The Impact of Digital Capability on Manufacturing Company Performance

1

School of Economics and Management, Northwest University, Xi’an 710127, China

2

Business School, Shandong University of Technology, Zibo 255000, China

*

Author to whom correspondence should be addressed.

Sustainability 2022, 14(10), 6214; https://0-doi-org.brum.beds.ac.uk/10.3390/su14106214

Submission received: 13 April 2022

/

Revised: 14 May 2022

/

Accepted: 16 May 2022

/

Published: 20 May 2022

(This article belongs to the Special Issue Digital Technologies and Digital Transformation: Recent Progress and Present Challenges)

Abstract

:Digital capability is an advanced capability that manufacturing companies need for their digital and intelligent development. At present, the influence mechanism behind the impact of digital capability on manufacturing companies’ performance is still unclear and lacks quantitative analysis. Based on the dynamic capability view, we propose a research model to investigate digital capability, digital innovation, value co-creation, and company performance and conduct an empirical study based on questionnaire data from 209 digital manufacturing companies. The empirical results show that digital capability has a significant positive impact on company performance. The results further show that digital innovation mediates the effect of digital capability on performance within a company, while outside the company, value co-creation mediates the impact of digital capability on company performance. This research provides empirical support in favor of companies developing digital capabilities in the context of digital transformation and offers theoretical insight into the contradiction between the potential value of digital capability and companies’ practice.

1. Introduction

With the booming digital economy, more and more manufacturing companies have been competing for the technological superiority of their products by embedding more intelligent and connectivity functions within them (such as smart cars, smart homes, and smart wear), or by delivering products or services to customers in a smarter way for greater reliability and efficiency (such as personalization, digital interaction and ultimate experience). Although manufacturing companies are eager to achieve service-oriented, digital, and intelligent transformations by adopting emerging digital technologies [1], significant changes in technology often create capability gaps in companies that require them to leverage their existing capabilities to unlock the potential value of technology [2,3]. In the context of digital transformation, digital-related capabilities have become key if companies are to obtain sustainable competitive advantages [4,5]. This is because these are not only critical capabilities for manufacturing companies to develop if they are to provide advanced services but are also necessary capabilities should they wish to integrate digital technology and professional digital talents [6]. As a potential premise for manufacturing companies’ digital and intelligent development, the academic and industrial fields have not yet developed a clear understanding of how digital capabilities affect company performance and the extent of this impact. In order to improve the adoption level of emerging digital technologies in manufacturing companies, to develop their digital capabilities, and to promote their digital and intelligent transformation, it is urgent that theoretical and empirical research is carried out on the mechanism behind the influence that digital capability has on company performance.

Existing research has explored the impact of digital technologies in multiple areas, including how coordination of the digital transformation of globally dispersed factories in international manufacturing networks has become a key issue for competitiveness [7]. The adoption of digital technologies improves the efficiency of organizational knowledge management, which in turn promotes product innovation, process innovation, and brings competitive advantages to companies [8]. Digitization creates new ways for companies to create added value [9] and digital transformation affects company competitiveness, mainly through innovation, efficiency and cost reduction [5]. The digital transformation of companies is not simply the adoption of emerging technologies, but involves the interaction of technology, business and society [10]. In the context of digital transformation, digital-related capabilities have received the extensive attention of scholars. This is because companies need to have the relevant capabilities to use digital technology effectively if they are to reap the positive impact of its adoption [11]. Edu et al. [12] have proposed a framework for the value creation perspective of digital application integration and its complementary characteristics, exploring how the integration of digital capabilities can support value creation in organizations. Hirvonen et al. [13] used the DigiMat method to assess the strengths and weaknesses of SMEs in terms of digital capabilities. In the field of information systems, the impact of IT-related capabilities on companies has been widely studied, including the impact of IT capabilities on company performance [14,15], the impact of ICT capabilities on value co-creation [16], and the impact of information interaction capabilities on value co-creation and its competitive advantage [17].

In recent years, scholars have begun to pay attention to the impact on companies of high-level capabilities driven by emerging digital technologies, such as the impact of data management capabilities on company productivity [18], company performance [6], the impact of big data capability and artificial intelligence capability on companies, the impact of sustainable growth and performance [3], the impact of big data analysis technology adoption on a company’s competitive advantage [19,20], and the impact of blockchain technology on the competitive advantage of financial transactions [21]. In the field of marketing, Social CRM capabilities are used to gain information in customer interactions [22]. Digital marketing capabilities and digital business capabilities are proposed to support or enhance the value proposition [23].

Compared with IT-related capabilities, digital-related capabilities are high-level capabilities, with a wider scope, that are driven by emerging digital technologies. The logic of value creation has also shifted from value chains to value networks, and the means of realization have changed from a single digital technology to combinations of digital technologies [23]. Considering that digital-related capabilities involve multidisciplinary knowledge and multidisciplinary backgrounds, there are research gaps in existing research, these include, firstly, a consideration of the disruptive impact of emerging digital technologies on original products, production processes, business models, and organizational forms. Whether the effect of low-level technical capabilities represented by IT capabilities and ICT capabilities on a company’s innovation, performance and influence mechanisms are still applicable remains to be tested theoretically and empirically. Secondly, although existing studies have theoretically demonstrated the potential benefits of emerging digital technologies, in reality, there are still a large number of companies that cannot improve their performance by using emerging digital technologies [24]. The impact and mechanism of emerging digital technology-related capabilities on the innovation and performance of manufacturing companies are still unclear.

This study aims to reveal the impact and mechanism of digital capability on the performance of manufacturing companies. On the basis of theoretical and literature analysis, we propose a theoretical model and research hypothesis that states that digital capability affects company performance. The theoretical model proposed in this study was verified through the analysis of questionnaire data from 209 digital manufacturing companies. The research shows that in the process of digital transformation and development of manufacturing companies, digital capability has a significant positive impact on company performance, providing empirical support for companies to develop digital capability. And by revealing the mechanism of the impact of digital capability on company performance, it provides theoretical and practical guidance for companies to utilize digital capability.

2. Theoretical Background

2.1. Digital Capability

Digital capability is the high-level capability of a company to leverage intelligent, connected products and data analytics to facilitate the development and delivery of services and products to create differentiated value [25]. Most of the existing research defines the concept of digital capability from the perspective of dynamic capabilities. For example, digital capability is composed of three elements: data capture capability, connect capability, and analytical capability [26]. Among these, data capture capability makes operations visible and provides valuable data, connect capability facilitates the transfer of information between interacting partners in a service network, and analytical capability facilitates data and information processing to provide insight to service companies. Annarelli et al. [4] has defined digitalization capabilities as the ability that enables companies to broadly incorporate digital assets and business resources and leverage digital networks to innovate products, services, and processes to achieve organizational learning and customer value. In addition, from the application areas of digital capabilities, digital capabilities are divided into three dimensions: product, business relationship, and software development [27]. From the perspective of technical composition, digital capabilities are divided into three aspects: internet of things (IoTs) capabilities, big data analytics capabilities, and cloud computing (CC) capabilities [12]. Appendix A presents the definition and measurement of digital capabilities in recent literature. In nature, digital capability is closely related to the three main characteristics of dynamic capabilities (sense, capture, and resource reconstruction) [4].

Annarelli et al. [4] has reviewed the nature and scope of digital capabilities in a multidisciplinary context, proposing that digital capabilities consist of (a) reconfiguring a firm’s digital resources and routines, (b) seizing a firm’s digital capabilities, and (c) sensing opportunities and threats along these three dimensions. This review article proposes a capability-based conceptual model of digital capabilities. Although our study may be in parallel with the work of Annarelli et al. [4], when we found their article we were pleasantly surprised to find that our view was so similar to theirs in regard to the way that digital capabilities affect a firm’s performance through both internal and external pathways. The conceptual framework of digital capabilities proposed by Annarelli et al. [4] provides the theoretical basis for our theoretical model. Our study will further explain what the internal and external pathways are.

