3.1. Data Analysis

The independent variables considered in this piece of research are gender, age, income, and occupation. We expect that consumers’ patterns of purchasing change with respect to these variables.

The sample respects the quotas of the total population, as seen in

Table 1,

Table 2,

Table 3 and

Table 4. Almost 50% of respondents are male and 50% are female, close to the statistical data for the total population in Bucharest.

Table 1.

Sample structure by gender, compared to total population.

Table 1.

Sample structure by gender, compared to total population.

| Variable | Gender |

|---|

| Total population | Sample |

|---|

| Absolute (persons) | Relative (%) | Absolute (persons) | Relative (%) |

|---|

| Male | 871,530 | 46.3 | 142 | 48.6 |

| Female | 1,011,895 | 53.7 | 150 | 51.4 |

Table 2.

Sample structure by age, compared to total population.

Table 2.

Sample structure by age, compared to total population.

| Variable | Age |

|---|

| Total population | Sample |

|---|

| Absolute (persons) | Relative (%) | Absolute (persons) | Relative (%) |

|---|

| 15–24 years | 225,820 | 13.7 | 49 | 17 |

| 25–44 years | 668,253 | 40.5 | 125 | 43 |

| 45–65 years | 483,045 | 29.3 | 80 | 27 |

| over 65 years | 272,151 | 16.5 | 38 | 13 |

The sample consists of 17%young people (ages between 15 and 24 years old), 43% people aged between 25 and 44 years old, 27% people aged between 45 and 65 years old, and 13% aged over 65 years old. As seen in

Table 2, the quotas of the sample are close to the quotas of the total population.

With regards to income (

Table 3), the sample slightly differs compared to the total population. Statistics show that 15% of the population has an income under 160 euros, but 25% of respondents belong to this low-income category. These results have been achieved because the sample contains numerous young people, considering the sample structure by age (17% young people within the sample, compared to 13.7% of the statistical data), and young people have lower incomes.

Table 3.

Sample structure by income, compared to total population.

Table 3.

Sample structure by income, compared to total population.

| Variable | Income |

|---|

| Total population | Sample |

|---|

| Absolute (persons) | Relative (%) | Absolute (persons) | Relative (%) |

|---|

| < 700 lei (under 160 euros) | - | 15 | 75 | 25.7 |

| 700–1500 lei (160–340 euros) | - | 37 | 98 | 33.6 |

| > 1500 lei (over 340 euros) | - | 48 | 119 | 40.7 |

Finally, the sample structure by occupation (

Table 4) shows similarities between the sample and total population and small differences only for entrepreneurs (1.2% of the total population compared to 4.5% of the sample).

Table 4.

Sample structure by occupation, compared to total population.

Table 4.

Sample structure by occupation, compared to total population.

