2.1. The Impact of Financialization on Economy

There is extensive theoretical literature on the impact of financialization on the economy from macroeconomic perspectives. Most economists generally view excessive financialization as a significant obstacle for economic development [

4,

13,

14,

15]. Several previous studies [

16,

17,

18] empirically establish that excessive financialization has a negative effect on capital accumulation when resource and production input factors are established. The findings of Singh [

19], Krugman and Anthony [

20] and Orhangazi [

4] indicate that financialization hinders economic growth by extracting additional profits from the economy into the financial sector; likewise, corporate expenditures are allocated from production activities to financial investments. Sweezy [

21] argues that the dramatic expansion of the financial sector, high degree of independence within the financial sector, and gradual dominance of the real production system pose potential financial risks to the economy. The findings of Lazonick [

22] demonstrate that the overspending of manufacturing firms leads to decreased investments in production and increased unemployment rates. The empirical result implies that over-financialization has a negative effect on unemployment. China’s increasing capital flows into the stock market and real estate industries represent expanding financialization for the economy. Zhang et al. [

23] examines the negative impact of excessive spending on the enterprise’s physical investment ratio and indicates that these aspects play a significant role in weakening monetary policy. Wang et al. [

24] also confirms that excessive corporate financialization exacerbates asset bubbles. In particular, Law and Singh [

25] explore the possible asymmetric relationship between the extension of financial resources and growth, which indicates that the expansion of the financial system benefits growth to a certain extent. Sahay et al. [

26] presents a similar argument by indicating that excessive financial resources increases economic risk and financial volatility.

2.3. Nonlinear Effects of Financialization on Entrepreneurship

There are two types of literature that cover the financial assets of firms and capital accumulation. Two main views exist, leading to ambiguous conclusions. One group of researchers believes that moderate financialization results in high capital gains and secures TFP. The second group of researchers believe that excessive financialization hinders the growth of TFP by inhibiting technological innovation and capital accumulation. However, both of these arguments are true to some extent. Thus, the extent to which TFP is affected depends on why financial assets are held. If motivated by speculation, firms will hold more financial assets considering the balance between risk and return.

When there has been a change in corporate management or corporate management is unable to meet the company’s financial goals, they allocate financial assets [

10,

33]. This allocation of financial assets enhances capital liquidity, improves financing capacity, increases the return on assets [

7,

9] increases short-term shareholder value, and integrates production and finance [

34], which contributes to the growth of TFP. Non-financial firms can capture higher returns during market booms by investing in diversified financial instruments, which provides a cushion and reduces risk during market downturns [

8]. Arcand et al. [

35] argue that the essential function of finance is to serve the entire economy. Only when financial development exceeds reasonable limits, does it shift from promoting economic growth to inhibiting economic growth. Again, as the return on investment of financial assets is higher than that of physical investments, enterprises will rely on financial investment income rather than working to improve operational efficiency. Liquidity plays a crucial role in investment decisions [

36]. Financialization offers firms the flexible option of investing in reversible short-term financial assets instead of irreversible long-term physical assets; therefore, financial assets displace productivity accumulation as preferred by shareholders [

37] mainly as a result of change in corporate management [

22,

38]. Therefore, this management leads to changes in decision-making related to capital structure and production allocation. This evidence indicates that a reasonable level of financialization does not hinder production, but it may effectively promote technology upgrades and improvements of research and development (R&D) [

34]. Zhang and Luo [

39] also argue that financialization of private firms contributes to the improvement of productivity improvement through actions such as reducing financing costs and easing financing constraints.

Bonfiglioli [

7] identified that financialization could broaden finance options to allocate capital more efficiently. Adequate capital would give businesses and investors more choice and improve resource allocation; besides, financial constraints can limit the inputs in R&D, which is a significant determinant of TFP [

40]. More specifically, financial support is provided for firms’ technological progress, upgrade of human capital, and productivity improvements. Overall, moderate financialization has a profound impact on enhancing the ability to create value, but excessive financialization is likely to lead to the misallocation of productivity factors, which ultimately affects the productive efficiency.

The growth theory suggests that the original driver of economic growth is productivity [

41]. Economists generally agree that technology leads to productivity improvement; in other words, the increase in the growth of TFP is driven by technological innovation [

42]. More recently, Seo et al. [

13] examined nonfinancial Korean corporations from 1994 to 2009 and found that increased financial investment and profit opportunities displaced R&D investment. Likewise, Xu and Liu [

43] empirically examine the impact of financial asset allocations on R&D activities in China from 2007 to 2015, and the results show evidence of a strong negative correlation between financial asset allocations and firms’ innovations. From the empirical point of view, financialization may affect firms’ productivity through technological improvement. This paradigm is based on the realization that technological innovation is a long-term capital input that contributes to growth through the reallocation of productive resources. Economic outcomes are difficult to determine because corporate investment decisions are complex due to the trade-off between short-term profits that are not guaranteed and sustainability strategies. Orhangazi [

4] explains that a higher return from financial activities should drive a change in the priorities of strategies. A reasonable level of financialization plays an active role in generating new profit sources, thus improving liquidity. However, excessive financialization that replaces long-term R&D investments with short-term profits that are not guaranteed may displace resources for economic development.