Regarding the empirical analysis of digital capabilities, existing studies have found that digital transformation is an important antecedent to driving the formation of digital capabilities, and the digital transformation of enterprises is usually accompanied by the formulation and implementation of digital strategies [28]. An empirical analysis by Proksch et al. [29] of 102 new ventures found that digital strategy alone is not sufficient to achieve high digitalization, and that the impact of digital strategy on process digitization is mediated by digital IT capabilities and digital culture. Calle et al. [27] analyzed more than 2000 Spanish manufacturing firms and found that advanced manufacturing technologies did not have a positive or significant impact on servitization unless combined with digital capabilities for internet-based marketing. Heredia et al. [30] further confirmed that digital capabilities positively impact firm performance only through technological capabilities. In general, current conceptualizations and measures of digital capabilities still vary widely. Mainstream research is still dominated by qualitative analysis, and more quantitative research is needed to confirm the theoretical model or proposition proposed by theoretical research.

2.2. Dynamic Capability View

The Dynamic Capability View explains why businesses are able to thrive and prosper in turbulent environments and aims to identify the underlying drivers of business survival and success over the long term. This theoretical view believes that dynamic capabilities are the source of continuous competitive advantage for enterprises in a complex, uncertain, and turbulent competitive environment. Dynamic capability is the ability of an enterprise to integrate, construct and reconfigure heterogeneous resources in response to a rapidly changing environment [31]. From a company perspective, dynamic capabilities are the ability of a company system to solve problems, formed by the propensity to perceive opportunities and threats, make timely market-oriented decisions, and change its resource base [32]. Scholars such as Winter [33] have divided capabilities into “zero-level“ capabilities and “high-level“ capabilities. “zero-level“ capabilities correspond to common capabilities, “high-level“ capabilities correspond to the ability to expand, modify or create common capabilities, and dynamic capabilities are “high-level“ capabilities. From the perspective of information systems, dynamic capabilities are composed of three dimensions: sensing capacity, seizing capacity, and transforming capacity. Sensing capacity refers to identifying, developing, co-developing, extensive, and evaluating technological opportunities related to customer needs; seizing capacity refers to mobilizing resources to address needs and opportunities identified by perceived actions and extracting value from those actions; transforming capacity involves the continuous updating of asset adjustments, synergistic adjustments, re-adjustments, and redeployments [34]. In the context of digital transformation, Warner et al. [35] has further proposed that dynamic capabilities consist of three dimensions: digital sensing capabilities, digital seizing capabilities, and digital transforming capabilities.

In contrast to the conceptualization of digital capabilities, it is not difficult to find that the three characteristics of digital capabilities mentioned above are derived from dynamic capabilities. Therefore, we naturally chose the dynamic capability view as the theoretical basis. In addition, numerous studies on the impact of dynamic capabilities at the firm-level, such as innovation, performance, and competitive advantage, provide a theoretical basis for our study to further explore how digital capabilities affect company outcomes. We will further explore the mechanisms and outcomes of the impact of digital capability on companies in the context of digital transformation and digital technologies.

3. Theoretical Model and Hypotheses Development

3.1. Digital Capability and Company Performance

On the one hand, digital capability helps companies use digital technology to create value and improve company efficiency in a customized service environment; on the other hand, digital capability increases the possibilities for the value that manufacturing companies can provide and deliver to their customers. According to the theoretical study of digital capability [36], in terms of intelligence, digital capability can sense and capture information with low human intervention by configuring hardware components, thereby reducing human resources and information search costs and increasing the opportunities for value creation. In terms of connectivity, digital capability can connect digital products and services through wireless communication networks, and digital interactions between digital products, product users, and companies and stakeholders directly or indirectly promote value creation. In terms of analytics, digital capability transforms the mastered data into valuable insights and actionable guidance, improving the value conversion efficiency of data elements. Therefore, digital capability not only helps companies adapt to dynamic and complex internal and external environmental changes, but also expands the depth and breadth of value creation for manufacturing companies, which is an important prerequisite for a sustainable source of competitive advantage for companies [5].

Research on SMEs’ IT capability in the field of information and communication found that digital capability has a significant positive impact on enterprise performance [6]. At present, there are few direct studies on the impact of digital capability on company performance, and the research on the impact of basic information technology-related capabilities on company performance is relatively abundant. For example, IT capability has a significant positive impact on company performance [14,37], open innovation performance [38,39], and ICT on company performance [40]. Recent studies have found that big data analysis capability has a positive impact on company performance [41], and big data analysis and artificial intelligence capabilities have a positive impact on the sustainable growth and performance of companies [3]. Although existing research has provided some valuable insights, the contribution of different dynamic capabilities to firm performance remains unclear, mainly due to differences in the type and nature of dynamic capabilities, the types of performance indicators used in the studies, and the research methods [42]. From research on the concept and connotation of digital capability, it can be seen that digital capability is a new dynamic capability driven by digital technologies such as big data, cloud computing, internet of things, and artificial intelligence, and plays an important role in the digital and intelligent transformation of manufacturing companies. Therefore, based on the analysis and research on the impact of information technology-related capabilities and single digital technology-related capability on company performance, we proposed the following assumptions:

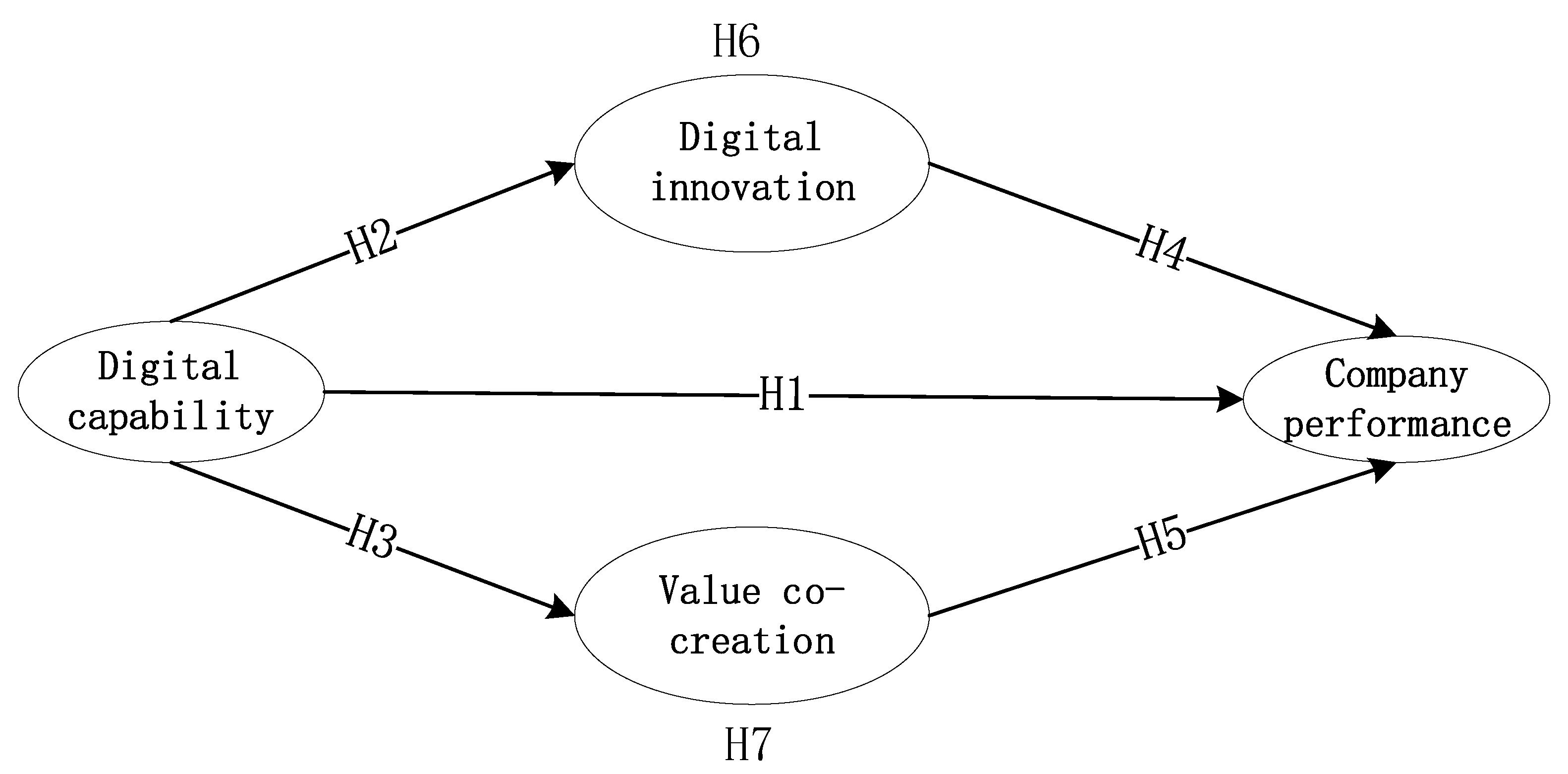

Hypothesis 1 (H1).