| Variable | Occupation |

|---|

| Total population | Sample |

|---|

| Absolute (persons) | Relative (%) | Absolute (persons) | Relative (%) |

|---|

| employee with secondary education | - | 67.3 | 112 | 66.10 |

| employee with higher education | 81 |

| unemployed, students | - | 15.5 | 45 | 15.4 |

| entrepreneur | - | 1.2 | 13 | 4.5 |

| other | - | 16 | 41 | 14.0 |

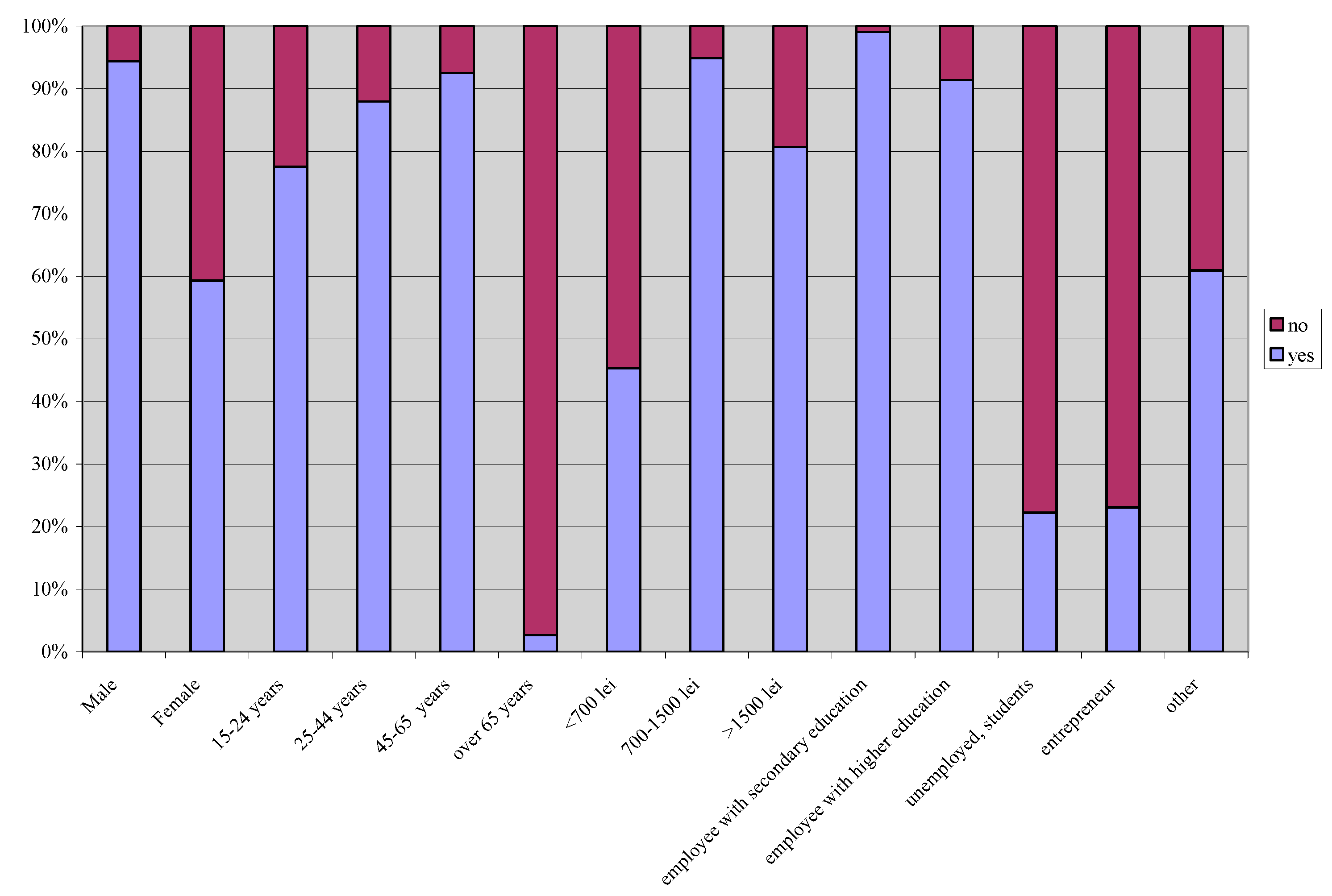

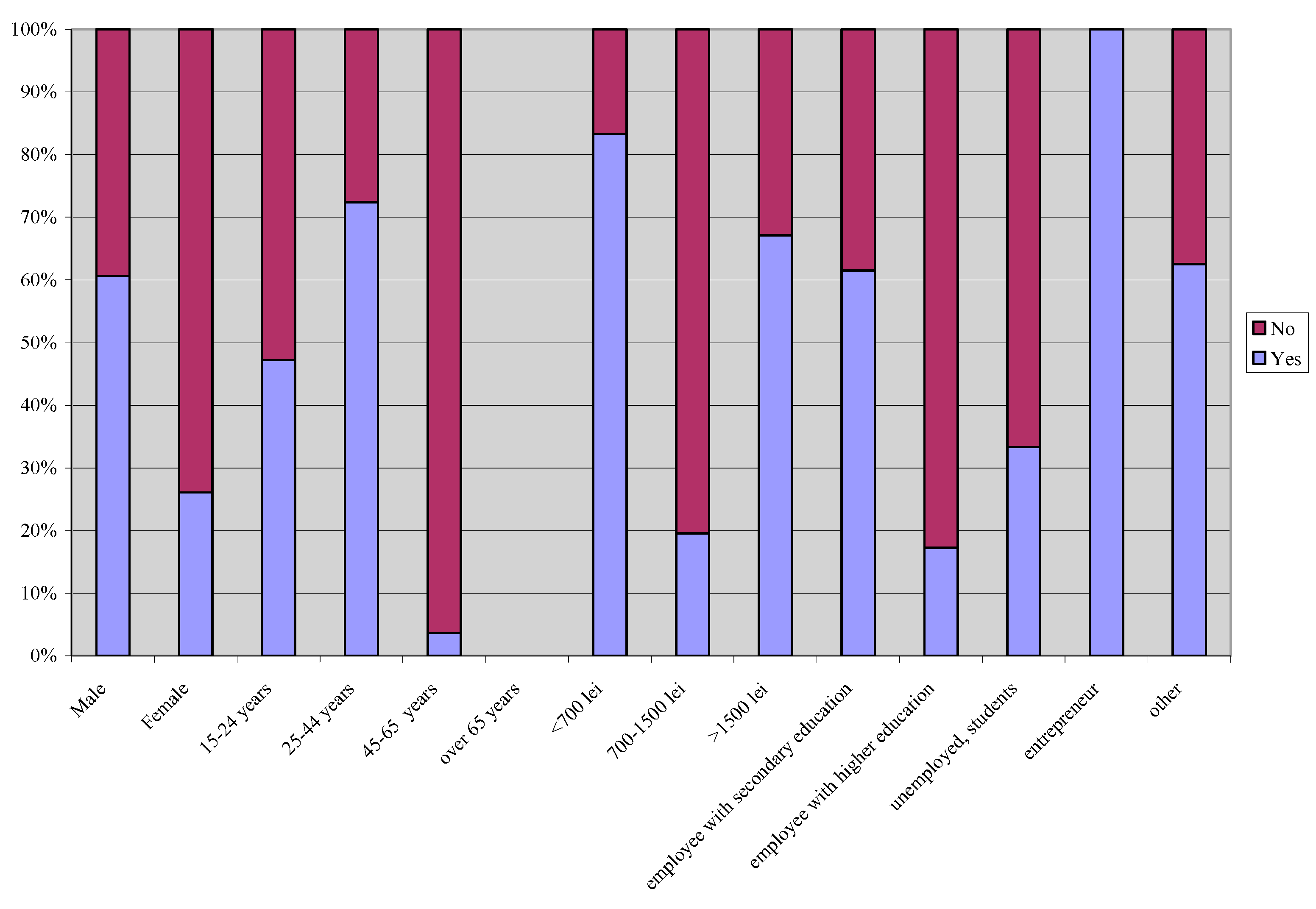

The first question aims to identify the number of private brands users and their profile. Seventy-six percent of people bought private brands in the last three months. As seen in

Figure 1, men buy private brands more often than women. Their age is between 45 and 65 years old; they have middle level income and are employees with secondary education. People who do not buy private brands are over 65 years old, with no active occupation and low income. Age and occupation are the variables that divide markets into private brands users and non-users. Thus, 97% of people over 65 years old and 76% of unemployed people do not buy private brands. In return, 97% of people aged between 45 and 65 years old and 99% of employees with secondary education buy private brands. Income has a significant influence, as well: 94% of people with an income range in the middle level buy private brands, while 55% of people with low income do not buy them.

Figure 1.

Have you bought private brands in the last three months?

Figure 1.

Have you bought private brands in the last three months?

