, and secondly - to develop a new, desired delivery model.

5. Results

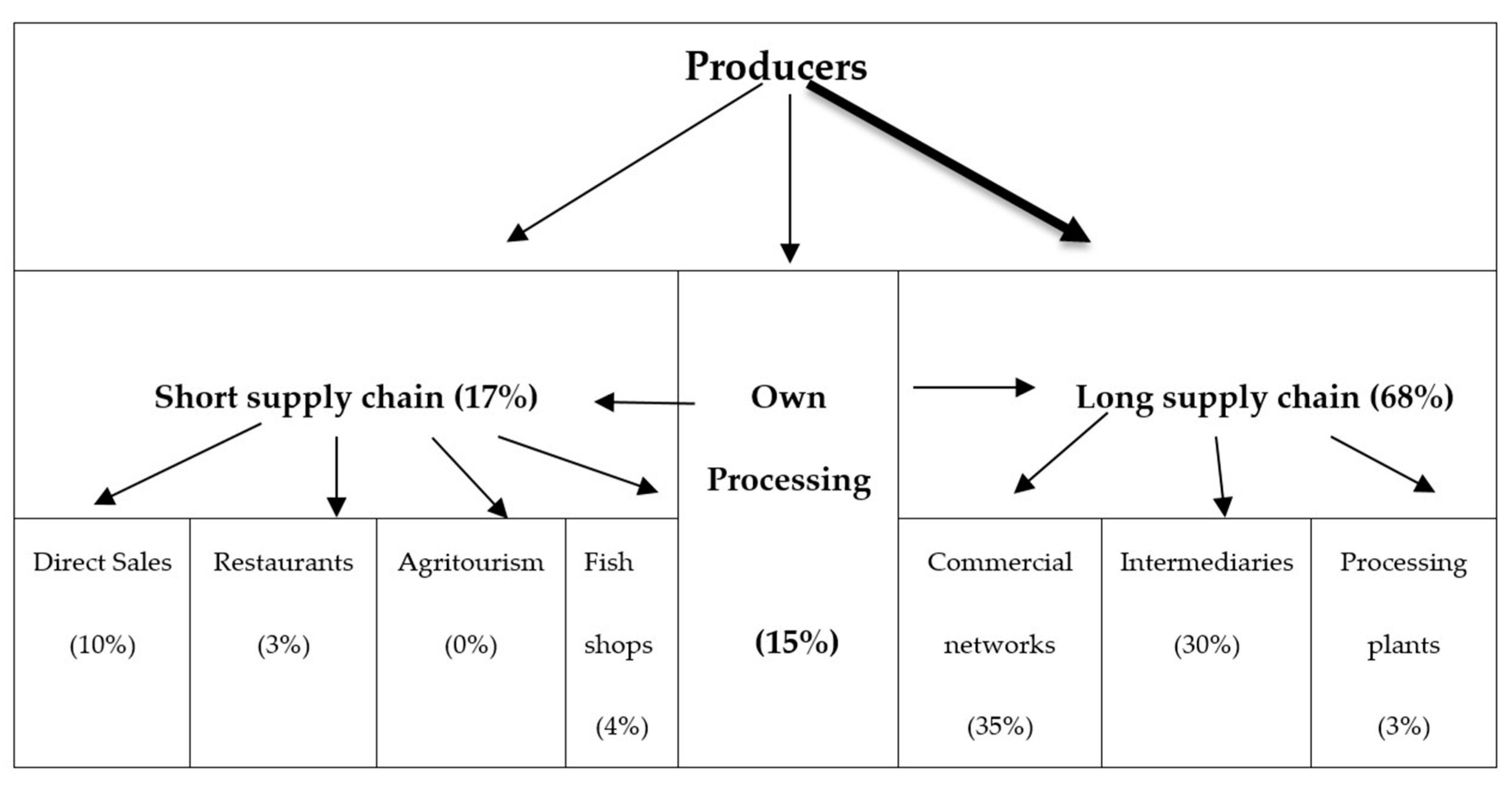

As the analysis of the obtained research results indicates, the dominant is the long supply chain. Around 68% of the Milicz carp production is sold through it. The short one, on the other hand, serves only 17%, mainly through direct sales to consumers. Processing also does not constitute a significant market share (Figure 2).

Table 2 presents the average sales prices in particular supply chains.

It is worth emphasizing that among the links in the long supply chain, retail chains (including supermarkets) and intermediaries are dominating. This is because carp is primarily sold as live fish or in the form of fillets. There is a lack of processed food produced from carp. From an economic point of view, the current state should be assessed negatively. The dominant carp economy is of the raw material character and does not create added value, which is so important from the point of view of the local, regional, and national development. Besides, it should be emphasized that the need to transport carp negatively affects the state of the natural environment, contributing to the phenomenon of so-called low emissions.