Digital capability has a significant positive impact on manufacturing company performance.

Hypothesis 1a (H1a).

Digital capability has a significant positive impact on the financial performance of manufacturing companies.

Hypothesis 1b (H1b).

Digital capability has a significant positive impact on the non-financial performance of manufacturing companies.

3.2. Digital Capability, Digital Innovation, and Value Co-Creation

A manufacturing company’s digital capability reflects the organization’s ability to create new products and processes and respond to changing market conditions [6]. Within the company, digital capability is closely linked to digital innovation. Digital innovation is the change or creation of products, processes, organizational models, and business models that are composed or supported by digital technology [43]. The application of digital technology to changes in products, processes, or business models requires company absorptive capabilities, dynamic resource combination capabilities, and digital environment scanning capabilities [44,45]. Therefore, the initiation, development, and application of digital innovation are inseparable from the process of enabling digital capability support. Capability is a comprehensive mechanism that provides the coherence and integration of practice, and value co-creation practice is inseparable from capability [46]. In the interaction between companies and their external stakeholders, digital capability directly impacts the value co-creation of the company and external stakeholders. In the B2C context, company ICT capabilities affect the value co-creation between companies and customers through perceived value and loyalty [16]. In the B2B context, the information interaction capability (the ability of a company to configure, apply and integrate various information interaction resources) affects the value co-creation and its competitive advantage between companies [17]. The technological capabilities embedded in the digital service process are vital in determining service quality and, ultimately, customer satisfaction, enabling businesses to understand their customers better, improve their service delivery, and respond to customer needs. Empirical research shows that digital service capability is positively correlated with value co-creation [47]. Research on industrial manufacturing companies has found that digital capability affects the value co-creation between companies and customers through perception mechanism and response mechanism [38]. Recent research has also shown that digital capability can trigger, initiate and facilitate interactions between manufacturers and customers, enabling customized service delivery and thus co-creation value [26]. Therefore, based on the relationship mentioned above and research on digital innovation, value co-creation, and digital capability, we proposed the following assumptions:

Hypothesis 2 (H2).

Digital capability has a significant positive impact on digital innovation within an organization.

Hypothesis 3 (H3).

Digital capability has a significant positive impact on external value co-creation in organizations.

3.3. Digital Innovation, Value Co-Creation and Company Performance

The most important characteristic of digital innovation is the successful generation of new IT-enabled products, services, and processes [45]. Most literature regards digital innovation as key for companies to build a sustainable competitive advantage [5,9], and the underlying assumption is that digital innovation has a positive impact on company performance, but few studies have directly examined the impact of digital innovation on company performance. In traditional innovation research, only sporadic studies have concluded that product innovation has a negative impact on performance, and more studies agree that the positive impact of innovation on performance is obvious. In the context of digital technology, due to the very high externalities of digital technology, whether companies can benefit from digital innovation faces great challenges [48]. Most theoretical studies have argued that firm performance is a direct consequence of digital innovation. For example, digital product innovation improves company performance by creating new value for customers, while digital process innovation and digital organization innovation help companies increase the number of new products and improve performance. Digital business model innovation improves performance because it changes the original value acquisition and value creation methods of enterprises, and flexibly responds to dynamic environmental changes [43]. Based on theoretical and empirical research on the impact of digital innovation on company performance, we proposed:

Hypothesis 4 (H4).

Digital innovation has a significant positive impact on manufacturing company performance.

Regarding the results of value co-creation, previous studies have focused mainly on the impact of value co-creation on customer satisfaction and customer loyalty, providing a wealth of indirect evidence for the relationship between value co-creation and firm performance. For example, value co-creation behavior has a positive impact on customer attitude loyalty and behavior loyalty [49]. Furthermore, customer loyalty has an obvious impact on performance indicators such as sales, market share, and profit [50]. Some studies have explored the relationship between value co-creation and firm performance. Consumer-inspired products outperformed their designer-designed counterparts in key market performance indicators, including revenue and profit [51]. In a recent study, the impact of consumer-participated value co-creation on SMEs’ performance in the manufacturing and service industries was investigated, and it was found that value co-creation brought positive operational performance to service providers and manufacturers and to financial performance and that it has a more substantial impact on service-oriented companies than manufacturing companies [52]. In existing research, the relationship between value co-creation and firm performance is indirect and uncertain. From the perspective of the practice of digital manufacturing companies, its value creation activities are no longer limited to the company, and the co-creation of value by multiple subjects has become the normal state of value creation. Based on empirical evidence and theoretical research, we proposed the following hypothesis:

Hypothesis 5 (H5).

Value co-creation has a significant positive impact on manufacturing firm performance.

3.4. The Mediating Effect of Digital Innovation and Value Co-Creation

Research has found no correlation between IT capabilities and business performance, and this study calls on future researchers to identify other variables that may affect the relationship between IT capabilities and business performance [53]. The relationship between digital technology-related capabilities and company performance has attracted scholars’ attention. Khin and Ho [6] have proposed that digital innovation plays a mediating effect in the impact of digital orientation and digital capabilities on company performance. This mediating effect has been supported by empirical research on IT SMEs in the ICT field. As digitally native companies, IT companies are born with digital capabilities and are easily able to apply digital capabilities to the innovation process. Therefore, the applicability of the research conclusions of Khin and Ho [6] to other fields or types of companies deserves further exploration. Zhang et al. [3] have further investigated how the innovation process (sustainable design and commercialization) translates big data analysis capability and artificial intelligence capability into sustainable growth and performance, providing inspiration for this study. The above analysis finds that the link between digital capability and firm performance has not been established in transformative manufacturing firm research. Drawing on existing theoretical and empirical studies, we proposed the following hypothesis:

Hypothesis 6 (H6).

Within companies, digital innovation plays a mediating effect between digital capability and company performance.

Emerging digital technologies affect the internal and external operating environments of companies. Digital capability driven by digital technologies not only affects the internal innovation process, operation process and organizational structure of companies, but also plays an important role in the interaction between companies and their external stakeholders. When the exchange of resources outside the company depends on the availability and accessibility of information and communication technologies, the complex interactions between economic actors are value co-creation processes enabled by technology. Digital capability expands the space for value co-creation and increases the depth of interactions between firms and external stakeholders [36]. The value co-creation enabled by digital capability promotes the exchange of resources between enterprises and external stakeholders. The higher the external stakeholders depend on digital technology, the more opportunities for value co-creation and the greater the co-created value.

With modern digital technology, the business environment is transforming into a digital ecosystem, the interdependence between companies, and between companies and customers is increasingly affected by digital connections. Traditional companies can embrace digital ecosystems through digital customer orientation, thereby creating value together with external stakeholders [54]. Therefore, based on empirical evidence and theoretical analysis, we proposed:

Hypothesis 7 (H7).

Outside the company, value co-creation plays a mediating effect between digital capabilities and company performance.

To sum up, we proposed a theoretical model of the relationship between digital capabilities and company performance based on the dynamic capability view, as shown in Figure 1.

4. Research Design

4.1. Sample and Data Collection

Manufacturing companies are our research objects. Our survey found that traditional manufacturing companies’ understanding of digital capability is limited to traditional IT capabilities, ICT capabilities and other low-level information technology capabilities. Manufacturing companies that are undergoing digital transformation or have successfully transformed their understanding of the concept and connotation of digital capability are closer to our research. In order to accurately reveal the impact of digital capability on company performance, we took manufacturing companies undergoing digital transformation and successful transformation as the survey objects and collected relevant data through questionnaires.

