The Consequences of Indirect Taxation on Consumption in Nigeria

Department of Accounting, College of Management and Social Sciences, Covenant University, Ota 110001, Nigeria

J. Open Innov. Technol. Mark. Complex. 2020, 6(4), 105; https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc6040105

Submission received: 16 July 2020

/

Revised: 15 August 2020

/

Accepted: 17 August 2020

/

Published: 7 October 2020

Abstract

:This research tests the consequences of Nigeria’s indirect taxes on consumption. There are two reasons why the government imposes taxes on goods and services in Nigeria. The primary purpose is to produce income for the smooth running of the administration. Another silent reason is to discourage the ingestion of prohibited products and services, and that is through customs and excise duties (CED). This study assesses both Value Added Tax (VAT) and CED to determine their effects on consumption using various econometric tools, such as trend analysis, pairwise Granger causality tests, unrestricted co-integration rank test, least squares technique, and data that cover the period from 2005 to 2019. The results indicate that VAT insignificantly but positively influences consumption, while CED has a considerable auspicious influence on use. This result shows that VAT imposition on merchandises and services is discouraging the absorption of specific foodstuffs and services and allowing the operation of informal economic activities to thrive in Nigeria. However, CED charges do not reduce the use of certain illegal products purposely taxed to discourage their consumption. This study recommends a reduction in the prices of food items and services to enable consumers to increase their patronage, while the products that attract CED but are harmful should be banned entirely. Thus, offenders should be allowed to face the wrath of the law.

1. Introduction

Value Added Tax (VAT) is an indirect tax levied on all merchandises and amenities manufactured or rendered in a country except for supplies and facilities that are VAT relieved. VAT is a levy on the number of products and provisions that the end user ultimately endures, and its collection is designed and made possible at each phase of the manufacturing and delivery sequence. It implies that VAT is a consumption tax collected from individuals who only suffer a little incidence of taxation that allows the persons who pays VAT not to bear the entire cost of the charge [1]. Following the enactment of Value Added Tax Act (VATA) 1993, VAT was introduced in Nigeria as specified in No. 102 of the VATA 1993 to replace the sales tax that was then the consumption tax supported by the Federal Government Decree No. 7 of 1986. Since the introduction of VAT in 1993, the Nigerian VAT rate remained at 5% and is one of the lowest globally. President Obasanjo’s Administration considered a VAT increment from 5% to 10%, but the proposal was turned down by the Late President Yar’Adua’s administration due to stiff resistance from the Nigerian people.

Section 34 of the Finance Act of 2020 increased the VAT rate from 5% to 7.5%, which is one of the major changes in Nigerian VAT administration. President Buhari signed the Finance Bill of 2019 into law on 13 January 2020, and the Finance Act 2020 became effective from 1 February 2020. However, Table A1 in Appendix A shows that VAT is not applicable in countries such as Bermuda, Cayman Islands, Gibraltar, Greenland, Guernsey, Channel Islands, Hong Kong SAR, Kuwait, Libya, Macau SAR, Oman, Qatar, Turks and Caicos Islands, and the United States [2]. In Table A2 in Appendix B, Nigeria falls within the countries with the lowest VAT rate, which ranges from 2.5% to 9%. These countries include Bahrain 5%, Fiji 9%, Japan 8%, Jersey, Channel Islands 5%, Liechtenstein 7.7%, Nigeria 7.5%, Panama 7%, Saudi Arabia 5%, Singapore 7%, Sri Lanka 8%, Switzerland 7.7%, Taiwan 5%, Thailand 7%, Timor-Leste 2.5%, and the United Arab Emirates 5% [2]. Countries with the highest VAT rate that is noteworthy and ranges between 20 and 27 per cent include Albania 20%, Argentina 21%, Slovenia 22%, Poland 23%, Finland 24%, Denmark 25%, and Hungary 27%, among others [2].

It is worthy of note that VAT imposition on all goods and services does not include exempted goods, which are not subject to VAT as specified in No. 102 of VATA 1993 include everything medicinal in addition to pharmacological goods, essential foodstuff, books and learning resources, infant foods, and nourishment. The exemption includes domestically manufactured agrarian and veterinary medication, agricultural equipment and agribusiness conveyance tools, all exports, plants and machines traded in for usage in the export handling sector. The VATA 1993 also excludes plant and equipment acquired for operation of gas in downstream gasoline processes, tractors, and cultivators and agronomic apparatuses bought for agricultural tenacities from VAT payment. The relieved services include medicinal services, services rendered by community banks, the People’s Bank and secured loan organizations, shows and concerts produced by enlightening institutes as part of education, and all exported facilities [3,4]. The zero-rated goods and services specified by the VATA 2007 (as amended) include non-oil exports, merchandises and services procured by ambassadors, and privileges obtained for use in philanthropic sponsored schemes.

The new Finance Act 2020 has improved the goods and services exempted from VAT by extending the list of essential food items that are free from VAT. The additional items included in the list of necessary food items that are VAT free comprise seasonings (honey), dough, mueslis, catering apply oil, gastronomic parsleys, fish, flour and thickener, and berries (fresh or dried). The list also includes animal protein sources, milk, nuts, throbs, tubers, saline, spuds, H2O, domestically produced sterile bath sheets, swabs, or wipes. The additional services exempted for VAT under the new Finance Act 2020 consist of services rendered by microfinance banks, training involving kindergarten, and other levels of schooling. Section 38 of the Finance Act 2020 exempts businesses with a turnover that is less than N25 million from payment of VAT. Nigeria’s VAT revenue sharing formula is 85% to the states and local governments, while the federal government has only a 15% share. From the 85% share, 50% is allocated to the state, governments, while the local governments’ share is 35%. The idea behind this sharing preference to states and local governments is to enable them to carry out their social responsibilities and economic obligations to the citizens, which invariably includes the new minimum wage the state governors committed themselves to satisfy [5].

