Strategy and Human Resources Management in Non-Profit Organizations: Its Interaction with Open Innovation

Abstract

:1. Introduction

2. Literature Review

2.1. Governance and Strategic Management

2.2. Strategy and Human Resources Management

2.3. Human Resource Management and Governance

3. Methodology

3.1. Validity and Reliability of the Measurement Model

3.2. Confirmatory Factorial Analysis

4. Results

Analysis and Discussion of Results

5. Discussion: Open Innovation in Non-Profit Organizations

6. Conclusions, Limitations and Future Research

6.1. Conclusions

6.2. Limitations and Future Research

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Dimensions | Sub Dimensions | Questions | Authors Reference |

|---|---|---|---|

| Strategy (STR) | Strategy formulation | The entity periodically conducts an internal and external analysis to define objectives to formulate appropriate strategies. | Rodrigues and Malo [44] |

| Strategic choices | The entity periodically reviews its strategic choices, considering the goals and indicators of achievement of objectives. | Bukhari et al. [45] | |

| Implementation of strategies | The entity implements its strategic choices, rectifies deviations and establishes action plans, taking into account strategic partnerships, identifying and allocating resources, priorities, and activities to be developed. | Taylor [46] | |

| Identification of externalities | The entity can identify the externalities it generates for the community, considering the improvement of processes, development of the mission, and social value creation. | Cabral De Ávila and Bertero [47] | |

| Measuring externalities | The entity can quantify and measure the externalities it generates for the community. | Garcia [26] | |

| Disclosure of externalities | The entity can publicize the externalities it generates for the community and captures the perceived value. | Kicová [51] | |

| Human Resources Management (HRM) | Motivation | The entity’s human resources have good levels of motivation. | Devanna et al. [56] |

| Performance | Human resources are subject to a performance assessment, formal or informal, aimed at the entity’s proper functioning. | Boselie and Paauwe [22] | |

| Practices | The entity promotes practices aimed at promoting, developing, and encouraging human resources. | Boselie and Paauwe [22] | |

| Training support instruments | The entity identifies and provides resources that aim to provide human resources with better access to training. | Bloom and Chatterji [58] | |

| Volunteering | The entity promotes, disseminates and evaluates voluntary work. | Bloom and Smith [59] | |

| Governance (GOV) | Knowledge of the user’s family reality | The entity has strategies that promote the relationship with users’ family members to increase their family reality knowledge. | Saltaji [40] |

| Ethics and social responsibility | The entity has a system for promoting and monitoring ethical practices and social responsibility of its employees. | Tsai and Yamamoto [48] | |

| Action with the community | The entity promotes practices of action with the community, with positive impacts, whether at social, environmental, economic or financial levels, contributing to its sustainable development. | Leal and Famá [50] | |

| Performance impacts | The entity promotes external audits that include the impacts of its activities on a social, environmental, economic, financial level and the community’s sustainable development. | Machado Filho et al. [49] | |

| Quality system | The entity promotes a culture of quality, continuous improvement and adaptation of organizational processes. | Woerrlein and Scheck [15] | |

| Relationship networks | The entity promotes initiatives aimed at strengthening relations between people inside and outside the organization to capture and develop new ideas, good practices, and legislation compliance. | Saltaji [40] | |

| Communication plan | The entity has a communication plan, defined and diversified channels, to transmit its projects and their value to the community. | Garcia [26] | |

| Marketing | The entity has and streamlines marketing tools and strategies to cover the different target audiences in sufficient diversity. | Garcia [26] | |

| Community involvement | The organization organizes events open to the community and participates in third party events. | Saltaji [40] |

References

- Shi, Y.; Jang, H.S.; Keyes, L.; Dicke, L. Nonprofit Service Continuity and Responses in the Pandemic: Disruptions, Ambiguity, Innovation, and Challenges. Public Adm. Rev. 2020, 80, 874–879. [Google Scholar] [CrossRef] [PubMed]

- Macías Ruano, A.J.; Pires Manso, J.R.; de Pablo Valenciano, J.; Marruecos Rumí, M.E. The Misericórdias as Social Economy Entities in Portugal and Spain. Religions 2020, 11, 200. [Google Scholar] [CrossRef] [Green Version]