We conducted filed survey research on companies around us that claim to be digitally transforming or have completed the digital transformation. During the survey, it was found that most of the surveyed companies only included digitalization and digital transformation in their company development plans. The underlying reason is that the digital transformation of most traditional manufacturing companies is demand-oriented. When the current production and management of companies meet customer needs, companies are not motivated to digital transformation. Due to resource constraints, time costs, and company licenses, it is difficult to collect data that meet research requirements. To this end, we commissioned a third-party questionnaire survey agency (Questionnaire Star) to collect data. A total of 433 questionnaires were distributed through filed survey and email, and the data that affected the accuracy and quality of the questionnaire, such as vacancies in key items, invalid company establishment time, and online questionnaire filling time fewer than 3 min and more than 20 min, were removed. Finally, 209 valid questionnaires were obtained. The effective questionnaire recovery rate was 48.27%. Table 1 shows the demographic information of the sample.

4.2. Measures

All constructs in the study were measured using a 7-point Likert scale, with values from 1 (strongly disagree or very low) to 7 (strongly agree or very high), in order to test the quality of the questionnaire, certain items were measured in reverse. The sources of the items in the questionnaire are as follows:

The measurement of digital capability draws on Zhou and Wu [55]’s measurement of technical capability and Khin and Ho [6]’s measurement of digital capability, including five items: acquiring important digital skills; identifying new digital opportunities; respond to digital transformation; master the most advanced digital technologies; use digital technologies to continuously develop a series of innovations. Although some scholars have carried out conceptual dimension research on digital capability, arguing that digital capability is composed of three dimensions: intelligence capability (data capture capability), connectivity capability, and analytical capability [26,36], there is currently no specific measure of digital capability. Zhou and Wu [55] published an article in Strategic Management Journal on the basis of existing research and proposed five measurement indicators for measuring technical capabilities, which have been recognized by management scholars and are widely used in the measurement of technology-related capabilities. Therefore, we mainly draw on this maturity measure.

The measurement of digital innovation draws on the measurement of company innovation by Paladino [56]. The original scale includes seven items. On this basis, Khin and Ho [6] modified it in combination with the background of digital innovation, and the revised scale includes six items. Since the definition of digital innovation is similar to that of Khin and Ho [6], we draw on their five measurement items for digital innovation: our digital solutions are of superior quality compared to our competitors; our digital solutions are even more functional; the application of our digital solutions is completely different from that of our competitors; our digital solutions differ from our competitors in terms of product platforms; and at release, some of our digital solutions are new to the market.

The measurement of value co-creation draws on the two-dimensional and third-order construct measures proposed by Ranjan and Read [57]. The scale measures from two dimensions of co-production and value in use. After expert evaluation and pre-filling of the questionnaire, according to the research context of our research, one item was deleted from the co-production dimension, three items were deleted from the value in use dimension, and the other items remained unchanged. In addition to the Ranjan and Read [57] scales, the value co-creation measurement based on the DART model is also widely used in academia. Comparing the two value co-creation scales, the measurement items of Ranjan and Read [57] can better reflect the value co-creation process between enterprises and external stakeholders in the context of the digital economy and are more suitable for the context of our study.

The measurement of company performance uses two widely used indicators of financial performance and non-financial performance. Referring to the measurement of company performance by Hogan and Coote [58], the financial performance is measured by three items: “compare with competitors, the overall profit/net profit rate/sales growth rate of the company”; non-financial performance is measured by three items, “Company’s customer satisfaction/customer retention/attraction of new customers compared to competitors”. The questionnaire is given in Appendix B.

5. Data Analysis and Results

5.1. Control and Testing for Common Method Variation

Common method variation refers to the bias caused by the measuring method, which may cause correlations between constructs to expand or contract when the same method is used to measure two or more constructs [59]. We used self-reported data and collected data on all constructs at the same time, so there may be problems with common methodological variability. For the possible common method bias problem, measures such as anonymous measurement and reverse measurement of some items were adopted in the implementation process to control the common method variation procedurally. After data collection, Harman’s single factor test was used to test for common method variance. The generated principal components analysis output revealed 8 components with eigenvalues greater than 1 explain 58.657% of the total variance; the first unrotated factor captured only 32.457% (less than 40%), indicating that there was no serious common method variation in this study.

5.2. Reliability and Validity Testing

The reliability of the questionnaire was tested by Cronbach’s α coefficient and the overall reliability of the questionnaire was 0.937. As Table 2 reports, except for measurement variable “DI_3” whose factor loading was 0.687, the factor loading of other measurement variables reached 0.7. The commonly used Kline criterion shows that the scale has high consistency reliability.

The measurement items of the questionnaire are all scales that have been studied and are widely used by scholars in related research fields, which ensures the content validity of the scale. Further confirmatory factor analysis was performed using AMOS 24.0. As Table 2 reports, the results show that the factor loadings of the four latent variables of digital capability, digital capability, digital innovation, value co-creation, and company performance are all greater than 0.5 and are significant at the significance level of 0.05 and that the estimated values of all parameter statistics reach the significance level. Furthermore, the absolute value of the standardized residuals is less than 2, the composite reliability (CR) of the latent variables is all greater than 0.7, and the average variance extraction (AVE) value is great than the commonly used standard (0.5). Therefore, it can be considered that the scale has good validity.

5.3. Hypothesis Testing

The research obtained the latent variable data by adding and averaging the measurement items. Table 3 presents the means, standard deviation, and correlation coefficient of the independent, mediator, and dependent variables. It can be seen from Table 3 that digital capability is significantly positively correlated with digital innovation, value co-creation, and corporate performance. Digital innovation is significantly positively correlated with company performance, and value co-creation is significantly positively correlated with company performance. When the correlation between variables is high, there may be multicollinearity problems. The variance inflation factor (VIF) test was performed, and the results show that the VIF value of each variable was between [2, 3.5], which was less than the threshold of 10, indicating that there was no serious multicollinearity problem between the variables.

5.3.1. Main Effect Test

We firstly examined the impact of digital capability on company performance. The results of the regression analysis are shown in Table 4. It can be seen from Table 4 that digital capability had a significant impact on company financial performance, non-financial performance, and overall company performance, with partial regression coefficients of 2.143, 1.905 and 0.675, respectively. After controlling for the variables of the company’s age, asset size, operating revenue and industry sector, digital capability had a significant impact on company financial performance, non-financial performance, and overall company performance. The partial regression coefficients are 2.118, 1.885, and 0.668, respectively. Thus, hypothesis H1 was supported. The control variables of the company’s age, asset size, operating revenue and industry sectors have no significant impact on company performance.

We further regression analyzed the impact of digital capability on digital innovation and value co-creation. It can be seen from Table 5 that digital capability had a significant positive impact on digital innovation, and the partial regression coefficient is 0.619. After controlling for the company’s age, assets scale, operating revenue and the industry to which it belongs, the impact of digital capability on digital innovation was still significant, so hypothesis H2 was supported. Digital capability also had a significant positive impact on value co-creation, with a partial regression coefficient of 2.349. After controlling for the variables of the company’s age, asset size, operating revenue and industry sector, the impact of digital capability on value co-creation was still significant. Thus, hypothesis H3 was supported.

On this basis, the impact of digital innovation and value co-creation on company performance was analyzed. It can be seen from Table 6 that the impact of digital innovation on the financial performance, non-financial performance and company performance was 2.160, 2.014 and 0.696 respectively, p < 0.001, reaching a significant level, indicating that digital innovation had a significant positive impact on corporate performance. So, hypothesis H4 was supported. The impact of value co-creation on financial performance, non-financial performance and company performance was 2.371, 2.545 and 0.819 respectively, p < 0.001, reaching a significant level, indicating that value co-creation had a significant positive impact on overall performance. Thus, hypothesis H5 was supported.