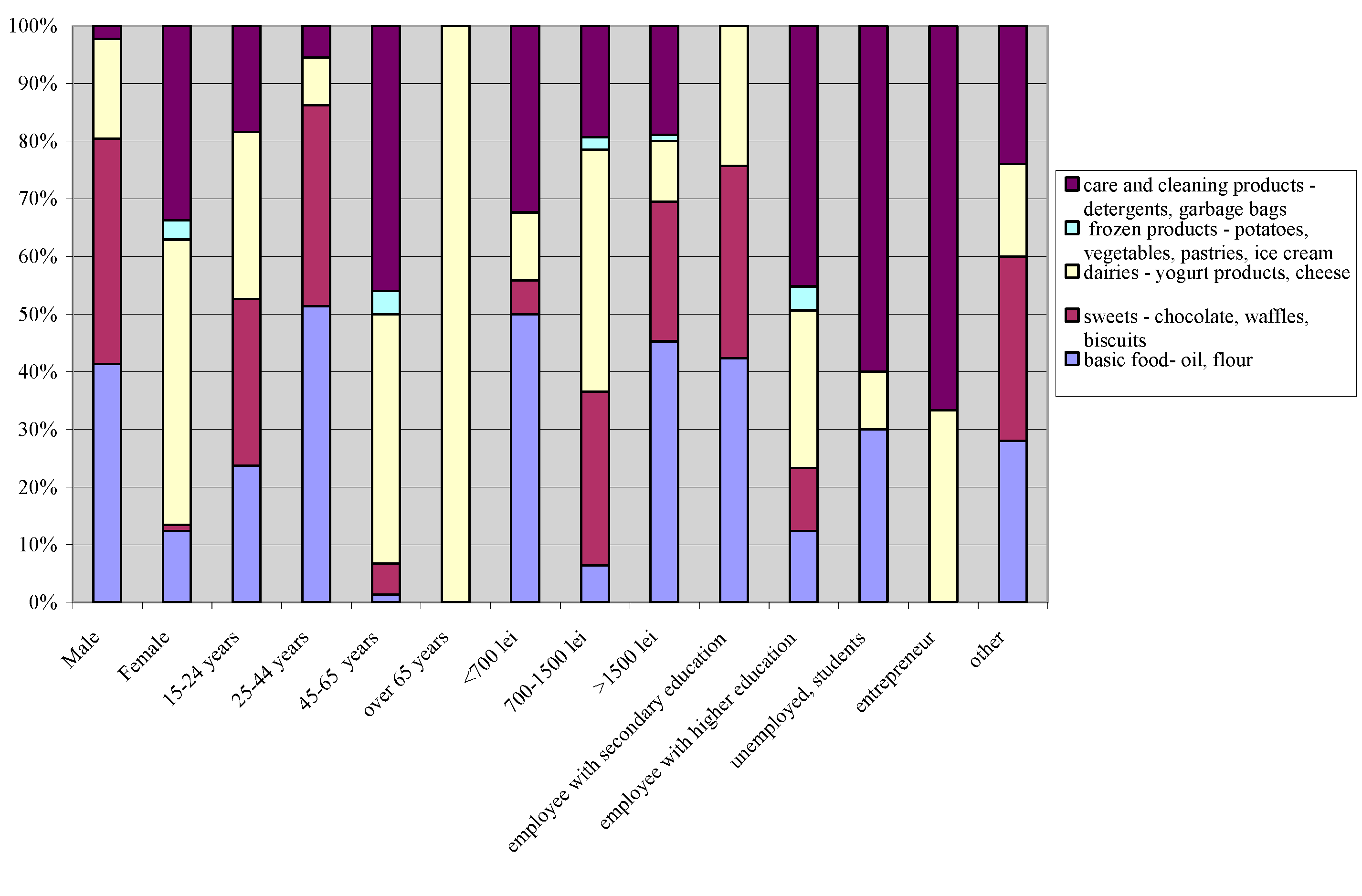

The second objective is to identify types of products within private brands that are bought more often (

Figure 2). The answers are distributed almost equally between basic foods (22% of people chose this category) and dairy products (23%). With a distribution of 11%, home care and cleaning products are less often purchased. Eighteen percent of people buy sweets (chocolate, waffles, and biscuits) from private brands. The market is highly segmented by age: people aged between 15 and 24 years buy sweets and dairy products; people aged between 25 and 44 years old buy basic foods and sweets; people aged between 45 and 65 years buy dairy and care and cleaning products; and people over 65 years old buy dairy products. People also act differently depending on their gender. Men are purchasing basic foods and sweets with private brands and women are purchasing dairy products, home care and cleaning products from private brands.

Figure 2.

What kind of products with private brands do you buy more often?

Figure 2.

What kind of products with private brands do you buy more often?