- Weerawardena, J.; McDonald, R.E.; & Mort, G.S. Sustainability of nonprofit organizations: An empirical investigation. J. World Bus. 2010, 45, 346–356. [Google Scholar] [CrossRef]

- Knutsen, W.L. Value as a self-sustaining mechanism: Why some nonprofit organizations are different from and similar to private and public organizations. Nonprofit Volunt. Sect. Q. 2013, 42, 985–1005. [Google Scholar] [CrossRef]

- Coelho, D.; Miranda, J.; Portela, F.; Machado, J.; Santos, M.F.; Abelha, A. Towards of a business intelligence platform to Portuguese Misericórdias. Procedia Comput. Sci. 2016, 100, 762–767. [Google Scholar] [CrossRef] [Green Version]

- Petitgand, C. Business tools in nonprofit organizations: A performative story. Int. J. Entrep. Behav. Res. 2018, 24, 667–682. [Google Scholar] [CrossRef]

- Suykens, B.; De Rynck, F.; Verschuere, B. Examining the influence of organizational characteristics on nonprofit commercialization. Nonprofit Manag. Leadersh. 2019, 30, 339–351. [Google Scholar] [CrossRef]

- Greiling, D. Performance Measurement in Nonprofit-Organisationen; Springer: Berlin, Germany, 2009. [Google Scholar]

- Meyer, M.; Simsa, R. Entwicklungsperspektiven des Nonprofit-Sektors. In Handbuch der Nonprofit-Organisation, 3rd ed.; Simsa, R., Meyer, M., Badelt, C., Eds.; Schäffer-Poeschel: Stuttgart, Germany, 2013. [Google Scholar]

- Zimmer, A.; Priller, E.; Anheier, H.K. Der Nonprofit-Sektor in Deutschland. Handb. Der Nonprofit-Organ. 2013, 5, 15–36. [Google Scholar]

- Dawson, A. A case study of impact measurement in a third sector umbrella organisation. Int. J. Product. Perform. Manag. 2010, 59, 519–533. [Google Scholar] [CrossRef]

- Grimes, M. Strategic sensemaking within funding relationships: The effects of performance measurement on organizational identity in the social sector. Entrep. Theory Pract. 2010, 34, 763–783. [Google Scholar] [CrossRef]

- Gill, S.J. Developing a Learning Culture in Nonprofit Organizations; Sage: Southend Oaks, CA, USA, 2010. [Google Scholar]

- Albrecht, K.; GAG, P.; Beck, S.; Hoelscher, P.; Plazek, M.; von der Ahe, B. Wirkungsorientierte Steuerung. In Non-Profit-Organisationen; Institut für den öffentlichen Sektor & KPMG, Ed.; PHINEO gAG: Berlin, Germany, 2013. [Google Scholar]

- Woerrlein, L.M.; Scheck, B. Performance management in the third sector: A literature-based analysis of terms and definitions. Public Adm. Q. 2016, 40, 220–255. [Google Scholar]

- Acosta-Prado, J.C.; López-Montoya, O.H.; Sanchís-Pedregosa, C.; Zárate-Torres, R.A. Human Resource Management and Innovative Performance in Non-profit Hospitals: The Mediating Effect of Organizational Culture. Front. Psychol. 2020, 11, 1422. [Google Scholar] [CrossRef]

- Wernerfelt, B. A resource-based view of the firm. Strateg. Manag. J. 1984, 5, 171–180. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Conner, K.R. A historical comparison of resource-based theory and five schools of thought within industrial organization economics: Do we have a new theory of the firm? J. Manag. 1991, 17, 121–154. [Google Scholar] [CrossRef]

- Grant, R. The Resource Based Theory of Competitive Advantage: Implications for Strategy Formulation. Calif. Manag. Rev. 1991, 33, 114–135. [Google Scholar] [CrossRef] [Green Version]