The dominance of ‘long distribution’ is the result of several factors, including the following:

- Seasonality of consumption resulting from the Polish tradition—the concentration of consumption falls on the Christmas period (80%–90% of carp sales) and thus a short period of generating income for farms;

- Poorly developed own processing;

- Atrophy and negative image of fish stores—as a result, these stores do not generate adequate demand for carp;

- Poorly developed direct sales channel—resulting from both consumer attitudes and previous experience of fishing farms.

As emphasized above, the advantage sources of a long supply chain can be primarily found in the traditional attitudes of consumers and producers. Intermediaries in whose interest it is to preserve the current status quo also play an important role. However, they are not the main obstacle hindering the transformation of existing chains.

The negative consumers’ attitudes from the perspective of the possibility of functioning short supply chains on the carp market were reflected in the results of conducted surveys. Although 79% of respondents declared they consume carp, they usually do so only at Christmas (63% of respondents). Only less than 1% of respondents consume carp regularly. It is worth noting that about 21% of respondents do not consume carp at all. At the same time, surveys show that carp was most often purchased in large stores (supermarkets/discount stores), 25.2% of respondents indicated the above answer. Less often, carp was supplied at the marketplace (18%), directly at the fishing farm (13.7%), or in the local store (11.5%). Interestingly, currently 52.5% of respondents are not (or rather not) interested in buying carp themselves directly from producers.

Research shows that an important barrier to implementing short supply chains is the weakness of links such as restaurants, agritourism farms, and fish shops. This is especially visible in the case of restaurants. These entities do not regularly offer carp on their menus, which does not properly stimulate demand and does not shape the tastes and eating habits of consumers.

The above statement is confirmed by the results of surveys. Only seven out of 11 surveyed restaurants located in Wrocław offered carp dishes, but only three of them served carp delivered from local fishing farms. The main reasons given for this situation were: Lack of demand reported by customers for carp dishes, as well as seasonality and lack of boneless carp (filleted). Opinions of restaurateurs correspond with the results of consumer surveys. Only about 4% of surveyed consumers eat carp in a restaurant.

As a result, about 3% of the total carp production goes to restaurants, while the share of agritourism farms is virtually zero. Carp is also not present in the menu of kindergartens or schools. The reasons for this condition should be seen not so much in the price of the carp as in the fact that there is a lack of fish fillets, and for safety reasons fish with bones cannot be given to children. Additionally, the introduction of carp in pre-school and school meals is not conducive to the law itself. The recommendations contained in the relevant Ordinance of the Minister of Health of 2016 assume the inclusion of a greater amount of only fatty marine fish in meals due to the presence of omega-3 fatty acids [20].

Fish shops are also a weak link in the carp supply chain to the consumer, where only 4% of the total carp caught is sold. Unfortunately, this is a much-underestimated link that, if used properly, can be an alternative to the large commercial networks. The strength of such stores should, however, be a permanent relationship with fishing farms, based on trust, loyalty, and guaranteed high quality of offered products.

The potential for direct sales, especially initiated at fish farms, is also unused. It is worth noting here that the financial simulations show that retail sales were the most profitable. This profitability was from 38.5% to 56.6%. In the case of sales to supermarkets, the profitability rate ranged from 27.3% to 43.0%, and in the case of intermediaries from 20.9% to 47.8%. The above analyses lead to the general conclusion that the extension of the supply chain negatively affects the profitability of sales, as shown in Table 3.

The confrontation of the real prices per kilogram of carp with consumer expectations expressed in surveys seems interesting. As can be seen from the table above, the sale price of carp to retail consumers ranged from PLN 13/kg in Farm 2 to PLN 15/kg in Farm 1. At the same time, surveys show that for carp purchased from a producer, consumers can pay an average of PLN 15, and PLN 20 for home delivery. This leads to the conclusion that for Farms 2 and 3 the price can be increased, which will further increase the profitability of direct sales.

Another problem, but not less important, is the poor development of their own processing. Still underestimated, mainly due to the relatively high capital intensity of investments, should in the future be an important factor strengthening short distribution channels. Unfortunately, the researched farms cooperated mainly with external fish processing plants, located outside the Lower Silesian Province. The nearest processing plant was 20 km from the fishing farm, while the furthest was 230 km away.

Besides, it should be emphasized that carps processed on fishing farms are sold, at least in part, using long supply chains, particularly via commercial networks. The above situation needs to be changed. Processed carp should first reach mass caterers and local consumers.

By confronting the current state of the Milicz carp supply chain with the observed changes (both on the demand and supply side), the thesis can be formulated that the main destimulants of the development of short distribution channels will be gradually weakening. According to the authors, this is due to several fundamental premises, namely [2]:

- Growing problems with the sale of live carp forcing fishing farms to search for new, alternative distribution channels;

- Offer diversification, including the development of own processing;

- New trends in carp consumption (slow food, shock food);

- Umbrella stores development and the ‘return’ of carp to the fish shops offer;

- The need to protect the environment, which in the future will lead to an increase in transport costs, which will then further shorten the supply chain;

- Climate change, a bigger problem with access to water will force fishing farms to strive to increase production profitability by developing processing and looking for alternative distribution channels.

