1. Introduction

The concepts of Corporate Social Responsibility (CSR) and business models have been frequently addressed in academic studies in the last decades. Both of these concepts are often listed among the key concerns in contemporary management theory and practice. They are looked at from various research perspectives, including macroeconomic [

1], microeconomic [

2], management [

3,

4], and marketing [

5]. There is no lack of conceptual studies trying to integrate CSR with developing strategies and business models. For example, Pyszka [

6] is proposing a mechanism whereby traditional business models can be transformed into CSR-enabled ones, with the aim of enhancing a company’s competitive advantage, in particular its innovativeness. When it comes to practical guidance for managers, some authors developed various sets of tools that practitioners can use to diagnose the current state of CSR and sustainability involvement and implement needed changes, bearing in mind the short- and long-term economic benefits for the company. In this vein, Bocken

et al. [

7] offer a number of value-mapping tools to support sustainable business modeling, including the interests of the four major stakeholder groups, here labeled as environment, society, customer, and network actors. The topic of the interlink between CSR, sustainability, business models, and strategy is also ever-present in business and trade journals, where various authors often depict these management concepts as means of enhancing competitiveness and achieving other benefits [

8]. What these published works, both academic and otherwise, have in common is a lack of empirical proof (as in the case of conceptual papers) or reliance on qualitative and anecdotal evidence e.g., [

9,

10]. In fact, there is a surprising dearth of works exploring the quantitative evidence for possible links between types of adopted business models and the level of CSR practices. As such, the aim of our paper is to address this issue and attempt to bridge the knowledge gap. Building on previous studies, we conclude that the type of business model used should affect a firm’s CSR involvement, and then test this proposition with survey data collected from managers of medium and large companies in Polish manufacturing and service industries.

The paper is structured as follows. First, we summarize relevant literature sources on CSR to discuss various understandings of the concept. Next, we survey popular definitions and taxonomies of business models. The third section looks at previous studies where associations between business models and CSR were investigated. Then, we detail the business model definition and classification adopted in this paper and set out the rationale for our hypotheses. The methods section comes next, followed by findings. The paper concludes with a discussion of theoretical and practical implications of the study, limitations, and suggestions for further research.

2. Corporate Social Responsibility in Literature

Corporate Social Responsibility and related concepts (e.g., sustainable development) have been playing an increasingly prominent role in recent years, both in economic and academic research. Despite its popularity—and perhaps in part because of it—authors of numerous publications in this area have not shown a uniform understanding of these constructs, which are sometimes vague and tends to vary from publication to publication. This is reflected in how many distinct terms were used, including Corporate Sustainability and Responsibility, Corporate Citizenship, Corporate Social Rectitude, Corporate Social Performance, Corporate Social Responsiveness, Social Performance, or Sustainable Responsible Business. In fact, in a review of the CSR literature Dahlsrud [

11] counted no fewer than 37 different definitions of the concept. Below we shortly outline the history of the idea of sustainable responsibility and wrap up by offering the definition that we assumed in our study.

In terms of social duties of business, for many years the dominant perspective was that of Friedman [

12], who maintained that what firms should care for was generating profits, and social responsibilities were no concern of business; indeed, his strongly held conviction was that any action on the part of managers that did not amount to increased profits was tantamount to theft. However, the notion of firms supporting social goals is not new, since the first publications on this topic appeared in the 1930s, e.g., [

13,

14], and the first formalized definitions date back to the 1950s–60s [

15,

16,

17,

18,

19,

20]. Rapid growth in CSR has been particularly evident since the 70s, when accelerating globalization made the impact of companies on society and environment a more pertinent problem than ever before [

21]. At that time, it was proposed that CSR could offer effective solutions for outstanding societal issues, in large part due to the strong effects of businesses, in particular multinationals, on economy, politics, environment, and local communities [

22]. In the 1980s the idea of sustainable development emerged to represent such “development that meets the needs of the present without compromising the ability of the future generations to meet their own needs” [

23]. Its proponents advocate sustainable development in economy, society, and the natural environment that would aim to eradicate poverty and moderate excessive consumption in both developed and developing countries [

24]. As noted by Vos [

25], many definitions of sustainability are similar in that they identify three aspects of the term: economic, social, and environmental.

The growing importance of CSR was recognized by the International Organization for Standardization (ISO), which set up a special task group for social responsibility. As a result of the group’s work, a system of guidelines was revealed in 2010 to help businesses operate in a more “ethical and transparent way that contributes to the health and welfare of society” [

26]. The ISO 2600 manual outlines specific benefits that can be derived from implementing CSR principles, including enhancing competitive advantage; attracting and retaining employees, shareholders, and clients; improving the morale, commitment, and productivity of employees; and fostering better image and goodwill from clients, suppliers, local communities, and other stakeholders of the company.

The first definition of CSR that gained wide acceptance was that of Caroll [

27]. Caroll proposed a CSR pyramid with four levels representing CSR dimensions: (1) economical (at the base of the pyramid; denoting all activities yielding profit for the company’s owners), (2) legal (acting within the law regulating environmental protection, consumer and employee relations, and adhering to contractual agreements), (3) ethical (acting in an ethical and honest way towards stakeholders), and (4) philanthropic (the firm as a good citizen should undertake special programs for the benefit of the society). Later on, Schwartz and Caroll [

28], building on the previous model, came up with a non-hierarchical structure with only three dimensions—economical, legal, and ethical—whereby the philanthropic element was split between economical and ethical areas, depending on the dominant underlying motivations behind specific charitable activities. Another popular conceptualization of CSR, known as the triple bottom line (TBL), calls for companies to operate in ways that are socially responsible, eco-friendly, and economically valuable [

29]. The three focal points of TBL are people (involving responsible business practices towards employees, customers, society at large, and local communities), the planet (activities aimed at protecting the natural environment), and economic value, or profits earned after contributing to the other two CSR dimensions. According to the TBL perspective, its three dimensions are equal in terms of importance, which should be reflected in corporate reporting. Therefore, not only financial metrics should be reported, but also accounts of the company’s social and ecological performance. Such integrative reports should merge both short-term and long-term perspectives [

30]. One of the most recent outlooks on CSR and the last one reviewed in this section is that of Chen and Wongsurawat [

31], whose definition we chose to adopt in our research. These authors looked to combine Caroll’s [

27] perspective and TBL with the ISO recommendations. In their view CSR should encompass: (1) competitiveness (

i.e., cooperation with stakeholders in building strong market position of the company and its products); (2) transparency (removing barriers for members of the public to accessing corporate information; the aim here is to provide means for fast and efficient communication with a wider audience on the firm’s activities with potential social and environmental impacts); (3) responsibility (complying with legal regulations and contractual terms pertaining to different stakeholder groups); (4) accountability (making thoughtful and justified business decisions accommodating the interests of various groups of stakeholders).