5.3.2. Mediation Effect Test

The mediation effect test follows the Bootstrapping mediation effect testing method and procedure proposed by Zhao et al. [60] and Hayes et al. [61]. The PROCESS V3.5 plug-in was used, model 4 was selected, the sample size was selected as 5000, and the sampling method was selected as a bias-corrected nonparametric percentile method, the statistical results of which are shown in Table 7. The standardized coefficient of the total effect of digital capability on company performance was 0.693, p < 0.001, reaching a significant level, indicating that digital capability had a significant positive impact on company performance, which is consistent with the main effect test and further supports hypothesis H1. The standardized coefficient of the direct effect of digital capability on company performance was 0.312, p < 0.001, reaching a significant level. The standardized coefficient of the indirect effect of digital capability on company performance was 0.381, the 95% confidence interval CI was [0.242, 0.518], and the confidence interval does not include 0, reaching a significant level, indicating that digital capability had a positive indirect effect on company performance. The direct and indirect effects of digital capability on company performance were significant, indicating that there is a partial mediation between digital capability and company performance.

Both digital innovation and value co-creation mediate the impact of digital capabilities on company performance. Among them, in the path of “digital capabilities → Digital innovation → company performance”, the size of the mediating effect of digital innovation was 0.189, and the 95% confidence interval CI was [0.073, 0.293], the confidence interval does not contain 0, reaching the significance level, indicating that digital innovation played a significant mediating effect between digital capabilities and company performance, so hypothesis H6 was supported. In the path of “digital capability → value co-creation → company performance”, the size of the mediating effect of value co-creation was 0.192, the 95% confidence interval CI was [0.087, 0.306], and the confidence interval does not include 0, reaching a significant level, indicating that the value of co-creation is significant. This reveals that value co-creation exerts a significant mediating effect between digital capability and firm performance. Thus, hypothesis H7 was supported.

5.4. Robustness Test

In order to test the reliability of the research conclusions, we selected two ways to conduct robustness tests:

(1) Change the measurement of digital capability and add digital infrastructure as a control variable. According to theoretical studies such those by Lenka et al. [18] and Ajaegbu [26], digital capability consists of three dimensions. Based on the connotation of each dimension, each dimension is measured by two items. For example, the intelligence capability dimension is measured by “① smart products or components can wirelessly transmit information or signals to storage or processing centers” and “② various smart products or hardware are connected together through the network to realize the network function”. The connect dimension is measured by the two items of “① enhancing intelligent functions by embedding intelligent components” and “② perceiving and capturing data in use and operation”. The analytic capability dimension is measured by two items: “① predict or gain insight into customer needs through logical data processing” and “② realize value visualization through scenario simulation”. Digital infrastructure is measured by the status of software and hardware equipment owned by companies (“the number of servers, processors, sensors, intelligent machines and other information and communication equipment owned by the company” and “the company network adopts a more advanced network architecture”). The degree of informatization of the production, manufacturing and operation of the company is measured through “the level of digital realization of informatization in the design, manufacturing, distribution and other links of the company” and “the data of different departments and systems can communicate with each other, and the centralized management of company data is realized”. The degree of information communication between the company and its partners is measured by two items, “there is a digital interactive platform, application or website between the company and the partner” and “the APIs are open between the company and the partner”. The Cronbach’s α of the above scales are all greater than 0.7, indicating that the scales have good reliability.

The main effects and mediating effects are shown in Table 8 and Table 9. It can be seen from Table 6 that after changing the measurement indicators, the digital capability still has a significant positive impact on company performance, digital innovation, and value co-creation, and the control variable digital infrastructure variable is added. Afterward, the positive impact of digital capability on digital innovation and value co-creation has weakened, and the direct effect on company performance is no longer significant. It can be seen from Table 7 that after changing the digital capability measurement indicators, although the direct effect is not significant, the indirect effect is still significant, and the effect is increased compared with the previous one.

(2) Use The sequential test method to test the mediating effect. Regarding the mediation effect test, the commonly used methods include the regression coefficient sequential test method and the bootstrap method. Currently, it is recognized that the bootstrap method is more powerful than the sequential test method. That is, the sequential test method is less likely to detect a significant mediating effect [62]. Therefore, we used the sequential test method to test the robustness of the mediation effect. With reference to the multiple mediation effect test operation, Table 10 and Table 11 were obtained through STATA14 analysis.

It can be seen from Table 10 that the regression coefficient of digital innovation on digital capability (0.604) is significant (SE = 0.050, Z = 11.980), the regression coefficient of value co-creation on digital capability (0.740) is significant (SE = 0.031, Z = 23.910), the regression coefficients (0.357, 0.483) of company performance on digital innovation and value co-creation were significant (SE = 0.064, Z = 5.570; SE = 0.104, Z = 4.640), while the regression coefficient (0.093) of company performance on digital capabilities was not significant (SE = 0.091, Z = 1.020), it can be seen that the direct effect of digital capability on company performance was not significant. It can be seen from Table 9 that the indirect effects were all significant. The indirect effect of digital innovation was 0.215 (SE = 0.043, Z = 5.050), and the indirect effect of value co-creation was 0.358 (SE = 0.079, Z = 4.550). The total indirect effect was 0.572 (SE = 0.083, Z = 6.900).

To sum up, when the digital capability is measured by conceptual studies of digital capability, the direct impact of digital capability on company performance is not significant, but the indirect effects of digital innovation and value co-creation are still significant. This is because the digital capability measure used in this paper was adapted from a technology capability-related measure, which understands a firm’s digital capability level through a report on the firm’s digital technology, acquisition, and identification of digital capability. The measurement based on the theoretical study of digital capability focuses on the level of use of digital infrastructure by companies, so the control variable “digital infrastructure” is added. From the regression analysis, it can be seen that the impact of digital infrastructure on company performance weakens the impact of digital capability on company performance. The above robustness test results once again prove the reliability of the double-mediation effect model. Regarding the direct effect of digital capability on firm performance, the research calls for the development of specialized digital capability measurement scales for broader empirical testing.

6. Conclusions and Discussion

6.1. Conclusions

According to the empirical test results, we draw the following conclusions: Digital capability has a significant and positive impact on business performance. Our research conclusion is consistent with that of Khin and Ho [6] and Hao et al. [41]. Digital capability is a composite capability driven by emerging digital technologies. It not only emphasizes the use of a certain digital technology (such as big data, and artificial intelligence) to gather, integrate and deploy specific company resources but also emphasizes the formation of comprehensive capabilities through the use of multiple digital technologies. The digital infrastructure, the scope of influence, application areas, and value creation logic of digital capabilities are fundamentally different from IT-related capabilities. From Appendix A, we can see that there are still differences in the definition and measurement of digital capability in existing research. Many studies measure the digital capability of companies from the number of computers, the number of IT software, ICT proficiency, and IT human resources, which obviously cannot reflect the intelligent, connected, and insightful nature of digital capability. IT-related capabilities support the informatization and automation transformation of companies, while digital capabilities support the digital and intelligent transformation of companies. In-depth interviews with manufacturing executives also support the study’s conclusion that digital capability not only affects innovation, organization, and management processes within a company but also enables customized service delivery by triggering, initiating, and facilitating interactions between companies and customers, enabling customized service delivery, thereby promoting business performance.

Within companies, digital innovation plays a partial mediating role in the impact of digital capability on company performance. Digital capabilities are higher-level company capabilities than basic information technology capabilities such as IT and ICT capabilities and are composite capabilities empowered by emerging digital technologies. Empirical research shows that digital capability can directly affect the digital innovation process. In the case of digital innovation, digital capability is necessary to integrate digital technologies and professional digital talents. This makes up for the deficiencies of companies in the implementation of digital innovation, because only companies with management that understands new technologies and skills are willing to adopt these technologies and are able to commit to transforming these technologies and capabilities into new products, services and improvements to innovative processes.

For outside companies, value co-creation plays a partial mediating role in the impact of digital capabilities on company performance. The connect and analytical capabilities that digital capability brings to companies play an important role in the interaction between companies and their external stakeholders. Based on the wireless communication network, companies can not only connect and share information in real-time with suppliers, distributors, customers, and other stakeholders but also transform the in-use information shared by stakeholders into valuable insights made feasible through data analysis and processing. Through empirical analysis, we further discovered the impact of digital capabilities on internal and external enterprises, indicating that external digital capabilities mainly affect company performance through value co-creation.