The Finance Act 2020 [6] also clarifies that VAT record should be on a cash basis and no longer had invoice based, which is on an accrual basis. The reason is that a taxpayer can only recover input VAT against output VAT that is collected. This treatment agrees with the prudence concept of accounting, which encourages revenue recognition and financial planning based on income earned and not revenue expected.

However, the debate on the influence of incidental levies (VAT and CED) on the fiscal progress of a nation has been ongoing among scholars, using different models, parameters, and tools of measurement coupled with varying analysis outcomes. For instance, [7] found significant positive input of VAT on Romanian economic growth using GDP, while [8] used the Romanian national income to assess VAT contribution to economic growth and also found it significantly positive. Simionescu and Albu [9] tested the effect of VAT on the monetary progression of CEE-5 and a significant favorable impression of VAT on GDP was established, but [10] found that VAT contributions to Kenya’s GDP was inconsequentially positive. Ikeokwu and Micah [11] found the impact of CED and VAT on Nigeria’s Per Capita Income (PCI) materially positive, while [12] revealed that VAT and CED had an insignificant negative impact on Nigeria’s monetary evolution. These differences prompted the current enquiry, which focused on the impact of VAT and CED on consumption in Nigeria. This study uses the consumer price index (CPI) as a proxy for consumption. CPI represents consumption expenses, which measure the average variation in costs over time that consumers pay for a basket of goods and services. It covers the period from 2005 to 2019 and tries to make a substantial difference by using consumption patterns as the response variable, assessing how people’s consumption levels in Nigeria respond to VAT and CED charges imposed on goods and services.

Nevertheless, it is worthy to note that tax revenue in an unindustrialized state such as Nigeria is fraught with tax avoidance and evasions due to a high rate of underground economic activities [13] of which VAT is not an exemption. Majorly, the informal economy forms a significant aspect of Nigeria’s economy. It remains a wonder how VAT revenues accruing from such shadow economic activities will get to the government. That is, it is probable VAT charges are not obtainable in the informal sector where every business is undercover without proper disclosure to the relevant authorities [14]. Where companies do not register officially due to underground economy, it will be difficult to account for VAT revenue. Individuals who get involved in the informal sector evade all manner of tax payment [15], which consequently and negatively affects government public service delivery [16]. According to [17], VAT is the leading source of global tax proceeds, but it is confronted with the challenges of tax avoidance due to shadow economic activities and corruption among business participants. However, this study examines the effect of indirect taxes on consumption. Consumption of certain goods and services could be discouraged through indirect taxes such as customs and excise duties, while VAT is such an indirect tax that does not discourage consumption of goods and services because its payment is not felt by an individual at any stage in the consumption chain, but the challenge is its remittance to the government, which sometimes is hindered due to frequent tax evasion.

2. Collected Works Appraisal

2.1. Theoretical Assessment

2.1.1. Value Added Tax (VAT)

Value added tax (VAT) refers to an ingestion charge imposed at every phase of the absorption sequence and suffered by the ultimate end user of the product or service [18]. Prior to the implementation of the 2020 Finance Act in Nigeria and under the VAT Act of 1993 as emended, it was obligatory for an individual seller to levy and pull together the VAT at a uniform ratio of 5% on all billed sums for merchandises and services that are not freed from VAT. However, with the introduction and implementation of the 2020 Finance Act, all materials and business activities that are not excused from VAT attract a charge of 7.5% VAT, which accounts for 50% increase in the VAT rate. Sections 10 and 11 of VATA offers the dissimilarity amid contribution VAT and production VAT. Involvement VAT refers to the tax paid to suppliers on the purchase of taxable materials and financial undertakings while the productivity VAT is the tax received from customers on the value of taxable supplies and business activities sold or rendered [12] (Andersen Tax Digest, 2020). According to [19], if the VAT received on behalf of the government (production VAT) in a specific period surpasses the VAT paid to other individuals (contribution VAT) in the same period, the taxable individual or company is expected to pay the variance to the government periodically, which is monthly. Wherever the converse becomes the circumstance, the taxpayer is permitted to a reimbursement of the extra VAT funded or he may virtually obtain a tax credit of the surplus VAT from the administration [20]. Following the affirmation of [21], every export is zero ranked for VAT, i.e., no VAT is billed on products shipped out to other countries for sale. Furthermore, VAT is allocated with the legal tender of the business under which products or financial deeds are contracted [22].

Sections 8, 28 and 35 of VATA (as amended) enforces a fine of N50,000 for the initial month of not being able to register and inability to notify the Federal Inland Revenue Service (FIRS) of variation in business address or perpetual termination of trade or business and failure to file returns [22]. All other subsequent months of failure attract a fine of N25,000 each month in addition to the initial N50,000 in the first month that the disappointment ensues [22]. However, failure to remit VAT attracts a penalty of the VAT, in addition to 10% of the VAT plus interest rate based on the Central Bank of Nigeria’s prevailing monetary policy rate [22]. The new Finance Act 2020 provides punishment for late filing of VAT returns. Inability to remit VAT revenues attracts a penalty of N50,000 in the first month of defaulting and N25,000 for the succeeding months [22]. Due to the upward review necessitated by the Finance Act 2020, the penalty was reviewed upward from N10,000 to N50,000 for the first month and N5000 to N25,000 for the successive periods the taxpayer fails to file VAT returns. The fine for failing to register for VAT is appraised upwards to N50,000 for the first month of failure and N25,000 for each consequent month of failure to register for VAT. The penalties are explained in the Table 1 below:

Section 10 of VATA (as amended) provides that it is mandatory for a non-resident individual who makes chargeable deliveries to somebody residing in Nigeria to register with the FIRS for VAT. The non-resident individual is to use the address of the person to whom he/she is supplying the materials as its Nigerian address, for communication reasons in connection with the VAT. The non-resident person is required to include VAT on its invoice for the supply of goods or services made, while the person who receives the supply in Nigeria is mandated to withhold and remit the VAT due on the invoice to the FIRS in the currency of transaction [22].

