Accounting Information Systems: Scientific Production and Trends in Research

1

Porto Accounting and Business School, Polytechnic Institute of Porto, 4465-004 São Mamede de Infesta, Portugal

2

Department of Accounting, University of Minho, 4704-553 Braga, Portugal

*

Author to whom correspondence should be addressed.

Systems 2021, 9(3), 67; https://0-doi-org.brum.beds.ac.uk/10.3390/systems9030067

Submission received: 12 July 2021

/

Revised: 28 August 2021

/

Accepted: 30 August 2021

/

Published: 3 September 2021

Abstract

:This paper aims to provide a state-of-the-art overview in research on Accounting Information Systems, analyzing scientific production characteristics and identifying this topic research trends. A quantitative bibliometric analysis is conducted on papers specifically focused on Accounting Information Systems, published in journals indexed on Web of Science database. The research methodology and design were based on an inductive approach of a set of studies with the objective of theoretical development in the field of investigation. We found 144 articles on this subject. The first article was published in 1973. However, most papers were published during the last 10 years although the highest interest in Accounting Information Systems study among scholars concentrates on a short period, which is around 2020. We identify three research topics, as the following research trends: (1) the Accounting Information System impact in the organization (e.g., performance, innovation, reorganization of activities, information reporting); (2) the Accounting Information System Construction, (3) the importance of implementation of the Accounting Information System in small and medium-sized enterprises and Public-Sector; and (4) the factors that contribute to Accounting Information System efficiency/quality. These themes fit into a theoretical framework, in which agency and contingency theory are highlighted. In addition, by promoting the analysis of strict bibliometric tools, we also identified authors, journals, organizations and countries/regions that contributed most to the development of the investigation in this research topic. The results of this research add insights to the existing literature and serve as a guide for future research in Accounting Information Systems context, as well as help organizations, public, private and governments to establish their strategies in this area.

1. Introduction

Digital technology has revolutionized our daily lives and the way we carry out our human activities within our homes and at work [1]. Advances in information technology indicate that most manual accounting systems are being replaced by digital Accounting Information Systems, which are faster and more accurate [2].

Information System can be defined as the set of human and capital resources within an organization that is responsible for collecting and processing data to produce useful information to all management levels in planning and controlling the organization activities [3].

Accounting information is required by managers to predict and establish the firm’s future strategic goals [4]. Management Accounting Information System implementation, when successful, has a significant impact on improving the organization or company performance [5]. To achieve decision-making success, accounting information must be of high quality, relevant and useful in the decision-making process [6]. However, currently, many companies have not been able to produce quality accounting information [4], useful for decision-making.

According to Septriadi et al. [6], the measurement of information quality is based on its relevance, precision, accessibility, timeliness, completeness, clarity and consistency.

McCallig et al.’s [7] (p. 40) study shows that an Accounting Information System can be developed to increase the “representational faithfulness of its accounting data by emulating the audit function”.

In this recent theme, literature has attempted to respond to the problems that Accounting Information Systems presents. For Monteiro et al. [8] and Hla and Teru [9], Accounting Information System quality can be maintained if there is a sound and effective internal control system. In this context, Christensen [10] refers that auditor can enhance financial reporting credibility; however, it introduces a new agency problem between stakeholders and auditors [7]. This agency problem may arise because auditors may act in the stakeholders’ interest in order to hire them [11].

On the other hand, another problem that literature presents is the difficulty that stakeholders may have in establishing whether financial information presents a true and appropriate company image due to information asymmetries and agency problems [12]. Given this importance, Kumar et al.’s [13] study did a retrospective analysis of articles in the International Journal of Accounting Information Systems and his results show that one of the most dominant themes that the journal has followed over the years is related to emerging technologies in accounting, and the application of technologies to business assurance and information disclosure.

This investigation is based on contingency and agency theory specifically the positive agency theory, according to positive philosophy. Positive agency theory proposes that principals can mitigate agency costs by establishing appropriate incentive contracts and by incurring monitoring costs. The first theory, recognize that external environment influences companies’ actions, on the other hand, agency theory seeks to understand the problems created when one party, the agent, is acting for another, the principal, the agency, problem refers to a conflict of interest between a company’s management and the company’s shareholders [14]. Both theories have great relevance to Accounting Information Systems. First, in contingency theory, the external environment has been one of the pillars for the evolution and implementation of Accounting Information Systems; second, in agency theory, when implementing Accounting Information Systems, there will be certain actions depending on the interests of different agents [15].

Accounting literature makes a significant contribution to information systems management, it highlights that accounting insights can help information systems profession manage the intangible aspects of information technology projects, including risk assessment, control and coordination; the biases associated with the use of decision support systems, and the company’s authority and incentive structure [16,17]. Accounting Information System study is of high relevance given the rapid technological and digital evolution. In this sense, the benefits of its application are also discussed in literature. For Soudani [17] (p. 137), the main benefits of optimal use of an Accounting Information System in a company are linked to “better adaptation to a changing environment, better management of arm’s length transactions and a high degree of competitiveness”. Sari et al. [18] state that Accounting Information System should provide relevant information to reduce uncertainty in decision-making and promote better planning and control of business activities. Kamanga and Alexandra´s [1] study found that the adoption of Accounting Information Systems can be a critical step in the participation of township microenterprises in the formal and digital economy.

The benefits and difficulties that may face the implementation of a modern management accounting system were also discussed in Moustafa [19] article. Other articles focused on different case studies in the Accounting Information System application. In this context, Perez and Morote [20] analyzed an accounting evolution system in a San Julian Hospital, Brazil, and more recently, Huy and Phuc [21] analyzed the Accounting Information System with the application of Blockchain Technology to the public sector.

In addition to the implications of implementing an Accounting Information System, its construction has also been discussed in literature. Li [22] simulated a business Accounting Information System based on an enhanced neural network and a cloud computing platform. On the other hand, Shen and Han [23] studied the design optimization and analysis process of the profit calculation module of the financial Accounting Information System deployment based on particle swarm optimization.

To advance research in Accounting Information Systems, it is of particular importance to understand what has already been accomplished and what research is needed. In this study, we hope to link results to agency and contingency theories. Thus, based on a literature bibliometric review, research objectives are summarized as follows:

- Identify how many articles specifically focused on Accounting Information Systems have been published and how has been their evolution.

- Identify which journals, authors, countries/regions and organizations have more publications specifically focused on Accounting Information Systems, as well as the most frequent keywords.

- Identify which articles, sources, authors, organizations and countries/regions are the most cited.

- Explores the main research topics and trends in Accounting Information Systems.

- Explores the structural knowledge groups based on the co-citations network between articles, sources and authors.

This study follows Ezenwoke et al. [24] study who performed a bibliometric analysis on Accounting Information Systems based on Scopus database. Thus, we found that there is a gap in literature regarding the study of research conducted in WoS database and research trends in Accounting Information Systems. Furthermore, this study contributes to a more comprehensive understanding by including the analysis of all articles published in all journals indexed to the aforementioned database, adding additional knowledge to existing research.

This article is structured as follows. After introduction, Section 2 and Section 3 will present the theoretical framework, methodological procedures and results concerning the scientific production evolution within the scope of Accounting Information Systems. In the last section, conclusion and final considerations will be presented.

2. Theoretical Framework

For digital transformation to take hold in all communities, it is necessary to try to solve real-world issues [1]. Digital technology has changed the way we carry out our human activities, making it almost unthinkable for any business owners do not have access to some form of digital technology regardless of what part of the world they are or their business size [1]. According to Ezenwoke et al. [24] (p. 168), “the phenomenon ʻAccounting information Systemʼ, is wide and multidisciplinary in nature”.

Accounting Information Systems automates information produced by accounting. In fact, with the continuing advancement of technology, manual accounting systems are being replaced by digital Accounting Information Systems [1,24]. Therefore, improvements in information technology have facilitated financial accounting, as well as the use of cost and management accounting procedures [2]

Accounting Information System “collects and processes data which is measured in terms of money” [3] (p. 40). According to Neogy [3], this system “processes accounting transactions and provides information to interested users that are used to make effective decisions, to help management execute business activities correctly and finally to measure the performance of the company” (p. 40). However, it must be kept in mind that Accounting Information Systems effectiveness has significant implications for firm performance [5]. Soudani [17] study found that Accounting Information System is very useful and influenced the organizational performance of companies listed on Dubai financial market.

Sari et al. [18] (p. 188) state that “quality of Accounting Information System has implications for the quality of accounting information”. In this regard, literature in Accounting Information Systems is based on the concept of double-entry accounting, financial and management accounting. More recently, sustainable accounting is also included. “Accounting system is a recording process system such as a journal, ledger, worksheet, trial balance and procedures that are produced reliable and relevant information for preparing the financial statements and other accounting reports for the satisfaction of the different users to effective decision making” [3] (p. 40). For an Accounting Information System to be reliable it needs good documentation/reports to provide reliable and relevant information so that it is useful to all its users in performing and managing business activities [3]. The study by Puspitawati [4] found that accounting information quality is influenced by the good application of Accounting Information Systems and that company’s business strategy affects the effectiveness of accounting software. Monteiro et al. [8] found that the quality and consequent usefulness of financial reportings are directly impacted by the internal control system quality and the Accounting Information System quality.

In addition, Suzan et al. [5] concluded intellectual capital, operational risk management and business strategy have a significant positive effect on the Accounting Information System effectiveness. Accounting Information Systems are useful to a wide range of users because they provide information that supports all levels of management activity at the operational, middle and senior management levels [3]. Hence, the efficiency of Accounting Information Systems is essential because it ensures that all levels of management obtain sufficient, adequate, relevant and true information for planning and controlling the business organization activities [8]. In a business environment, which is affected by its entire external environment, there are numerous interests among stakeholders [15]. Thus, this study takes contingency and agency theories as its theoretical lens given the influence that external and internal environment can have on the firm. Regarding agency theory, there is a concern with a specific class of transactional relationships, those involving actors with partially conflicting interests that are potentially burdened by imperfect and/or asymmetric information [14]. In addition to possible internal conflicts, business environment can be affected by external factors. Thus, the implementation/efficiency of Accounting Information Systems can also be influenced by the companies, environment external [14]. Literature highlights the importance of internal and external factors for the company when assessing the implementation/quality of Accounting Information Systems. In addition, it also focuses on their antecedents and consequences.

Indeed, the accounting perspective is relevant to many issues in the Accounting Information Systems area. Recently, advances in this area focus on management decisions and control after the information system has been implemented [16].

Given the relevance that accounting has for the development of Accounting Information Systems, provide an overview of the state-of-the-art in research on Accounting Information Systems is necessary because, in prior studies, there is no consensus as to research areas to be included or excluded from Accounting Information Systems research. While there are previous studies that conduct a literature review on this research topic, they are specifically focused on: Scopus database and in a bibliometric technique to quantitatively analyze volume and impact of publications in the research domain, however, do not identify key research topics and trends [24], specific journals and limited to a period of time, from 1982 to 1998, [25] and from 1999 to 2009 [26], or in a single journal, whose scope is not only limited to Accounting Information System topic [13].

Poston and Grabski [25] (p. 9) verify that “the trend analysis is structured across underlying theory, research method and information systems lifecycle topics”. Fergusona and Seow´s [26] study, which continued to Poston and Grabski´s [25] work shows a continuing decline in analytical and model-building research in Accounting Information System research, which is associated with a similar decline in the use of computer science theory to motivate this research. Authors also find that two theoretical platforms, in particular, now account for almost half of all Accounting Information System research: cognitive psychology and economics. These authors identify the following main research topics: (1) organization and management of information systems (26 percent), internal control and auditing (21 percent), judgement and decision-making (19 percent), capital market (11 percent), and expert systems, artificial intelligence and decision aids (11 percent). In this work, authors also verify that the most research methods used are model building and experimental.

This research is focused on all articles published in journals indexed to WoS database, not yet researched. Taking into consideration that WoS includes the most authoritative and highest impact academic journals [8] this article uses WoS database and compares the results of previous Scopus-based study. In this way, it is possible to analyze the scientific production of Accounting Information Systems on a large scale. In addition to being essentially focused on a broader analysis of the scientific production on Accounting Information Systems, not being limited to certain journals or time.

