Supreme Audit Institutions and Sustainability of Public Finance. Links and Evidence along the Economic Cycles

,

,  ,

,  , and

, and

Abstract

:1. Introduction

2. Literature Review

2.1. Sustainability of Public Finances

2.2. Supreme Audit Institutions

2.3. The SAIs and Public Finances Sustainability

3. Methodology

- -

- concern for selecting a period of analysis not exposed to major transformations; 2002 is the year of single currency introduction in 12 of the 15 Member States; The largest EU expansion took place in 2004, but the ten new states had been already engaged in ensuring the stability of institutions guaranteeing democracy, the rule of law, and human rights;

- -

- availability of data at the time of database construction.

- -

- Government deficit/surplus, debt, and associated data (GDS). EUROSTAT [72] and ONS [73] calculate this indicator as a proportion of net lending (+)/net borrowing (−) to the total gross domestic product. The indicator is given a positive or negative value depending on whether the budget execution ends with a surplus or deficit. This indicator was selected to emphasize solvability (defined as the government’s capacity to pay its financial obligations [28]), one of the four dimensions of public finance sustainability. According to the Maastricht Treaty, the reference value for this indicator is 3%.

- -

- General governmental gross debt (GGGD). According to the EUROSTAT [72] and ONS [73] methodology, public debt includes the elements of gross liability in cash and deposits, debt instruments, and loans that exist at the end of the year in the public administration sector, calculated at nominal value and consolidated. This indicator was selected to assess fairness (defined as the government’s capacity to pay its current obligations without transferring its costs to future generations [28]), one of the four dimensions of public finance sustainability. This indicator reflects the size of public debt as a percentage in GDP, and it is representative of the entire public administration sector (it includes both the government’s and central public administration’s debts, as well as the debts of local administration and social security funds). According to the Maastricht Treaty, the reference value for this indicator is 60%.

- -

- Government effectiveness (GE). According to the World Bank [76], this indicator measures the degree of satisfaction of citizens with the public services provided by the state and the degree of independence in the exercise of public office from political interference. The estimation of this indicator is a score situated in the interval of standard distribution between [−2.5, 2.5]. The introduction into the analysis of this indicator aimed to assess the degree to which SAIs, through their organizational structures and quality of activities, ensures the fair use of public resources.

- -

- Control of corruption (CC). Calculated by the World Bank [76], the degree to which political power is diverted to serve individual/private group interests and the degree to which the state is “captured” by elite and private interests. The estimation of this indicator is a score situated in the interval of standard distribution [−2.5, 2.5].