2.1.2. Custom and Excise Duties

The Finance Act 2020 provides amendments to the Customs and Excise Tariff Act in order to encourage domestic industries. Based on the Finance Act 2020 provisions, excise duties will now apply to excisable goods, such as cigarettes, wines, spirit, beer, and stout, among others, only when they are imported into Nigeria. Specific domestically produced items are subject to excise duties at definite rates. These domestic products include tobacco, spirits, and alcohol. Other items in the schedule of excisable products but now suspended and no longer apply include perfumes, cosmetics, toilet papers, non-alcoholic beverages, telephone recharge vouchers, soaps and detergents, paper packaging, spaghetti, and noodles, among others.

2.1.3. Open Innovation and Tax Administration in Nigeria

Open innovation is a synergy of external and internal ideas pooled together to facilitate the adoption of technological advancement in businesses and in the public sector. The implication is that open innovation is a combination of technology and internal and external philosophies to facilitate the economic progress of a nation, which comprises the input of both private and public sectors. Thus, open innovation is both social and market based. The social open innovation tends to combine technology and the society [23]. According to [23], the government has the responsibility to make policies that will promote open innovation both in the private and public sector operations. Over the years, VAT and CED administration in Nigeria was done manually through multitasking activities of physically going to the tax office to do the necessary filings of tax returns, submit audited financial statements, and all other relevant documents. Due to the COVID-19 pandemic, the government and the Federal Inland Revenue Services (FIRS) in Nigeria initiated online filing of tax returns (including VAT and CED returns) and also encouraged taxpayers’ complaints through emails [24]. The adoption of social open innovation encouraged the society (taxpaying community) to embrace the new technologies of filing tax returns without further struggle. However, with the open platform, the government is able to reduce tax filing stress on the taxpayer and also promote the mobility of highly skilled laborers to ensure efficient tax administration.

2.2. Review of Related Studies

Stailova & Patonov [25] established empirical evidence on the effect of direct and indirect taxes on economic growth of the EU-27 using data that covered the period from 1995 to 2010. The study employed a regression model, which used variables such as the tax-to-GDP ratio and the tax arrangement such as the value of direct taxes, indirect taxes, and public donations. The study found that direct taxes had a significant impact on economic growth because they were economical for the EU countries. However, indirect taxes showed the propensity to reduce the revenue estimate due to the disparity in the indirect tax organization. Asogwa and Nkolika [26] focused their study on the impact of VAT on investment growth in Nigeria. Following that all government revenue collection should be aimed at executing developmental projects that will enhance economic growth in the country. Thus, the result of the study revealed that VAT had significant effect on investment in Nigeria. Muresan, David, Elek, and Dumiter [8] assessed the impact of VAT on the economic activity of Romania. The study revealed that national income improved in proportion with aggregate demand. This result implied that economic activity was growing as consumption grew, resulting in more VAT revenue to the government. Onwuchekwa and Aruwa [27] examined the contribution of VAT on the total tax revenue of the government in Nigeria. The study covered the period from 1994 to 2011, and data were collected from the CBN Statistical Bulletin, FIRS, and Nigeria Bureau of Statistics. Using the ordinary least squares technique, the study found that VAT contributed significantly to total tax revenue of government.

Simionescu and Albu [9] analyzed the impact of the standard VAT rate on economic growth of five Central and Eastern European Countries (CEE-5), which include Bulgaria, Czech Republic, Hungary, Poland, and Romania. The study made use of panel data models including random effect model, dynamic panel, panel vector-autoregression, and data that spanned from 1995 to 2015. The findings revealed that VAT rate had a significant positive impact on economic growth. The study further applied bilateral Granger causality and Bayesian linear models, and the result indicated that VAT rate had a positive influence on the GDP rate of Hungary only. Kolahi and Noor [28] investigated the effect of VAT on the economic growth of 19 emerging nations from 1995 to 2010 using GMM-system estimator. The study found evidence that VAT had a negative influence on capital accumulation growth and productivity, while a positive effect of VAT on the level of economic growth was established. Inyiama and Ubesie [29] investigated the effect of VAT and customs and excise duties (CED) on Nigeria’s economic growth from 2000 to 2014 using a simple regression technique. The study found that both VAT and CED were significantly affecting the GDP, and there was an existence of a very strong relationship among them. Akhor and Ekundayo [12] probed the impact of indirect tax revenue on economic growth in Nigeria from 1993 to 2013 using a co-integration test and error correction model regression. The result indicated that VAT exerted a significant negative impact on economic growth, while CED had an insignificant negative influence on real gross domestic product.

Oraka, Okegbe, and Ezejiofor [17] investigated the effect of value added tax on the Nigerian economy from 2003 to 2015 using a simple regression analysis. The study found evidence that VAT has a negative relationship with per capita income, while a positive relationship existed between VAT and the government total revenue. Bazgan [7] studied the impact of direct and indirect taxes on economic growth of Romania from 2009 to 2017. The econometric model included direct taxes, indirect taxes, and GDP. The examination gave a result, which showed that positive changes implemented in the indirect tax structure had a strong positive influence on economic growth, while such variation in the direct tax structure negatively affected the economy in the immediately following fiscal year. Olatunji and Ayeni [30] assessed the effects of VAT and customs duties on revenue generation in Nigeria from 2000 to 2016 using autoregressive distributed lag (ARDL) and Granger causality tests. The result of the Granger causality tests revealed that customs duty and VAT did not result to revenue generation as originally expected.

Abomaye, Williams, Michael, and Friday [31] analyzed the contribution of petroleum profit tax (PPT), company income tax (CIT), and customs and excise duties (CED) to Nigeria’s economic growth using the Ordinary Least Squares method and data covering the period from 1980 to 2015. The result of the study revealed that PPT, CIT, and CED contributions were insignificant in affecting economic growth in Nigeria. Owino [10] appraised the effect of VAT on economic growth of Kenya from 1973 to 2010 using the ordinary least squares technique. The results revealed the existence of a positive but insignificant relationship between VAT revenue and Kenya’s GDP. The finding implied that VAT revenue in Kenya was not sufficient to influence economic growth. Ikeokwu and Micah [11] examined the influence of indirect taxes on the economic growth of Nigeria using data that covered the period from 2000 to 2016. The study found evidence that both CED and VAT exerted a significant positive influence on PCI and GDP used as a proxy for economic growth.