Obviously, the results derived from the above researches are not conclusive in matters of the exact relationship of financialization and TFP. Most of the empirical studies are based on ordinary least squares, which ignores the existence of asymmetries. Hence, based on the existing literature, we have assumed non-linearity in the relationship between financialization and TFP, to be empirically verified at a later stage of the study.

Following the arguments above, this study posits that holding excessive amounts of cash destroys the firm’s value through maintenance costs. Therefore, in a comparable level of financialization, the effects of capital accumulation positively impact TFP. However, when the level of financialization exceeds a certain point, displacement, low resource allocation, and efficiency offset the positive effects of capital accumulation. This paper hypothesizes that the positive effects of financialization on innovation declines when a certain threshold is exceeded. Based on the above discussion, the paper hypothesizes the following:

Hypothesis (H1). The relationship between financialization and TFP is asymmetric.

The level of cash holding is not significant determinants of TFP in this sample because of coexistence of what I call “positive” and “crowding out channels” of effect running from technical innovation to factors that affect TFP in the growth prospects. Evidence of the existence of both types of channel will be presented.

Hypothesis (H2). The threshold effect between financialization and TFP depends on a certain level of cash holdings and innovation.

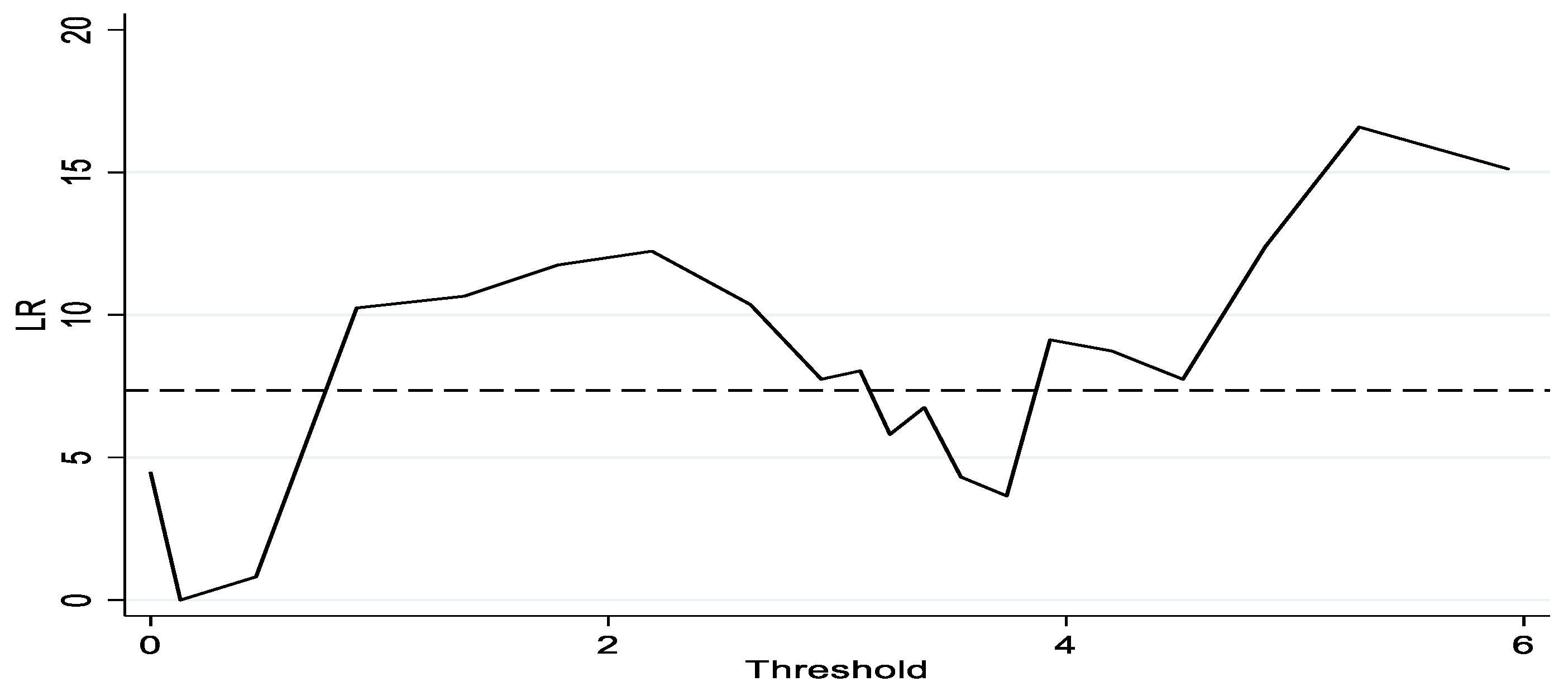

As an alternative method, we propose a quadratic explanatory variable to examine the dual effect. To further analyze the channels through which financialization affects TFP, this paper applies the Hansen [

12] fixed effect panel threshold model convey to explain non-line relationships.

{kind=link}