3. Materials and Methods

Following previous studies [27,28,29], we conducted comprehensive research focused on Accounting Information Systems based on literature bibliometric review. Bibliometrics, “as a data analytic research methodology, comes from the library and information science” [30] (p. 6). Bibliometric analysis is used to capture quantitative data regarding publications, sources authors, organizations, keywords, topics and trends. In this study, the method was used to identify trends, impacts by use and topics in the research field (Accounting Information System). Additional statistics are performed to evaluate the scientific production (per year, source, authors, organizations and countries/regions) and its influence [13]. This methodology was deemed appropriate to gather the complex academic evidence available in WoS database to help analyze research topics and tell the story of the impact of Accounting Information Systems [30]. In this study, we used the four major bibliometric methods, citation, co-occurrence, bibliographic coupling and co-citation analyses. In these analyses, the relatedness of items is determined based on the number of times they cite each other (citation analysis, not counting self-citations), number of documents in which they occur together (co-occurrence analysis), number of references they share (bibliographic coupling) and number of times they are cited together (co-citation analysis).

The analysis of research trends considered the most recent publications and suggestions for future lines of research, as well as the most frequently used keywords in most recent studies.

To achieve this, a positivist research method and conceptual framework [31] was used, the approach applied was numerical, descriptive and exploratory, allowing a longitudinal description of the methodology academic use, focusing on the qualities of publications and public metrics. The basic assumptions underlying this philosophical position of applying positivist lens to the study of Accounting Information Systems start from a broad commitment to the idea that social sciences should “emulate” themselves with natural sciences [32]. Ontologically, with positivist research authors position an objective physical and social world that exists independently of human beings, and whose nature can be grasped in a relatively unproblematic, characterized and measured way” ([33], p. 9). Thus, the focus of positivist research is to discover objective reality by devising measures that detect the dimensions of reality that interest the researcher [34].

Data was collected from WoS database because there are no bibliometric studies on this topic in existing literature. In addition, this WoS database “includes the most authoritative and high-impact academic journals [8,30] (p. 4). The VOSviewer program, version 1.5.15, was used for this analysis.

In this research, we followed Ezenwoke et al. [24] study, who used Scopus database to compare results, although in the results comparison there is the need to keep in mind that different databases lead to different impacts in terms of citation, co-occurrence, bibliographic coupling and co-citation.

In this study, we followed the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) [30].

First, we identify the database. The sampling was limited to one database (WoS) to avoid double inclusion of documents with different metadata and differences in citation methodology [34]. Different citation sources lead to a different number of citations and the WoS Core Collection includes only high-quality indexed journals [35]. Second, we sought to identify keywords to use in the database to select articles focused on the research topic. After exhaustive research to identify keywords to use in the search for articles focused on the research topic, we found that the single use of the password “Accounting Information System*” is enough, which is in line with the criterion used by Ezenwoke et al. [24].

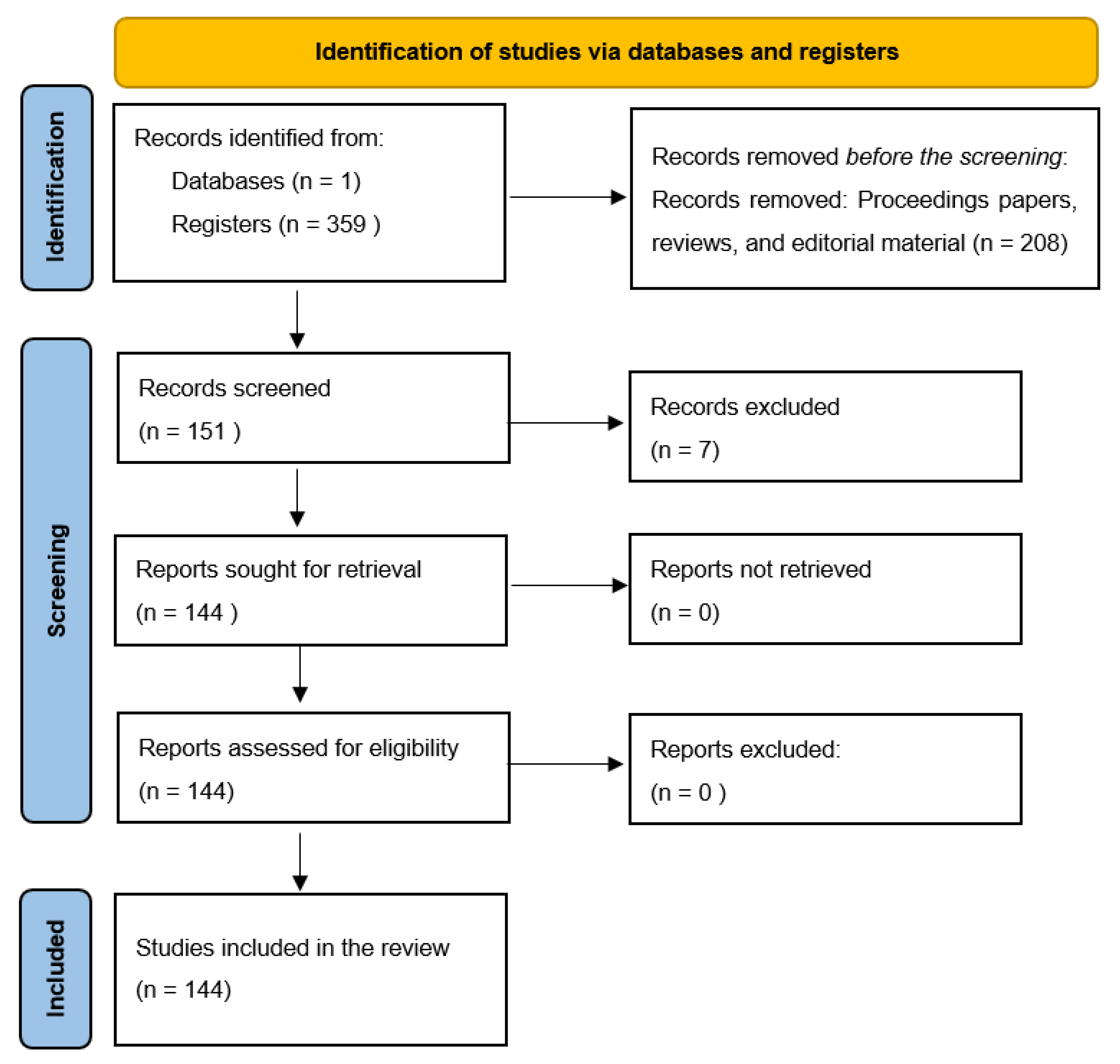

The search query used is framed thus: TITLE-ABS-KEY (“Accounting Information System*”). From the search 359 publications were generated, 151 articles, 204 proceedings papers, 3 reviews, 6 early access and 1 editorial material. Proceedings papers, reviews and editorial material were excluded (n = 208).

After reviewing all articles, only those articles where the study objective focuses on development of Accounting Information Systems were selected. The final sample comprises 144 articles selected on 15 May 2021, from WoS database. The study includes all articles published up to the date of collection. Figure 1 presents the sample process selection (PRISMA).

4. Results

4.1. Scientific Production on Accounting Information Systems

Objective 1: How many articles specifically focused on Accounting Information Systems have been published and how has been their evolution?

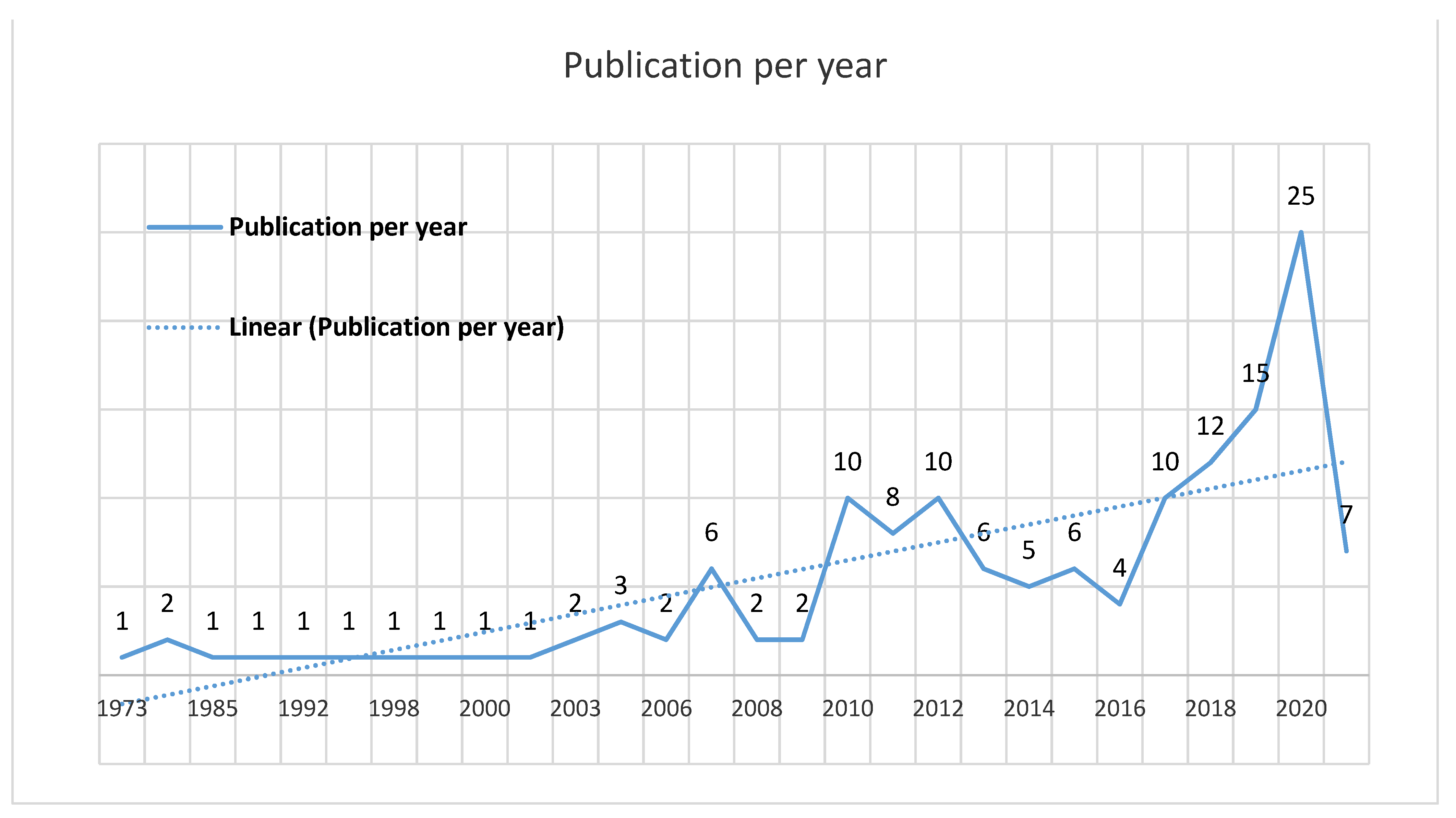

As we can see in Figure 2, the first article published in this area in WoS database was in 1973 by Marshall titled “Determining an optimal Accounting Information System for an unidentified user”. The study´s objective was to formulate a decision model for the problem of determining an optimal system in training for an unidentified user and specify conditions that must be satisfied for an optimal system to exist [36].

This research topic has been gaining space in researchers, however, until 2010 there was only an average of 1 article published per year on Accounting Information Systems. Since 2010 there has been a growing trend, with 2020 standing out as the year with fewest publications, and it is expected that 2021 equal or surpass 2020.

