The Dynamic Relationship between China’s Economic Cycle, Government Debt, and Economic Policy

,

,

Abstract

:1. Introduction

2. Research on the Characteristics of China’s Economic Cycle, Economic Policy, and Government Liabilities

3. Empirical Analysis

3.1. Empirical Model Selection and Construction

- (1)

- The synchronization relationship between and

- (2)

- The synchronization relationship between and , and

- (3)

- The synchronization relationship between , and

- (4)

- The synchronization relationship between and

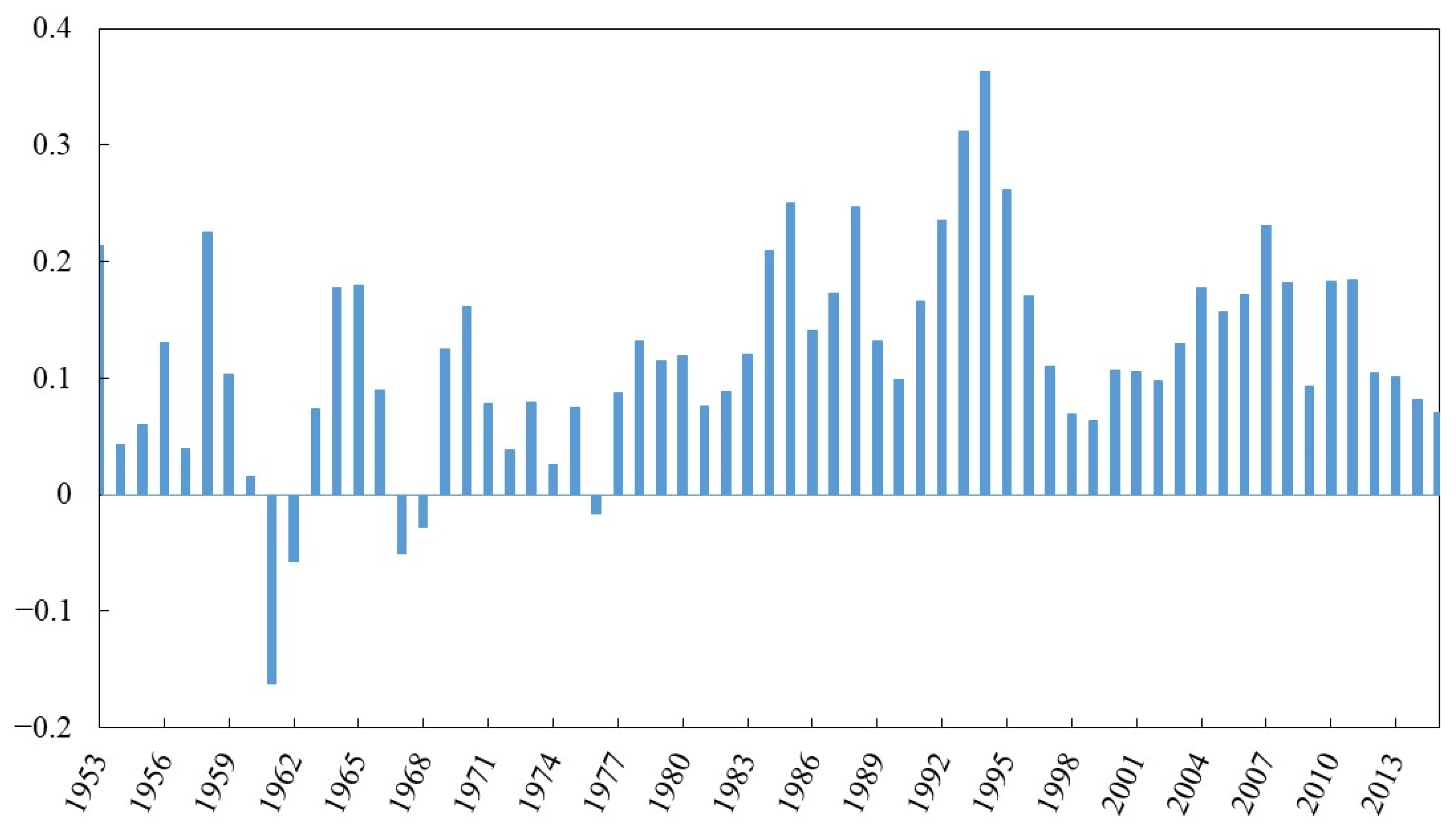

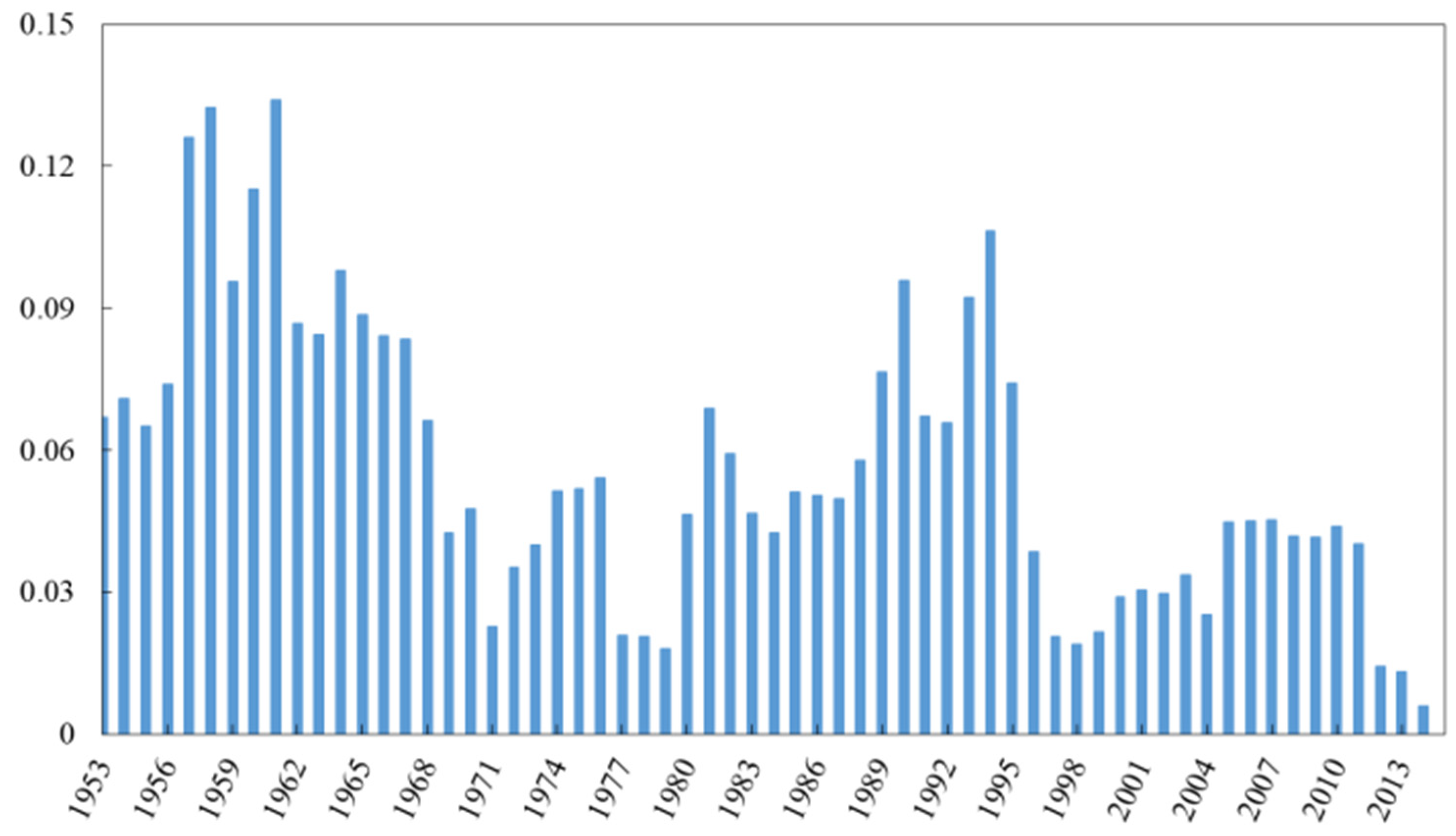