- Collis, D.J.; Montgomery, C.A. Competing on Resources: Strategy in the 1990s. Knowl. Strategy 1995, 73, 25–40. [Google Scholar]

- Boselie, P.; Paauwe, J. Human resource function competencies in European companies. Pers. Rev. 2005, 34, 550–566. [Google Scholar] [CrossRef] [Green Version]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Nickson, D.; Warhurst, C.; Dutton, E.; Hurrell, S. A job to believe in: Recruitment in the Scottish voluntary sector. Hum. Resour. Manag. J. 2008, 18, 20–35. [Google Scholar] [CrossRef]

- Baines, D. ‘If We Don’t Get Back to Where We Were Before’: Working in the restructured non-profit social services. Br. J. Soc. Work 2010, 40, 928–945. [Google Scholar] [CrossRef]

- Atkinson, C.; Lucas, R. Worker responses to HR practice in adult social care in England. Hum. Resour. Manag. J. 2013, 23, 296–312. [Google Scholar] [CrossRef]

- Ariza-Montes, A.; Lucia-Casademunt, A.M. Nonprofit versus for-profit organizations: A european overview of employees’ work conditions. Hum. Serv. Organ. Manag. Leadersh. Gov. 2016, 40, 334–351. [Google Scholar] [CrossRef]

- Colbert, B.A. The complex resource-based view: Implications for theory and practice in strategic human resource management. Acad. Manag. Rev. 2004, 29, 341–358. [Google Scholar] [CrossRef]

- Akingbola, K. Resource-based view (RBV) of unincorporated social economy organizations. Can. J. Nonprofit Soc. Econ. Res. 2013, 4, 66–85. [Google Scholar] [CrossRef] [Green Version]

- de Oliveira, S.B.; Toda, F.A. O planejamento estratégico e a visão baseada em recursos (RBV): Uma avaliação da tecnologia da informação na gestão hospitalar. Rev. Eletrônica Ciência Adm. 2013, 12, 39–57. [Google Scholar] [CrossRef] [Green Version]

- Brown, W.A.; Andersson, F.O.; Jo, S. Dimensions of capacity in nonprofit human service organizations. Volunt. Int. J. Volunt. Nonprofit Organ. 2016, 27, 2889–2912. [Google Scholar] [CrossRef]

- Gile, P.P.; Buljac-Samardzic, M.; Van De Klundert, J. The effect of human resource management on performance in hospitals in Sub-Saharan Africa: A systematic literature review. Hum. Resour. Health 2018, 16, 34. [Google Scholar] [CrossRef] [Green Version]

- Nielsen, C.; Lund, M.; Montemari, M.; Palolone, F.; Massaro, M.; Dumay, J. Business Models: A Research Overview; Routledge: London, UK, 2019. [Google Scholar]

- Sanderse, J.; de Langen, F.; Salgado, F.P. Proposing a business model framework for nonprofit organizations. J. Appl. Econ. Bus. Res. 2020, 10, 40–53. [Google Scholar]

- Hwang, H.; Powell, W.W. The rationalization of charity: The influences of professionalism in the nonprofit sector. Adm. Sci. Q. 2009, 54, 268–298. [Google Scholar] [CrossRef] [Green Version]

- Hvenmark, J. Business as usual? On managerialization and the adoption of the balanced scorecard in a democratically governed civil society organization. Adm. Theory Prax. 2013, 35, 223–247. [Google Scholar]

- Laurett, R.; Ferreira, J.J. Strategy in nonprofit organizations: A systematic literature review and agenda for future research. Voluntas Int. J. Volunt. Nonprofit Organ. 2018, 29, 881–897. [Google Scholar] [CrossRef]

- Hudson, M. Managing without Profit: Leadership Management and Governance of Third Sector Organizations; Directory of Social Change: London, UK, 2009. [Google Scholar]

- Garcia, C.M.S. Governança: Uma estratégia para o terceiro setor face ao contexto de austeridade. Rev. Psicol. Criança Adolesc. 2016, 7, 1–2. [Google Scholar]

- Saltaji, I.M.F. Corporate Governance Relationship with Strategic Management. Intern. Audit. Risk Manag. 2013, 30, 301–308. [Google Scholar]