4. Results and Discussion

- -

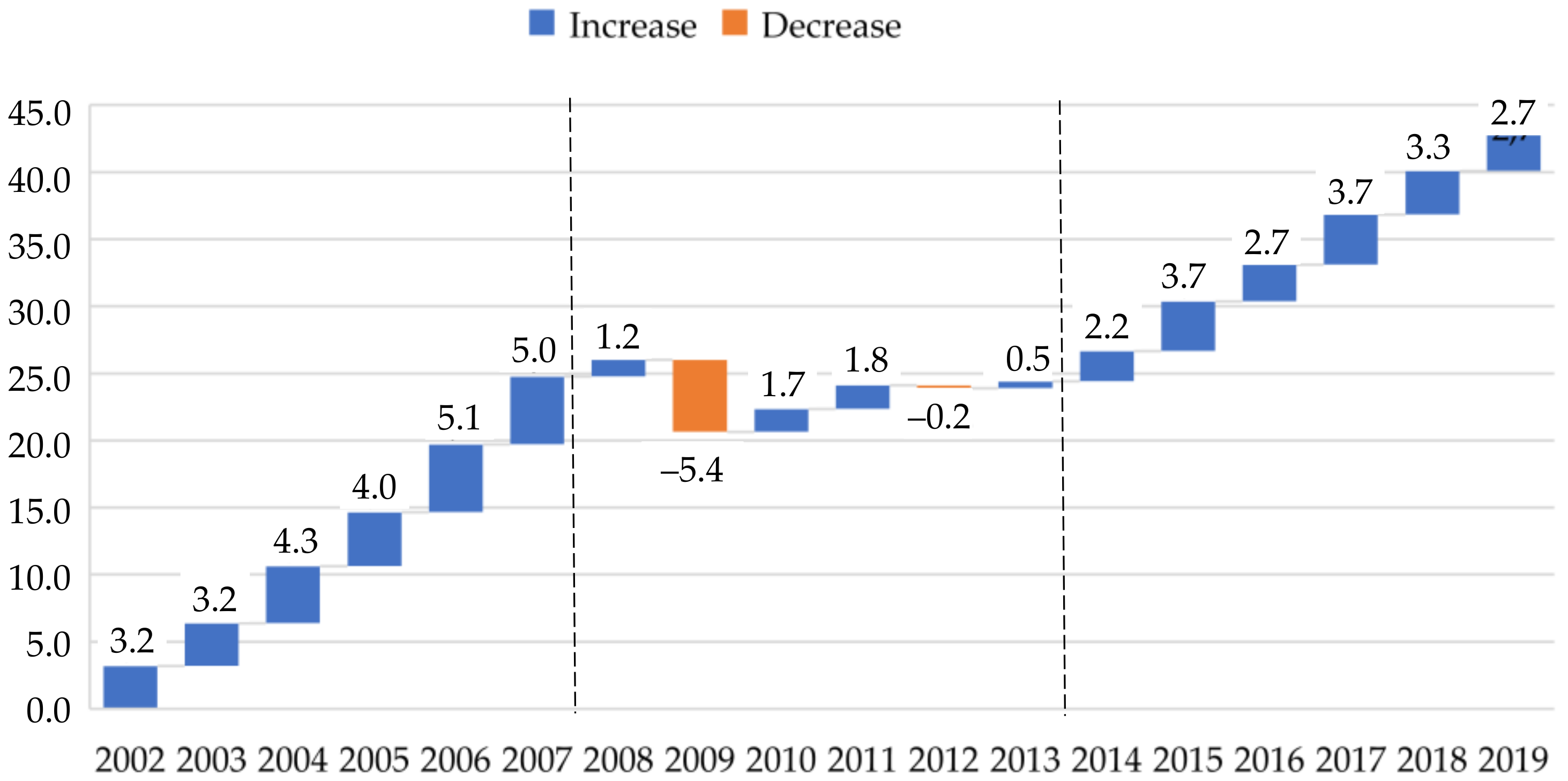

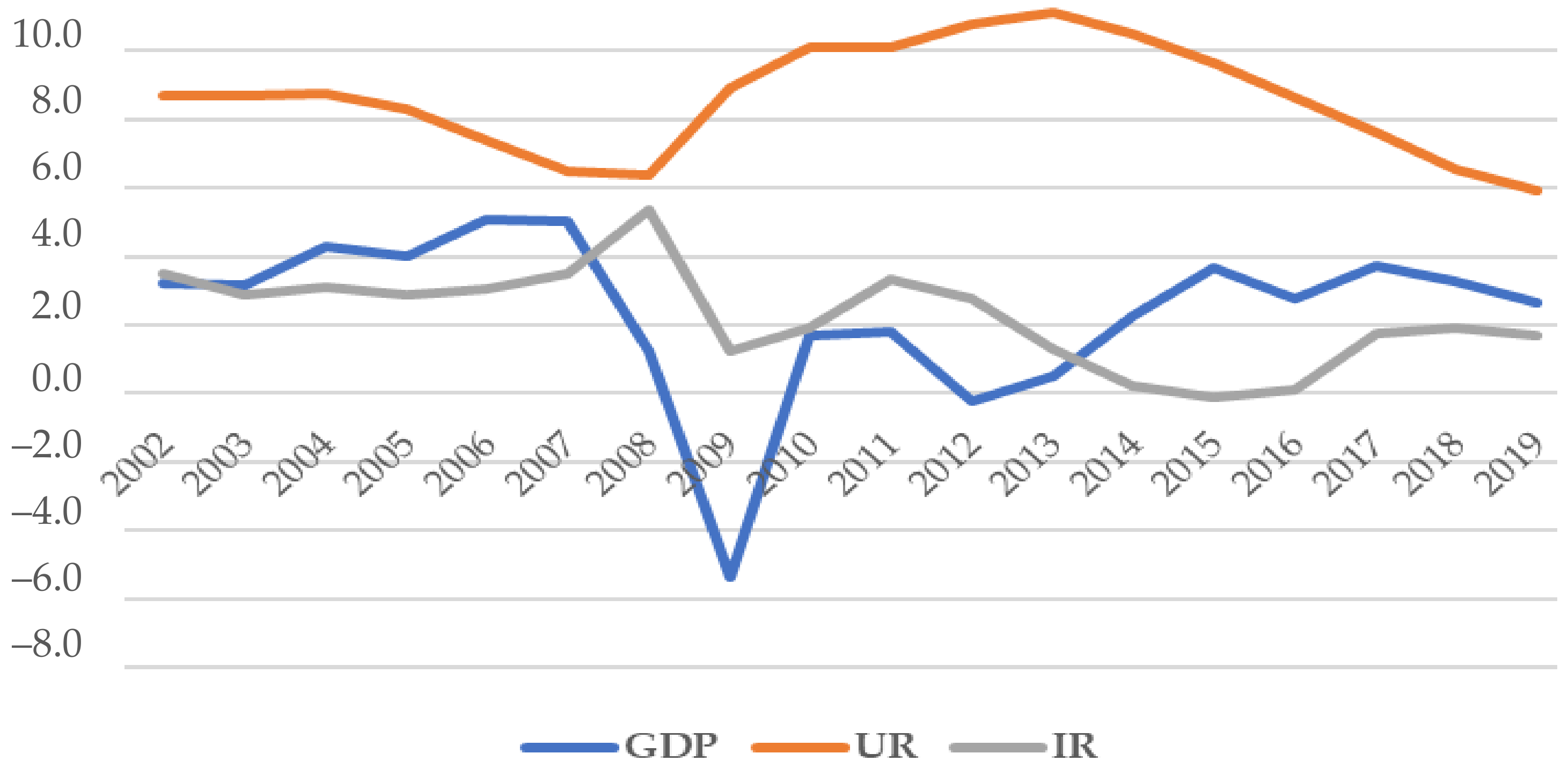

- The average GDP growth rate was 2.4%, oscillating between a minimum of −14.8% (Lithuania, 2009) and a maximum of 25.2% (Ireland, 2015);

- -

- The average unemployment rate was 8.6%, indicating that about 9 out of 100 active people were jobless; the lowest rate of unemployment was found in the Czech Republic (2.01% in 2019), and the highest in Greece (27.5% in 2016);

- -

- The average inflation rate was 2.2%; the inflation rate oscillated between a minimum of−4.5% (Ireland, 2009) and a maximum of 22.5% (Romania, 2002).

- -

- In the countries included in the sample, SAIs are governed either by a president (14 countries) or a governing body (14 countries); the average mandate is 13 years, keeping in mind that 5 out of 28 states have no legal provision for the length of the mandate; to make the calculations for these states, a general longest mandate of 40 years was considered;

- -

- In the case of 22 states, the mandate for the representatives of SAIs is renewable (mean Rm = 1.2);

- -

- Fourteen belong to governmental control bodies, seven have jurisdictional positions, and eight do not belong to any of these bodies (mean 2.1);

- -

- SAIs in the EU Member States have, on average, 556 employees; the biggest organizational structure was found in Italy (2658 employees), and the smallest in Luxemburg; as this indicator is relevant if it is interpreted in a sterile way, it was calculated as the number of SAIs employees per 1 million inhabitants; in this case, the states with the biggest organizational structure (over 1000 employees) are: Romania 1/83, Italy 1/44, Poland 1/42, and Germany (1/14); for the entire sample, the most negative situation was found in Cyprus (with a ratio of 1/160), Malta (1/145), Lithuania (1/103), and Romania 1/83); the most favorable values appear for France (1/11), Great Britain (1/13), the Netherlands, and Germany with one SAIs employee to 14 citizens;

- -

- Regarding the scope of SAI competencies, in ten countries it covers all levels that use public money (central, regional, and local; SAIs in seven countries only audit the financial statements of central, regional and local public administrations and state enterprises);

- -

- Regarding the number of years of SAIs activity, it differs by country (varying from 16 to 212 years); the mean value of the sample is 72 years;

- -

- SAIs in five states have explicit legal provisions for the responsibility to take action for financial/public debt;

- -

- All 28 SAIs in the analyzed countries perform financial and performance audits; only six performing legality and regularity audits, and 16 conducting compliance audits; Four SAIs perform special audits, such as technical and environmental audits (Cyprus), an external audit of EU community public funds (Romania), and budgetary policy audit (Finland).

- -

- As a symmetry measure, Kurtosis indicates that 11 of the 17 variables have values lower than 3 (meaning a flattening of the curve reflecting the distribution of values); four variables (GDS, GDP, IR, and M) take values higher than 3 (indicating a leptokurtic distribution); only one of the variables (UR) has an average bolt value (3.1);

- -

- Ten of the analyzed variables have an approximately symmetrical distribution (Skewness taking values between E −1/2 and +1/2); seven variables show asymmetric distributions (skewness values being less than −1 or higher +1); a single variable has a moderate asymmetric distribution (GGGD).