To sum up the discussion so far on popular conceptualizations of CSR, and to present our own understanding of the concept used in this work, we distinguish the following four aspects of the CSR involvement: (1) value chain relations (entailing conscientious attitude in interactions with suppliers, customers, and other supply chain partners); (2) community relations (communication, cooperation, and support for local and wider social partners); (3) natural environment (commitment to running business operations with the smallest possible negative impacts on the environment); and (4) employee relations (all corporate socially responsible activities aimed at employees). In keeping with the above taxonomy of CSR, we developed a Likert-type scale for use in the survey questionnaire. The measurement scale was outlined in more detail in the methods section.

3. Overview of Conceptualizations of Business Models

The interest in business models has grown, particularly since the 1990s, when a number of seminal papers were published. The dominant theme for many papers was Internet business, which coincided with—and was sparked by—the dot-com boom and bust, e.g., [

32,

33,

34,

35]. Academic writing on business models, even more so than on CSR, is affected by a lack of consensus as to what constitutes a business model. So far many definitions and typologies had been proffered, some more popular than others, but no single dominant approach emerged. On the other hand, and quite similar to CSR, most views of business models have considerable overlap, which makes it easier and more meaningful to compare findings across different works. In this section we summarize the more popular ways to think about business models, and present our own approach that was used in the questionnaire design to collect responses from managers.

One way to look at business models was offered by Afuah and Tucci [

33], who proposed that it is how a firm builds up and deploys its resources to provide customers with products of value superior to competitors’ offerings in order to generate profits. According to Linder and Cantrell [

36], a business model is a logical basis for creating a company’s value , reflected in a coherent action plan aimed at developing a strategy that meets customer expectations through the optimal use of resources and relations. Here, a business model specifies such elements as: types of customers, products or services, pricing policy, customer benefits, distribution channels, unique competences, and revenue sources. Betz [

37] considers a business model as a composition of three elements necessary for the firm to operate: benefits or values for customers and business partners, revenue sources, and logistics arrangements. Osterwalder

et al. [

38] give the following constituting elements of business models as part of their strategic template for crafting new or documenting existing business models: value proposition for customers, corporate infrastructure (including key activities, key resources, and partner network), targeted customers (composed of market segmentation, distribution channels, and customer relationships), cost structures, and revenue streams.

In terms of business model typologies, many authors propose divergent classifications based on different sets of criteria, with many of them mostly relevant to e-business [

32,

33,

35,

39,

40,

41,

42]. Just a handful of authors attempted to develop a more universal typology system, suitable for classifying a wider range of business models, including traditional, “bricks-and-mortar” companies [

36,

37,

43,

44,

45,

46].

4. Earlier Studies on the Links between Business Models and CSR

Even though the problem of how companies with different types of business models get involved in CSR has arguably both practical and theoretical merits, it has rarely been explored as a topic of an academic study. Some authors proposed to introduce new paradigms in management to effectively counteract social and environmental degradation, e.g., [

47,

48,

49,

50], but only a few incorporated elements of business models in their analyses of CSR, e.g., [

51,

52,

53,

54]. In recent years, several new pertinent management concepts emerged, such as so-called “sustainable business models” [

55,

56,

57], “sustainability business models” [

58], “business models for sustainability” [

51], and “sustaining supply chain management” [

59,

60,

61]. All of these new constructs build on the theory of corporate sustainability management, which—at a general level—aims to integrate multiple corporate activities and impacts in societal, environmental, and economic areas. Those authors give different definitions of sustainable business models (SBM); for example, they say that it is “a model where sustainability concepts are the driving force of the firm and its decision making” [

58], or ”a new model of the firm where sustainability concepts play an integral role in shaping the mission or driving force of the firm and its decision making” [

62]. Regarding the interplay between business models and CSR, some authors suggest the existence of a feedback loop, whereby certain types of business models can foster stronger CSR involvement [

63], while implementing CSR has the potential to transform business models in the long run [

53]. In the same vein, Schaltegger and Wagner [

64] observe that business models of firms following CSR principles are changing both through purposeful effort and unconscious adjustments. This points to the conclusion that not only strategic management but also daily operational tasks are factors in shaping a business model setup. This view finds support in Elkington [

55], who noted that business models are determinants of organizational behaviors, and as such have influence on strategic management as well as operations, including assorted CSR activities. The literature, but also more casual observations and common experience, imply that sustainable management, CSR, and business models are in constant interaction, and firms intending to improve their CSR metrics have to work towards revising their business model [

65]. Indeed, deep changes to a business model can be a way of achieving radical improvement to a firm’s CSR status through creating more environmental and social value in an economically viable manner [

58,

66,

67], or—to put it another way—capturing economic value while generating social and environmental values [

7]. Accordingly, the concept of business models could be a useful tool for reconciling and integrating the often divergent needs and wants of stakeholders in terms of the sustainable development of a company [

68]. For that purpose, firms should make a conscious effort to plan and manage the sustainability aspects of their business models [

51]. In light of the above, it seems relevant to study links between various types of business models and the CSR record of companies, since there is a good theoretical reason to believe that different business models yield different CSR attitudes and implementations. As such, we propose that:

Hypothesis 1: The intensity of CSR involvement is related to the business model followed by a company.

The second hypothesis for the study will be developed in the following sections of the paper.