3.2. Data Source

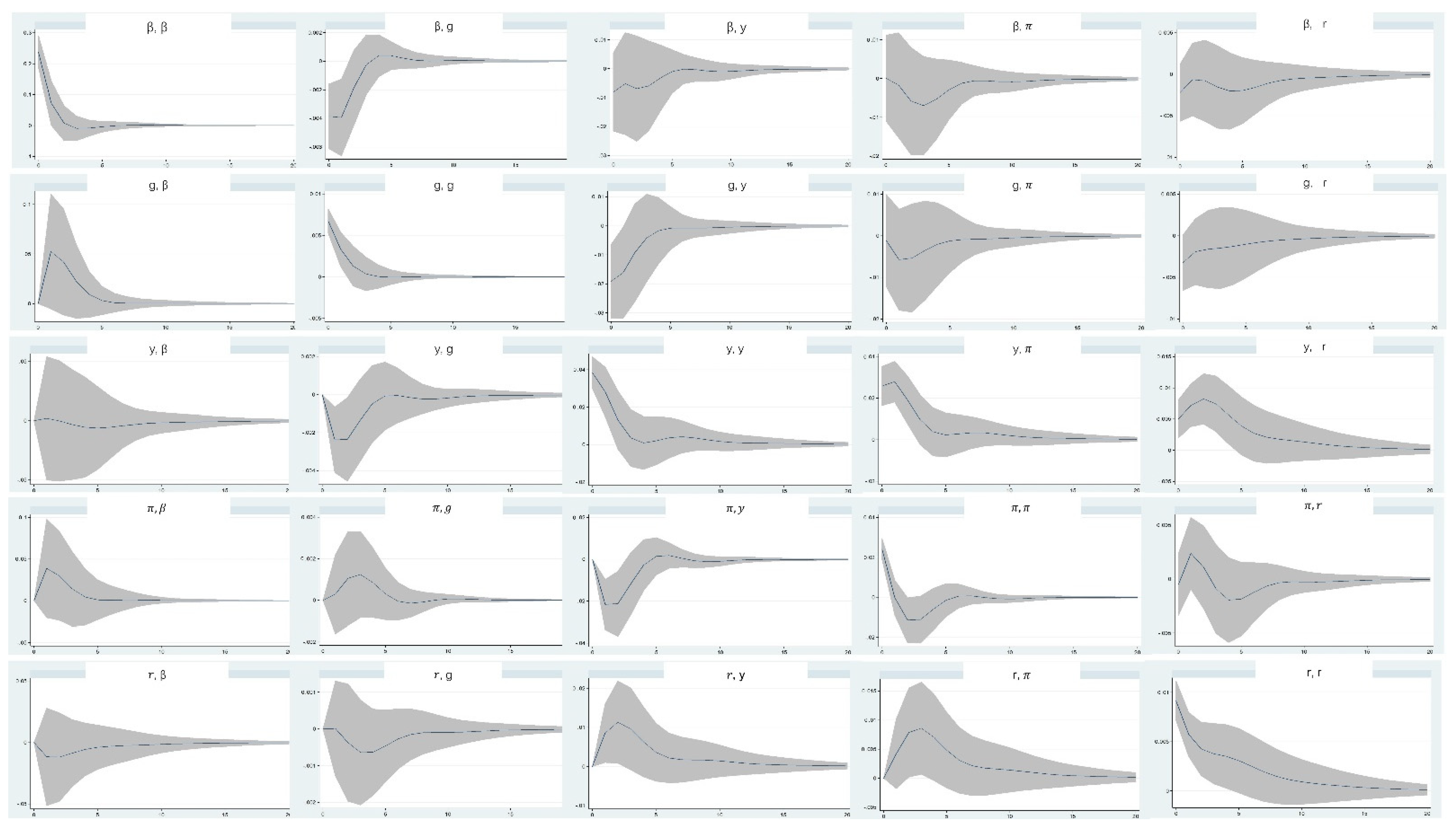

3.3. Impulse Response Analysis

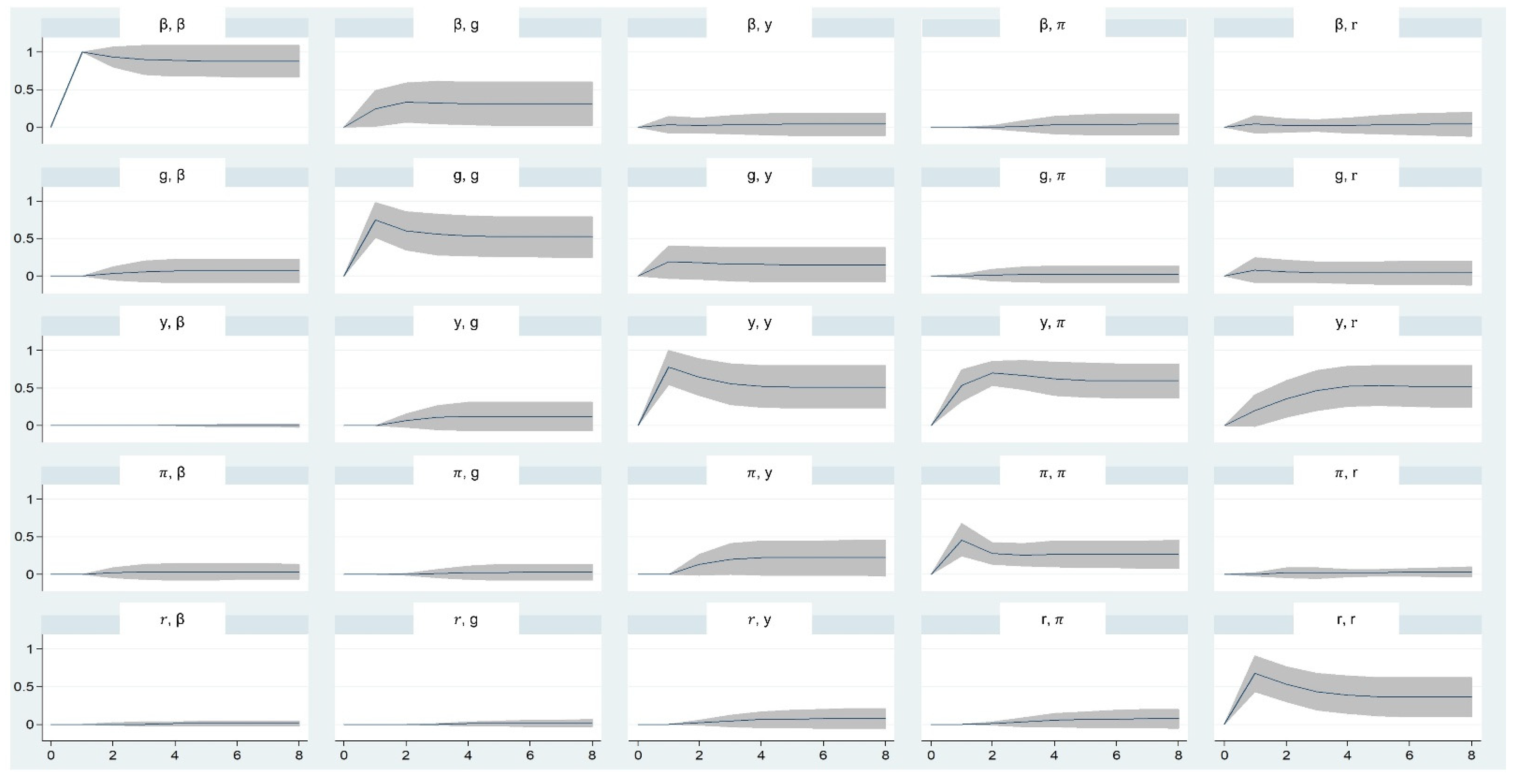

3.4. Variance Decomposition

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Yu, J.; Zhou, K.; Yang, S. Regional heterogeneity of China’s energy efficiency in “new normal”: A meta-frontier Super-SBM analysis. Energy Policy 2019, 134, 110941. [Google Scholar] [CrossRef]

- Cuestas, J.C.; Regis, P.J. On the dynamics of sovereign debt in China: Sustainability and structural change. Econ. Model. 2018, 68, 356–359. [Google Scholar] [CrossRef]