- Pimenta, S.M.; Brasil, E.R. Gestores e Competências Organizacionais no Terceiro Setor em Itabira. Gestão Reg. 2006, 22, 78–89. [Google Scholar]

- Cruz, J.A.W.; Quandt, C.O.; Martins, T.S.; da Silva, W.V. Performance no terceiro setor uma abordagem de Accountability: Estudo de caso em uma Organização Não Governamental Brasileira. Rev. Adm. Ufsm 2010, 3, 58–75. [Google Scholar] [CrossRef]

- da Silveira, D.; Borba, J.A. Evidenciação Contábil de Fundações Privadas de Educação e Pesquisa: Uma Análise da Conformidade das Demonstrações Contábeis de Entidades de Santa Catarina. Rev. Contab. Vista Rev. 2010, 21, 41–68. [Google Scholar]

- Rodrigues, A.L.; Malo, M.C. Estruturas de governança e empreendedorismo coletivo: O caso dos doutores da alegria. Rev. Adm. Contemp. 2006, 10, 29–50. [Google Scholar] [CrossRef] [Green Version]

- Bukhari, I.S.; Jabeen, N.; Jadoon, Z.I. Governance of third sector organizations in Pakistan: The role of advisory board. South Asian Stud. 2014, 29, 579–592. [Google Scholar]

- Taylor, K. Learning from the Co-operative Institutional Model: How to Enhance Organizational Robustness of Third Sector Organizations with More Pluralistic Forms of Governance. Adm. Sci. 2015, 5, 148–164. [Google Scholar] [CrossRef] [Green Version]

- Cabral De Ávila, L.; Bertero, C. Third sector governance: A case study in a university support foundation. Rev. Bus. Manag. 2016, 18, 125–144. [Google Scholar] [CrossRef] [Green Version]

- Tsai, P.Y.; Yamamoto, M.M. Governança corporativa: Análise comparativa entre o setor privado e o terceiro setor. In Proceedings of the Congresso USP Controladoria e Contabilidade, São Paulo, Brasil, 10–11 October 2005. [Google Scholar]

- Machado Filho, C.A.P.; Mizumoto, F.M.; Zylbersztajn, D. Governance and strategy of Private Interest Associations: A case study of the Brazilian Pasta Association. Rege Rev. Gestão 2006, 13, 1–10. [Google Scholar]

- Leal, E.A.; Famá, R. Governança nas organizações do terceiro setor: Um estudo de caso. In Proceedings of the SEMEAD—Seminários em Administração, São Paulo, Brasil, 9–10 September 2007. [Google Scholar]

- Kicová, E. Specifics of human resources in non-profit organizations in the process of globalization. SHS Web Conf. 2020, 74, 1011. [Google Scholar] [CrossRef]

- Miller, E.W. Nonprofit strategic management revisited. Can. J. Nonprofit Soc. Econ. Res. 2018, 9. [Google Scholar] [CrossRef]

- OECD. G20/OECD Principles of Corporate Governance. 2015. Available online: http://www.oecd.org/corporate/principles-corporate-governance/ (accessed on 10 January 2021).

- Ulrich, D. Recursos Humanos Champions; Ediciones Granica SA: Lavalle, Argentina, 1997. [Google Scholar]

- Porter, M. Clusters and the New Economics of Competition. Harv. Bus. Rev. 1998, 76, 75–90. [Google Scholar]

- Devanna, M.A.; Fombrun, C.; Tichy, N.; Warren, L. Strategic planning and human resource management. Hum. Resour. Manag. 1982, 21, 11–17. [Google Scholar] [CrossRef]

- Meyer, K.E.; Xin, K.R. Managing talent in emerging economy multinationals: Integrating strategic management and human resource management. Int. J. Hum. Resour. Manag. 2018, 29, 1827–1855. [Google Scholar] [CrossRef]

- Bloom, P.N.; Chatterji, A.K. Scaling social entrepreneurial impact. Calif. Manag. Rev. 2009, 51, 114–133. [Google Scholar] [CrossRef]