5. Business Model Definition and Taxonomy Adopted in the Study

As the theoretical background for our approach to defining and classifying business models we used a framework developed by Dudzik and Witek-Hajduk [

69], with further extensions and modifications by Gołębiowski

et al. [

46]. According to the framework, a business model represents the logic underlying a firm’s business activities in a given area and encompasses a description of the value proposition offered by the firm to its customer groups, with a specification of essential resources, processes (activities), and external relationships of the firm, serving to build, offer, and deliver the value proposition, ensure the firm’s competitiveness, and enhance its equity. The “area of activity” referred to in the definition, depending on the scope of operations, can concern the whole of a company or an individual strategic business unit (SBU); thus a firm can operate distinct business models in various SBUs at the same time. Gołębiowski

et al. [

46] point to the following constituting elements of a business model: (1) value proposition to the customer, comprising products offered, benefits delivered at different steps of the transaction process, subjective customer assessment of the acquired benefits

versus incurred costs, and relationships with final consumers/users of the products; (2) key resources of the company, such as managerial competences, technology, brands, patents, designs, tools, equipment, infrastructure, and market knowledge; (3) the firm’s role within the value chain, in particular activities within its internal value chain and their ties with external links of the integrated value chain; (4) revenue sources from selling manufactured goods and rendered services, offering rights to tangible and intangible products through leasing, renting, franchising or licensing, subscription and usage-based fees, and brokerage fees from performing the role of an intermediary for other companies.

Employing this concept of a business model, Dudzik and Witek-Hajduk [

69] conducted a survey of Polish companies to arrive at a segmentation of business models that identified five distinct types of firms: (1) traditionalists, (2) market players, (3) contractors, (4) distributors, and (5) integrators.

Table 1 details the distinguishing features of each type of a business model. These descriptions were presented to managers participating in our study so they could choose the one category that was most consistent with their company.

Table 1.

Characteristics of business models in the study.

Table 1.

Characteristics of business models in the study.

| Business Model | Business Model Description |

|---|

| Traditionalist | The main source of value for customers is functional benefits from products, and the relationship of these benefits to costs. The firm does not have unique resources (e.g., a strong brand, patents, designs, technology, and/or recipes). The internal supply chain is long (R&D, production, marketing, sales and after-sales services). Most of the revenues are sales of manufactured products. |

| Market player | Customers derive most of the value from functional benefits offered by products, as well as the strength of the brand and relationships with other members of the value chain. The firm deploys its unique resources, such as advanced technologies, strong brand, patents, unique designs and recipes, and managerial skills. The internal supply chain is long (R&D, production, marketing, sales and after-sales services). A market player tends to be the leader of its supply chain. Revenues are mostly obtained through the sale of self-manufactured products, supplemented by income from licensing technology, brand names and franchising. |

| Contractor | The value proposition for customers is mostly based on offering functional product benefits. The main asset of the company is its production facility and equipment, which it employs to manufacture products on contract for other businesses. Its internal supply chain is focused on the production function. Proceeds from manufacturing contracts account for the bulk of the revenues. |

| Distributor | The value proposition here relies on a favorable relation of functional and emotional benefits of products to their costs. The key distinguishing competency of the company is market knowledge (about suppliers and customers). The internal supply chain is short and focused on the sales function. Revenues are mostly earned through fulfilling the role of a trade intermediary. |

| Integrator | Customer benefits can come from favorable functional features of products, but also from a strong brand and cohesive partner relationships with members of a supply chain. The distinguishing attributes of an integrator are managerial competences, management information systems, recipes, designs, patents, brand names, and market knowledge. Its internal supply chain is short: as the supply chain leader, an integrator is focused on a few core competences, such as R&D, designing, marketing, sales and after-sales services, while it tends to outsource manufacturing. Income is generated through sales of its own brand-name products and offering its own unique know-how and technology by means of franchising and/or licensing. |

From the salient features of various types of business models, as outlined in

Table 1, one can reasonably expect considerable differences in the extent of CSR implementation. In seems that out of the four groups of criteria used in the segmentation procedure yielding the above classification, those that are likely to have the strongest bearing on CSR compliance are value proposition, key resources, and the role of a company within its supply chain. Arguably, no salient elements of sustainable business are conditional on a particular setup of revenue sources, so any differences in this regard should be of no consequence to the CSR standing of a company.

Value propositions of market players and integrators are set apart from those of other companies not only by unique combinations of functional features, but also an emphasis on developing strong brand names and cohesive relationships with channel partners. In the current state of the economy in Poland, similar to other developed and emerging countries, consumers in many market segments have been growing ever more sensitive to the ethical behavior of the firms they patronize. As such, these groups of consumers may derive distinctive utility from the fact that their purchasing decisions can support the good citizens among available suppliers of goods and services. On the other hand, firms that aggressively seek to increase the perceived value of their offerings, which are market players and integrators, may choose to get involved in CSR programs specifically for that reason. Consequently, these firms are apt to promote their brands more frequently through charitable programs, whereby, for example, customers can feel better knowing that a part of the paid price goes to support a socially valuable cause. In the same vein, market players and integrators may also see business rationale in establishing and financing charitable foundations, and implementing changes to their core processes (e.g., phasing in eco-friendly technologies) to make assertions of responsible behavior more credible. To further strengthen their case, they also may choose to encourage employees to get involved with local communities to assist in enhancing their capabilities to satisfy salient infrastructural, educational, cultural, and sports-related needs. If that was indeed the main motivation to get involved in CSR, companies might be inclined to follow up this initial actions by overhauling their employee relations and organizational culture—this way employees can become more involved and convinced of the true and honest nature of the managerial push towards sustainable and responsible business practices. With more involved employees it is arguably easier to make a company’s CSR claims seem more genuine to its customers, which can foster higher loyalty and greater sales. Quite naturally, the other business models—traditionalists, contractors, and distributors—with their lower interest in creating strong brands will not experience the same motivation, and therefore may display weaker CSR involvement.

Another distinctive feature of market players and integrators is their reliance on unique resources to underlie their competitive advantages. Among these resources are superior managerial competences, innovative and productive organizational culture, proprietary technology, and market knowledge. Many of these capabilities have better chances of being achieved in corporate settings where employees are loyal, highly motivated, and emotionally involved with their workplace. Such conditions are among the likely benefits of implementing CSR programs aimed at improving employee relations, which is another reason to believe that these two business models will show higher CSR ratings.