- Xu, J.; Zhang, X. China’s sovereign debt: A balance-sheet perspective. China Econ. Rev. 2014, 31, 55–73. [Google Scholar] [CrossRef]

- Lavee, D.; Beniad, G.; Solomon, C. The effect of investment in transportation infrastructure on the debt-to-GDP ratio. Transport. Rev. 2011, 31, 769–789. [Google Scholar] [CrossRef]

- Taylor, L.; Proano, C.R.; de Carvalho, L.; Barbosa, N. Fiscal deficits, economic growth and government debt in the USA. Camb. J. Econ. 2012, 36, 189–204. [Google Scholar] [CrossRef]

- Parkyn, O.; Vehbi, T. The effects of fiscal policy in New Zealand: Evidence from a VAR model with debt constraints. Econ. Rec. 2014, 90, 345–364. [Google Scholar] [CrossRef] [Green Version]

- Afonso, A.; Gonçalves, L. The policy mix in the US and EMU: Evidence from a SVAR analysis. N. Am. J. Econ. Financ. 2020, 51, 100840. [Google Scholar] [CrossRef] [Green Version]

- Égert, B. Public debt, economic growth and nonlinear effects: Myth or reality? J. Macroecon. 2015, 43, 226–238. [Google Scholar] [CrossRef] [Green Version]

- Checherita-Westphal, C.; Rother, P. The impact of high government debt on economic growth and its channels: An empirical investigation for the euro area. Eur. Econ. Rev. 2012, 56, 1392–1405. [Google Scholar] [CrossRef]

- Watkins, K. Debt relief for Africa. Rev. Afr. Polit. Econ. 1994, 21, 599–609. [Google Scholar] [CrossRef]

- Austin, D.A. Debt Limit: History and Recent Increases; DIANE Publishing: Darby, PA, USA, 2010. [Google Scholar]

- Reinhart, C.M.; Rogoff, K.S. Growth in a Time of Debt. Am. Econ. Rev. 2010, 100, 573–578. [Google Scholar] [CrossRef] [Green Version]

- Jayadev, A.; Konczal, M. The Boom Not the Slump: The Right Time for Austerity. Economics Faculty Publication Series. 26. Available online: https://scholarworks.umb.edu/econ_faculty_pubs/26 (accessed on 15 December 2021).

- Spilioti, S.; Vamvoukas, G. The impact of government debt on economic growth: An empirical investigation of the Greek market. J. Econ. Asymmetries 2015, 12, 34–40. [Google Scholar] [CrossRef]

- Pfaff, B. VAR, SVAR and SVEC models: Implementation within R package vars. J. Stat. Softw. 2008, 27, 1–32. [Google Scholar] [CrossRef] [Green Version]

- Adenomon, M.O.; Oyejola, B.A. Impact of Agriculture and Industrialization on GDP in Nigeria: Evidence from VAR and SVAR Models. Int. J. Anal. Appl. 2013, 1, 40–78. [Google Scholar]

- Zhang, S.; Han, G.; Yu, R.; Wen, Z.; Xu, M.; Yang, Y. The Sustainable Development Path of the Gold Exploration and Mining of the Sanshan Island-Jiaojia Belt in Laizhou Bay: A DID-SVAR Approach. Sustainability 2021, 13, 11648. [Google Scholar] [CrossRef]

- Ahmed, H.J.A.; Wadud, I.M. Role of oil price shocks on macroeconomic activities: An SVAR approach to the Malaysian economy and monetary responses. Energy Policy 2011, 39, 8062–8069. [Google Scholar] [CrossRef]

- Beard, E.; Marsden, J.; Brown, J.; Tombor, I.; Stapleton, J.; Michie, S.; West, R. Understanding and using time series analyses in addiction research. Addiction 2019, 114, 1866–1884. [Google Scholar] [CrossRef] [PubMed]

- Lienau, O. Rethinking Sovereign Debt; Harvard University Press: Cambridge, MA, USA, 2014. [Google Scholar]

- Waibel, M. Decolonization and Sovereign Debt: A Quagmire. In Sovereign Debt Diplomacies; Oxford University Press: Oxford, UK, 2019; pp. 213–231. [Google Scholar]