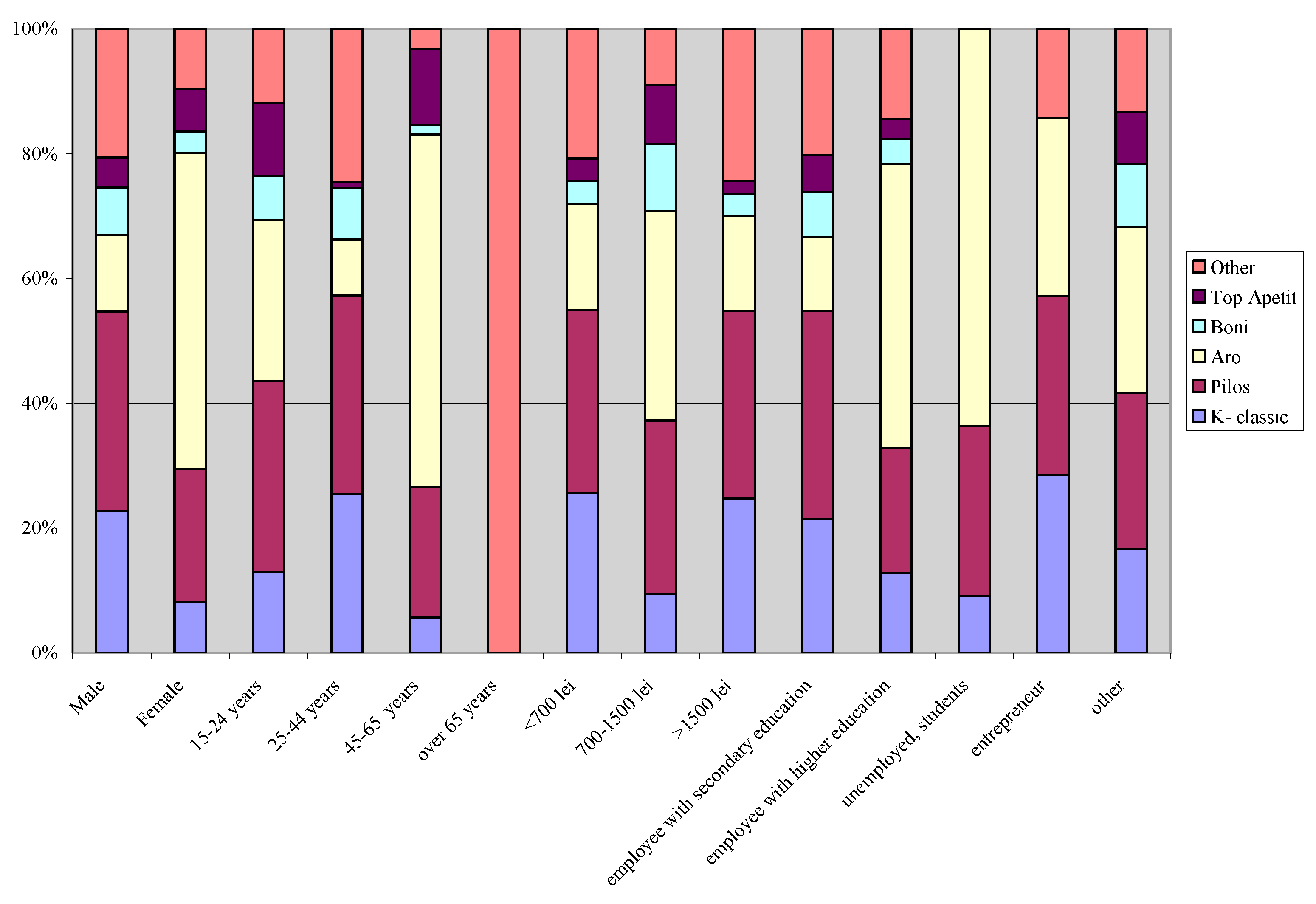

Another important objective is private brand awareness (

Figure 3). The most famous brand is Pilos, the brand of German retailer Lidl, as shown by the 52% of people who chose it. The next famous brand is Aro, the brand of German retailer Metro, as shown by the 41% of people who recognized it. Less recognized brands are Boni and Top Apetit. Considering gender, male recognized Pilos and women Aro. With regards to age, young people recognized Pilos and mature people Aro. People with no occupation and employees with higher education chose Aro.

Figure 3.

What private brands do you know?

Figure 3.

What private brands do you know?

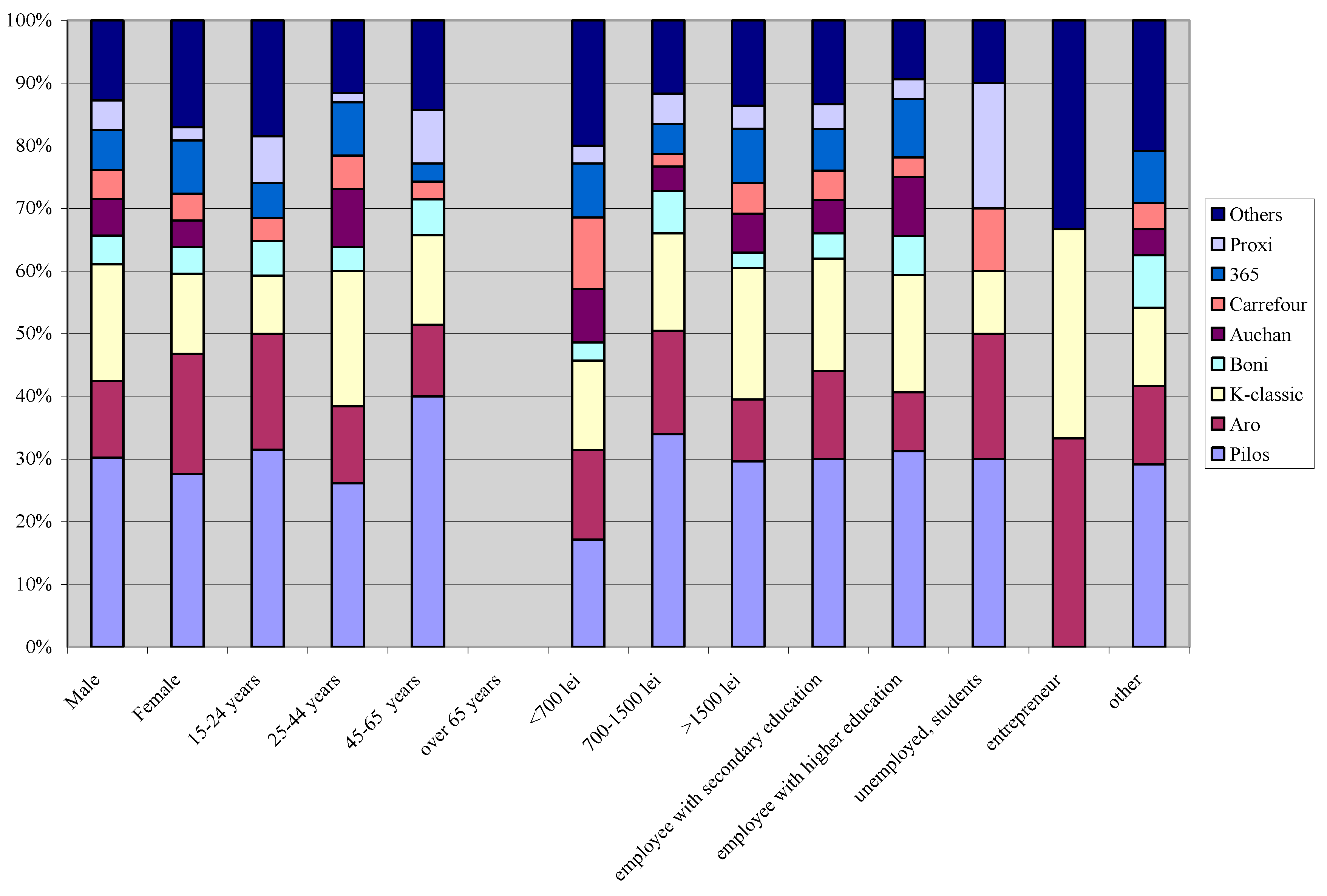

The following objective is to identify people preferences for private brands (

Figure 4). Overall, Pilos is the most preferred brand (almost 30% of people chose this brand). K-classic and Aro are also among people’s preferences, with 17% and 14%, respectively. Respondents also named the brands 365, the brand of Mega Image retailer, Carrefour, Auchan, Boni, Proxi, and others. All people prefer Pilos as first choice, but the second choice is up for debate. The second choice for men is K-classic, while for women it is Aro. The second choice for young people is Aro and for mature people is K-classic. With regards to income, people with high levels of income prefer K-classic as their second choice, while low-income respondents prefer Aro. Entrepreneurs prefer Aro, unemployed people prefer Proxi, and employees prefer Pilos and then K-classic.

