2.1. Balanced Scorecard

The Balanced Scorecard constitutes one of the most important business tools developed in recent years and is widespread in business, industry, governments, and non-profit organizations (

Grigoroudis et al. 2012). The thorough research of

Madsen and Slåtten (

2013) identified which factors are responsible for the wide diffusion of the Balanced Scorecard in certain countries. The role of consulting and software firms seems to be of great importance. In their recent study,

Madsen and Slåtten (

2015) illustrated how the idea of the Balanced Scorecard spread among countries, sectors, or organizations and how it is implemented within an organization. It is evident that the adoption process of management ideas such as the Balanced Scorecard is driven by supply and demand. This is due to the fact that consultants try to discover more complex management concepts and provide their clients with customized consulting services.

The present research utilizes the Balanced Scorecard as a tool in order to assess the effectiveness of a co-financed European Union program, which is aimed at fortifying the competitiveness of Greek SMEs. Recent research efforts highlight the importance of the Balanced Scorecard in assessing the performance of various schemes. For instance,

Chen et al. (

2020) applied the Balanced Scorecard in order to evaluate the sustainable performance of Chinese emerging family farms. Similarly,

Pham et al. (

2020) evaluated the performance of public hospitals in Vietnam, while

Bawaneh (

2019) measured the effectiveness of Jordanian manufacturing companies. The present study differs from several other studies as it utilizes intelligent analytics in order to predict the values of the financial indicators given the implemented actions.

The Balanced Scorecard supports the strategic planning and change management by aligning and transmitting the strategy and vision of the organization for each and every employee (

Kaplan and Norton 1996). This is achieved by connecting the targets of the organization with the targets of its relevant departments. It is evident that organizational environments are evolving rapidly and becoming increasingly complex. They are also more capable in dealing with organizational changes and innovations in order to cope with corporate competitiveness. As a consequence, which

Kim and Choi (

2020) have pointed out, the shorter product life-cycles because of rapid technological change make competition more intense and demand highly unpredictable. Thus, the use of balanced approaches to performance management is absolutely vital.

The Balanced Scorecard investigates the organization by means of four different perspectives (

Kaplan and Norton 1992):

The financial perspective (earnings per share, return on total assets, return on equity, etc.);

The customer perspective (market share, customer satisfaction, brand recognition, customer retention, customer complaints, etc.);

The internal business process perspective (cycle time, cost of services, capacity usage rate, labor utilization rate, etc.);

The learning and innovation perspective (employee productivity, employee satisfaction, number of cross-trained employees, leadership development, etc.).

Identifying and analyzing the intricate relations among the four aforementioned perspectives is of great importance in the implementation of the Balanced Scorecard. An important finding in the relevant literature is that this is because the changes which take place affect each other in a non-linear form (

Salmon et al. 2019). In each and every perspective, the Balanced Scorecard places emphasis not only on result-oriented criteria concerning what should be achieved, but also on criteria targeted as to how it should be achieved. Following this scheme,

Papalexandris et al. (

2005) have highlighted in their study that a satisfactory equilibrium is achieved among short- and long-term objectives concerning the outcomes (lag performance measures) and the performance drivers (lead performance measures) of these particular outcomes.

Nevertheless, the contribution of the Balanced Scorecard—the evident realization of a great many performance alternatives, not considering the situation from the viewpoint of financial standards, adds complexity to the measurement of performance. Studies have brought to our attention the fact that the size of an organization, its structural complexities, and the variety of processes involved, are some of the important issues which make the measurement of organizational performance a complex issue (

Keeble et al. 2003). The development of the right set of performance indicators within an organization requires the involvement of every unit which is demanded to apply them. In order to solve the problem at hand, the use of predefined models such as the Balanced Scorecard, so as to measure overall organizational performance, is a common practice (

Medne and Lapina 2019). With regard to the so-called information overload, one should bear in mind the existing biases and the various evaluations which enhance the indicators of the Balanced Scorecard (

Chan 2009).

Siskos and Spyridakos (

1999) came to the conclusion that multi-criteria applied in the decision-making process are absolutely necessary for dealing with this elaboration, in an attempt to evaluate performance and reach the desired outcomes.

Concerning the correct application of the Balanced Scorecard, organizations should closely examine their strategy so as to develop the strategic objectives which will be closely interrelated to the cause and effect target. In turn, the strategic objectives must be related to qualitative measures, which will be specifying what the organization should do in an attempt to achieve them. These indicators are connected with specific targets, which have a predetermined timetable of materialization. The last vital step according to

Salmon et al. (

2019), concerning the achievement of the aforementioned targets, is that specific action plans will be selected, which also have predefined timetable and budget constraints.

Falle et al. (

2016) in their research presented a solid example of the development and implementation of the Balanced Scorecard in an SME, illustrating various supporting factors and challenges which affect this process. The special needs of each and every organization should always be taken into account throughout the application process.

It should be kept in mind that although a solid evaluation metric is in existence, the results cannot always be predictable. In those cases that the distance between company goals and current criteria is enlarged, the use of feedback systems may boost its effectiveness (

Cha et al. 2019).