3. Research Resources and Techniques

The research evaluates the consequences of Nigeria’s indirect taxation on consumption. The examination uses an ex-post facto inquiry strategy to enable the use of existing historical data, which are also a secondary form of data spanning from 2005 to 2019. This research design does not give room for data manipulation; rather, they are obtained from economic activities that have already taken place and are essential for upcoming predictions. The appropriate diagnostic tests are carried out to establish data normality and ensure absence of serial correlation as well as multicollinearity. The analysis of data is done with PGCT (pairwise Granger causality tests) in addition to the OLS (ordinary least squares) method in order to avoid vagueness in explanation of the arithmetical fallouts. All the data obtained for this study were gathered from the CBN (Central Bank of Nigeria) Numerical Communiqué, and the World Bank Economic Indicators. For the purpose of uniformity and to avoid misuse of numbers, all the datasets are communicated in their logarithm form due to the difference in their values. The reason for the application of CPI as proxy for consumption cost is that CPI “is the proportion of living costs dependent on changes in retail costs” [32]. CPI measures the variation in the price a buyer pays for products and services obtained [32]. Thus, if the price change of a product or activity is abnormally high, the law of demand and supply applies. The consumers will cease consumption of the product or service, except where it is a necessity and there are cheaper alternatives that can adequately satisfy the need. This study actually finds this proxy very useful especially as VAT and CED imposition on goods and services increases their consumption cost in such a manner that prompts different reactions from consumers. These reactions can affect the revenue from VAT and CED adversely or positively.

Typical Description

This research provides practical mathematical association amid reliance as well as predictor factors as described in the following equations:

where: CPI = consumer price index; VAT = value added tax; CED = custom and excise duties; β0 = constant; β1–β2 = regression coefficients; µ = error term.

CPI = f (VAT, CED)

LOGCPI = β0 + β1LOGVAT + β2LOGCED + µ

The earlier expectancy: it is anticipated: β1 > 0, β2 < 0.

The anticipation is that VAT will have a progressive and noteworthy influence on consumption, while CED should discourage consumption.

4. Statistics Breakdown Plus Interpretation

Diagnostic Tests

Table 2, Table 3 and Table 4 depict an absence of the serial correlation, heteroskedasticity, and multicollinearity, respectively. The probability of 0.81 (Table 2) and 0.76 (Table 3) imply non-existence of serial correlation and heteroskedasticity accordingly, as they are both greater than 5%.

Similarly, the variance inflatory factor (VIF) of 8.6 is below the benchmark of value of 10, meaning multicollinearity does not exist in the study sample [29].