0.31·Ns − 0.13·C − 0.41·O + 0.64·D + 0.07·Ta − 0.92·Sa − 3.27

0.21·Ns − 0.12·C − 0.45·O + 0.44·D + 0.05·Ta − 0.64·Sa − 1.52

0.99·Ns + 5.14·C + 20.33·O − 2.95·D − 14.29·AM + 18.01·Sa − 54.17

2.62·S − 1.41·Ns + 4.34·C + 22.57·O − 0.80·D − 11.73·AM + 17.11·Sa − 57.51

+ 0.23·O + 0.04·D + 0.18·Ta + 0.19·Sa + 1.47

+ 0.18·D + 0.32·Ta + 0.09·Sa + 0.91

- -

- The impact of macroeconomic variables on public deficits (GDS) is more significant during the crisis periods; the acceleration in the pace of growth of GDP may diminish public debt (GGGD) during the pre-crisis periods;

- -

- How SAIs are represented (Gb) is important only during crisis and post-crisis periods, having an impact only on GDS;

- -

- The length of the mandate of SAIs representatives (M) is important for control of GDS and GGGD only in the post-crisis periods; the impact of this variable on GE and CC is positive during pre-crisis and crisis periods, and negative in the post-crisis;

- -

- The option of renewable mandate (Rm) amplifies GGGD; the abandoning of this option may improve the perception of GE in the post-crisis periods;

- -

- The integration of SAIs into parliamentary bodies (S) may deteriorate the perceptions of GE and CC; the impact grows in the crisis periods and diminishes in the post-crisis;

- -

- The growth in the number of employees of SAIs (Ns) does not influence the perceptions of GE and CC in the pre-crisis and post-crisis periods positively;

- -

- By extending the scope of competencies of SAIs (C), the debt of governments grows progressively (once there is a movement from pre-crisis to crisis and post-crisis) and affects the perceptions of GE and CC similarly;

- -

- The maturity of SAIs measured by the number of years of experience (O) is not favorable for the decrease of GGGD but improves the perceptions of GE and CC, being more prevalent in crisis and post-crisis periods;

- -

- Conducting regularity and legality audits, as well as compliance audits (Ta), decreases GGGD and improves perceptions of GE and CC;

- -

- Conducting special audits (SA) favors the growth of GGGD during crisis and post-crisis and improves the perceptions of GE in the post-crisis.

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Onofrei, M.; Gavriluță (Vatmanu), A.; Bostan, I.; Oprea, F.; Paraschiv, G.; Lazăr, C.M. The Implication of Fiscal Principles and Rules on Promoting Sustainable Public Finances in the EU Countries. Sustainability 2020, 12, 2772. [Google Scholar] [CrossRef] [Green Version]

- Giosi, A.; Testarmata, S.; Brunelli, S.; Staglianò, B. The dimensions of fiscal governance as the cornerstone of public finance sustainability: A general framework. J. Public Budg. Account. Financ. Manag. 2014, 26, 94–139. [Google Scholar] [CrossRef] [Green Version]

- Kargol-Wasiluk, A.; Wildowicz-Giegiel, A. The quality of public finance in the light of fiscal governance concept: Implications for the European Union countries. Equilib. Q. J. Econ. Econ. Policy 2019, 13, 411–426. [Google Scholar] [CrossRef]

- Rodriguez-Vives, M. The quality of public finances: Where do we stand? Econ. Bus. Lett. 2019, 8, 97–105. [Google Scholar] [CrossRef]

- Pinsard, N.; Tadjeddine, Y. The marketization of the French public finance before capitalism: The paulette edict of 1604. Econ. Soc. 2021, 50, 471–493. [Google Scholar] [CrossRef]

- Ermasova, N.; Guzman, T.; Ceka, E. Legacy Effect of Soviet Budgeting System on Public Capital Budgeting: Cases of Russia, Moldova, and Uzbekistan. Int. J. Public Adm. 2021. [CrossRef]

- Hao, J.; Tang, C.; Zhu, J.; Jiang, J. The Impacts of Flattening Fiscal Reform on Health Expenditure in China. Front. Public Health 2021, 9, 614915. [Google Scholar] [CrossRef] [PubMed]

- Bertoa, F.C.; Rama, J. Paying for appeasement: On the moderating role of public subsidies in East Central European party politics. Party Politics 2021. [Google Scholar] [CrossRef]

- Pulay, G.; Simon, J. Measuring the Macroeconomic Performance of Public Finance Management. Public Financ. Q. 2020, 23–43. [Google Scholar] [CrossRef]

- Guter-Sandu, A.; Murau, S. The Eurozone’s Evolving Fiscal Ecosystem: Mitigating Fiscal Discipline by Governing Through Off-Balance-Sheet Fiscal Agencies. New Political Econ. 2021. [Google Scholar] [CrossRef]

- Hickey, R.; Lozej, M.; Smyth, D. Financing government investment and its implications for public capital: A small open economy perspective. Econ. Model. 2020, 93, 620–641. [Google Scholar] [CrossRef]

- Novo-Corti, I.; Picatoste, X. Sustainable Public Finance and Debt Management. In Financing Sustainable Development. Palgrave Studies in Impact Finance; Ziolo, M., Sergi, B., Eds.; Palgrave Macmillan: Cham, Switzerland, 2019; pp. 227–247. [Google Scholar] [CrossRef]

- Afonso, A.; Erbert, W.; Schuknect, L.; Thone, M. Quality of Public Finance and Growth; EBC Working Paper Series n. 438; European Central Bank: Frankfurt, Germany, 2005; p. 45. [Google Scholar]

- Barrios, S.; Schaechter, A. The Quality of Public Finance and Economic Growth; European Economy Economic Paper n. 337; Directorate-General for Economic and Financial Affairs: Brussels, Belgium, 2008; p. 48. [Google Scholar]

- OECD. Supreme Audit Institutions and Good Governance: Oversight, Insight and Foresight. 2016. Available online: https://0-www-oecd--ilibrary-org.brum.beds.ac.uk/governance/supreme-audit-institutions-and-good-governance_9789264263871-en (accessed on 19 June 2021).

- Dobrowolski, Z.; Sułkowski, Ł. Implementing a Sustainable Model for Anti-Money Laundering in the United Nations Development Goals. Sustainability 2020, 12, 244. [Google Scholar] [CrossRef] [Green Version]

- Nagy, S. The role of Supreme Audit Institutions in fight against the consequences of financial and economic crisis: A theoretical approach. In Crisis Aftermath: Economic Policy Changes in the EU and Its Member States; Conference Proceedings; University of Szeged: Hungary, Szeged, 2012; pp. 270–282. [Google Scholar]

- Bergman, U.M.; Hutchison, M.M.; Hougaard Jensen, S.E. Promoting sustainable public finances in the European Union: The role of fiscal rules and government efficiency. Eur. J. Political Econ. 2016, 44, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Caldeira, V. Audit is Vital to Transparent and Accountable Public Finances. In ICAEW, Sustainable Public Finances: Global Views; ICAEW: London, UK, 2012; p. 6. Available online: https://www.ifac.org/system/files/news/files/ICAEW%20Sustainable%20public%20finances%20global%20views.pdf (accessed on 10 June 2021).

- Hay, D.C.; Cordery, C.J. Evidence about the value of financial statement audit in the public sector. Public Money Manag. 2021, 41, 304–314. [Google Scholar] [CrossRef]

- Zeti, C.F.; Luca, M.; Pirvu, C. The Impact of External Public Audit on Public Administration Efficiency. Ann. Constantin Brancusi Univ. Targu-Jiu. Econ. Ser. 2020, 2, 58–66. [Google Scholar]

- Van Loocke, E.; Put, V. The impact of performance audits: A review of the existing evidence. In Performance Auditing: Contributing to Accountability in Democratic Government; Lonsdale, J., Wilkins, P., Ling, T., Eds.; Edward Elgar Publishing: Northampton, MA, USA, 2011; pp. 175–208. [Google Scholar]

- Hay, D.C.; Cordery, C.J. The value of public sector audit: Literature and history. J. Account. Lit. 2018, 40, 1–15. [Google Scholar] [CrossRef] [Green Version]

- Cordery, C.J.; Hay, D.C. Supreme audit institutions and public value: Demonstrating relevance. Financ. Account. Manag. 2019, 35, 128–142. [Google Scholar] [CrossRef]

- Antohi, V.-M.; Zlati, M.L.; Ionescu, R.V.; Neculita, M.; Rusu, R.; Constantin, A. Attracting European Funds in the Romanian Economy and Leverage Points for Securing their Sustainable Management: A Critical Auditing Analysis. Sustainability 2020, 12, 5458. [Google Scholar] [CrossRef]

- Blume, L.; Voigt, S. Does organizational design of supreme audit institutions matter? A cross-country assessment. Eur. J. Political Econ. 2011, 27, 215–229. [Google Scholar] [CrossRef]

- Council for Budget Responsibility. How to Evaluate the Long-Term Sustainability of Public Finances? 2013. Available online: https://www.rozpoctovarada.sk/download2/dp1_2012_final_eng.pdf (accessed on 19 June 2021).