We may also identify the profile of consumers for each brand. The customer of brand Pilos has middle or low income and prefers to purchase food daily from a discounter in proximity to his home, such as Lidl. Other customers—employed, with high income—prefer to buy food from a supermarket in proximity to their home, such as Mega Image. Finally, occasional customers buy food on weekends (stocking up) and choose between a hypermarket, Cash & Carry (Metro with brand Aro) and hyper-hard discount (Kaufland with brand K-classic).

To reach our research objectives, for correlations between variables we used the linear regression method described below:

where:

y = estimated result (age of consumers that would buy a specific brand)

x = known variable (income level)

My = average age

Mx = average income

Sy = standard age deviation

Sx = standard income deviation

a = intercept

b = regression slope

In our research, for Pilos brand consumers’ profile, the average income was 1500 lei with a standard deviation of 500 lei; and average age of 46 years with a standard deviation of 5 years.

;

.

Thus, the regression equation that we used was

for Pilos brand consumers’ profile identification.

This helps us to better understand the customer profile of Pilos private brand. Through the regression method, an extrapolation can be done to the age variable, knowing the income level of potential persons added to the panel.

Figure 4.

What private brands have you bought in the last three months?

Figure 4.

What private brands have you bought in the last three months?

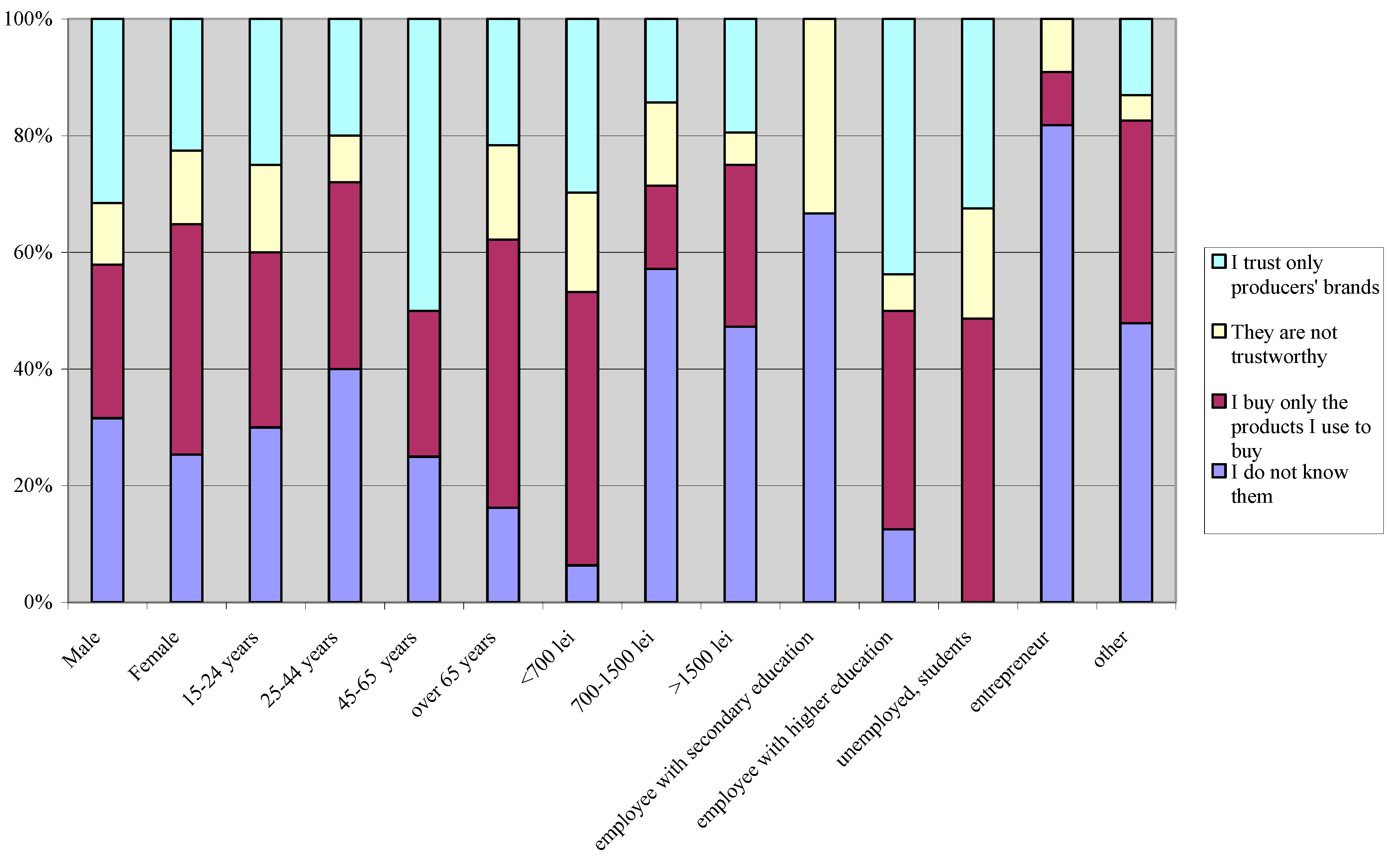

Identifying the main reason why people do not buy private brands is another aim of this piece of research (

Figure 5). The reason why people do not buy private brands is that they are buying only the products they are used to buy, which shows high loyalty to products and relative stable purchasing patterns (36% of respondents have chosen this reason). Twenty-six percent of people do not know them and 24% of people trust producers’ brands. The results of this question allow us to identify the patterns of purchasing, as well. The pattern “I do not know them” corresponds to young men with middle income, employees with secondary education, or entrepreneurs. The pattern “I buy only the products I am used to buying” corresponds to women over 65 years old, with low income and no occupation. The pattern “Private brands are not trustworthy” corresponds to both men and women, young or over 65 years old with low income, the unemployed, or employees with secondary education. The pattern “I trust only producers’ brands” corresponds to middle-aged men with low income or employees with higher education.