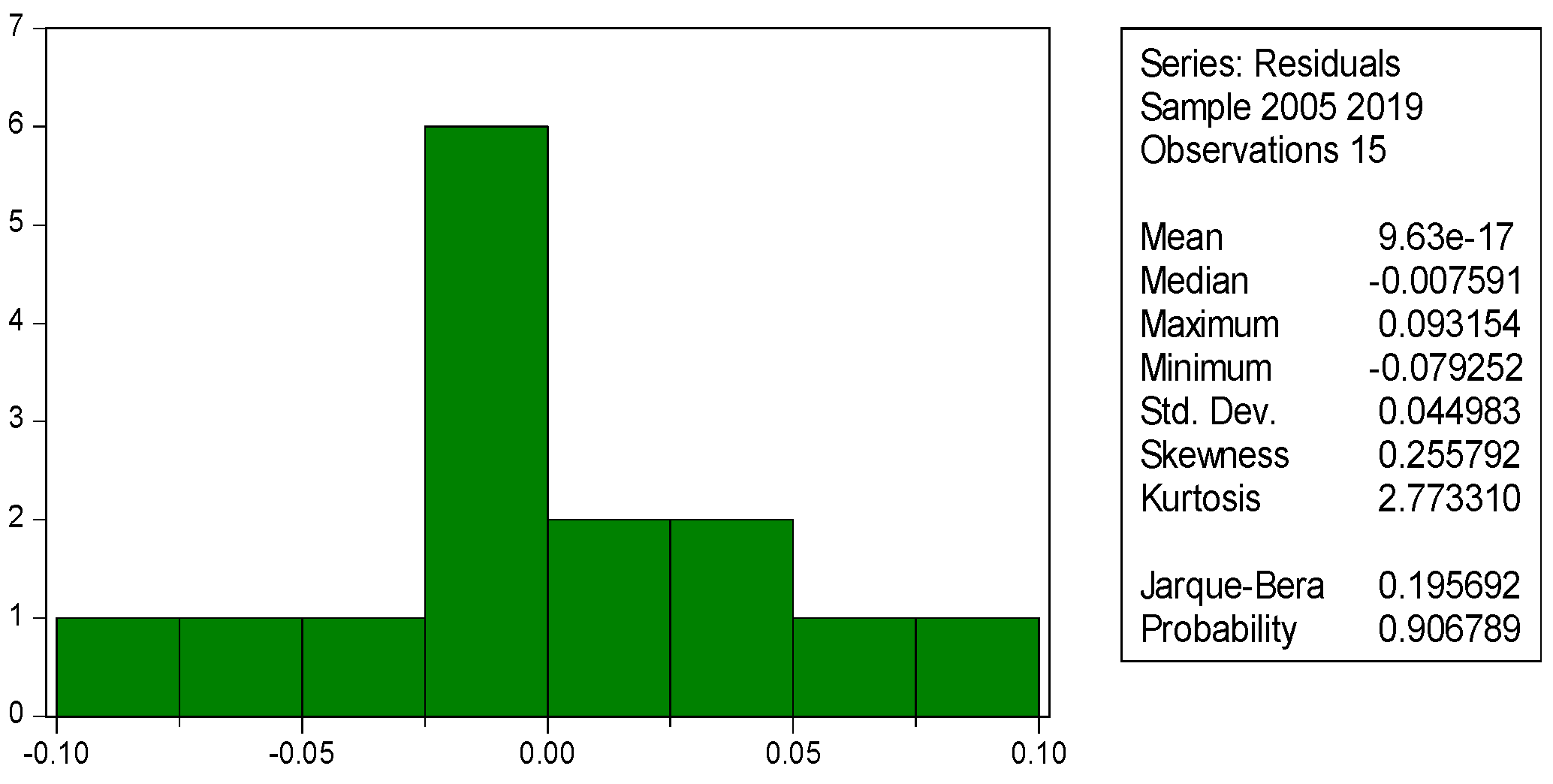

Figure 1 appraises a dataset distribution normality. Using Jarque–Bera probability, the value of 0.9, which is greater than the 0.05 significance level, shows that the distribution is normal and free from error. The Kurtosis is approximately 3, which also signifies normality in the data distribution because the Kurtosis of a normal distribution is usually 3. The skewness of 0.25 is greater than zero, which implies the spread is moderate and the skewness is within the normal region, while the standard deviation shows a lesser range meaning that the figures cluster round the mean values.

In Table 5, the pairwise Granger causality tests depict that VAT does not influence the consumption pattern (CPI) in Nigeria and likewise does CPI affect VAT collection or revenue. This result shows that VAT revenue collection is still very low or not effective. It is obvious that tax evasion or avoidance is playing out, whichever way. The VAT imposition on some products may be affecting consumers’ choice of product, which means consumers may be avoiding some products with a high level of VAT on them. At the same time, this action will be reducing government revenue expected from VAT collection in a fiscal year. The result also shows that customs and excise duties (CED) do not possess momentous consequence on consumption, rather consumption causes CED revenue generation significantly. The result on Table 1 further revealed that CED does not affect VAT collection and VAT collection does not influence CED collection. That is, a uni-directional or bi-directional relationship does not exist between VAT and CED or VAT and CPI. Looking at the result further, the reason for CED imposition on products is to encourage expansion of domestic industries and to discourage the consumption of harmful products, such as cigarettes, wines, spirit, beer, and stout, especially where importation of these products is required. It is expected that consumption of these products should reduce, thereby resulting in a corresponding decrease in CED collection, but the reverse is the case. The implication is that the consumers of these products in Nigeria are strongly addicted to them and will not reduce their consumption pattern because of tax.

Table 6 establishes the type of connection existing among the elements under study. From the result, there is the presence of At most 1 * co-integrating equation at 5% degree of importance, which confirms the existence of a long-run equilibrium relationship between CPI and the explanatory variables. This is based on the information on Table 6 showing that the p-value is below 5% substantial amount.

The trend of data on Figure 2 depicts a steady rise in consumption cost, a little drop in VAT revenue from 2014 to 2016. The CED kept rising and declining depending on the variations in economic policies affecting the consumption of commodities that attract CED. The correlation result on Table 6, put forward a very strong association between the CPI and the autonomous variables (VAT & CED). The correlation (R) value is 97%, which is the square root of the R-squared of 95%. The R-squared value of 95% ratifies the extent to which VAT and CED define the disparities in CPI. Thus, the remaining 5% is accounted for by other economic elements that the model of this study did not capture. The Durbin–Watson of 1.6—which is 2 in approximation—specifies nonappearance of autocorrelation in this study sample [33]. The F-statistic is 115.8682, while the p-value is 0.000 < 0.05. The value of the F-statistic is a pointer depicting the numerical importance of the model employed and its appropriateness for the research. Therefore, both the VAT and CED collectively impact on CPI.

The standard error of regression in Table 7 is employed to check the correctness of the estimates represented by the regression line measuring the accuracy of the projected values. When it is very inconsequential, that is less than 1 or 0, it is faultless. Thus, the standard error of regression has the value of 0.048, which suggests that the regression line and the correlation as well as the predicted values are at liberty with inaccuracies. The t-statistic in Table 7 is used to determine the distinct effects of VAT and CED on consumption. VAT has 1.287825 (t-statistic) and 0.22 > 0.05 (p-value) as its materiality magnitude. This result agrees with [10] but is in conflict with [9]. However, the consequence confirms that VAT is inconsequentially positive in affecting consumption. In other words, consumption of certain goods and services are discouraged and have less patronage due to VAT. Apart from the low patronage of these goods and services, lack of VAT returns to the government after collection by individuals and companies is another challenge affecting VAT contribution. The challenge of official economic activities prevailing in the country also accounts for less VAT remittances to the relevant authority.

On a divergent note, CED t-statistic in Table 7 is 3.951279 with the p-value of 0.00 < 0.05 degree of importance. The outcome reveals that CED imposition to discourage consumption of certain goods and services cannot achieve its objective, rather consumers of those selected products tend to increase in number, so their patronage of those products continues to multiply. Thus, this result disagrees with [12] but is in harmony with the findings of [11]. CED is majorly a mechanism to discourage consumption of certain harmful products and imported goods, such as cigarettes and alcoholic drinks by the government, but from the result of this study, it is obvious that the purpose is yet to be achieved.

5. Conclusions and Recommendation

This research determines the incidental assessments aftermath on consumption in Nigeria. One of the objectives of this study is to keep in line with the open innovation concept and trends in businesses, which includes amendment in the associated indirect taxes. Chesbrough [34] explained that open innovation is “a paradigm that assumes that firms can and should use external ideas as well as internal ideas, and internal and external paths to market as the firms look to advance their technology”. In order to pursue the open innovation goal of using external and internal ideas to improve business operations in Nigeria, Section 38 of the Finance Act 2020 relieves businesses with a revenue that is less than N25 million from the payment of VAT. It is important to understand that consumers react to changes in prices of goods and services either directly or indirect. The reaction could result in affirmative, sometimes undesirable, but it is subject to the value each consumer attaches to the products or services being consumed. In this study, we discovered that VAT impacts positively on consumption, but its influence is very immaterial to reckon with. However, VAT’s insignificant influence on consumption could be likened to low patronage of some goods and services due to VAT imposition on them. Another scenario could be due to informal economic activities hindering the collection of VAT revenue and the nonchalant behavior of some companies and individuals who fail to remit VAT revenues to the appropriate government revenue authorities.