- Schick, A. Sustainable Budget Policy: Concepts and Approaches. OECD J. Budg. 2005, 5, 107–126. [Google Scholar] [CrossRef]

- European Union. Long-Term Sustainability of Public Finances for a Recovering Economy. EU 2011/C 161 E/17. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52010IP0190&from=EN (accessed on 18 June 2021).

- Vukčević, I.; Jovović, R. The Quality of Public Finance in the Countries of South-East Europe. J. Cent. Bank. Theory Pract. 2020, 1, 169–184. [Google Scholar] [CrossRef] [Green Version]

- Bethlendi, A.; Lentner, C. Subnational Fiscal Consolidation: The Hungarian Path from Crisis to Fiscal Sustainability in Light of International Experiences. Sustainability 2018, 10, 2978. [Google Scholar] [CrossRef] [Green Version]

- Baland, J.M.; Bourguignon, F.; Platteau, J.P.; Verdier, T. Economic Development and Institutions. In The Handbook of Economic Development and Institutions; Baland, J.M., Bourguignon, F., Platteau, J.P., Verdier, T., Eds.; Princeton University Press: New Jersey, NJ, USA, 2020; pp. 1–20. [Google Scholar]

- Iacobuță, A.-O.; Ifrim, M. Welfare Mentality as a Challenge to European Sustainable Development. What Role for Youth Inclusion and Institutions? Sustainability 2020, 12, 3549. [Google Scholar] [CrossRef]

- Iacobuta, A.O.; Mursa, G.C.; Mihai, C.; Cautisanu, C.; Cismas, L.M. Institutions and Sustainable Development: A Cross-Country Analysis. Transform. Bus. Econ. 2019, 18, 628–646. [Google Scholar]

- Praščević, A.; Ješić, M. Modeling Macroeconomic Policymakers’ Interactions under Zero Lower Bound Environment: The New Keynesian Theoretical Approach. J. Cent. Bank. Theory Pract. 2019, 8, 5–38. [Google Scholar] [CrossRef] [Green Version]

- INTOSAI. 40 Years of Lima Declaration of INTOSAI. 2017. Available online: https://www.intosai.org/fileadmin/downloads/documents/open_access/INTOSAI_Publications/Publication_40y_Lima_Declaration/EN_40_Jahre_Lima_Deklaration.pdf (accessed on 10 June 2021).

- Bringselius, L. Efficiency, economy and effectiveness-but what about ethics? Supreme audit institutions at a critical juncture. Public Money Manag. 2018, 38, 105–110. [Google Scholar] [CrossRef]

- Stapenhurst, R.; Titsworth, J. Features and Functions of Supreme Audit Institutions; PREM-notes No 59; World Bank: Washington, DC, USA, 2001; Available online: https://openknowledge.worldbank.org/handle/10986/11363 (accessed on 7 June 2021).

- Cordery, C.J.; Hay, D.C. Public Sector Audit, 1st ed.; Routledge Taylor and Francis Group: London, UK, 2021. [Google Scholar]

- Groenendijk, N.S. Assessing member states’ management of EU finances: An empirical analysis of the annual reports of the European Court of Auditors, 1996–2001. Public Adm. 2004, 82, 701–725. [Google Scholar] [CrossRef]

- Pollitt, C.; Summa, H. Comparative and international administration reflexive watchdogs? How supreme audit institutions account for themselves. Public Adm. 1997, 75, 313–336. [Google Scholar] [CrossRef]

- Scott, C.D. Speaking Softly Without Big Sticks: Meta-Regulation and Public Sector Audit. Law Policy 2003, 25, 203–219. [Google Scholar] [CrossRef]

- Bonollo, E. Measuring supreme audit institutions’ outcomes: Current literature and future insights. Public Money Manag. 2019, 39, 468–477. [Google Scholar] [CrossRef]

- Jacobs, K. Making sense of social practice: Theoretical pluralism in public sector accounting research. Financ. Account. Manag. 2012, 28, 1–25. [Google Scholar] [CrossRef]

- Di Maggio, P.; Powell, W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Frumkin, P.; Galaskiewicz, J. Institutional isomorphism and public sector organizations. J. Public Adm. Res Theory 2004, 14, 283–307. Available online: https://0-www-jstor-org.brum.beds.ac.uk/stable/3525838 (accessed on 10 June 2021). [CrossRef] [Green Version]

- Van Der Meer, F.B. Evaluation and the social construction of impacts. Evaluation 1999, 5, 387–406. [Google Scholar] [CrossRef] [Green Version]

- Morin, D. Measuring the impact of value- for- money audits: A model for surveying audited managers. Can. Public Adm. 2004, 47, 141–164. [Google Scholar] [CrossRef]

- Dye, K.M.; Stapenhurst, R. Pillars of Integrity: The Importance of Supreme Audit Institutions in Curbing Corruption; The Economic Development Institute—World Bank: Washington, DC, USA, 1998; Available online: http://info.worldbank.org/etools/docs/library/18120/pillars.pdf (accessed on 7 June 2021).

- Gustavson, M. Auditing Good Government in Africa: Public Sector Reform, Professional Norms and the Development Discourse; Palgrave Macmillan: Basingstoke, UK, 2014. [Google Scholar]

- Isaksson, A.-S.; Bigsten, A. Institution building with limited resources: Establishing a supreme audit institution in Rwanda. World Dev. 2012, 40, 1870–1881. [Google Scholar] [CrossRef] [Green Version]

- Busse, K.H. The SAI’s Role in Combating Corruption. Int. J. Gov. Audit. 2007, 34, 8–11. [Google Scholar]

- Dye, K.M. Corruption and Fraud Detection by Public Sector Auditors. EDP Audit Control Secur. Newsl. 2007, 36, 6–15. [Google Scholar] [CrossRef]

- Assakaf, E.A.; Samsudin, R.S.; Othman, Z. Public sector auditing and corruption: A literature. Asian J. Financ. Account. 2018, 10, 226–241. [Google Scholar] [CrossRef] [Green Version]

- Gustavson, M.; Sundström, A. Organizing the Audit Society: Does Good Auditing Generate Less Public Sector Corruption? Adm. Soc. 2016, 50, 1508–1532. [Google Scholar] [CrossRef]