In terms of a value chain position and relations, market players and integrators follow more active and “social” policies as compared to other categories of firms. Here, the goals and ways of operating create a strong incentive to develop close partnerships with other crucial supply chain members so that market players and integrators could assume the role of a dominant value chain member. This role is critical to their business strategies, which rely on the ability to shape value chains to achieve a higher level of efficiency and effectiveness than the networks controlled by competitors. One of the main prerequisites to achieving such a goal is a high level of trust and commitment among cooperating firms, which is promoted by ethical and responsible behavior from all involved parties. As such, this is another reason to expect more social responsibility (this time aimed at business partners) among market players and integrators than other firms with business models less dependent for success on the quality of everyday channel relations.

To conclude, considering the attributes of the identified types of business models and relating them to the CSR dimensions, it is possible to propose which types of companies will be most likely to operate in the manner consistent with the principles of responsible business. In particular, it can be expected that market players and integrators show higher levels of CSR implementations. On the other hand, the attributes of traditionalists, contractors, and distributors could create less of an incentive to function in a more sustainable way.

Consequently, it is possible to supplement the previous general hypothesis with a more specific proposition:

Hypothesis 2: Among the five types of business models, the highest level of CSR involvement will be found in market players and integrators.

The other possible distinctions between business models are difficult to extrapolate from an a priori analysis based on previous research, conceptual papers, and the authors’ own observations and experiences.

The empirical part of the research was dedicated to validating the two hypotheses. The methods employed and obtained outcomes are described next.

6. Methods

The study involved a net sample of 385 mangers from medium and large enterprises, who were contacted through a combination of CATI and CAWI methods. In particular, the respondents answered via phone (the CATI part) while looking at the web-based version of the questionnaire (the CAWI component). The inclusion of the web component was essential to make respondents fully understand the rather lengthy business model characteristics presented in

Table 1, and choose the model that best described their firms. The respondents were initially contacted via an e-mail outlining the research project, inviting them to participate, and offering a link to a dedicated web-page with a digital questionnaire. Within a few days of receiving the e-mail, phone calls followed during which interviews were conducted or arrangements were made to set up a later interview date. Despite several contact attempts, not all selected sample members could participate: the gross sample initially drawn from a database encompassing almost all companies in Poland was 535, which amounted to a response rate of 72%.

The final (net) sample included manufacturers of food (31.7%) and chemicals (31.2%), as well as retailers and wholesalers of these products (37.1%). In terms of the number of employees, 75.3% firms had between 50 and 249 staff, with the rest employing more than 250 people; 76.9% of the sample had solely Polish owners, while 23.1% reported various levels of foreign ownership.

The statistical analysis in this project was twofold. First, we validated our measurement model of CSR involvement with confirmatory factor analysis (CFA) using the AMOS 23 software. The second step involved employing one-way analysis of variance (ANOVA) as the means of testing the hypotheses of differences between various business models in terms of CSR involvement. Here, we used five dependent variables: one for the general level of a firm’s engagement in CSR and four depicting its respective dimensions. The factor scores for each latent variable for every company were obtained through a regression method from the preciously validated CFA model.

7. Research Findings

We start this section by explaining how business models were identified. Then we specify the CSR measurement model, followed by its diagnostics and concluding with the outcomes of the ANOVA.

To determine which of the predefined business models best describes each company, managers were offered descriptions of five distinct profiles and asked to choose only one that best portrayed their main area of operation in Poland. Recognizing that this mode of collecting answers, if employed over the phone, may produce biased results (due to extensive textual descriptions) respondents were able to see the relevant parts of the questionnaire on a web page while interacting with an interviewer through the CATI method.

English translations of characteristics of business models were presented in

Table 1 earlier in the paper.

Table 2 below gives sample frequencies and percentages for the different types of business models.

Table 2.

Frequency distribution of business models in the study sample.

Table 2.

Frequency distribution of business models in the study sample.

| Business model | Sample Frequency | Sample Percentage |

|---|

| Traditionalist | 168 | 43.6 |

| Market player | 71 | 18.4 |

| Contractor | 30 | 7.8 |

| Distributor | 66 | 17.2 |

| Integrator | 50 | 13.0 |

| Together | 385 | 100 |

Considering that the studied companies were part of long-established industries, it comes as no surprise that nearly half of them declared that they were operating according to a traditionalist business model. The smallest number of studied firms was identified by their managers as contractors, which is also understandable since Poland is not a very popular location for contractual manufacturing, especially compared to East Asian countries, the long-standing providers of outsourcing services. On the whole, the frequency of each of the subgroups was sufficient to perform reliable analysis of variance tests—as a rule of thumb, 20 is often given as a minimum sample size per group [

70].

As discussed before, the adopted understanding of social responsibility assumed that CSR involvement is a second-order reflective construct expressed through four dimensions. The CSR dimensions, themselves being first order reflective latent variables, were measured with five-point Likert-scale items. The specific content of the items used in the survey questionnaire is given in the following table. Literature sources that were used to inform the scale building choices were also indicated in

Table 3.

Table 3.

Dimensionality and manifest variables in the CSR involvement model.

Table 3.

Dimensionality and manifest variables in the CSR involvement model.