Businesses operating underground and failing to remit VAT revenues is one of the challenges of open innovation, which has made it difficult for SMEs to be transformed despite government’s efforts to improve their operations. On the contrary, CED has a substantial positive impact on consumption. That means instead of CED imposition discouraging the consumption of imported goods and services and other harmful materials, their consumption is on the increase. From the foregoing, the research recommends that governments endeavor to reduce the prices of products and services attracting value added tax charges. The reduction in the prices of these consumable products will enhance their consumption despite the VAT charges levied on them. This study is also proposing the initiation of other mechanisms by the designated authorities to depress the intake of unsafe foodstuffs in the country. Import of such products should be totally banned and a strict check should be put in place against smugglers of these prohibited goods and services.

The underlying forces propelling the improvement culture openly adopted by the government to modernize VAT and CED administration in Nigeria is a function of prevailing economic realities, while keeping in line with universal best practices. This study highlights several innovative outcomes occasioned by changes in VAT and CED policies in Nigeria. The fundamental reason behind the open innovation culture promoted by this study is to ensure that the public is abreast with the changes that have occurred in recent times in VAT and CED administration in the country. The knowledge this study is providing will help to improve and sustain entrepreneurship operations, especially in VAT remittances to the government. It will also help to give the public the enlightenment to inhibit the consumption of items with extraordinary CED charges on them. The government will also ensure that open innovation engineering on tax policies do not cripple economic activities or adversely affect private sector operations in the country. The adoption of modernization principles should not also discourage foreign direct inflows in Nigeria. The government should ensure that VAT and CED practices encourage international business participation and investment to boost the economic growth of the nation.

Funding

This research received no external funding.

Conflicts of Interest

The author declares no conflict of interest.

Appendix A

{kind=link}

{kind=link}

Table A1.

Countries where VAT is not application.

| TERRITORY | STANDARD VAT RATE (%) |

|---|---|

| Bermuda (last reviewed 10 February 2020) | NA |

| Cayman Islands (last reviewed 7 January 2020) | NA |

| Gibraltar (last reviewed 12 February 2020) | NA |

| Greenland (last reviewed 9 January 2020) | NA |

| Guernsey, Channel Islands (last reviewed 6 January 2020) | NA |

| Hong Kong SAR (last reviewed 30 December 2019) | NA |

| Kuwait (last reviewed 12 January 2020) | NA |

| Libya (last reviewed 22 November 2019) | NA |

| Macau SAR (last reviewed 13 January 2020) | NA |

| Oman (last reviewed 26 April 2020) | NA |

| Qatar (last reviewed 10 December 2019) | NA |

| Turks and Caicos Islands (last reviewed 13 January 2020) | NA |

| United States (last reviewed 14 January 2020) | NA |

Source: Adapted from PWC, 2020.

Appendix B

Table A2.

Countries with the lowest VAT rate from 2.5–9 percent.

| TERRITORY | STANDARD VAT RATE (%) |

|---|---|

| Bahrain (last reviewed 8 January 2020) | 5 |

| Fiji (last reviewed 27 January 2020) | 9 |

| Japan (last reviewed 27 December 2019) | Consumption tax: 8 |

| Jersey, Channel Islands (last reviewed 7 January 2020) | Goods and services tax (GST): 5 |

| Liechtenstein (last reviewed 20 December 2019) | 7.7 |

| Nigeria (last reviewed 28 January 2020) | 5% to be increased to 7.5% effective 1 February 2020 |

| Panama (last reviewed 31 December 2019) | Movable goods and services transfer tax: 7 |

| Saudi Arabia (last reviewed 27 December 2019) | 5 |

| Singapore (last reviewed 6 February 2020) | Goods and services tax: 7 |

| Sri Lanka (last reviewed 17 February 2020) | 8 |

| Switzerland (last reviewed 31 December 2019) | 7.7 |

| Taiwan (last reviewed 18 February 2020) | 5% to general industries |

| Thailand (last reviewed 14 January 2020) | 7 |

| Timor-Leste (last reviewed 12 February 2020) | Sales tax on imported goods: 2.5; sales tax on other goods: 0 |

| United Arab Emirates (last reviewed 4 February 2020) | 5 |

SOURCE: Adapted from PWC, 2020.

References

- Oyedokun, G.E. Nigerian value added tax system and the concept of basic food items. SSRN Electron. J. 2016. [Google Scholar] [CrossRef]

- PricewaterhouseCoopers. FIRS Issues Information Circular on the Implementation of VAT Changes. 2020. Available online: https://www.pwc.com/ng/en/assets/pdf/firs-circular-vat-changes.pdf (accessed on 26 August 2020).

- Laws of the Federation. Value Added Tax Act (Amended). Available online: https://jtb.gov.ng/wp-content/uploads/2019/05/Value_Added_Tax_Amendment_Act__2007_.pdf (accessed on 26 August 2020).

- Laws of the Federation. Value Added Tax Act No.102. 1993. Available online: https://www.firs.gov.ng/sites/Authoring/contentLibrary/035860b3-9ecf-400f-8d03-4335e4be5d19Value%20Added%20Tax%20(VAT).pdf (accessed on 26 August 2020).

- Akande, L. Finance Act 2019: 20 Basic Food Items, Sanitary Pad, Others Make List of VAT Exemption List. Available online: https://statehouse.gov.ng/news/finance-act-2019-20-basic-food-items-sanitary-pads-others-make-list-of-vat-exemption-list/ (accessed on 2 June 2020).