- Melo, M.A.; Pereira, C.; Figueiredo, C.M. Political and institutional checks on corruption: Explaining the performance of Brazilian audit institutions. Comp. Political Stud. 2009, 42, 1217–1244. [Google Scholar] [CrossRef]

- Pereș, I.; Gherai, D.S.; Balaciu, D.E. Research on the Contribution of Supreme Audit Institutions to Government Efficiency and to Corruption Perception. Audit. Financ. 2014, 12, 28–38. [Google Scholar]

- Tara, I.G.; Gherai, D.S.; Droj, L.; Matica, D.E. The Social Role of the Supreme Audit Institutions to Reduce Corruption in the European Union—Empirical Study. Rev. Cercet. Interv. Soc. 2016, 52, 217–240. [Google Scholar]

- Gherai, D.S.; Tara, I.G.; Matica, D.E. The Supreme Audit Institution Can Control the Corruption or Not. Ann. Univ. Oradea Econ. Sci. Ser. 2016, 25, 465–476. [Google Scholar]

- Stuiveling, S.J.; Turksema, R.W. Public expenditure control in the Netherlands. In Public Expenditure Control in Europe. Coordinating Audit Functions in the European Union; Crespo, M.G., Ed.; Edward Elgar Publishing Limited: Cheltenham, UK, 2005; pp. 55–78. [Google Scholar]

- PEFA. Framework for Assessing Public Financial Management. 2019. 2nd ed. Washington, DC. Available online: https://www.pefa.org/sites/pefa/files/resources/downloads/PEFA%202016_latest%20version_with%20links%20%282%29.pdf (accessed on 1 July 2021).

- Olken, B. Monitoring corruption: Evidence from a field experiment in Indonesia. J. Political Econ. 2007, 115, 200–249. [Google Scholar] [CrossRef] [Green Version]

- Liu, J.; Lin, B. Government auditing and corruption control: Evidence from China’s provincial panel data. China J. Account. Res. 2012, 5, 163–186. [Google Scholar] [CrossRef] [Green Version]

- Tăvală, F.M. The Public Debt Audit—An Important Form of Public Audit in the Current Macroeconomic Context. Rev. Econ. 2018, 70, 131–142. [Google Scholar]

- Karabayev, E.B.; Sembiyeva, L.M.; Zeinelgabdin, A.B.; Beisenova, L.Z.; Pankou, D.A. The Role of External Public Audit in Ensuring the Financial Stability of the Budgets of Developing Countries. Public Policy Adm. 2021, 20, 108–117. [Google Scholar]

- Schelker, M.; Eichenberger, R. Auditors and fiscal policy: Empirical evidence on a little big institution. J. Comp. Econ. 2010, 38, 357–380. [Google Scholar] [CrossRef]

- Eichenberger, R.; Schelker, M. Independent and competing agencies: An effective way to control government. Public Choice 2007, 130, 79–98. [Google Scholar] [CrossRef] [Green Version]

- Torgler, B. A Knight without a Sword? The Effects of Audit Courts on Tax Morale. J. Inst. Theor. Econ. 2005, 161, 735–760. Available online: https://0-www-jstor-org.brum.beds.ac.uk/stable/40752549 (accessed on 10 June 2021). [CrossRef]

- Blume, L.; Voigt, S. Supreme Audit Institutions: Supremely Superfluous? A Cross Country Assessment. SSRN Electron. J. 2007. [Google Scholar] [CrossRef]

- Yalçin, S. The Effects of Supreme Audit Institutions’ independency on Public Debt Sustainability: An Investigation for Turkey. Muhasebe Bilim Dünya. Derg. 2018, 20, 375–388. [Google Scholar] [CrossRef]

- OECD. General Government Debt (Indicator). 2020. Available online: https://0-doi-org.brum.beds.ac.uk/10.1787/a0528cc2-en (accessed on 10 June 2021).

- Eurostat Database. 2020. Available online: https://ec.europa.eu/eurostat/web/main/data/database (accessed on 10 June 2021).

- Office for National Statistics. Government, Public Sector and Taxes. 2020. Available online: https://www.ons.gov.uk/economy/governmentpublicsectorandtaxes (accessed on 8 June 2021).

- Cordery, C.J.; Hay, D.C. Public sector audit in uncertain times. Financ. Account. Manag. 2021, 1–20. [Google Scholar] [CrossRef]

- Hay, D.C.; Cordery, C.J. The future of auditing research in the public sector. J. Public Budg. Account. Financ. Manag. 2021, 33, 234–242. [Google Scholar] [CrossRef]

- Worldwide Governance Indicators. 2020. Available online: http://info.worldbank.org/governance/wgi/ (accessed on 10 June 2021).

- The World Bank Indicators. 2020. Available online: https://data.worldbank.org/indicator (accessed on 7 June 2021).

- European Court of Auditors. Public Audit in the European Union; Publications Office of the European Union: Luxembourg, 2019; Available online: https://op.europa.eu/en/publication-detail/-/publication/5ff4cf77-2b53-11e9-8d04-01aa75ed71a1/language-en/format-PDF/source-218220259 (accessed on 20 June 2021).

- Rigsrevisionen. Available online: https://uk.rigsrevisionen.dk/about-us/history-and-background (accessed on 2 June 2021).

- The Bulgarian National Audit Office. 2015. Available online: https://www.bulnao.government.bg/en/articles/national-audit-office-act-1035 (accessed on 2 June 2021).

- Croatia State Audit Act. 1999. Available online: http://webcache.googleusercontent.com/search?q=cache:N6IG4cfZvfsJ:www1.worldbank.org/publicsector/pe/BudgetLaws/CroatiaStateAuditAct1999.doc+&cd=4&hl=en&ct=clnk&gl=ro (accessed on 2 June 2021).

- The State Audit Office of Hungary. 2020. Available online: https://www.asz.hu/en/ (accessed on 2 June 2021).

{kind=link}

{kind=link}

| Variables | Symbol | Sources/Calculation/Representation | |

|---|---|---|---|

| Dependent variables | |||

| Government deficit/surplus | GDS | [72,73] | |

| General government gross debt | GGGD | [72,73] | |

| Government effectiveness | GE | [76] | |

| Control of corruption | CC | [76] | |

| Independent variables | |||

| Macro-economics | GDP growth rate | GDPgr | [77] |

| Unemployment rate | UR | [77] | |

| Inflation rate | IR | [77] | |

| Related to SAI | Governing body | Gb | 1 = one person, 2 = a group |

| President/Body mandate | M | Number of years (natural logarithm of number of years) | |

| Renewable mandate | Rm | 1 = Yes, 2 = No | |

| Part of a structure | S | 1 = Parliamentary, 2 = Jurisdictional, 3 = Neither | |

| Number of staff | Ns | Number of staff (natural logarithm of NS) | |

| Covered level | C | 1 = Central Government, 2 = Central + Regional Government, 3 = Central + Regional +Local Government, 4 = 3 + State Enterprises, 5 = 4+Public Bodies, 6 = 5+Municipalities, 7 = 6+Other beneficiaries | |

| Old | O | Number of years of activity (on 31 December of each year of the analysis period) (natural logarithm of years number) | |

| Actions regarding the financial/public debt situation | D | 1 = Yes, 2 = No | |

| Types of audits | Ta | All institutions perform financial and performance audits. 1 = Legality and regularity audit, 2 = Compliance audit 3 = Neither 1 nor 2 | |