| Item Designation in Measurement Model | Item Content | Literature Sources |

|---|

| Latent variable: Value Chain Relations |

| VAL_1 | We use CSR principles in selecting suppliers. | [71,72,73,74,75,76,77,78] |

| VAL_2 | We create the image of our firm, brands, and products with reference to social values. |

| VAL_3 | Our customers are aware that part of our product prices supports our CSR initiatives. |

| VAL_4 | Payments to our suppliers are made in keeping with contractual obligations. |

| VAL_5 | Our firm seeks to follow international standards and certificates (e.g., ISO 26000, SA 8000, Fair Trade). |

| Latent variable: Community Relations |

| COM_1 | We are involved in charitable initiatives. | [71,75,79,80] |

| COM_2 | We have a special organizational unit (e.g., a foundation) tasked with social and/or charitable objectives. |

| COM_3 | Our employees are involved in voluntary charitable activities. |

| COM_4 | We provide financial support to local communities in terms of their infrastructural, cultural, educationalm and sports-related needs. |

| Latent variable: Natural Environment |

| ENV_1 | We take care to prevent events that could have negative impacts on environment and society | [71,79,80,81,82] |

| ENV_2 | We strive to limit our use of energy, water, and other resources. |

| ENV_3 | We use recycling and try to limit our waste. |

| ENV_4 | We aim to curb our CO2 emissions. |

| ENV_5 | We use eco-friendly technologies and materials in our processes, products, and packaging. |

| Latent variable: Employee Relations |

| EMP_1 | We have control and supervision mechanisms to monitor, support, and enforce ethical behavior among employees. | [80,83,84] |

| EMP_2 | Our employees have ways to report unethical conduct without fear of retribution. |

| EMP_3 | We have implemented procedures to enable swift reaction against acts of breaching employee rights. |

| EMP_4 | In our company we respect principles of diversity management, including gender and disabilities. |

| EMP_5 | We have implemented a system of creating good CSR practices by employees. |

| EMP_6 | Employees are consulted before we implement changes in our company. |

The validity of the above model was tested with confirmatory factor analysis using the maximum likelihood estimation.

Considering that the sample was composed of firms representing three distinct industries (

i.e., food production, chemical manufacturing, and commerce, both wholesale and retail), it was essential to test the model structure for measurement invariance. Measurement invariance is found when all relevant subgroups could be equally well represented by the same pattern of regression weights and covariances in the model. A common way to test for measurement invariance is to compare an unconstrained model (assuming that all groups have all parameters estimated independently) with a model where regression weights and covariances are set to be equal across all groups. Then chi-square statistics are computed for alternative models and the chi-square differential is obtained. Evidence for measurement invariance is found when the chi-square difference is insignificant [

85] and so—consistent with the principle of parsimony—the simpler (

i.e., constrained) option should be retained. In the current study, the chi-square value representing discrepancies between the two models was 47.426, with 40 degrees of freedom and a p-value of 0.196. This implies that the model where all firms are pooled together as a single group is superior, as the more complex solution with different parameters across groups does not offer markedly better accuracy. From a practical perspective, our research appears to suggest that CSR involvement (at least when measured using the metrics deployed in our survey) is a universal characteristic reflected in a similar way (following the same structural patterns) in firms with various backgrounds.

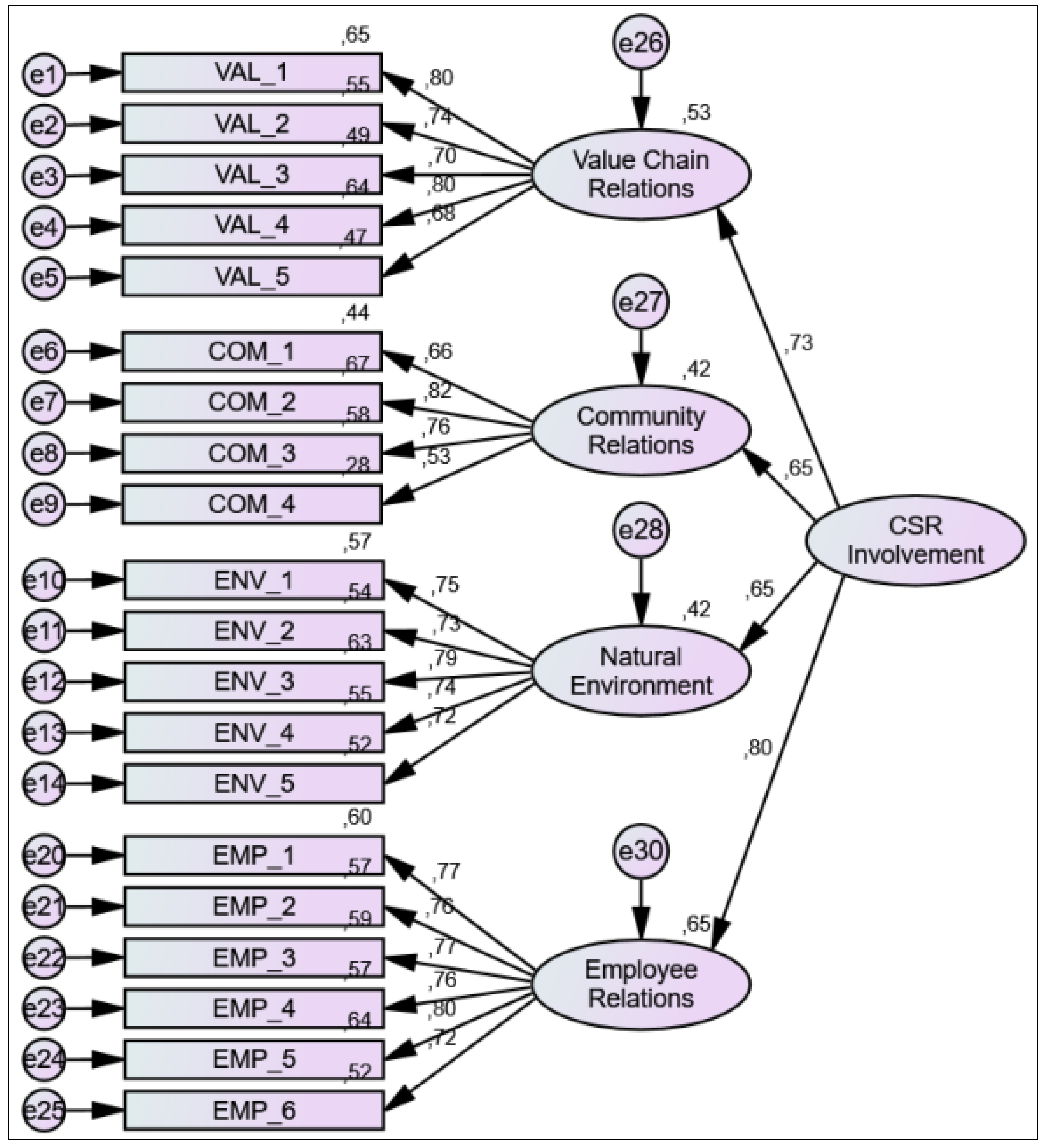

The resultant CFA diagram, with its standardized regression parameters and squared multiple correlations, is depicted in

Figure 1.