- The Federal Government of Nigeria. Finance Act in Federal Republic of Nigeria Official Gazette; The Federal Government of Nigeria: Abuja, Nigeria, 2020.

- Bazgan, R.M. The impact of direct and indirect taxes on economic growth: An empirical analysis related to Romania. In Proceedings of the 12th International Conference on Business Excellence 2018, Bucharest, Romania, 21–25 March 2018; pp. 114–127. [Google Scholar]

- Muresan, M.; David, D.; Elek, L.; Dumiter, F. Value added tax impact on economic activity: Importance, implication and assessment in the Romanian experience. Transylv. Rev. Adm. Sci. 2014, 2014, 131–151. [Google Scholar]

- Simionescu, M.; Albu, L. The impact of standard value added tax on economic growth in CEE-5 countries: Econometric analysis and simulations. Technol. Econ. Dev. Econ. 2016, 22, 850–866. [Google Scholar] [CrossRef]

- Owino, O.B. An empirical analysis of value added tax on economic growth, evidence from Kenya data set. J. Econ. Manag. Trade 2019, 22, 1–14. [Google Scholar] [CrossRef]

- Ikeokwu, Q.C.; Micah, L.C. Indirect taxes and economic growth in Nigeria. Adv. J. Manag. Account. Financ. 2019, 4, 13–31. [Google Scholar]

- Akhor, S.O.; Ekundayo, O.U. The impact of indirect tax revenue on economic growth: The Nigerian experience. Igbinedion Univ. J. Account. 2016, 2, 62–87. [Google Scholar]

- Omodero, C.O. The financial and economic implications of underground economy: The Nigerian perspective. Acad. J. Interdiscip. Stud. 2019, 8, 155–167. [Google Scholar] [CrossRef]

- Omodero, C.O. Tax evasion and its consequences on an emerging economy: Nigeria as a focus. Res. World Econ. 2019, 10, 127–135. [Google Scholar] [CrossRef] [Green Version]

- Omodero, C.O. Taxation income, graft and informal sector operating in Nigeria in In relation to other African Countries. Int. J. Financ. Res. 2020, 11, 163–172. [Google Scholar] [CrossRef]

- Omodero, C.O.; Dandago, K.I. Tax revenue and public service delivery: Evidence from Nigeria. Int. J. Financ. Res. 2019, 10, 82–91. [Google Scholar] [CrossRef]

- Yoon, S.M. The effects of the RCS’s application in the Value Added Tax collecting process on the perception of SME taxpayer in Korea’s trace activity: Transparency and fairness in trade. Sustainability 2018, 10, 4132. [Google Scholar] [CrossRef] [Green Version]

- Oraka, A.O.; Okegbe, T.O.; Ezejiofor, R. Effect of value added tax on the Nigerian economy. Eur. Acad. Res. 2017, 5, 1185–1223. [Google Scholar]

- Oserogho and Associates. VAT and Foreign Non Resident Companies in Nigeria, Legal Alert March; Oserogho and Associates: Lagos, Nigeria, 2008. [Google Scholar]

- Andersen Tax Digest. The New VAT Regime and the Potential Implications. 2020. Available online: www.businessday.ng (accessed on 26 August 2020).

- Umeora, C.E. The effects of Value Added Tax (VAT) on the economic growth of Nigeria. J. Econ. Sustain. Dev. 2013, 4, 190–201. [Google Scholar]

- Federal Inland Revenue Service. Clarification on the Implementation of the Value Added Tax (VAT) Provisions in the Finance Act 2019; Federal Inland Revenue Service: Abuja, Nigeria, 2020.

- Yun, J.J.; Liu, Z. Micro and Macro-Dynamics of open innovation with a Quadruple-Helix model. Sustainability 2019, 11, 3301. [Google Scholar] [CrossRef] [Green Version]

- Federal Inland Revenue Service. COVID-19: Message to Taxpayers from Executive Chairman, of the Federal Inland Revenue Service, Muhammad Nami to Taxpayers. Available online: https://assets.kpmg/content/dam/kpmg/ng/pdf/tax/FIRS-chairman-message-to-taxpayers.pdf (accessed on 15 August 2020).

- Stailova, D.; Patonov, N. An empirical evidence for the impact of taxation on economy growth in the European Union. Tour. Manag. Stud. 2012, 3, 1030–1039. [Google Scholar]

- Asogwa, F.O.; Nkolika, O.M. Value added tax and investment growth in Nigeria: Time series analysis. IOSR J. Humanit. Soc. Sci. 2013, 18, 28–31. [Google Scholar]

- Onwuchekwa, J.C.; Aruwa, S.A.S. Value added tax and economic growth in Nigeria. Eur. J. Account. Audit. Financ. Res. 2014, 2, 62–69. [Google Scholar]

- Kolahi, S.H.G.; Noor, Z.B.M. The effect of value added tax on economic growth and Its sources in developing countries. Int. J. Econ. Financ. 2016, 8, 217–228. [Google Scholar] [CrossRef]

- Inyiama, O.I.; Ubesie, M.C. Effect of value added tax, customs and excise duties on nigeria economic growth. Int. J. Manag. Stud. Res. 2016, 4, 53–62. [Google Scholar] [CrossRef]

- Olatunji, O.C.; Ayeni, O.F. Effects of value added tax and custom duties on revenue generation in Nigeria (2000–2016). Eur. J. Account. Audit. Financ. Res. 2018, 6, 78–85. [Google Scholar]

- Abomaye, N.; Williams, A.S.; Michael, J.E.M.; Friday, H.C. An empirical analysis of tax revenue and economic growth in Nigeria from 1980 to 2015. Glob. J. Hum. Soc. Sci. F Political Sci. 2018, 18, 8–40. [Google Scholar]

- Omodero, C.O.; Egbide, B.; Madugba, J.U.; Ehikioya, B.I. A mismatch between external debt finances and consumption cost in Nigeria. J. Open Innov. Technol. Mark. Complex. 2020, 6, 58. [Google Scholar] [CrossRef]

- Gujarati, D.N.; Porter, D.C. Basic Econometrics, 5th ed.; McGraw-Hill Irwin: Boston, MA, USA, 2009; ISBN 9780073375779. [Google Scholar]

- Chesbrough, H.W. Open Innovation: The New Imperative for Creating and Profiting from Technology; Harvard Business Press: Boston, MA, USA, 2003. [Google Scholar]

Figure 1.