However, one should be aware that the transformations in the distribution of the Milicz carp will not take place without institutional support measures, especially from local self-government authorities. The role of local government is invaluable here. The authorities have the opportunity to generate additional and constant demand for carp from local producers through several healthy eating programs (shaping proper eating habits and reducing the incidence of diet-related diseases, e.g., abdominal obesity, especially among children and adolescents) in subordinate educational and nursing institutions, etc.

In-depth interviews with local municipal authorities from the Barycz Valley area have shown openness and the will to cooperate in promoting the idea of shortening the supply chain on the Milicz carp market.

These activities can also transfer into some other multidimensional benefits as part of implementing the concept of sustainable development, such as accelerating local economic development by increasing employment among the local community or enriching the natural environment (aquaculture does not contribute to the creation of natural ecosystems, but rather ‘agri-environmental systems’ inscribed in the natural ecosystem of greater range and complexity, which is always, to a greater or lesser extent, influenced by such activities [21]).

The diagnosis of the current supply chain of the Milicz carp became the starting point for undertaking work aimed at remodeling and shortening them. The impetus to take such a step is, on the one hand, the need to ensure and maintain high economic efficiency of fish farms in a changing environment, and on the other hand the need to facilitate consumers’ access to high-quality and healthy food. Not without significance is the fact that reasonably managed fisheries contribute to maintaining high environmental values of naturally valuable areas. It should be emphasized that most areas where fishing activities are conducted in the Barycz Valley are covered by the NATURA 2000 program as special bird protection areas. It also houses the largest ornithological reserve ‘Stawy Milickie’ and the largest Landscape Park in Poland ‘Barycz Valley.’