Figure 5.

Why do you not buy private brands?

Figure 5.

Why do you not buy private brands?

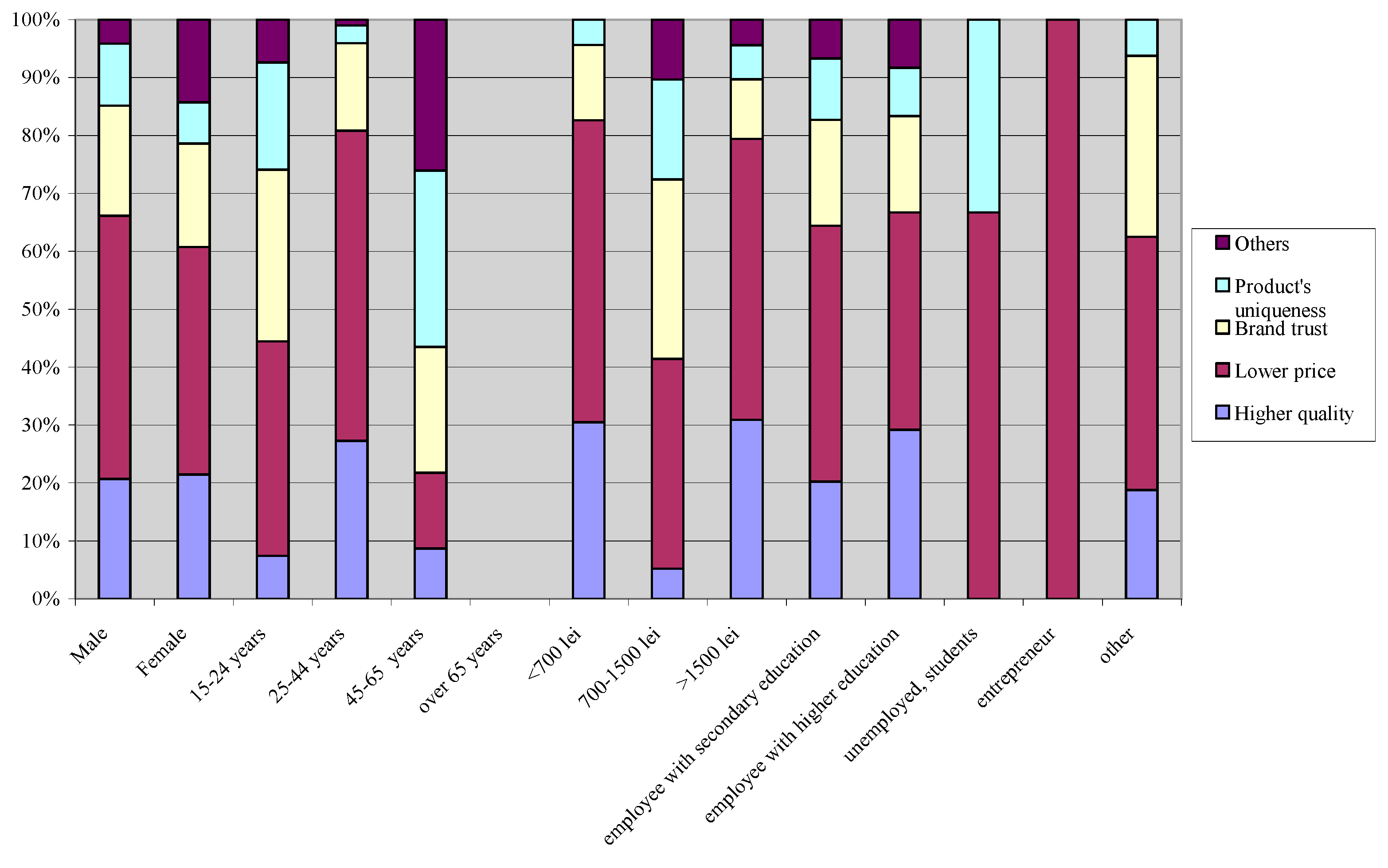

Figure 6 shows the results for identifying the reasons why people buy private brands. The main reason why people buy private brands is their lower price (44% of people chose this answer). High quality and brand trust were also mentioned by 20% or 19%, respectively. Products’ uniqueness accounts for 10% of people. High quality is important for both men and women aged between 25 and 44 years, with low or high income, and employees with higher education. Low price is significant for young men with low income, the unemployed, or entrepreneurs. Brand trust is important for both young men and women with middle-level income. Products’ uniqueness is significant for middle-aged men with middle-level income, and those with no active occupation. People aged over 65 did not answer the question.

Figure 6.

What are the reasons for choosing a particular brand among others?

Figure 6.

What are the reasons for choosing a particular brand among others?