Histogram normality.

Figure 2.

Trend of data from 2005 to 2019. Source of data: Central Bank of Nigeria (CBN) Statistical Bulletin and Work Bank Economic Indicators.

Figure 2.

Trend of data from 2005 to 2019. Source of data: Central Bank of Nigeria (CBN) Statistical Bulletin and Work Bank Economic Indicators.

Table 1.

Penalties for failure to file VAT returns.

| VATA | Description of Default | Penalty for the First Month of Failure to File for VAT Returns | Penalty for the Each Subsequent Month of Failure to Remit VAT |

|---|---|---|---|

| S.8 | Failure to register for VAT | NGN50,000.000 | NGN25,000.00 |

| S.28 | Failure to notify change of address or permanent cessation of trade or business | NGN50,000.000 | NGN25,000.00 |

| S.35 | Failure to submit VAT returns | NGN50,000.000 | NGN25,000.00 |

Source: Adapted from Federal Inland Revenue Service, 2020.

Table 2.

Breusch–Godfrey serial correlation test.

| F-statistic | 0.162633 | Prob. F(2,10) | 0.8521 ** |

| Observed R-squared | 0.472528 | Prob. Chi-Square(2) | 0.7896 |

Notes: ** Absence of serial correlation as p-value > 5%. Source: Author’s computation, 2020.

Table 3.

Heteroskedasticity test: Breusch–Pagan–Godfrey.

| F-statistic | 0.219866 | Prob. F(2,12) | 0.8058 ** |

| Observed R-squared | 0.530235 | Prob. Chi-Square(2) | 0.7671 |

| Scaled explained SS | 0.300887 | Prob. Chi-Square(2) | 0.8603 |

Notes: ** Absence of heteroskedasticity as p-value > 5%. Source: Author’s computation, 2020.

Table 4.

Multicollinearity test: variance inflation factors.

| Variable | Coefficient | Uncentered | Centered |

|---|---|---|---|

| Variance | VIF | VIF | |

| LOG_CED | 0.037117 | 1612.226 | 8.633768 ** |

| LOG_VAT | 0.023347 | 1142.373 | 8.633768 ** |

| C | 0.031886 | 202.6024 | NA |

Notes: ** Absence of multicollinearity as Variance Inflatory Factor (VIF) < 10. Source: Author’s computation, 2020.

Table 5.

Pairwise Granger Causality Tests.

| Sample: 2005–2019 | |||

|---|---|---|---|

| Lags: 2 | |||

| Null Hypothesis: | Obs | F-Statistic | Prob. ** |

| LOG_VAT does not Granger cause LOG_CPI | 13 | 0.42106 | 0.6701 |

| LOG_CPI does not Granger cause LOG_VAT | 3.27419 | 0.0914 | |

| LOG_CED does not Granger cause LOG_CPI | 13 | 1.40751 | 0.2994 |

| LOG_CPI does not Granger cause LOG_CED | 5.65742 | 0.0294 | |

| LOG_CED does not Granger cause LOG_VAT | 13 | 0.56807 | 0.5879 |

| LOG_VAT does not Granger cause LOG_CED | 0.82811 | 0.4711 | |

Notes: ** Significant at 5%. Source: Author’s computation, 2020.

Table 6.

Unrestricted Cointegration Rank Test (Trace).

| Sample (Adjusted): 2007–2019 | ||||

|---|---|---|---|---|

| Hypothesized | Eigenvalue | Trace | 0.05 | Prob. ** |

| No. of Co-integration in Existence | Statistic | Critical Value | ||

| None | 0.892148 | 44.91968 | 29.79707 | 0.0005 |

| At most 1 | 0.687409 | 15.96880 | 15.49471 | 0.0424 |

| At most 2 | 0.063410 | 0.851620 | 3.841466 | 0.3561 |

Notes: ** Substantial at 5% level of significance. Source: Author’s computation, 2020.

Table 7.

Regression result.

| Dependent Variable: LOG_CPI | ||||

|---|---|---|---|---|

| Method: Least Squares | ||||

| Sample: 2005 2019 Included Observations: 15 | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| LOG_VAT | 0.196778 | 0.152799 | 1.287825 | 0.2221 |

| LOG_CED | 0.761247 | 0.192658 | 3.951279 | 0.0019 ** |

| C | −0.440881 | 0.178566 | −2.469002 | 0.0295 ** |

| R-squared | 0.950766 | Mean dependent var | 2.088117 | |

| Adjusted R-squared | 0.942561 | S.D. dependent var | 0.202731 | |

| S.E. of regression | 0.048587 | Akaike info criterion | −3.034051 | |

| Sum squared resid. | 0.028329 | Schwarz criterion | −2.892441 | |

| Log likelihood | 25.75538 | Hannan–Quinn criter. | −3.035560 | |

| F-statistic | 115.8682 | Durbin–Watson stat | 1.673473 | |

| Prob (F-statistic) | 0.000000 | |||

Notes: ** Significant at 5%. Source: Author’s computation, 2020.

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Omodero, C.O. The Consequences of Indirect Taxation on Consumption in Nigeria. J. Open Innov. Technol. Mark. Complex. 2020, 6, 105. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc6040105

AMA Style

Omodero CO. The Consequences of Indirect Taxation on Consumption in Nigeria. Journal of Open Innovation: Technology, Market, and Complexity. 2020; 6(4):105. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc6040105

Chicago/Turabian StyleOmodero, Cordelia Onyinyechi. 2020. "The Consequences of Indirect Taxation on Consumption in Nigeria" Journal of Open Innovation: Technology, Market, and Complexity 6, no. 4: 105. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc6040105