| Special audit | Sa | 1 = Yes, 2 = No | |

| GDS | GGGD | GE | CC | GDP | UR | IR | Gb | LN_M | Rm | S | LN_ Ns | C | LN_O | D | Ta | Sa | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | −2.1 | 56.9 | 1.1 | 1.0 | 2.4 | 8.6 | 2.2 | 1.5 | 3.3 | 1.2 | 2.1 | 5.9 | 5.6 | 3.8 | 1.8 | 2.0 | 1.9 |

| Standard Error | 0.2 | 1.6 | 0.0 | 0.0 | 0.2 | 0.2 | 0.1 | 0.0 | 0.2 | 0.0 | 0.0 | 0.0 | 0.1 | 0.0 | 0.0 | 0.0 | 0.0 |

| Median | −2.1 | 50.2 | 1.1 | 1.0 | 2.4 | 7.5 | 2.0 | 1.5 | 2.2 | 1.0 | 2.0 | 5.8 | 6.0 | 3.7 | 2.0 | 2.0 | 2.0 |

| Standard Deviation | 3.7 | 35.7 | 0.6 | 0.8 | 3.5 | 4.3 | 2.3 | 0.5 | 4.1 | 0.4 | 0.9 | 1.0 | 1.2 | 1.0 | 0.4 | 0.7 | 0.4 |

| Kurtosis | 8.8 | 1.1 | −0.6 | −1.2 | 6.5 | 3.1 | 16.5 | −2.0 | 23.8 | 0.0 | −1.7 | −0.2 | −1.5 | −1.3 | 0.8 | −0.7 | 2.2 |

| Skewness | −1.3 | 0.9 | −0.2 | 0.1 | −0.4 | 1.6 | 2.8 | 0.0 | 4.7 | 1.4 | −0.1 | −0.2 | −0.2 | 0.1 | −1.7 | 0.0 | −2.0 |

| Range | 42.1 | 184.3 | 2.7 | 2.9 | 40.0 | 25.5 | 27.0 | 1.0 | 26.9 | 1.0 | 2.0 | 4.4 | 3.0 | 3.7 | 1.0 | 2.0 | 1.0 |

| Minimum | −32.1 | 1.9 | −0.4 | −0.4 | −14.8 | 2.0 | −4.5 | 1.0 | 1.1 | 1.0 | 1.0 | 3.5 | 4.0 | 1.6 | 1.0 | 1.0 | 1.0 |

| Maximum | 10.0 | 186.2 | 2.4 | 2.5 | 25.2 | 27.5 | 22.5 | 2.0 | 28.0 | 2.0 | 3.0 | 7.9 | 7.0 | 5.4 | 2.0 | 3.0 | 2.0 |

| Count | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 | 504 |

| GDS | GGGD | GE | CC | GDP | UR | IR | Gb | LN_M | Rm | S | LN_Ns | C | LN_O | D | Ta | Sa | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| GDS | 1 | ||||||||||||||||

| GGGD | −0.4 | 1 | |||||||||||||||

| GE | 0.3 | −0.1 | 1 | ||||||||||||||

| CC | 0.3 | −0.1 | 0.9 | 1 | |||||||||||||

| GDP | 0.3 | −0.3 | −0.1 | −0.1 | 1 | ||||||||||||

| UR | −0.4 | 0.4 | −0.3 | −0.4 | −0.2 | 1 | |||||||||||

| IR | 0.0 | −0.3 | −0.3 | −0.3 | 0.2 | −0.1 | 1 | ||||||||||

| Gb | −0.2 | 0.2 | −0.2 | −0.1 | −0.1 | 0.1 | 0.1 | 1 | |||||||||

| LN_M | 0.0 | −0.1 | 0.1 | 0.1 | −0.1 | −0.1 | 0.1 | −0.2 | 1 | ||||||||

| Rm | 0.1 | 0.0 | −0.2 | −0.1 | −0.1 | 0.0 | 0.1 | 0.2 | 0.0 | 1 | |||||||

| S | 0.0 | −0.1 | −0.3 | −0.3 | 0.0 | 0.1 | 0.1 | 0.3 | −0.1 | 0.1 | 1 | ||||||

| LN_Ns | −0.2 | 0.3 | −0.4 | −0.3 | −0.1 | 0.2 | 0.1 | 0.4 | 0.0 | 0.4 | −0.1 | 1 | |||||

| C | −0.3 | 0.3 | −0.5 | −0.5 | 0.0 | 0.4 | 0.1 | −0.1 | −0.1 | 0.0 | 0.0 | 0.2 | 1 | ||||

| LN_O | 0.0 | 0.4 | 0.5 | 0.5 | −0.2 | −0.1 | −0.3 | 0.2 | −0.1 | −0.1 | −0.2 | 0.1 | −0.2 | 1 | |||

| D | 0.0 | −0.1 | 0.1 | 0.1 | 0.0 | 0.0 | 0.0 | 0.1 | 0.0 | −0.2 | 0.0 | 0.1 | −0.2 | 0.0 | 1 | ||

| Ta | 0.3 | −0.3 | 0.4 | 0.4 | 0.1 | −0.2 | 0.0 | −0.3 | 0.0 | 0.3 | −0.1 | −0.4 | −0.3 | 0.0 | 0.0 | 1 | |

| Sa | −0.1 | 0.1 | 0.2 | 0.2 | −0.1 | 0.0 | −0.2 | 0.0 | 0.0 | −0.3 | −0.2 | 0.0 | 0.0 | 0.1 | 0.3 | 0.0 | 1 |

| Regression Statistics | GDS | GGGD | GE | CC | ||

|---|---|---|---|---|---|---|

| with GE | with CC | with GE | with CC | |||

| Multiple R | 0.60 | 0.60 | 0.76 | 0.77 | 0.81 | 0.84 |

| R Square | 0.37 | 0.36 | 0.58 | 0.60 | 0.66 | 0.70 |

| Adjusted R Square | 0.35 | 0.34 | 0.57 | 0.59 | 0.65 | 0.69 |

| Standard Error | 3.00 | 3.02 | 23.39 | 22.88 | 0.35 | 0.44 |

| Observations | 504 | 504 | 504 | 504 | 504 | 504 |

| ANOVA | ||||||

| Significance F | 4.57 × 1040 | 5.28 × 1039 | 2.52 × 1083 | 5.59 × 1088 | 1.68 × 10106 | 1.66 × 10119 |

| Models 1 &2 GDS | Coefficients | Standard Error | t Stat | p-Value | Lower 95% | Upper 95% | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| GE | CC | GE | CC | GE | CC | GE | CC | GE | CC | GE | CC | |

| Intercept | −3.27 | −1.52 | 2.10 | 2.05 | −1.56 | −0.74 | 0.12 | 0.46 | −7.38 | −5.55 | 0.85 | 2.50 |

| GE or CC | 2.19 | 1.61 | 0.39 | 0.31 | 5.68 | 5.18 | 0.00 | 0.00 | 1.43 | 1.00 | 2.94 | 2.23 |