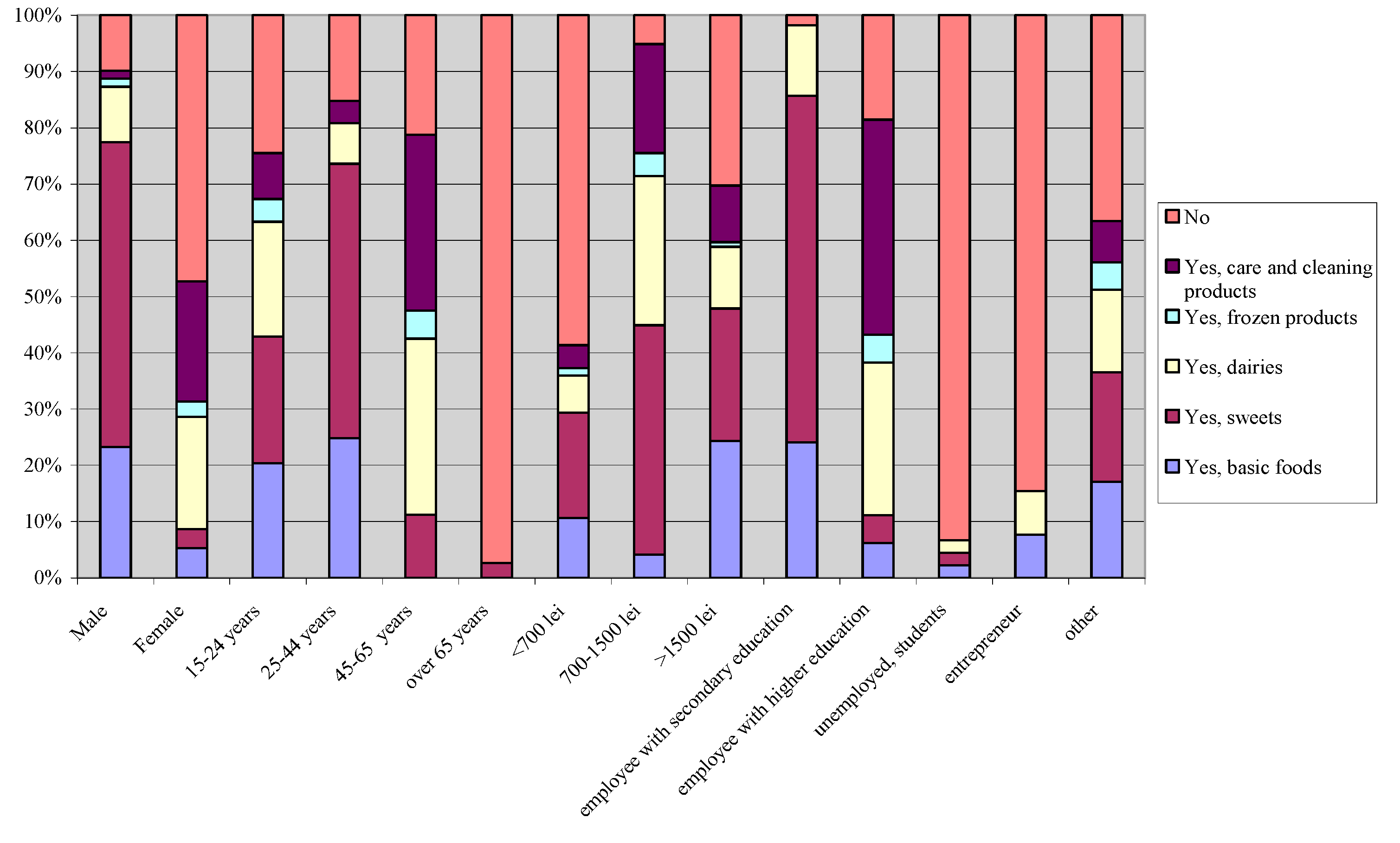

The following objective is to identify people’s willingness to pay more for private brands’ products with an improved level of quality and identification of these categories of products (

Figure 7). Overall, 70% of people agree to pay more for an improved quality of private brands. The frequently chosen categories are: sweets, dairy products, and basic foods. Men would pay more for sweets, while women would not pay more. People aged between 25 and 44 years would pay more for sweets, and people aged between 45 and 64 years old would pay more for home care and cleaning products. People with low income would not pay more for private brands and people with middle-level income would pay more for sweets. Employees with secondary education would pay more for sweets, and employees with higher education would pay more for home care and cleaning products; unemployed people and entrepreneurs would not pay more for improved private brands.

Figure 7.

Do you agree to pay more for a private brand with an improved quality? If yes, choose a category.

Figure 7.

Do you agree to pay more for a private brand with an improved quality? If yes, choose a category.