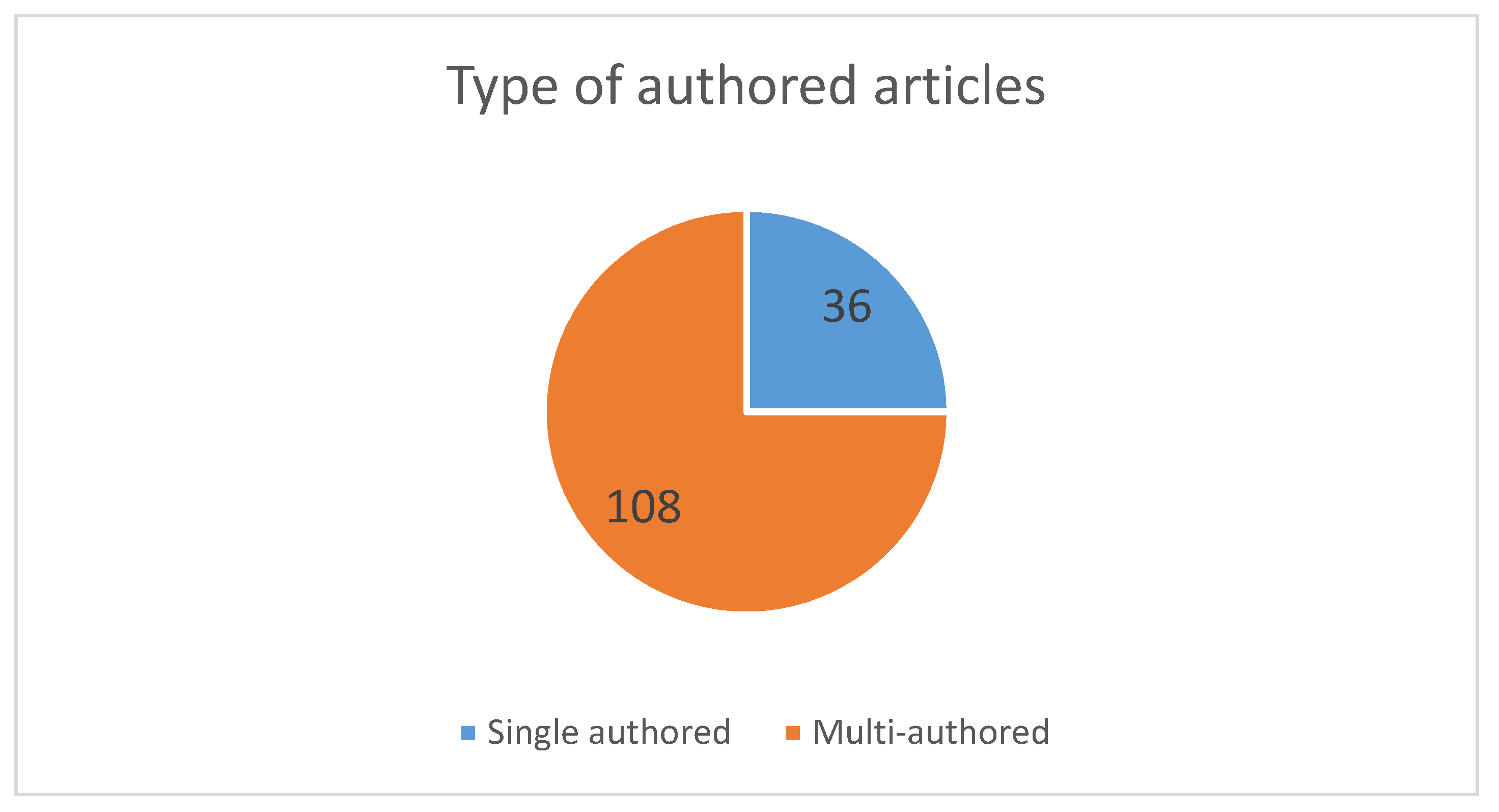

In addition, we verify that, of the 144 publications, only 25% (36) were produced by one author, 75% (108) were multi-authored. Figure 3 presents the single and multi-authored publications.

Objective 2: Which journals, authors, countries/regions and organizations have more publications specifically focused on Accounting Information Systems, as well as the most frequent keywords?

In a total of 109 journals and according to Table 1, the “Journal of Asian Finance Economics and Business” is the journal with more publications in the time period under study (6 publications), followed by the “International Journal of Accounting Information Systems”, with 5 publications, “Journal of Information Systems”, with 4 and “Global Business Review”, “Management Theory and Studies for Rural Business and Infrastructure” and “Pertanika Journal of Social Science and Humanities”, with 3 each. Other journals only have 2 or 1 publication in the timeline under study. Table 1 presents the journals with 2 or more publications, as well as its 2019 impact factor.

For the calculation of h-index, the study sample of 144 articles on the subject of “accounting information systems” and the time base of 1973 to 15 May 2021, were considered. With a total of 322 authors, authors with more than two publications in the timeline under study are Povilas Domeika, Ilham Hidayah Napitupulu, Carmela Rizza, Daniela Ruggeri are the authors with more publications (3). The other 7 authors have published 2 articles. Table 2 shows the publication per author.

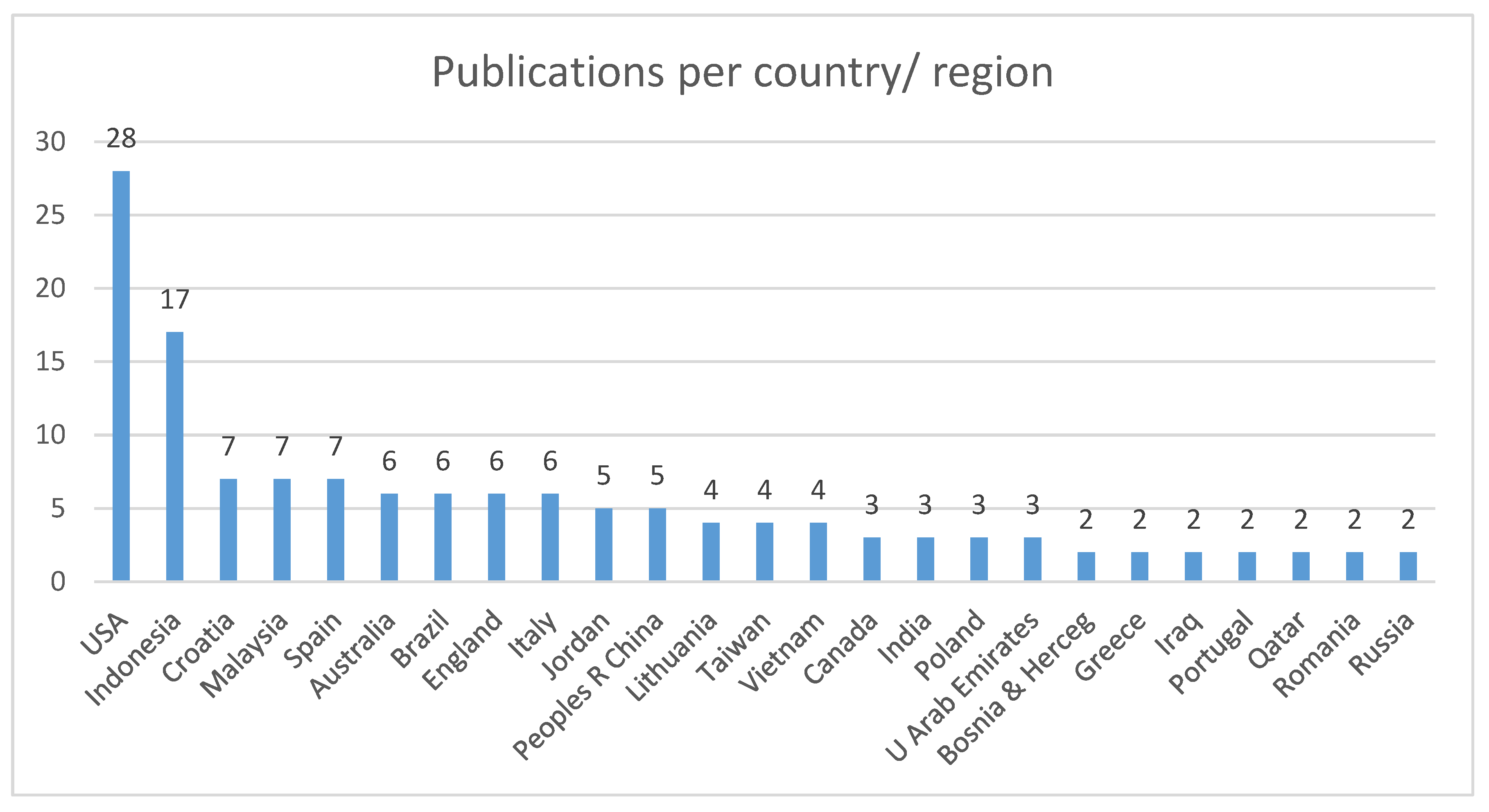

Figure 4 shows the countries/regions with more than 2 publications in the timeline under study. In a total of 57 countries/regions with publications on Accounting Information Systems, the United States of America (USA) is the region with most publications in the area, with 28 publications. The second most published country is Indonesia, with 17 publications, following Croatia, Malaysia and Spain with 7 and Australia, Brazil, England and Italy with 6. All other countries have less than 5 publications to date this research.

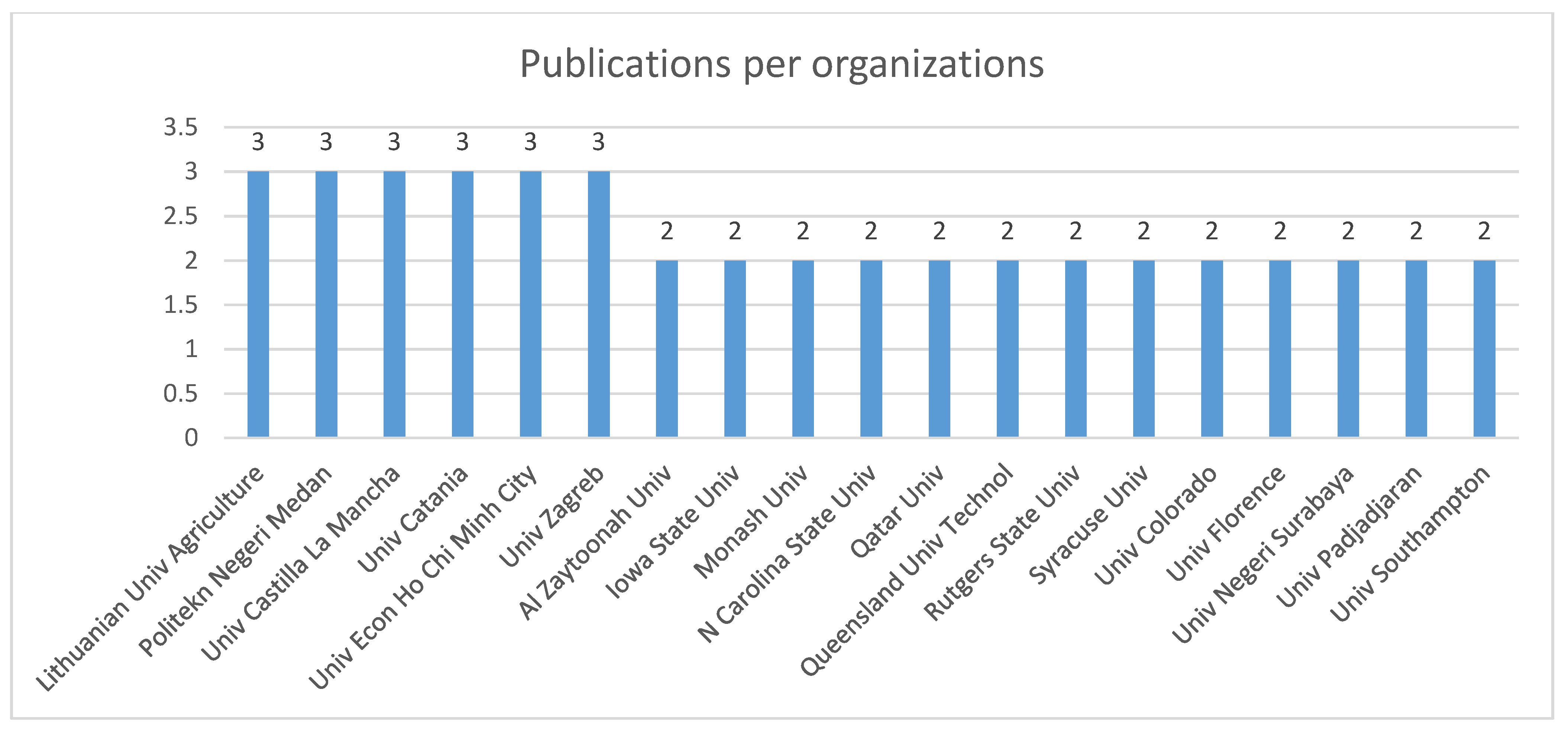

In a total of 213 organizations with publications on Accounting Information Systems, Lithuanian University of Agriculture, Politekn Negeri Medan, University Castilla La Mancha, University of Catania, University of Economics Ho Chi Minh City and University Zagreb stand out with 3 publications in timeline under study. This is followed by another 13 organizations with 2 publications as shown in Figure 5.