6.2. Theoretical Contributions

This study makes some contributions to the literature. First, the digital capability research literature proposes three outcomes of digital capability: building competitive advantage within the company, building competitive advantage outside the company, and realizing value co-creation [4]. Through the mediation effect test, this study finds that digital capabilities establish internal competitive advantages of enterprises by influencing digital innovation. Although digital capabilities not only affect the innovation of products (or services) within the company but also affect the degree of process digitization, organizational management, organizational structure, and design, for manufacturing companies, manufacturing is its core department. Digital innovation in core sectors is a key source of competitive advantage within a company. Furthermore, digital capability increases the opportunities for companies to share information and create value with multiple external stakeholders, thereby enhancing the company’s position and power in its stakeholder network and achieving external competitive advantages.

Second, digital transformation is a process in which digital technology induces disruption, triggering a strategic response from an organization that seeks to change its value creation path while managing both positive and negative outcomes that affect the process [1]. Digital technologies provide the impetus for organizations to implement countermeasures to gain or maintain their competitive advantage. A key issue related to the effectiveness of these responses is the digital capabilities of the company. Our study examined the positive impact of digital capabilities on digital innovation and value co-creation through two measures. Empirical evidence was provided to examine the role of digital capabilities in the digital transformation of companies. Although this paper mainly focused on the positive impact of digital capability on companies, one should also be aware that excessive reliance on digital capabilities in the process of digital transformation may also bring limitations to companies [63], such as functional stupidity and occupational risks, etc.

Finally, the impact of technology and capability on value creation has been a concern for research in the stream of value co-creation research [1,26,36]. Our study further confirms that digital capability is an antecedent to value co-creation. In manufacturing, digital capability further facilitates the creation of co-production and value-in-use. With the adoption of digital technology and the development of digital capabilities, the value creation activities of manufacturing companies have expanded from production ecosystems to consumption ecosystems, and all value creation activities have co-creation characteristics. Our paper also responds to Ramaswamy et al. [64], who proposed an interactional creation framework.

6.3. Management Implications

Manufacturing companies that are undergoing digital transformation and that have completed digital transformation need to pay attention to and cultivate digital capability. As a high-level dynamic capability, digital capability can help manufacturing companies quickly respond to internal and external environment changes and provide innovative digital solutions according to market competition and customer needs. In the context of modern digital technologies, business environments are transforming into digital ecosystems, and the interdependence of traditional companies is increasingly affected by digital connectivity. From the sensors placed in the soles of sports shoes to sense and capture user information and perform motion analysis (such as “Nike+”), to smart homes that can sense the environment, air quality, and personalized recommendations (such as “Haier U-home”), to 5G, internet of things self-driving cars (such as “Tesla”) that use a combination of digital technologies such as artificial intelligence. The realization of these products, services and processes is inseparable from the use of the company’s digital capability. As proposed by management scholars, companies need to cultivate a new capability to embrace the digital ecosystem to create value, and digital capability is the key capability that manufacturing companies need to possess in the context of the digital economy.

Digital innovation and value co-creation are important ways to leverage the impact of digital capability on company performance. Whether digital capability can be translated into business performance depends to a large extent on the application of digital capability by companies. Within the company, although the scenarios and spaces for the application of digital capability are large, the key to transforming digital capability into company performance is to help companies provide new products, and services and optimize processes. Therefore, companies need to apply digital capability to the links and scenarios that can bring substantial changes to the company in order to avoid the dilemma that large-scale and high-cost economic investment cannot be transformed into company performance. Outside the company, digital capability can help companies establish new resource connections with external stakeholders, gain insight into value co-creation opportunities, and improve market value creation methods. Thus, participants will realize value co-creation, benefit-sharing and risk-sharing.

6.4. Limitations and Direction for Future Research

There are deficiencies in our research. First, the questionnaire survey only obtained data from 209 companies, and the sample size is limited. Only half of the sample companies have completed the digital transformation, and small and medium-sized companies account for a large proportion, which has limitations in terms of sample size and company scale. Future research can expand the sample size and the proportion of companies of different sizes to obtain more convincing research results. Secondly, since there is no measurement scale on the three dimensions of digital capability, the measurement of digital capability mainly draws on the improved items of the technical capability maturity scale, which may affect the accuracy of digital capability measurement. Future research can develop special digital capability measurement scale.

Author Contributions

Conceptualization, X.W. and Y.G.; methodology, X.W., M.A. and C.X.; data collection X.W. and Y.G.; writing—original draft preparation, X.W. and Y.G. writing—review & editing, X.W., C.X., M.A. and Y.G. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by the project supported by the Social Science Fund of Shandong (grant number 21CSDJ02). The authors are grateful for the receipt of these funds.

Data Availability Statement

The datasets used or analyzed in this are accessible from the corresponding author on demand.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

Representative literature of empirical research on digital capability in the past five years.

Table A1.

Representative literature of empirical research on digital capability in the past five years.

| Authors (Year) | Area (Industry) | Construct | Measure | Research Design |

|---|---|---|---|---|

| Lenka et al. (2017) [36] | Europe (Manufacturing companies) | Digitalization capabilities: (1) intelligence capability, (2) connect capability, and (3) analytic capability. | \ | Case study |

| Khin and Ho (2019) [6] | Malaysia (ICT industry) | Digital capability | Measured by 5 items: (1) Acquiring important digital technologies; (2) Identifying new digital opportunities; (3) Responding to digital transformation; (4) Mastering the state-of-the-art digital technologies; (5) Developing innovative products/service/process using digital technology. | Quantitative analysis |

| Calle et al. (2020) [27] | Spanish (manufacturing Companies) | Digital capabilities: (1) for production, (2) for commercial relationships within the company’s supply chain and (3) for developing and implementing software and applications. | Measured items mainly involve the use of CDA, Internet, and ICT technologies. | Quantitative analysis |

| Hirvonen et al. (2020) [13] | Finland (manufacturing SMEs) | Digital capabilities | The DigiMat method was used for the evaluation. | Quantitative analysis |

| Ajaegbu (2020) [26] | Britain (truck manufacturing) | Digital capabilities: (1) data capturing capability, (2) connectivity capability, and (3) analytical capability. | \ | Case study |

| Edu et al. (2020) [12] | \ | Digital innovation capabilities: (1) internet of things (IoTs) capabilities, (2) big data analytics capabilities, (3) cloud computing (CC) capabilities | \ | Qualitative analysis |

| Proksch et al. (2021) [29] | German (new ventures) | Digital IT capabilities | Measured by 7 items: (1) We adapt our digital offerings whenever changing business needs arise. (2) We implement new digital products and services on a regular basis. (3) Our IT integrates the most current digital offerings by third parties like digital payments, customer relationship management systems, and others. (4) Our company provides access to a variety of digital devices. (5) We use the most current IT infrastructure. (6) We store all data digitally. (7) We have Internet access with gigabit speed. | Quantitative analysis |

| Wielgos et al. (2021) [23] | \ | Digital business capability: (1) digital strategy;(2) digital integration;(3) digital control | Measured by 11 items involving digital strategy, digital integration and digital control. | Qualitative and quantitative analysis |

| Vasconcellos et al. (2021) [28] | Brazil (different industries) | Digital Capabilities | Measured by 25 items involving digital technology, ecosystem connectivity (digital ecosystem and digital platform) | |

| Annarelli et al. (2021) [4] | \ | Digitalization capabilities: (1) reconfiguring firms’ digital resources and routines, (2) seizing firm’s digital capabilities, (3) sensing opportunities and threats | \ | review |

| Heredia et al. (2022) [30] | Multiple countries (\) | Digital capabilities | Measured by online activity, delivery, and the adoption of remote work. | Quantitative analysis |

Appendix B

Table A2.