- Bloom, P.N.; Smith, B.R. Identifying the drivers of social entrepreneurial impact: Theoretical development and an exploratory empirical test of SCALERS. J. Soc. Entrep. 2010, 1, 126–145. [Google Scholar] [CrossRef]

- Winter, S. Knowledge and competence as strategic assets. In The Competitive Challenge: Strategies for Industrial Innovation and Renewal; Teece, D.J., Ed.; Ballinger: Cambridge, MA, USA, 1987; pp. 159–184. [Google Scholar]

- Amit, R.; Shoemaker, P.J.H. Strategic assets and organizational rent. Strateg. Manag. J. 1993, 14, 33–46. [Google Scholar] [CrossRef]

- Mueller, F. Strategic Human Resource Management and the Resource-Based View of the Firm: Toward a Conceptual Integration; Working Paper; Aston University Business School: Birmingham, UK, 1994. [Google Scholar]

- Peteraf, M.A. The cornerstones of competitive advantage: A resource-based view. Strateg. Manag. J. 1993, 14, 179–191. [Google Scholar] [CrossRef]

- Wright, P.M.; Mcmahan, G.C.; McWilliams, A. Human resources and sustained competitive advantage: A resource-based perspective. Int. J. Hum. Resour. Manag. 1994, 5, 301–326. [Google Scholar] [CrossRef]

- Mueller, F. Human Resources as Strategic Assets: An Evolutionary Resource-Based Theory. J. Manag. Stud. 1996, 33, 757–785. [Google Scholar] [CrossRef]

- Prahalad, C.K.; Hamel, G. A competência essencial da corporação. In Estratégia: A Busca da Vantagem Competitiva; Montegomery, C.A., Porter, M.E., Eds.; Elsevier: Rio de Janeiro, Brazil, 1998. [Google Scholar]

- Medeiros, N.; Meirelles, A.; Jeunon, E. A Gestão Estratégica nos departamentos de tratamento técnico a partir da visão de Porter e de Prahalad e Hamel: Fator de competitividade e sobrevivência das unidades de informação. Inf. Soc. 2008, 18, 171–182. [Google Scholar]

- Oyewunmi, O.A.; Osibanjo, A.O.; Falola, H.O.; Olujobi, J.O. Optimization by Integration: A corporate governance and human resource management dimension. Int. Rev. Manag. Mark. 2017, 7, 265–272. [Google Scholar]

- Zollo, L.; Laudano, M.C.; Boccardi, A.; Ciappei, C. From governance to organizational effectiveness: The role of organizational identity and volunteers’ commitment. J. Manag. Gov. 2019, 23, 111–137. [Google Scholar] [CrossRef]

- Akinlade, D.; Shalack, R. Strategic human resource management in nonprofit organizations: A case for mission-driven human resource practices. Glob. J. Manag. Mark. 2017, 1, 121–146. [Google Scholar]

- Hair, J.F., Jr.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial least squares structural equation modeling (PLS-SEM) An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis: Pearson New International Edition; Pearson: New York, NY, USA, 2013. [Google Scholar]

- Hoelter, J.W. The analysis of covariance structures: Goodness-of-fit indices. Sociol. Methods Res. 1983, 11, 325–344. [Google Scholar] [CrossRef]

- Bagozzi, R.P.; Yi, Y. Specification, evaluation, and interpretation of structural equation models. J. Acad. Mark. Sci. 2012, 40, 8–34. [Google Scholar] [CrossRef]

- Brown, T.A. Confirmatory Factor Analysis for Applied Research; Guilford Publications: New York, NY, USA, 2015. [Google Scholar]

- Ringle, C.M.; Wende, S.; Becker, J.M. SmartPLS 3; SmartPLS GmbH: Boenningstedt, Germany, 2015. [Google Scholar]

- Taber, K.S. The use of Cronbach’s alpha when developing and reporting research instruments in science education. Res. Sci. Educ. 2018, 48, 1273–1296. [Google Scholar] [CrossRef]