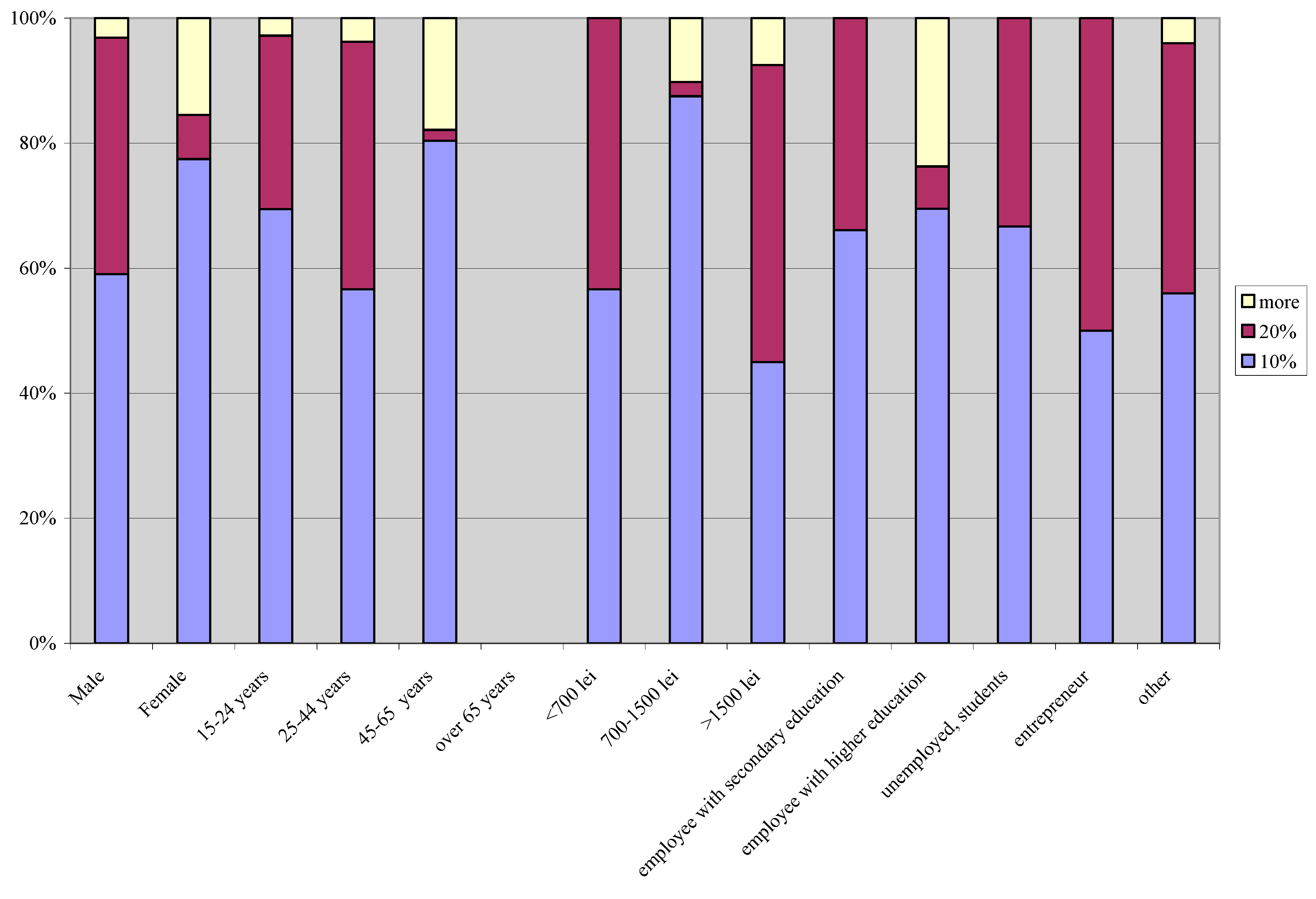

People who agreed to pay more for an improved quality of private brands express their willingness for different levels of prices: 10% higher, 20% higher, more than 20% (

Figure 8). Most people, 65%, chose the first category. They are middle-aged women with a middle level of income, or employees with higher education. Men aged between 25 and 44 years with high income, and entrepreneurs would pay 20% more for private brands of improved quality.

This piece of research also investigates people expectations with regards to products’ quality compared to what they have experienced after buying the private brands’ products (

Figure 9), asking whether people found a weaker product or not. Overall, the answers are equally distributed between yes and no (48.5% and 51.5%, respectively). People who experienced a weaker product are men aged between 25 and 44 years, with low income, and employees with secondary education and entrepreneurs. The most common criticism of private brand products is related to their taste: “yogurt tastes like powdered milk,” “pasta crumbles in water,” canned fish quality is perceived as low since “their contents are more liquid than solid,”

etc. People who do not consider that private brand products are weaker than what they expected are women, aged between 45 and 64 years, with middle-level income, and employees with higher education.

Figure 8.

How much more money would you pay for private brands?

Figure 8.

How much more money would you pay for private brands?

Figure 9.

Did you experience a weaker product than you expected when you bought private brands?

Figure 9.

Did you experience a weaker product than you expected when you bought private brands?

Finally, the research aims to rank the actions needed for increasing consumers’ trust in private brands (

Table 5).

Table 5.

Results of the question: Which actions do you consider the most important for increasing consumers’ trust in private brands, among the following variants?

Table 5.

Results of the question: Which actions do you consider the most important for increasing consumers’ trust in private brands, among the following variants?

| Actions | Very important | Important | Less important |

|---|

| To mention the name of the producer closer to the retailer on the label | 146 | 130 | 10 |

| To communicate certifications and independent tests on products’ labels | 169 | 100 | 12 |

| Tasting private brands’ products in stores | 96 | 144 | 45 |

| To be recommended by a specialist (e.g., Master Chef, TV star) | 62 | 107 | 110 |

| To be promoted by producers via fairs and specific contests | 98 | 138 | 42 |

People consider that the most important action is to communicate certifications and independent tests on products’ labels, because this variant has the highest average mark of 2.56, on a scale from 1 to 3, where 1 is less important and 3 is very important. This is closely followed by a mention of the name of the producer closer to the retailer on the label, with an average mark of 2.48. Specialists’ recommendations and producers’ promotions via fairs and specific contests are important (2.18) and less important (1.83), respectively.

3.2. Discussion

The results of this piece of research validate some of the hypotheses. The assumptions made at the beginning of the survey are based on results of other researchers and marketing studies. In this section, we aim to identify whether the results of the survey validate the findings of other studies.

Based on other findings [

23] and market information, we argued that about 70% of people have bought private brands in the last three months. The results from the survey showed that 76% of people have bought a private brand, which validates the premise.

We expected that the most popular private brands would be in the food category, specifically basic food. The results show that both basic food and dairy products are popular, because people chose the two of them equally (22.9% and 22.6%, respectively).

As other findings show [

24,

25] the most known private brand is K-classic. This hypothesis is not true, according to the results from the survey. Fifty-two percent of people recognized Pilos, 41% recognized Aro, and 33% chose K-classic. Pilos awareness is based not only on its low price and high quality, but on ready availability in supermarkets close to customers’ residences.

Based on the same studies [

24,

25], we argued that people prefer the brand K-classic. However, the results of our study show that people buy Pilos more often than other private brands.

In relation to the first hypothesis arguing that 70% of people bought private brands in the last three months, we claimed that 30% of people did not buy private brands and 50% of non-buyers have trust in producers’ famous brands. The results of the survey show that 24% of people did not buy private brands, close to what we expect, but the main reason is that they buy only products they are used to buying. Consumption pattern stability is more valuable than consumers’ fidelity to producers’ brands. This cautious pattern of purchase is based on customers’ resistance to change, which has implications on retailers’ marketing strategies.

We argued that lower price is the reason why people buy private brands, which is true: 44% of people chose this answer. Indeed, products with private brands are priced 15–20% lower than the same products from producer brands and this varies from a product category to other.

We assumed that 80% of people have the willingness to pay higher prices if the quality of private brands’ products increases. In fact, the results show that 71% would pay more for improved quality private brands, especially for sweets, corresponding to what we actually argued—that the products for which people would pay more are sweets and dairy products.

Estimating the price level for private brands’ products of improved quality, we claimed that 50% of people would pay a price 10% higher. The findings show that 65.7% of people would pay 10% more for improved quality.

The answers to the question “Did you experience a weaker product than you expected when you bought private brands?” are opposite to what we expected: 15% of people would have higher expectations with regards to products’ quality compared to what they have experienced. In fact, almost half of respondents have higher expectations from private brands and they experienced weaker products. This result has practical implications for retailers in their efforts to develop and sell private brands.

We considered that the most significant action needed to increase consumers’ trust in private brands is “communicating certification and independent tests on products’ labels.” The answers of the survey jump to the same results, because most respondents have considered this action as very important.

Research limitations. We supposed that people over 65 years old did not know what a private brand means, as shown by the 97% of people in this category who answered that they did not buy private brands in the last three months (

Figure 1). This claim is also supported by the fact that people over 65 years old did not answer the question: What private brands have you bought in the last three months? This limit does not significantly change the results of our research.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}