The remaining 194 organizations have only published one article in the Accounting Information Systems area.

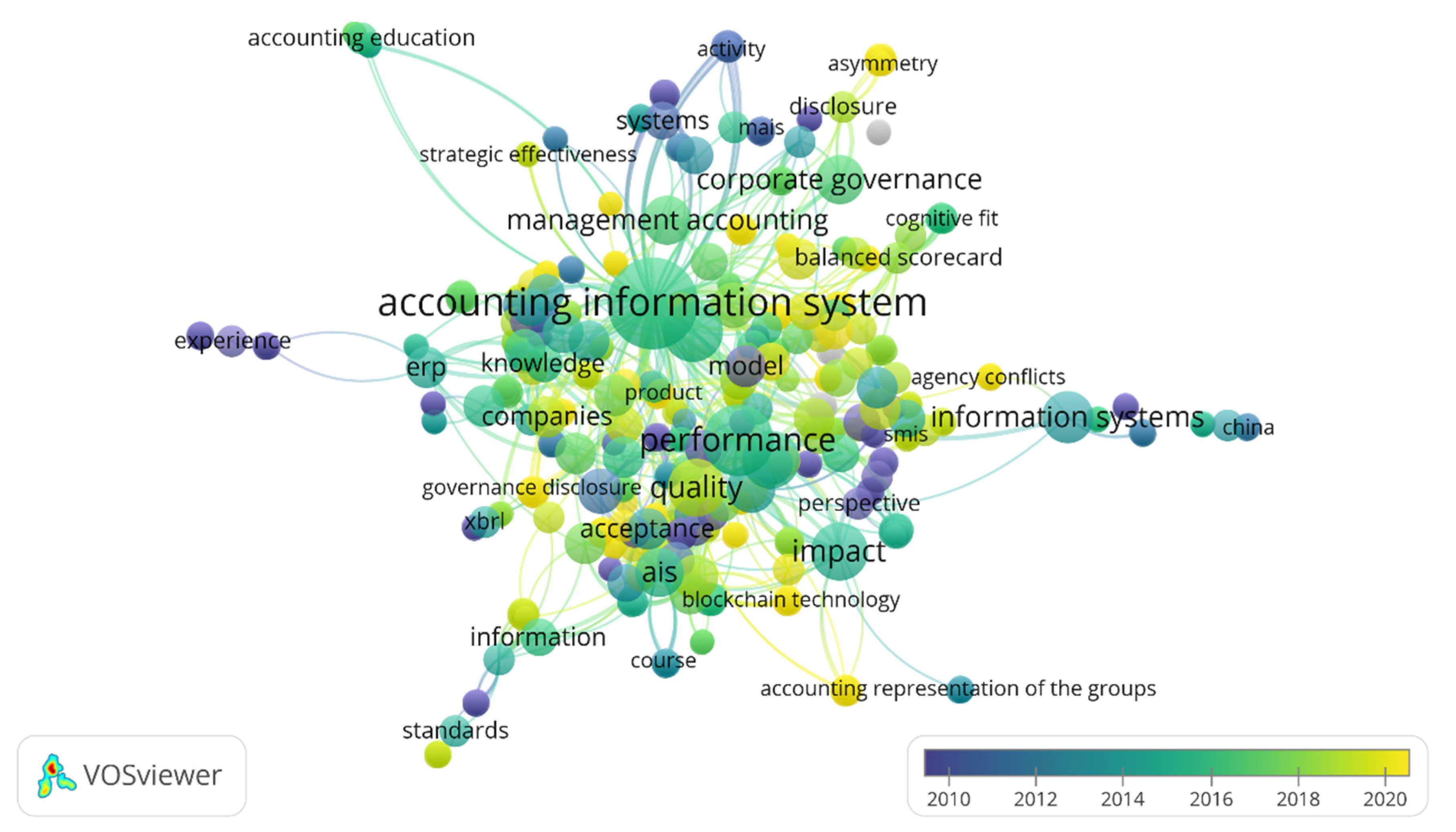

After analyzing the total keyword occurrence, we conclude that the most used keywords were “Accounting Information Systems”, Performance”, “Management Accounting” and “Information System”, as shown in Figure 6. These keywords meet the research topics, representing research trends in the field of Accounting Information Systems.

In the last few years, the most used words have been “Balanced Scorecard”, “Asymmetry”, “Accounting”, “blockchain technology” and “Governance disclosure”.

4.2. Most Cited Publications, Sources, Authors, Organizations and Countries/Regions

Objective 3: Which articles, sources, authors, organizations and countries/regions are the most cited?

With a total of 144 articles, the article with highest number of citations, with a total of 168, belongs to Pacini et al. [36]. In this paper, authors measured the environmental performance of farming systems through the application of an Accounting Information System.

The second most cited article, with 61 citations, belongs to Córcoles et al. [37]. This article demonstrates the need for universities to include information on intellectual capital in their Accounting Information Systems.

In third place, with 47 citations, is Brazel and Agoglia [38] article. Authors study investigated the quality effects of work provided by both computer assurance specialists and the expertise of Accounting Information Systems auditor on auditors’ planning judgments in a complex Accounting Information Systems environment.

In fifth place is Choe’s [39] article, with 39 citations. The author, by surveying companies through a structured questionnaire, investigated the interactions between contextual variables (task uncertainty and organizational structure), information characteristics (scope, timeliness and aggregation) and participation of users in designing the Management Accounting Information System.

In sixth place is Chen’s [40] study, with 34 citations. The author by developing an adapted web-based learning system proposes a design model for system designers to adapt the preferences linked to each cognitive style.

Masanet-Llodra’s [41] work is in seventh place with 33 citations. The article conducts an in-depth study on environmental management systems developed in the ceramics sector. With one citation less (32) is Eldenburg et al. [42] article. This study, also geared towards management accounting, the research examines physicians’ response to the implementation of an activity-based costing (ABC) system developed and designed with input from physicians.

The publications identified above have more than 30 citations The remaining articles have less than 30. Table 3 shows the articles with more than 10 citations.

According to Table 4, the most cited authors are Giesen, G; Huirne, R; Pacini, C; Vazzana, C and Wossink, A, with 168 citations. These authors belong to the most cited article entitled “Evaluation of sustainability of organic, integrated and conventional farming systems: a farm and field-scale analysis” [36]. The most cited journal is “Agriculture Ecosystems & Environment”. The most cited organization is North Carolina State University, with 215 citations. The most cited region, also with the most publications in the area, is the USA, with 379 citations.

4.3. Research Topics and Trend

Objective 4: Which are the main research topics and trends in Accounting Information Systems?

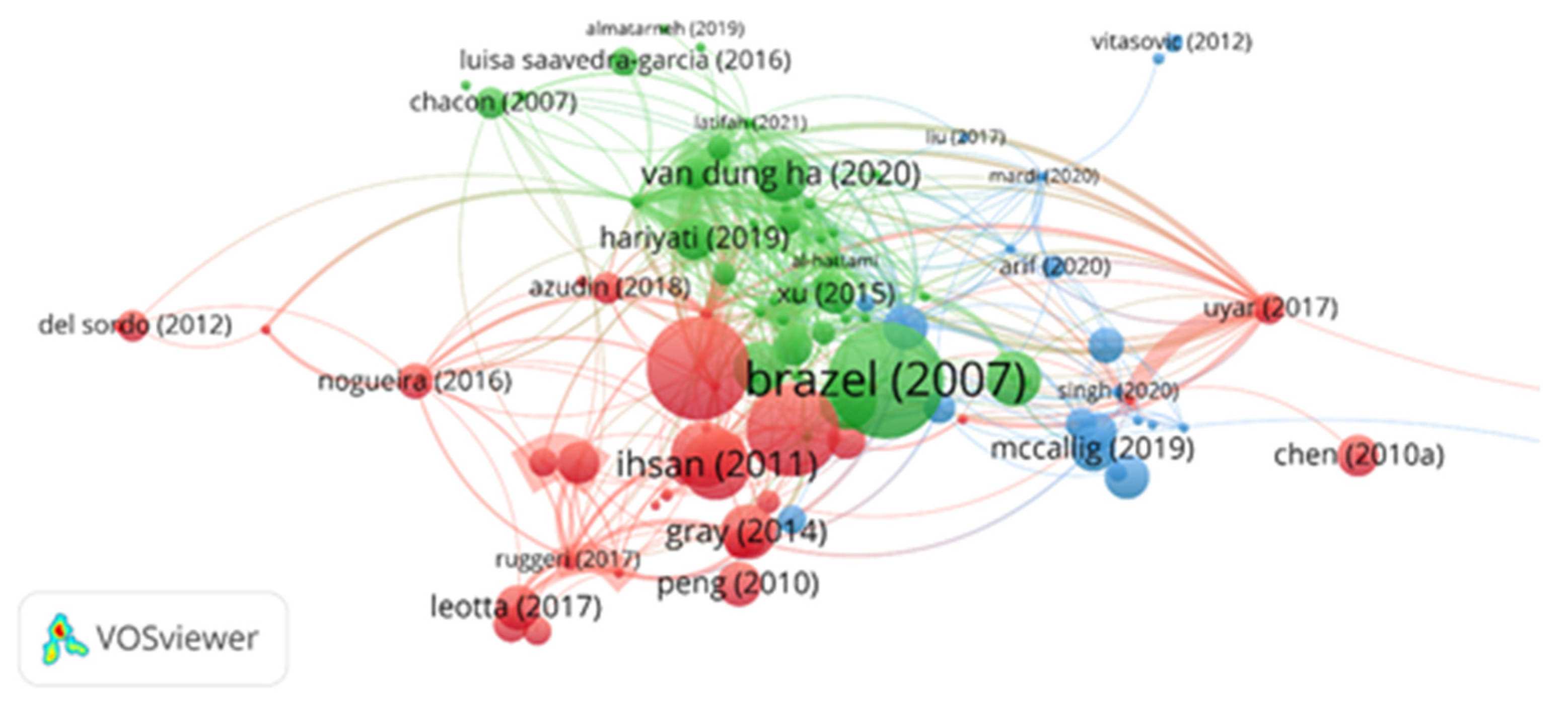

In the total of 144 articles, the software eliminated 35 articles because they had no link strength with the others. Form the 109 articles with more link strength, 44 are part of the first cluster (red), 41 are part of the second cluster (green) and 24 are part of the third cluster (blue). After bibliographic coupling through VOSviewer it was possible to verify 3 research topics, each topic with a different color represents a cluster and the lines represent the link strength between them as shown in Figure 7.

We have identified that the main research topic will be in “research, behavior/experience/system requirements and trust relationship” (cluster red representing 40% of the total articles) and “the importance of organizational culture and management accounting and the effects for auditors, accountants, managers (decision-making), entities and countries” (cluster green representing 38% of the total articles) and “the importance of the internal control and the effects for the quality of financial information, skills development and business ethics” (cluster blue representing 22% of the total articles).

Table 5, Table 6 and Table 7 show the top 10 articles by topic. For each article, we present the title, journal, methodology, study objective, total citations and total link strength that indicates the number of publications in which two keywords occur together.

Regarding Cluster red - Research, behaviour/experience/system requirements and trust relationship, we find that this cluster includes studies focused on the investigation on Accounting Information Systems. Moreover, the interactions between contextual variables and information characteristics are critical to the development of accounting information system [43].

This development, when successfully implemented in different types of companies, tends to generate improved financial performance [15,42]. Thus, literature shows that the implementation of accounting information systems, such as the “ABC” example, results in more efficient management and greater transparency and accountability [42,44]. The behaviour and experience of users, both individually and collectively, become critical to the successful implementation of accounting information system [45]. This cluster also includes studies focused on the potential of accounting information systems to contribute to trusting relationships between the parties involved. Table 5 shows the TOP 10 publications in this cluster.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 5.