Figure 1.

CFA model of the CSR involvement construct.

Figure 1.

CFA model of the CSR involvement construct.

Source: Own elaboration.

In order to evaluate the model fit with the sample data, we used a set of common indices as set out in

Table 4.

Table 4.

Overall fit measures for the CFA model.

Table 4.

Overall fit measures for the CFA model.

| Metric | Value | Threshold for a Well-Fitting Model |

|---|

| Chi-square/df (relative chi-square) | 2.326 | <3 for good fit |

| p-value for the model | <0.001 | >0.05 |

| GFI (goodness of fit index) | 0.905 | ≥0.9 |

| CFI (comparative fit index) | 0.942 | ≥0.9 |

| AGFI (adjusted goodness of fit index) | 0.880 | ≥0.8 |

| PCFI (parsimony comparative fit index) | 0.823 | ≥0.8 |

| RMSEA (root mean square of approximation) | 0.059; HI90 = 0.066 | ≤0.05 for good model fit; ≤0.08 for adequate fit; in addition, the upper 90% confidence limit (HI 90) should be no more than 0.08 for a well-fitting model |

The above metrics indicate a close match between the model and the data. The only exception is the chi-square test, which is significant and rejects the null hypothesis of the lack of differences between the observed covariance matrix and the one implied by the model. However, the chi-square statistic tends to be considerably inflated for large samples, which results in excessive sensitivity of the test. Therefore, this measure is considered unreliable and could be disregarded if other metrics point to a well-fitting solution [

85,

87], which is what happens in the current analysis.

Table 5 provides insights into CSR dimensions in terms of reliability (Cronbach’s Alpha), convergent validity (AVE, or average variance extracted) and discriminant validity (MSV, or maximum shared variance).

Table 5.

Reliability and validity measures of CSR involvement dimensions.

Table 5.

Reliability and validity measures of CSR involvement dimensions.

| Construct | Cronbach’s Alpha | AVE | MSV |

|---|

| Value Chain Relations | 0.839 | 0.596 | 0.345 |

| Community Relations | 0.788 | 0.493 | 0.272 |

| Natural Environment | 0.861 | 0.562 | 0.271 |

| Employee Relations | 0.896 | 0.583 | 0.345 |

The metrics in

Table 5 are implying a solution that does not reveal any apparent issues compromising its interpretability. In particular, it seems that the manifest variables used to represent the latent constructs have high levels of internal consistency—Cronbach’s alphas are all greater than 0.07, as suggested in Malhotra [

88]. AVE values, which show how well hidden variables are represented by their corresponding indicators, should be at least 0.5 [

89], which is true for all constructs except Community Relations; however, even there the cut-off is missed by only a small amount. As such, Community Relations appear to explain only 49% of variance in its indicators, with the rest of the variability accounted for by other factors outside of the model. This outcome is not entirely unexpected, since it could easily be argued that a firm’s contributions to local communities through financial aid or the work of its employees are strongly context-sensitive and determined—for example—by the particular locale in which the firm operates. Naturally, these external influences seem to be quite independent of the company’s stance on CSR.

Having concluded that the CSR involvement model is at least adequate in how it fits the collected data, we derived from it five new variables to represent the latent constructs in further analysis.

To investigate how various business models compared in terms of CSR involvement, we performed five one-way ANOVA tests. Each test had a different dependent variable; either the general CSR involvement level or one of the four of its dimensions. As an independent variable, the same factor was used in each test, which showed which of the five business models each company followed. The outcomes of the ANOVA were given in

Table 6.

Table 6.

One-way ANOVA outcomes for differences in CSR involvement among business models.

Table 6.

One-way ANOVA outcomes for differences in CSR involvement among business models.

| Business Model | N | Mean | Std. Error | ANOVA Test Results |

|---|

| Overall CSR Involvement | traditionalist | 168 | −0.141 | 1.007 | F (4;380) = 5.688 p < 0.001 |

| market player | 71 | 0.420 | 0.886 |

| contractor | 30 | −0.129 | 0.932 |

| distributor | 66 | −0.206 | 1.029 |

| integrator | 50 | 0.225 | 0.948 |

| total | 385 | 0.000 | 1.000 |

| Employee Relations | traditionalist | 168 | −0.154 | 1.015 | F (4;380) = 4.670 p = 0.001 |

| market player | 71 | 0.337 | 0.944 |

| contractor | 30 | −0.011 | 0.930 |

| distributor | 66 | −0.177 | 1.019 |

| integrator | 50 | 0.278 | 0.892 |

| total | 385 | 0.000 | 1.000 |

| Community Relations | traditionalist | 168 | −0.142 | 0.952 | F (4;380) = 5.542 p < 0.001 |

| market player | 71 | 0.431 | 0.921 |

| contractor | 30 | −0.207 | 0.964 |

| distributor | 66 | −0.153 | 1.011 |

| integrator | 50 | 0.190 | 1.095 |

| total | 385 | 0.000 | 1.000 |

| Natural Environment | traditionalist | 168 | −0.031 | 1.010 | F (4;380) = 3.618 p = 0.007 |

| market player | 71 | 0.299 | 0.827 |

| contractor | 30 | −0.116 | 1.068 |

| distributor | 66 | −0.303 | 1.087 |

| integrator | 50 | 0.150 | 0.924 |

| total | 385 | 0.000 | 1.000 |

| Value Chain Relations | traditionalist | 168 | −0.109 | 1.011 | F (4;380) = 3.212 p = 0.013 |

| market player | 71 | 0.353 | 0.851 |

| contractor | 30 | −0.175 | 1.018 |

| distributor | 66 | −0.084 | 0.994 |

| integrator | 50 | 0.081 | 1.066 |

| total | 385 | 0.000 | 1.000 |

As evidenced in

Table 6, the ANOVA tests were all significant, implying the existence of meaningful differences among business models. This outcome supports our first hypothesis (H.1) predicting unalike involvement in CSR from firms following dissimilar business models.