Nigri and Del Bardo (

2018) investigated the integration of sustainability indicators in an attempt to apply them in managerial systems. In addition, they examined a variety of management systems to be used as a benchmark for reporting the outcomes.

According to

Yun and Yigitcanlar (

2017), in an attempt to be highly competitive, organizations should take into account altering their business models constantly. They must also assess the results of their decisions and actions while they continuously compete for resources and customers (

Bentes et al. 2012). Knowledge management is a key element in favor of this process. Knowledge assets instigate an organization’s success and are an important parameter in the creation of values in order to ameliorate business performance together with entrepreneurial thinking and increasing business opportunities (

Yan et al. 2019). Organizations using the Balanced Scorecard can better closely examine the extent to which their strategies bring about positive results. However, it should be reminded that due to the fact that they have a tendency to become increasingly service-oriented with less concrete expected results, the implementation of the Balanced Scorecard scheme provides a real challenge to them.

Bearing in mind that a relevant performance measurement tool is at hand like the Balanced Scorecard, enterprises of all kinds are capable of specifying their vision by means of outcomes which can be measured (

Shepko and Douglas 1998). In this way, the projects within a particular structure can be better monitored and directly related to the individual strategic plans of the organization. Projects can be perceived as “mini-organizations”, demanding the exact specification and benchmarks of the parent corporation. Due to the fact that projects are somewhat more structured and controllable in conjunction to a specific organization, they have been associated with a high failure rate in the majority of the success-oriented variables (

Stewart 2001). In an attempt to manage projects more successfully, as well as the general wellbeing of the organization which is the main provider of these services, the Balanced Scorecard methodological approach can be implemented with the aim of conducting health checks for the entire life-cycle of a particular project.

The Balanced Scorecard has been traditionally applied in private enterprises but recently it has proved useful in a variety of publicly funded projects (

Kim et al. 2017). Due to the fact that the use of public funds has been scrutinized by governments, many public organizations have resorted to the private sector in an attempt to improve their accountability (

Northcott and Taulapapa 2012). One should bear in mind that the transition from private to public enterprises in terms of using the Balanced Scorecard is not an easy one and many modifications are required in its implementation. This is because there seem to be multiple conglomerates of both customers and stakeholders, concerning the dissimilar elements of public organizations (

Greatbanks and Tapp 2007).