Top 10 articles on subtopic research, behaviour/experience/system requirements and trust relationship.

Table 5.

Top 10 articles on subtopic research, behaviour/experience/system requirements and trust relationship.

| RO | Author/s (Year) | Title | Journal | Methodology | Objective | TLS |

|---|---|---|---|---|---|---|

| 1 | Choe (1998) [39] | The effects of user participation on the design of accounting information systems | Information & Management | Quantitative | This study investigated the interactions between contextual variables (task uncertainty and organizational structure), information characteristics (scope, timeliness and aggregation) and UP | 32 |

| 2 | Eldenburg, Soderstrom, Willis and Wu (2010) [42] | Behavioral changes following the collaborative development of an accounting information system | Accounting, Organizations and Society | Quantitative | Authors contribute to research on the influence of user participation on accounting system success, ABC system success and hospital accounting information systems. | 17 |

| 3 | Ihsan, SHHM Ibrahim–Humanomics (2011) [44] | WAQF accounting and management in Indonesian WAQF institutions: The cases of two WAQF foundations | Humanomics | Quantitative and qualitative | The purpose of this study is to examine accounting and management practices in two Indonesian WAQF institutions. It intends to seek evidence about how mutawallis discharge their accountability. | 1 |

| 4 | Hunton and Gibson (1999) [45] | Soliciting user-input during the development of an accounting information system: investigating the efficacy of group discussion | Accounting, Organizations and Society | Quantitative | This study reports the results of a longitudinal field experiment designed to examine the impact of group discussion when soliciting user requirements of an accounting information system | 22 |

| 5 | Gray, Chiu, Liu and Li (2014) [46] | The expert systems life cycle in AIS research: What does it mean for future AIS research? | International Journal of Accounting Information Systems | Quantitative | This paper explores the life cycle of expert systems research by accounting researchers in order to provide an overview of the role of accounting researchers in technology domains. | 6 |

| 6 | Woodward and Woodward (2001) [47] | The Efficacy of Action at a Distance as a Control Mechanism in the Construction Industry When a Trust Relationship Breaks Down: an Illustrative Case Study | British Journal of Management | Qualitative | A paper published by one of the authors (Woodward and Squires, 1996), described a situation where the accounting information system used by a geographically distant project manager to report the progress of a project to his headquarters proved inadequate for that task. The purpose of this paper is to analyze previously reported situation in the context of a perceived breakdown in the existing trust relationship between the project manager and his superior, the company’s general manager. | 39 |

| 7 | Mahama, Elbashir, Suttonc and Arnoldc (2016) [43] | A further interpretation of the relational agency of information systems: A research note | International Journal of Accounting Information Systems | Quantitative | This paper proposes a reinterpretation of the agency of information system as relational. | 27 |

| 8 | Lehman and Heagy (2008) [48] | Effects of Professional Experience and Group Interaction on Information Requested in Analyzing IT Cases | Journal of Education for Business | Quantitative | Authors investigated the effects of professional experience and group interaction on the information that information technology professionals and graduate accounting information system (AIS) students request when analyzing business cases related to information systems design and implementation. | 1 |

| 9 | Kostić, Jovanović and, Jurić, (2019) [49] | Cost Management at Higher Education Institutions–Cases of Bosnia and Herzegovina, Croatia and Slovenia | Central European Public Administration Review | Quantitative | The main aim of this paper is to overview the legal and organizational accounting systems’ characteristics focusing on external and internal reporting requirements and study the level of development and usage of cost accounting at HEIs in selected countries. | 2 |

| 10 | Kopel, Riegler, and Schneider, G (2020) [50] | Providing Managerial Accounting Information in the Presence of a Supplier | European Accounting Review | Quantitative | This paper identifies a novel effect which is crucial for the design of a management accounting information system. | 1 |

Legend: RO–Ranking Order; TLS –Total Link Strength. Source: VOSviewer.

Table 6.

Top 10 articles on subtopic importance of organizational culture and management accounting and the effects for auditor accountants, managers, entities and countries.

Table 6.

Top 10 articles on subtopic importance of organizational culture and management accounting and the effects for auditor accountants, managers, entities and countries.

| RO | Author/s (Year) | Title | Journal | Methodology | Objective | TLS |

|---|---|---|---|---|---|---|

| 1 | Brazel and Agoglia (2007) [38] | An Examination of Auditor Planning Judgements in a Complex Accounting Information System Environment | Contemporary Accounting Research | Quantitative | The study investigates the effects of computer insurance specialist (CAS) and accounting information systems auditor (AIS) competence on auditor planning judgements in a complex AIS environment. | 8 |

| 2 | Chen, Huang, Chiu and Pai (2012) [40] | The ERP system impact on the role of accountants | Industrial Management & Data Systems | Quantitative | The purpose of this paper is to discuss the impact of an Enterprise Resources Planning (ERP) system on the role of accountants, to provide job qualifications for their reference. | 0 |

| 3 | Tarek, Mohamed and Hussain (2017) [51] | The implication of information technology on the audit profession in developing country: Extent of use and perceived importance | International Journal of Accounting & Information Management | Both quantitative and qualitative | This study aims to explore the impact of implementing Information Technologies on auditing profession in a developing country, namely, Egypt | 12 |

| 4 | Alewine, Allport and Shen (2016) [52] | How measurement framing and accounting information system evaluation mode influence environmental performance judgements | International Journal of Accounting Information Systems | Quantitative | This study introduces attribute framing to the General Evaluability Theory framework as important to consider when analyzing environmental decision differences across modes, because frames are often a necessary component of information presentation and different descriptions often lead to different decisions | 22 |

| 5 | Dobroszek, Zarzycka, Almasan and Circa (2019) [53] | Managers’ perception of the management accounting information system in transition countries | Economic Research-Ekonomska Istraživanja | Quantitative | This study aims to investigate managers perception from transition countries, as regards the management accounting information system. | 17 |

| 6 | Khadra, Al-Hayale and Al-Nasir (2012) [54] | Contingent Effects of System Development Life Cycle Critical Success Factors on Accounting Information System Effectiveness: Using Balance Scorecard Perspectives—Empirical Study Applied on the Jordanian Industrial Companies | International Journal of Information Technology Project Management | Quantitative | This study aims to explore the critical success factors that affect accounting information systems development fitness in Jordanian industrial companies. | 20 |

| 7 | Al-Hattami (2021) [55] | Validation of the D&M IS success model in the context of accounting information system of the banking sector in the least developed countries | Journal of Management Control | Quantitative | This study aims to validate D&M IS success model (for the first time) in the context of accounting information system (AIS) of the banking sector in the least developed countries, in this case Yemen. | 74 |

| 8 | Al-Dmour, Abood and Al-Dmour (2019) [56] | The implementation of SysTrust principles and criteria for assuring reliability of AIS: empirical study | International Journal of Accounting & Information Management | Quantitative | This study aims at investigating the extent of SysTrust’s framework (principles and criteria) as an internal control approach for assuring the reliability of Accounting Information System (AIS) were being implemented in Jordanian business organizations. | 19 |

| 9 | Alamin, Wilkin, Yeoh and Warren (2020) [57] | The Impact of Self-Efficacy on Accountants’ Behavioral Intention to Adopt and Use Accounting Information Systems | Journal of Information Systems | Quantitative | The study of Libyan accountants shows that in adopting a mandated technologically enabled accounting information system, they were influenced by a range of perceptional, dispositional and environmental factors. | 15 |

| 10 | HA (2020) [58] | Impact of Organizational Culture on the Accounting Information System and Operational Performance of Small and Medium-Sized Enterprises in Ho Chi Minh City | Journal of Asian Finance, Economics, and Business | Both qualitative and quantitative | This study focuses on determining the impacts of organizational culture on accounting information system and operational performance of small and medium-sized enterprises in Ho Chi Minh City. | 7 |

Legend: RO–Ranking Order; TLS –Total Link Strength. Source: VOSviewer.

Regarding the Cluster green–the importance of organizational culture and management accounting and the effects for auditors, accountants, managers, entities and countries. Information technology applications, such as enterprise resource planning (ERP) systems, are significantly changing the ways companies operate their businesses and auditors perform their duties [38,51]. The implementation and use of accounting information systems can increase audit-related risks and therefore auditors must keep up with technological developments and expand their knowledge and competence [38,51]. In addition to auditors, accountants must also keep up with evolving technology for the proper pursuit of accounting activities in new contexts [40]. The role of accountants in society thus becomes even more demanding [40]. Considering that organizational culture influences company’s performance, the role of information makers and the role of decision-makers (managers) is of utmost importance for the implementation of accounting information systems [52]. The accounting information system is an important source of information for management and decision making. This type of information is provided by accountants and used by managers operating in different organizations and economies [53]. Table 6 shows the TOP 10 publications in this cluster.

The third cluster is Cluster blue-the importance of internal control and effects on the quality of financial information, skills development and business ethics.

Stakeholders, as technology evolves, tend to demand more information [59]. Accounting information systems capture and process accounting data and provide valuable information to all stakeholders [60]. However, in a rapidly changing environment, continuous information system management is necessary for organizations to optimize performance results [60]. For good performance, the quality of accounting information is enhanced because the information in this system can be used by stakeholders who need credible information about the entity [61]. The effect of the accounting information system implementation is thus influenced by the internal control system, and the competence of human resources on the quality of financial statements [62]. Table 7 shows the TOP 10 publications in this cluster.

The presentation of the obtained clusters allows us to verify that both internal and external factors affect the accounting information system. Thus, theories of agency and contingency are of high importance because they interfere with the implementation of accounting information systems quality [63]. When the implementation is successful, it has a significant impact on improving the organization or company performance [5]. However, to achieve successful decision-making, accounting information must be of high quality, relevant and useful in the decision-making process [6]. Thus, factors external to firms, their organizational culture, internal control and the role of managers, accountants and auditors are factors that condition the accounting information system.

The company external and internal environment is contingent on the proper application of the accounting information system, so it is necessary to take into account the different interests of different agents.

Furthermore, we found that the methodology used in most studies is quantitative.

Considering the most recent publications, suggestions for future investigation and most recently used keywords, we identified the following research trends: (1) the impact of Accounting Information System in organizations (performance, innovation, reorganization of activities, information reporting); (2) the Accounting Information System Construction, (3) the importance of implementation of the Accounting Information System in small and medium-sized enterprises and Public-Sector; and (4) the factors that contribute to Accounting Information System efficiency/quality.

On one hand, literature has highlighted the enhancement of firms’ performance with the implementation of this information system [40,41] however, its construction has been the subject of numerous debates in literature given the improvements in business environment [19,20]. Thus, the topic of Accounting Information System construction will always keep pace with the evolution of technology and the constant developments in the information system [19].

In this context, our analysis points out as future research the topics Accounting Information System and organization performance and Accounting Information System Construction.

Table 7.

Top 10 articles on the internal control importance and effects on the quality of financial information, skills development and business ethics.

Table 7.