Constructs, questionnaire items and literature.

| Questionnaire Items | Source |

|---|---|

| Digital capability: Please rate whether the following statements apply to your company on a scale from 1 (strongly disagree) to 7 (strongly agree). DCL_1: Our company can acquire important digital technologies. DCL_2: Our company can identify new digital opportunities. DCL_3: Our company can respond to digital transformation. DCL_4: Our company mastering the state-of-the-art digital technologies. DCL_5: Our company developing innovative products/service/process using digital technology. | Zhou and Wu (2010) [55]; Khin and Ho (2019) [6] |

| Digital innovation: Please rate whether the following statements apply to your company on a scale from 1 (strongly disagree) to 7 (strongly agree). DI_1: Our digital solutions are of superior quality compared to our competitors. DI_2: Our digital solutions are even more functional. DI_3: The application of our digital solutions is completely different from that of our competitors. DI_4: Our digital solutions differ from our competitors in terms of product platforms. DI_5: At release, some of our digital solutions are new to the market. | Khin and Ho (2019) [6] |

| Value co-creation: Please rate whether the following statements apply to your company on a scale from 1 (strongly disagree) to 7 (strongly agree). CP_1: Our company was open to my ideas and suggestions about its existing products or towards developing a new product. CP_2: Our company provided sufficient illustrations and information to me. CP_3: I would willingly spare time and effort to share my ideas and suggestions with the company in order to help it improve its products and processes further. CP_4: Our company provided suitable environment and opportunity to me to offer suggestions and ideas. CP_5: Our company had an easy access to information about my preferences. CP_6: Our company considered my role to be as important as its own in the process. CP_7: We shared an equal role in determining the final outcome of the process. CP_8: During the process I could conveniently express my specific requirements. CP_9: Our company conveyed to its consumers the relevant information related to the process. CP_10: Our company allowed sufficient consumer interaction in its business processes (product development, marketing, assisting other customers, etc.). CP_11: In order to get maximum benefit from the process (or, product), I had to play a proactive role during my interaction (i.e., I have to apply my skill, knowledge, time, etc.). ViU_1: It was a memorable experience for our customers (i.e., the memory of the process lasted for quite a while). ViU_2: It was possible for a consumer to improve the process by experimenting and trying new things. ViU_3: The benefit, value, or fun from the process (or, the product) depended on the user and the usage condition. ViU_4: The party tried to serve the individual needs of each of its consumer. ViU_5: Different consumers, depending on their taste, choice, or knowledge, involve themselves differently in the process (or, with the product). ViU_6: I felt an attachment or relationship with the company. ViU_7: There was usually a group, a community, or a network of consumers who are a fan of the company. ViU_8: The company was renowned because its consumers usually spread positive word about it in their social networks. | Ranjan and Read (2016) [57] |

| Company Performance: Please rate whether the following statements apply to your company on a scale from 1 (very low) to 7 (very high). FP_1: Compare with competitors, the overall profit rate of the company. FP_2: Compare with competitors, the net profit rate of the company. FP_3: Compare with competitors, the sales growth rate of the company. FP_4: Company’s customer satisfaction compared to competitors. FP_5: Company’s customer retention compared to competitors. FP_6: Company’s attraction of new customers compared to competitors. | Hogan and Coote (2014) [58] |

References

- Vial, G. Understanding digital transformation: A review and a research agenda. J. Strateg. Inf. Syst. 2019, 28, 118–144. [Google Scholar] [CrossRef]

- Karimi, J.; Walter, Z. The role of dynamic capabilities in responding to digital disruption: A factor-based study of the newspaper industry. J. Manag. Inf. Syst. 2015, 32, 39–81. [Google Scholar] [CrossRef]

- Zhang, H.; Song, M.; He, H. Achieving the success of sustainability development projects through big data analytics and artificial intelligence capability. Sustainability 2020, 12, 949. [Google Scholar] [CrossRef] [Green Version]

- Annarelli, A.; Battistella, C.; Nonino, F.; Parida, V.; Pessot, E. Literature review on digitalization capabilities: Co-citation analysis of antecedents, conceptualization and consequences. Technol. Forecast. Soc. Change 2021, 166, 120635. [Google Scholar] [CrossRef]

- Leão, P.; da Silva, M.M. Impacts of digital transformation on firms’ competitive advantages: A systematic literature review. Strateg. Change 2021, 30, 421–441. [Google Scholar] [CrossRef]

- Khin, S.; Ho, T.C. Digital technology, digital capability and organizational performance: A mediating role of digital innovation. Int. J. Innov. Sci. 2019, 11, 177–195. [Google Scholar] [CrossRef]

- Badasjane, V.; Granlund, A.; Ahlskog, M.; Bruch, J. Coordination of digital transformation in international manufacturing networks—Challenges and coping mechanisms from an organizational perspective. Sustainability 2022, 14, 2204. [Google Scholar] [CrossRef]

- Mingaleva, Z.; Deputatova, L.; Starkov, Y. Management of organizational knowledge as a basis for the competitiveness of enterprises in the digital economy. In Proceedings of the International Conference on Integrated Science, Georgia, Batumi, 10–12 May 2019; pp. 203–212. [Google Scholar]

- Berawi, M.A.; Suwartha, N.; Asvial, M.; Harwahyu, R.; Suryanegara, M.; Setiawan, E.A.; Maknun, I.J. Digital innovation: Creating competitive advantages. Int. J. Technol. 2020, 11, 1076–1080. [Google Scholar] [CrossRef]

- Van Veldhoven, Z.; Vanthienen, J. Digital transformation as an interaction-driven perspective between business, society, and technology. Electron. Mark. 2021. [Google Scholar] [CrossRef]

- Anim-Yeboah, S.; Boateng, R.; Odoom, R.; Kolog, E.A. Digital transformation process and the capability and capacity implications for small and medium enterprises. Int. J. E-Entrep. Innov. 2020, 10, 26–44. [Google Scholar] [CrossRef]

- Edu, S.A.; Agoyi, M.; Agozie, D.Q. Integrating digital innovation capabilities towards value creation: A conceptual view. Int. J. Intell. Inf. Technol. 2020, 16, 37–50. [Google Scholar] [CrossRef]

- Hirvonen, J.; Majuri, M. Digital capabilities in manufacturing SMEs. Procedia Manuf. 2020, 51, 1283–1289. [Google Scholar] [CrossRef]

- Song, M.; Di Benedetto, C.A.; Nason, R.W. Capabilities and financial performance: The moderating effect of strategic type. J. Acad. Mark. Sci. 2007, 35, 18–34. [Google Scholar] [CrossRef]

- Bharadwaj, A.S. A resource-based perspective on information technology capability and firm performance: An empirical investigation. Manag. Inf. Syst. Q. 2000, 24, 169–196. [Google Scholar] [CrossRef]

- Polo Peña, A.I.; Frías Jamilena, D.M.; Rodríguez Molina, M.Á. Value co-creation via information and communications technology. Serv. Ind. J. 2014, 34, 1043–1059. [Google Scholar] [CrossRef]

- Sun, L. Research on the Influence of Enterprise Information Interaction Ability on Value Co-Creation and Competitive Advantage. Ph.D. Thesis, Harbin Institute of Technology, Haerbin, China, 2016. [Google Scholar]

- Li, T.; Li, Q.; Chen, C.X. The influence of data management ability on enterprise productivity: New findings from the survey of chinese enterprise-labor matching. Chin. Ind. Econ. 2020, 174–192. [Google Scholar] [CrossRef]

- Shan, S.; Luo, Y.; Zhou, Y.; Wei, Y. Big data analysis adaptation and enterprises’ competitive advantages: The perspective of dynamic capability and resource-based theories. Technol. Anal. Strateg. Manag. 2019, 31, 406–420. [Google Scholar] [CrossRef]

- Akter, S.; Gunasekaran, A.; Wamba, S.F.; Babu, M.M.; Hani, U. Reshaping competitive advantages with analytics capabilities in service systems. Technol. Forecast. Soc. Chang. 2020, 159, 120180. [Google Scholar] [CrossRef]

- Vovchenko, N.G.; Andreeva, A.V.; Orobinskiy, A.S.; Filippov, Y.M. Competitive advantages of financial transactions on the basis of the blockchain technology in digital economy. Eur. Res. Stud. J. 2017, 20, 193. [Google Scholar] [CrossRef] [Green Version]

- Wang, Z.; Kim, H.G. Can social media marketing improve customer relationship capabilities and firm performance? Dynamic capability perspective. J. Interact. Mark. 2017, 39, 15–26. [Google Scholar] [CrossRef]