Looking at the means, it is clear that market players followed by integrators consistently had the highest scores on the general metric of CSR, as well as on its particular dimensions. At the other end of the spectrum were traditionalists, contractors, and distributors, with quite similar negative averages. Considering that the basic ANOVA test only informs about the presence or lack of at least one difference between all pairs of subgroups, to formally verify our second more specific hypothesis we defined a specific comparison of two groups of firms using contrasts. As per the second hypothesis, the first group consisted of market players and integrators, while the second comprised traditionalists, contractors, and distributors. The contrast weights assigned to particular business models were as follows: market players 3, integrators 3, traditionalists –2, contractors –2, and distributors –2. It can be noted that the members of the same comparison groups have identical weights, and the sum of all weights is 0, which is required from a correctly specified test.

Table 7 shows the outcomes of the contrast tests for the general CSR involvement and its respective dimensions.

Table 7.

Contrast test results comparing two groups of business models in terms of CSR involvement.

Table 7.

Contrast test results comparing two groups of business models in terms of CSR involvement.

| CSR Metrics | Value of Contrast | Std. Error | t | df | Sig. (2-Tailed) |

|---|

| Overall CSR Involvement | 2.887 | 0.707 | 4.082 | 380 | 0.000 |

| Employee Relations | 2.529 | 0.710 | 3.559 | 380 | 0.000 |

| Community relations | 2.865 | 0.708 | 4.048 | 380 | 0.000 |

| Natural Environment | 2.245 | 0.715 | 3.142 | 380 | 0.002 |

| Value chain relations | 2.037 | 0.716 | 2.842 | 380 | 0.005 |

As can be seen, the values of contrasts are all positive and significant, which indicates that the first group of market players and integrators had consistently greater values on all CSR metrics then the second group. This evidence points to the second hypothesis being correct, which in substantive terms means that market players and integrators displayed stronger CSR involvement than other types of business models.

To further investigate the individual pairwise differences and similarities between various business models, it is informative to use

post hoc tests, which compare individual ANOVA subgroups while controlling for familywise error. Hence,

Table 8 sets out significant

post hoc tests for all possible pairings of business models calculated with the Games–Howell procedure.

Table 8.

Games–Howell multiple comparisons of business models on CSR involvement (only differences significant at the 0.05 and 0.1 levels were included).

Table 8.

Games–Howell multiple comparisons of business models on CSR involvement (only differences significant at the 0.05 and 0.1 levels were included).

| Dependent Variable | Comparison Pairs of Business Models that Best Describes Respondents’ Firms | Mean Difference | Std. Error | Sig. |

|---|

| Overall CSR Involvement | traditionalist | market player | −0.561 | 0.131 | 0.000 |

| market player | traditionalist | 0.561 | 0.131 | 0.000 |

| contractor | 0.549 | 0.200 | 0.061 |

| distributor | 0.626 | 0.165 | 0.002 |

| contractor | market player | −0.549 | 0.200 | 0.061 |

| distributor | market player | −0.626 | 0.165 | 0.002 |

| integrator | | Significant differences not found |

| Employee Relations | traditionalist | market player | −0.491 | 0.137 | 0.004 |

| integrator | −0.432 | 0.149 | 0.036 |

| market player | traditionalist | 0.491 | 0.137 | 0.004 |

| distributor | 0.514 | 0.168 | 0.022 |

| contractor | | Significant differences not found |

| integrator | market player | −0.514 | 0.168 | 0.022 |

| integrator | −0.456 | 0.178 | 0.085 |

| traditionalist | 0.432 | 0.149 | 0.036 |

| distributor | 0.456 | 0.178 | 0.085 |

| Community Relations | traditionalist | market player | −0.572 | 0.132 | 0.000 |

| market player | traditionalist | 0.572 | 0.132 | 0.000 |

| contractor | 0.638 | 0.207 | 0.026 |

| distributor | 0.583 | 0.166 | 0.005 |

| contractor | market player | −0.638 | 0.207 | 0.026 |

| distributor | market player | −0.583 | 0.166 | 0.005 |

| integrator | | Significant differences not found |

| Natural Environment | traditionalist | market player | −0.329 | 0.125 | 0.070 |

| market player | traditionalist | 0.329 | 0.125 | 0.070 |

| distributor | 0.602 | 0.166 | 0.004 |

| contractor | | Significant differences not found |

| distributor | market player | −0.602 | 0.166 | 0.004 |

| integrator | | Significant differences not found |

| Value Chain Relations | traditionalist | market player | −0.462 | 0.128 | 0.004 |

| market player | traditionalist | 0.462 | 0.128 | 0.004 |

| distributor | 0.437 | 0.159 | 0.052 |

| contractor | | Significant differences not found |

| distributor | market player | −0.437 | 0.159 | 0.052 |

| integrator | | Significant differences not found |

At the 0.05 significance level, the Games–Howell tests confirm the earlier observation that market players displayed the best results of all investigated business models in terms of following the CSR guidelines, in both the general and particular sense. On the other hand, traditionalists, distributors, and contractors showed significant discrepancies when compared to market players, but not to integrators. The fact that market players are significantly different from all other types of business models except integrators, coupled with the observation that there were no significant differences among traditionalists, contractors, and distributors, lends further support to our theory-based assumption that there were two general groups of business models in terms of adherence to the CSR principles. A part of that proposition was already validated with the contrast tests, but post hoc tests provide more evidence by implying that the two groups might be internally homogenous in their degrees of CSR implementation.

8. Theoretical and Practical Implications of the Study

This study has made several valuable contributions to the theory and practice of management.