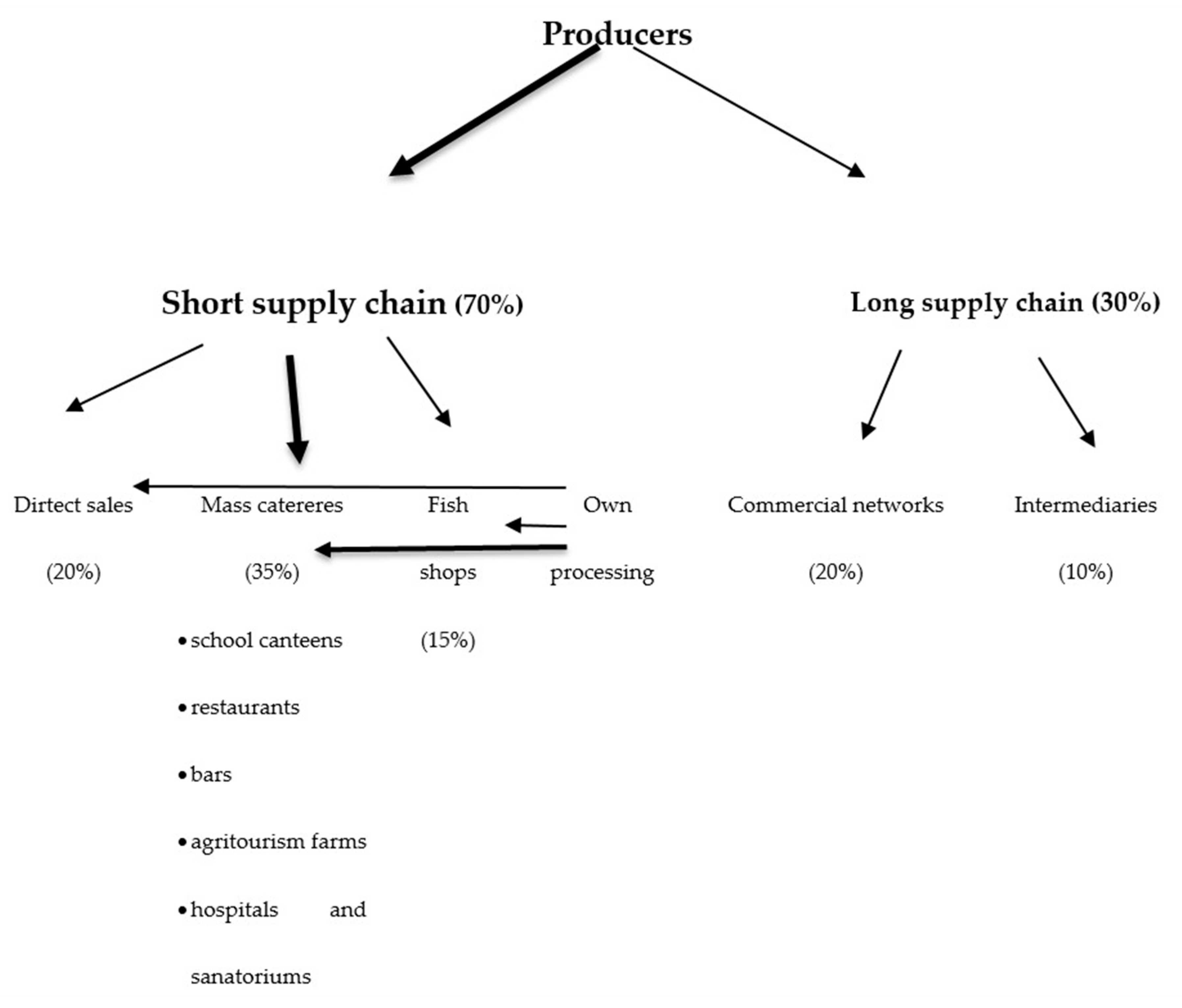

Chances for shortening the supply chain should be seen in increasing carp sales in the local and regional markets. The main generators of local (regional) demand should be broadly understood collective nutrition entities, fish shops, and individual consumers, supported by local authorities (Figure 3). Thus, short distribution channels can ‘handle’ about 70% of sales.

A necessary condition for short supply chains is to maintain a certain balance of producers’ expectations as to the volume of sales and the price obtained, and consumers who articulate the will to buy fish at a given time, place, and price. It should also be emphasized that the said transformation will take place gradually. The volume of generated production will continue to trigger sales via wholesalers and commercial networks. However, their role in distribution channels should be weakened, because of various social movements in defense of animal life and dignity.

6. Discussion

In recent years, the popularity and significance of short food supply chains as alternatives [22] and possibilities to solve some problems related to food safety issues [23] and conventional distribution systems has been constantly growing. This process allows the development of partner relations between producers and consumers and promotes the implementation of sustainable development principles [24,25,26].

Based on the conducted research, it can be concluded that the carp economy in the Barycz Valley has to face numerous challenges, economic, environmental, legislative, social, and image-related. Distribution in the model of short supply chains on the carp market is still just an addition to mass December sales, although there are more and more farms with a positive attitude to such solutions. On the other hand, the element that additionally stimulates the development of long supply chains in these markets is the small amount of local processing and dynamic development of transport within the global food industry network. Low transport charges further extend the roads between harvesting, processing, and consumers.

Discussion regarding the distribution of the Milicz carp goes far beyond the scope of this article. It focuses on many specific issues and problems for producers. Nevertheless, it is needed and inevitable, especially since there is a gap in the literature on the short supply chains regarding the carp market in Poland. Few publications that discuss the problem of shortening supply chains in aquaculture focus mainly on saltwater farms, or bypass the case of Poland [27,28]. In contrast, the pilot study by Raftowicz et al. [29], on carp supply chains in 2016 did not include consumers in the final research.

Little interest in both theoretical and practical problems of supply chains not only on the carp market but also on the freshwater fish market in general, is evidenced by the fact that no standard has yet been developed that would regulate its functioning. It is important that such a standard exists for marine fish. An example is the supply chain standard developed by the Marine Stewardship Council [30] which regulates the rules of catching and transporting fish so that the principles of sustainable development are met.

So far, the carp market has lacked studies analyzing supply chains from the perspective of their importance for the sustainable development. This article, by demonstrating that short supply chains are not only economically viable, but also positively influence the social and environmental spheres, partially bridges this gap.

Building a modern, competitive carp market cannot be based on the old habits of both producers and consumers. The partnership relations between the producer (fish farm) and the consumer, mentioned at the beginning, are becoming more and more important. Relationships based on consumer confidence in the manufacturer that the product delivered is the one we expect in terms of quality, source, and loyalty.

Unfortunately, long distribution channels are not conducive to the development of this type of behavior. However, they allow the transaction participants to remain anonymous, which promotes various types of distortions (selling fish from foreign farms as Milicz carp, financial benefits of intermediaries at the expense of producers and consumers, no guarantee of high-quality carp—lack of knowledge about the source, etc.). Additionally, the extension of supply chains negatively affects the natural environment by increasing environmental pollution because of the transport development.

At the same time, according to conducted research, carp processing is underdeveloped in the Barycz Valley. Carp is processed not only outside the analyzed area, but also outside of the Lower Silesian Province. As a result, the Barycz Valley and, more broadly, the province itself plays a raw material role, and to a limited extent in its area added value is generated. This situation has a negative impact on both regional and local development.

Short distribution channels are therefore extremely desirable, and not just because of cost rationalization. Their meaning is much deeper. In the era of growing uncertainty on the market and what cannot be underestimated by deep changes in the mentality and eating habits of consumers, they are one of the alternative solutions for rational business operations. On the other hand, it is a very difficult distribution channel. For it to exist and fulfil its role, one cannot forget about trust, communication, commitment of the parties, understanding expectations, cooperation, and interpersonal relations, i.e., all those elements that build social capital.

This article demonstrates that shortening the supply chain can be cost-effective for both producers and consumers. Besides, the development of processing can make aquaculture an important branch of development in the Lower Silesian Province. The fact that currently long supply chains dominate, and processing is located outside the province, means that aquaculture is treated marginally by regional authorities. This is confirmed by the lack of records on the development of aquaculture in such an important document as ‘Lower Silesia Green Valley of Food and Health,’ which sets the leading directions for the development of agriculture and food economy.