- Wielgos, D.M.; Homburg, C.; Kuehnl, C. Digital business capability: Its impact on firm and customer performance. J. Acad. Mark. Sci. 2021, 49, 762–789. [Google Scholar] [CrossRef]

- WU, L.; HITT, L.; Lou, B. Data analytics, innovation, and firm productivity. Manage. Sci. 2020, 66, 2017–2039. [Google Scholar] [CrossRef]

- Sjödin, D.R.; Parida, V.; Wincent, J. Value co-creation process of integrated product-services: Effect of role ambiguities and relational coping strategies. Ind. Market. Manag. 2016, 56, 108–119. [Google Scholar] [CrossRef]

- Ajaegbu, A. The Role and Impact of Digital Capabilities on Value Co-Creation of Servitising Organisations. Ph.D. Thesis, Aston University, Birmingham, UK, 2020. [Google Scholar]

- Calle, A.D.L.; Freije, I.; Ugarte, J.V.; Larrinaga, M.Á. Measuring the impact of digital capabilities on product-service innovation in Spanish industries. Int. J. Bus. Environ. 2020, 11, 254–274. [Google Scholar] [CrossRef]

- Vasconcellos, S.L.D.; Silva Freitas, J.C.D.; Junges, F.M. Digital capabilities: Bridging the gap between creativity and performance. In The Palgrave Handbook of Corporate Sustainability in the Digital Era; Palgrave Macmillan: London, UK, 2021; pp. 411–427. [Google Scholar]

- Proksch, D.; Rosin, A.F.; Stubner, S.; Pinkwart, A. The influence of a digital strategy on the digitalization of new ventures: The mediating effect of digital capabilities and a digital culture. J. Small Bus. Manag. 2021. [Google Scholar] [CrossRef]

- Heredia, J.; Castillo-Vergara, M.; Geldes, C.; Gamarra, F.M.C.; Flores, A.; Heredia, W. How do digital capabilities affect firm performance? The mediating role of technological capabilities in the “new normal”. J. Innov. Knowl. 2022, 7, 100171. [Google Scholar] [CrossRef]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strateg. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef] [Green Version]

- Winter, S.G. Understanding dynamic capabilities. Strateg. Manag. J. 2003, 24, 991–995. [Google Scholar] [CrossRef] [Green Version]

- Yeow, A.; Soh, C.; & Hansen, R. Aligning with new digital strategy: A dynamic capabilities approach. J. Strateg. Inf. Syst. 2018, 27, 43–58. [Google Scholar] [CrossRef]

- Warner, K.S.R.; Wäger, M. Building dynamic capabilities for digital transformation: An ongoing process of strategic renewal. Long Range Plan. 2019, 52, 326–349. [Google Scholar] [CrossRef]

- Lenka, S.; Parida, V.; Wincent, J. Digitalization capabilities as enablers of value co-creation in servitizing firms. Psychol. Mark. 2017, 34, 92–100. [Google Scholar] [CrossRef] [Green Version]

- Melville, N.; Kraemer, K.; Gurbaxani, V. Information technology and organizational performance: An integrative model of IT business value. Manag. Inf. Syst. Q. 2004, 28, 283–322. [Google Scholar] [CrossRef] [Green Version]

- Gómez, J.; Salazar, I.; Vargas, P. Does information technology improve open innovation performance? an examination of manufacturers in Spain. Inf. Syst. Res. 2017, 28, 661–675. [Google Scholar] [CrossRef]

- Ding, X.H.; Wu, S. The impact of IT capabilities on open innovation performance: The mediating effect of knowledge integration capabilities. Bus. Rev. 2020, 32, 149–159. [Google Scholar]

- Yunis, M.; Tarhini, A.; Kassar, A. The role of ICT and innovation in enhancing organizational performance: The catalysing effect of corporate entrepreneurship. J. Bus. Res. 2018, 88, 344–356. [Google Scholar] [CrossRef]

- Hao, S.; Zhang, H.; Song, M. Big data, big data analytics capability, and sustainable innovation performance. Sustainability 2019, 11, 7145. [Google Scholar] [CrossRef] [Green Version]

- Karna, A.; Richter, A.; Riesenkampff, E. Revisiting the role of the environment in the capabilities–financial performance relationship: A meta-Analysis. Strateg. Manage. J. 2016, 37, 1154–1173. [Google Scholar] [CrossRef]

- Liu, Y.; Dong, J.Y.; Wei, J. Digital innovation management: Theoretical framework and future research. Manag. World 2020, 36, 198–217+219. [Google Scholar]

- O’Reilly, C.A.; Tushman, M.L. Organizational ambidexterity: Past, present, and future. Acad. Manag. Perspect. 2013, 27, 324–338. [Google Scholar] [CrossRef] [Green Version]

- Kohli, R.; Melville, N.P. Digital innovation: A review and synthesis. Inf. Syst. J. 2019, 29, 200–223. [Google Scholar] [CrossRef] [Green Version]

- Marcos-Cuevas, J.; Nätti, S.; Palo, T.; Baumann, J. Value co-creation practices and capabilities: Sustained purposeful engagement across B2B systems. Ind. Mark. Manag. 2016, 56, 97–107. [Google Scholar] [CrossRef] [Green Version]

- Saunila, M.; Ukko, J.; Rantala, T. Value co-creation through digital service capabilities: The role of human factors. Inf. Technol. People 2019, 32, 627–645. [Google Scholar] [CrossRef]

- Teece, D.J. Profiting from innovation in the digital economy: Enabling technologies, standards, and licensing models in the wireless world. Res. Policy 2018, 47, 1367–1387. [Google Scholar] [CrossRef]

- Cossío-Silva, F.J.; Revilla-Camacho, M.Á.; Vega-Vázquez, M.; Palacios-Florencio, B. Value co-creation and customer loyalty. J. Bus. Res. 2016, 69, 1621–1625. [Google Scholar] [CrossRef]

- Belás, J.; Gabčová, L. The Relationship among customer satisfaction, loyalty and financial performance of commercial banks. Econom. Manag. 2016, 19, 132–147. [Google Scholar] [CrossRef]

- Nishikawa, H.; Schreier, M.; Ogawa, S. User-generated versus designer-generated products: A performance assessment at Muji. Int. J. Res. Mark. 2013, 30, 160–167. [Google Scholar] [CrossRef]

- Zaborek, P.; Mazur, J. Enabling value co-creation with consumers as a driver of business performance: A dual perspective of polish manufacturing and service SMEs. J. Bus. Res. 2019, 104, 541–551. [Google Scholar] [CrossRef]

- Chae, H.C.; Koh, C.E.; Prybutok, V.R. Information technology capability and firm performance: Contradictory findings and their possible causes. Manag. Inf. Syst. Q. 2014, 38, 305–326. [Google Scholar] [CrossRef]

- Kopalle, P.K.; Kumar, V.; Subramaniam, M. How legacy firms can embrace the digital ecosystem via digital customer orientation. J. Acad. Mark. Sci. 2020, 48, 114–131. [Google Scholar] [CrossRef]

- Zhou, K.Z.; Wu, F. Technological capability, strategic flexibility, and product innovation. Strateg. Manag. 2010, 31, 547–561. [Google Scholar] [CrossRef]

- Paladino, A. Investigating the drivers of innovation and new product success: A comparison of strategic orientations. J. Prod. Innov. Manag. 2007, 24, 534–553. [Google Scholar] [CrossRef]

- Ranjan, K.R.; Read, S. Value co-creation: Concept and measurement. J. Acad. Mark. Sci. 2016, 44, 290–315. [Google Scholar] [CrossRef]

- Hogan, S.J.; Coote, L.V. Organizational culture, innovation, and performance: A test of schein’s model. J. Bus. Res. 2014, 67, 1609–1621. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; Mackenzie, S.B.; Lee, J.Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef]

- Zhao, X.; Lynch, J.G., Jr.; Chen, Q. Reconsidering baron and kenny: Myths and truths about mediation analysis. J. Consum. Res. 2010, 37, 197–206. [Google Scholar] [CrossRef]

- Hayes, A.F. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach; Guilford Publications: New York, NY, USA, 2017. [Google Scholar]