- Marôco, J. Structural Equation Analysis: Theoretical Fundamentals, Software & Applications; ReportNumber. Análise e Gestão de Informação, Lda.: Pêro Pinheiro, Portugal, 2010. [Google Scholar]

- Chesbrough, H.W. The era of open innovation. MIT Sloan Manag. Rev. 2003, 44, 35–41. [Google Scholar]

- Rajagukguk, S. Accounting Control Systems, Open Innovation and Sustainable Competitive Advantage. KnE Soc. Sci. 2018, 3, 74–85. [Google Scholar]

- Holmes, S.; Smart, P. Exploring open innovation practice in firm-nonprofit engagements: A corporate social responsibility perspective. R&d Manag. 2009, 39, 394–409. [Google Scholar]

- Trentini, A.; Furtado, I.; Dergint, D.; Reis, D.; Carvalho, H. Inovação Aberta e Inovação Distribuída, Modelos Diferentes de Inovação? Rev. Eletr. Eletrônica Negócios 2012, 5, 88–109. [Google Scholar] [CrossRef] [Green Version]

- Brondizio, E.S.; Ostrom, E.; and Young, O.R. Connectivity and the governance of multilevel social-ecological systems: The role of social capital. Annu. Rev. Environ. Resour. 2009, 34, 253–781. [Google Scholar] [CrossRef]

- Phills, J.A., Jr.; Deiglmeier, K.; Miller, D.T. Rediscovering social innovation. Stanf. Soc. Innov. Rev. 2008, 6, 34–44. [Google Scholar]

- MacCallum, D.; Moulaert, F.; Hillier, J.; Vicari, S. (Eds.) Social Innovation and Territorial Development; Ashgate: Farnham, UK, 2009. [Google Scholar]

- Evans, B.; Joas, M.; Sundback, S.; Theobald, K. Institutional and social capacity enhancement for local sustainable development: Lessons from european urban settings. In Pursuit of Sustainable Development: New Governance Practices at the Sub-National Level in Europe; Baker, S., Eckerberg, K., Eds.; Routledge: Abingdon, IL, USA; ECPR Studies in European Political Science: New York, NY, USA, 2008; pp. 74–95. [Google Scholar]

| Constructs | Items | Loadings | Composite Reliability | Average Variance Extracted | Cronbach’s Alpha |

|---|---|---|---|---|---|

| Strategy | STR1 STR2 STR3 STR4 STR5 STR6 | 0.854 0.879 0.881 0.780 0.760 0.753 | 0.847 | 0.671 | 0.924 |

| Human Resources Management | HRM1 HRM2 HRM4 HRM5 HRM6 | 0.677 0.676 0.963 0.937 0.868 | 0.848 | 0.504 | 0.912 |

| Governance | GOV5 GOV6 GOV7 GOV8 GOV9 GOV10 GOV11 GOV13 GOV14 GOV15 GOV17 | 0.733 0.675 0.626 0.752 0.748 0.737 0.722 0.756 0.762 0.782 0.550 | 0.848 | 0.520 | 0.935 |

| Hypothesis | Relation | Regression Coefficient | Standard Error | t | p-Value | Result |