- Tan, K.H. Fiscal Policy in Dynamic Economies; Routledge: Abingdon, UK, 2016. [Google Scholar]

- Benigno, P.; Woodford, M. Optimal monetary and fiscal policy: A linear-quadratic approach. NBER Macroecon. Annu. 2003, 18, 271–333. [Google Scholar] [CrossRef]

- Bohn, H. The sustainability of fiscal policy in the United States. Sustain. Public Debt 2008, 15–49. [Google Scholar]

- Hansen, A.H. Fiscal Policy & Business Cycles; Routledge: Abingdon, UK, 2013. [Google Scholar]

- Mbanga, C.L.; Darrat, A.F. Fiscal policy and the US stock market. Rev. Quant. Financ. Account. 2016, 47, 987–1002. [Google Scholar] [CrossRef]

- Baharumshah, A.Z.; Mohd, S.H.; Masih, A.M.M. The stability of money demand in China: Evidence from the ARDL model. Econ. Syst. 2009, 33, 231–244. [Google Scholar] [CrossRef]

- Liao, W.; Tapsoba, M.S.J.-A. China’s Monetary Policy and Interest Rate Liberalization: Lessons from International Experiences; International Monetary Fund: Washington, DC, USA, 2014. [Google Scholar]

- Fung, M.K.-Y.; Ho, W.-M.; Zhu, L. The impact of credit control and interest rate regulation on the transforming Chinese economy: An analysis of long-run effects. J. Comp. Econ. 2000, 28, 293–320. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Wang, Y. How stable is the demand for money in China? J. Econ. Dev. 2007, 32, 21. [Google Scholar] [CrossRef]

- Gottschalk, J. An Introduction into the SVAR Methodology: Identification, Interpretation and Limitations of SVAR Models; Kiel Working Paper: Kiel, Germany, 2001. [Google Scholar]

- Giannini, C. Impulse Response Analysis and Forecast Error Variance Decomposition in SVAR Modeling. In Topics in Structural VAR Econometrics; Springer: Berlin/Heidelberg, Germany, 1992; pp. 44–57. [Google Scholar]

- Pesaran, H.H.; Shin, Y. Generalized impulse response analysis in linear multivariate models. Econ. Lett. 1998, 58, 17–29. [Google Scholar] [CrossRef]

- Ivanov, V.; Kilian, L. A practitioner’s guide to lag order selection for VAR impulse response analysis. Stud. Nonlinear Dyn. Econom. 2005, 9, 1–36. [Google Scholar] [CrossRef]

- Campbell, J.Y.; Ammer, J. What moves the stock and bond markets? A variance decomposition for long-term asset returns. J. Financ. 1993, 48, 3–37. [Google Scholar] [CrossRef]

- Callen, J.L.; Segal, D. Do accruals drive firm-level stock returns? A variance decomposition analysis. J. Account. Res. 2004, 42, 527–560. [Google Scholar] [CrossRef]

- Gorodnichenko, Y.; Lee, B. A Note on Variance Decomposition with Local Projections; National Bureau of Economic Research: Cambridge, MA, USA, 2017. [Google Scholar]

- Campbell, S.D.; Davis, M.A.; Gallin, J.; Martin, R.F. What moves housing markets: A variance decomposition of the rent–price ratio. J. Urban. Econ. 2009, 66, 90–102. [Google Scholar] [CrossRef]

- Jawadi, F.; Mallick, S.K.; Sousa, R.M. Fiscal and monetary policies in the BRICS: A panel VAR approach. Econ. Model. 2016, 58, 535–542. [Google Scholar] [CrossRef]

- Yang, X.; Han, L.; Li, W.; Yin, X.; Tian, L. Monetary policy, cash holding and corporate investment: Evidence from China. China Econ. Rev. 2017, 46, 110–122. [Google Scholar] [CrossRef]

- Guo, Q.; Jia, J.; Zhang, Y.; Zhao, Z. Mix of Fiscal and Monetary Policy Rules and Inflation Dynamics in China. China World Econ. 2011, 19, 47–66. [Google Scholar] [CrossRef]