Top 10 articles on the internal control importance and effects on the quality of financial information, skills development and business ethics.

| RO | Author/s (Year) | Title | Journal | Methodology | Objective | TLS |

|---|---|---|---|---|---|---|

| 1 | Córcoles, Penalver and Ponce (2011) [37] | Intellectual capital in Spanish public universities: stakeholders’ information needs | Journal of Intellectual Capital | Qualitative | This paper aims to demonstrate the need for universities to include information on intellectual capital in their accounting information system. | 27 |

| 2 | Córcoles, Peñalver and Ponce (2012) [59] | Demanda de información sobre capital intelectual en las Universidades públicas españolas | Cuadernos de Gestión | Qualitative | This paper objective will be to demonstrate the need for universities to incorporate information on intellectual capital in their current accounting information system. | 28 |

| 3 | Prasad and Green (2015) [60] | Organizational Competencies and Dynamic Accounting Information System Capability: Impact on AIS Processes and Firm Performance | Journal of Information Systems | Quantitative | Using the dynamic capabilities framework (Teece 2007) it proposes that a dynamic AIS capability can be developed through the synergy of three competencies: having (1) a flexible AIS, (2) a complementary business intelligence system and (3) accounting professionals with IT technical competency. | 55 |

| 4 | McCallig, Robb and Rohde (2019) [7] | Establishing the representational faithfulness of financial accounting information using multiparty security, network analysis and a blockchain | International Journal of Accounting Information Systems | Quantitative | This paper aims to develop a design for an accounting information system that will enhance the representational faithfulness of financial reporting information. | 19 |

| 5 | Tan and Low (2019) [61] | Blockchain as the Database Engine in the Accounting System | Australian Accounting Review | Quantitative | This paper examines the prediction that blockchain technology will transform accounting and the profession because transactions recorded on a blockchain can be aggregated into financial statements and confirmed as true and accurate. | 3 |

| 6 | Sumaryati, Novitasari and Machmuddah (2020) [63] | Accounting Information System, Internal Control System, Human Resource Competency and Quality of Local Government Financial Statements in Indonesia | The Journal of Asian Finance, Economics, and Business | Quantitative | This study seeks to determine the effect of the application of accounting information system (AIS), internal control system and human resource (HR) competency on the quality of local government financial statements (FS). | 10 |

| 7 | Janvrin, Payne and Byrnes (2012) [62] | The Updated COSO Internal Control—Integrated Framework: Recommendations and Opportunities for Future Research | Journal of Information Systems | Qualitative | Authors review the updated Framework and discuss the comments we (as the Environmental Scanning Committee of the American Accounting Association’s Information Systems Section) offered COSO regarding how to improve the Framework. In addition, we identify research opportunities for accounting information system scholars related to the new Framework. | 12 |

| 8 | Burney, Radtke and Widener(2017) [64] | The Intersection of “Bad Apples,” “Bad Barrels,” and the Enabling Use of Performance Measurement Systems | Journal of Information Systems | Quantitative | The purpose of this study is to examine the intersection of AIS and business ethics by focusing on how a specific type of AIS is used; namely, the Performance Measurement Systems | 3 |

| 9 | Arif, Yucha, Setiawan, Oktarina andMuttaqiin (2020) [65] | Applications of Goods Mutation Control Form in Accounting Information System: A Case Study in Sumber Indah Perkasa Manufacturing, Indonesia | The Journal of Asian Finance, Economics and Business | Quantitative | This study analyzes the new GMCF method applied by the company to find out how the production of Accounting Information Systems (AIS) implemented by the company can be managed properly. | 5 |

| 10 | Alawaqleh (2021) [66] | The Effect of Internal Control on Employee Performance of Small and Medium-Sized Enterprises in Jordan: The Role of Accounting Information System | The Journal of Asian Finance, Economics and Business | Quantitative | This study explores the role of the Accounting Information System (AIS) in mediating the relationship between internal control and the performance of employees. | 15 |

Legend: RO–Ranking Order; TLS—Total Link Strength. Source: VOSviewer.

4.4. Structural Knowledge Groups

Objective 5: Which structural knowledge groups can be identified based on the co-citations network between articles, sources and authors?

In a total of 5821 references, Claes Fornell and David F. Larcker study titled “Evaluating Structural Equation Models with Unobservable Variables and Measurement Error” was the most co-cited with a total of 10 citations and 38 from Total link strength that indicates the number of publications in which two keywords occur together. Fornell, C.; Larcker’s [67] study examines the statistical tests used in the analysis of structural equation models with unobservable variables and measurement error. This indicates that studies in this area of research use the Structural Equation Model technique to analyze the unobserved statistical correlation variable.

The second place with 9 citations belongs to Otley [68] study. Otley [68] addressed contingency theories of management accounting by surveying the development and content of these theories. In this way, they presented an improved model, based on ideas of organizational control and effectiveness, which suggests appropriate directions for future work that will be both perceptive and cumulative.

In third place with 8 citations is DeLone and LcLean’s [69] study. Their study identified 43 specific variables posed to influence different dimensions of IS success and organized these success factors into five categories based on the Leavitt Diamond of Organizational Change: task characteristics, user characteristics, social characteristics, project characteristics and organizational characteristics. Table 8 presents the TOP 10 most co-cited references ordered by total citations.

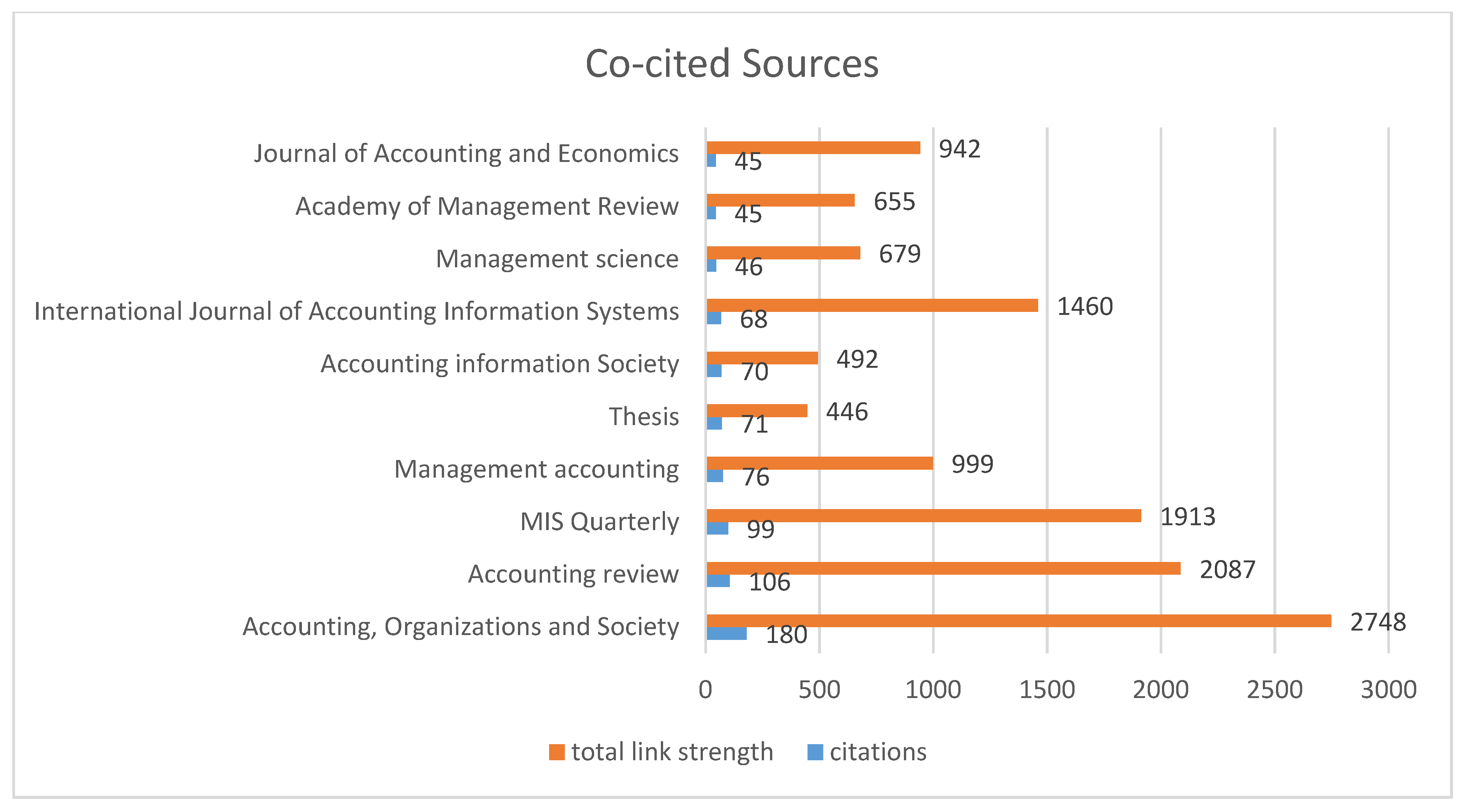

Out of a total of 3034 co-cited journals, the journal that stands out the most is Accounting Organizations and Society with 180 citations and 2748 Total link strength that indicates the number of publications in which two keywords occur together. Figure 8 represents the most co-cited journals.

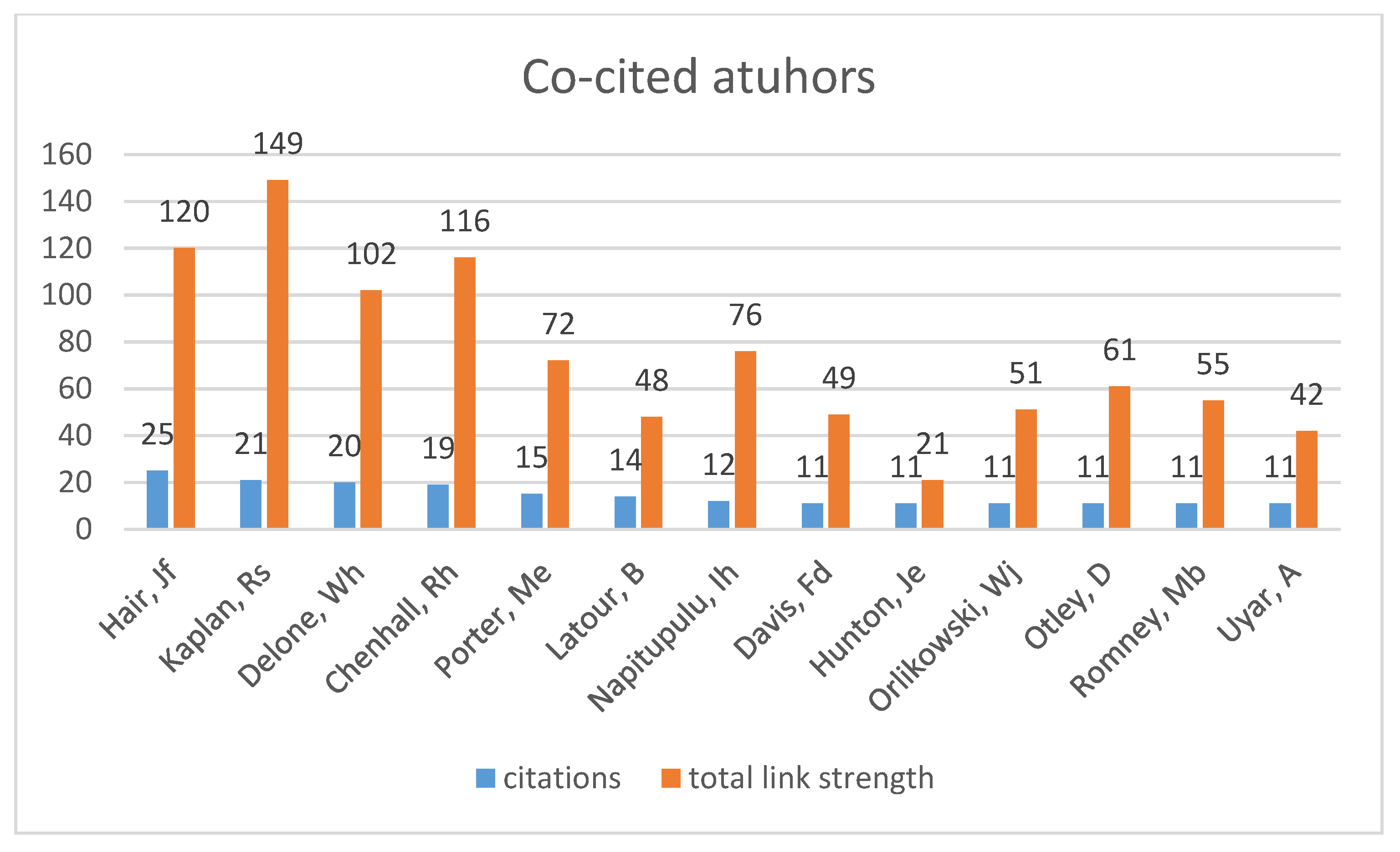

Finally, out of a total of 4575 co-cited authors Hair, JF stands out with 25 citations and 120 Total link strength who indicates the number of publications in which two keywords occur together. Figure 9 highlights the most co-cited authors.

5. Discussion and Concluding Remarks

Digital technology has revolutionized the daily lives of us all. Advances in information technology make accounting increasingly dependent on Accounting Information Systems. This transformation leads to more digital accounting, faster processes and more accurate information.