Further, it is worth emphasizing that short supply chains strengthen the food security of the area. Although this problem has been overlooked for years, the events of recent months confirm its importance.

Summing up, the considerations regarding the potential of short distribution channels on the Milicz carp market, it is worth presenting the conclusions that have been formulated by the completed research. Obviously, they cannot be generalized regarding all carp producers in Poland, and they do not illustrate the attitudes of most consumers. It can be assumed, however, that in-depth and extended research would not bring far-reaching results in relation to those presented.

7. Conclusions

Taking into consideration the conducted research, it can be concluded that the carp economy in the Barycz Valley has to face numerous challenges, including economic, environmental, legislative, social, and image-related. Changing trends on the carp market (in particular moving away from the sale of live fish) lead to a reflection that one of the future distribution models should be recognized in the development of short supply chains. However, at present, distribution in the short supply chain model on the carp market is still only an addition to mass December sales, although there are more and more households enthusiastic about such solutions. One of the crucial incentives for this transformation should be proven higher sales profitability. The conclusions and recommendations presented below can therefore be treated as a starting point while formulating alternative directions in which this market should go in the coming years.

The analyzed market is not yet fully shaped in terms of building partnerships. The undertaken cooperation is rather individual and is mostly initiated because of specific problems. The reasons for this can be seen in the insufficient (multilateral) exchange of information, and not only between producers themselves but also on the line of carp producers, potential buyers or producers, consumers associations, industry organizations, local authorities. Consequently, the state of specific ignorance fosters distrust, and thus a kind of isolation. As a result, fishing farms prefer regular and proven recipients, such as commercial networks and intermediaries guaranteeing the collection of large batches of fish. Although the price offered by intermediaries and commercial networks is lower than that offered by consumers, certainty of receipt and payment compensates for the income loss. Thus, it can be asserted that the activities of commercial networks and intermediaries reduce transaction costs, which are high in the conditions of direct sales (in the absence of trust).

The demand for carp is dispersed, diverse, and with unequal impact on processes in the supply chain itself. It is still not fully recognized (e.g., on the side of the restaurant, but also institutions such as kindergartens, schools, hospitals, sanatoriums). Consumer behavior is subject to rapid changes due to various factors (e.g., eating habits, promoted ecological attitudes protecting animals, natural disasters limiting supply, excessive imports e.g., from the Czech Republic or even China).

Dynamically changing attitudes of consumers, increasingly inclined to consume food produced in a traditional way by local producers, will even enforce shortening distribution channels. In addition, activist movements will force stores, including large retail chains, to withdraw live fish from the offer.

Open and closed nutrition catering establishments will play a significant role in creating new distribution channels. The element supporting this process should be the processing and involvement of local government authorities at various levels.

The involvement of local authorities will probably reduce the level of market uncertainty and thus reduce the transaction costs mentioned above. Additionally, through subordinate nutrition centers, local authorities may not only generate additional demand, but can also spread it over time, or contribute to reducing the problem of hyper seasonality.

Shortening the supply chain also requires action on the part of fisheries farms. They must develop their own processing and, to a greater extent, enter into cooperation with other farms, even as a part of network connections.

The transition from long to short supply chains on the Milicz carp market requires undertaking multifaceted activities in which producers, consumers, restaurateurs, local government units, public sector institutions, non-governmental institutions supporting agriculture, fisheries, and rural development should participate. Therefore, it seems reasonable to recommend [2]:

- Development of infrastructure enabling the consumption of carp in fish farms and other places located in communes;

- Obligatory introduction of the Milicz carp to the menu of school canteens subordinated to local government units;

- Establishing a network of patronage fish shops operating under the joint name of ‘carp from the Barycz Valley area’;

- Propagating the idea of healthy nutrition based on the nutritional values of carp.

It is worth emphasizing once again the place of distribution channels in business operations. Extremely fast changes in the market environment, which are not only caused by the carp producers, even force us to think differently about the ‘path to reach’ the final recipient. Distribution ceased to be seen through the prism of a simple function related to the flow of goods and products. It is considered as a systematic approach to create, by all its participants, a common value for the final customer. Still, regardless of the chain length, it will remain an individual structure, located in specific conditions, characterized by a unique resource in the form of the specificity of a given company, its location, adopted strategy, features of manufactured products, forms of cooperation with other entities, and specific buyer segments.

Author Contributions

Conceptualization, M.R., M.K.-M. and M.S.; methodology, M.R., M.K.-M. and M.S.; validation, M.R., M.K.-M. and M.S.; formal analysis, M.R., M.K.-M. and M.S.; resources, M.R., M.K.-M. and M.S.; data curation, M.R., M.K.-M. and M.S.; writing—original draft preparation, M.R., M.K.-M. and M.S.; writing—review and editing, M.R., M.K.-M. and M.S.; visualization, M.R. and M.S; supervision, M.R., M.K.-M. and M.S.; project administration, M.R.; funding acquisition, M.R. and M.K.-M. All authors have read and agreed to the published version of the manuscript.