- Liu, J.; Zhang, L. Review, Experience Summary and Prospect of Fiscal and Monetary Policy Coordination Paradigm in the 70 Years of People’s Republic of China. China Financ. Econ. Rev. 2019, 8, 66–82. [Google Scholar]

- Wu, H.; Gao, K.; Hao, X.-J.; Shi, W. The Fiscal Policy of China’s Economic Kinetic Energy Conversion. Soc. Sci. 2018, 7, 115–124. [Google Scholar]

- Qin, D.; Cagas, M.A.; Quising, P.; He, X.-H. How much does investment drive economic growth in China? J. Policy Model. 2006, 28, 751–774. [Google Scholar] [CrossRef] [Green Version]

- Afonso, A.; Aubyn, M.S. Macroeconomic rates of return of Public and Private investment: Crowding-in and Crowding-out effects. Manch. Sch. 2009, 77, 21–39. [Google Scholar] [CrossRef]

- Traum, N.; Yang, S.C.S. When does government debt crowd out investment? J. Appl. Econom. 2015, 30, 24–45. [Google Scholar] [CrossRef] [Green Version]

- Shetta, S.; Kamaly, A. Does the budget deficit crowd-out private credit from the banking sector? The case of Egypt. Top. Middle East. Afr. Econ. 2014, 16, 251–279. [Google Scholar]

- Friedman, B.M. Crowding Out or Crowding in? The Economic Consequences of Financing Government Deficits; National Bureau of Economic Research: Cambridge, MA, USA, 1978. [Google Scholar]

- Levine, R. Financial development and economic growth: Views and agenda. J. Econ. Lit. 1997, 35, 688–726. [Google Scholar]

- Acemoglu, D.; Johnson, S.; Robinson, J.A. The colonial origins of comparative development: An empirical investigation. Am. Econ. Rev. 2001, 91, 1369–1401. [Google Scholar] [CrossRef]

- Rodrik, D. The past, present, and future of economic growth. Challenge 2014, 57, 5–39. [Google Scholar] [CrossRef]

- Wood, A. Openness and wage inequality in developing countries: The Latin American challenge to East Asian conventional wisdom. World Bank Econ. Rev. 1997, 11, 33–57. [Google Scholar] [CrossRef] [Green Version]

- Drucker, P.F. The Changed World Economy; De Gruyter: Berlin, Germany, 2013. [Google Scholar]

- Fischer, S. Growth, macroeconomics, and development. NBER Macroecon. Annu. 1991, 6, 329–364. [Google Scholar] [CrossRef]

- Stiglitz, J.E. The current economic crisis and lessons for economic theory. East. Econ. J. 2009, 35, 281–296. [Google Scholar] [CrossRef]

- Linnemann, L.; Schabert, A. Fiscal policy in the new neoclassical synthesis. J. Money Credit. Bank. 2003, 35, 911–929. [Google Scholar] [CrossRef]

- Goodfriend, M. Monetary policy in the new neoclassical synthesis: A primer. FRB Richmond Econ. Q. 2004, 90, 21–45. [Google Scholar] [CrossRef] [Green Version]

- Mazzocchi, R. Scope and flaws of the new neoclassical synthesis. DEM Discuss. Pap. 2013, 13. [Google Scholar] [CrossRef]

- Taylor, J.B. Discretion Versus Policy Rules in Practice, Carnegie-Rochester Conference Series on Public Policy; Elsevier: Amsterdam, The Netherlands, 1993; pp. 195–214. [Google Scholar]

- Kesha, G. Avoiding the impact of deflation and deflation expectations on economic growth. China Financ. Econ. Rev. 2016, 5, 14–28. [Google Scholar]

- Tooze, A. Is the coronavirus crash worse than the 2008 financial crisis. Foreign Policy 2020. Available online: https://foreignpolicy.com/2020/03/18/coronavirus-economic-crash-2008-financial-crisis-worse/ (accessed on 10 December 2021).