|---|---|---|---|---|---|---|

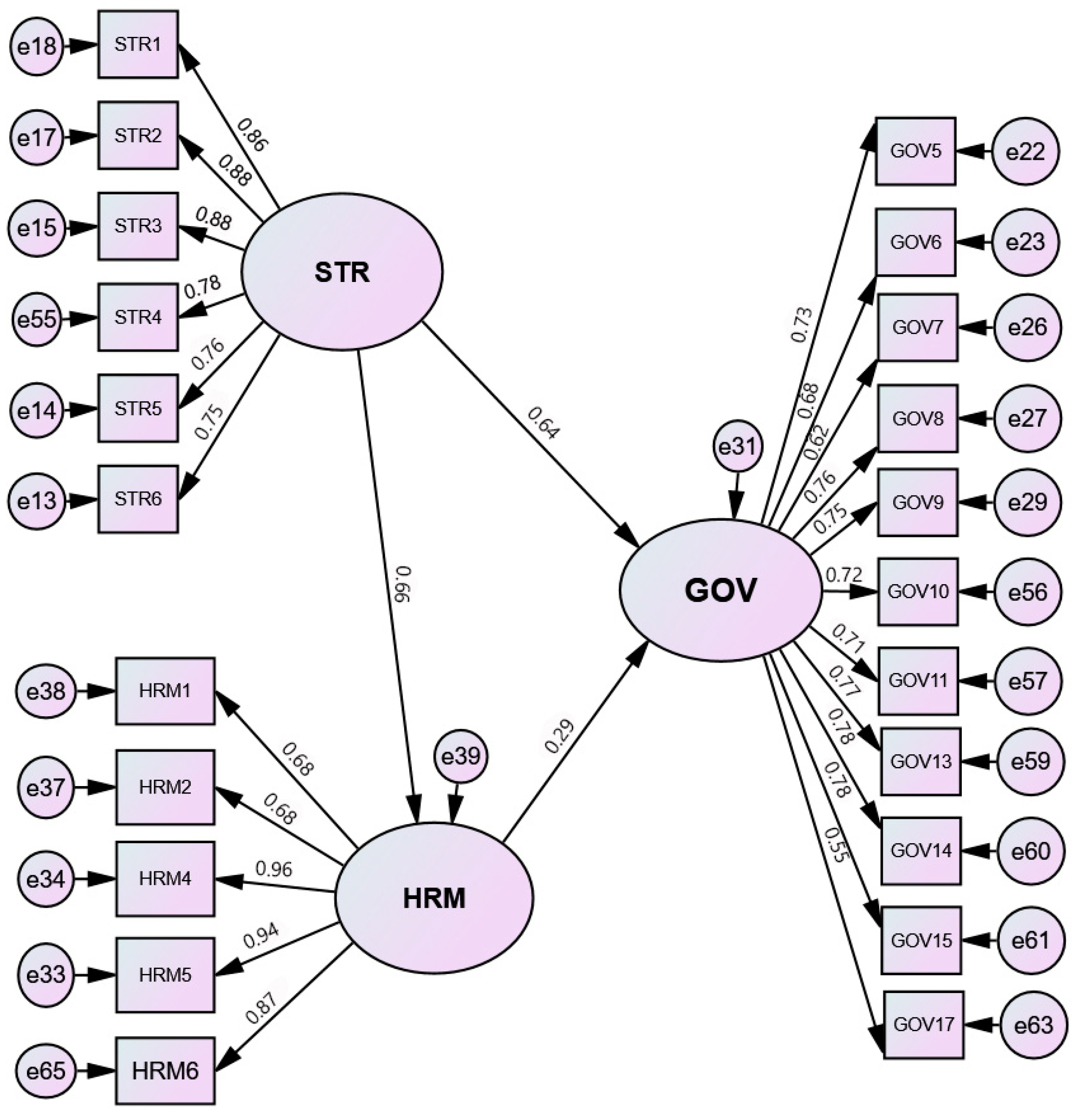

| H1 | STR→GOV | 0.640 | 0.059 | 7.503 | <0.001 | Supported |

| H2a | STR→HRM | 0.660 | 0.061 | 7.404 | <0.001 | Supported |

| H2b | STR→HRM→GOV | 0.422 | 0.004 | 4.318 | <0.001 | Supported |

| H3 | HRM→GOV | 0.290 | 0.070 | 4.171 | <0.001 | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oliveira, M.; Sousa, M.; Silva, R.; Santos, T. Strategy and Human Resources Management in Non-Profit Organizations: Its Interaction with Open Innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 75. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7010075

Oliveira M, Sousa M, Silva R, Santos T. Strategy and Human Resources Management in Non-Profit Organizations: Its Interaction with Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity. 2021; 7(1):75. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7010075

Chicago/Turabian StyleOliveira, Márcio, Marlene Sousa, Rui Silva, and Tânia Santos. 2021. "Strategy and Human Resources Management in Non-Profit Organizations: Its Interaction with Open Innovation" Journal of Open Innovation: Technology, Market, and Complexity 7, no. 1: 75. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc7010075