Funding

The research is co-financed under the pro-development project B011/0010/20 from Wrocław University of Environmental and Life Sciences.

Conflicts of Interest

The authors declare no conflict of interest.

References

- De Silva, D. Value chain of fish and fishery products: Origin, functions and application in developed and developing country markets. Food Agric. Organ. 2011, 63, 1–53. [Google Scholar]

- Raftowicz, M.; Kalisiak-Mędelska, M.; Kurtyka-Marcak, I.; Struś, M. Short Supply Chains on the Example of the Milicz Carp; CeDeWu: Warszawa, Poland, 2019. [Google Scholar]

- Marsden, T.; Banks, J.; Bristow, G. Food supply chain approaches: Exploring their role in rural development. Sociol. Rural. 2000, 40, 424–438. [Google Scholar] [CrossRef]

- Official Journal of the European Union, Regulation (EU) No 1305/2013 of the European Parliament and of the Council of 17 December 2013 on support for rural development by the European Agricultural Fund for Rural Development (EAFRD) and repealing Council Regulation (EC) No 1698/2005. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32013R1305&from=EN (accessed on 31 March 2020).

- Official Journal of the European Union, Commission Delegated Regulation (EU) No 807/2014 of 11 March 2014 supplementing Regulation (EU) No 1305/2013 of the European Parliament and of the Council on support for rural development by the European Agricultural Fund for Rural Development (EAFRD) and introducing transitional provisions, art. 11. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014R0807&from=en (accessed on 31 March 2020).

- Local Agriculture and Short Food Supply Chains. Available online: https://epthinktank.eu/2013/10/14/local-agriculture-and-short-food-supply-chains/ (accessed on 31 March 2020).

- Serafin, R. Bariery i szanse dla rozwoju systemów KŁŻ dla potrzeb Kampanii “Wiedz i Mądrze Jedz” [Barriers and Opportunities for the Development of KŁŻ Systems for the needs of the ‘Know and Eat Smartly’ Campaign], an Expertise under National Rural Network No. 2/2018/038. 2018. Available online: http://faow.org.pl/wp-content/uploads/2018/12/4-BarierySzanse_15102018.pdf (accessed on 31 March 2020).

- French Agency for Environment and Energy Management, ADEME. 2012. Available online: http://www.ademe.fr/sites/default/files/assets/documents/avis_ademe_circuits_courts_alimentaires_proximite_avril2012.pdf (accessed on 31 March 2020).

- Kapała, A. Short food supply chains in the EU Law. In Food Security, Food Safety, Food Quality, Current Developments and Challenges in European Union Law; Härtel, I., Budzinowski, R., Eds.; Hart Publishing: Oxford, UK; Nomos: Baden-Baden, Germany, 2016. [Google Scholar]

- Migliore, G.; Schifani, G.; Cembalo, L. Opening the black box of food quality in the short supply chain: Effects of conventions of quality on consumer choice. Food Qual. Prefer. 2015, 39, 141–146. [Google Scholar] [CrossRef]

- Canfora, I. Is the short food supply chain an efficient solution for sustainability in food market? Agric. Agric. Sci. Procedia 2016, 8, 402–407. [Google Scholar] [CrossRef] [Green Version]

- De Fazio, M. Agriculture and sustainability of the welfare: The role of the short supply chain. Agric. Agric. Sci. Procedia 2016, 8, 461–466. [Google Scholar] [CrossRef] [Green Version]

- Forssell, S.; Lankoski, L. The sustainability promise of alternative food networks: An examination through “alternative” characteristics. Agric. Human Values 2014, 32, 63–75. [Google Scholar] [CrossRef] [Green Version]

- Raftowicz, M.; Kalisiak-Mędelska, M.; Kachniarz, M. The Influence of Local Government on the Development of Short Food Supply Chains. In Proceedings of the Conference Proceedings of the Boston Conference Series–November 2019; FLE Learning Ltd.: Ryde, UK, 2019; pp. 69–74. [Google Scholar]

- Babczuk, A.; Kachniarz, M.; Piepiora, Z. Work Efficiency of Local Government. In Proceedings of the 15th International Scientific Conference on Hradec Economic Days 2017, Hradec Králové, Czech Republic, 31 January–1 February 2017; Volume 7, pp. 20–28. [Google Scholar]

- Kneafsey, M.; Venn, L.; Schmutz, U.; Balázs, B.; Trenchard, L.; Eyden-Wood, T.; Bos, E.; Sutton, G.; Blackett, M. Short Food Supply Chains and Local Food Systems in the EU. A State of Play of Their Socio-Economic Characteristics; European Commision: Brussels, Belgium, 2013. [Google Scholar]

- Raftowicz, M.; Struś, M.; Wodnicka, M. The Need to Rebuild the Food Supply Chain. In Knowledge on Economics and Management: Profit or Purpose Conference Proceedings; Talášek, T., Stoklasa, J., Slavícková, P., Eds.; Palacký University Olomouc: Olomouc, Czech Republic, 2019; pp. 227–232. [Google Scholar]

- Community-led Local Development Strategy (CLLD) for the Barycz Valley for the years 2016–2022. Available online: http://projekty.barycz.pl/files/?id_plik=1971 (accessed on 31 March 2020).