- Eggertsson, G.B.; Krugman, P. Debt, deleveraging, and the liquidity trap: A Fisher-Minsky-Koo approach. Q. J. Econ. 2012, 127, 1469–1513. [Google Scholar] [CrossRef] [Green Version]

- Okina, K.; Shirakawa, M.; Shiratsuka, S. The asset price bubble and monetary policy: Japan’s experience in the late 1980s and the lessons. Monet. Econ. Stud. (Spec. Ed.) 2001, 19, 395–450. [Google Scholar]

- Bernanke, B.S. The new tools of monetary policy. Am. Econ. Rev. 2020, 110, 943–983. [Google Scholar] [CrossRef] [Green Version]

- Reifschneider, D.; Williams, J.C. Three lessons for monetary policy in a low-inflation era. J. Money Credit. Bank. 2000, 32, 936–966. [Google Scholar] [CrossRef] [Green Version]

- Reifschneider, D.; Wascher, W.; Wilcox, D. Aggregate supply in the United States: Recent developments and implications for the conduct of monetary policy. IMF Econ. Rev. 2015, 63, 71–109. [Google Scholar] [CrossRef] [Green Version]

- Chen, Y. National Finance: A Chinese Perspective; Springer Nature: Heidelberg, Germany, 2021. [Google Scholar]

- Tobin, J. Money and finance in the macroeconomic process. J. Money Credit. Bank. 1982, 14, 171–204. [Google Scholar] [CrossRef]

- Schularick, M.; Taylor, A.M. Credit booms gone bust: Monetary policy, leverage cycles, and financial crises, 1870–2008. Am. Econ. Rev. 2012, 102, 1029–1061. [Google Scholar] [CrossRef] [Green Version]

- Naughton, B. Understanding the Chinese stimulus package. China Leadersh. Monit. 2009, 28, 1–12. [Google Scholar]

- Morrison, W.M. In China and the Global Financial Crisis: Implications for the United States; Library of Congress Washington DC Congressional Research Service: Washington, DC, USA, 2009. [Google Scholar]

- Yufeng, C.; Zhipeng, Y.; Guan, H. The Financial Crisis in Wenzhou: An Unanticipated Consequence of China’s “Four Trillion Yuan Economic Stimulus Package”. China An. Int. J. 2018, 16, 152–173. [Google Scholar]

- Whalley, J.; Zhao, X. The relative importance of the Chinese stimulus package and tax stabilization during the 2008 financial crisis. Appl. Econ. Lett. 2013, 20, 682–686. [Google Scholar] [CrossRef]

- Balfoussia, H.; Gibson, H.D. Firm investment and financial conditions in the euro area: Evidence from firm-level data. Appl. Econ. Lett. 2019, 26, 104–110. [Google Scholar] [CrossRef]

- Alpanda, S.; Zubairy, S. Addressing household indebtedness: Monetary, fiscal or macroprudential policy? Eur. Econ. Rev. 2017, 92, 47–73. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable Name and Unit | Index Name | Index Description | Calculation Formula (in Period t) |

|---|---|---|---|

| (%) | Government debt ratio | Government debt scale | Central government accumulated debt/nominal in period t |

| (%) | Fiscal deficit ratio | Fiscal policy style | Fiscal deficit/ |

| (%) | Economic growth rate | Business cycle | |

| (%) | Inflation rate | Monetary policy style | |

| (%) | Real interest rate | Monetary policy style | Annual average real interest rate |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, Y.; Zhang, S.; Zhang, N.; Wen, Z.; Zhang, Q.; Xu, M.; Zhang, Y.; Niu, M. The Dynamic Relationship between China’s Economic Cycle, Government Debt, and Economic Policy. Sustainability 2022, 14, 1029. https://0-doi-org.brum.beds.ac.uk/10.3390/su14021029

Yang Y, Zhang S, Zhang N, Wen Z, Zhang Q, Xu M, Zhang Y, Niu M. The Dynamic Relationship between China’s Economic Cycle, Government Debt, and Economic Policy. Sustainability. 2022; 14(2):1029. https://0-doi-org.brum.beds.ac.uk/10.3390/su14021029

Chicago/Turabian StyleYang, Yifu, Sheng Zhang, Nannan Zhang, Zuhui Wen, Qihao Zhang, Meng Xu, Yingfan Zhang, and Muchuan Niu. 2022. "The Dynamic Relationship between China’s Economic Cycle, Government Debt, and Economic Policy" Sustainability 14, no. 2: 1029. https://0-doi-org.brum.beds.ac.uk/10.3390/su14021029