Accounting information is essential for managers to forecast and define the company’s strategic objectives in the future, as well as to make decisions that will lead them to success. Accounting Information Systems purpose “is to collect, store and process financial and accounting data and produce informational reports that managers or other interested parties can use to make business decisions” [70]. However, the Accounting Information System implementation will have a significant and positive impact on accounting information quality and consequently on business performance.

In this recent theme, literature has tried to respond to the problems that Accounting Information System presents, however, literature presents the difficulty that stakeholders may have in establishing whether financial information represents what it refers to due to information asymmetries and agency problems. Literature also shows that on the topic of information systems in general, emerging technologies in accounting and the application of technologies to business assurance and disclosure have been of much interest to researchers [13].

Thus, this study focuses on the contingency and agency theories, as Accounting Information Systems are dependent on contingent factors, such as rapidly evolving technologies and digitization, as well as the effects of Accounting Information Systems will depend on the interests of different actors (managers-owners/shareholders). In this sense, the benefits of its application are also discussed in literature.

Through the analysis of rigorous bibliometric tools, this research reveals the influential authors, top journals and top contributing organizations and countries in the Accounting Information Systems domain. In addition, research topics and trends were identified.

Results show that the first article published in this area in WoS was in 1973 by Marshall and that this topic has been gaining space in researchers, however, until 2010, there was only an average of 1 article published per year on Accounting Information Systems. Since 2010, there has been an increasing trend, with 2020 standing out as the year with fewest publications and 2021 is expected to surpass 2020. Ezenwoke [24], using Scopus database, found the first articles in 1975 and that last year, scientific production increased significantly in the area of research.

Results also show that the author, journal, organization and region with most publications are Rizza Camela, Journal of Asian Finance, Economics and Business, University of Economics Ho Chi Minh City and the USA. Ezenwoke [24] identifies Susanto, A as the author with more publication, the journal International Journal of Accounting Information Systems, the organization Universitas Padjadjaran, Indonesia. Similarly, the region with most publications is the USA.

In addition, we found that in a total of 144 articles the most used keywords were “Accounting Information Systems”, “Performance”, “Management Accounting” and Information System. Ezenwoke’s [24] study shown the keywords group most used were Audit and Control; Information Systems; Decision Management and Accounting Education.

Regarding research topics, we found that the most addressed themes were: (1) “research, behavior/experience/system requirements and trust relationship”; (2) “the importance of organizational culture and management accounting and the effects for auditors, accountants, managers (decision-making), entities and countries”; and (3) “the importance of the internal control and the effects for the quality of financial information, skills development and business ethics”. Regarding Poston and Grabski’s [25] work, the research topics were, (1) organization and management of information systems, internal control and auditing, judgment and decision-making, capital market and expert systems, artificial intelligence and decision aids.

At the level of future research lines, we identified the research trends in research: (1) the impact of the Accounting Information System in the organization (e.g., performance, innovation, reorganization of activities, information reporting); (2) the Accounting Information System Construction, (3) the importance of implementation of the Accounting Information System in Small and medium-sized enterprises and Public-Sector; and (4) the factors that contribute to Accounting Information System efficiency/quality. Poston and Grabski [25] (p. 9) verify that “the trend analysis is structured across underlying theory, research method and information systems lifecycle topics”.

In this study, we found that publications in the research area cited important works, such as those by Fornell and Larcker [67], Otley [68], DeLone and McLean [69], and Jensen and Meckling [12]. These works are related to statistical techniques of data analysis (Structural Equation Model) and using as theoretical reference the contingency theory and the firm theories (managerial behavior, agency and ownership structure).

The results of this study are limited to articles published in journals indexed in the WoS database, which does not allow us to generalize results. This study focuses on bibliometric analysis of literature rather than on the analysis of the publications content. Search trends were performed manually, not using the technique used by Kumar et al. [13]. We discuss results that used different methodologies (database, journals, period of analysis) of previous studies, so comparing results raises some reservations. In the article search, other keywords could be combined with the keyword used, although the keyword used to be comprehensive.

In terms of futures lines of research, we suggest the content analysis, i.e., objectives, methodology, main results and suggestions for future research. On the other hand, to identify the important articles we suggest performing a regression of the citation count on metadata from previous publications according to Staszkiewicz [71] study. On the other hand, given that in WoS the Cited Reference Web of Science function only includes citations to journals that are listed in ISI and given that only a limited number of journals are listed in ISI, we suggest applying this study to the Google Scholar database and also Scopus to compare the results.

In this study, we reinforce the importance of Accounting Information Systems for technological and digital evolution, survival and growth of organizations, public and private and, consequently, for the countries development.

Author Contributions

Conceptualization, A.M. and C.C.; data curation, A.M. and C.C.; formal analysis, A.M. and C.C.; investigation, A.M. and C.C.; methodology, A.M. and C.C.; project administration, A.M.; resources, A.M. and C.C.; software, A.M. and C.C.; supervision, A.M.; validation, A.M. and C.C.; visualization, A.M.; writing—original draft, A.M. and C.C.; writing—review and editing, A.M. and C.C. Both authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses or interpretation of data; in the writing of the manuscript or in the decision to publish the results.

References

- Kamanga, R.; Alexandra, P.M. Facilitated Adoption of Accounting Information Systems: A First Step to Digital Transformation in Township Microenterprises. Open Innov. 2019, 312–319. [Google Scholar] [CrossRef]

- Dalci, G.A.; Tanis, V.N. Benefits of Computerized Accounting Information Systems on the JIT Production Systems. Rev. Soc. Econ. Bus. Stud. 2003, 2, 45–64. [Google Scholar]

- Neogy, D. Evaluation of efficiency of Accounting Information Systems: A study on mobile telecommunication companies in Bangladesh. Glob. Discl. Econ. Bus. 2014, 3, 40–55. [Google Scholar] [CrossRef] [Green Version]

- Puspitawati, L. Strategic Information Moderated by Effectiveness Management Accounting Information Systems: Business Strategy Approach. J. Akunt. 2021, 25, 101–119. [Google Scholar] [CrossRef]

- Suzan, L.; Mulyani, S.; Sukmadilaga, C.; Farida, I. Empirical Testing of the Implementation of Supply Chain Management and Successful Supporting Factors of Management Accounting Information Systems. Int. J. Sup. Chain. Mgt. 2019, 8, 629. [Google Scholar]

- Septriadi, D.; Zarkasyi, W.; Mulyani, S.; Sukmadilaga, C. Management Accounting Information System in gas station business. Utopía Y Prax. Latinoam. Rev. Int. Filos. Iberoam. Y Teoría Soc. 2020, 25, 244–254. [Google Scholar]

- McCallig, J.; Robb, A.; Rohde, F. Establishing the representational faithfulness of financial accounting information using multiparty security, network analysis and a blockchain. Int. J. Account. Inf. Syst. 2019, 33, 47–58. [Google Scholar] [CrossRef]

- Monteiro, A.P.; Vale, J.; Silva, A.; Pereira, C. Impact of the Internal Control and Accounting Systems on the Financial Information Usefulness: The Role of the Financial Information Quality. Acad. Strateg. Manag. J. 2021, 20, 1–13. [Google Scholar]

- Hla, D.; Teru, S.P. Efficiency of accounting information system and performance measures. Int. J. Multidiscip. Curr. Res. 2015, 3, 976–984. [Google Scholar]

- Christensen, J. Conceptual frameworks of accounting from an information perspective. Account. Bus. Res. 2010, 40, 287–299. [Google Scholar] [CrossRef]

- Watts, R.; Zimmerman, J. The Markets for Independence and Independent Auditors; Graduate School of Management, University of Rocheste, Center for Research in Governement Policy & Business, Suzanne Bel: Palo Alto, CA, USA, 1981. [Google Scholar]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Kumar, S.; Marrone, M.; Liu, Q.; Pandey, N. Twenty years of the International Journal of Accounting Information Systems: A bibliometric analysis. Int. J. Account. -Form. Syst. 2020, 39, 100488. [Google Scholar] [CrossRef]

- Mitnick, B.M. Agency theory. Wiley Encycl. Manag. 2015, 2, 1–6. [Google Scholar] [CrossRef]

- Rom and Rohde, Management accounting and integrated information systems: A literature review. Manag. Account. Res. 2007, 8, 40–68.

- O’Connor, N.G.; Martinsons, M.G. Management of information systems: Insights from accounting research. Inf. Manag. 2006, 43, 1014–1024. [Google Scholar] [CrossRef]

- Soudani, S.N. The usefulness of an Accounting Information System for effective organizational performance. Int. J. Econ. Financ. 2012, 4, 136–145. [Google Scholar] [CrossRef]

- Sari, N.Z.M.; Afifah, N.N.; Susanto, A.; Sueb, M. Quality Accounting Information Systems with 3 Important Factors in BUMN Bandung Indonesia. Adv. Soc. Sci. Educ. Humanit. Res. 2019, 343, 93–96. [Google Scholar] [CrossRef] [Green Version]

- Moustafa, E. An Application of Activity-Based-Budgeting in Shared Service Departments and Its Perceived Benefits and Barriers under Low-IT Environment Conditions. J. Econ. Adm. Sci. 2005, 21, 42–72. [Google Scholar] [CrossRef]

- Perez, M.D.M.L.; Morote, R.P. Accounting Information at the Hospital San Julian in Albacete among 1838 and 1859. De Comput. -Rev. Esp. Hist. Contab. 2007, 4, 55–117. [Google Scholar]

- Huy, P.Q.; Phuc, V.K. Accounting Information Systems in Public Sector towards Blockchain Technology Application: The Role of Accountants’ Emotional Intelligence in the Digital Age. Asian J. Law Econ. 2021, 12, 73–94. [Google Scholar] [CrossRef]

- Li, J. Simulation of enterprise accounting information system based on improved neural network and cloud computing platform. J. Ambient Intell. Humaniz. Comput. 2021, 1–14. [Google Scholar] [CrossRef]

- Shen, J.; Han, L. Design process optimization and profit calculation module development simulation analysis of financial accounting information system based on particle swarm optimization (PSO). Inf. Syst. E-Bus. Manag. 2020, 18, 809–822. [Google Scholar] [CrossRef]

- Ezenwoke, O.A.; Ezenwoke, A.; Eluyela, F.D.; Olusanmi, O. A bibliometric study of Accounting Information Systems research from 1975–2017. Asian J. Sci. Res. 2019, 12, 167–178. [Google Scholar] [CrossRef] [Green Version]

- Poston, R.S.; Grabski, S.V. Accounting information systems research: Is it another QWERTY? Int. J. Account. Inform. Syst. 2000, 1, 9–53. [Google Scholar] [CrossRef]

- Ferguson, C.; Seow, P.S. Accounting information systems research over the past decade: Past and future trends. Account. Financ. 2011, 51, 235–251. [Google Scholar] [CrossRef]

- Monteiro, A.P.; Aibar-Guzmán, B.; Garrido-Ruso, M.; Aibar-Guzmán, C. Employee-Related Disclosure: A Bibliometric Review. Sustainability 2021, 13, 5342. [Google Scholar] [CrossRef]

- Yu, Y.; Li, Y.; Zhang, Z.; Gu, Z.; Zhong, H.; Zha, Q.; Yang, L.; Zhu, C.; Chen, E. A bibliometric analysis using VOSviewer of publications on COVID-19. Ann. Transl. Med. 2020, 8, 816. [Google Scholar] [CrossRef]

- Van Eck, N.J.; Waltman, L. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Warren, S.; Sauser, B.; Nowicki, D.A. bibliographic and visual exploration of the historic impact of soft systems methodology on academic research and theory. Systems 2019, 7, 10. [Google Scholar] [CrossRef] [Green Version]

- Rosenberg, A. Philosophy of Social Science, 5th ed.; Westview Press: New York, NY, USA, 2015. [Google Scholar]

- Lee, A.S. A Scientific Methodology for MIS Case Studies. Mis Q. 1989, 13, 33–52. [Google Scholar] [CrossRef] [Green Version]

- Orlikowski, W.J.; Baroudi, J. Studying IT in Organizations: Research Approaches and Assumptions. Inf. Syst. Res. 1991, 2, 1–28. [Google Scholar] [CrossRef] [Green Version]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ 2021, 372, 71. [Google Scholar] [CrossRef]