- Czarkowski, T.K.; Stabiński, R. Description, preferences, and opinions of consumers who buy fish directly from fisheries enterprises. Fish. Announc. 2015, 1, 1–6. [Google Scholar]

- Ministerstwo Zdrowia [Ministry of Health]. Rozporządzenie Ministra Zdrowia z dnia 26 lipca 2016 r. [Ordinance of the Minister of Health of July 26, 2016]; Dz. U. z 2016 r. [Journal of Laws of 2016], item 1154. Available online: http://prawo.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU20160001154 (accessed on 31 March 2020).

- Gil, F.M. Natura 2000 and Aquaculture; Ministry of the Environment: Warszawa, Poland, 2009; p. 13. [Google Scholar]

- Mancini, M.C.; Menozzi, D.; Donati, M.; Biasini, B.; Veneziani, M.; Arfini, F. Producers’ and Consumers’ Perception of the Sustainability of Short Food Supply Chains: The Case of Parmigiano Reggiano PDO. Sustainability 2019, 11, 721. [Google Scholar] [CrossRef] [Green Version]

- Todorovic, V.; Maslaric, M.; Bojic, S.; Jokic, M.; Mircetic, D.; Nikolicic, S. Solutions for More Sustainable Distribution in the Short Food Supply Chains. Sustainability 2018, 10, 3481. [Google Scholar] [CrossRef]

- Vittersø, G.; Torjusen, H.; Laitala, K.; Tocco, B.; Biasini, B.; Csillag, P.; de Labarre, M.D.; Lecoeur, J.-L.; Maj, A.; Majewski, E.; et al. Short Food Supply Chains and Their Contributions to Sustainability: Participants’ Views and Perceptions from 12 European Cases. Sustainability 2019, 11, 4800. [Google Scholar] [CrossRef] [Green Version]

- Nagy-Pércsi, K. Food safety requirements in case of short food supply chain. Studia Mundi-Economica 2018, 5, 79–86. [Google Scholar]

- Galli, F.; Brunori, G. (Eds.) Short Food Supply Chains as Drivers of Sustainable Development. Evidence Document; Document Developed in the Framework of the FP7 Project FOODLINKS (GA No. 265287. Laboratorio di studi rurali Sismondi); 2013; Available online: https://orgprints.org/28858/1/evidence-document-sfsc-cop.pdf (accessed on 31 March 2020).

- FAO Fisheries and Aquaculture Technical Paper. Value Chain Dynamics and the Small-Scale Sector Policy Recommendations for Small-Scale Fisheries and Aquaculture Trade; FAO: Rome, Italy, 2014. [Google Scholar]

- European Market Observatory for Fisheries and Aquaculture Products. Price Structure in the Supply Chain for Fresh Carp in Central Europe; Maritime Affairs and Fisheries: Brussels, Belgium, 2016. [Google Scholar]

- Raftowicz, M.; Le Gallic, B. Inland aquaculture of carps in Poland: Between tradition and innovation. Aquaculture 2020, 518, 1–8. [Google Scholar] [CrossRef]

- Marine Stewardship Council Fisheries Standard and Guidance v2.01, Version 2.01. 31 August 2018. Available online: https://www.msc.org/docs/default-source/po-files/certyfikacja-lancucha-dostaw/standard-lancucha-dostaw-msc---wersja-podstawowa---v-5-0---2019.pdf?sfvrsn=83373a75_20 (accessed on 31 March 2020).

Figure 1.

Map of the Barycz Valley.

Figure 2.

Share of the short and long supply chains on the Milicz carp market. Source: [2].

Figure 2.

Share of the short and long supply chains on the Milicz carp market. Source: [2].

Figure 3.

An alternative share distribution of the short and long supply chains of the Milicz carp. Source: [2].

Figure 3.

An alternative share distribution of the short and long supply chains of the Milicz carp. Source: [2].

{kind=link}

{kind=link}

{kind=link}

Table 1.

Characteristics of researched fishing farms.

| Year of Establishment | Farm Area [in ha] | Water Surface [in ha] | Average Annual Production Volume on the Farm [in tones] | Production Costs of 1 kg of Carp [in PLN/kg] | Annual Sales around Christmas Time [in %] | |

|---|---|---|---|---|---|---|

| Farm 1 | 1980 | 141 | 101 | 70 | 6.5 | 90 |

| Farm 2 | 1998 | 320 | 285 | 160 | 8 | 90 |

| Farm 3 | 1991 | 175 | 166 | 53 | 8.3 | 95 |

| Farm 4 | 1989 | 10 | 10 | 35 | 5 | 34 |

| Farm 5 | 1990 | 30 | 20 | 100 | 14 | 80 |

Source: Own study based on surveys. 1 EUR = 4.3 PLN (polish zloty).