We have shown that CSR could be a universal phenomenon in that it appears in a similar manner in manufacturing and service companies of different industries and sizes. This is not to say that all groups of companies are the same in terms of the intensity of involvement in CSR, but rather it suggests the same underlying mechanism governing relationships between the second-order CSR construct, its four dimensions, and their measurable indicators. This conclusion seems to be generally in line with many earlier works based on a case study method. Many of them are relying on the conceptual framework of CSR with four similar dimensions that appeared to show equal relevance when applied to firms from different industries, e.g., [

7,

9,

10,

57]. However, with survey research, due to its high level of standardization, developing a measurement tool adequate for many types of companies is more problematic. The previous quantitative research that we know of involved narrowly defined industries, very often manufacturing, which amounted to relatively homogeneous samples more suited for statistical analysis, e.g., [

80,

82,

84]. In contrast, this current paper offers questionnaire scales with statistical evidence, implying that the same measurement model could be used in all three industries with similar validity and reliability. On the face of it, it would seem that firms operating in such different contexts would display considerable dissimilarities. One source of such differences could be in distinct legal frameworks regulating environmental issues in chemical industry, food manufacturing, and retailing, with the chemical industry subjected to the most stringent conditions. However, most of these differences pertain to very specific limits on emissions, use of energy and resources, and other aspects of environmental protection, while our measurement scales ask about those things only in a general way that seems to be applicable to all studied companies.

Arguably the most natural area where CSR could be applied in a similar fashion across all three industries is employee relations. This is not only because of the intrinsic versatility of human resources, which can take a similar form in many different settings, but also in large part due to the same system of legal regulations applying to each and every firm. This comes as no surprise since “it is clear that law and legal standards in various forms … play a considerable role in relation to the substance of CSR, and for implementation and communication of CSR” [

90].

Considering that the studied firms were medium and large in size, and most of those firms in said industries in Poland are operating with various implementations of ISO systems, this could also be a unifying factor. The ISO systems have many regulations that determine how firms should organize their assorted functions and processes, including guidelines that are consistent with CSR principles (e.g., environmental protection, employee relations, external stakeholder relations, value chain cooperation). The capability of ISO standards to drive similar implementations of responsible business practices was shown before in papers by other authors [

91,

92].

Given the discussion so far, it seems that our multiple measurement scale could be a versatile and capable tool for studying CSR in companies across various business contexts.

One practical application of our outcomes could be in the area of public policy. Even though most governments in developed countries make efforts to support responsible business standards, there are reasons to believe that these actions have only limited effectiveness [

93]. As such, our findings suggest that local and national governments, as well as other policymakers interested in promoting sustainable growth and ethical standards in business, should support above all enterprises operating in line with the business models of market players and integrators. The present research indicates that these business models are most CSR-oriented, which should bring about the best effects in terms of—for example—environmental protection, employee relations, harmonious cooperation with local communities, and conscientious attitude towards other stakeholders. In other words, here public policy measures would be the most aligned with the intrinsic tendencies of these types of businesses to act in a responsible fashion.

Another possibly useful insight for mangers is our observation that CSR involvement might contribute to enhancing brand equity, leading to a higher brand value and increased value for shareholders. This corroborates some earlier research, involving quantitative surveys, demonstrating that CSR can build trust with customers, which in turn enhances corporate reputation and results in greater brand equity [

94]. This stems from the fact that market players and integrators both had higher levels of CSR implementation, and one likely reason for that could be related to them building stronger brands among consumers and business partners, which is among the defining features of their business models. It should be noted, though, that this is more of a supposition than a finding based on direct evidence. Despite a degree of uncertainty, such a relationship points to an interesting topic of a follow-up study explicitly investigating the links between business models, CSR involvement, and brand value.

Our research seems to substantiate a theoretical proposition of a feedback link between CSR and business models, which can be found in many conceptual papers, e.g., [

95]. According to theory and—mostly qualitative—observations, firms that adopt successful CSR programs and initiatives tend to experience changes in organizational culture, which becomes more CSR-oriented and promotes further responsible corporate behaviors, including deeper structural changes to strategies and business models [

96]. This mechanism could arguably result in a self-perpetuating virtuous circle, driving sustainability commitment to become ever deeper. Based on the current study, it can be noted that the business models supporting CSR, and in turn being supported by it, are market players and integrators. Their CSR metrics, markedly better than those of other types of companies, can be interpreted as pointing to the presence of such a feedback mechanism.

The tendency of market players and integrators to act in a more socially responsible way towards their stakeholders, including value chain members, could serve other companies as a sign of good candidates for mutually beneficial partnerships. Indeed, it is more so because the business classification scheme employed in the study is easy to use by practitioners, who can readily identify market players and integrators among their potential partners.

The study findings could also provide a measure of reassurance to those consumers who are keen to support ethical companies but are uncertain about the sincerity of their CSR claims. According to a recent segmentation study of Polish households, those who are sensitive to cause-related marketing and are willing to pay more for products of firms that contribute to solving relevant social problems make up almost 30% of the adult population [

97]. It seems that CSR in most active companies (market players and integrators) is not “skin deep” but tends to be implemented quite thoroughly and comprehensively. Therefore, it is believable that many of the CSR claims used as promotional devices are genuine projections of strategic orientation and organizational culture values in firms with the two most “sustainability-friendly” business models.

9. Limitations and Directions for Further Research

Similar to other projects of this kind, one rather obvious constraining feature of the study that could limit the scope of possible generalizations is the nature of the surveyed population. It could be contended that locating the survey in Poland in the context of the three industries can make it problematic to infer beyond this research setting to other countries or types of companies. However, the patterns that transpired in our data seem to be of a general nature, well grounded in theory, and explainable in terms of their underlying causal mechanism. These likely causal mechanisms, tying up the two types of business models with a more active stance in social responsibility, as explained earlier in the paper, could conceivably be found in firms using the same business models from beyond our research population. It would be, nevertheless, interesting to see if the outcomes can be replicated in different research settings.

Another idea for supplementary research is a qualitative multiple-case study where causal mechanisms, leading from types of business models to various levels of CSR involvement, could be probed in depth. Such an investigation could serve to validate our literature and experience-based suppositions about the reasons for differences between business models, and possibly identify new patterns of relevant factors. Those new factors might involve propositions of mediating or moderating variables that could be controlled for in survey research to outline a more complete picture of associations between business models and CSR.

New research, in addition to including mediating and moderating variables, could also look at financial metrics (e.g., profit margin, ROA, ROE), and how these correspond to CSR levels among firms with different business models. It is plausible that correlations from CSR involvement to financial outcomes might vary in significance and strength in different business model groups.

{kind=link}