- Marshall, R.M. Determining an optimal accounting information system for an unidentified user. J. Account. Res. 1972, 10, 286–307. [Google Scholar] [CrossRef]

- Pacini, C.; Wossink, A.; Giesen, G.; Vazzana, C.; Huirne, R. Evaluation of sustainability of organic, integrated and conventional farming systems: A farm and field-scale analysis. Agric. Ecosyst. Environ. 1972, 95, 273–288. [Google Scholar] [CrossRef]

- Córcoles, Y.R.; Penalver, J.F.S.; Ponce, Á.T. Intellectual capital in Spanish public universities: Stakeholders’ information needs. J. Intellect. Cap. 2011, 12, 356–376. [Google Scholar] [CrossRef]

- Brazel, J.F.; Agoglia, C.P. An examination of auditor planning judgements in a complex Accounting Information System environment. Contemp. Account. Res. 2007, 24, 1059–1083. [Google Scholar] [CrossRef]

- Choe, J.M. The effects of user participation on the design of Accounting Information Systems. Inf. Manag. 1998, 34, 185–198. [Google Scholar] [CrossRef]

- Chen, L.H. Web-based learning programs: Use by learners with various cognitive styles. Comput. Educ. 2010, 54, 1028–1035. [Google Scholar] [CrossRef]

- Masanet-Llodra, M.J. Environmental management accounting: A case study research on innovative strategy. J. Bus. Ethics 2006, 68, 393–408. [Google Scholar] [CrossRef]

- Eldenburg, L.; Soderstrom, N.; Willis, V.; Wu, A. Behavioral changes following the collaborative development of an Accounting Information System. Account. Organ. Soc. 2010, 35, 222–237. [Google Scholar] [CrossRef]

- Mahama, H.; Elbashir, M.Z.; Sutton, S.G.; Arnold, V. A further interpretation of the relational agency of information systems: A 780 research note. Int. J. Account. Inf. Syst. 2016, 20, 16–25. [Google Scholar] [CrossRef]

- Ihsan, H.; Ibrahim, S.H.H.M. WAQF accounting and management in Indonesian WAQF institutions: The cases of two WAQF foundations. Humanomics 2011, 27, 252–269. [Google Scholar] [CrossRef]

- Hunton, J.E.; Gibson, D. Soliciting user-input during the development of an accounting information system: Investigating the efficacy of group discussion. Account. Organ. Soc. 1999, 24, 597–618. [Google Scholar] [CrossRef]

- Gray, G.L.; Chiu, V.; Liu, Q.; Li, P. The expert systems life cycle in AIS research: What does it mean for future AIS research? Int. J. Account. Inf. Syst 2014, 15, 423–451. [Google Scholar] [CrossRef]

- Woodward, D.; Woodward, T. The efficacy of action at a distance as a control mechanism in the construction industry when a trust relationship breaks down: An illustrative case study. Br. J. Manag. 2001, 12, 355–384. [Google Scholar] [CrossRef]

- Lehmann, C.M.; Heagy, C.D. Effects of professional experience and group interaction on information requested in analyzing IT cases. J. Educ. Bus. 2008, 83, 347–354. [Google Scholar] [CrossRef]

- Kostic, M.D.; Jovanovic, T.; Juric, J. Cost Management at Higher Education Institutions-Cases of Bosnia and Herzegovina, Croatia and Slovenia. Cent. Eur. Pub. Admin. Rev. 2019, 17, 131. [Google Scholar] [CrossRef] [Green Version]

- Kopel, M.; Riegler, C.; Schneider, G. Providing Managerial Accounting Information in the Presence of a Supplier. Eur. Account. Rev. 2020, 29, 803–823. [Google Scholar] [CrossRef] [Green Version]

- Tarek, M.; Mohamed, E.K.; Hussain, M.M.; Basuony, M.A. The implication of information technology on the audit profession in developing country: Extent of use and perceived importance. Int. J. Account. Inf. Manag. 2017, 25, 237–255. [Google Scholar] [CrossRef]

- Alewine, H.C.; Allport, C.D.; Shen, W.C.M. How measurement framing and accounting information system evaluation mode influence environmental performance judgments. Int. J. Account. Inf. Syst. 2016, 23, 28–44. [Google Scholar] [CrossRef]

- Dobroszek, J.; Zarzycka, E.; Almasan, A.; Circa, C. Managers’ perception of the management accounting information system in transition countries. Econ. Res. -Ekon. Istraživanja 2019, 32, 2798–2817. [Google Scholar] [CrossRef] [Green Version]

- Khadra, H.A.; Al-Hayale, T.; Al-Nasir, N. Contingent effects of system development life cycle critical success factors on accounting information system effectiveness: Using balance scorecard perspectives—Empirical study applied on the Jordanian industrial companies. Int. J. Inf. Technol. Proj. Manag. 2012, 3, 38–61. [Google Scholar] [CrossRef]

- Al-Hattami, H.M. Validation of the D&M IS success model in the context of accounting information system of the banking sector in the least developed countries. J. Manag. Control 2021, 32, 127–153. [Google Scholar]

- Al-Dmour, A.H.; Abood, M.; Al-Dmour, H.H. The implementation of SysTrust principles and criteria for assuring reliability of AIS: Empirical study. Int. J. Account. Inf. Manag. 2019, 27, 461–491. [Google Scholar] [CrossRef] [Green Version]

- Alamin, A.A.; Wilkin, C.L.; Yeoh, W.; Warren, M. The impact of self-efficacy on accountants’ behavioral intention to adopt and use accounting information systems. J. Inf. Syst. 2020, 34, 31–46. [Google Scholar] [CrossRef]

- HA, V.D. Impact of organizational culture on the accounting information system and operational performance of small and medium sized enterprises in Ho Chi Minh City. J. Asian Financ. Econ. Bus. 2020, 7, 301–308. [Google Scholar] [CrossRef]

- Córcoles, Y.R.; Santos Peñalver, J.F.; Tejada Ponce, Á. Demanda de Información Sobre Capital Intelectual en las Universidades Públicas Españolas. Cuad. De Gestión 2012, 12, 83–106. [Google Scholar] [CrossRef] [Green Version]

- Prasad, A.; Green, P. Organizational competencies and dynamic accounting information system capability: Impact on AIS processes and firm performance. J. Inf. Syst. 2015, 29, 123–149. [Google Scholar] [CrossRef]

- Tan, B.S.; Low, K.Y. Blockchain as the database engine in the accounting system. Aust. Account. Rev. 2019, 29, 312–318. [Google Scholar] [CrossRef]

- Janvrin, D.J.; Payne, E.A.; Byrnes, P.; Schneider, G.P.; Curtis, M.B. The updated COSO Internal Control—Integrated Framework: Recommendations and opportunities for future research. J. Inf. Syst. 2012, 26, 189–213. [Google Scholar] [CrossRef]

- Sumaryati, A.; Praptika Novitasari, E.; Machmuddah, Z. Accounting Information System, Internal Control System, Human Resource Competency and Quality of Local Government Financial Statements in Indonesia. J. Asian Financ. Econ. Bus. 2020, 7, 795–802. [Google Scholar] [CrossRef]

- Burney, L.L.; Radtke, R.R.; Widener, S.K. The intersection of “bad apples”, “bad barrels,” and the enabling use of performance measurement systems. J. Inf. Syst. 2017, 31, 25–48. [Google Scholar] [CrossRef]

- Arif, D.; Yucha, N.; Setiawan, S.; Oktarina, D.; Martah, V. Applications of Goods Mutation Control Form in Accounting Information System: A Case Study in Sumber Indah Perkasa Manufacturing, Indonesia. J. Asian Financ. Econ. Bus. 2020, 7, 419–424. [Google Scholar] [CrossRef]

- Alawaqleh, Q.A. The Effect of Internal Control on Employee Performance of Small and Medium-Sized Enterprises in Jordan: The Role of Accounting Information System. J. Asian Financ. Econ. Bus. 2021, 8, 855–863. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Otley, D.T. The contingency theory of management accounting: Achievement and prognosis. In Readings in Accounting for Management Control; Springer: Boston, MA, USA, 1980; pp. 83–106. [Google Scholar]

- DeLone, W.H.; McLean, E.R. Information systems success: The quest for the dependent variable. Inf. Syst. Res. 1992, 3, 60–95. [Google Scholar] [CrossRef] [Green Version]

- Ibrahim, F.; Ali, D.N.H.; Besar, N.S.A. Accounting information systems (AIS) in SMEs: Towards an integrated framework. Int. J. Asian Bus. Inf. Manag. 2020, 11, 51–67. [Google Scholar] [CrossRef]

- Staszkiewicz, P. The application of citation count regression to identify important papers in the literature on non-audit fees. Manag. Audit. J. 2019, 34, 96–115. [Google Scholar] [CrossRef]

Figure 1.

Sample process selection (PRISMA).

Figure 2.

Scientific production per year.

Figure 3.

Single and multi-authored publications.

Figure 4.

Countries/regions with more than 2 publications. Source: VOSviewer.

Figure 5.

Organizations with more than 2 publications. Source: VOSviewer.

Figure 6.

Most used keywords. Source: VOSviwer.

Figure 7.

Bibliographic coupling in digital accounting. Source: VOSviewer.

Figure 8.

Co-cited sources. Source: VOSviewer.

Figure 9.

Most co-cited authors. Source: VOSviwer.

Table 1.

Publications and impact factor per journal with more than 2 publications.

| Journals | TP | Impact Factor 2019 |

|---|---|---|

| Journal of Asian Finance Economics and Business | 6 | JCR-0.37 |

| International Journal of Accounting Information Systems | 5 | JCR-0.9 |

| Journal of Information Systems | 4 | JCR-2.64 |

| Global Business Review | 3 | JCR-0.42 |

| Management Theory and Studies for Rural Business and Infrastructure | 3 | ESCI |

| Pertanika Journal of Social Science and Humanities | 3 | JCR-0.17 |

| Accounting Organizations and Society | 2 | JCR-2.62 |

| Accounting Review | 2 | JCR-5.68 |

| Actualidad Contable Faces | 2 | ESCI |

| Asian Journal of Business and Accounting | 2 | JCR-0.19 |

| Contemporary Accounting Research | 2 | JCR-2.77 |

| De Computis-Revista Espanola de História de la Contabilidad | 2 | ESCI |

| Economic Research-Ekonomska Istrazivanja | 2 | JCR-0.51 |

| Ekonomski Pregled | 2 | JCR-0.13 |

| Ekonomski Vjesnik | 2 | ESCI |

| Industrial Management and Data Systems | 2 | JCR-0.99 |

| International Journal of Accounting and Information Management | 2 | JCR-0.46 |

| Journal of Information and Organizational Sciences | 2 | JCR-0.15 |

| Journal of Management Control | 2 | JCR-0.67 |

| Journal of Small Business and Enterprise Development | 2 | JCR-0.73 |

| Polish Journal of Management Studies | 2 | JCR-0.32 |

| Reunir-Revista de Administração Contabilidade e Sustentabilidade | 2 | ESCI |

| Revista de Contabilidad-Spanish Accounting Review | 2 | JCR-0.38 |

Legend: TP–Total Publications. Source: VOSviewer; WoS Database.

Table 2.

Publications number per author.

| Author | TP | h-Index |

|---|---|---|

| Domeika, Povilas | 3 | 1 |

| Napitupulu, Ilham Hidayah | 3 | 2 |

| Rizza, Carmela | 3 | 2 |

| Ruggeri, Daniela | 3 | 3 |

| Hariyati | 2 | 2 |

| Janvrin, Diane J. | 2 | 11 |

| Ramirez Corcoles, Yolanda | 2 | 8 |

| Sacer, Ivana Mamic | 2 | 3 |

| Santos Penalver, Jesus F. | 2 | 1 |

| Tejada Ponce, Angel | 2 | 6 |

| Tjahjadi, Bambang | 2 | 4 |

Legend: TP–Total Publications; h-index-author-level metric that measures both the productivity and citation impact of the publications. Source: VOSviewer.

Table 3.

Articles with more than 10 Citations.

| RO | Author/s (Year) | Title | TC |

|---|---|---|---|