Table 2.

Average sales prices in particular supply chains [in PLN/kg].

| Retail Customers— Direct Sales | Supermarkets | Fish Shops | Restaurants | Own Fisheries | Processing Plants | Intermediaries |

|---|---|---|---|---|---|---|

| 14 | 11.625 | 11.66 | 12.5 | 12 | 9.25 | 11 |

Source: Own study based on surveys. 1 EUR = 4.3 PLN (polish zloty).

Table 3.

Analysis of income, cost, profit, and sales profitability on Farms 1, 2, 3, and 4.

| Farm 1 | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Specifications | Unit of Measure | Retail Customer | Supermarkets | Intermediaries | ||||||||||

| Revenue = price/kg × sale (production x% share in sales) | PLN | 15 × 7000 = 105,000 | 11.50 × 42,000 = 483,000 | 11.5 × 21,000 = 241,500 | ||||||||||

| Cost = Cost of 1 kg × sale | PLN | 6.5 × 7000 = 45,500 | 6.5 × 42,000 = 273,000 | 6.5 × 21,000 = 136,500 | ||||||||||

| Profit on sales = income − costs | PLN | 59,500 | 483,000 – 273,000 = 210,000 | 115,500 | ||||||||||

| Profitability of sales profit/income × 100% | % | 56.6 | 43 | 47.82 | ||||||||||

| Farm 2 | ||||||||||||||

| Specifications | Unit of measure | Retail customer | Supermarkets | Fish shops | Restaurants | Intermediaries | ||||||||

| Revenue = price/kg × sale (production x% share in sales) | PLN | 13 × 16,000 = 208,000 | 11 × 48,000 = 528,000 | 11 × 16,000 = 176,000 | 13 × 16,000 = 208,000 | 11.5 × 48,000 = 552,000 | ||||||||

| Cost = Cost of 1 kg x sale | PLN | 8 × 16,000 = 128,000 | 8 × 48,000 = 384,000 | 8 × 16,000 = 128,000 | 8 × 16,000 = 128,000 | 8 × 48,000 = 384,000 | ||||||||

| Profit on sales = income − costs | PLN | 80,000 | 144,000 | 48,000 | 80,000 | 168,000 | ||||||||

| Profitability of sales profit/income × 100% | % | 38.46 | 27.27 | 27.27 | 38.46 | 30.43 | ||||||||

| Farm 3 | ||||||||||||||

| Specifications | Unit of measure | Retail customer | Supermarkets | Fish shops | Own fisheries | Intermediaries | ||||||||

| Revenue = price/kg × sale (production x% share in sales) | PLN | 14 × 2650 = 37,100 | 12 × 5300 = 63,600 | 12 × 2650 = 31,800 | 12 × 2650 = 31,800 | 10.5 × 33,920 = 356,160 | ||||||||

| Cost = Cost of 1 kg x sale | PLN | 8.3 × 2650 = 21,995 | 8.3 × 5300 = 43,990 | 8.3 × 2650 = 21,995 | 8.3 × 2650 = 21,995 | 8.3 × 33,921 = 281,544.3 | ||||||||

| Profit on sales = income − costs | PLN | 15,105 | 19,610 | 9805 | 9805 | 74,615.7 | ||||||||

| Profitability of sales profit/income × 100% | % | 40.71 | 30.83 | 30.83 | 30.83 | 20.95 | ||||||||

| Farm 4 | ||||||||||||||

| Specifications | Unit of measure | Supermarkets | Own smokehouse | Wholesalers | ||||||||||

| Revenue = price/kg x sale (production x% share in sales) | PLN | 12 × 13,300 = 159,600 | 12,250 | 9450 | ||||||||||

| Cost = Cost of 1 kg × sale | PLN | 5 × 13,300 = 66,500 | Nd | Nd | ||||||||||

| Profit on sales = income − costs | PLN | 93,100 | Nd | Nd | ||||||||||

| Profitability of sales profit/income × 100% | % | 58.33 | Nd | Nd | ||||||||||

Source: Own study based on surveys. 1 EUR = 4.3 PLN. There is no data for Farm 5.

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Raftowicz, M.; Kalisiak-Mędelska, M.; Struś, M. Redefining the Supply Chain Model on the Milicz Carp Market. Sustainability 2020, 12, 2934. https://0-doi-org.brum.beds.ac.uk/10.3390/su12072934

AMA Style

Raftowicz M, Kalisiak-Mędelska M, Struś M. Redefining the Supply Chain Model on the Milicz Carp Market. Sustainability. 2020; 12(7):2934. https://0-doi-org.brum.beds.ac.uk/10.3390/su12072934

Chicago/Turabian StyleRaftowicz, Magdalena, Magdalena Kalisiak-Mędelska, and Mirosław Struś. 2020. "Redefining the Supply Chain Model on the Milicz Carp Market" Sustainability 12, no. 7: 2934. https://0-doi-org.brum.beds.ac.uk/10.3390/su12072934

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.