| GDP | 0.33 | 0.32 | 0.04 | 0.04 | 8.05 | 7.83 | 0.00 | 0.00 | 0.25 | 0.24 | 0.41 | 0.40 |

| UR | −0.22 | −0.21 | 0.04 | 0.04 | −5.95 | −5.56 | 0.00 | 0.00 | −0.30 | −0.29 | −0.15 | −0.14 |

| IR | −0.04 | −0.06 | 0.07 | 0.07 | −0.64 | −0.87 | 0.52 | 0.38 | −0.17 | −0.19 | 0.09 | 0.07 |

| Gb | −0.97 | −0.98 | 0.35 | 0.35 | −2.77 | −2.76 | 0.01 | 0.01 | −1.67 | −1.67 | −0.28 | −0.28 |

| LN_M | −0.03 | −0.03 | 0.04 | 0.04 | −0.91 | −0.89 | 0.37 | 0.37 | −0.10 | −0.10 | 0.04 | 0.04 |

| Rm | 1.33 | 1.20 | 0.49 | 0.49 | 2.71 | 2.45 | 0.01 | 0.01 | 0.37 | 0.24 | 2.29 | 2.17 |

| S | 0.35 | 0.34 | 0.19 | 0.19 | 1.82 | 1.76 | 0.07 | 0.08 | −0.03 | −0.04 | 0.72 | 0.72 |

| LN_Ns | 0.31 | 0.21 | 0.23 | 0.22 | 1.35 | 0.92 | 0.18 | 0.36 | −0.14 | −0.23 | 0.75 | 0.65 |

| C | −0.13 | −0.12 | 0.14 | 0.15 | −0.88 | −0.82 | 0.38 | 0.42 | −0.41 | −0.40 | 0.16 | 0.17 |

| LN_O | −0.41 | −0.45 | 0.19 | 0.20 | −2.20 | −2.29 | 0.03 | 0.02 | −0.78 | −0.84 | −0.04 | −0.06 |

| D | 0.64 | 0.44 | 0.41 | 0.41 | 1.58 | 1.06 | 0.12 | 0.29 | −0.16 | −0.37 | 1.44 | 1.24 |

| Ta | 0.07 | −0.05 | 0.31 | 0.32 | 0.24 | −0.15 | 0.81 | 0.88 | −0.53 | −0.67 | 0.68 | 0.58 |

| Sa | −0.92 | −0.64 | 0.45 | 0.44 | −2.07 | −1.44 | 0.04 | 0.15 | −1.80 | −1.51 | −0.05 | 0.23 |

| Models 3&4 GGGD | Coefficients | Standard Error | t Stat | p-Value | Lower 95% | Upper 95% | ||||||

| GE | CC | GE | CC | GE | CC | GE | CC | GE | CC | GE | CC | |

| Intercept | −54.17 | −57.51 | 16.34 | 15.54 | −3.31 | −3.70 | 0.00 | 0.00 | −86.28 | −88.05 | −22.06 | −26.98 |

| GE or CC | −11.15 | −14.32 | 3.00 | 2.36 | −3.71 | −6.06 | 0.00 | 0.00 | −17.05 | −18.97 | −5.25 | −9.68 |

| GDP | −0.78 | −0.83 | 0.32 | 0.31 | −2.44 | −2.67 | 0.02 | 0.01 | −1.41 | −1.44 | −0.15 | −0.22 |

| UR | 2.11 | 1.84 | 0.29 | 0.29 | 7.23 | 6.31 | 0.00 | 0.00 | 1.54 | 1.27 | 2.69 | 2.41 |

| IR | −2.20 | −2.29 | 0.51 | 0.50 | −4.33 | −4.62 | 0.00 | 0.00 | −3.20 | −3.27 | −1.20 | −1.32 |

| Gb | −4.98 | −4.62 | 2.75 | 2.69 | −1.82 | −1.72 | 0.07 | 0.09 | −10.38 | −9.89 | 0.41 | 0.66 |

| LN_M | 0.84 | 0.99 | 0.28 | 0.27 | 3.03 | 3.65 | 0.00 | 0.00 | 0.30 | 0.46 | 1.38 | 1.52 |

| Rm | 16.30 | 16.49 | 3.82 | 3.72 | 4.27 | 4.43 | 0.00 | 0.00 | 8.79 | 9.17 | 23.80 | 23.80 |

| S | −1.58 | −2.62 | 1.49 | 1.46 | −1.07 | −1.80 | 0.29 | 0.07 | −4.51 | −5.50 | 1.34 | 0.25 |

| LN_Ns | −0.99 | −1.41 | 1.76 | 1.70 | −0.56 | −0.83 | 0.57 | 0.41 | −4.46 | −4.75 | 2.47 | 1.94 |

| C | 5.14 | 4.34 | 1.12 | 1.10 | 4.59 | 3.94 | 0.00 | 0.00 | 2.94 | 2.17 | 7.33 | 6.50 |

| LN_O | 20.33 | 22.57 | 1.47 | 1.49 | 13.87 | 15.13 | 0.00 | 0.00 | 17.45 | 19.64 | 23.21 | 25.50 |

| D | −2.95 | −0.80 | 3.17 | 3.12 | −0.93 | −0.26 | 0.35 | 0.80 | −9.18 | −6.94 | 3.27 | 5.34 |

| Ta | −14.29 | −11.73 | 2.41 | 2.42 | −5.93 | −4.85 | 0.00 | 0.00 | −19.03 | −16.47 | −9.56 | −6.98 |

| Sa | 18.01 | 17.11 | 3.48 | 3.36 | 5.18 | 5.09 | 0.00 | 0.00 | 11.18 | 10.51 | 24.85 | 23.71 |

| Model 5: GE | Coefficients | Standard Error | t Stat | p-Value | Lower 95% | Upper 95% |

|---|---|---|---|---|---|---|

| Intercept | 1.47 | 0.24 | 6.20 | 0.00 | 1.00 | 1.93 |

| GDP | −0.02 | 0.00 | −3.25 | 0.00 | −0.02 | −0.01 |

| UR | −0.02 | 0.00 | −5.36 | 0.00 | −0.03 | −0.01 |

| IR | −0.03 | 0.01 | −3.57 | 0.00 | −0.04 | −0.01 |

| Gb | 0.04 | 0.04 | 1.04 | 0.30 | −0.04 | 0.12 |

| LN_M | 0.02 | 0.00 | 4.55 | 0.00 | 0.01 | 0.03 |

| Rm | −0.11 | 0.06 | −1.99 | 0.05 | −0.23 | 0.00 |

| S | −0.13 | 0.02 | −6.26 | 0.00 | −0.18 | −0.09 |

| LN_Ns | −0.16 | 0.03 | −6.12 | 0.00 | −0.21 | −0.11 |

| C | −0.09 | 0.02 | −5.45 | 0.00 | −0.12 | −0.06 |

| LN_O | 0.23 | 0.02 | 11.89 | 0.00 | 0.19 | 0.27 |

| D | 0.04 | 0.05 | 0.83 | 0.41 | −0.05 | 0.13 |

| Ta | 0.18 | 0.04 | 5.04 | 0.00 | 0.11 | 0.25 |

| Sa | 0.19 | 0.05 | 3.77 | 0.00 | 0.09 | 0.30 |

| Model 6: CC | Coefficients | Standard Error | t Stat | p-Value | Lower 95% | Upper 95% |