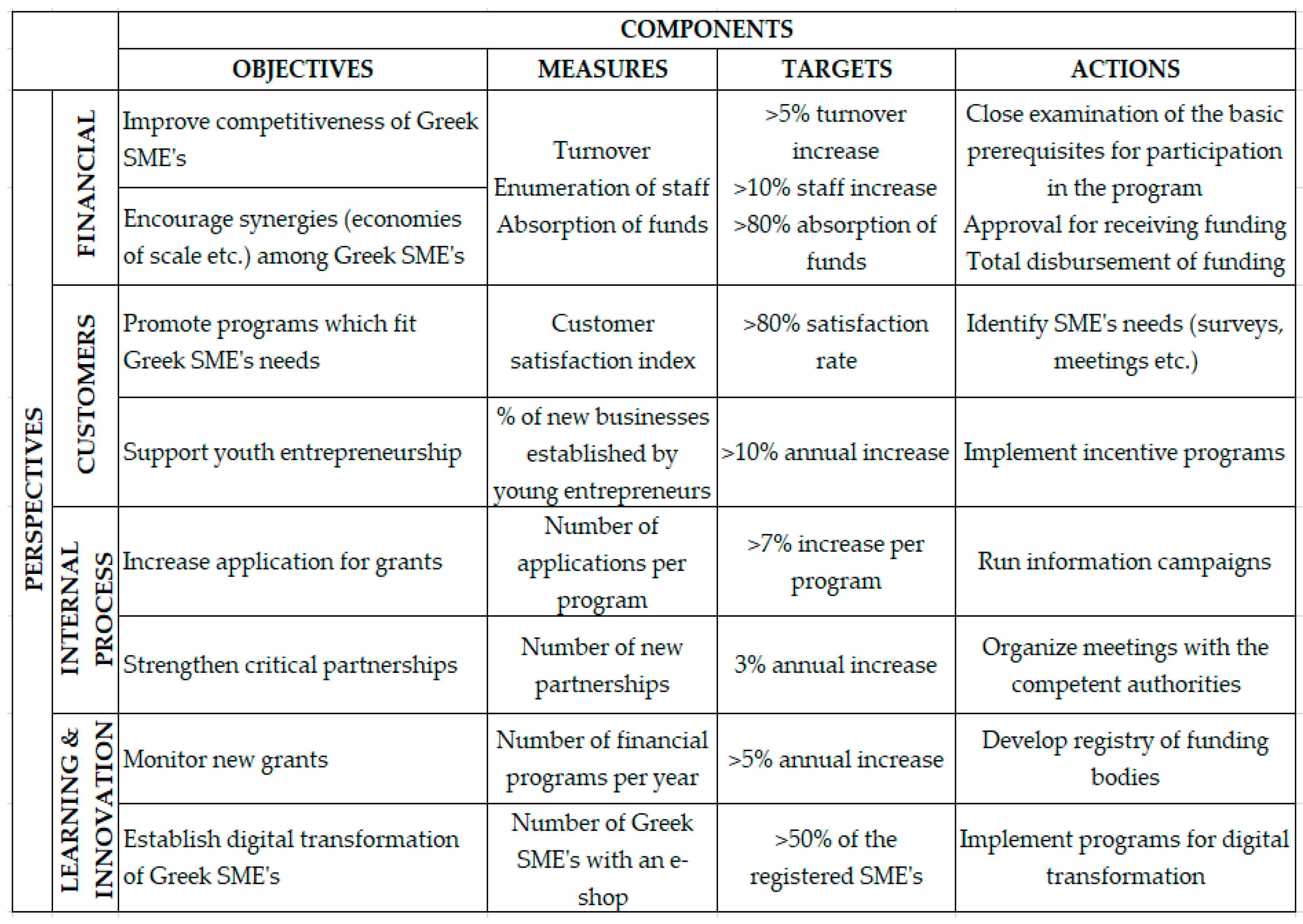

Given the aforementioned,

Figure 1 exhibits the Balanced Scorecard of the government body which materialized the financial program studied in the present paper.

2.2. Predictive Analytics

Invaluable information can be extracted using Big Data Analytics (BDA) including descriptive, predictive, and prescriptive research. Recent studies have highlighted the contributions of big data and predictive analytics in tackling modern era problems and in creating cutting edge technologies.

Lyons and Lăzăroiu (

2020) and

Scott et al. (

2020) investigated the use of smart city data in dealing with the COVID-19 crisis.

Poliak et al. (

2020) conducted a research study to investigate the social dimensions of a new technology which is based on BDA, like self-driving cars. Similarly,

Bourke et al. (

2019) and

Eysenck et al. (

2019) highlighted with their research how predictive analytics can assist decision-making concerning the evolution of Industrial Internet of Things Systems.

In business environments, the use of analytics and advanced machine learning promotes the decision-making process for each and every organizational structure (

Lismont et al. 2017).

Meyers et al. (

2019) have studied how the use of workforce analytics facilitates personnel objective settings and planning. Other researchers have used analytics to estimate future financial performance.

Lee et al. (

2018) have studied the extent to which there is a connection between business sales patterns and business text patterns, in an attempt to predict the future financial performance of a company by means of business text analysis. The analysis of data patterns and variables can lead to improved statistical models and a great variety of related applications. It has been customary to utilize machine learning algorithms in order to conduct effective analyses in the process industry. The various existing applications of machine learning have not only provided invaluable information in the decision-making process but have also modified the style of the process industry as a whole (

Ge et al. 2017).

There is a great variety of reasons why organizations utilize analytics. Some of these are: advancing the effectiveness of financial and operational outcomes, reinforcing both local and global perspectives, and the establishment of funding programs of changing economies. The implementation of predictive analytics suggests a great variety of benefits, such as the achievement of a more satisfactory organizational performance as well as a better understanding of organizational dynamics including a better application of available data (

Rajni and Malaya 2015). The final gains of BDA in business management is to arrive at more effective decision-making processes, comprehend business activities to a greater degree, minimize risk, and contribute to a better understanding of consumer behavior, always aiming at customer satisfaction (

Mello and Martins 2019).

The starting block in machine learning model development is data preparation. This involves extracting the dataset from the database, examining the dataset structure, and making data selections (

Ge et al. 2017). After the dataset is identified, a suitable regression model is selected in order to perform the analysis. There are various regressors that can be selected in order to analyze the dataset, such as Linear Regression, Support Vector Regression (SVR), Artificial Neural Network (ANN), k-Nearest Neighbors (k-NN), and M5 model tree. Linear regression is used in order to model the relationship between a dependent variable and one or more independent variables. On the other hand, SVR tries to maintain the error within a certain threshold, while the majority of linear regression models aim at minimizing the sum of squared errors. From another perspective, SVR allows us to examine the acceptable error within the model.

In addition, ANN’s attempt at investigating systems of interrelated neurons which are involved in the mutual exchange of messages is just like the biological neural networks. Each and every connection has been assigned with numeric weights, which can be modified based on the experience related to the entire learning process. Thus, ANNs are able to approximate any type of function by learning from the available data (

Ge et al. 2017). Furthermore, k-NN can be used for both classification and regression. In both cases, the input consists of the k closest training samples while the output is related to the extent to which the method is applied to either classification or regression (

Ge et al. 2017). Finally, the M5 model tree constitutes a decision tree learner applied in predicting values for a numerical response variable Y and can predict continuous numerical attributes. The M5 model tree is a way of simulating even hundreds of attributes with wide varieties of dimensionality (

Kisi et al. 2017).

,

,

{kind=link}