| Intercept | 0.91 | 0.29 | 3.09 | 0.00 | 0.33 | 1.49 |

| GDP | −0.02 | 0.01 | −2.66 | 0.01 | −0.03 | 0.00 |

| UR | −0.04 | 0.01 | −6.97 | 0.00 | −0.05 | −0.03 |

| IR | −0.03 | 0.01 | −2.90 | 0.00 | −0.05 | −0.01 |

| Gb | 0.06 | 0.05 | 1.15 | 0.25 | −0.04 | 0.16 |

| LN_M | 0.02 | 0.01 | 4.93 | 0.00 | 0.02 | 0.03 |

| Rm | −0.08 | 0.07 | −1.06 | 0.29 | −0.22 | 0.06 |

| S | −0.18 | 0.03 | −6.64 | 0.00 | −0.23 | −0.12 |

| LN_Ns | −0.15 | 0.03 | −4.75 | 0.00 | −0.21 | −0.09 |

| C | −0.13 | 0.02 | −6.16 | 0.00 | −0.16 | −0.09 |

| LN_O | 0.34 | 0.02 | 13.92 | 0.00 | 0.29 | 0.38 |

| D | 0.18 | 0.06 | 3.07 | 0.00 | 0.07 | 0.30 |

| Ta | 0.32 | 0.04 | 7.24 | 0.00 | 0.23 | 0.40 |

| Sa | 0.09 | 0.06 | 1.37 | 0.17 | −0.04 | 0.21 |

| Regression Statistics | GDS | GGGD | GE | CC | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Pre- Crisis | Crisis | Post-Crisis | Pre- Crisis | Crisis | Post-Crisis | Pre- Crisis | Crisis | Post-Crisis | Pre- Crisis | Crisis | Post-Crisis | |

| Multiple R | 0.68 | 0.65 | 0.71 | 0.75 | 0.77 | 0.88 | 0.87 | 0.84 | 0.83 | 0.88 | 0.86 | 0.87 |

| R Square | 0.46 | 0.42 | 0.51 | 0.57 | 0.59 | 0.78 | 0.75 | 0.70 | 0.69 | 0.78 | 0.75 | 0.75 |

| Adjusted R Square | 0.41 | 0.37 | 0.47 | 0.53 | 0.55 | 0.76 | 0.73 | 0.67 | 0.66 | 0.76 | 0.72 | 0.73 |

| Standard Error | 2.39 | 3.67 | 1.65 | 19.10 | 23.97 | 19.56 | 0.34 | 0.34 | 0.31 | 0.38 | 0.42 | 0.40 |

| Observa- tions | 168 | 168 | 168 | 168 | 168 | 168 | 168 | 168 | 168 | 168 | 168 | 168 |

| ANOVA | ||||||||||||

| Significance F | 1.3 × 1014 | 1.6 × 1012 | 1.3 × 1017 | 1.3 × 1021 | 6.8 × 1023 | 1.5 × 1042 | 1.4 × 1039 | 1.3 × 1033 | 2.9 × 1032 | 3.7 × 1044 | 3.4 × 1039 | 5.9 × 1040 |

| Regression Statistics | GDS | GGGD | GE | CC | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Pre-Crisis | Crises | Post-Crises | Pre-Crisis | Crises | Post-Crises | Pre-Crisis | Crises | Post-Crises | Pre-Crisis | Crises | Post-Crises | |

| Intercept | −3.75 | −4.95 | 0.55 | 32.42 | −74.80 | −109.02 | 1.63 | 1.86 | 1.66 | 1.33 | 0.85 | 1.24 |

| GE | 3.09 | 4.10 | 0.31 | −7.84 | −9.01 | −9.55 | − | − | − | − | − | |

| GDP | 0.51 | 0.17 | 0.02 | −4.22 | −0.43 | 0.80 | −0.05 | 0.002 | −0.05 | −0.07 | 0.00 | −0.06 |

| UR | −0.05 | −0.23 | −0.18 | −0.37 | 2.00 | 4.35 | −0.02 | −0.03 | −0.03 | −0.03 | −0.04 | −0.05 |

| IR | 0.02 | 0.38 | 0.07 | −0.84 | −1.81 | 0.81 | −0.06 | −0.05 | −0.05 | −0.07 | −0.05 | −0.09 |

| Gb | −0.07 | −1.96 | −0.95 | −2.67 | −8.87 | −0.41 | 0.05 | 0.00 | 0.03 | 0.11 | 0.10 | −0.09 |

| LN_M | 0.02 | −0.08 | −0.67 | 0.15 | 0.60 | 9.71 | 0.01 | 0.01 | −0.07 | 0.02 | 0.02 | −0.12 |

| Rm | −0.54 | 2.01 | 1.46 | 13.02 | 21.93 | 18.14 | −0.06 | −0.12 | −0.28 | 0.04 | −0.24 | −0.17 |

| S | 0.04 | 0.71 | 0.30 | −1.74 | −2.19 | −2.63 | −0.11 | −0.15 | −0.09 | −0.13 | −0.18 | −0.11 |

| LN_Ns | 0.45 | 0.95 | 0.01 | −0.96 | −1.15 | −4.52 | −0.14 | −0.19 | −0.09 | −0.16 | −0.13 | −0.08 |

| C | −0.21 | −0.42 | −0.42 | 4.70 | 4.73 | 8.14 | −0.07 | −0.07 | −0.13 | −0.05 | −0.12 | −0.18 |

| LN_O | −0.28 | −1.33 | 0.09 | 9.16 | 22.93 | 21.16 | 0.19 | 0.24 | 0.23 | 0.22 | 0.36 | 0.44 |

| D | 0.63 | 0.36 | −0.28 | −1.22 | 0.23 | −1.80 | 0.15 | 0.05 | −·0.11 | 0.27 | 0.14 | 0.09 |

| Ta | 0.61 | −0.46 | 0.46 | −15.13 | −17.04 | −18.42 | 0.22 | 0.14 | 0.25 | 0.35 | 0.38 | 0.36 |

| Sa | −2.94 | −0.56 | 0.91 | 7.97 | 23.94 | 23.96 | 0.04 | 0.14 | 0.24 | −0.13 | 0.08 | 0.07 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bostan, I.; Tudose, M.B.; Clipa, R.I.; Chersan, I.C.; Clipa, F. Supreme Audit Institutions and Sustainability of Public Finance. Links and Evidence along the Economic Cycles. Sustainability 2021, 13, 9757. https://0-doi-org.brum.beds.ac.uk/10.3390/su13179757

Bostan I, Tudose MB, Clipa RI, Chersan IC, Clipa F. Supreme Audit Institutions and Sustainability of Public Finance. Links and Evidence along the Economic Cycles. Sustainability. 2021; 13(17):9757. https://0-doi-org.brum.beds.ac.uk/10.3390/su13179757

Chicago/Turabian StyleBostan, Ionel, Mihaela Brindusa Tudose, Raluca Irina Clipa, Ionela Corina Chersan, and Flavian Clipa. 2021. "Supreme Audit Institutions and Sustainability of Public Finance. Links and Evidence along the Economic Cycles" Sustainability 13, no. 17: 9757. https://0-doi-org.brum.beds.ac.uk/10.3390/su13179757